nation religious king 0 fiscal system for petroleum and ... - eng ratana_petroleum and...

TRANSCRIPT

The Asia Tax Forum20-22 October, 2010, Sokha Angkor Hotel

Siem Reap, Cambodia

FiscalSystemforPetroleumandMineralsinCambodia

The Kingdom of CambodiaNation Religious King

0

Presented by Mr. Eng RatanaDeputy directorDepartment of Large TaxpayersGeneral Department of Taxation

0

2

I. Overview of Cambodian Petroleum and MineralsI. Overview of Cambodian Petroleum and Minerals 1. Petroleum Resources (oil and gas) 1. Petroleum Resources (oil and gas) 2. Mineral Resources 2. Mineral ResourcesII. Fiscal Regime for Petroleum and MineralsII. Fiscal Regime for Petroleum and Minerals 1. Existing Law on Taxation (LOT) 1. Existing Law on Taxation (LOT) 2. Draft of Petroleum Tax Law 2. Draft of Petroleum Tax Law 3. Petroleum Regulation (PR) 3. Petroleum Regulation (PR) 4. Petroleum Agreement (PA) 4. Petroleum Agreement (PA)III. ChallengesIII. Challenges

OUTLINEOUTLINE

3

Cambodia may have significant of natural resources such asCambodia may have significant of natural resources such aspetroleum (oil & gas), and many different kinds of mineralpetroleum (oil & gas), and many different kinds of mineralresources including iron, coal, bauxite, copper, gold, silicaresources including iron, coal, bauxite, copper, gold, silica……etc.etc.1. Petroleum Resources (Oil & Gas):1. Petroleum Resources (Oil & Gas): CambodiaCambodia’’s petroleum industry is in the early stages;s petroleum industry is in the early stages; The The first geological surveys conducted by Chinesefirst geological surveys conducted by Chinese geologists geologists between 1958-1960; followed by geological and structural between 1958-1960; followed by geological and structural mapping mapping made by made by Polish and Russia geologists in 1960s;Polish and Russia geologists in 1960s; In In 1972-1974, Elf and 1972-1974, Elf and EssoEsso had been awarded Blocks I, III had been awarded Blocks I, III and IV in the offshore areas; and IV in the offshore areas; In 1987, Russian and Cambodian geologists conductedIn 1987, Russian and Cambodian geologists conducted geological and geophysical studies. geological and geophysical studies.

I. Overview of Cambodian Petroleum andI. Overview of Cambodian Petroleum andMineralsMinerals

4

1. Petroleum Resources ( 1. Petroleum Resources (concon’’tt):): The studies have been divided into 25The studies have been divided into 25 blocks blocks

(offshore and onshore); and 4 areas in the(offshore and onshore); and 4 areas in theOverlapping Claim Areas (OCA). The offshore is 6Overlapping Claim Areas (OCA). The offshore is 6blocks located in the Gulf of Thailand, and onshoreblocks located in the Gulf of Thailand, and onshoreconsists of 19 blocks. The four (OCA) areas are in aconsists of 19 blocks. The four (OCA) areas are in along sea border of Cambodia-Thailand;long sea border of Cambodia-Thailand;

Petroleum regulation (Petroleum regulation (PR) introduced in 1991, sincePR) introduced in 1991, sinceexploration licensing has been awarded to differentexploration licensing has been awarded to differentforeign investors;foreign investors;

So far all offshore blocks (A-F) and 2 onshore blocksSo far all offshore blocks (A-F) and 2 onshore blocks(B12 &B15) are given Exploration License Permit;(B12 &B15) are given Exploration License Permit;

Only block (A) given to Chevron is in the early stages Only block (A) given to Chevron is in the early stagesof development.of development.

