nailing jell-o® to the wall: choice of form and structure

TRANSCRIPT

Online CLE

Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1.25 General CLE credits

From the Oregon State Bar CLE seminar 18th Annual Oregon Tax Institute, presented on June 7 and 8, 2018

© 2018 Robert Keatinge. All rights reserved.

ii

Chapter 1

Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA—Presentation Slides

RobeRt Keatinge

Holland & Hart LLPDenver, Colorado

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–ii18th Annual Oregon Tax Institute

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–118th Annual Oregon Tax Institute

NAILING JELL-O® TO THE WALL: CHOICE OF FORM AND STRUCTURE AFTER TCJA

ROBERT KEATINGEHOLLAND & HART LLP

[email protected]/295-8595

TUESDAY, JUNE 7, 2018

18TH ANNUAL OREGON TAX INSTITUTE

DISCLAIMERTHIS PRESENTATION IS FOR EDUCATIONAL AND INFORMATIONAL PURPOSES ONLY AND , BY MEANS OF THIS PRESENTATION, NONE OF THE AUTHORS, PRESENTERS OR SPONSORS ARE RENDERING ACCOUNTING, BUSINESS, FINANCIAL, INVESTMENT, LEGAL, TAX, OR OTHER PROFESSIONAL ADVICE OR SERVICES. THIS PRESENTATION IS NOT A SUBSTITUTE FOR PROFESSIONAL ADVICE OR SERVICES, AND SHOULD NOT BE USED AS A BASIS FOR ANY DECISION OR ACTION THAT MAY AFFECT YOUR BUSINESS, LEGAL OR TAX SITUATION. LIGHT OF THE COMPLEXITY AND THE RAPIDLY CHANGING AND INCOMPLETE STATE OF THE LAW, BEFORE MAKING ANY DECISION OR TAKING ANY ACTION THAT MAY AFFECT YOU, YOU SHOULD CONSULT A QUALIFIED PROFESSIONAL ADVISOR. NONE OF THE AUTHORS, PRESENTERS, OR SPONSORS SHALL BE RESPONSIBLE FOR ANY LOSS SUSTAINED BY ANY PERSON WHO RELIES ON THIS PRESENTATION.

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–218th Annual Oregon Tax Institute

3

Allows “the Finance Committee to reduce revenues and change outlays to increase the deficit by not more than $1.5 trillion over the next 10 years.”

U.S. Senate Committee on the Budget Summary FY 2018 Budget Resolution

INTRODUCTION TO THE TCJA

4

• November 16, 2017: House draft passed.• December 2, 2017: Senate draft passed.• December 15, 2017: Joint Committee and Explanation (Report 115-

466) released.• December 20, 2017: Senate modified Conference Committee bill

and House concurred.• December 22, 2017: TCJA (P.L. 115-97) enacted.• January 1, 2018: TCJA effective.• March 22, 2018 Joint Committee on Taxation, Technical Explanation

of the Revenue Provisions of the House Amendment to the Senate Amendment to H.R. 1625 (Rules Committee Print 115-66), (JCX-6-18), March 22, 2018 (“JCT CAA Report”)

• March 23, 2018: Consolidated Appropriations Act(“CAA”) (P.L. 115-141) enacted.

ENACTMENT OF THE TCJA

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–318th Annual Oregon Tax Institute

5

• Many of the provisions of the TCJA (noted in this outline as “Temporary”) are effective only until December 31, 2025.

• Under the TCJA, many of the indexed provisions will be indexed using the Chained Consumer Price Index for All Urban Consumers (“C-CPI-U”), which increases more slowly than does the CPI traditionally used.

TCJA GENERAL PROVISIONS

6

• Compensatory taxes including (SECA/FICA/NII).

• Classification rules.• Partnership audit rules – but the

CAA Added new “pull-in” alternative procedures and other changes.

SOME ITEMS NOT MODIFIED BY TCJA

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–418th Annual Oregon Tax Institute

7

• Individual rate structure.

• Disallowance of deductions for unreimbursed employee business expenses.

• Carried interest changes.

• New Section 199A deduction.

• Corporate rate structure.

TCJA TOPICS THAT WILL BE DISCUSSED

8

• Capital expensing rules.

• Specific reduction or elimination of some deductions (including state taxes).

• Modification of interest deductions.

• Change in net operating loss rules.

• Estate tax changes.

• Changes in individual alternative minimum tax.

• International provisions.

• The application of the Pass-Thru deductions to REITs, qualified publicly traded partnerships, or cooperatives.

