namibia rare earths inc. rare earths inc. 1 ... the lofdal heavy rare earth project december 2014 ....

TRANSCRIPT

Namibia Rare Earths Inc.

1

Corporate Overview and PEA Update The Lofdal Heavy Rare Earth Project

December 2014

Forward Looking Statements This presentation contains forward-looking statements that relate to the Company's current expectations and views of future events.

In some cases, these forward-looking statements can be identified by words or phrases such as "may", "will", "expect", "anticipate", "aim", "estimate", "intend", "plan",

"seek", "believe", "potential", "continue", "is/are likely to" or the negative of these terms, or other similar expressions intended to identify forward-looking statements. The

Company has based these forward-looking statements on its current expectations and projections about future events and financial trends that it believes may affect its

financial condition, results of operations, business strategy and financial needs. These forward-looking statements include, among other things, statements relating to (i)

the Company's strategy, growth, development and acquisition opportunities, return on existing assets, operational excellence and financial management; (ii) the

Company's expectations regarding its revenue, expenses and operations; (iii) the Company's anticipated cash needs and its estimates regarding its capital and operating

expenditures; (iv) capital requirements, needs for additional financing and the Company's ability to raise additional capital; (v) the Company's estimates of future cash

flows, financial condition and operating performances of the Company and its subsidiaries; (vi) the estimation of any mineral resources and the realization of mineral

reserves based on mineral resource, estimates and estimated future development, if any, and possible variations of ore grade or recovery rates; (vii) estimated results of

planned exploration and development activities; (viii) the Company's competitive position and its expectations regarding competition from other companies globally; (ix)

the Company's ability to maintain customer and supplier relationships; (x) anticipated trends and challenges in the Company's business and the markets in which it

operates, including with respect to potential new rare earths projects, supply outlook and growth opportunities; (xi) limitations of insurance coverage; (xii) the future price

of and future demand for rare earths elements and their derivative products; (xiii) economic and financial conditions; (xiv) interest rates and foreign exchange rates; (xv)

performance of counterparties in fulfilling their obligations; (xvi) government regulation of mining operations, accidents, environmental risks, exploration risks, reclamation

and rehabilitation expenses; (xvii) title disputes or claims; and (xviii) the timing and possible outcome of pending regulatory and permitting matters.

Forward-looking statements are based on certain assumptions and analyses made by the Company in light of its experience and perception of historical trends, current

conditions and expected future developments and other factors it believes are appropriate. These assumptions include continued political stability in Namibia, that

permits required for the Company's operations will be obtained in a timely basis in order to permit the Company to proceed on schedule with its planned drilling

programs, that skilled personnel and contractors will be available as the Company's operations continue to grow, that the price of rare earths will remain at levels that will

render the Company's projects economic and that the Company will be able to continue raising the necessary capital to finance its operations. Forward-looking

statements involve a variety of known and unknown risks, uncertainties and other factors, including those listed under the heading "Risk Factors" in the prospectus of the

Company dated April 7, 2011 (filed on SEDAR www.sedar.com), which may cause the Company's actual results, performance or achievements to be materially different

from any future results, performances or achievements expressed or implied by the forward-looking statements.

The forward-looking statements made in this presentation relate only to events or information as of the date on which the statements are made in the presentation.

Except as required by law, the Company undertakes no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, a

future event or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events.

There can be no assurance that such forward looking information will prove to be accurate, as actual results and future events could differ materially from those

anticipated in such information. Accordingly, potential investors should not place undue reliance on forward-looking information.

2

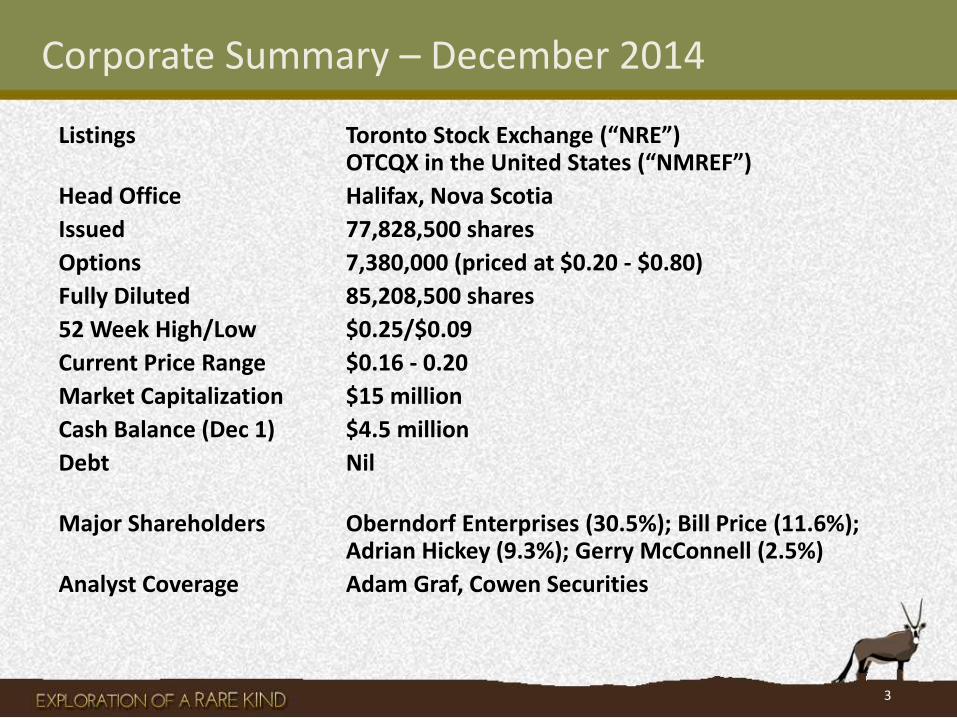

Corporate Summary – December 2014

Listings Toronto Stock Exchange (“NRE”) OTCQX in the United States (“NMREF”)

Head Office Halifax, Nova Scotia

Issued 77,828,500 shares

Options 7,380,000 (priced at $0.20 - $0.80)

Fully Diluted 85,208,500 shares

52 Week High/Low $0.25/$0.09

Current Price Range $0.16 - 0.20

Market Capitalization $15 million

Cash Balance (Dec 1) $4.5 million

Debt Nil

Major Shareholders Oberndorf Enterprises (30.5%); Bill Price (11.6%); Adrian Hickey (9.3%); Gerry McConnell (2.5%)

Analyst Coverage Adam Graf, Cowen Securities

3

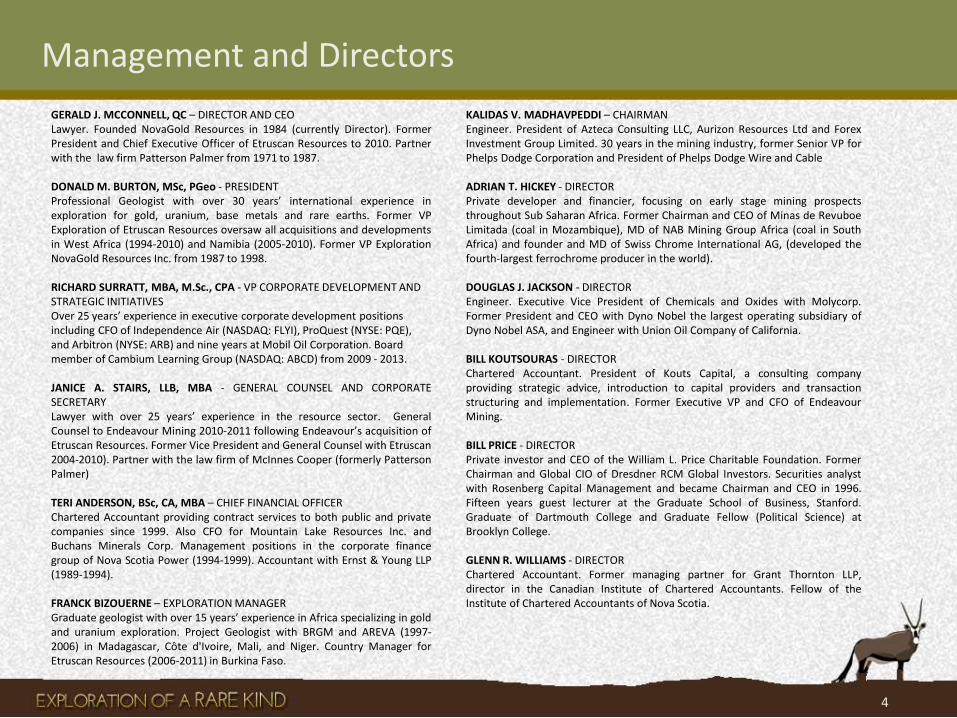

Management and Directors

GERALD J. MCCONNELL, QC – DIRECTOR AND CEO Lawyer. Founded NovaGold Resources in 1984 (currently Director). Former President and Chief Executive Officer of Etruscan Resources to 2010. Partner with the law firm Patterson Palmer from 1971 to 1987.

DONALD M. BURTON, MSc, PGeo - PRESIDENT Professional Geologist with over 30 years’ international experience in exploration for gold, uranium, base metals and rare earths. Former VP Exploration of Etruscan Resources oversaw all acquisitions and developments in West Africa (1994-2010) and Namibia (2005-2010). Former VP Exploration NovaGold Resources Inc. from 1987 to 1998. RICHARD SURRATT, MBA, M.Sc., CPA - VP CORPORATE DEVELOPMENT AND STRATEGIC INITIATIVES Over 25 years’ experience in executive corporate development positions including CFO of Independence Air (NASDAQ: FLYI), ProQuest (NYSE: PQE), and Arbitron (NYSE: ARB) and nine years at Mobil Oil Corporation. Board member of Cambium Learning Group (NASDAQ: ABCD) from 2009 - 2013. JANICE A. STAIRS, LLB, MBA - GENERAL COUNSEL AND CORPORATE SECRETARY Lawyer with over 25 years’ experience in the resource sector. General Counsel to Endeavour Mining 2010-2011 following Endeavour’s acquisition of Etruscan Resources. Former Vice President and General Counsel with Etruscan 2004-2010). Partner with the law firm of McInnes Cooper (formerly Patterson Palmer) TERI ANDERSON, BSc, CA, MBA – CHIEF FINANCIAL OFFICER Chartered Accountant providing contract services to both public and private companies since 1999. Also CFO for Mountain Lake Resources Inc. and Buchans Minerals Corp. Management positions in the corporate finance group of Nova Scotia Power (1994-1999). Accountant with Ernst & Young LLP (1989-1994). FRANCK BIZOUERNE – EXPLORATION MANAGER Graduate geologist with over 15 years’ experience in Africa specializing in gold and uranium exploration. Project Geologist with BRGM and AREVA (1997-2006) in Madagascar, Côte d'Ivoire, Mali, and Niger. Country Manager for Etruscan Resources (2006-2011) in Burkina Faso.

