ncl-coverage initiation

TRANSCRIPT

Aba Ali Habib Securities | Suite # 419,419-A, 421 4th Floor Pakistan Stock exchange building, Stock Exchange Road, Karachi, Pakistan.

24 September 2016

www.jamapunji.pk

Pakistan Research Textile Composite Sector

REP-055

December 16, 2016

We initiate coverage on Nishat Chunian Limited (NCL) with a BUY recommendation based

on a Jun-17 target price (TP) of PKR 83.1/share, offering an upside of 37.5% along with

dividend yield of 5.9%.

Initiation of coal based captive power plant will result in significant cost savings of

around PKR 4/KWH and will result in an EPS contribution of PKR 2.0/2.1/2.1 in

FY18/19/20.

Expansion in weaving and home textile division is likely to increase capacity by 3% and

15% respectively. It is likely to help EPS grow at CAGR of 13.2% during FY17-19.

Substantial Income received from subsidiary in form of dividends will continue due to

guaranteed income received from NTDCL/CPPA.

Valuation & recommendation

We initiate coverage on Nishat Chunian Limited (NCL) with a buy recommendation and Jun-17

price target (PT) of PKR 83.1/share, which offers an upside of 37.5% along with dividend yield of

5.9%. Our TP is derived by using FCFF based discounted cash flow methodology with WACC of

9.75% and terminal growth rate of 2.0%. NCL trades at an attractive LTM PER of 7.1x that is much

cheaper than industry LTM PER of 13.7x.

Coal based Captive power plant to result to healthy margins

Commencement of coal power plant in Feb’17 is likely to reduce cost/KWH by 30% from 13.5/unit

to ~9.5/unit. Consequently, savings are expected at PKR 473mn and PKR 487mn during FY18 and

FY19 respectively. Per share impact on bottom line is expected to be PKR 2.0-2.1 during FY17-19.

Moreover, export bailout package of ~PKR 75bn is also in the works by GoP and is likely to be a

strong upside trigger to scrip; however, absent particulars, it is difficult to guage the impact of the

bailout at this stage.