SOME TCJA TOPICS THAT WILL NOT BE DISCUSSED

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–518th Annual Oregon Tax Institute

9

Marginal Tax Rates [Married Filing Jointly]

TCJA TAX RATES FOR ORDINARY INCOME (Temporary)

Taxable Income 2018 without TCJA 2018 (TCJA)

$0 to $19,050 10% 10%

$19,050.01 to $ 77,400 15% 12%

$77,400.01 to $156,150 25% 22%

$156,150.01 to $165,000 28%

$165,00.01 to $237,950 24%

$233,350.01 to $315,000 33%

$315,001 to $400,000 32%

$400,000.01 to $424,950 35%

$424,950.01 to $480,050 35%

$480,050.01 to $600,000 39.6%

Over $600,000 37%

10

Marginal Tax Rates [Single]

TCJA TAX RATES FOR ORDINARY INCOME (Temporary)

Taxable Income 2018 without TCJA 2018 (TCJA)

$0 to $9,525 10% 10%

$9,525.01 to $38,700 15% 12%

$38,700.01 to $82,500 25% 22%

$82,500.01 to $ 93,700 24%

$93,700.01 to $157,500 28%

$157,500.01 to $195,450 32%

$195,450.01 to $200,000 33%

$200,000.01 to $424,950 35%

$425,950.01 to $426,700 35%

$426,700.01 to $500,000 39.6%

Over $500,000 37%

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–618th Annual Oregon Tax Institute

11

• Capital Gains Rates terminology modified but rates are unchanged from 2017:

• Unrecaptured section IRC § 1250 gain continues to be taxed at a maximum rate of 25%, and 28% rate gain at a maximum rate of 28%.

• Self-Created Property (patents, models, designs, secret formulae or processes) are no longer capital assets or IRC § 1231 property.

INDIVIDUAL CAPITAL GAINS UNDER TCJA

Tax Rate on net capital gain

Taxable Income (including adjusted capital gain)Married

filing jointlyHead of

householdOther

individualsEstate or

trust0% ≤ $77,200 ≤ $51,700 ≤ $38,600 ≤$2,60015% (maximum zero rate amount)

$77,200 < and

≤$479,000

$77,200 < and

≤$452,400

$38,600 < and ≤$239,500

$2,600 < and

≤$12,70020% (maximum 15-percent rate amount)

>479,000 >$ 452,400 > $239,500 >$ 12,700

12

For pre-2018 tax years:• Taxable Income = Adjusted Gross Income

reduced by the sum of:• Personal Exemptions, and• Either:

• Standard Deductions, or• Itemized Deductions.

• Itemized deductions of married filing jointly were phased out for adjusted gross income over $318,200.

PRE -2018 TAXABLE INCOME

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–718th Annual Oregon Tax Institute

13

Under TCJA:Taxable Income = Adjusted Gross Income reduced by either:• Standard Deductions, or• Itemized Deductions.

TCJA TAXABLE INCOME (Temporary)

14

Under pre-2018 law, personal exemptions of $4,050 for each spouse and dependent and for the “aged and blind” were allowed but were phased out at higher income levels:

PRE-2018 PERSONAL EXEMPTIONS

Filing Status Phaseout RangeMarried Filing Jointly $313,800 to $436,300

Married Filing Separately $156,900 to $218,150

Single $261,500 to $384,00

Head of Household $ 287,650 to $410,150

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–818th Annual Oregon Tax Institute

15

Under TCJA personal and dependent exemptions are eliminated.

TCJA PERSONAL EXEMPTIONS (Temporary)

16

Under pre-2018 law individual taxpayers filing jointly were entitled to standard deduction as follows:

PRE-2018 STANDARD DEDUCTIONS

Filing Status Standard DeductionMarried Filing Jointly $12,700

Married Filing Separately $6,350

Single $6,350Head of Household $9,350

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–918th Annual Oregon Tax Institute

