need analysis and professional judgments justin chase brown cortneyjo sandidge university of...

TRANSCRIPT

NEED ANALYSISANDPROFESSIONALJUDGMENTS

JUSTIN CHASE BROWN

CORTNEYJO SANDIDGEUNIVERSITY OF MISSOURI

TRAINING OBJECTIVES

i. Principles of Need Analysis

ii. Need Analysis Variations

iii. Professional Judgment

iv. Dependent Case Study

v. Case Study On Your Own

http://ifap.ed.gov/efcformulaguide/attachments/091913EFCFormulaGuide1415.pdf

PRINCIPLES OF NEED ANALYSIS

the assessment of the difference between a family’s ability to pay for college (EFC) and the college’s cost of attendance (COA)

Guiding premise: Students and their families are primarily responsible for the funding of

a student’s educational expenses, to the extent possible.

PRINCIPLES OF NEED ANALYSIS

First step Calculating the Expected Family Contribution (EFC)

Operational principles Federal methodology is intended to measure the ability of the student

and his/her family to contribute to the total cost of a college education.

Only after the family’s ability to contribute has been measured will need-based financial aid be used to pay for postsecondary education.

PRINCIPLES OF NEED ANALYSIS

Student/family files FAFSA

Federal processor performs calculations Student information = Student Contribution

Including spouse, if independent and married

Parental information = Parent Contribution

For dependent students

Household size and number in college

Student Contributio

n

Parent Contributi

on

EFC

NEED ANALYSIS COMPONENTS

Basic components: Income

Allowances

Assets

Number in household

Number in college

NEED ANALYSIS FORMULA IN A NUTSHELL

Income

Allowances

Available income

AssetsCost of

living

Contribution # in

college

EFC

ALLOWANCES

U.S. income tax paid allowance

State and other tax allowance

Social Security tax allowance

Income Protection Allowance

Parent’s negative Adjusted Available Income (dependent students only)

INCOME PROTECTION ALLOWANCE

Allowance for basic living expenses of a family, which varies according to the number in the household and college

In general, it can be assumed that: 30% of IPA is for food 22% of IPA is for housing 9% of IPA is for transportation expenses 16% of IPA is for clothing/personal care 11% of IPA is for medical care 12% of IPA is for other family consumption

SAVING FOR COLLEGE

Many families feel they are penalized if they save money for college. Two largest assets for most families are not included in need analysis

(home equity and retirement savings)

There is also an asset protection allowance that varies according to eldest parent’s age

Assessment rate on assets is relatively low

NEED ANALYSIS VARIATIONS

FORMULA A Dependent students

FORMULA B

Independent student without dependents other

than spouse

FORMULA C

Independent students with dependents other

than spouse

NEED ANALYSIS VARIATIONS

Regular (full) Formula

Simple Needs FormulaLower-income families (assets not considered)

Automatic Zero FormulaVery low-income families (Zero EFC)