I. Overview of Cambodian Petroleum andI. Overview of Cambodian Petroleum andMineralsMinerals

5

2. Mineral resources:2. Mineral resources:■ ■ CambodiaCambodia’’s mineral resources s mineral resources are also in the early stages. are also in the early stages. The geologicalThe geological studies & mineral investigations indicated significant mineral resources; studies & mineral investigations indicated significant mineral resources;■ ■ TheThe LawLaw onon MineralMineral ResourceResource ManagementManagement && ExploitationExploitation adopted inadopted in 2001;2001;■ ■ Fiscal regime is divided into non-tax and tax charges. The non-tax chargesFiscal regime is divided into non-tax and tax charges. The non-tax charges based on law & regulations issued by Ministry of Industry, Mines and based on law & regulations issued by Ministry of Industry, Mines and Energy (MIME) or inter-ministries MEF-MIME; Energy (MIME) or inter-ministries MEF-MIME;■ ■ If exploration study is successful, investors required to present a masterIf exploration study is successful, investors required to present a master project plan to CDC & MIME before granted a mining license; project plan to CDC & MIME before granted a mining license;■ ■ So far MIME has issued mineral licenses to more than 60 investors;So far MIME has issued mineral licenses to more than 60 investors;■ ■ All holding mineral license, shall pay the state fees for registration, mineralAll holding mineral license, shall pay the state fees for registration, mineral license, renewal of mineral license, right transfer, annual land rental, and license, renewal of mineral license, right transfer, annual land rental, and royalties of the values of minerals exploited; and tax on profit (LOT). royalties of the values of minerals exploited; and tax on profit (LOT).

I. Overview of Cambodian Petroleum andI. Overview of Cambodian Petroleum andMinerals (contMinerals (cont’’))

6

II. Fiscal Regime for Petroleum andII. Fiscal Regime for Petroleum andMineralsMinerals

1. Existing Law on Taxation (LOT):1. Existing Law on Taxation (LOT): LOT was adopted in 1997 and amended in 2003. There is noLOT was adopted in 1997 and amended in 2003. There is no specific rule on natural sector and the coverage of the law is very specific rule on natural sector and the coverage of the law is very

limited:limited: Tax Rate: 30% on oil and gas (PSA) and other natural resources;Tax Rate: 30% on oil and gas (PSA) and other natural resources; Used UOP for Depletion of exploration & development costs;Used UOP for Depletion of exploration & development costs; Interest attributable to exploration & development costs;Interest attributable to exploration & development costs; Taxable losses carried forward for 5 years;Taxable losses carried forward for 5 years; Import for petroleum operation are exempted only explorationImport for petroleum operation are exempted only exploration

and development stages (LOI);and development stages (LOI); VAT paid on goods & services for local supplies are refundable.VAT paid on goods & services for local supplies are refundable.