17

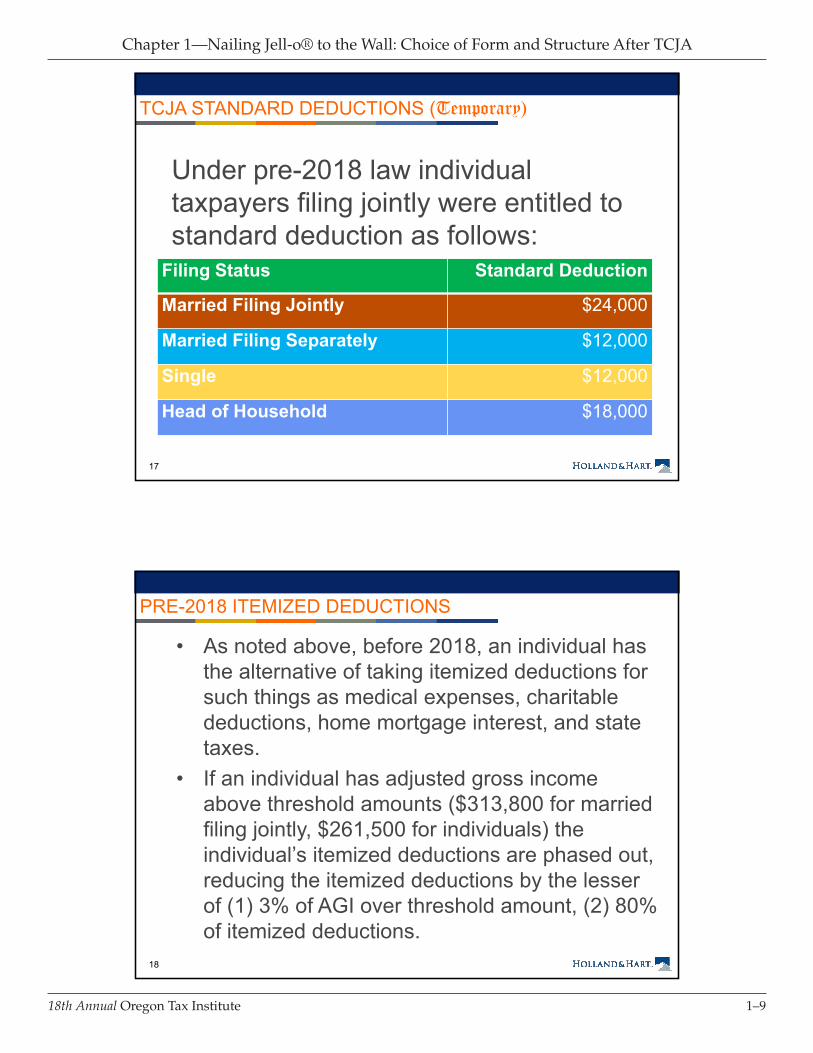

Under pre-2018 law individual taxpayers filing jointly were entitled to standard deduction as follows:

TCJA STANDARD DEDUCTIONS (Temporary)

Filing Status Standard Deduction

Married Filing Jointly $24,000

Married Filing Separately $12,000

Single $12,000

Head of Household $18,000

18

• As noted above, before 2018, an individual has the alternative of taking itemized deductions for such things as medical expenses, charitable deductions, home mortgage interest, and state taxes.

• If an individual has adjusted gross income above threshold amounts ($313,800 for married filing jointly, $261,500 for individuals) the individual’s itemized deductions are phased out, reducing the itemized deductions by the lesser of (1) 3% of AGI over threshold amount, (2) 80% of itemized deductions.

PRE-2018 ITEMIZED DEDUCTIONS

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–1018th Annual Oregon Tax Institute

19

• Many itemized deductions have been eliminated or reduced – including state taxes (limited), unreimbursed employee business expenses (eliminated), and IRC § 212 (investment expenses) (eliminated).

• Even where the itemized deduction is not eliminated or denied, it may be less useful for many middle-income taxpayers (e.g., taxpayer having allowable itemized deductions of less than the standard deduction will not be able to use them.

• For upper income taxpayers, the phase-out of the itemized deductions has been repealed.

TCJA ITEMIZED DEDUCTIONS (Temporary)

20

Under administrative guidance, a partner who receives a “profits” interest in a partnership in exchange for services rendered to a partnership does not recognize gain on the receipt subject to certain exceptions. Upon disposition of the partnership interest after holding it for one year the gain is taxable under the favorable net capital gains rules.

PRE-2018 CARRIED INTEREST

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–1118th Annual Oregon Tax Institute

21

A partner in an “applicable partnership” (one engaged in: “(1) raising or returning capital, and either (2) investing in (or disposing of) specified assets (or identifying specified assets for investing or disposition), or (3) developing specified assets”) who receives a “profits” interest in a partnership in exchange for services rendered to a partnership does not recognize gain on the receipt subject to certain exceptions. Upon disposition of the partnership interest after holding it for less than three years the gain is taxable as short-term capital gains rules (i.e., subject to ordinary income rates).

TCIJA CARRIED INTEREST

22

• Applicable Partnership Interest is “a partnership which, directly or indirectly, is transferred to (or is held by) the taxpayer in connection with the performance of substantial services by the taxpayer, or any other related person, in any applicable trade or business.”

• Applicable Trade or Business is an “activity conducted on a regular, continuous, and substantial basis which, regardless of whether the activity is conducted in one or more entities, consists, in whole or in part, of— raising or returning capital, and either— investing in (or disposing of) specified assets (or identifying specified assets for such investing or disposition), or developing specified assets.”

• Specified Assets are “securities, commodities, real estate held for rental or investment, cash or cash equivalents, options or derivative contracts with respect to any of the foregoing, and an interest in a partnership to the extent of the partnership's proportionate interest in any of the foregoing.”

TCIJA CARRIED INTEREST DEFINED TERMS

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–1218th Annual Oregon Tax Institute

23

The new carried interest provisions do not apply to:• “[A]ny partnership interest owned directly or

indirectly by a [C] corporation.” (Notice 2018-18)• Any “capital interest in the partnership which

provides the taxpayer with a right to share in partnership capital commensurate with— the amount of capital contributed (determined at the time of receipt of such partnership interest), or the value of such interest subject to tax under section 83 upon the receipt or vesting of such interest.”

TCIJA CARRIED INTEREST EXCEPTIONS

24

• Under new IRC § 199A, an individual who is an owner of a “pass-thru” activity that is a Qualified Trade or Business is entitled to a deduction (the “Pass-Thru Deduction”).