KALIDAS V. MADHAVPEDDI – CHAIRMAN Engineer. President of Azteca Consulting LLC, Aurizon Resources Ltd and Forex Investment Group Limited. 30 years in the mining industry, former Senior VP for Phelps Dodge Corporation and President of Phelps Dodge Wire and Cable

ADRIAN T. HICKEY - DIRECTOR Private developer and financier, focusing on early stage mining prospects throughout Sub Saharan Africa. Former Chairman and CEO of Minas de Revuboe Limitada (coal in Mozambique), MD of NAB Mining Group Africa (coal in South Africa) and founder and MD of Swiss Chrome International AG, (developed the fourth-largest ferrochrome producer in the world).

DOUGLAS J. JACKSON - DIRECTOR Engineer. Executive Vice President of Chemicals and Oxides with Molycorp. Former President and CEO with Dyno Nobel the largest operating subsidiary of Dyno Nobel ASA, and Engineer with Union Oil Company of California. BILL KOUTSOURAS - DIRECTOR Chartered Accountant. President of Kouts Capital, a consulting company providing strategic advice, introduction to capital providers and transaction structuring and implementation. Former Executive VP and CFO of Endeavour Mining. BILL PRICE - DIRECTOR Private investor and CEO of the William L. Price Charitable Foundation. Former Chairman and Global CIO of Dresdner RCM Global Investors. Securities analyst with Rosenberg Capital Management and became Chairman and CEO in 1996. Fifteen years guest lecturer at the Graduate School of Business, Stanford. Graduate of Dartmouth College and Graduate Fellow (Political Science) at Brooklyn College. GLENN R. WILLIAMS - DIRECTOR Chartered Accountant. Former managing partner for Grant Thornton LLP, director in the Canadian Institute of Chartered Accountants. Fellow of the Institute of Chartered Accountants of Nova Scotia.

4

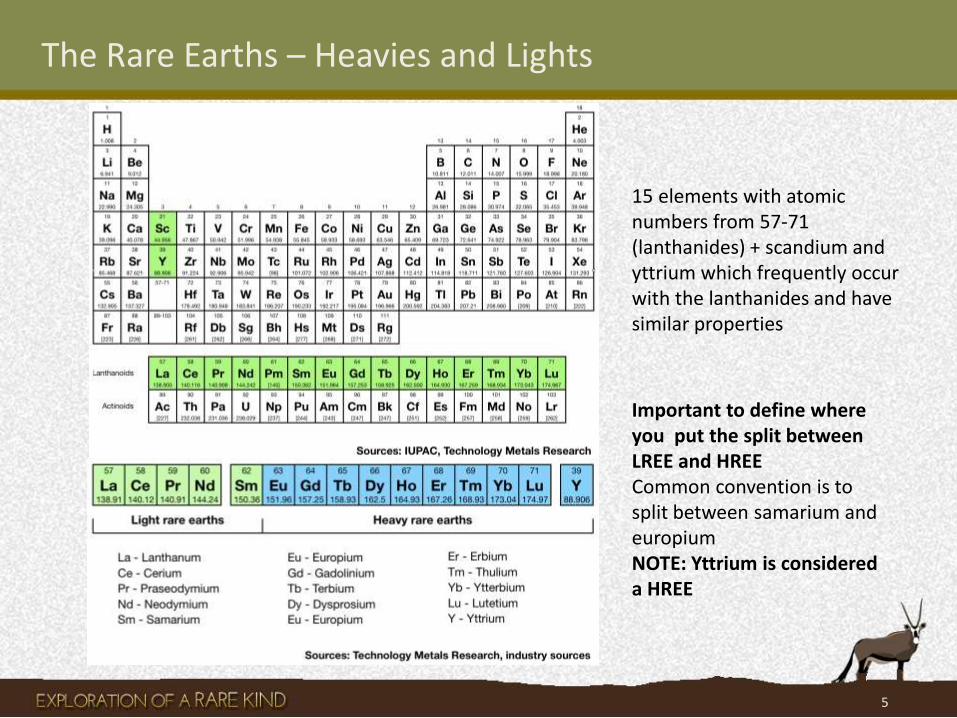

The Rare Earths – Heavies and Lights

15 elements with atomic numbers from 57-71 (lanthanides) + scandium and yttrium which frequently occur with the lanthanides and have similar properties

Important to define where you put the split between LREE and HREE Common convention is to split between samarium and europium NOTE: Yttrium is considered a HREE

5

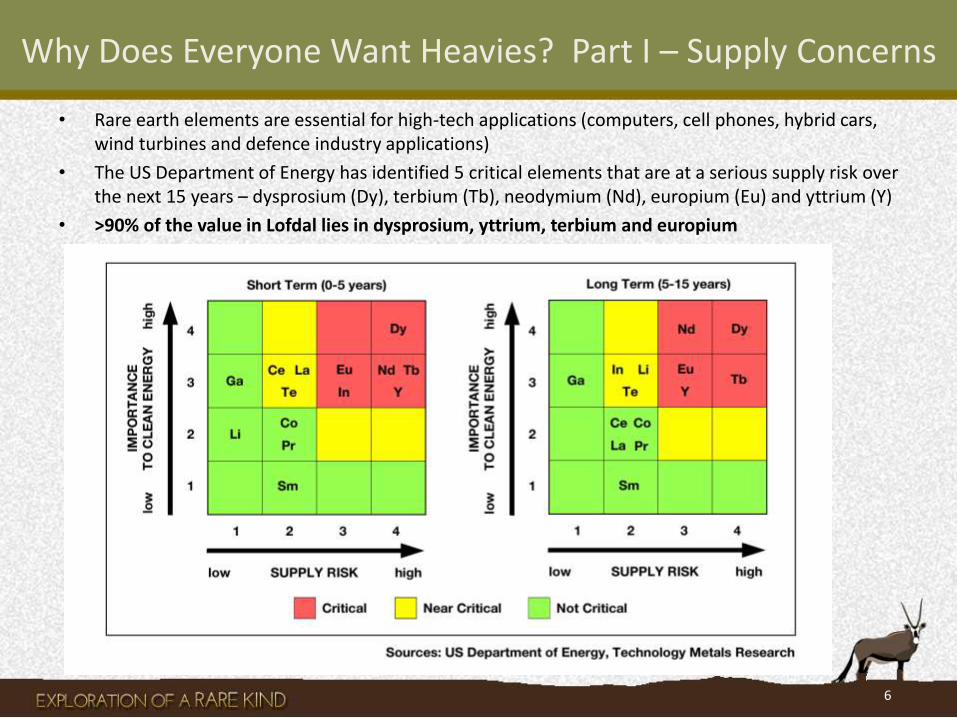

Why Does Everyone Want Heavies? Part I – Supply Concerns

• Rare earth elements are essential for high-tech applications (computers, cell phones, hybrid cars, wind turbines and defence industry applications)

• The US Department of Energy has identified 5 critical elements that are at a serious supply risk over the next 15 years – dysprosium (Dy), terbium (Tb), neodymium (Nd), europium (Eu) and yttrium (Y)

• >90% of the value in Lofdal lies in dysprosium, yttrium, terbium and europium

6

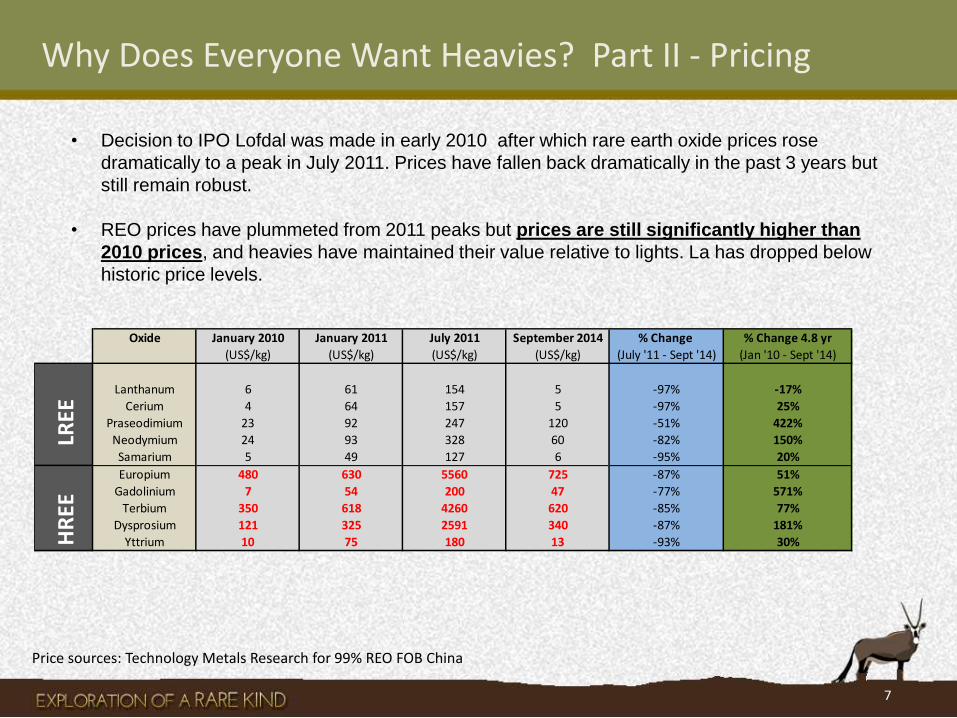

Oxide January 2010 January 2011 July 2011 September 2014 % Change % Change 4.8 yr

(US$/kg) (US$/kg) (US$/kg) (US$/kg) (July '11 - Sept '14) (Jan '10 - Sept '14)

Lanthanum 6 61 154 5 -97% -17%

Cerium 4 64 157 5 -97% 25%

Praseodimium 23 92 247 120 -51% 422%

Neodymium 24 93 328 60 -82% 150%

Samarium 5 49 127 6 -95% 20%

Europium 480 630 5560 725 -87% 51%

Gadolinium 7 54 200 47 -77% 571%

Terbium 350 618 4260 620 -85% 77%

Dysprosium 121 325 2591 340 -87% 181%

Yttrium 10 75 180 13 -93% 30%

Why Does Everyone Want Heavies? Part II - Pricing

• Decision to IPO Lofdal was made in early 2010 after which rare earth oxide prices rose

dramatically to a peak in July 2011. Prices have fallen back dramatically in the past 3 years but

still remain robust.

• REO prices have plummeted from 2011 peaks but prices are still significantly higher than

2010 prices, and heavies have maintained their value relative to lights. La has dropped below

historic price levels.