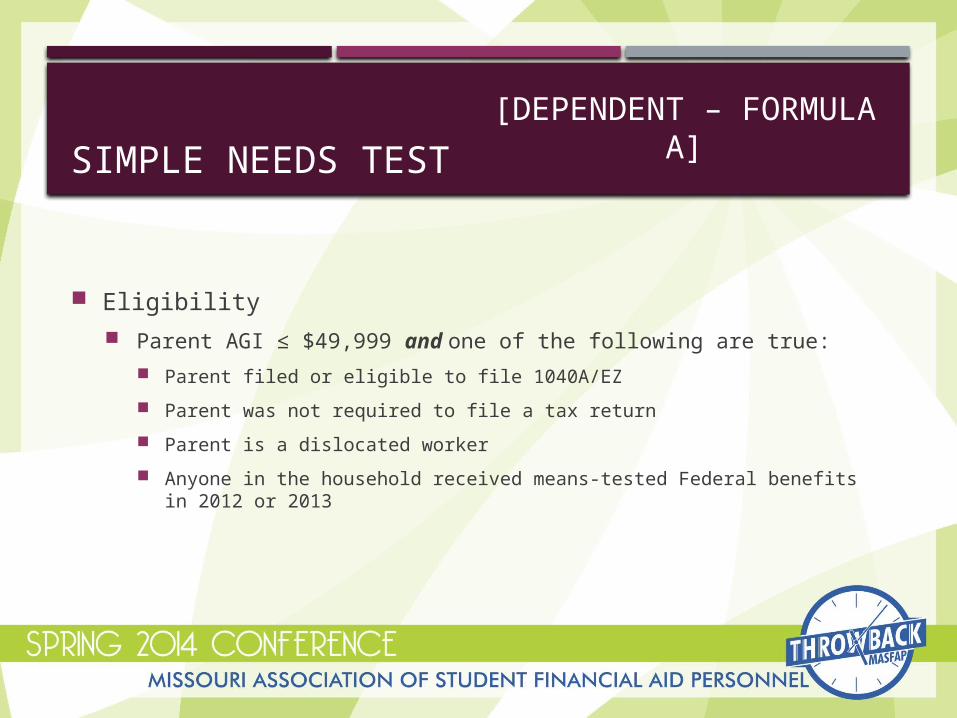

SIMPLE NEEDS TEST

Eligibility Parent AGI ≤ $49,999 and one of the following are true:

Parent filed or eligible to file 1040A/EZ

Parent was not required to file a tax return

Parent is a dislocated worker

Anyone in the household received means-tested Federal benefits in 2012 or 2013

[DEPENDENT – FORMULA A]

SIMPLE NEEDS TEST

Eligibility Student/spouse AGI ≤ $49,999 and one of the following are true:

Student/spouse filed or eligible to file 1040A/EZ

Student/spouse was not required to file a tax return

Student/spouse is a dislocated worker

Anyone in the student/spouse household received means-tested Federal benefits in 2012 or 2013

[INDEPENDENT – FORMULA C]

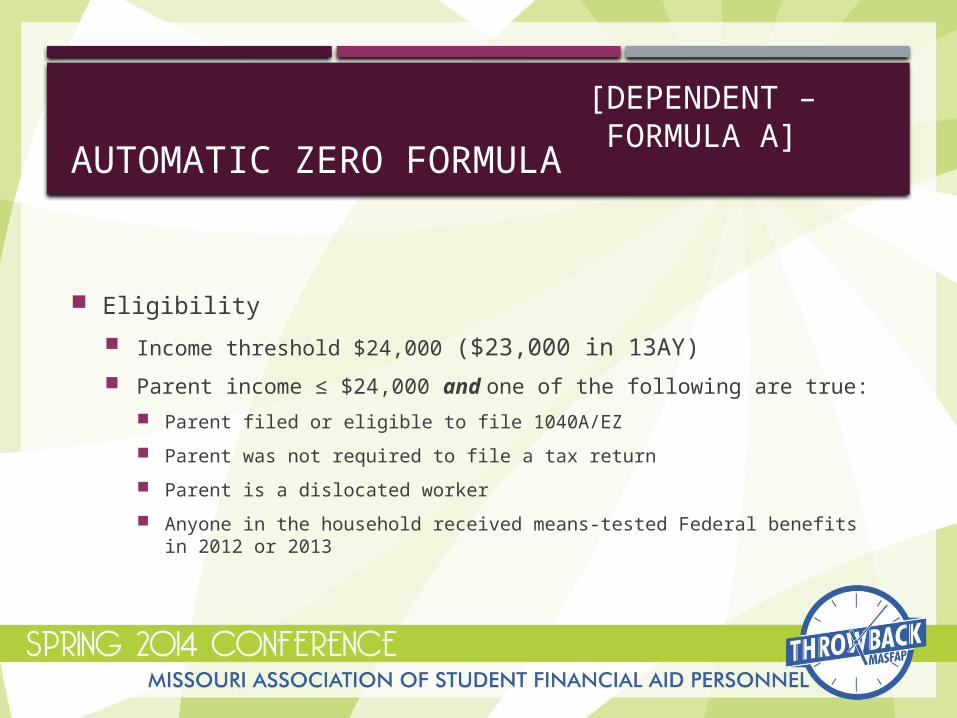

AUTOMATIC ZERO FORMULA

Eligibility

Income threshold $24,000 ($23,000 in 13AY) Parent income ≤ $24,000 and one of the following are true:

Parent filed or eligible to file 1040A/EZ

Parent was not required to file a tax return

Parent is a dislocated worker

Anyone in the household received means-tested Federal benefits in 2012 or 2013

[DEPENDENT – FORMULA A]

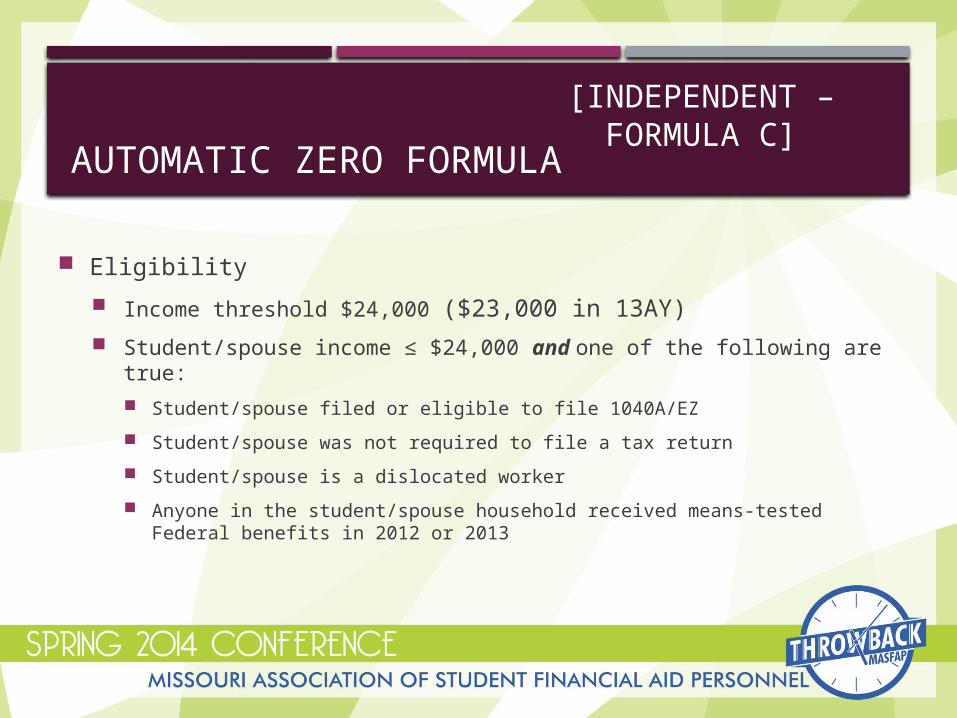

AUTOMATIC ZERO FORMULA

Eligibility

Income threshold $24,000 ($23,000 in 13AY) Student/spouse income ≤ $24,000 and one of the following are true:

Student/spouse filed or eligible to file 1040A/EZ

Student/spouse was not required to file a tax return

Student/spouse is a dislocated worker

Anyone in the student/spouse household received means-tested Federal benefits in 2012 or 2013

[INDEPENDENT – FORMULA C]

NEED ANALYSIS TERMS

Base year Refers to the tax year the FAFSA calculates

Available Income Refers to the assessed portion of discretionary income

Adjusted Available Income Refers to the available income plus contribution from

assets/discretionary net worth

NEED ANALYSIS TERMS

Terms you should know… Income Protection Allowance

Base Year

Available Income

Adjusted Available Income

Simplified/Simple Needs Formula

Automatic Zero Formula

Dependent versus Independent

PROFESSIONAL JUDGMENT

Can you apply professional judgment to the need analysis formula? NO! The need analysis formula cannot be altered

Elements of the formula may be changed with professional judgment (e.g., income earned from work, adjusted gross income, child support received, etc.)

