naturhouse health, s.a. and subsidiaries sales of all kinds of products related to dietetics,...

TRANSCRIPT

Naturhouse Health, S.A. and Subsidiaries

Consolidated Abridged Interim Financial Statements and Consolidated Management Report for the six months ending 30th June 2016, drawn up in accordance with International Accounting Standard 34, together with the Limited Review Report

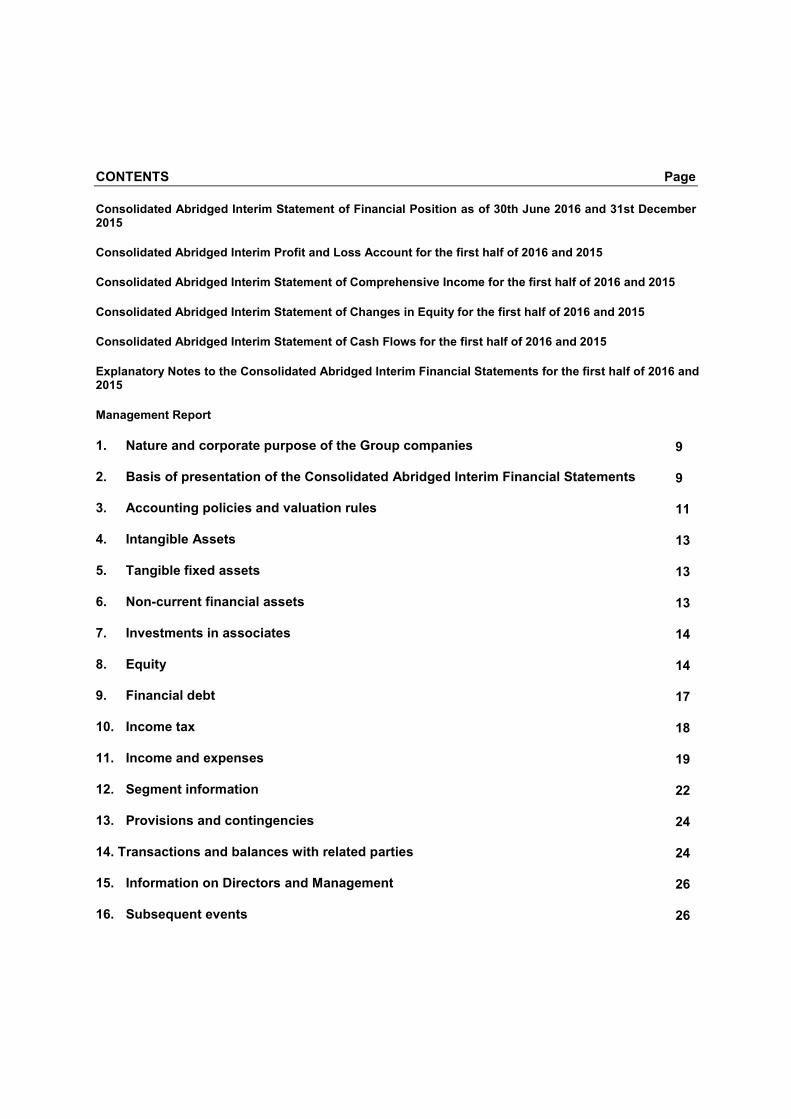

CONTENTS Page

Consolidated Abridged Interim Statement of Financial Position as of 30th June 2016 and 31st December 2015

Consolidated Abridged Interim Profit and Loss Account for the first half of 2016 and 2015

Consolidated Abridged Interim Statement of Comprehensive Income for the first half of 2016 and 2015

Consolidated Abridged Interim Statement of Changes in Equity for the first half of 2016 and 2015

Consolidated Abridged Interim Statement of Cash Flows for the first half of 2016 and 2015

Explanatory Notes to the Consolidated Abridged Interim Financial Statements for the first half of 2016 and 2015

Management Report

1. Nature and corporate purpose of the Group companies

2. Basis of presentation of the Consolidated Abridged Interim Financial Statements

3. Accounting policies and valuation rules

4. Intangible Assets

5. Tangible fixed assets

6. Non-current financial assets

7. Investments in associates

8. Equity

9. Financial debt

10. Income tax

11. Income and expenses

12. Segment information

13. Provisions and contingencies

14. Transactions and balances with related parties

15. Information on Directors and Management

16. Subsequent events

9

9

11

13

13

13

14

14

17

18

19

22

24

24

26

26

3

Naturhouse Health, S.A. and Subsidiaries

CONSOLIDATED ABRIDGED INTERIM STATEMENT OF FINANCIAL POSITION AS OF 30TH JUNE 2016 AND 31ST DECEMBER 2015

(Thousands of Euros)

ASSETS

Notes

30/06/2016

31/12/2015

EQUITY AND LIABILITIES

Notes

30/06/2016

31/12/2015

NON-CURRENT ASSETS:

Intangible assets

Tangible fixed assets

Non-current financial assets

Investments in associates- Holdings

consolidated under the equity method

Deferred tax assets

Total non-current assets

CURRENT ASSETS:

Stock

Customers receivable for sales and provision of

services

Customers, related companies

Current tax assets and other credits with public

administrations

Other current assets Current

financial assets

Cash and other equivalent liquid assets

Total current assets

4

5

6

7

10.1

14

14

2,065

4,874

832

2,983

2,983

509

2,193

5,025

813

3,140

3,140

369

EQUITY:

Capital and

reserves- Share

capital Issue

premium Reserves

Own shares and company shares

Conversion differences

Profit for the financial

year Interim dividend

EQUITY ATTRIBUTABLE TO THE PARENT

COMPANY'S SHAREHOLDERS

EQUITY ATTRIBUTABLE TO THIRD-PARTY SHAREHOLDERS

Total Equity

NON-CURRENT LIABILITIES:

Non-current provisions

Non-current debts

Deferred tax liabilities

Total non-current liabilities

CURRENT LIABILITIES:

Current debts

Financial liabilities with related parties Trade

creditors and other accounts payable Suppliers,

related companies

Current tax liabilities and other debts with public

administrations

Total current liabilities

TOTAL EQUITY AND LIABILITIES

8

13

9

10.2

9

14

14

3,000

2,149

12,176

(249)

(306)

13,920

-

30,690

56

3,000

2,149

8,225

(214)

(115)

22,860

(14,050)

21,855

161

11,263 11,540

3,657

3,541

30,746 22,016

1,108

1,044

3,093 2,930

397 478

4,598 4,452

329

1,960

6,801 4,952

1 21

233 569 5,313 4,776

780 876 6,063 4,424

604 42 3,445

2,298 28,600 19,830

40,676 29,831 16,595 14,903

51,939 41,371 51,939 41,371

Notes 1 to 16 and Annex I attached are an integral part of the consolidated abridged statement of financial position as of 30th June 2016.

4

Naturhouse Health, S.A. and Subsidiaries

CONSOLIDATED ABRIDGED INTERIM PROFIT AND LOSS ACCOUNT FOR THE FIRST HALF OF 2016 AND 2015

(Thousands of Euros)

Notes

First half of the

2016 financial

First half of the

2015 financial

CONTINUING OPERATIONS: 11

54,503

52,556 Net Turnover

Supplies (15,984) (15,471)

Gross Margin 38,519 37,085

Other operating income 354 371

Personnel expenses 11.a (9,539) (9,276)

Other operating expenses (9,403) (8,815)

Operating income before amortizations, impairments and other results 19,931 19,365

Amortization of fixed assets (538) (602)

Impairment and income from disposal of fixed assets (183) (22)

OPERATING RESULT 19,210 18,741

Financial income 11.b (61) (224)

Share in profits from equity-accounted companies 7 528 579

PRE-TAX CONSOLIDATED PROFIT OR LOSS 19,677 19,096

Corporate Tax (5,764) (5,872)

NET PROFIT OR LOSS FROM CONTINUING OPERATIONS 13,913 13,224

NET CONSOLIDATED PROFIT OR LOSS

13,913 13,224

Profit or loss attributable to third party shareholders 7 60

NET PROFIT OR LOSS ATTRIBUTABLE TO THE PARENT COMPANY 13,920 13,284

Profit/(loss) per share (in euros per share): 8 0.23

0.22 - Basic

- Diluted 0.23 0.22

Notes 1 to 16 and Annex I attached are an integral part

of the consolidated abridged interim profit and loss account for the first half of the 2016 financial year

5

Naturhouse Health, S.A. and Subsidiaries

CONSOLIDATED ABRIDGED INTERIM STATEMENT OF COMPREHENSIVE

INCOME FOR THE FIRST HALF OF 2016 AND 2015

(Thousands of Euros)

First half of the

2016 financial

First half of the

2015 financial

A- PROFIT AND LOSS ACCOUNT BALANCE

B- OTHER COMPREHENSIVE INCOME RECOGNISED DIRECTLY IN EQUITY

Items not to be transferred to income

Items that can later be transferred to income:

Differences due to the conversion of financial statements in foreign currency

C- TRANSFER TO THE PROFIT AND LOSS ACCOUNT

TOTAL CONSOLIDATED COMPREHENSIVE INCOME FOR THE FINANCIAL YEAR (A+B+C)

Total Comprehensive Income attributable to:

- The Parent Company

- Minority shareholders

TOTAL CONSOLIDATED COMPREHENSIVE INCOME

13,913 13,224

-

-

(197)

(58)

- -

13,716 13,166

13,729

13,252

(13) (86)

13,716 13,166

Notes 1 to 16 and Annex I attached are an integral part of the consolidated abridged interim

statement of comprehensive income for the first half of the 2016 financial year.