Price sources: Technology Metals Research for 99% REO FOB China

LREE

H

REE

7

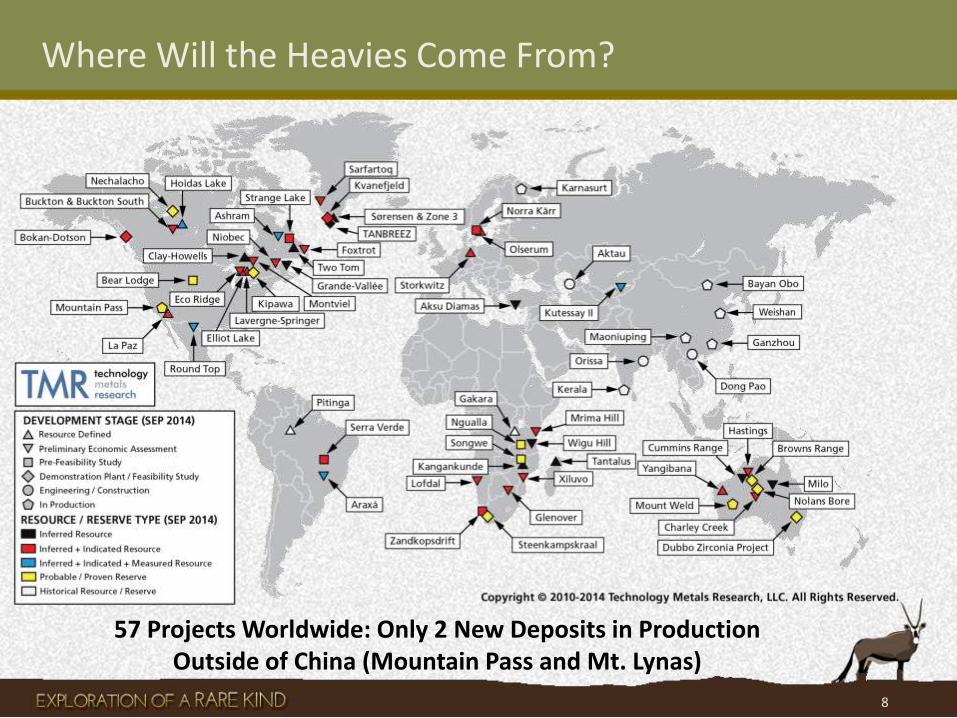

Where Will the Heavies Come From?

8

57 Projects Worldwide: Only 2 New Deposits in Production Outside of China (Mountain Pass and Mt. Lynas)

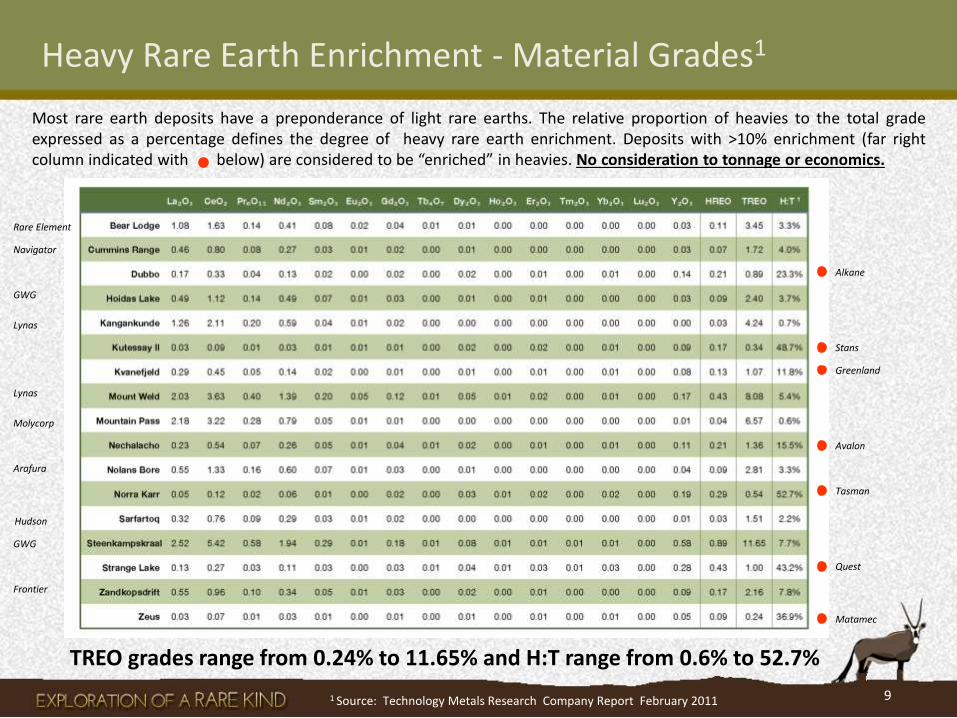

Heavy Rare Earth Enrichment - Material Grades1

Most rare earth deposits have a preponderance of light rare earths. The relative proportion of heavies to the total grade expressed as a percentage defines the degree of heavy rare earth enrichment. Deposits with >10% enrichment (far right column indicated with below) are considered to be “enriched” in heavies. No consideration to tonnage or economics.

TREO grades range from 0.24% to 11.65% and H:T range from 0.6% to 52.7%

Rare Element

Navigator

Alkane

GWG

Lynas

Stans

Greenland

Lynas

Molycorp

Avalon

Arafura

Tasman

Hudson

GWG

Quest

Frontier

Matamec

1 Source: Technology Metals Research Company Report February 2011 9

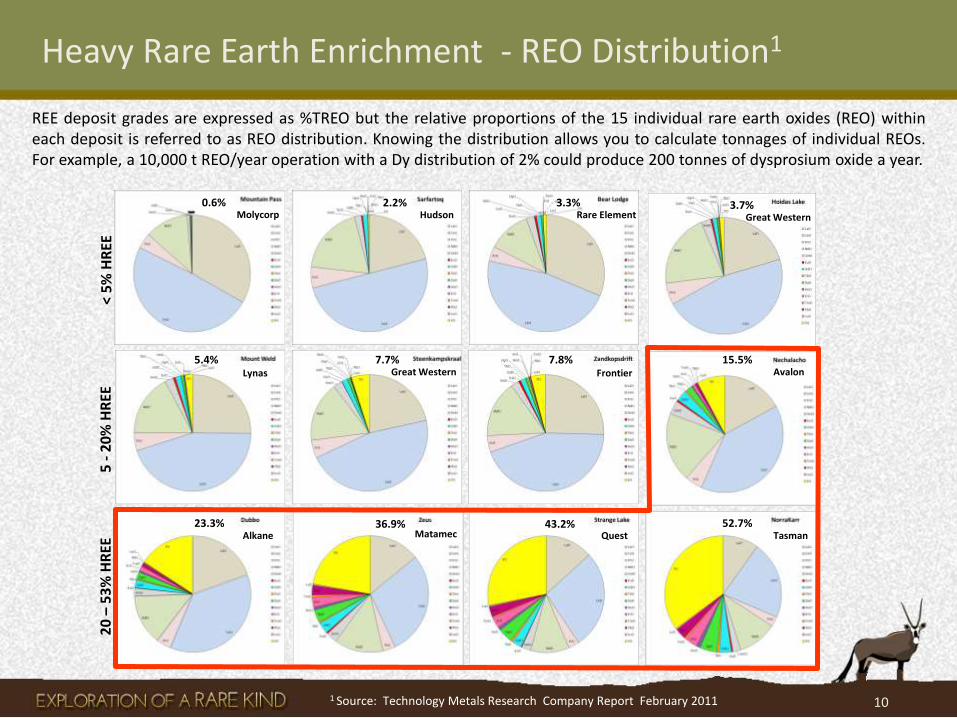

Heavy Rare Earth Enrichment - REO Distribution1

1 Source: Technology Metals Research Company Report February 2011

< 5

% H

REE

5

- 2

0%

HR

EE

20

– 5

3%

HR

EE

0.6% Molycorp

3.3% Rare Element

5.4% Lynas

7.7% Great Western

7.8% Frontier

15.5% Avalon

23.3% Alkane

43.2% Quest

52.7% Tasman

2.2% Hudson

3.7% Great Western

36.9% Matamec

10

REE deposit grades are expressed as %TREO but the relative proportions of the 15 individual rare earth oxides (REO) within each deposit is referred to as REO distribution. Knowing the distribution allows you to calculate tonnages of individual REOs. For example, a 10,000 t REO/year operation with a Dy distribution of 2% could produce 200 tonnes of dysprosium oxide a year.

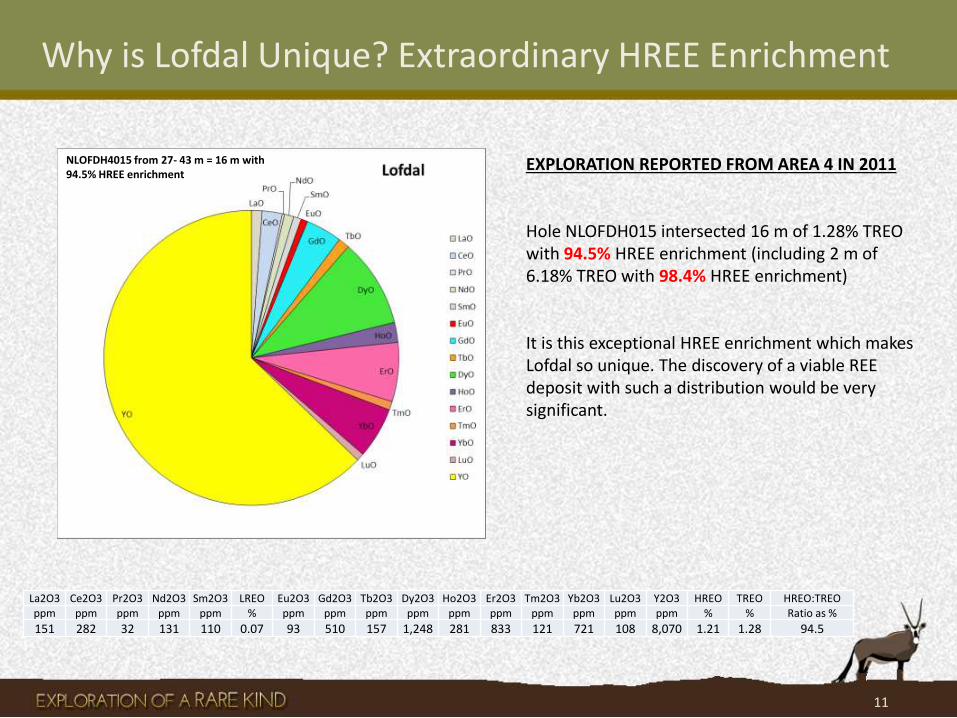

Why is Lofdal Unique? Extraordinary HREE Enrichment

EXPLORATION REPORTED FROM AREA 4 IN 2011 Hole NLOFDH015 intersected 16 m of 1.28% TREO with 94.5% HREE enrichment (including 2 m of 6.18% TREO with 98.4% HREE enrichment) It is this exceptional HREE enrichment which makes Lofdal so unique. The discovery of a viable REE deposit with such a distribution would be very significant.