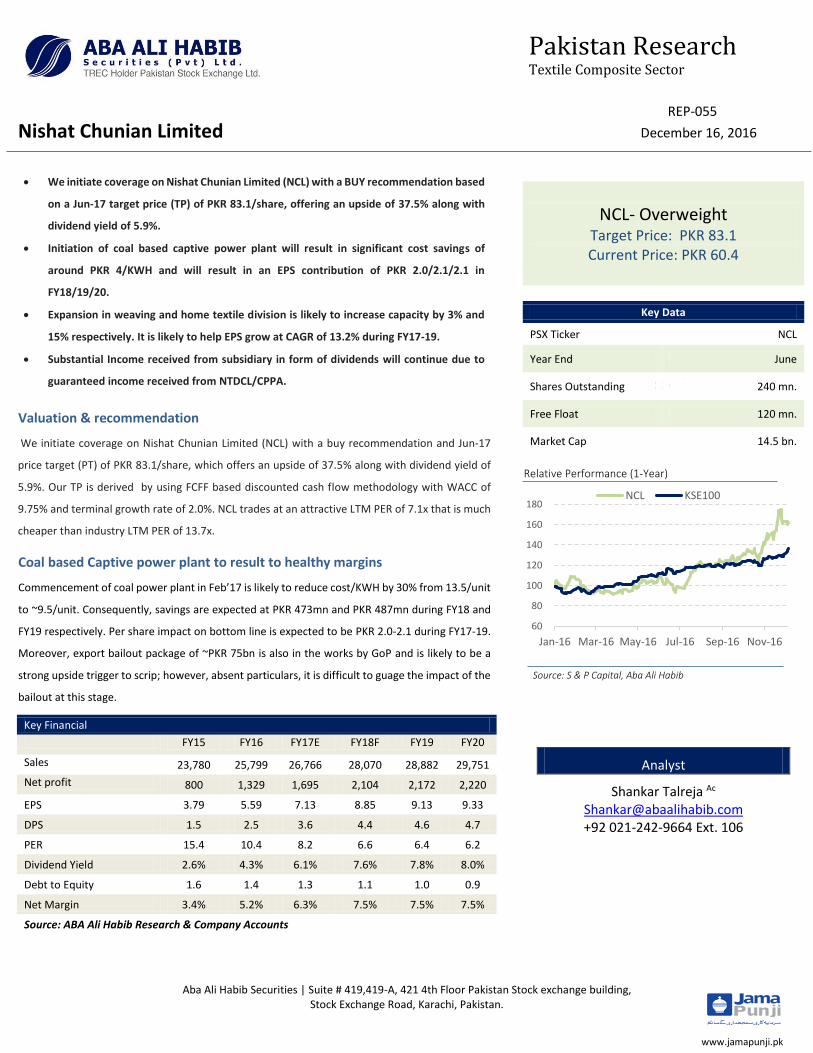

NCL- Overweight Target Price: PKR 83.1 Current Price: PKR 60.4

Key Data

PSX Ticker NCL

Year End June

Shares Outstanding 240 mn.

Free Float 120 mn.

Market Cap 14.5 bn.

Key Financial

FY15 FY16 FY17E FY18F FY19 FY20

Sales 23,780 25,799 26,766 28,070 28,882 29,751

Net profit 800 1,329 1,695 2,104 2,172 2,220

EPS 3.79 5.59 7.13 8.85 9.13 9.33

DPS 1.5 2.5 3.6 4.4 4.6 4.7

PER 15.4 10.4 8.2 6.6 6.4 6.2

Dividend Yield 2.6% 4.3% 6.1% 7.6% 7.8% 8.0%

Debt to Equity 1.6 1.4 1.3 1.1 1.0 0.9

Net Margin 3.4% 5.2% 6.3% 7.5% 7.5% 7.5%

Source: ABA Ali Habib Research & Company Accounts

Nishat Chunian Limited

Analyst

Shankar Talreja Ac [email protected] +92 021-242-9664 Ext. 106

Relative Performance (1-Year)

Source: S & P Capital, Aba Ali Habib

60

80

100

120

140

160

180

Jan-16 Mar-16 May-16 Jul-16 Sep-16 Nov-16

NCL KSE100

Aba Ali Habib Securities (Pvt.) Ltd.

2

Pakistan Research

Capacity expansion to result in topline growth in value added segment

NCL plans to continue expansion of its capacities in weaving and home textile segments. Company

is expected to install 12 additional looms for its weaving segment which will increase its weaving

capacity by 3%. Moreover, in home textile division company is likely to install modern mercerizing

machine with continuous washing plant which will increase capacity by 15%. Helped by savings

from the coal based power plant and expansion in the weaving and home textile segments, NCL’s

EPS is expected to grow at CAGR of 13.2% during FY17-19.

Dividend income from NCPL poised to remained strong

Dividend income of the company during FY16 clocked in at PKR 1.19bn which translates EPS

contribution of PKR 4.73/share against PKR 6.65/share in FY15. We anticipate a continuing trend

in forthcoming years and company will receive dividend income of PKR 1.36bn in FY17 from its

subsidiary NCPL, which will contribute an EPS of PKR 5.52.

Deleveraging to improve profitability

NCL continued to pay off its debt which has reduced its debt to capital from 61% in FY14 to 55%

in FY16. We foresee timely payments of debt will bring debt to capital ratio to 43% in FY21. Lower

debt level would reduce finance cost from PKR 1.02bn in FY16 to PKR 834mn in FY21.

Key risks

Shortage of cotton crop in ongoing fiscal year heightened cotton spot price to ~PKR 6300 in Dec’16

from PKR 5900 in mid of Nov ’16. Any further surge in cotton prices can negatively impact spinning

segment of the company.