7

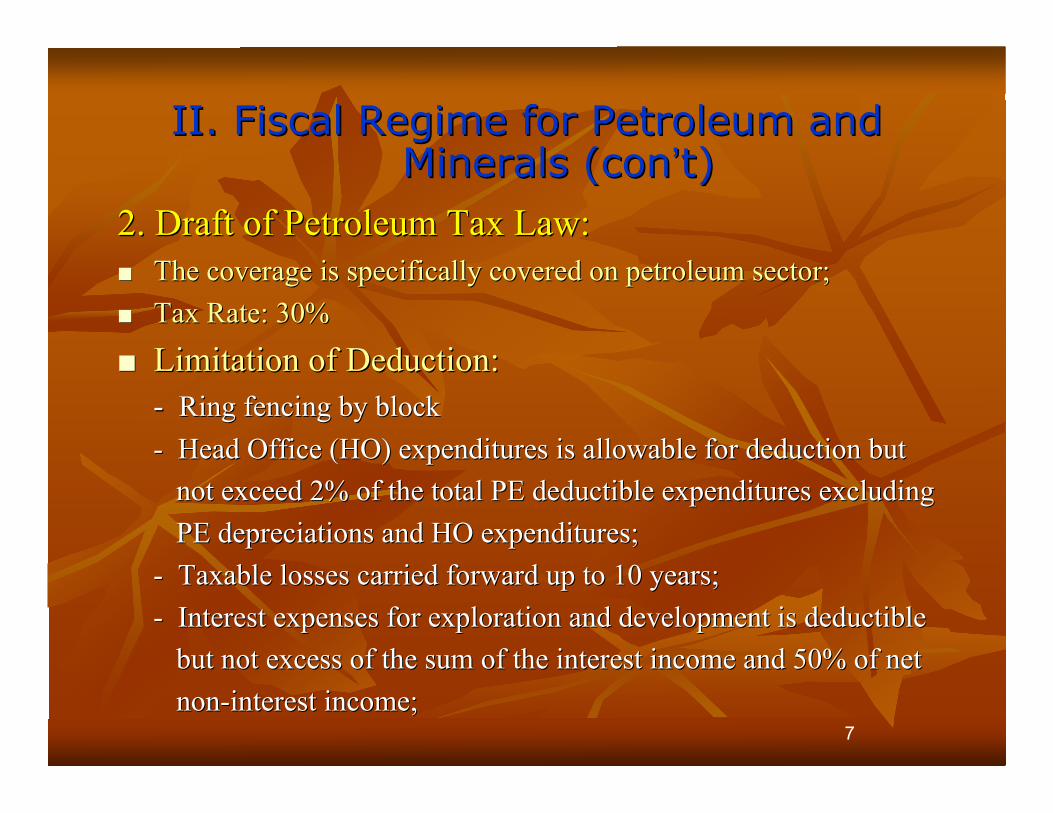

2. Draft of Petroleum Tax Law:2. Draft of Petroleum Tax Law: The coverage is specifically covered on petroleum sector;The coverage is specifically covered on petroleum sector; Tax Rate: 30%Tax Rate: 30%

Limitation of Deduction:Limitation of Deduction:- - Ring fencing by blockRing fencing by block- Head Office (HO) expenditures is allowable for deduction but- Head Office (HO) expenditures is allowable for deduction but

not exceed 2% of the total PE deductible expenditures excluding not exceed 2% of the total PE deductible expenditures excluding PE depreciations and HO expenditures; PE depreciations and HO expenditures;

- Taxable losses carried forward up to 10 years;- Taxable losses carried forward up to 10 years;- Interest expenses for exploration and development is deductible- Interest expenses for exploration and development is deductible

but not excess of the sum of the interest income and 50% of net but not excess of the sum of the interest income and 50% of net non-interest income; non-interest income;

II. Fiscal Regime for Petroleum andII. Fiscal Regime for Petroleum andMinerals (Minerals (concon’’tt))

8

2. Draft of Petroleum Tax Law (2. Draft of Petroleum Tax Law (concon’’tt):): Limitation of Deduction ( Limitation of Deduction (concon’’tt):):

- - Provision on Decommissioning Costs are deductible;Provision on Decommissioning Costs are deductible;- C- Contractor has alternative to use UOP or Straight Line (SL) forontractor has alternative to use UOP or Straight Line (SL) for

exploration & development costs; exploration & development costs;- If the SL is elected, the depletion of exploration cost is equal to- If the SL is elected, the depletion of exploration cost is equal to

the projected life or five years, whichever is the lesser; and the the projected life or five years, whichever is the lesser; and the depletion of development cost is equal to the projected life or ten depletion of development cost is equal to the projected life or ten years, whichever is the lesser. years, whichever is the lesser.

- The exploration & development costs, incurred after the start of- The exploration & development costs, incurred after the start of commercial production, accumulated & depreciated on yearly basic. commercial production, accumulated & depreciated on yearly basic.

II. Fiscal Regime for Petroleum andII. Fiscal Regime for Petroleum andMinerals (Minerals (concon’’tt))

9

2. Draft of Petroleum Tax Law (2. Draft of Petroleum Tax Law (concon’’tt):): Transfer of Interest in PA : Transfer of Interest in PA :

- If the transferred value > NBV, the difference recognized as- If the transferred value > NBV, the difference recognized as goodwill & depreciated for 10 years or remaining life. goodwill & depreciated for 10 years or remaining life.

- If the transferred value < NBV, the difference recognized as- If the transferred value < NBV, the difference recognized as taxable revenues and allocated for 10 years or remaining life. taxable revenues and allocated for 10 years or remaining life.

Join Venture: Join Venture:- The draft covers the definition of join venture, obligation of- The draft covers the definition of join venture, obligation of

file tax returns; and administration procedures of contractor file tax returns; and administration procedures of contractor operator of join venture. operator of join venture.

II. Fiscal Regime for Petroleum andII. Fiscal Regime for Petroleum andMinerals (Minerals (concon’’tt))

10

3. Petroleum Regulation (PR):3. Petroleum Regulation (PR): The PR was established in 1991;The PR was established in 1991; Allowed to used the Production Sharing Agreement (PSA);Allowed to used the Production Sharing Agreement (PSA); Fiscal Regime:Fiscal Regime:

Royalty 12.5%Royalty 12.5% (negotiable) (negotiable) The limitation on cost oil is up to 90% The limitation on cost oil is up to 90% (negotiable);(negotiable); The net oil is split based on annual average barrels of oil per dayThe net oil is split based on annual average barrels of oil per day

(BOPD) (BOPD) (negotiable)(negotiable);; Certain fees: surface rental, signature bonusCertain fees: surface rental, signature bonus…… are are negotiablenegotiable;; Profit tax: 25%-50% on net petroleum;Profit tax: 25%-50% on net petroleum; Exemption all taxes including direct and indirect taxes;Exemption all taxes including direct and indirect taxes;

Draft Law on Petroleum is under reviewing by cabinet of minister.Draft Law on Petroleum is under reviewing by cabinet of minister.

