naiop 2012 texas shoot out case challenge

TRANSCRIPT

averick

evelopment

April 19, 2012| Lee Mazurek | Jason Turnbow | Eric Hendrickson | Tyler Clayton | Jeff Peanick | Nathan Beaman |

Introduction

Overview of Site

Functional Design

Linkages

Economic Base

Financial Analysis

Questions & Answers

Dallas Potential

“Great cities are the product of four

qualities: quality of place, quality of

talent, quality of opportunity, and

quality of leadership.”

Ms. Carol ColettaPresident & CEO of CEOs for Cities

Recommendation

Multi-use Development With High-Rise Office

Buildings, Retail Space, A Residential Area,

Entertainment, Restaurants, And Public Transit.

Reunion Park Site Plan

Retain existing frontage roads

to provide access to grade-

level streets and parking

structures for new

development

Develop “Lot E” with

mid- and high-rise

mixed-use development

rising to Houston

/Jefferson viaduct level

Establish strong connections

within development to

encourage pedestrian

circulation and support

walkable blocks

Create new terraced park

providing visual connection to

Trinity Park

Ensure compatibility with

Dallas Convention Center

Ensure stop along Houston

viaduct streetcar line to serve

new development

Enhance sidewalks along

viaducts to strengthen

pedestrian connection

between Omni Hotel and

new development

City of Dallas

Geographic Center of North AmericaA

Dallas Hub

− 20 Fortune 500 Companies

− 269 Headquartered CompaniesA

600,000+ Workforce

− 30% Have at Least a College Degree

1.3 Million within City of Dallas

− 9th Largest in U.S.

−7,000 Central Business District

− Median Income of $62,000

Accessibility Overview

Superior Location with DART Rail

Easy Access to Dallas Love Field Airport

More Than 1,900 Flights Daily

Dallas is Centrally Located

4-Hour Flight To Most North American Cities

Surrounded by Three Major Highways

Highways Connect to Entire Metroplex

7 Miles from Dallas Love Field

20 Miles from DFW International Airport

1) Location: Inside CBD Loop | High Visibility | View of Trinity River

2) Timing: Many Real Estate Development Projects in Dallas

3) Capital: Economic Resiliency Compared to National Average

Benefit Analysis

PROS

1) Location: Dart Rail Cutoff Across From Project Site

2) Location: ½ Mile From Trinity River Project

3) Capital: Private / Public Land Swap Not A Viable Option

CONS

Development Impact

Adjacent Land Use(s)

The City of Dallas

Economic Base of Dallas

I-35 / Reunion Blvd:

235,466

Commerce St. / S. Houston St.:

13,778

S. Lamar St. / ERL Thornton

Fwy: 15,584

I-30 / S. Akard St.:

189,442

I-35 / S. Market St.:

141,048

I-35 / I-30:

118,432

Site Traffic Count

Number of Businesses

Business Sector Analysis

Consumer Spending

Employment

Site Vision

Target Market

Dallas Has 28+ Million Annual Visitors

3%+ of The Air Market Visit Dallas Each Year

Within 500-Mile Radius

34 Million People

Investment Strategy

Structured Site Plan

+ 5-Year, 4 Phase Development Project

Create 2,092,650 Additional Square Feet

+ 957,250 Retail Space

+ 823,400 Office Space

+ 312,000 Residential Space

5-Year Investment Horizon

+ 2-Year Residential Exposure

+ 5-Year Office & Retail Exposure

Phase I

2 High-Rise Office Buildings

- 823,400 sq. ft. | $320.00 sq. ft.

Light Rail Transportation

- 82,680 sq. ft. | $800.00 sq. ft.

Bike Path

- 37,500 sq. ft. | $30.00 sq. ft.

Adaptive Reuse of Parking Garage

- 134,000 sq. ft. | $45.95 sq. ft.

$367,720,211 Total Cost

4-Year Development Timeline | Start Year 1

Phase II

3 Condominium Buildings

- 468,000 sq. ft. | $132.00 sq. ft.Central Retail Building

- 189,000 sq. ft. | $103.00 sq. ft.

Cinema

- 40,000 sq. ft. | $45.95 sq. ft.

$85,723,000 Total Cost

2-Year Development Timeline | Start Year 3

Phase III

Reunion Village

- 143,000 sq. ft. | $103.00 sq. ft.LeReunion Mall

- 135,000 sq. ft. | $140.00 sq. ft.