6

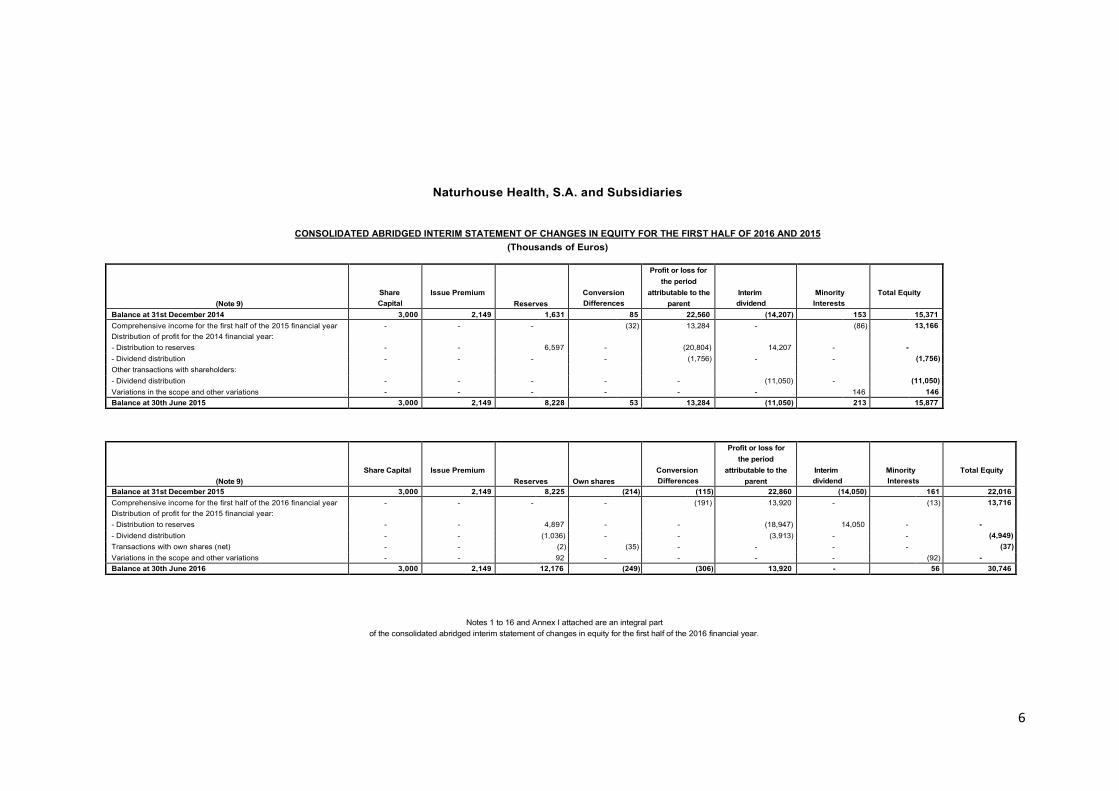

Naturhouse Health, S.A. and Subsidiaries

CONSOLIDATED ABRIDGED INTERIM STATEMENT OF CHANGES IN EQUITY FOR THE FIRST HALF OF 2016 AND 2015

(Thousands of Euros)

(Note 9)

Share

Capital

Issue Premium

Reserves

Conversion

Differences

Profit or loss for

the period

attributable to the

parent

Interim

dividend

Minority

Interests

Total Equity

Balance at 31st December 2014 3,000 2,149 1,631 85 22,560 (14,207) 153 15,371

Comprehensive income for the first half of the 2015 financial year - - -

(32) 13,284 -

(86)

13,166

Distribution of profit for the 2014 financial year:

- Distribution to reserves - -

6,597 -

(20,804)

14,207 -

-

- Dividend distribution - - -

-

(1,756) -

-

(1,756)

Other transactions with shareholders:

- Dividend distribution - - -

-

-

(11,050) -

(11,050)

Variations in the scope and other variations - - -

-

- -

146

146

Balance at 30th June 2015 3,000 2,149 8,228 53 13,284 (11,050) 213 15,877

(Note 9)

Share Capital

Issue Premium

Reserves

Own shares

Conversion

Differences

Profit or loss for

the period

attributable to the

parent

Interim

dividend

Minority

Interests

Total Equity

Balance at 31st December 2015 3,000 2,149 8,225 (214) (115) 22,860 (14,050) 161 22,016

Comprehensive income for the first half of the 2016 financial year - - -

-

(191)

13,920 -

(13)

13,716

Distribution of profit for the 2015 financial year:

- Distribution to reserves - -

4,897 -

-

(18,947) 14,050 -

-

- Dividend distribution - -

(1,036) -

-

(3,913) - -

(4,949)

Transactions with own shares (net) - -

(2)

(35) -

-

- -

(37)

Variations in the scope and other variations - -

92 -

-

-

-

(92) -

Balance at 30th June 2016 3,000 2,149 12,176 (249) (306) 13,920 - 56 30,746

Notes 1 to 16 and Annex I attached are an integral part

of the consolidated abridged interim statement of changes in equity for the first half of the 2016 financial year.

7

Naturhouse Health, S.A. and Subsidiaries

CONSOLIDATED ABRIDGED INTERIM STATEMENT OF CASH FLOWS FOR THE FIRST HALF OF 2016

AND 2015

(Thousands of Euros)

First half of the

2016 financial

First half of the

2015 financial

CASH FLOWS FROM OPERATING ACTIVITIES

Pre-tax profit or loss for the financial year

Adjustments to the profit or loss:

- Amortization of fixed assets (+)

- Impairment losses of tangible fixed assets and stock (+/-)

- Variation in provisions (+/-)

- Financial income (-)

- Financial expenses (+)

- Exchange differences (+/-)

- Share in profits or losses (losses) from equity-accounted companies (+/-)

Changes in working capital

- Stock (+/-)

- Debtors and other accounts receivable (+/-)

- Other current assets (+/-)

- Creditors and other accounts payable (+/-)

Other cash flows from operating activities

- Interest payments (-)

- Collection of interest (+)

- Collections (payments) of income tax (+/-)

CASH FLOWS FROM INVESTMENT ACTIVITIES

Payments for investments (-)

- Intangible and tangible fixed assets

- Other financial assets

Collections from divestments (+)

- Collections from related companies

- Intangible and tangible fixed assets

- Other financial assets

CASH FLOWS FROM FINANCING ACTIVITIES

Collections and payments for equity instruments

- Net acquisition of own equity instruments (-)

Collections and payments for financial liability instruments

- Repayment and amortization of:

Debts with credit institutions (-)

Dividend payments and remuneration of other equity instruments

- Dividends (-)

EFFECT OF VARIATIONS IN EXCHANGE RATES NET

INCREASE/DECREASE IN CASH AND CASH EQUIVALENTS

Cash or cash equivalents at the start of the

financial year

Cash or cash equivalents at year-end

15,711 13,692

19,677 19,096

254 392

538 602

183 22

-

123

(31) (18)

76 230

16 12

(528) (579)

(345) (261)

(116) (57)

(1,493) (1,645)

96 92

1,168 1,349

(3,875) (5,535)

(76) (230)

31 18

(3,830) (5,323)

(397) 10,680

(461)

(443)

(442)

(241)

(19)

(202)

64

11,123

-

11,007

-

116

64 -

(6,454) (15,390)

(37) -

(37) -

(1,468)

(2,584)

(1,468) (2,584)

(4,949)

(12,806)

(4,949)

(12,806)

(90) 65

8,770 9,047

19,830 8,659

28,600 17,706

Notes 1 to 16 and Annex I attached are an integral part of the consolidated abridged interim

statement of cash flows for the first half of the 2016 financial year.

9

Naturhouse Health, S.A. and Subsidiaries Explanatory Notes to the Consolidated Abridged Interim Financial Statements for the first half of the 2016 financial year

1. Nature and corporate purpose of the Group companies

Naturhouse Health, S.A. (hereinafter, the "Company" or the "Parent Company"), was founded for an indefinite period in Barcelona on 29th July 1991 with VAT number A-01115286.

At the start of the 2015 financial year, its registered offices were located at Calle Botánica 57-61, en L’Hospitalet

de Llobregat, Barcelona. On 24th May 2016, the registered offices were moved to Calle Pasaje Pedro Rodríguez, número 6, in Barcelona.

The Company's corporate purpose, in accordance with its articles of association, is the export and wholesale and retail sales of all kinds of products related to dietetics, medicinal herbs and natural cosmetics, as well as the preparation, promotion, creation, edition, dissemination, sale and distribution of all kinds of magazines, books and brochures and the marketing of dietary products, medicinal herbs and natural cosmetics. This activity is mainly carried out through its own shops or through franchisees. In addition to the operations carried out directly, the Company is the parent of a group of subsidiaries that engage in the same activity and which, together with it, make up Grupo Naturhouse Health (hereinafter, the "Group" or "Naturhouse Group"). Note 3 and Annex I detail the main data related to the subsidiaries in which the Parent Company, directly or indirectly, has a holding that have been included in the scope of the consolidation.

At present, Naturhouse Group mainly operates in Spain, Italy, France and Poland.