La2O3 Ce2O3 Pr2O3 Nd2O3 Sm2O3 LREO Eu2O3 Gd2O3 Tb2O3 Dy2O3 Ho2O3 Er2O3 Tm2O3 Yb2O3 Lu2O3 Y2O3 HREO TREO HREO:TREO

ppm ppm ppm ppm ppm % ppm ppm ppm ppm ppm ppm ppm ppm ppm ppm % % Ratio as %

151 282 32 131 110 0.07 93 510 157 1,248 281 833 121 721 108 8,070 1.21 1.28 94.5

NLOFDH4015 from 27- 43 m = 16 m with 94.5% HREE enrichment

11

Namibia Overview

• Mining friendly, politically stable jurisdiction - 4th or 5th largest uranium producer in the world

• Excellent infrastructure

• Major mine operators and developers include:

– Rio Tinto (Rossing)

– Paladin Energy (Langer Heinrich)

– Areva (Trekkopje)

– Forsys Metals (Valencia)

– Bannerman Mining (Etango)

– Extract (now Swakop Uranium)

– B2 Gold (Otjikoto)

– AngloGold Ashanti (Navachab)

– De Beers (Namdeb)

• A dedicated and highly organized approach to support the exploration community from the Ministry of Mines and Energy, and from the Geological Survey of Namibia

12

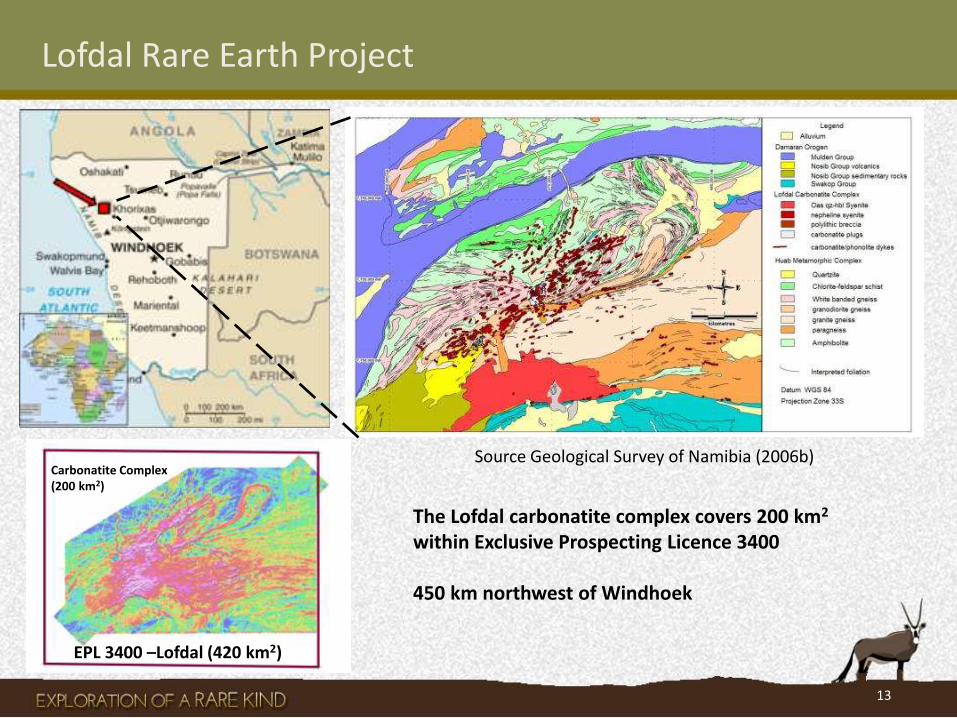

Lofdal Rare Earth Project

Source Geological Survey of Namibia (2006b)

13

EPL 3400 –Lofdal (420 km2)

Carbonatite Complex (200 km2)

The Lofdal carbonatite complex covers 200 km2 within Exclusive Prospecting Licence 3400 450 km northwest of Windhoek

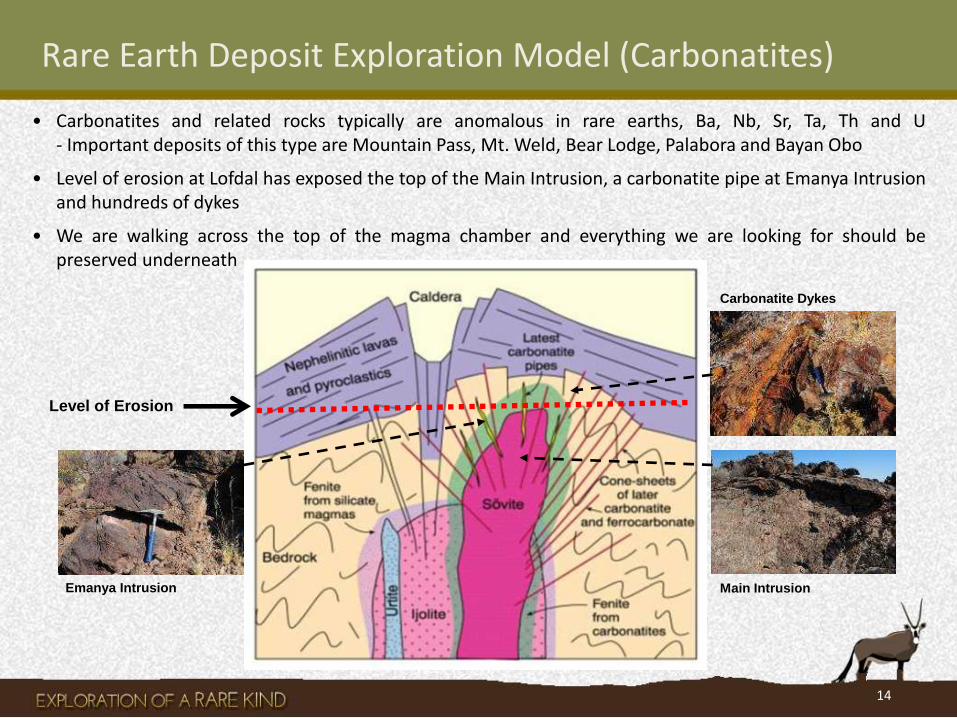

Rare Earth Deposit Exploration Model (Carbonatites)

• Carbonatites and related rocks typically are anomalous in rare earths, Ba, Nb, Sr, Ta, Th and U - Important deposits of this type are Mountain Pass, Mt. Weld, Bear Lodge, Palabora and Bayan Obo

• Level of erosion at Lofdal has exposed the top of the Main Intrusion, a carbonatite pipe at Emanya Intrusion and hundreds of dykes

• We are walking across the top of the magma chamber and everything we are looking for should be preserved underneath

Level of Erosion

Emanya Intrusion

Carbonatite Dykes

Main Intrusion

14

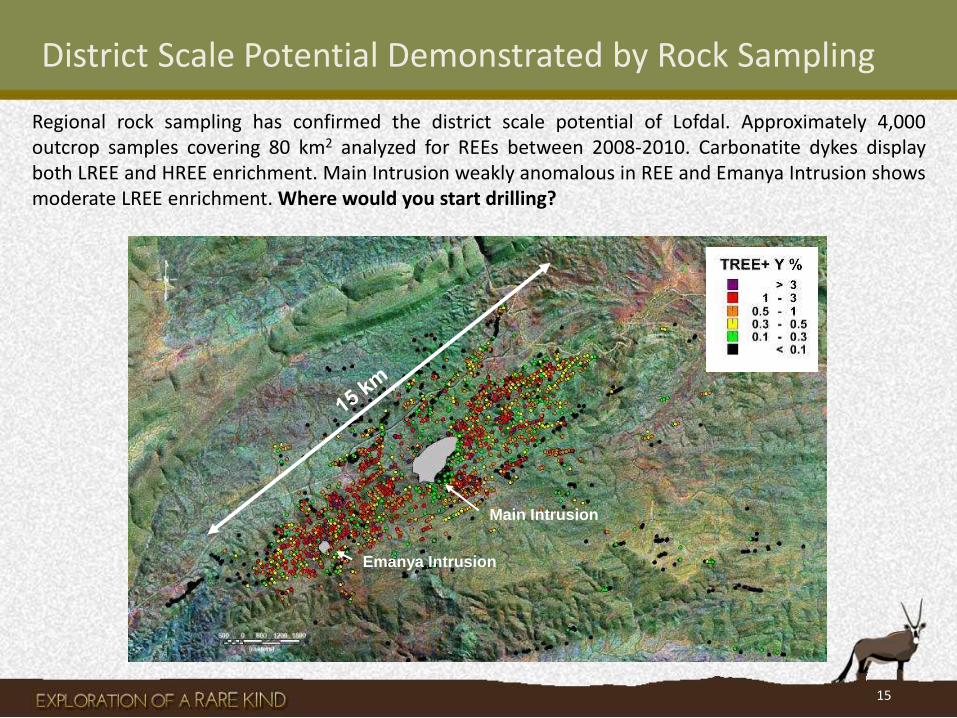

District Scale Potential Demonstrated by Rock Sampling

Main Intrusion

Emanya Intrusion

Regional rock sampling has confirmed the district scale potential of Lofdal. Approximately 4,000 outcrop samples covering 80 km2 analyzed for REEs between 2008-2010. Carbonatite dykes display both LREE and HREE enrichment. Main Intrusion weakly anomalous in REE and Emanya Intrusion shows moderate LREE enrichment. Where would you start drilling?

15

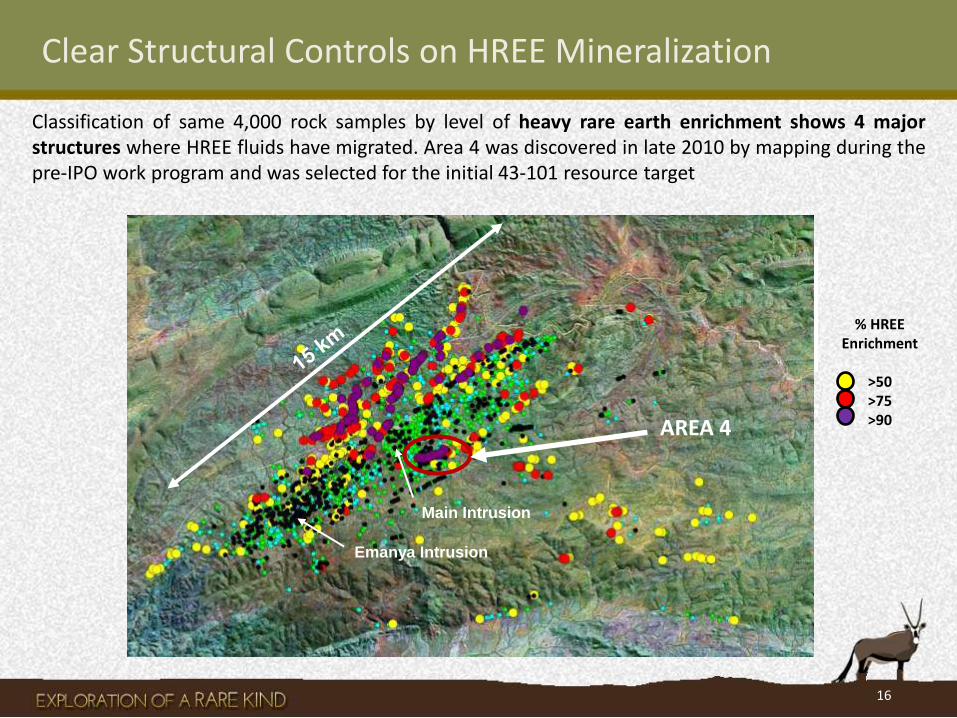

Clear Structural Controls on HREE Mineralization

Main Intrusion

Emanya Intrusion

Classification of same 4,000 rock samples by level of heavy rare earth enrichment shows 4 major structures where HREE fluids have migrated. Area 4 was discovered in late 2010 by mapping during the pre-IPO work program and was selected for the initial 43-101 resource target