When adjusted, these elements will change the result of the EFC when the formula is applied

Permissible under Section 479A of the HEA. Must have adequate documentation and adjustments must be made on a case-by-case basis (cannot apply to a category of students)

Professional judgment can also apply to areas such as dependency status, cost of attendance, satisfactory academic progress, etc.

EXAMPLES OF SPECIAL CIRCUMSTANCES IN HEA

Elementary or secondary school tuition expenses

Medical, dental, or nursing home expenses not covered by insurance Remember that approximately 11% of the Income Protection

Allowance is set aside from the need analysis formula for the family’s medical costs

Unusually high or dependent care costs

Recent unemployment of family member or independent student Notice what effect Dislocated Worker status has on the need analysis

formula

“UNREASONABLE” ADJUSTMENT EXAMPLES

Vacation expenses

Tithing expenses

Standard living expenses such as utilities, bills, credit card payments, cell phone, children’s allowances, etc.

Standard maintenance items such as lawn care, home repair, fuel, etc. Remember the Income Protection Allowance in which these types of

costs are already protected from the need analysis formula

VERIFICATION

If the student is selected for verification, you must verify the file before making any professional judgment adjustment. You may have an institutional

policy to verify any file prior to making a professional judgment decision.

PJ CASE STUDIES:

Xena is married and has two children Had $2,300 in unreimbursed medical expenses

Xena is the only family member in college

Daisy is a dependent student living with her mother and sister; she is the only family member in college

Daisy’s mother has incurred credit card debt of $8,000

PJ CASE STUDIES:

Topanga’s parent’s own a rental home with a net worth of $145,000 The rental home is destroyed due to Hurricane Sandy

Family loses potential rental income and insurance settlement is expected

Screech is a 20-year-old student and had lived with his mother and two younger siblings when in high school. His mother remarried last year and has a prenuptial agreement with the stepfather that he will not cover expenses for Screech.

Screech asks that his stepfather’s income be excluded because his mother and stepfather married after he started college.

WORKSHEETS AND TABLES

DEPENDENT CASE STUDY

Clint Westwood lives with two sisters, Gretchen and Winifred, and parents in Cooter, MO. He is enrolling in college as a freshman this year. He has a summer job where he earned $1,300 last year and has $200 in a savings account.

His mother, Dolly, is a secretary and earned $31,987 in 2013, and step-father, Cecil, works for the city and has one other child, Bartholomew (age 22), who attends college half-time. Last year, Cecil earned $62,246 and they have $0 in investments, $0 in a checking account, $0 in education tax credits, and $5,331 in federal income tax paid. They will file an IRS 1040.

Cecil is 50 years old and Dolly is 47 years old and AGI is $106,400.

CLINT WESTWOOD$106,400

$62,246

$31,987

$94,233

$106,400

$0

$106,400

$0

$106,400

$5,331

4% $4,256

$4,762

$2,447

$34,040

$4,000

$54,836

$106,400$54,836

$51,564

$0

$0

$0

$0

$0

$34,600

- $34,600

$0

$51,564$0

$51,564

($51,564 - $31,500) x 47% + $8,523 =

$17,953

2

$8,977

$8,977

$0

$40

$9,017

CASE STUDY ON YOUR OWN

Quinn Fabray [Dependent] Napoleon Dynamite [Dependent] Emma Pillsbury [Independent] Rudy Ruettiger [Dependent] Anheuser Busch [Dependent] Ronald Burgundy [Independent] Larry Crowne [Independent]

NEED ANALYSISANDPROFESSIONALJUDGMENTS

JUSTIN CHASE BROWN

CORTNEYJO SANDIDGEUNIVERSITY OF MISSOURIQUESTIONS?