On 9th April 2015, the Board of Directors, exercising the delegation of its Sole Shareholder of the Parent Company of 2nd October 2014, requested official listing for trading on the Stock Exchanges of Madrid, Barcelona, Bilbao and Valencia and the subsequent public stock offering on the Spanish Stock Market, which culminated successfully, consequently, the securities of the Parent Company have been listed since 24th April 2015 (See Note 8.a).

2. Basis of presentation of the Consolidated Abridged Interim Financial Statements

a) Basis of presentation

These consolidated abridged interim financial statements for the six months ending 30th June 2016 have been drawn up in accordance with International Accounting Standard 34 (IAS 34) "Interim Financial Information" included in the International Financial Reporting Standards adopted by the European Union (EU-IFRS). These interim financial statements do not include all the information required of complete consolidated financial statements under the EU-IFRS. Therefore, these consolidated abridged interim financial statements should be read in conjunction with the consolidated financial statements for the financial years ending 31st December 2015, which were drawn up in accordance with EU-IFRS. Consequently, it has not been necessary to repeat or update certain notes or estimates included in the aforementioned consolidated financial statements. Instead, the accompanying selected explanatory notes include an explanation, where appropriate, of any events or variations that are material to understanding the changes in the consolidated financial position and in the consolidated results of operations, the consolidated comprehensive income and the consolidated cash flows of the Naturhouse Group from 31st December 2015, the date of the aforementioned consolidated financial statements, to 30th June 2016.

10

In accordance with IAS 8, the accounting principles and valuation rules applied by the Group have been applied uniformly across all transactions, events and items in the first half of the 2016 financial year and in the 2015 financial year.

The figures contained in all the financial statements forming part of the consolidated abridged interim financial statements (consolidated abridged statement of financial position, consolidated abridged interim profit and loss account, consolidated abridged interim statement of comprehensive income, consolidated abridged interim statement of changes in equity, consolidated abridged interim statement of cash flows) and the explanatory notes to the consolidated abridged interim financial statements are expressed in thousands of euros, unless otherwise stated.

Also, in order to present the different items making up the consolidated abridged interim financial statements, in a standardised manner, the valuation rules and principles used by the Parent Company have been applied to all the companies included within the scope of the consolidation.

The consolidated abridged financial statements for the first half of 2016 have been subjected to a limited review by the auditor.

b) Responsibility for the information and accounting estimates and judgements made

The preparation of the summary consolidated intermediate financial statements under IFRS/EU requires the Parent Company's Directors to perform certain accounting estimates and to consider certain elements of judgement. These are continually evaluated and are based on historical experience and other factors, including expectations of future events, which have been considered reasonable under the circumstances. While the estimates have been made on the best information available as of the date of preparing these consolidated financial statements, in accordance with IAS 8, any amendment in the future to these estimates would be applied prospectively, recognising the effect of the change in the estimate made in the consolidated profit and loss account for the financial year in question. The main accounting principles and policies and valuation criteria are given in Notes 2 and 5 of the Explanatory Notes to the 2015 financial year's consolidated financial statements.

The main estimates and judgements considered in drawing up the consolidated abridged interim financial statements are as follows:

- Useful lives of intangible and tangible fixed assets.

- Impairment losses of non-financial assets.

- Evaluation of occurrence and quantification of litigation, commitments, contingent assets and liabilities at close.

- Estimate of impairments for defaults in accounts receivable and inventory obsolescence.

- Estimate of income tax expenses (which, according to IAS 34, is recognised in interim periods based on the best estimate of the average weighted tax rate that the Group expects for the annual period) and recoverability of deferred tax assets.

c) Information comparison

According to paragraph 20 of IAS 34, and in order to have comparative information available, these consolidated abridged interim financial statements include the consolidated abridged statements of financial position as of 30th June 2016 and 31st December 2015 and the consolidated abridged interim profit and loss accounts, the consolidated abridged interim statements of comprehensive income, the consolidated abridged interim statements of changes in equity and the consolidated abridged interim statements of cash flows for the six-month periods ending 30th June 2016 and 2015, in addition to the explanatory notes to the consolidated abridged interim financial statements for the six-month period ending 30th June 2016.

The main variations in the scope of the consolidation are described in Note 3c.

11

d) Seasonality of transactions

The Group is subject to seasonal fluctuations in the demand for its dietary, medicinal herbal and natural cosmetic products, primarily. In this regard, it tends to experience higher sales in the months preceding the summer (March to July), although without the seasonality having a very significant impact. Consequently, this aspect should be taken into consideration when comparing the Group's half-yearly and yearly information, as well the interim periods.

e) Relative importance

When determining the information to be broken down in these explanatory notes on the different items of the financial statements or other matters, the Group, in accordance with IAS 34, has taken into consideration the relative importance in relation to the half-yearly consolidated abridged financial statements.

f) Correction of errors

No correction of errors have been made in the consolidated abridged financial statements for the six months ending 30th June 2016.

3. Accounting policies and valuation rules

The accounting policies and valuation rules that have been followed in these consolidated abridged interim financial statements as of 30th June 2016 are the same as those used in the consolidated financial statements for the financial year ending 31st December 2015, except for the following:

a) Changes in accounting policies and breakdown of information effective in the 2016 financial year

New accounting standards came into effect in the 2016 financial year, therefore, they have been taken into consideration in the preparation of the attached summary consolidated intermediate financial statements.

The following standards have been applied in these consolidated abridged interim financial statements, but they did not have a significant impact on the figures and breakdown therein:

New standards, amendments and interpretations:

Contents: Mandatory application

for financial years from:

Amendments to IAS 19 - Employee contributions to defined benefit plans (published in November 2013)

The amendment is issued to facilitate the ability to deduct these service cost contributions in the same period in which they are paid if certain requirements are met.

1st February 2015 (1)

Improvements to IFRS 2010-2012 Cycle (published in December 2013)

Minor amendments to a series of standards. 1st February 2015 (1)

Amendments to IAS 16 and IAS 38 - Acceptable methods of depreciation and amortization (published in May 2014)

Clarifying acceptable methods of depreciation and amortization of intangible and tangible fixed assets, which do not include those based on revenue.

1st January 2016

Amendments to IFRS 11 - Accounting for acquisitions of holdings in joint ventures (published in May 2014)

Specifying the accounting for the acquisition of a holding in a joint venture whose activities constitute a business.

1st January 2016

Amendments to IAS 16 and IAS 41: Producing plants (published in June 2014)

Producing plants shall be taken at cost, rather than fair value.

1st January 2016

Improvements to IFRS 2012-2014 Cycle (published in September 2014)

Minor amendments to a series of standards. 1st January 2016

Amendments to IAS 27 Equity Method in Separate Financial Statements (published in August 2014)

The equity application of individual financial statements of an investor will be allowed.

1st January 2016

Modifications IAS 1: Breakdowns initiative (December 2014)

Various clarifications regarding breakdowns (materiality, aggregation, order of notes etc.).

1st January 2016

(1) The date of entry into force of this standard was from 1st July 2014.

12

b) Accounting policies issued not in force for the 2016 financial year

At the date of preparing these Summary consolidated intermediate financial statements , the following standards and interpretations had been published by the International Accounting Standard Board (IASB) but had not yet entered into force, either because their effective date is later than the date of these Summary consolidated intermediate financial statements , or because they have not yet been adopted by the European Union (EU-IFRS):

New standards, amendments and interpretations Mandatory application for

financial years from:

Not yet approved for use in the European Union on this document's date of publication

Amendments to IFRS 10, IFRS 12 and IAS 28: Investment Companies (December 2014)

Clarifications on the exception regarding consolidation of investment companies

1st January 2016

New standards

IFRS 15 Revenue from contracts with customers (published in May 2014) and its clarifications (published in April 2016)

New revenue recognition standard (replaces IAS 11, IAS 18, IFRIC 13, IFRIC 15, IFRIC 18 and SIC 31).

1st January 2018

IFRS 9 Financial Instruments (last phase published in July 2014)

Replacing the requirements for classification, valuation, recognition and derecognition of financial assets and liabilities, hedge accounting and impairment of IAS 39.

1st January 2018

IFRS 16 Leases (published in January 2016)

Replacing IAS 17 and associated interpretations. The main new development lies in the new standard proposing a single accounting model for lessees, which will include all the leases in the balance sheet (with some limited exceptions) with an impact similar to that of the current financial leases (there will be amortization of the asset for the right of use and a financial expense for the amortized cost of the liability).

1st January 2019

Amendments and interpretations

Amendment to IAS 7 Breakdowns initiative (published in January 2016)

Introducing additional breakdown

requirements in order to improve the

information provided to users.

1st January 2017

Amendment to IAS 12 Recognition of deferred tax assets for unrealised losses (published in January 2016)

Clarification of the principles established regarding the recognition of deferred tax assets for unrealised losses

1st January 2017

Amendment to IFRS 2 Classification and measurement of share-based payments (published in June 2016)

These are limited amendments clarifying specific issues such as the effects of vesting conditions on cash-settled share-based payments, the classification of share-based payments with net settlement features and some aspects of the amendments to the type of share-based payments.

1st January 2018

Amendments to IFRS 10 and IAS 28 Sale or assets contribution between an investor and its associate/joint venture (published in September 2014)

Clarification regarding the income from these operations in the case of asset businesses.

No definite date

(1) The state of approval of the standards by the European Union can be consulted on the EFRAG website.

The Parent Company's Directors have not considered the early application of the aforementioned Standards and Interpretations and, in any case, their application will be considered by the Group once approved, where appropriate, by the European Union.