$33,269,000 Total Cost

2-Year Development Timeline | Start Year 3

The Past Meets The Future

LeReunion Grande Casino

Phase IV

LeReunion Grande Casino

Largest Luxury Casino in North AmericaA

Recaptures $2.7B Texas Gaming RevenuesA

Generates 1.2M Hotel “Rooms Nights” AnnuallyA

Generates $740M in Hotel RevenueA

Creates 8,000 Casino JobsA

Generates $18M Annually in Hotel TaxA

Generates $12M Annually in State Sales Tax

Texas Gaming Legislation

Article 17

- Requires Constitutional Amendment

A

3 .2

2 .5

10 .3

2 .5

2 .0

0 .3

0 .7

0 .0 5 .0 1 0 .0 1 5 .0

Ok l ah oma

Lou is ian a

N evada

M iss iss ippi

A r izon a

N ew M ex ic o

Co l o r ado

2 0 0 9 GAMIN G REVENUES

Tex as Va l ue Cas in o Reven ue

In B il l ion s

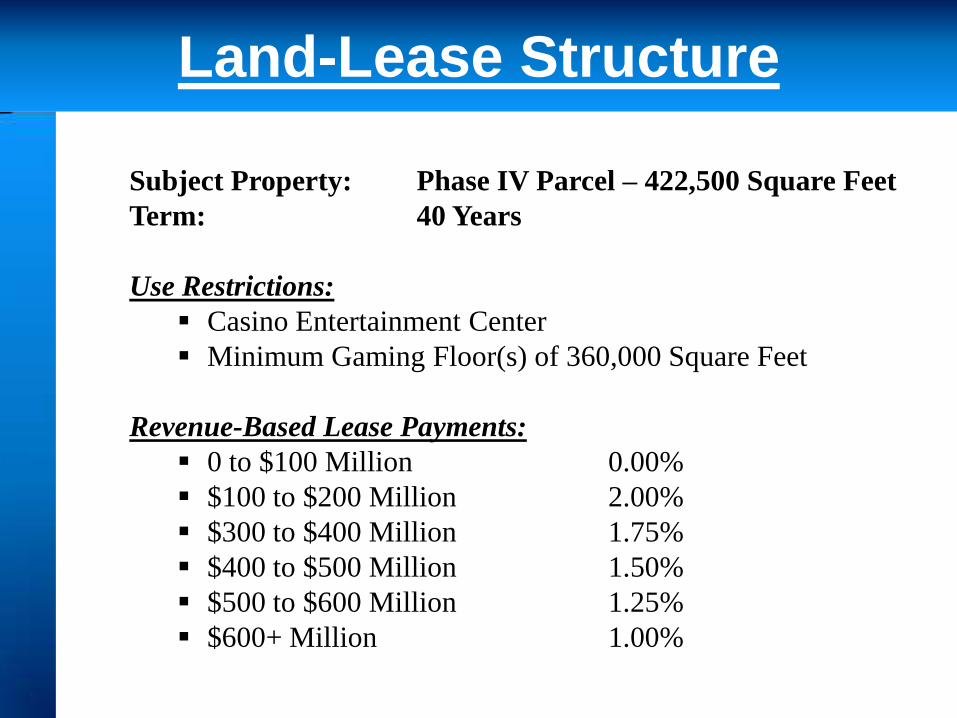

Land-Lease Structure

Subject Property: Phase IV Parcel – 422,500 Square Feet

Term: 40 Years

Use Restrictions:

Casino Entertainment Center

Minimum Gaming Floor(s) of 360,000 Square Feet

Revenue-Based Lease Payments:

0 to $100 Million 0.00%

$100 to $200 Million 2.00%

$300 to $400 Million 1.75%

$400 to $500 Million 1.50%

$500 to $600 Million 1.25%

$600+ Million 1.00%

Dallas’ LeReunion Grande Casino

Lease Offset

Fees Will Be Applied Against Lease Expense

8 Years From Initial Option Date

Term I for 3 Years

– Option 1: $10.8 Million

Term II for 2 Years

– Option 2: $7.2 Million

Option Term Sheet

Term Sheet Continued

$175,000,000A

Maturity – 30 Years

Fixed 4.75% Rate

Coverage Ratio – 1.2 Times

• Level Sinking Fund Payments

Security

Assignment of 40-Year Land Lease

Deed of Trust on Parcel 4

Enterprise Revenue Bond Issue

Term Sheet

Facility: 5-Year Syndicated Revolving Line of Credit

Amount: $600 Million

Purpose: Interim Construction Finance plus Interest Reserve

Repayment Source :