Main Intrusion

Emanya Intrusion

% HREE Enrichment

>50 >75 >90 AREA 4

16

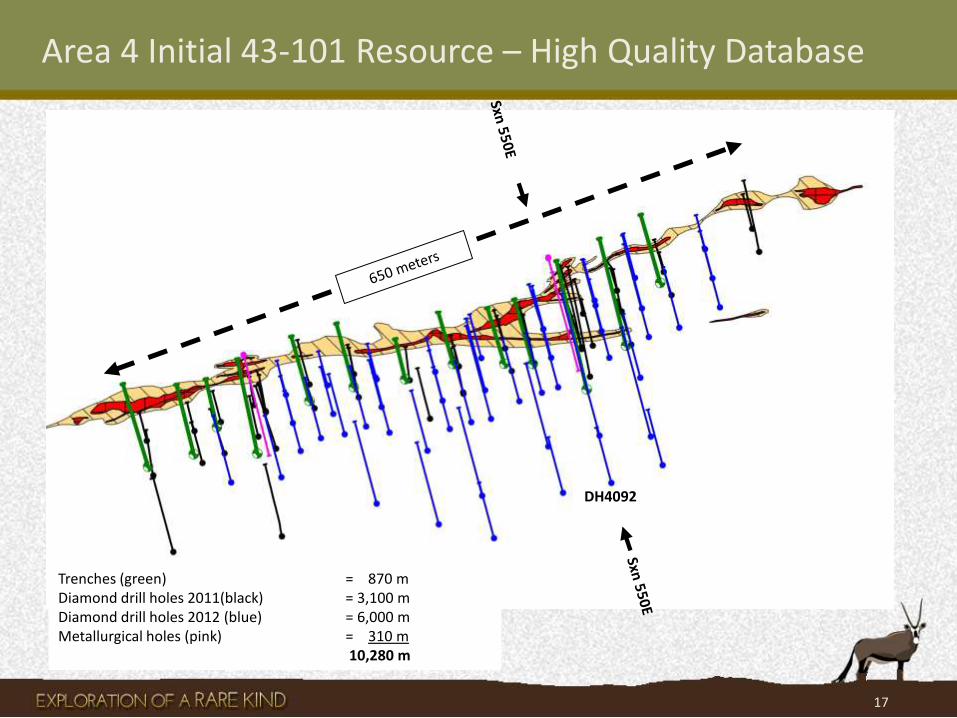

Area 4 Initial 43-101 Resource – High Quality Database

Trenches (green) = 870 m Diamond drill holes 2011(black) = 3,100 m Diamond drill holes 2012 (blue) = 6,000 m Metallurgical holes (pink) = 310 m 10,280 m

DH4092

17

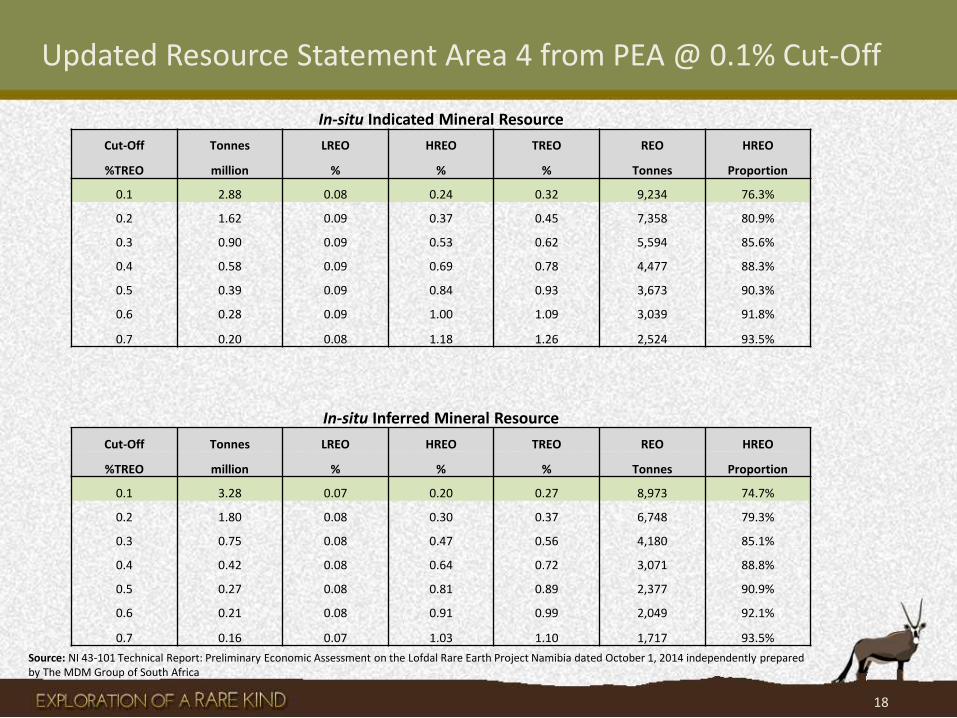

Updated Resource Statement Area 4 from PEA @ 0.1% Cut-Off

Source: NI 43-101 Technical Report: Preliminary Economic Assessment on the Lofdal Rare Earth Project Namibia dated October 1, 2014 independently prepared by The MDM Group of South Africa

18

In-situ Indicated Mineral Resource

Cut-Off Tonnes LREO HREO TREO REO HREO

%TREO million % % % Tonnes Proportion

0.1 2.88 0.08 0.24 0.32 9,234 76.3%

0.2 1.62 0.09 0.37 0.45 7,358 80.9%

0.3 0.90 0.09 0.53 0.62 5,594 85.6%

0.4 0.58 0.09 0.69 0.78 4,477 88.3%

0.5 0.39 0.09 0.84 0.93 3,673 90.3%

0.6 0.28 0.09 1.00 1.09 3,039 91.8%

0.7 0.20 0.08 1.18 1.26 2,524 93.5%

In-situ Inferred Mineral Resource

Cut-Off Tonnes LREO HREO TREO REO HREO

%TREO million % % % Tonnes Proportion

0.1 3.28 0.07 0.20 0.27 8,973 74.7%

0.2 1.80 0.08 0.30 0.37 6,748 79.3%

0.3 0.75 0.08 0.47 0.56 4,180 85.1%

0.4 0.42 0.08 0.64 0.72 3,071 88.8%

0.5 0.27 0.08 0.81 0.89 2,377 90.9%

0.6 0.21 0.08 0.91 0.99 2,049 92.1%

0.7 0.16 0.07 1.03 1.10 1,717 93.5%

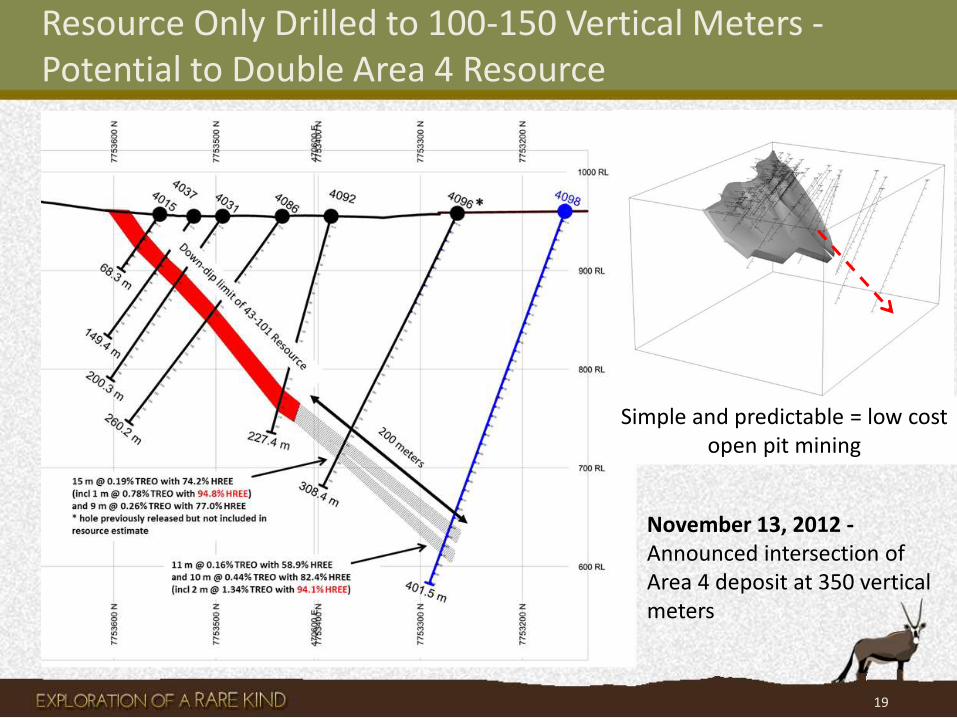

Resource Only Drilled to 100-150 Vertical Meters - Potential to Double Area 4 Resource

November 13, 2012 -Announced intersection of Area 4 deposit at 350 vertical meters

19

Simple and predictable = low cost open pit mining

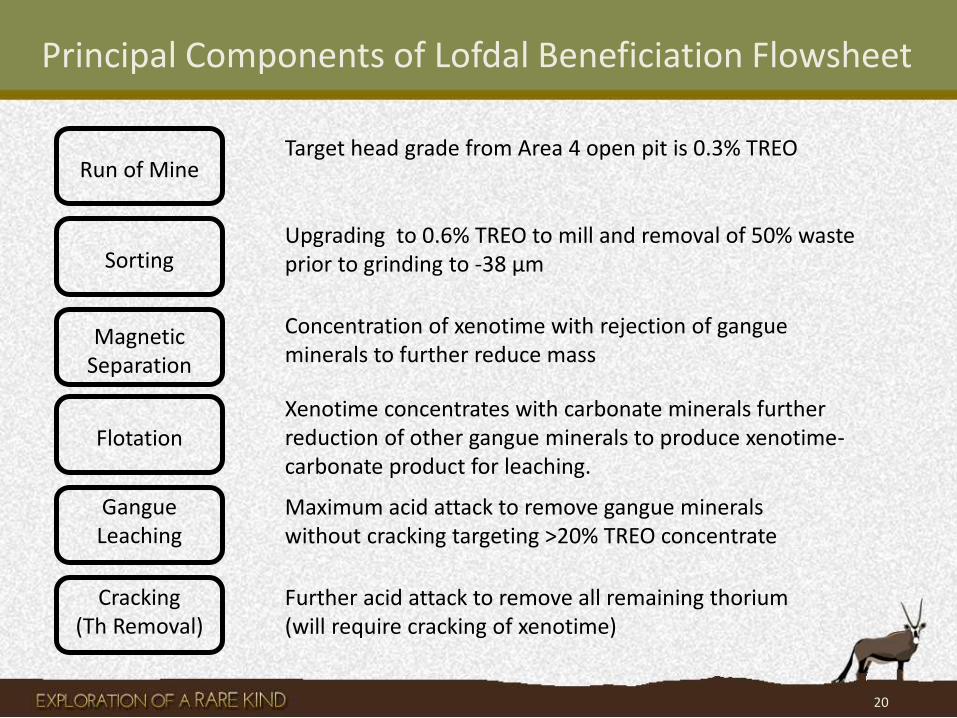

Principal Components of Lofdal Beneficiation Flowsheet

20

Run of Mine

Sorting

Magnetic Separation

Flotation

Gangue Leaching

Cracking (Th Removal)

Target head grade from Area 4 open pit is 0.3% TREO

Upgrading to 0.6% TREO to mill and removal of 50% waste prior to grinding to -38 µm

Concentration of xenotime with rejection of gangue minerals to further reduce mass

Xenotime concentrates with carbonate minerals further reduction of other gangue minerals to produce xenotime-carbonate product for leaching.