13

In any case, the Directors of the Parent Company are assessing the potential impact of the future application of these standards.

c) Variations in the scope of the consolidation

During the first half of the 2016 financial year, the Naturhouse Group increased its share in the company Zamodiet México S.A. de C.V. from 51% to 79%, since the Parent Company acquired 29,389 new shares through the capitalisation of credits. On the other hand, the variations in the first half of the 2015 financial year corresponded to the establishment of three new subsidiaries: Naturhouse d.o.o. (Croatia), UAB Naturhouse (Lithuania) and Naturhouse Inc. (USA). The Group paid approximately 100 thousand euros as share capital, both in Naturhouse d.o.o. (Croatia), as well as in UAB Naturhouse (Lithuania), through its subsidiary Naturhouse S.p Zo.o. (Poland), while as of 30th June 2015, no disbursement had been made for the subsidiary established in the USA through Naturhouse Health, S.A.

4. Intangible Assets

During the first half of the 2016 financial year, there have been no significant additions to intangible assets. The decrease corresponds to the amount allocated for amortization in the period. In addition, the main asset recorded under this heading corresponds to brands acquired in previous financial years by Kiluva, S.A. amounting to 2,331 thousand euros, for which impairment indicators have not been demonstrated in accordance with the sales and margins obtained in the commercialisation of the products related to these brands.

5. Tangible fixed assets

During the first half of the 2016 financial year, there have been no significant additions to the Group's tangible fixed assets, with the variation in this heading basically corresponding to the amount allocated to the amortization thereof as well as to the derecognitions of non-transferable items recorded as a result of the Parent Company's change of registered offices. The Group recorded a loss amounting to 201 thousand euros corresponding to the net book value of the non-transferable items.

The Group's policy is to take out insurance policies to cover the potential risks to which the tangible fixed asset elements are subject. As of 30th June 2016, the Parent Company's Directors deem that there was no deficit in insuring against these risks.

As of the end of the first half of the 2016 financial year, the Group had no significant firm commitments to purchase tangible assets.

6. Non-current financial assets

As of 30th June 2016 and 31st December 2015, the breakdown on the various non-current financial investment accounts is as follows:

Thousands of Euros

30/06/2016 31/12/2015

Equity instruments

- Assets available for sale 42 42

- Other equity instruments 76 76

Other financial assets

- Long term deposits and guarantees 714 695

Total 832 813

14

During the first half of the 2016 financial year, there have been no significant movements under this heading.

7. Investments in associates

Participation in equity-accounted companies

The participation in equity-accounted companies corresponds to the investee company Ichem, Sp. zo.o. The breakdown on investment in equity-accounted companies at the end of the first half of the 2016 financial year and the movement occurring during this period is as follows:

June 30, 2016 – Thousands of Euros

Balance on

January 1,

2016

Participation

in results

from equity-

accounted

companies

Conversion

differences Dividends

Balance on

June 30,

2016

Participation in equity-accounted companies 3,140 528 (123) (562) 2,983

Total 3,140 528 (123) (562) 2,983

Other information related to this investee is as follows (figures as of 30 June 2016 and in thousands of Euros):

Name and Registered

Office Activity Total Assets Equity Sales (*)

Result after tax

(*)

Ichem Sp. Zo.o Production and commercialisation of

pharmaceutical and dietary

products

Dostawcza 12 19,483 13,093 11,061 2,120

93-231 Lodz (Poland)

(*) Sales and result from Ichem, Sp. Zo.o included that corresponding to the 6 months period ended June 30, 2016. The total assets and equity is presented at the closing exchange rate as of 30th June 2016, while sales and the post-tax profit or loss is presented at the average exchange rate for the six-month period ending 30th June 2016.

As of 30th June 2016, the Group had the dividends approved by Ichem Sp. zo.o. to be recovered, amounting to 562 thousand euros (Note 14).

8. EQUITY

The movement occurring in the first half of 2016 and 2015 under "Equity" in the consolidated abridged interim statement of financial position as of 30th June 2016 was as follows:

Thousands of Euros

30.06.2016 30.06.2015

Balance at start of period 22,016 15,371

Dividend distribution (4.949) (12.806)

Recognised income and expenses 13,716 13,166

Net transactions with shares (37) -

Variations in the scope - 146

Balance at end of period 30,746 15,877

a) Share Capital

As of 30th June 2016 and 31st December 2015, the Parent Company's share capital is represented by 60,000,000 ordinary shares of 0.05 euros nominal value each, fully subscribed and paid.

15

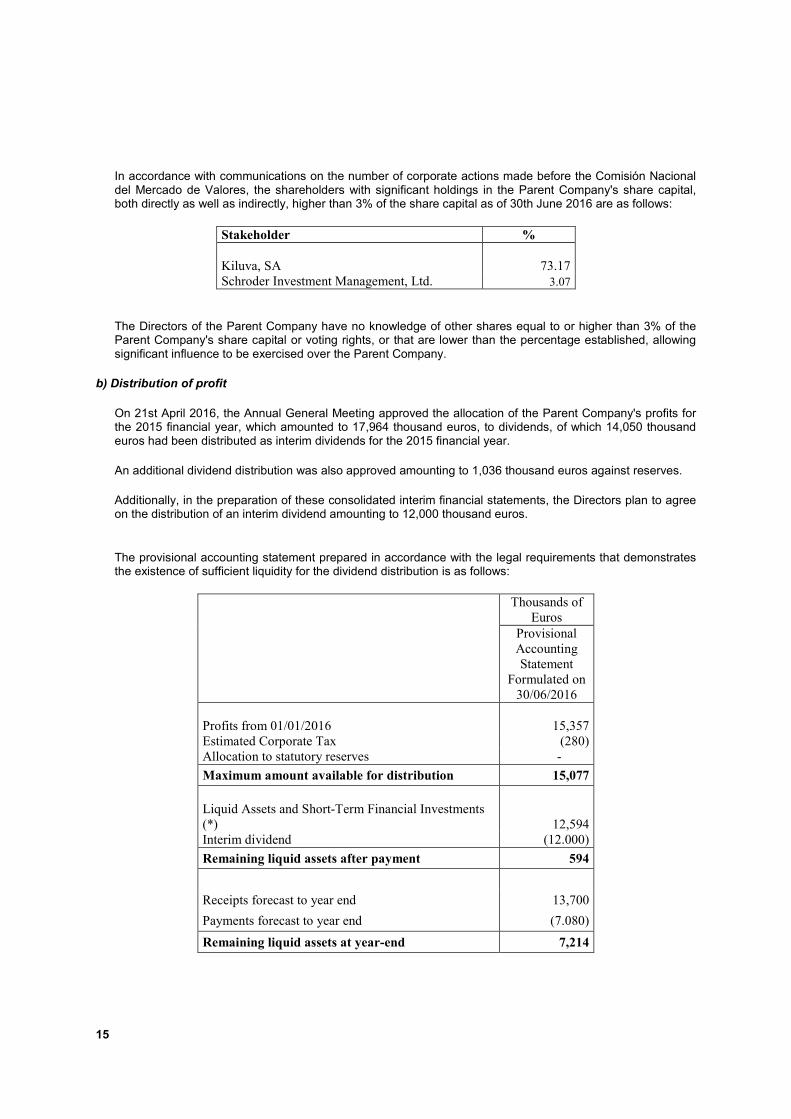

In accordance with communications on the number of corporate actions made before the Comisión Nacional del Mercado de Valores, the shareholders with significant holdings in the Parent Company's share capital, both directly as well as indirectly, higher than 3% of the share capital as of 30th June 2016 are as follows:

Stakeholder %

Kiluva, SA 73.17

Schroder Investment Management, Ltd. 3.07

The Directors of the Parent Company have no knowledge of other shares equal to or higher than 3% of the Parent Company's share capital or voting rights, or that are lower than the percentage established, allowing significant influence to be exercised over the Parent Company.

b) Distribution of profit

On 21st April 2016, the Annual General Meeting approved the allocation of the Parent Company's profits for the 2015 financial year, which amounted to 17,964 thousand euros, to dividends, of which 14,050 thousand euros had been distributed as interim dividends for the 2015 financial year.

An additional dividend distribution was also approved amounting to 1,036 thousand euros against reserves.

Additionally, in the preparation of these consolidated interim financial statements, the Directors plan to agree on the distribution of an interim dividend amounting to 12,000 thousand euros.

The provisional accounting statement prepared in accordance with the legal requirements that demonstrates

the existence of sufficient liquidity for the dividend distribution is as follows:

Thousands of

Euros

Provisional

Accounting

Statement

Formulated on

30/06/2016

Profits from 01/01/2016 15,357

Estimated Corporate Tax (280)

Allocation to statutory reserves -

Maximum amount available for distribution 15,077

Liquid Assets and Short-Term Financial Investments

(*) 12,594

Interim dividend (12.000)

Remaining liquid assets after payment 594

Receipts forecast to year end 13,700

Payments forecast to year end (7.080)

Remaining liquid assets at year-end 7,214

16

The previous provisional accounting statement was drawn up based on the Parent Company's figures and on the current forecast for receipts and payments thereof. However, the Group has freely available liquid assets and other cash equivalents amounting to a total of 28,600 thousand euros at 30th June 2016.

c) Own Shares

As of the end of the first half of 2016, the Parent Company held own shares in accordance with the following breakdown:

Year Number of

shares

Nominal value

(euros)

Average

acquisition price

(euros)

Total acquisition

cost (thousands

of euros)

2016 64,203 3,210 3.9 249

As of 30th June 2016, the Parent Company's shares held by it represent 0.11% of the Parent Company's share capital, totalling 64,203 shares with a value of 249 thousand euros and an average purchase price of 3.9 euros per share.