Primary : Permanent 20-Year Take-Out by Insurer for $320 Million (80% LTV)

Secondary: Proceeds From Sale of Condos &Lease Income From Office And Retail Space

Tertiary : Enterprise Revenue Bond

Pricing: Libor + 2.0% *

Security:

• Deed of Trust on Reunion Park

• Assignment of Lease Proceeds

* Based on 5-Year Libor Swaps (1.134%) plus a spread of 200 bps, the estimated fixed cost

of funds is 3.5% , including the net cost of selling an interest rate floor against buying an

interest rate cap.

| Interim Construction Financing |

Unlevered Return

INTERIM CONSTRUCTION FINANCE UTILIZATION

Year 1 Year 2 Year 3 Year 4 Year 5

Operating Cash Flow

Lease Revenue $0.00 $0.00 $0.00 $42,075,810 $84,038,640

Operating Expense $0.00 $0.00 $0.00 -$38,221,666 -$76,340,701

Land Lease Option Fees $10,800,000 $7,128,000

Total Operating Cash Flow 10,800,000$ -$ -$ 10,982,144$ 7,697,939$

Construction Costs

Phase 1 (Central Development) $91,930,053 $91,930,053 $91,930,053 $91,930,053

Phase 2 (East Side Development) $42,861,500 $42,861,500

Phase 3 (West Side Development) $16,814,500 $16,814,500

Phase 4 (West Side Develoment)

Total $91,930,053 $91,930,053 $151,606,053 $151,606,053 $0

Total (91,930,053)$ (91,930,053)$ (151,606,053)$ (151,606,053)$ -$

ICF UTILIZATION

Phase 1 (Central Development) 91,930,053$ 91,930,053$ 91,930,053$ 91,930,053$ (0)$

Phase 2 (East Side Development) -$ -$ 42,861,500$ 42,861,500$

Phase 3 (West Side Development) -$ -$ 16,814,500$ 16,814,500$

Phase 4 (West Side Develoment) -$ -$ -$ -$

TOTAL CONSTRUCTION ADVANCES 91,930,053$ 91,930,053$ 151,606,053$ 151,606,053$ -$

ICF REPAYMENTS (10,800,000)$ -$ (79,560,000)$ (166,134,618)$

Capitalized Interest 1,230,776$ 4,491,405$ 8,910,486$ 14,528,565$

Capitalized Interest Reserve 1,230,776$ 5,722,181$ 14,632,667$ 29,161,232$

TOTAL ICF UTILIZATION 82,360,829$ 178,782,286$ 339,298,825$ (0)$ (0)$

ICF REPAYMENTS (0)$ -$

Operating Cash Flow (10,800,000)$ -$ -$ (10,982,144)$

Phase 1 (Central Development) -$ -$ -$ -$

Phase 2 (East Side Development) -$ -$ -$ -$

Phase 3 (West Side Development) -$ -$ -$ (10,819,200)$

Phase 4 (West Side Develoment) -$ -$

Permanent Take-Out Financing Phase 1 -$ (340,000,000)$

Proceeds of Condo Sales -$ -$ (79,560,000)$ (79,560,000)$

TOTAL ICF REPAYMENTS (10,800,000)$ -$ (79,560,000)$ (166,134,618)$

PROJECT CASH OUT -$ -$ -$ 275,226,727$

5-Year Libor Swap 1.1340%

Spread 1.5000%

Forward Rate Agreement Costs (Amortized) 0.866%

Total Blended Interest Cost 3.5000% Terminal Value: $681,036,835

Unlevered IRR: 7.656%

Outstanding Credit

$ (5 0 )

$ -

$ 50

$ 10 0

$ 15 0

$ 20 0

$ 25 0

$ 30 0

$ 35 0

$ 40 0

1 2 3 4 5

Mil

lio

ns

Yea r

IC F UTILIZATION

* 3% Growth Annual Growth Rate Assumed

ICF UTILIZATION

Phase 1 (Central Development) 91,930,053$ 91,930,053$ 91,930,053$ 91,930,053$ (0)$