II. Fiscal Regime for Petroleum andII. Fiscal Regime for Petroleum andMinerals (Minerals (concon’’tt))

11

4. Petroleum Agreement (PA):4. Petroleum Agreement (PA): PA awarded to join venture of foreign contractors (ChevronPA awarded to join venture of foreign contractors (Chevron……)) Royalty 12.5%Royalty 12.5% Cost oil deduction is up to 90% of production after the royalty;Cost oil deduction is up to 90% of production after the royalty; The net oil is split based on annual average barrels of oil per dayThe net oil is split based on annual average barrels of oil per day

(BOPD); Govt. share is rising from 42% (up to 10,000 BOPD) to 47%(BOPD); Govt. share is rising from 42% (up to 10,000 BOPD) to 47%(excess10,000 to 25,000 BOPD), and 62% (excess of 50,000 BOPD).(excess10,000 to 25,000 BOPD), and 62% (excess of 50,000 BOPD).The The govgov’’tt share of gas is fixed 35%; share of gas is fixed 35%;

Certain fees: surface rental, signature bonus, annual feeCertain fees: surface rental, signature bonus, annual fee……etc.etc. Profit tax: 25% on net petroleumProfit tax: 25% on net petroleum Petroleum costs deduction is authorized by CNPAPetroleum costs deduction is authorized by CNPA Exemption all taxes including direct and indirect taxes.Exemption all taxes including direct and indirect taxes.

II. Fiscal II. Fiscal RegimeRegime for Petroleum and for Petroleum andMinerals (Minerals (concon’’tt))

12

ContentsContents ExistingExistingLOTLOT

Draft PetroleumDraft PetroleumTax LawTax Law

PAPA

1. Income Tax Rate1. Income Tax Rate 30%30% 30%30% 25%25%

2. Income Tax Based2. Income Tax Based Taxable profit.Taxable profit. Taxable profit.Taxable profit. Profit oilProfit oil

3. Depreciation3. Depreciation Unit of ProductionUnit of Production Alternative UOP or Straight lineAlternative UOP or Straight line No mentionedNo mentioned

4. Loss carry forward4. Loss carry forward 5 years5 years 10 years10 years unlimitedunlimited

5. Ring Fencing5. Ring Fencing Not mentionNot mention Ring fencing by blockRing fencing by block No mentionedNo mentioned

6. HO expenditures6. HO expenditures Not mentionNot mention 2% of PE deductible expenses2% of PE deductible expenses No limitationNo limitation

7. Interest expenses7. Interest expenses Included in exploration/DevelopIncluded in exploration/Develop LOT general ruleLOT general rule No mentionedNo mentioned

8. Decommission cost8. Decommission cost Not mentionNot mention Allowable deductionAllowable deduction No mentionedNo mentioned

9. Transfer of interest9. Transfer of interest Not mentionNot mention Depreciation same as transferorDepreciation same as transferor No mentionedNo mentioned

10. Withholding tax10. Withholding tax on non-residents on non-residents

14% on interest, royalties, rent,14% on interest, royalties, rent,management or technical services,management or technical services,dividends (existing LOT)dividends (existing LOT)

14% on interest, royalties, rent,14% on interest, royalties, rent,management or technicalmanagement or technicalservices, dividends (LOT)services, dividends (LOT)

ExemptionExemption

11. VAT local or export11. VAT local or export 10% or 0% (existing LOT)10% or 0% (existing LOT) 10% or 0% (existing LOT)10% or 0% (existing LOT) ExemptionExemption

12. Salary Tax12. Salary Tax 20% for non residents and20% for non residents andprogressive rate 0% progressive rate 0% –– 20% 20%for resident (Existing LOT)for resident (Existing LOT)

20% for non residents and20% for non residents andprogressive rate 0% progressive rate 0% –– 20% 20%for resident (Existing LOT)for resident (Existing LOT)