The movement in own shares during the first half of 2016 has been as follows:

Number of shares 2016

Start of the financial year 52,816

Purchases 134,869

Sales (123.482)

Year end 64,203

Additionally, profits from the sale of own shares have been registered in equity for a total amount of 2 thousand euros.

d) Profit / (loss) per share

The profit or loss per share is calculated based on the profit or loss corresponding to the Parent Company's shareholders for the average number of ordinary shares outstanding during the period; the profit or loss per share as of 30th June 2016 and 30th June 2015 are as follows:

30.06.2016 30.06.2015

Number of shares 60,000,000 60,000,000

Weighted average number of shares 59,931,947 60,000,000

Parent Company's Consolidated Net Profit or Loss (thousands of euros) 13,920 13,284

Number of own shares 64,203 -

Profit /(loss) per share (in Euros per share)

- Basic 0.23 0.22

- Diluted 0.23 0.22

There are no financial instruments that could dilute the earnings or loss per share.

17

e) Net equity attributable to minority interests

The balance under this heading on the attached consolidated abridged interim statement of financial position as of 30th June 2016 includes the value of the minority shareholders' share in the consolidated companies. In addition, the balance shown on the attached consolidated abridged interim profit and loss account in "Profit or loss attributable to third party shareholders" represents the share of such minority shareholders in the consolidated abridged interim profit or loss.

The breakdown on the interests of third party shareholders in companies that are consolidated by the full integration method in which ownership is shared with third parties is as follows:

Thousands of Euros

30.06.2016 31.12.2015

Zamodiet México, S.A de C.V. 56 161

Total 56 161

9. Financial debt

The composition of debts with credit institutions as of 30th June 2016 and 31st December 2015 on the attached consolidated abridged interim statement of financial position as of 30th June 2016 is as follows, according to maturity:

June 30, 2016 – Thousands of Euros

Amount Maturity

Initial Current Current

or Limit

current Total

Amounts owed to credit institutions:

Loans 6,000 272 - 272

Financial leases - 13 24 37

Subtotal of debts to credit

institutions

6,000

Other financial liabilities - 44 3,069 3,113

TOTAL 6,000 329 3,093 3,422

December 31, 2015 – Thousands of Euros

Amount Maturity

Initial Current Current

or Limit

current Total

Amounts owed to credit institutions:

Loans 12,000 1,885 - 1,885

Financial leases - 45 85 130

Subtotal of debts to credit

institutions 12,000 1,930 85 2,015

Other financial liabilities - 30 2,845 2,875

TOTAL 12,000 1,960 2,930 4,890

18

Amounts owed to credit institutions

The Group has several loans granted by different credit institutions in which both Kiluva, S.A. (Majority Shareholder) as well as the companies related thereto Finverki, S.L.U. and Tartales, S.L.U. act as guarantors. There are no additional guarantees in relation to such loans.

The decrease in debt with credit institutions as of 30th June 2016 basically corresponds to the payment of the instalments for the first half of 2016.

Other financial liabilities Included under the heading "Other non-current financial liabilities" are the amounts given as surety by franchisees of S.A.S Naturhouse (France) to guarantee compliance with its contractual obligations. Naturhouse (France) in guaranteeing compliance with its contractual obligations. In the other Group companies such guarantees are obtained by bank guarantees. As of 30th June 2016 and 31st December 2015, these guarantee deposits are valued at amortized cost.

10. Income tax

10.1 Deferred tax assets

The breakdown of deferred tax assets as of 30th June 2015 and 31st December 2014 is as follows:

Thousands of Euros

30.06.2016 31.12.2015

Temporary differences (prepaid taxes):

Tax effect of the consolidation adjustments 144 198

70% depreciation limit 113 119

Tax-loss carryforwards 251 -

Others 1 52

Total deferred tax assets 509 369 During the first half of 2016, the Parent Company recorded on the attached consolidated statement of financial position deferred tax assets for negative tax bases from the 2012 financial year amounting to 502 thousand euros as the Directors consider their future set-off probable given that it is no longer in the Kiluva S.A. tax consolidation group. The attached consolidated abridged interim profit and loss account includes this positive impact under "Corporate Tax". In addition, as of 30th June 2016, the Parent Company has considered the set-off of such tax credits amounting to 251 thousand euros (share) in the estimate of the Corporate Tax payable for the period ending 30th June 2016. 10.2 Deferred tax liabilities

The heading "Deferred tax liabilities" in the liability figures for the attached consolidated abridged statement of financial position is composed of the following, as of 30th June 2016 and 31st December 2015:

Thousands of Euros

30.06.2016 31.12.2015

Temporary differences (deferred taxes):

Financial leases 332 362

Others 65 116

Total deferred tax liabilities 397 478

19

10.3 Years pending approval and auditing actions

The interim statements and income to tax account are made regularly and based on the book record transactions, but are not considered definitive until the tax authorities have inspected them or the statute of limitation has lapsed, which in Spain is five years for Corporation Tax and four years for other applicable taxes. The companies making up the Group do not currently have any ongoing tax inspections relating to tax for the last five financial years, except for the French subsidiary for which, during the 2016 financial year, the French tax authorities launched an inspection regarding the tax corresponding to the 2013, 2014 and 2015 financial years. To date, it has received notice of a proposed penalty and interest amounting to 64 thousand euros. Additionally, the following inspection was finalised during the 2016 financial year:

- Tax inspection for the 2013 financial year of the Italian subsidiary, giving rise to assessments amounting to 409 thousand euros. Specifically, 299 thousand euros as adjustments to the tax base for the financial years inspected, 90 thousand euros as a penalty and 20 thousand euros for interest on arrears. These amounts have been recorded on the attached consolidated abridged interim profit and loss account according to their nature.

It is not expected that additional liabilities will be accrued for the Group as a result of the upcoming years pending tax inspections. The directors of the Parent Company consider that said taxes have been appropriately settled, so that even in the case of discrepancies in the interpretation of standards in effect for tax treatment afforded to the transactions, the contingent liabilities, should they arise, would not significantly affect the consolidated financial statements attached.

11. Income and expenses

a) Personnel Expenses

The composition of Personnel Expenses in the attached consolidated abridged interim profit and loss account is as follows:

Thousands of Euros

30.06.2016 30.06.2015

Wages, salaries and similar

expense 7,237 7,027

Severance indemnities 107 174

Social security contributions 2,195 2,075

Total 9,539 9,276

20

The average number of people employed by Group companies, distributed by professional category and gender, was as follows:

Average number of employees

Professional category First half of 2016 First half of 2015

Senior Management 8 8

Rest of Senior Staff 21 18

Administrative and technical staff 83 89

Commercial, sales' staff and operators 359 309

Total 471 424

In addition, the gender distribution at the end of the first half of 2016 and 2015, detailed by category, is as follows:

Number of employees

30.06.2016

Professional category Men Women Total

Senior Management 7 1 8

Rest of Senior Staff 4 15 19

Administrative and technical staff 21 55 76

Commercial, sales' staff and operators 40 346 386

Total 72 417 489

Number of employees

30.06.2015

Professional category Men Women Total

Senior Management 7 1 8

Rest of Senior Staff 6 9 15

Administrative and technical staff 29 66 95

Commercial, sales' staff and operators 42 280 322

Total 84 356 440

21

b) Financial income

The breakdown of financial income during the first half of 2016 and 2015, broken down by the nature thereof, is as follows:

Thousands of Euros

30/06/2016 30/06/2015

Financial income

Securities and other financial instruments

In related companies (Note 14) - 1

In third parties 31 17

Financial expenses

Debts with third parties (76) (230)

Exchange differences (16) (12)

Financial Result (61) (224)

12. Segment information

As the Group operates in different countries, the information has been grouped by geographical areas.

The information for the consolidated abridged interim profit and loss account for the first half of 2016 and 2015, broken down by segment, is as follows:

Thousands of Euros

Sectors Total

Spain France Italy Poland Other countries Other and eliminations

30.06.2016 30.06.2015 30.06.2016 30.06.2015 30.06.2016 30.06.2015 30.06.2016 30.06.2015 30.06.2016 30.06.2015 30.06.2016 30.06.2015 30.06.2016 30.06.2015

External Sales 11,087 10,870 22,629 22,186 12,566 12,054 6,844 6,030 1,377 1,416 - - 54,503 52,556

Sales between sectors 2,682 2,253 175 217 5 - 21 13 - 114 (2.883) (2.597) - -

Other operating income 80 50 124 101 78 166 77 41 57 13 (62) - 354 371

Total revenues 13,849 13,173 22,928 22,504 12,649 12,220 6,942 6,084 1,434 1,543 (2.945) (2.597) 54,857 52,927

Supplies (3.796) (3.658) (6.705) (6.639) (3.636) (3.568) (2.899) (2.458) (481) (515) 1,533 1,367 (15.984) (15.471)

Personnel (3.337) (3.158) (2.389) (2.711) (2.672) (2.416) (626) (584) (515) (407) - - (9.539) (9.276)

Amortization (276) (335) (73) (73) (170) (148) (53) (67) (40) (64) 74 85 (538) (602)

Other operating costs (3.092) (3.062) (3.634) (3.245) (2.465) (2.314) (1.104) (875) (520) (549) 1,412 1,230 (9.403) (8.815)

Impairment losses and income

from disposal of fixed assets (183) (36) - 12 - - - 18 - (16) - - (183) (22)

Operating results 3,165 2,924 10,127 9,848 3,706 3,774 2,260 2,118 (122) (8) 74 85 19,210 18,741

Financial Result - - - - - - - - - - (61) (224) (61) (224)

Participation in benefit from

equity-accounted companies - - - - - - - - - - 528 579 528 579

Profit / (loss) before tax 3,165 2,924 10,127 9,848 3,706 3,774 2,260 2,118 (122) (8) 541 440 19,677 19,096

The segment "Other and eliminations" includes consolidation eliminations and financial income and expenses considered as corporate not assignable to any particular segment. There has been no distribution of revenue and general expenses between segments.