Phase 2 (East Side Development) -$ -$ 42,861,500$ 42,861,500$

Phase 3 (West Side Development) -$ -$ 16,814,500$ 16,814,500$

Phase 4 (West Side Develoment) -$ -$ -$ -$

TOTAL CONSTRUCTION ADVANCES 91,930,053$ 91,930,053$ 151,606,053$ 151,606,053$ -$

ICF REPAYMENTS (10,800,000)$ -$ (79,560,000)$ (166,134,618)$

Capitalized Interest 1,230,776$ 4,491,405$ 8,910,486$ 14,528,565$

Capitalized Interest Reserve 1,230,776$ 5,722,181$ 14,632,667$ 29,161,232$

TOTAL ICF UTILIZATION 82,360,829$ 178,782,286$ 339,298,825$ (0)$ (0)$

ICF REPAYMENTS (0)$ -$

Operating Cash Flow (10,800,000)$ -$ -$ (10,982,144)$

Phase 1 (Central Development) -$ -$ -$ -$

Phase 2 (East Side Development) -$ -$ -$ -$

Phase 3 (West Side Development) -$ -$ -$ (10,819,200)$

Phase 4 (West Side Develoment) -$ -$

Permanent Take-Out Financing Phase 1 -$ (340,000,000)$

Proceeds of Condo Sales -$ -$ (79,560,000)$ (79,560,000)$

TOTAL ICF REPAYMENTS (10,800,000)$ -$ (79,560,000)$ (166,134,618)$

PROJECT CASH OUT -$ -$ -$ 275,226,727$

5-Year Libor Swap 1.1340%

Spread 1.5000%

Forward Rate Agreement Costs (Amortized) 0.866%

Total Blended Interest Cost 3.5000%

Interim Construction Financing Utilization Schedule

Financing Schedule

$ -

$ 20

$ 40

$ 60

$ 80

$ 10 0

$ 12 0

$ 14 0

$ 16 0

1 2 3 4

Mil

lio

ns

Yea r

IC F UTILIZATION

* 3% Growth Annual Growth Rate Assumed

ICF UTILIZATION

Phase 1 (Central Development) 91,930,053$ 91,930,053$ 91,930,053$ 91,930,053$ (0)$

Phase 2 (East Side Development) -$ -$ 42,861,500$ 42,861,500$

Phase 3 (West Side Development) -$ -$ 16,814,500$ 16,814,500$

Phase 4 (West Side Develoment) -$ -$ -$ -$

TOTAL CONSTRUCTION ADVANCES 91,930,053$ 91,930,053$ 151,606,053$ 151,606,053$ -$

ICF REPAYMENTS (10,800,000)$ -$ (79,560,000)$ (166,134,618)$

Capitalized Interest 1,230,776$ 4,491,405$ 8,910,486$ 14,528,565$

Capitalized Interest Reserve 1,230,776$ 5,722,181$ 14,632,667$ 29,161,232$

TOTAL ICF UTILIZATION 82,360,829$ 178,782,286$ 339,298,825$ (0)$ (0)$

ICF REPAYMENTS (0)$ -$

Operating Cash Flow (10,800,000)$ -$ -$ (10,982,144)$

Phase 1 (Central Development) -$ -$ -$ -$

Phase 2 (East Side Development) -$ -$ -$ -$

Phase 3 (West Side Development) -$ -$ -$ (10,819,200)$

Phase 4 (West Side Develoment) -$ -$

Permanent Take-Out Financing Phase 1 -$ (340,000,000)$

Proceeds of Condo Sales -$ -$ (79,560,000)$ (79,560,000)$

TOTAL ICF REPAYMENTS (10,800,000)$ -$ (79,560,000)$ (166,134,618)$

PROJECT CASH OUT -$ -$ -$ 275,226,727$

5-Year Libor Swap 1.1340%

Spread 1.5000%

Forward Rate Agreement Costs (Amortized) 0.866%

Total Blended Interest Cost 3.5000%

2 0 .0 0 %

8 0 .0 0 %

C a pit a l St r uc t ur e F in a nc in g

Eq ui t y Debt

3 0 .2 6 % In t er n a l Ra t e o f Ret u r n (L ev er ed )

Capital Structure

37.83%

5:1 Levered Internal Rate of Return

2 0 .0 0 %

8 0 .0 0 %

C a pit a l St r uc t ur e F in a nc in g

Eq ui t y Debt

3 0 .2 6 % In t er n a l Ra t e o f Ret u r n (L ev er ed )