• Replaces the “qualified production activities” deduction under IRC §199.

PASS-THRU DEDUCTION (Temporary)

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–1318th Annual Oregon Tax Institute

25

The Pass-Thru Deduction works differently for individual taxpayers with taxable income:• below the “threshold amount,”• above the threshold amount

and below “the phase-in” amount

• above the phase-in amount

PASS-THRU DEDUCTION (Temporary)

26

• The threshold amount (IRC § 199A(e)(2)(A)) and phase-in limitations are subject to adjustment for inflation (IRC § 199A(e)(2)(B))

• The phase-in limitations (IRC §§ 199A(b)(3)(B)(ii) and 199A(d)(2)(B) amount continue to be $50,000 ($100,000 in the case of a joint return). Between the threshold amount and the phase-in limitation, the limitations on the pass-thru deduction are phased in arithmetically.

THRESHOLD AMOUNT (Temporary)

Filing status Threshold amount

Phase-in complete

Married filing jointly $315,000 $415,000All other individuals $157,500 $207,500

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–1418th Annual Oregon Tax Institute

27

A “qualified business activity” is a trade or busines that is conducted by the individual taxpayer through a “pass-thru entity” (generally an entity other than a C corporation) which may be :1. Partnership,2. S corporation, or3. Sole proprietorship (including one

conducted by an individual through a disregarded entity).

[Note: Special rules and alternative definitions apply in the case of certain REITs, publicly traded partnerships and cooperatives that are not discussed here.]

QUALIFIED BUSINESS ACTIVITY (BELOW THRESHOLD)

28

An individual may deduct:(1) the lesser of:

1. The qualified business income amount from an activity(“QBI”), or

2. 20% (taxable income less net capital gains).

Plus(2) the lesser of:

1. 20% (qualified cooperative dividends, or2. taxable income (less net capital gains).

AMOUNT OF PASS-THRU DEDUCTION (BELOW THRESHOLD)

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–1518th Annual Oregon Tax Institute

29

Qualified Business Income is the net amount of qualified items of income, gain, deduction, and loss with respect to a qualified trade or business (including carryovers of losses from qualified trades of businesses). QBI must be effectively to a U.S. Trade or business.

IRC §199A(c)(1)

QBI (BELOW THRESHOLD)

30

QBI does not include:• Capital gains or losses, dividends, interest (other than

that allocable to trade of business), and certain other investment income.

• Qualified REIT dividends, qualified cooperative dividends, or qualified publicly traded partnership income

• Amounts constituting “reasonable compensation,” guaranteed payments for services to partners or other payments to partners other than in their capacity as partners.

• Certain investment income

ITEMS EXCLUDED FROM QBI

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–1618th Annual Oregon Tax Institute

31

• IRC § 199A(c)(4)(A)(A) (“Qualified business income shall not include — reasonable compensation paid to the taxpayer by any qualified trade or business of the taxpayer for services rendered with respect to the trade or business . . .”).

• Report 115-466 Page 215 and the JCT CAA Report at page 15 (“Qualified business income does not include any amount paid by an S corporation that is treated as reasonable compensation of the taxpayer.”).

QBI (“EXCLUSION OF REASONABLE COMPENSATION”)

32

An individual may deduct:(1) the lesser of:

1. The combined qualified business income amount from an activity(“CQBI”), or

2. 20% (taxable income less net capital gains).

Plus(2) the lesser of:

1. 20% (qualified cooperative dividends, or2. taxable income (less net capital gains).

AMOUNT OF PASS-THRU DEDUCTION (ABOVE THRESHOLD)

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–1718th Annual Oregon Tax Institute

33

Combined Qualified Business Income is the lesser of:

(1) the QBI determined using a different definition of Qualified Trade or Business, or

(2) the W-2 Wages and Capital Limitation (“WWCL”).

CQBI (ABOVE THRESHOLD)

34

A Qualified Trade or Business is any trade or business other than:• the trade or business of being

an employee or • a specified trade or business

(“SSBI”). IRC §199A(d)(1)

QUALIFIED TRADE OR BUSINESS (ABOVE THE THRESHOLD)

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–1818th Annual Oregon Tax Institute

35

• Any trade or business involving the performance of services in the fields of health, law, engineering, architecture, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, including investing and investment management, trading, or dealing in securities, partnership interests, or commodities, and any trade or business where the principal asset of such trade or business is the reputation or skill of one or more of its employees.

• Architects and Engineers were expressly eliminated from this list.

IRC §199A(d)(2)

SPECIFIED SERVICE TRADE OR BUSINESS (“SSTB”)

36

The WWCL is the greater of:1. 50% of the “W-2 Wages” paid with

respect to the QTB, or2. 25% of the W-2 Wages paid with

respect to the QTB plus 2.5% of the unadjusted basis, immediately after acquisition of all “qualified property.”