The breakdown by segment of certain items on the consolidated statement of financial position as of 30th June 2016 and 31st December 2015 is as follows:

Thousands of Euros

Sectors Total

Spain France Italy Poland Other countries Other and eliminations

30.06.2016 31.12.2015 30.06.2016 31.12.2015 30.06.2016 31.12.2015 30.06.2016 31.12.2015 30.06.2016 31.12.2015 30.06.2016 31.12.2015 30.06.2016 31.12.2015

ASSETS

Intangible Assets 1,953 2,085 12 12 76 76 - 1 24 19 - - 2,065 2,193

Tangible fixed assets 2,376 2,671 634 556 783 737 106 45 975 1,016 - - 4,874 5,025

Total assets 16,615 9,983 15,377 14,757 9,337 5,521 4,321 4,957 2,812 3,121 3,477 3,032 51,939 41,371

Total liabilities 5,126 3,954 5,487 4,994 5,087 3,293 1,264 1,164 449 522 3,780 5,428 21,193 19,355

The segment "Other and eliminations" includes assets and liabilities considered as corporate and not attributable to any particular segment, basically corresponds to "Investments in associated companies", "Investments in related companies" and "Current financial assets" and to "Non-Current Liabilities" and " Current liabilities ", respectively, as well as consolidation eliminations.

Other segment information

None of the Group's customers accounts for over 10% of revenues from ordinary activities.

During the first half of the 2016 financial year, there have been no significant additions of fixed assets.

24

13. Provisions and contingencies

a) Non-current provisions

The balance of other non-current provisions mainly refers to a commitment that the Group has with certain employees of the company Naturhouse S.R.L. amounting to 772 thousand euros as of 30th June 2016 (686 thousand euros as of 31st December 2015). The balance of other non-current provisions refers basically to a commitment between the Group and certain employees of the Italian company Naturhouse S.R.L This TFR commitment (end-of-contract severance pay), payable at the time of termination of the employment relationship, regardless of whether the termination is voluntary or not. As of 1st January 2007, with the regulatory change in Italy, the reserve established for the TFR to 31st December 2006 has remain in the Company, revalued with the parameters of Law 297/82 and the subsequent retention of each employee paid to INPS (the Italian state agency for social security). This commitment is not externalised and the expenses thereof are recorded under "Personnel Expenses" on the consolidated profit and loss account.

The remaining non-current provisions registered correspond to obligations and risks that the Group keeps provisioned due to considering them to be probable.

b) Contingencies

The Directors of the Parent Company consider that there are no contingencies that could lead to unregistered liabilities or that could have a significant impact on the attached consolidated abridged interim financial statements.

14. Transactions and balances with related parties

Transactions between the Parent Company and its subsidiaries have been eliminated in the consolidation process and are not broken down in this note.

Transactions between the Group and its related companies are broken down below:

Balances with affiliate companies

Thousands of Euros

Debit balances Credit balances

Company 30.06.2016 31.12.2015 30.06.2016 31.12.2015

Current financial balances

Ichem, Sp. Zo.o. 562 - - -

Kiluva, SA - - 1,445 1,445

Total short-term financial balances 562 - 1,445 1,445

Current trade balances

Gartabo, SA 1 1 - -

Girofibra, SL - - 240 197

House Health Sun, SL - 16 2 -

Ichem, Sp. Zo.o. - 4 4,677 3,596

Indusen, SA - - 1,104 427

Kiluva, SA - - - 30

Laboratorios Abad, S.L.U. - - 31 12

U.D. Logroñés, SAD - - - 100

Zamodiet, S.A. - - 9 62

Total short-term commercial balances 1 21 6,063 4,424

Total balances with related companies 563 21 7,508 5,869

25

Transactions with related companies

During the first half of 2016 and 2015, Group companies conducted the following transactions with related companies that are not part of the Group:

Thousands of Euros

Company 30.06.2016 30.06.2015

Sales

Gartabo, SA 2 30

House Health Sun, SL 5 5

Ichem, Sp. Zo.o. - 58

Laboratorios Abat, S.L.U. 2 11

Services provided

Kiluva, SA - 161

Total revenues 9 265

Purchases

Girofibra, SL 716 727

House Health Sun, SL - 36

Ichem, Sp. Zo.o. 10,106 9,432

Indusen, SA 2,351 2,059

Laboratorios Abad, S.L.U. 115 78

Zamodiet, S.A. - 164

Services received

Girofibra, SL 2 2

Ichem, Sp. Zo.o. - 15

House Health Sun, SL 55 69

U.D. Logroñés, S.A.D. 131 65

Luair, S.L.U. (Directly and indirectly) 188 16

Leases

Tartales, SLU 153 205

Total operating expenses 13,817 12,868

Financial income

Kiluva, SA - 1

Total financial revenues - 1

In addition, consideration should be given to the dividend distributions described in Note 8.b

Finally, there are transactions with a company related to a member of the Parent Company's Board of Directors amounting to 31 thousand euros (68 thousand euros in the 2015 financial year).

The Company's Directors and its tax advisers believe that the transfer prices are properly accounted for, consequently, they believe that there are no significant risks in this regard that could lead to significant liabilities in the future.

26

The transactions and balances between the Group and other related parties (Directors and Management) are broken down in Note 15.

15. Information on Directors and Management

Remuneration and commitments to Directors

During the first semester 2016 the Directors of the Parent Company accrued compensation in fixed allowance and fees for attending meetings of the Board of Directors amounting to 123 thousand Euros (123 thousand Euros during the first semester 2015). Additionally, they have received remuneration indicated in the following paragraph for the development of their executive positions. The Directors do not hold any advances or loans with the Group as of 30th June 2016 (80 thousand euros of advances as of 31st December 2015). Finally, as of 30th June 2016 and 31st December 2015, there are no guarantees granted or other commitments in terms of pensions or life insurance policies with the Directors.

The remuneration received by the Group's Senior Executives during the first half of the 2016 financial year for salaries and wages and provision of services amounted to 1,849 thousand euros (1,980 thousand euros in the first half of 2015). Of this amount, 975 thousand euros were received by members of the Board of Directors in the development of their executive positions (1,114 thousand euros in the first half of 2015). The Senior Management of the Group has received no remuneration for other services.

At the end of the period ending 30th June 2016 and of the 2015 financial year, the Senior Management body is made up of the following persons:

30.06.2016 31.12.2015

Categories Men Women Men Women

Senior

Management 7 1 7 1

There are no advances or loans granted to Senior Management, or pensions or life insurance commitments, as of the end of the period ending 30th June 2016.

Information relating to conflicts of interest by the Directors

As of the end of the six-month period ending 30th June 2016, neither the members of the Board of Naturhouse Health, S.A. nor any persons related to them as defined by Spanish Corporate Law, have communicated to the other members of the Board of Directors any situation involving direct or indirect conflict that they or persons related to them, as defined by Spanish Corporate Law, may have with the Company's interests.

16. Subsequent events

There have been no significant events after the close of 30th June 2016 and before the preparation of these consolidated abridged interim financial statements for the first half of the 2016 financial year. Barcelona, 22nd July 2016 Board of Directors

27

Management Report

Consolidated abridged interim financial statements

First half of the 2016 financial year

INDEX

1. Situation and Business Development

2. Evolution of the main figures of the consolidated profit and loss account

3. Consolidated Statement of Financial Position

4. Financial risk management and use of hedging instruments

5. Risk Factors

6. R + D + i activities

7. Treasury Shares

8. Subsequent events

9. Capital structure and significant shareholdings

10. Shareholder agreements and restrictions on transferability and vote

11. Administrative Body, Board

12. Significant agreements

28

1. Situation and Business Development

Naturhouse Group is a business group dedicated to the dietetic and nutrition sector with its own exclusive business model based on the Naturhouse method. At first semester-end (2016) it had an active presence in 32 countries through a network of 2,214 centres, with France, Italy, Spain and Poland being its most important markets.

The companies included in the consolidation by full integration in the first half of 2016 are as follows: Naturhouse Health S.A. (Spain), S.A.S. Naturhouse (France), Housediet S.A.R.L. (France), Naturhouse S.R.L. (Italy), Naturhouse Sp Zo.o (Poland), Kiluva Portuguesa - Nutriçao e Dietética, Ltd (Portugal), Naturhouse Belgium S.P.R.L. (Belgium), Naturhouse Franchising Co, Ltd (United Kingdom), Naturhouse, Gmbh (Germany), Zamodiet México S.A. de C.V. (Mexico), Nutrition Naturhouse Inc. (Canada), Naturhouse d.o.o. (Croatia), UAB Naturhouse (Lithuania) and Naturhouse Inc. (USA).