Capital Structure

30.26%

4:1 Levered Internal Rate of Return

2 5 .0 0 %

7 5 .0 0 %

C a pit a l St r uc t ur e F in a nc in g

Eq ui t y Debt

W AC C 7 .5 0 %

Equity 30%

Debt 05%

P r o j ec t ed C a pit a l

Capital $162,051,877

Debt $979,591,193

To t a l C a pit a l C o st

Project $1,088,434,658

The Final Vision

Development Costs $ %

Phase 1 (Central Development) $367,720,211 75.5%

Phase 2 (East Side Development) $85,723,000 17.6%

Phase 3 (West Side Development) $33,629,000 6.9%

Phase 4 (West Side Development) $0 0.0%

Total $487,072,211 100%

Land Development Sq Ft %

Office Space 823,400 49.7%

Retail Space 957,250 57.8%

Green Space 208,900 12.6%

Residential Space 312,000 18.8%

Site Enhancement 120,180 7.3%

2,421,730 146%

Basic Per Foot Analysis $ %

Total Cost Per Square Foot (Land) $294.25

Total Cost Per Square Foot (Space) $201.13

Revenue Per Square Foot $42.63 14.49%

Revenue Analysis (Diversification) $ %

Office Revenue $29,642,400 13.8%

Retail Revenue $52,066,000 24.3%

Residential Revenue $132,350,400 61.8%

Total $214,058,800 100.0%

Gaming Hotel

Floor Rooms Employees

Ballys 225,756 2,000 3,649

Borgata 161,000 2,802 6,025

Caesars 145,000 1,158 3,052

Harrahs 160,000 2,588 3,959

Revel 150,000 1,399 3,333

Showboat 127,978 1,331 2,384

Tropicana 148,000 2,129 2,920

Trump Plaza 91,181 906 1,372

Trump Taj Mahal 167,321 2,248 3,325

Mean 152,915 1,840 3,335

LeReunion Grande 360,000 4,332 7,852

Casino Employees 7,852

Hotel Room Nights 1,264,966

Occupancy 80%

Hotel Avg Rate 100$

Hotel Revenue 126,496,642$

Hotel Occupancy Tax 0.09 11,384,698$

Texas Sales Tax 0.06 7,589,798$

ATLANTIC CITY CASINOS

Phase 1 (Central Development) $367,720,211

2 Skyscraper Office Buildings

Total Square Footage 823,400 $320.00

Number of Floors 56

Number of Parking Spaces (6 Floors Deep) 469

Cost------------------------------------------------ $263,488,000.00

Bike Paths

Length of Bike Path 37,500 $30.00

Cost--------------------------------------------------------------$1,125,000.00

Park ing Garage Renovation

Total Square Footage 134,750 $45.95

Number of Floors 5

Number of Parking Spaces 4,185

Cost---------------------------------------------------- $6,191,250.00

Light Rail Transportation System

Rail System 38,720 $800.00

Bridge 43,960 $1,500.00

$96,915,961.05

Phase 2 (East Side Development) $85,723,000

3 Individual Luxury Apartment Buildings

Total Square Footage 468,000 $132.00

Number of Floors (3 Parking & 6 Living) 9

Number of Parking Spaces 953

Cost---------------------------------------- $61,776,000.00

Central Retail Building

Total Square Footage 189,000 $103.00

Number of Floors 3

Number of Parking Spaces 191

Cost--------------------------------------- $19,467,000.00

Cinema

Total Square Footage 40,000 $112.00

Number of Floors 1

Number of Parking Spaces 191

Cost------------------------------------ $4,480,000.00

Phase 3 (West Side Development) $33,629,000

Reunion Village

Total Square Footage 143,000 $103.00

Number of Floors 2

Number of Parking Spaces -

Cost------------------------------------------ $14,729,000.00

La Reunion Mall

Total Square Footage 135,000 $140.00

Number of Floors 1

Number of Parking Spaces -

Cost---------------------------------------- $18,900,000.00

Phase 4 (West Side Development)

Luxury Casino

Total Square Footage 422,500 $135.00

Number of Floors 3

Number of Parking Spaces 611

Cost----------------------------------------- $57,038,484.47

Total Office Space 823,400

Total Retail Space 957,250

Total Residential Space 312,000

Total Office Space 39.35%

Total Retail Space 45.74%

Total Residential Space 14.91%

2,092,650

Costs & Investments

Total Development Costs $586,389,011

Total Debt Financing $340,474,958

Total Equity Financing $345,230,853

CHECK: TRUE $586,389,011

Article 17: "Mode of amending the Constitution of this State"

Notwithstanding the large number of amendments (and proposed amendments) that the constitution has had since its inception, the only method of amending the constitution prescribed by Article 17 is via the legislature, subject to voter approval. The constitution does not provide for amendment by initiative, constitutional convention, or any other means. A 1974 constitutional convention required the voters to amend the Constitution to add a separate section to this Article; the section was later repealed in 1999.