Maximum acid attack to remove gangue minerals without cracking targeting >20% TREO concentrate

Further acid attack to remove all remaining thorium (will require cracking of xenotime)

Every REE Deposit Must Demonstrate Amenability to Extraction – Lofdal has a Mineralogical Advantage

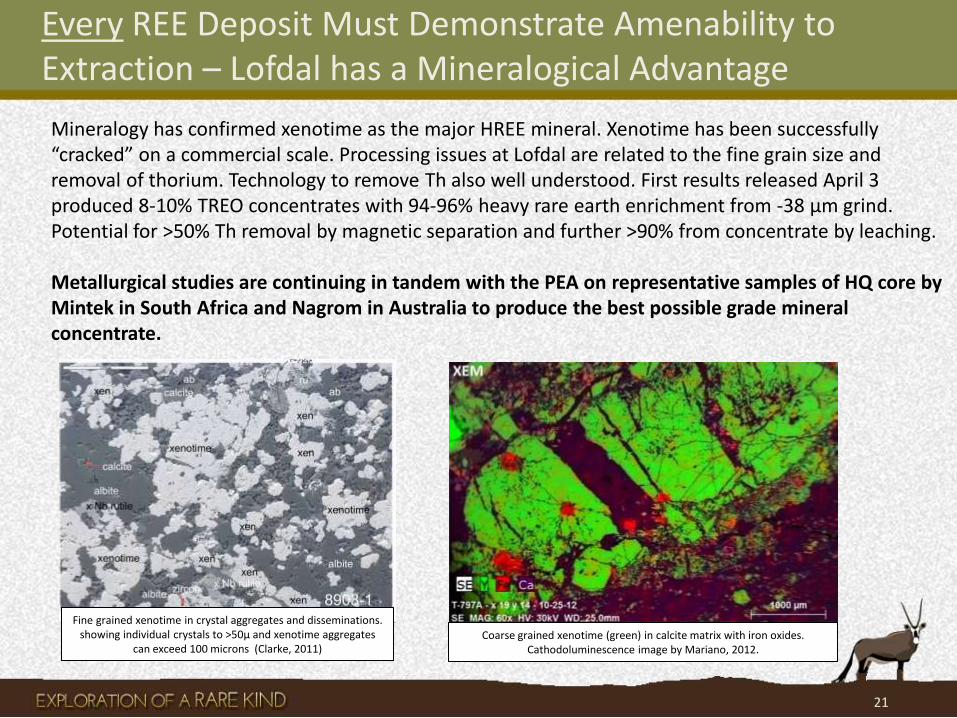

Mineralogy has confirmed xenotime as the major HREE mineral. Xenotime has been successfully “cracked” on a commercial scale. Processing issues at Lofdal are related to the fine grain size and removal of thorium. Technology to remove Th also well understood. First results released April 3 produced 8-10% TREO concentrates with 94-96% heavy rare earth enrichment from -38 µm grind. Potential for >50% Th removal by magnetic separation and further >90% from concentrate by leaching. Metallurgical studies are continuing in tandem with the PEA on representative samples of HQ core by Mintek in South Africa and Nagrom in Australia to produce the best possible grade mineral concentrate.

Fine grained xenotime in crystal aggregates and disseminations. showing individual crystals to >50µ and xenotime aggregates

can exceed 100 microns (Clarke, 2011)

21

Coarse grained xenotime (green) in calcite matrix with iron oxides. Cathodoluminescence image by Mariano, 2012.

Importance of Sorting to Lofdal

Initial scan showing variations in density

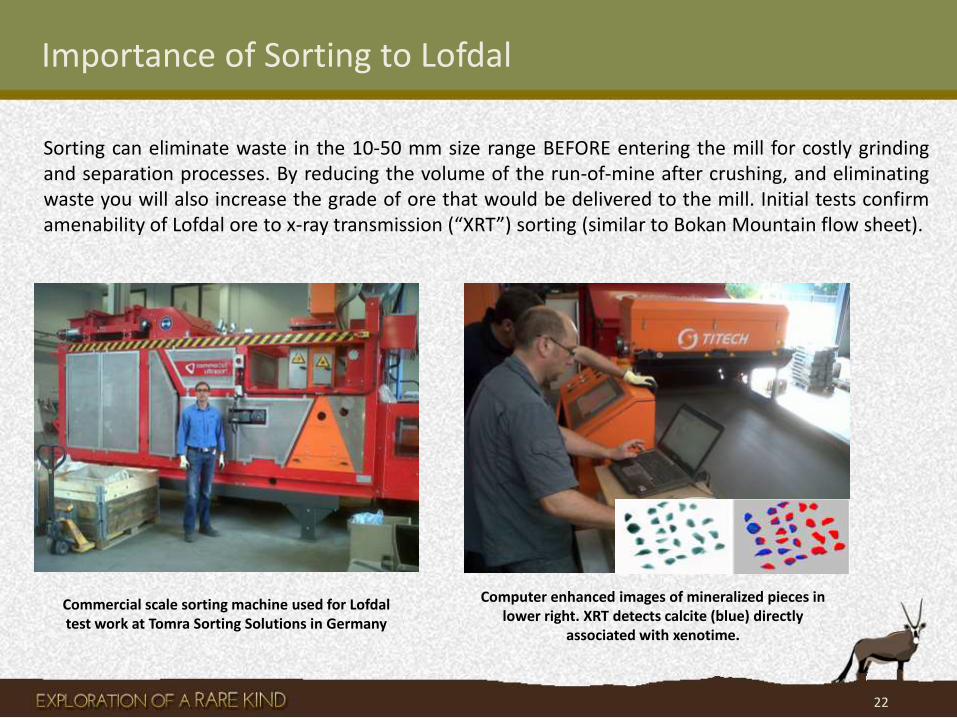

Sorting can eliminate waste in the 10-50 mm size range BEFORE entering the mill for costly grinding and separation processes. By reducing the volume of the run-of-mine after crushing, and eliminating waste you will also increase the grade of ore that would be delivered to the mill. Initial tests confirm amenability of Lofdal ore to x-ray transmission (“XRT”) sorting (similar to Bokan Mountain flow sheet).

22

Commercial scale sorting machine used for Lofdal test work at Tomra Sorting Solutions in Germany

Computer enhanced images of mineralized pieces in lower right. XRT detects calcite (blue) directly

associated with xenotime.

Preliminary Economic Assessment* Completed in 2014

23

• Initiated in June 2014 and completed Oct 2014 using 43-101 compliant resource from Area 4

• Metallurgical test work confirmed amenability to consider 0.1% TREO cut-off • Capital and operating cost estimates for an 840,000 tpa open pit mining

operation • Produce 1,500 tpa of mixed REO concentrate • Final concentrate product would be highly enriched in heavy rare earths • Positive NPV and IRR with robust cash flows over a 7 year life of mine • Geological evidence supports moving to a 15 year life of mine

Recommended to move to Prefeasibility Study with extended LOM • Can provide a sustainable source of heavy rare earths outside of China

* The PEA should not be considered to be a pre-feasibility or feasibility study, as the economics and technical viability of the Project has not been demonstrated at this time. The PEA is preliminary in nature and includes Inferred Mineral Resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as Mineral Reserves. Furthermore, there is no certainty that the PEA will be realized.

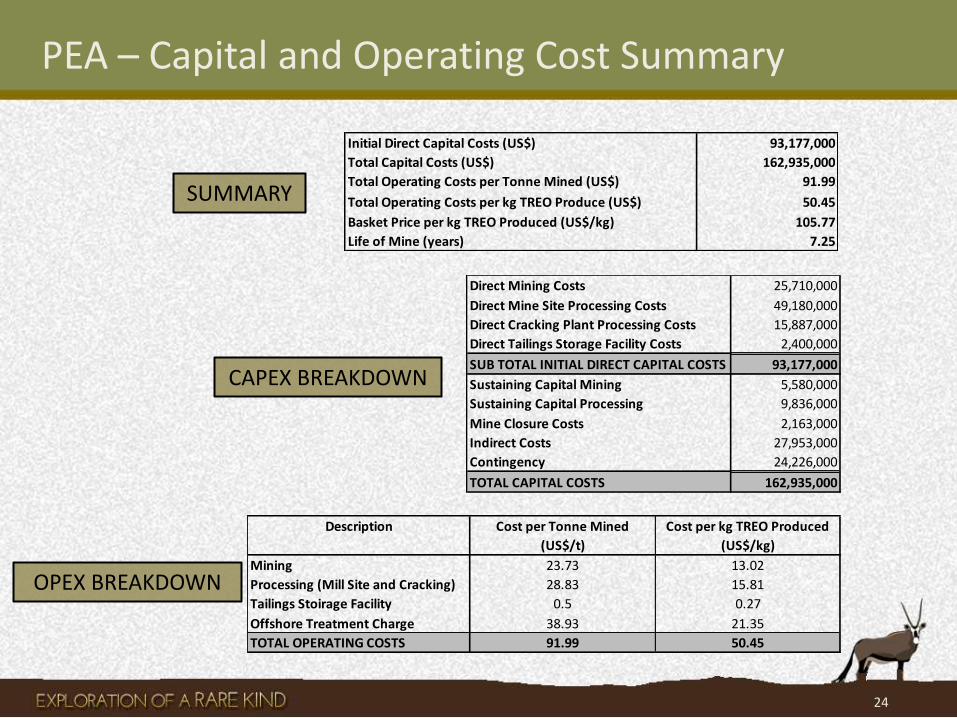

PEA – Capital and Operating Cost Summary

24

SUMMARY

CAPEX BREAKDOWN

OPEX BREAKDOWN

Initial Direct Capital Costs (US$) 93,177,000

Total Capital Costs (US$) 162,935,000

Total Operating Costs per Tonne Mined (US$) 91.99

Total Operating Costs per kg TREO Produce (US$) 50.45

Basket Price per kg TREO Produced (US$/kg) 105.77

Life of Mine (years) 7.25

Direct Mining Costs 25,710,000

Direct Mine Site Processing Costs 49,180,000

Direct Cracking Plant Processing Costs 15,887,000

Direct Tailings Storage Facility Costs 2,400,000

SUB TOTAL INITIAL DIRECT CAPITAL COSTS 93,177,000

Sustaining Capital Mining 5,580,000

Sustaining Capital Processing 9,836,000

Mine Closure Costs 2,163,000

Indirect Costs 27,953,000

Contingency 24,226,000

TOTAL CAPITAL COSTS 162,935,000

Description Cost per Tonne Mined Cost per kg TREO Produced

(US$/t) (US$/kg)