The first semester (2016) is marked by the marketing effort aimed at consolidating existing markets, especially in Europe, and the opening of new international geographic markets.

On 16th January 2016, there was a capital increase in the Mexican company of the Naturhouse Group, Zamodiet

de México S.A. de C.V., consequently, the Naturhouse Health S.A. stake has risen from 51% to 78.73%.

On 25th February 2016, the Board of Directors proposed the allocation of the Parent Company's profits for the 2015 financial year, which amounted to 17,964 thousand euros, to dividends, of which 14,050 thousand euros had been distributed as interim dividends for the 2015 financial year. An additional dividend distribution was also approved amounting to 1,036 thousand euros against reserves.

The Annual General Meeting was held on 21st April 2016, approving the following;

- Consolidated Financial Statements (Consolidated Balance Sheet, Consolidated Profit and Loss Account, Consolidated Statement of Comprehensive Income, Consolidated Statement of Changes in Equity, Consolidated Statement of Cash Flows and Consolidated Explanatory Notes and the Consolidated Management Report for the Consolidated Naturhouse Health, S.A. Group and subsidiaries for the financial year ending 31st December 2015.

- The proposed distribution of profit and management of the Naturhouse Health, S.A. Board of Directors for the 2015 financial year.

- Remuneration of the company's Board of Directors.

4.1 Advisory vote on the Annual Report on Remuneration of Naturhouse Health, S.A. Board Directors for the 2015 financial year.

4.2 Approval of the remuneration policy for Naturhouse Health, S.A. Board Directors for the 2016 financial year.

4.3 Approval of the remuneration for the Naturhouse Health, S.A. Board of Directors for the 2016 financial year.

- Amendment to the Naturhouse Health, S.A. Articles of Association to adapt them to the latest legislative reforms introduced by Law 9/2015 of 25th May on Urgent Measures in Bankruptcy, Law 15/2015 of 2nd July on Voluntary jurisdiction and Law 22/2015 of 20th July on Account Audits, which amend the Spanish Corporate Law. Specifically, the amendments proposed are as follows:

5.1 Amendment of section 2 of Article 3 of the Articles of Association, to adapt them to Law 9/2015 of 25th May on Urgent Measures in Bankruptcy.

5.2 Amendment of section 6 of Article 21 of the Articles of Association, to adapt them to Law 15/2015 of 2nd July on Voluntary Jurisdiction.

5.3 Amendment of Article 41.1 of the Articles of Association, to adapt them to Law 22/2015 of 20th July on Account Audits.

29

- Amendment of section 4 of Article 6 of the Regulations of the Annual General Meeting following the amendment of Article 21 of the Articles of Association mentioned in paragraph 5.2 above.

- Advisory vote on the amendment of Article 14.1 of the Regulations of the Company's Board of Directors, to adapt them to the aforementioned statutory reforms.

- Delegation to the Board of Directors, for a period of 5 years, of the power to increase the share capital at any time, once or several times, without such increases being higher in any case than half of the company's share capital at the time of authorisation, for the amount and under the conditions determined by the Board of Directors in each case, granting the power to exclude all or part of the preferential subscription right and with express authorisation to redraft Article 5 of the Articles of Association, if necessary, and to request admission, retention and/or exclusion of shares on the organised secondary markets, if necessary.

- Authorisation to the Board of Directors for the direct and indirect acquisition of own shares, under the legal limits and requirements. Authorisation for the disposal and amortisation of the same and authorisation to the Board of Directors for the application and enforcement of the agreements in accordance with the provisions of Article 146 of Spanish Corporate Law.

- Delegation of powers to supplement, develop, execute, remedy and

formalise the resolutions adopted by the General Meeting.

On 4th May 2016, the payment of dividends was made for the 2015 financial year, amounting to 4,949 thousand euros.

During the first half of 2016, three new agreements for master franchises in countries in which Naturhouse was not present, Malta, Hungary and India, were signed.

2. Evolution of the main figures of the consolidated profit and loss account

Consolidated Profit and Loss Account

30 June 30 June

(Thousands of Euros) 2016 2015

Net amount of revenue 54,503 52,556 Supplies (15.984) (15.471)

Gross Margin 38,519 37,085

Other operating income 354 371 Personnel costs (9.539) (9.276) Other operating costs (9.403) (8.815)

Operating income before depreciation and amortization, impairment and other results

19,931 19,365

Depreciation and amortization (538) (602) Impairment losses and income from disposal of fixed assets (183) (22)

OPERATING INCOME 19,210 18,741

Financial Result (61) (224)

Results of equity method associated companies 528 579

CONSOLIDATED PROFIT BEFORE TAX 19,677 19,096

Corporation Tax (5.764) (5.872)

NET INCOME FROM CONTINUING OPERATIONS 13,913 13,224

CONSOLIDATED NET INCOME 13,913 13,224

30.06.2016 30.06.2015

Average number of employees 471 424

Gross Margin without Sales 71% 71%

Operating Income without Sales 35% 36%

Net Income without Sales 26% 25%

30

• The net turnover is composed of two main aspects:

1. Sale of goods

Corresponds to the sale of products through the Naturhouse channel (either through franchising, master

franchising or centres of our property). Represents the bulk of revenues with 98,87% during the first

semester of 2016.

2. Provision of services

a. €600 annual fee paid by each franchise to subsidiaries of the Group. This represents 1.09% of net

turnover for the first half of 2016.

b. Master franchise fee: corresponds to the entry fee that the Group bills to the masters franchisees

for the operation of the business in an exclusively new country. This fee is charged in advance in

the first year of operation of the business and entitles the exploitation of the Naturhouse channel

for 7 years. The amount of the fee varies according to the estimated potential number of

Naturhouse centres in that country. During the first half of 2016, three new master franchise

agreements (Malta, Hungary and India) were signed. This represents 0.04% of net turnover for the

first half of 2016.

• Net turnover in the first half of 2016 amounted to 54,503 thousand euros, representing an increase of 3.70%

over the previous year. This variation mainly includes the following effects:

o In France sales are 22,629 thousand Euros. In the first half of 2015, there was 22,186 thousand

euros, as a result of the net opening of 28 centres during the first half of 2016.

o In Spain sales are 11,087 thousand Euros. In the first half of 2015, there was 10,870 thousand

euros, an increase of 2%. Despite having six centres less than at the end of 2015, we can observe

recovery in the market, which we hope will be consolidated over the coming quarters.

o In Italy sales are 12,566 thousand Euros. In the first half of 2015, there was 12,054 thousand

euros, an increase of 4.20%. It should be noted that in the first half of 2016, there has been an

increase in net opening of 10 centres.

o Increased sales in Poland of 814 thousand euros (+13.15%) to 6,844 thousand euros, arising from

the good performance of Naturhouse in Eastern Europe and the net opening of 44 centres during

the first half of 2016.

• The gross margin on net turnover remains at 71%.

• "Other operating income" corresponds to revenue from activities outside of the Naturhouse business.

• During the first semester of 2016 there is an average workforce of 471 employees in the Group, of which 76%

are direct employees of the Naturhouse centres under self-management and commercial offices that control

the smooth running of all the centres, both franchises and the Group's own centres, and the remaining 24% of

staff corresponds to general management, administration and accounting, logistics, marketing and technical

staff.

Personnel Expenses represents 18% of net revenues.

• Other Operating Expenses has increased by 6.67% over the first half of 2015, mainly due to:

o Increased leasing costs; arising from the group's strategy of moving into shopping centres.

o Expenses incurred by the Group being listed on the Stock Exchange, as well as by holding the

Annual General Meeting last April.

• The operating result on turnover reduced by one percentage point, from 36% to 35%, as a result of the 3

subsidiaries established in 2015, Croatia, Italy and USA, which had a negative contribution to the operating

result.

31

• As a result of the 24.9% stake of the company Ichem Sp Z.o.o, in the first half of 2016, 528 thousand euros is

registered in the "Share in profits from equity accounted companies" in the attached abridged profit and loss

account.

• The net result on turnover rose by one percentage point, from 25% to 26%, over the first half of 2015 as a

result of the reduction in financial expenses and in the various income taxes applicable to Naturhouse Group

companies.

32

3. Consolidated Statement of Financial Position

ASSET

(Thousands of Euros) 30.06.2016 31.12.2015

NON-CURRENT ASSETS: Intangible fixed assets 2,065 2,193

Tangible fixed assets 4,874 5,025

Non-current financial assets Investments in associates

832 2,983

813 3,140

Deferred tax assets 509 369

Non-current assets 11,263 11,540

CURRENT ASSETS:

Inventory 3,657 3,541

Customer receivables for sales and services 6,801 4,952

Customers, related companies 1 21

Current tax assets and other receivables

with public administrations 233 569

Other current assets 780 876

Current financial assets 604 42

Cash and cash equivalents 28,600 19,830

Total current assets 40,676 29,831

Total assets 51,939 41,371

LIABILITIES

(Thousands of Euros) 30.06.2016 30.12.2015

NET EQUITY:

Capital and reserves

Subscribed capital 3,000 3,000

Issue premium 2,149 2,149 Premium 12,176 8,225

Own shares and company shares (249) (214) Conversion differences (306) (115)

Results of the year 13,920 22,860 Interim dividend (14.050)

NET EQUITY ATTRIBUTABLE TO MEMBERS OF THE PARENT COMPANY 30,690 21,855

NET EQUITY ATTRIBUTABLE TO MINORITY INTERESTS 56 161

Total net equity 30,746 22,016

NON-CURRENT LIABILITIES: Non-current provisions 1,108 1,044

Non-current liabilities 3,093 2,930

Deferred tax liabilities 397 478

Non-current liabilities 4,598 4,452

CURRENT LIABILITIES:

Current liabilities 329 1,960

Financial liabilities with related parties 1,445 1,445

Trade creditors and other receivables 5,313 4,776 Suppliers, related companies 6,063 4,776

Current tax liabilities and other payables

with public administrations 3,445 2,298

Total current liabilities 16,595 14,903

TOTAL NET EQUITY AND LIABILITIES 51,939 41,371

• The reduction of 157 thousand euros in the "Investments in associates" is as a result of the share in profits

from the company Ichem Sp. Zo.o, the balance resulting from the distribution of dividends for the 2015

financial year and the contribution from profits for the first half of 2016.