IRC §199A(b)((2)(B)

W-2 WAGES AND CAPITAL LIMITATION (ABOVE THE THRESHOLD)

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–1918th Annual Oregon Tax Institute

37

With respect to any QTB, the total wages subject to wage withholding, elective deferrals, and deferred compensation paid by the QTB with respect to employment of its employees only will be W-2 Wages only if:1. The amounts are wages as described in IRC

§3401(a) or elective deferrals, and2. The amounts are properly included in a return

filed with the Social Security Administration on or before the 60th day after the due date (including extensions) for such return.

WWCL: W-2 WAGES (ABOVE THE THRESHOLD)

38

Qualified property is:• tangible property,• of a character subject to depreciation,• held by, and available for use in, the QTB at

the close of the taxable year, • used in the production of QBI, and • property for which the depreciable period

(beginning on acquisition and ending on the later of 10 years or IRC § 168 period (disregarding IRC § 168(g)) not ended before the close of the taxable year.

WWCL: QUALIFIED PROPERTY.

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–2018th Annual Oregon Tax Institute

39

The exclusion of an SSTB from the definition of a QTB and the WWCL phases in for a taxpayer with taxable income in excess over the Phase in amount • The Threshold Amount is $157,500 ($315,000

in the case of a joint return) indexed for inflation.

• The exclusion of an SSTB from the definition of QTB and the WWCL is fully phased in for a taxpayer with taxable income in excess of the threshold amount of $207,500 ($415,000 in the case of a joint return).

PHASE-IN OF SSTB AND WWCL LIMITATIONS (ABOVE THE THRESHOLD)

40

• The IRC § 199A deduction is a reduction in taxable income not adjusted gross income.

• The conference Committee Report notes: “Thus, for example, the provision does not affect limitations based on adjusted gross income. Similarly the conference agreement clarifies that the deduction is available to both non-itemizers and itemizers.”

IRC § 199A DEDUCTION REDUCES TI NOT AGI

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–2118th Annual Oregon Tax Institute

41

NET EFFECTIVE RATE AFTER 199A DEDUCTION

Marginal Income Tax Rate Before 199A

Deduction

Marginal Income Tax Rate After 199A

Deduction

10% 8.0%12% 9.6%22% 17.6%24% 19.2%32% 25.6%35% 28%37% 29.6%

42

Because the 3.8% IRC § 1401 (Self-Employment Tax) or IRC § 1411 (Unearned Income Medicare Contribution Tax (a/k/a Net Investment Income (“NII”) Tax are imposed under Chapter 2 of the Internal Revenue Code and IRC § 199A(f)(3) provides that the IRC § 199A deduction is only allowed for “this chapter,” he IRC § 199A deduction does not apply for purposes of computing the Self-Employment or NII Taxes.

199A DEDUCTION AND SELF-EMPLOYMENT AND NII TAX

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–2218th Annual Oregon Tax Institute

43

TCJA C CORPORATION RATES

Pre-2018 TCJAOrdinary

Corporations(Marginal)

Personal Service

Corporations

All Corporations

$0 to $50,000 15% 35% 21%$50,000.01 to $75,000 25%$75,000.01 to $100,000 34%$100,000.01 to $335,000 39%$335,000.01 to $10,000,000 34%$10,000,000.01 to$15,000,000

35%

$15,000,000.01 to$18,333,333

38%

Over $18,333,333 35%

44

• The corporate alternative minimum tax is repealed effective January 1, 2018.

• Unused corporate minimum tax credit may be:

• Refundable over tax years beginning in 2018 through .

• May be used in lieu of bonus depreciation.• May be used before 2022 to offset “built-in gain”

tax if the corporation converts to an S corporation.

CORPORATE ALTERNATIVE MINIMUM TAX

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–2318th Annual Oregon Tax Institute

45

IRC sections designed to prevent retention of corporate earnings for the avoidance of double taxation may apply:• Accumulated Earnings Tax (IRC §§ 531- 537)

imposes a 20% tax on retained earnings in excess of the reasonable needs of the business.

• Personal Holding Company Tax (IRC §§ 541-547) imposes a 20% tax on undistributed personal holding company income (generally rents, dividends and royalties).

SPECIAL CONCERNS WITH RETENTION OF EARNINGS

46

The following examples demonstrate the operation of the rates before and after the TCJA. This result is quasi-Temporary (Corporate rates are permanent but individual rates may change):They assume income of $100 and: • Corporations are not subject to IRC §§ 531 or 541

taxes.• HI taxes are (including the .9% ACA taxes) reduce the

net amount received by the individual • Individuals are subject to the top marginal rate

applies and that the AMT does not apply. • All income from partnership (or S corporation or sole

proprietorship): (1) is not subject to WWCL or SSTB limitations, and (2) is subject to NII or SECA.

EXAMPLES

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–2418th Annual Oregon Tax Institute

47

If a C corporation pays the entire amount of income as deductible compensation (and thus, has no corporate level income tax) and the individual reports and is taxed on the compensatory payment (after deducting income and HI taxes), the after-tax cash in shareholder’s hands is $58.05 for an effective rate of 43.40%:$100 - $43.40 ($39.60(income tax) + $3.80 (HI)) = $56.60.