Mining 23.73 13.02

Processing (Mill Site and Cracking) 28.83 15.81

Tailings Stoirage Facility 0.5 0.27

Offshore Treatment Charge 38.93 21.35

TOTAL OPERATING COSTS 91.99 50.45

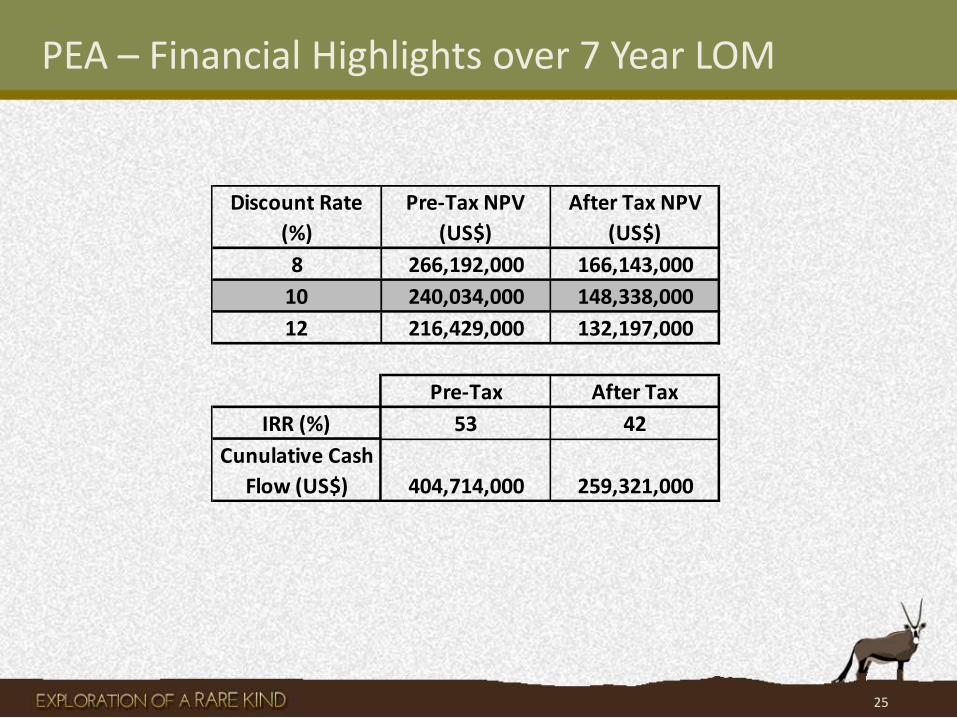

PEA – Financial Highlights over 7 Year LOM

25

Discount Rate Pre-Tax NPV After Tax NPV

(%) (US$) (US$)

8 266,192,000 166,143,000

10 240,034,000 148,338,000

12 216,429,000 132,197,000

Pre-Tax After Tax

IRR (%) 53 42

Cunulative Cash

Flow (US$) 404,714,000 259,321,000

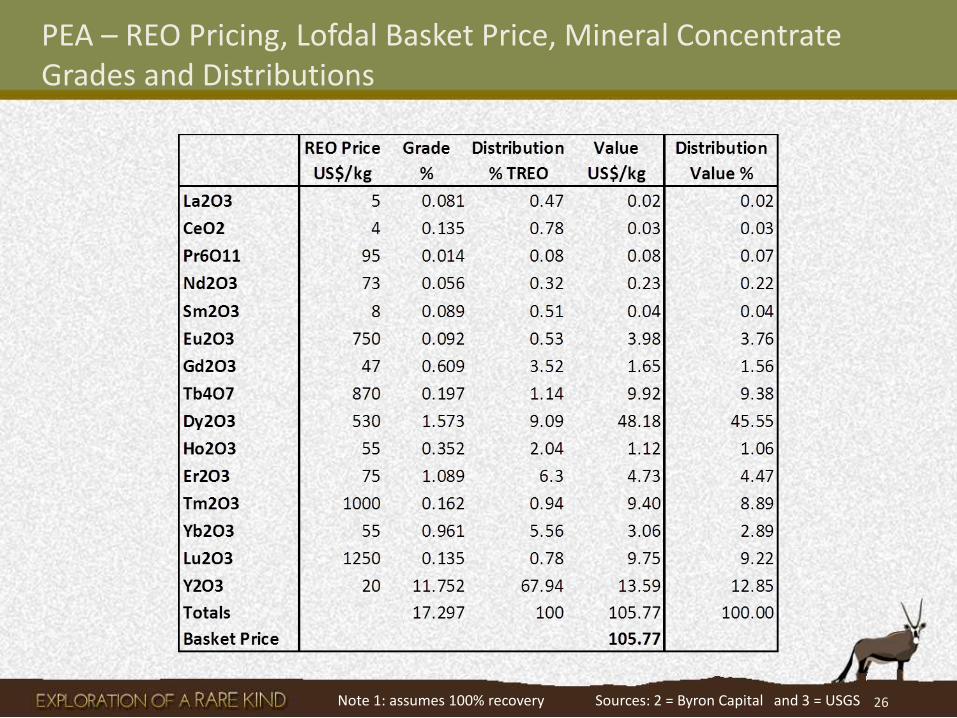

PEA – REO Pricing, Lofdal Basket Price, Mineral Concentrate Grades and Distributions