33

• In the first half of 2016, the Group's current and non-current financial debt was reduced to 1,468 thousand

euros (-30%). The Group has reduced its financial debt in recent years and will continue in this line. The

Company does not anticipate significant investments that require significant funding to banks.

4. Financial risk management and use of hedging instruments

The Group's activities are exposed to various financial risks: market risk (including foreign exchange and interest rate risk), credit risk, liquidity risk and interest rate risk on cash flows. Market risk in the interest rate and the exchange rate:

The Group's operating activities are largely independent with respect to changes in market interest rates. The interest rate risk of the Group arises from long-term borrowings. At June 30, 2016, 100% of the borrowings was at a variable interest rate. However, the Group has not considered it necessary to cover such interest rate fluctuations because the external financing of the Group is unimportant, so it has not contracted hedging instruments during the years in question Regarding the exchange rate risk, the Group does not operate internationally outside the Euro Currency to any great extent, so its exposure to exchange rate risk on foreign currency operations is not significant. Credit risk

In general the Group maintains its cash and equivalent liquid assets at banks with high credit ratings. It also performs adequate monitoring of accounts receivable individually, in order to determine situations of potential insolvency. The Group's credit risk is primarily attributable to its trade receivables. There is no significant concentration of credit risk, with exposure spread over a large number of customers, markets and geographic areas. Liquidity risk>

In order to ensure liquidity and be able to meet all payment obligations arising from its activities, the Group has abundant credit lines and financing with credit institutions. It has maintained a proactive policy on the management of liquidity risk, focusing primarily on the preservation of same, maintaining sufficient cash and marketable securities, the availability of funding through an adequate amount of credit facilities and the ability to liquidate market positions.

5. Risk Factors

The activities of the companies of the Group are developed in different countries with different socio-economic environments and regulatory frameworks. The authorities of the countries where the Group operates may adopt laws and regulations that impose new obligations which entail an increase in operating costs. Negative impact due to the difficult economic situation in Europe. The deep financial and consumer crisis has affected the opening of new franchises, the scarce funding provided by financial institutions, and final consumer purchases, inter alia, due to the difficult macroeconomic situation and high rates of unemployment. Although such adjustment is still present in some countries in which the Naturhouse Group operates, in the first half, indicators of improvement can be observed in several European countries, aiding the opening of new franchises. The competitive environment. The company competes with self-administered weight loss schemes and other commercial programmes from other competitors, along with other suppliers and food retailers that operate in this market. This competition and any future increases in same involving the development of pharmaceuticals and other technological and scientific advances in the field of weight loss could have a negative impact on the business, operating results and financial position of the Group.

34

6. R + D + i activities

The method used by the Group in relation to research and development of new products is as follows: It is in the commercial, technical and marketing department where the initial need to consider extending the range of products that Naturhouse offers arises, or simply modify one of the existing offers. This need is transferred to one or more of our current suppliers, according to the product format (sachets, vials or capsules). Suppliers develop and submit proposals according to our needs, and if these are covered from a commercial, technical and economic point of view, we proceed to launch the new product or format. Therefore the Group does not generate increased costs in R + D + i in the registration of the brand and the formula in the corresponding department for health. The main supplier of the Group is the Polish company Ichem Sp. Zo.o, accounting for 63% of total purchases consolidated to June 30, 2016. The Group holds 24.9% of its capital. The benefits sought with this holding are:

1. Faster launching of new products, sharing know-how in R & D

2. Ensure supply and reduce dependence on third party manufacturers outside the Group

3. Ensure product quality while maintaining high levels of competitiveness

By doing this Naturhouse is able to differentiate itself from its competitors because it is present throughout the entire value chain of the nutritional supplement industry, from R & D and product manufacturing to the final sale and client consultation.

Due to Ichem, the Group has a link with two other major groups of suppliers, the suppliers in which Kiluva S.A., the main shareholder of Naturhouse Health, S.A., holds shares (Indusen, S.A., Girofibra, S.L., Laboratorios Abad, S.L.U. and Zamodiet, S.A.), and which represent approximately 20% of total purchases in the first half of 2016, and suppliers that are unrelated to Naturhouse Health, S.A. or Kiluva S.A., which represent 17% of total purchases in the first half of 2016.

7. Treasury Shares

As of 30th June 2016, the Parent Company holds a total of 64,203 treasury shares. No affiliate company owns any shares or holdings of the Parent Company.

8. Subsequent events

There have been no significant subsequent events after the close of 30th June 2016 and the formulation of the

consolidated abridged interim financial statements.

9. Capital structure and significant shareholdings

At June 30, 2016, the Naturhouse Group has no restriction on the use of capital resources that, directly or indirectly, have affected or may significantly affect the operations, except those that are legally established. As of 30th June 2016, the share capital is represented by 60,000,000 shares. The Group's main shareholders are Kiluva, S.A. with a 73.17% stake and Schroder Investment Management Ltd. with 3.07%.

10. Shareholder agreements and restrictions on transferability and vote

There is no shareholders agreement or statutory restrictions on the free transferability of the shares of the Parent Company and there are no statutory restrictions or regulatory restrictions on voting rights.

35

11. Administrative Body, Board

The Parent Company's administrative body is made up of a Board of Directors composed of 8 members, Mr Félix Revuelta Fernández, Mr Kilian Revuelta Rodríguez, Ms Vanesa Revuelta Rodríguez, Mr Rafael Moreno Barquero, Mr José María Castellanos, Ms Isabel Tocino Biscarolasaga, Mr Pedro Nueno Iniesta and Mr Juan María Nin Génova.

12. Significant agreements

No significant agreements are recorded in terms of changes in the control of the Parent Company or between the Parent Company and its Manager and Directors or employees concerning compensation for resignation or dismissal. Barcelona, 22nd July 2016 Board of Directors

36

ANNEX I Companies included in the consolidation

As of 30th June 2016, the subsidiaries consolidated by full integration and by the equity method and the information related thereto are as follows:

37

Company Activity Holding %

Naturhouse Health S.A. Marketing of dietary products

Pasaje Pedro Rodríguez, 6 medicinal herbs and natural cosmetics

08028 Barcelona (Spain)

Housediet S.A.R.L. Marketing of dietary products 100%

75 rue Beaubourg medicinal herbs and natural cosmetics

75003 Paris (France)

Kiluva Portuguesa –Nutriçao e Dietetica, Lda Processing and marketing 100%

Avenida Dr. Luis SA, 9 9ª dietetic products

Parque Ind Montserrate Fraçao "M" Abruhneira 2710 Sintra (Portugal)

Ichem Sp. Zo.o (*) Production and marketing of 24.9%

ul. Dostawcza 12 dietetic products

93-231 Lodz (Poland)

Naturhouse Belgium S.P.R.L. Marketing of dietary products 100%

Rue Du Pont-Gotissart 6 medicinal herbs and natural cosmetics

Nijvel, Waals Brabant, 1400 Belgium

Naturhouse Franchising Co, Ltd Marketing of dietary products 100%

33 church road, Ashford medicinal herbs and natural cosmetics

Middlesex (Great Britain)

Naturhouse, Gmbh Marketing of dietary products 100%

Rathausplatz, 5 medicinal herbs and natural cosmetics

91052 Erlangen (Germany)

Naturhouse Inc. Marketing of dietary products 100%

1395 Brickellave 800 STE medicinal herbs and natural cosmetics

Miami FL (USA)

Naturhouse Sp. zo.o. Marketing of dietary products 100%

Ul/Dostawcza, 12 medicinal herbs and natural cosmetics

93-231 Lodz (Poland)

Naturhouse S.R.L. Marketing of dietary products 100%

Viale Panzacchi, nº 19 medicinal herbs and natural cosmetics

Bologna (Italy)

Nutririon Naturhouse Inc. Marketing of dietary products 100%

Rue de la Guachetière Ouest medicinal herbs and natural cosmetics

Montréal Québec (Canada)

Naturhouse d.o.o. Marketing of dietary products 100%

Ilica 126, medicinal herbs and natural cosmetics

Zagreb (Croatia)

S.A.S. Naturhouse Marketing of products 100%

12, Rue Philippe Lebon dietary

Zone de Jarlard, 81000 Albi, France

UAB Naturhouse Marketing of products 100%

Konstitucijos pr. 7 dietary

09308 Vilna (Lithuania)

Zamodiet México S.A. de C.V. Marketing of dietary products 79%

Boulevard Interlomas, nº 5

L4 Lomas Anahuac (Mexico)

(*) Sole company integrated with the equity-accounted method, and the rest by full consolidation.

38

FORMULATION DILIGENCE

Signature of the Directors