EXAMPLE (1): PRE-TCJA CORPORATION PAYS DEDUCTIBLE COMPENSATION

48

If a C corporation pays the entire amount of income as deductible compensation (and thus, has no corporate level income tax) and the individual reports and is taxed on the compensatory payment (after deducting income and HI taxes) the after-tax cash in shareholder’s hands is $59.20 for an effective rate of 40.8%:$100 - $40.80 ($37(income tax) + $3.80 (HI)) = $59.20.

EXAMPLE (2): TCJA CORPORATION PAYS DEDUCTIBLE COMPENSATION

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–2518th Annual Oregon Tax Institute

49

If a C corporation pays tax on the income and distributes the after tax cash to the shareholder as a dividend, the after tax cash in the shareholder’s hands is $49.53 for an effective rate of 50.47%:$100 - $35(corporate income tax) = $65 (distributed) - $15.47 ($13.00 [income tax on dividends @ 20%]+ $2.47 [NII of 3.8% x $65]) = $49.53

EXAMPLE (3): PRE-TCJA C CORPORATION MAKES DIVIDEND PAYMENT

50

If a C corporation pays tax on the income and distributes the after tax cash to the shareholder as a dividend, the after tax cash in the shareholder’s hands is $60.20 for an effective rate of 39.8%:

$100 - $21(corporate income tax) = $79 (distributed) - $18.80 ($15.80 [income tax on dividends @ 20%]+ $3.00 [NII of 3.8% x $65]) = $60.20 (Effective rate)

EXAMPLE (4): TCJA C CORPORATION MAKES DIVIDEND PAYMENT

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–2618th Annual Oregon Tax Institute

51

If a C corporation pays tax on the income and the shareholder subsequently disposes of the stock in the corporation in a transaction qualifying under IRC § 1202, the after tax cash in the shareholder’s hands is $65.00 for an effective rate of 35%:

$100 - $35(corporate income tax) = assets (or cash) of $65.00 in the corporation (assuming no discounts for a stock sale, on the sale of the stock for $65.00 (tax-free under IRC § 1202).

EXAMPLE (5): PRE-TCJA CORPORATION RETAINS INCOME AND SELLS STOCK

52

If a C corporation pays tax on the income and the shareholder subsequently disposes of the stock in the corporation in a transaction qualifying under IRC § 1202, the after tax cash in the shareholder’s hands is $79.00 for an effective rate of 21%:

$100 - $21(corporate income tax) = assets (or cash) of $79.00 in the corporation (assuming no discounts for a stock sale, on the sale of the stock for $79.00 (tax-free under IRC § 1202).

EXAMPLE (6): TCJA CORPORATION RETAINS INCOME AND SELLS STOCK

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–2718th Annual Oregon Tax Institute

53

The partnership will not be taxed on the partnership income. The after tax cash in the hands of an individual partner is $57.17 for an effective rate of 42.8%:

$100 – 42.83 ($39.03 [39.6% x $98.55 {$100 - $1.45 per IRC § 164(f)(1)}] + $3.80 [SECA HI taxes]) = $57.17.

EXAMPLE (7) PRE-TCJA PARTNERSHIP

54

The partnership will not be taxed on the partnership income. The after tax cash in the hands of an individual partner is $59.74 for an effective rate of 40.26%:

$100 – 40.26 ($36.46 [37% x $98.55 {$100 - $1.45 per IRC § 164(f)(1)}] + $3.80 [SECA HI taxes]) = $59.74.

EXAMPLE (8) TCJA PARTNERSHIP W/O 199A DEDUCTION

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–2818th Annual Oregon Tax Institute

55

Under the pre-TCJA rates, if a partnership has income of $100. it will not be taxed to the partnership.An individual partner will take the income into account at rates up to 37% on the income less $ 1.45 (1/2 of 2.9%) IRC §164(h) for a total income tax of $36.46 plus SECA of $3.80 for a net effective tax rate of 42.26%.

TCJA PARTNERSHIP EARNS INCOME

56

Under the TCJA rates, if a partnership has income of $100. it will not be taxed to the partnership.An individual partner will take the income into account at rates up to 37% on the income less $ 1.45 (1/2 of 2.9%) IRC §164(h) and $20.00 for a total income tax of $29.06 plus SECA of $3.80 for a net effective tax rate of 32.86%.

TCJA PARTNERSHIP EARNS INCOME WITH 199A DEDUCTION

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–2918th Annual Oregon Tax Institute

57

In each case, the ultimate choice of entity and structure will turn on the legal, tax an business consideration of each business objectives of the client (including tax efficiency, flexibility of management, limitation on liability, regulatory requirements, and many others). The TCJA modifies many of the Federal tax metrics of the choice.