Note 1: assumes 100% recovery Sources: 2 = Byron Capital and 3 = USGS 26

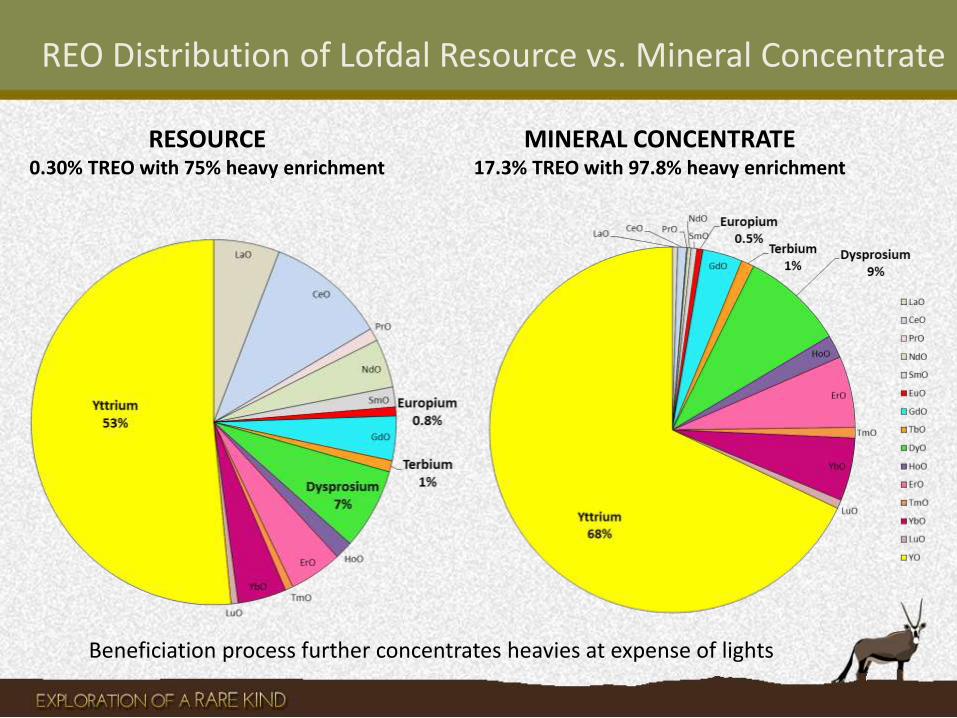

REO Distribution of Lofdal Resource vs. Mineral Concentrate

RESOURCE 0.30% TREO with 75% heavy enrichment

MINERAL CONCENTRATE 17.3% TREO with 97.8% heavy enrichment

Beneficiation process further concentrates heavies at expense of lights

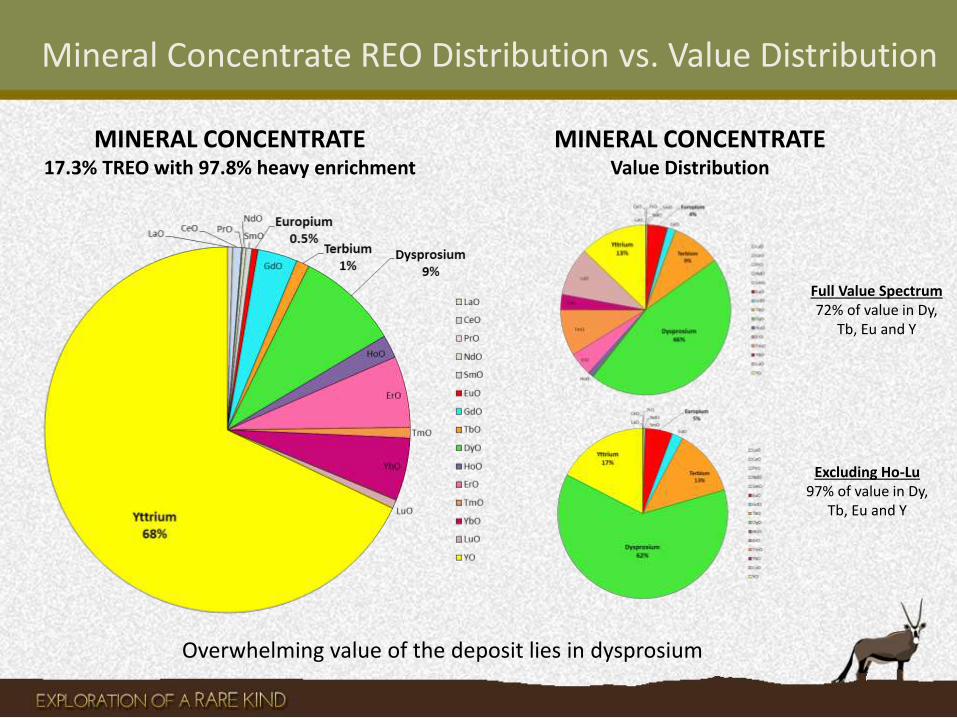

Mineral Concentrate REO Distribution vs. Value Distribution

Overwhelming value of the deposit lies in dysprosium

MINERAL CONCENTRATE 17.3% TREO with 97.8% heavy enrichment

MINERAL CONCENTRATE Value Distribution

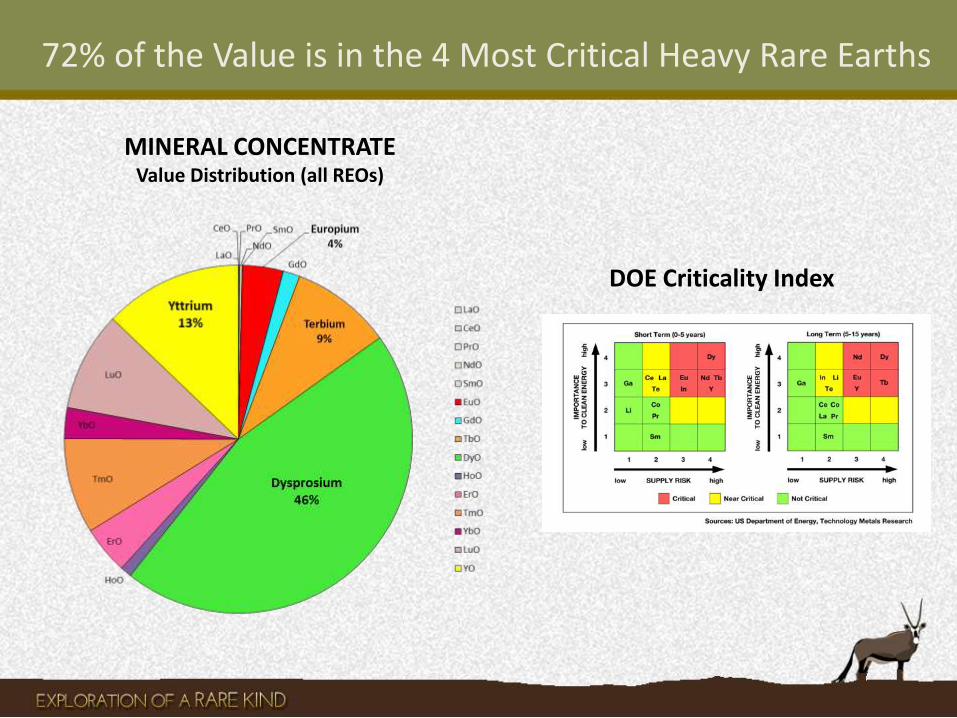

Full Value Spectrum 72% of value in Dy,

Tb, Eu and Y

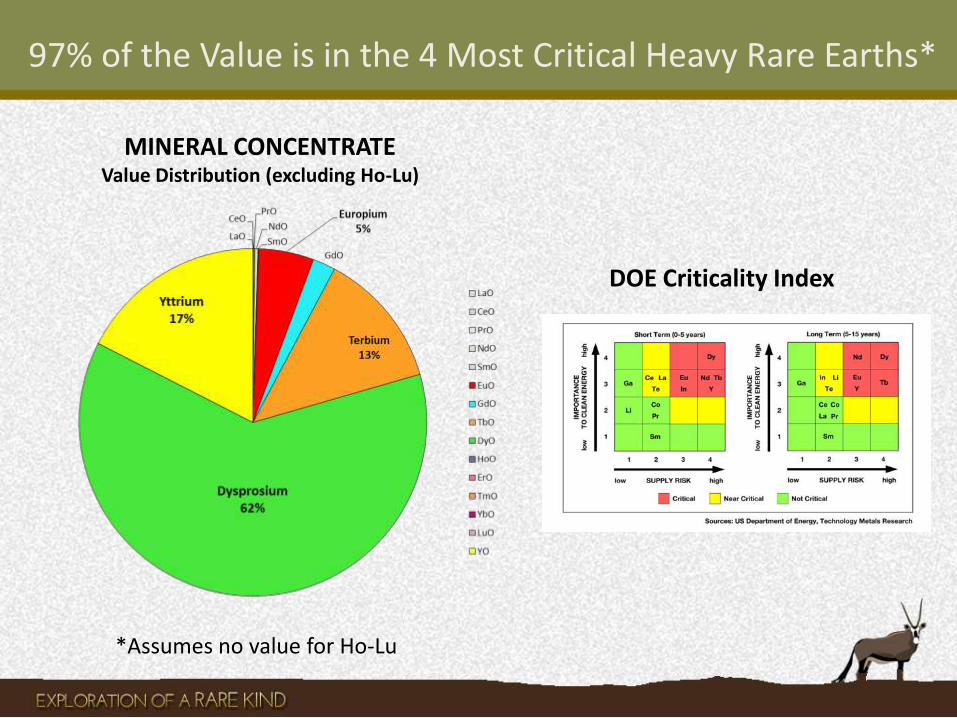

Excluding Ho-Lu 97% of value in Dy,

Tb, Eu and Y

72% of the Value is in the 4 Most Critical Heavy Rare Earths

DOE Criticality Index

MINERAL CONCENTRATE Value Distribution (all REOs)

97% of the Value is in the 4 Most Critical Heavy Rare Earths*

DOE Criticality Index

MINERAL CONCENTRATE Value Distribution (excluding Ho-Lu)

*Assumes no value for Ho-Lu

Projected Annual Outputs Based on REO Distribution*

31

*Assumes distribution of cracked product is same as mineral concentrate and no loss to cracking

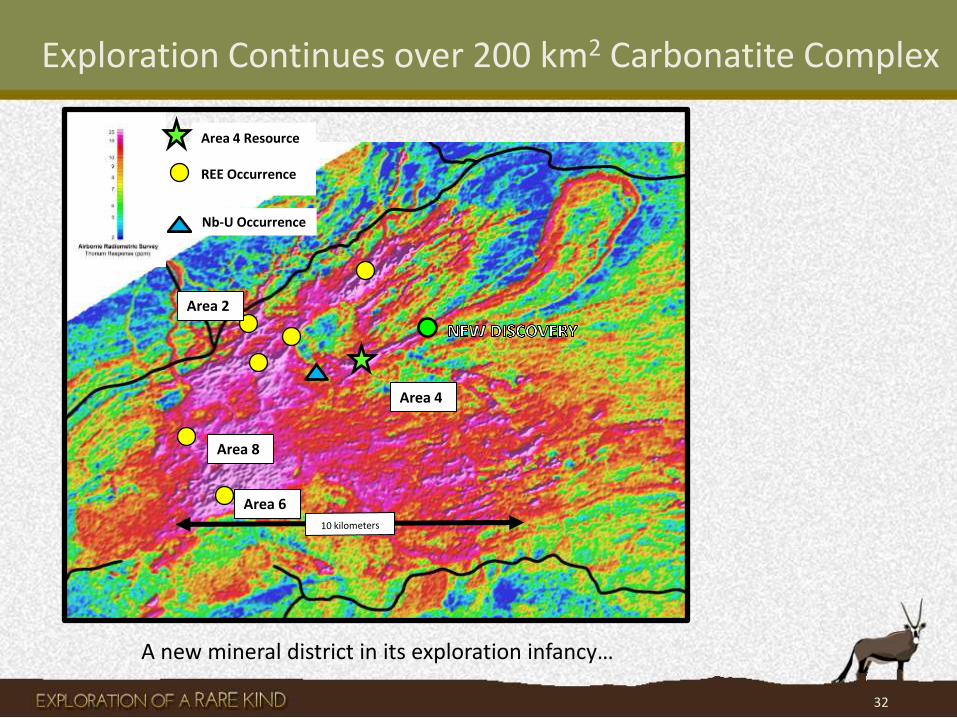

Exploration Continues over 200 km2 Carbonatite Complex

Area 4 Resource

REE Occurrence

Area 6

32

Nb-U Occurrence

Area 8

Area 2

Area 4

A new mineral district in its exploration infancy…

We Think Lofdal is Important – Who Else Does?

33

Brandon Tirpak – Asian Metals (Sept 11, 2012) “[NRE’s} project has very high HREE content. Its assays have typically shown HREE distributions in the 90th percentile.” Alex Knox – Consulting Geologist (Jan 22, 2013) “While a typical REE deposit is considered heavy if its distribution has 30 or 40% HREEs, the results of some of the exploration done by [NRE] show that it has 70, 80 or even 90% HREEs. So it is not going to have to market those LREEs that are presently going to be in at least equilibrium or oversupply. It will produce nothing but the HREEs that everybody needs.” Chris Berry – House Mountain Partners (July 30, 2013) “[NRE] has quietly pushed forward with exploration of the Lofdal deposit and recently was able to show that it can produce an attractive HREE concentrate there.” Tom Szabo – MetalAugmentor.com (Oct 15, 2013) “[NRE] doesn't have a particularly large deposit, but the development timeline could potentially be short. It also has a very high percentage of valuable heavy rare earths, probably one of the highest in the world.”

We Think Lofdal is Important – Who Else Does?

34

John Kaiser – Kaiser Research Online (Oct 22, 2013) “Within three years, I could see Namibia Rare Earths supplying a significant amount of HREEs, which make up 80–90% of the ore, furnishing about 50% of non-Chinese demand, all of which is currently supplied by China's depleting HREE enriched deposits. That's much faster than the four to six years we can expect for any of the bigger projects.” Adam Graf – Cowen and Company (Nov 21, 2013) “New results follow-up on test work completed in early April 2013, which confirmed - due to the presence of the mineral xenotime as the principle HREE host – a significant processing advantage than typically seen at rare earth deposits.” Mike Niehuser – Beacon Rock Research (Dec 4, 2013) “Namibia Rare Earths, being primarily heavies, has the highest basket price for contained minerals, contained within a well-defined resource with excellent expansion opportunity. Namibia Rare Earths recently reported steady progress on its metallurgical test work, which appears to build upon its credibility in locating a qualified joint venture partner.” Luisa Moreno – Euro Pacific Capital (Jan 28, 2014) “Namibia Rare Earths Inc. also has a xenotime deposit under development. Namibia’s Lofdal REE project is also attractive, as it has the potential to produce large amounts of these less common elements [heavy rare earths]”.

We Think Lofdal is Important – Who Else Does?

35

Ryan Castilloux – Adamas Intelligence (Feb 11, 2014) “Namibia Rare Earths Inc.'s Lofdal project in Namibia is very interesting. The resource to date is small: only around 10,000 metric tons of REOs in situ. However, these REOs are 80% heavy rare earth oxides (HREOs) and 70% CREOs.” Chris Berry – House Mountain Partners (June 17, 2014) “Namibia Rare Earths Inc. is also on my radar. We don't know a lot about the economics yet, but if an investor is patient and willing to take some risk, it is worth considering. Namibia has an attractive deposit and is an earlier-stage play that surprised a lot of people with some of its metallurgical results. The company's ability to produce a xenotime concentrate and potential catalysts from a preliminary economic assessment that is now underway and metallurgical optimization are all differentiators. There's a lot to learn here, but a lot of potential upside as well.” Adam Graf – Cowan and Company (Oct 2, 2014) “The initial PEA for Lofdal demonstrates a project with slightly better economics than we had been modeling. We continue to believe that NRE's Lofdal asset offers exposure to a deposit with high concentrations of HREE, potentially amenable to lower cost mining and processing.” Jack Lifton – Technology Metals Research, LLC (Nov 11, 2014) “In Africa, Namibia Rare Earths Inc. may be the lowest cost mine of all to bring to production. “