ExemptionExemption

Comparison TableComparison Table

13

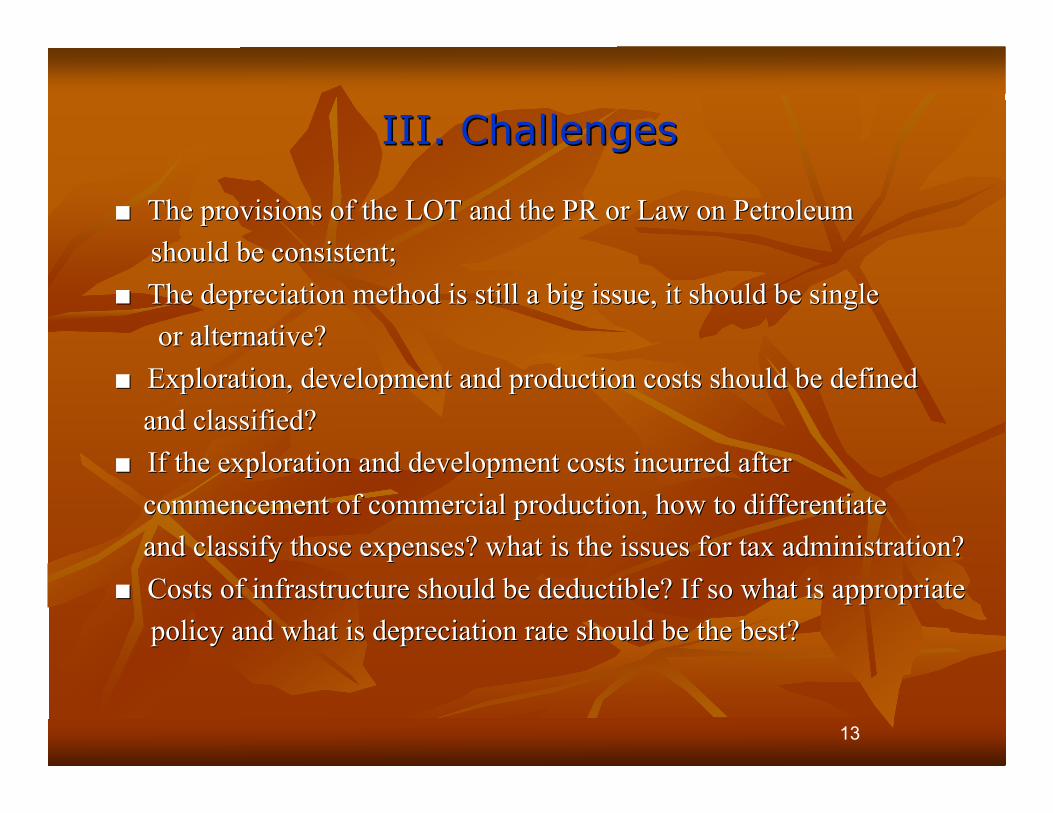

■ ■ The provisions of the LOT and the PR or Law on Petroleum The provisions of the LOT and the PR or Law on Petroleum should be consistent; should be consistent;■ ■ The depreciation method is still a big issue, it should be single The depreciation method is still a big issue, it should be single or alternative? or alternative?■ ■ Exploration, development and production costs should be defined Exploration, development and production costs should be defined and classified? and classified?■ ■ If the exploration and development costs incurred after If the exploration and development costs incurred after commencement of commercial production, how to differentiate commencement of commercial production, how to differentiate and classify those expenses? what is the issues for tax administration? and classify those expenses? what is the issues for tax administration?■ ■ Costs of infrastructure should be deductible? If so what is appropriate Costs of infrastructure should be deductible? If so what is appropriate policy and what is depreciation rate should be the best? policy and what is depreciation rate should be the best?

III. ChallengesIII. Challenges

14

■ ■ Interest deduction should be based on debt-equity ratio or existing Interest deduction should be based on debt-equity ratio or existing LOT general rule (Thin Capitalization Taxation); LOT general rule (Thin Capitalization Taxation);■ ■ HO expenses deduction should be limited at 2%? and how to HO expenses deduction should be limited at 2%? and how to control such expenses? control such expenses?■ ■ How to control provision of decommissioning costs? How to control provision of decommissioning costs?■ ■ What is the issues of transfer of interest in PA? What is the issues of transfer of interest in PA?■ ■ What is the issues of taxing on join venture? What is the issues of taxing on join venture?■ ■ What is the best transfer pricing management rule and; What is the best transfer pricing management rule and;■ ■ How to apply withholding tax on PE How to apply withholding tax on PE’’s profit after tax?s profit after tax?

III. III. ChallengesChallenges ( (concon’’tt))