HOW THE TCJA AFFECTS ENTITY CHOICE AND OPERATION

58

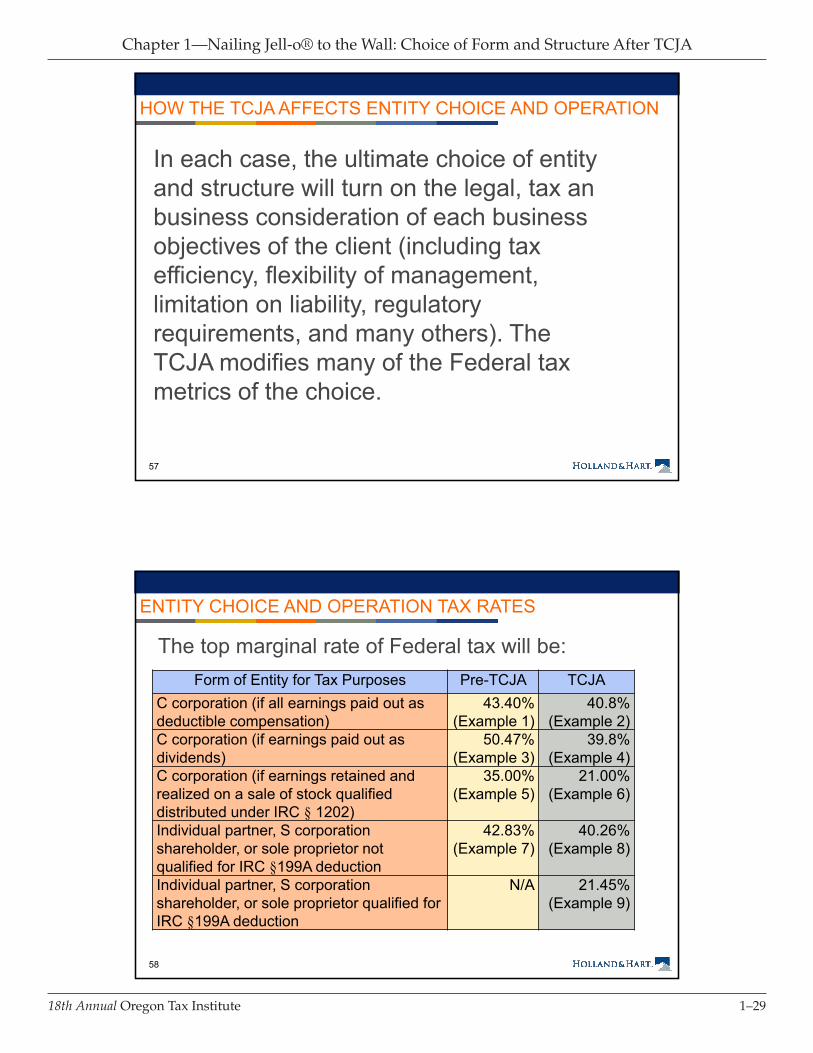

The top marginal rate of Federal tax will be:

ENTITY CHOICE AND OPERATION TAX RATES

Form of Entity for Tax Purposes Pre-TCJA TCJAC corporation (if all earnings paid out as deductible compensation)

43.40%(Example 1)

40.8%(Example 2)

C corporation (if earnings paid out as dividends)

50.47%(Example 3)

39.8%(Example 4)

C corporation (if earnings retained and realized on a sale of stock qualified distributed under IRC § 1202)

35.00%(Example 5)

21.00%(Example 6)

Individual partner, S corporation shareholder, or sole proprietor not qualified for IRC §199A deduction

42.83%(Example 7)

40.26%(Example 8)

Individual partner, S corporation shareholder, or sole proprietor qualified for IRC §199A deduction

N/A 21.45%(Example 9)

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–3018th Annual Oregon Tax Institute

59

The effect of the TCJA on entity selection and operation will turn on several considerations:• The nature of the business.• The ability of the business and owners to leave funds

in the business.• The taxable income of the owners.• The type of activities conducted by the business.• The amount of capital in the business.• The length of time the owners are willing to leave

capital in the business

HOW THE TCJA AFFECTS ENTITY CHOICE AND OPERATION

60

Personal Service Business:

• The reduction of the corporate rates makes a personal services C corporation less expensive but it is not entitled to IRC § 1202 exclusion.

• A personal services organization is an SSTB and owners with taxable income above the threshold will not be entitled to the IRC §199A deduction.

ENTITY CHOICE: NATURE OF BUSINESS

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–3118th Annual Oregon Tax Institute