The section also prescribes specific details for notifying the public of elections to approve amendments. It requires that the legislature publish a notice in officially approved newspapers that briefly summarizes each amendment and shows how each amendment will be described on the ballot. It also requires that the full text of each amendment be posted at each county courthouse at least 50 days (but no sooner than 60 days) before the election date.

Once an amendment passes it is compiled into the existing framework (i.e., text is either added or deleted), unlike the United States Constitution.

ICF

INTERIM CONSTRUCTION FINANCE UTILIZATION

Year 1 Year 2 Year 3 Year 4 Year 5

Operating Cash Flow

Lease Revenue $0.00 $0.00 $0.00 $42,075,810 $84,038,640

Operating Expense $0.00 $0.00 $0.00 -$38,221,666 -$76,340,701

Land Lease Option Fees $10,800,000 $7,128,000

Total Operating Cash Flow 10,800,000$ -$ -$ 10,982,144$ 7,697,939$

Construction Costs

Phase 1 (Central Development) $91,930,053 $91,930,053 $91,930,053 $91,930,053

Phase 2 (East Side Development) $42,861,500 $42,861,500

Phase 3 (West Side Development) $16,814,500 $16,814,500

Phase 4 (West Side Develoment)

Total $91,930,053 $91,930,053 $151,606,053 $151,606,053 $0

Total (91,930,053)$ (91,930,053)$ (151,606,053)$ (151,606,053)$ -$

ICF UTILIZATION

Phase 1 (Central Development) 91,930,053$ 91,930,053$ 91,930,053$ 91,930,053$ (0)$

Phase 2 (East Side Development) -$ -$ 42,861,500$ 42,861,500$

Phase 3 (West Side Development) -$ -$ 16,814,500$ 16,814,500$

Phase 4 (West Side Develoment) -$ -$ -$ -$

TOTAL CONSTRUCTION ADVANCES 91,930,053$ 91,930,053$ 151,606,053$ 151,606,053$ -$

ICF REPAYMENTS (10,800,000)$ -$ (79,560,000)$ (166,134,618)$

Capitalized Interest 1,230,776$ 4,491,405$ 8,910,486$ 14,528,565$

Capitalized Interest Reserve 1,230,776$ 5,722,181$ 14,632,667$ 29,161,232$

TOTAL ICF UTILIZATION 82,360,829$ 178,782,286$ 339,298,825$ (0)$ (0)$

ICF REPAYMENTS (0)$ -$

Operating Cash Flow (10,800,000)$ -$ -$ (10,982,144)$

Phase 1 (Central Development) -$ -$ -$ -$

Phase 2 (East Side Development) -$ -$ -$ -$

Phase 3 (West Side Development) -$ -$ -$ (10,819,200)$

Phase 4 (West Side Develoment) -$ -$

Permanent Take-Out Financing Phase 1 -$ (340,000,000)$

Proceeds of Condo Sales -$ -$ (79,560,000)$ (79,560,000)$

TOTAL ICF REPAYMENTS (10,800,000)$ -$ (79,560,000)$ (166,134,618)$

PROJECT CASH OUT -$ -$ -$ 275,226,727$

5-Year Libor Swap 1.1340%

Spread 1.5000%

Forward Rate Agreement Costs (Amortized) 0.866%

Total Blended Interest Cost 3.5000%

Term Sheet

Facility: 5-Year Syndicated Revolving Line of Credit

Amount: $600 Million

Purpose: Interim Construction Finance plus Interest Reserve

Repayment Source :

Primary : Permanent 20-Year Take-Out by Insurer for $320 Million (80% LTV)

Secondary: Proceeds From Sale of Condos &Lease Income From Office And Retail Space

Tertiary : Enterprise Revenue Bond

Pricing: Libor + 2.5% *

Security:

• Deed of Trust on Reunion Park

• Assignment of Lease Proceeds

* Based on 5-Year Libor Swaps (1.134%) plus a spread of 250 bps, the estimated fixed cost

of funds is 4.0% , including the net cost of selling an interest rate floor against buying an

interest rate cap.

| Interim Construction Financing |