Financial highlights 1QFY17

During 1QFY17 company posted EPS of PKR 2.35 against loss per share of 0.45 in SPLY on back of

rise in topline by 18.1% YoY and relatively stable exchange rate. Gross margins of the company

witnessed improvement of 4 ppts on account of lower crude oil prices. Moreover, Dividend income

received from NCPL was PKR 365mn which constituted 65% of overall EPS of NCL.

Key Financial Ratios

1QFY17 1QFY16 YoY FY15 FY16 YoY

PAT (mn) 565 (108) 622% 800.4 1,328.8 66.0%

EPS 2.35 (0.45) 622% 3.79 5.59 47.6%

Gross Margin 11.5% 7.5% -- 8% 10% -

Net Margin 8.2% (1.8%) -- 3% 5% -

Current Ratio 1.05 1.01 3.8% 1.05 1.01 -3.9%

Debt to Equity 1.28 1.44 (10.9%) 1.56 1.44 -7.8%

Source: Aba Ali Habib Research and Company Accounts

Source: S & P Capital, Aba Ali Habib

EPS & DPS Outlook

3.8

5.6

7.1

8.8 9.1 9.3

1.5

2.5

3.6 4.4 4.6 4.7

0

2

4

6

8

10

FY15 FY16 FY17E FY18F FY19F FY20F

EPS DPS

Source: S & P Capital, Aba Ali Habib

Aba Ali Habib Securities (Pvt.) Ltd.

3

Pakistan Research

Disclaimer

This report has been prepared by Aba Ali Habib Securities and is provided for information purposes only. Under no circumstances this is to be used or

considered as an offer to sell or solicitation of any offer to buy. While reasonable care has been taken to ensure that the information contained therein is

not untrue or misleading at the time of publication, we make no representation as to its accuracy or completeness and it should not be relied upon as

such. From time to time, Aba Ali Habib Securities and/or any of its officers or directors may, as permitted by applicable laws, have a position, or otherwise

be interested in any transaction, in any securities directly or indirectly subject of this report. This report is provided only for the information of professional

advisers who are expected to make their own investment decisions without undue reliance on this report. Investments in capital markets are subject to

market risk and Aba Ali Habib Securities accepts no responsibility whatsoever for any direct or indirect consequential loss arising from any use of this

report or its contents.

In particular, the report takes no account of the investment objectives, financial situation and particular needs of investors, who should seek further

professional advice or rely upon their own judgment and acumen before making any investment. The views expressed in this report are those of Aba Ali

Habib Securities’ Research Department and do not necessarily reflect those of the company or its directors. Aba Ali Habib as a firm may have business

relationships, including investment‐ banking relationships, with the companies referred to in this report. Aba Ali Habib Securities or any of its officers,

directors, principals, employees, associates, close relatives may act as a market maker in the securities of the subject company, may have a financial

interest in the securities of the subject company to an amount exceeding 1% of the value of the securities of the subject company, may serve or may have

served in the past as a director or officer of the subject company, may have received compensation from the subject company for corporate advisory

services, brokerage services or underwriting services or may expect to receive or intend to seek compensation from the subject company for the aforesaid

services, may have managed or co-managed a public offering, take-over, buyback, delisting offer of securities or various other functions for the subject

company.

All rights reserved by Aba Ali Habib Securities. This report or any portion hereof may not be reproduced, distributed or published by any person for any

purpose whatsoever. Nor can it be sent to a third party without prior consent of Aba Ali Habib Securities. Action could be taken for unauthorized

reproduction, distribution or publication.

Analyst Certification AC

The research Analyst(s) hereby certify that the views about the company/companies and the security/securities discussed in this report accurately reflect

his or her or their personal views and that s/he has not received and will not receive direct or indirect compensation in exchange for expressing specific

recommendation or views in this report. The analyst(s) is/are principally responsible for preparation of this research report and that s/he or his/her close

relative/family member doesn’t own 1% or more of a class of common equity securities of the following company/companies covered in this report.

Contact

Aba Ali Habib Securities (Pvt.) Limited

PH: 021-242-9664 (4 Lines), Fax: 021-241-3822