61

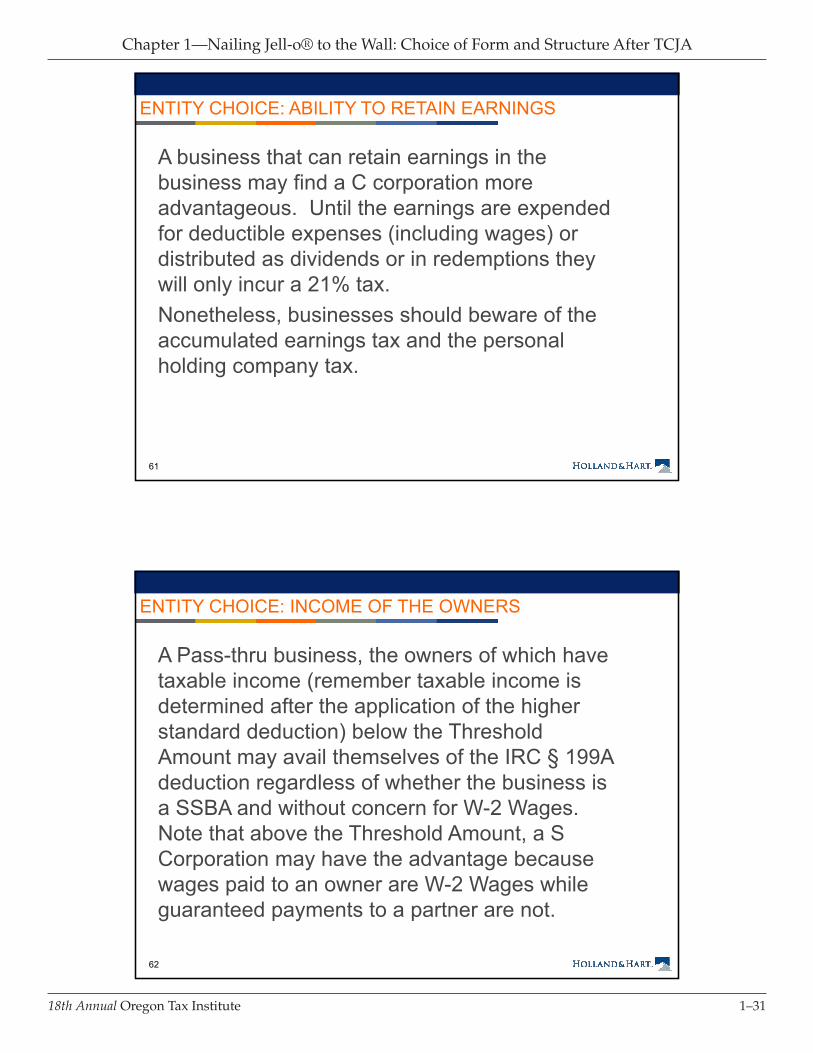

A business that can retain earnings in the business may find a C corporation more advantageous. Until the earnings are expended for deductible expenses (including wages) or distributed as dividends or in redemptions they will only incur a 21% tax. Nonetheless, businesses should beware of the accumulated earnings tax and the personal holding company tax.

ENTITY CHOICE: ABILITY TO RETAIN EARNINGS

62

A Pass-thru business, the owners of which have taxable income (remember taxable income is determined after the application of the higher standard deduction) below the Threshold Amount may avail themselves of the IRC § 199A deduction regardless of whether the business is a SSBA and without concern for W-2 Wages. Note that above the Threshold Amount, a S Corporation may have the advantage because wages paid to an owner are W-2 Wages while guaranteed payments to a partner are not.

ENTITY CHOICE: INCOME OF THE OWNERS

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–3218th Annual Oregon Tax Institute

63

Personal service businesses (specified service trades or businesses) are disfavored for purposes of the IRC § 199A deduction of owners above the Threshold Amount.Most service businesses conducted in C corporations are not entitled to the exclusion under IRC § 1202.In either case, it may be appropriate to separate the service business activity from the other business activities.

ENTITY CHOICE: TYPE OF BUSINESS ACTIVITIES

64

Partners, or in the case of an SSTB those partners with taxable income below the Threshold Amount, being able to characterize them as partners rather than employees may reduce taxes for them (and allow them to deduct unreimbursed expenses) without cost to those with taxable income above the Threshold Amount, as they would not benefit from W-2 Wages.

ENTITY CHOICE: PARTNER V. EMPLOYEE

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–3318th Annual Oregon Tax Institute

65

• For a pass-thru business having significant capital assets, the alternative combination of 25% of W-2 Wages and plus 2.5% of the unadjusted basis immediately after acquisition of qualified property test may be available.

• Because the rule requiring a corporation to recognize gain on the respect to distribution of appreciated property has not been modified, the new expensing rules may exacerbate the potential recognition of gain in a C or S corporation.

ENTITY CHOICE: AMOUNT OF CAPITAL IN THE BUSINESS

66

• In a business that can afford to retain capital and can avoid the anti-retention provisions (accumulated earnings tax and personal holding company tax), it may be possible to limit the tax burden to the 21% corporate rate (plus the state tax rates), particularly if the owner can dispose of the stock in a transaction that complies with IRC § 1202 or, to a lesser extent, a tax-free reorganization.

• The owner should consider the lack of flexibility (or at least the tax cost) in modifying the investment if necessary.

ENTITY CHOICE: THE PATIENCE OF THE OWNERS

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–3418th Annual Oregon Tax Institute

67

QUESTIONS

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–3518th Annual Oregon Tax Institute

Chapter 1—Nailing Jell-o® to the Wall: Choice of Form and Structure After TCJA

1–3618th Annual Oregon Tax Institute