my fund range for the j.p. morgan uk pension plan go the ...€¦ · my fund range for the j.p....

TRANSCRIPT

My Fund Range for the J.P. Morgan UK Pension Plan

Go the extra mile

J.P. Morgan UK Pension PlanYour future. Your choice.

J.P. Morgan UK Pension Plan2

My Investments

MyPlanner

MyPension Investment choices

Your future. Your choice. 3

« »

next

J.P. Morgan UK Pension PlanYour future. Your choice.

Prepared with you in mind

My Default Strategy for the J.P. Morgan UK Pension Plan

My Investments gives you an overview of the important things to consider when investing, plus it includes:

h the different types of investments available;

h an introduction to the types of risk;

h the investment options available to you within the Plan.

My Investments

We recognise that you will need different sources of information at different times. So, you might be interested to know about the ways in which you can access information to help you plan for your retirement:

Library

ToolsLibrary

Tools

You can find all of these guides in the Plan library

on MyPension and on MyPensionTools.

J.P. Morgan UK Pension PlanYour future. Your choice.

My Investments for the J.P. Morgan UK Pension Plan

Tending to your future

next

Performance history – quarter by quarter

Fund summaryFund Name Benchmark Target out-performance

(net of fees)Management Fees

Settlement Period

L&G DiversifiedFund

Bank of England Base Rate. n/a AMC: 0.13% p.a.TER: 0.13% p.a.

Trading day +2

AMC = Annual Management Charge TER = Total Expense Ratio

Fund performancePerformance

5 Years to 31.12.2014 Performance

3 Years to 31.12.2014Performance

1 Year to 31.12.2014Performance

Quarter 4 to 31.12.2014 Target ReturnsFund Benchmark Fund Benchmark Fund Benchmark Fund Benchmark

% p.a. % p.a. % p.a. % p.a. % % % % % p.a.

n/a n/a n/a n/a 10.1 10.8 3.3 4.1 n/a

Legal & General– Diversified Fund

Passive

Div

ersi

fied

Gro

wth

fun

d

J.P. Morgan UK Pension Plan | 1

Dec12

Mar13

Jun13

Sep13

Dec13

Mar14

Jun14

Sep14

Dec14

Jun12

Sep12

-24.0

-16.0

-8.0

0.0

8.0

16.0

24.0

-8.0

-12.0

-16.0

-4.0

0.0

4.0

8.0

12.0

16.0

L&G Diversified FundExcess Return in Multi-asset Diversified Growth from Jun 2012 to Dec 2014

LGIM DG vs. BoAML 3 month LIBOR (after fees)*

Qua

rter

ly E

xces

s R

etur

n (%

)

Excess R

eturn (%)

Falling Markets Rising Markets 1 Year Rolling Excess Return Upper Quartile Upper Quartile Median

* For comparative purposes, we have compared the performance of the Fund to the Bank of America Merrill Lynch LIBOR 3 month average due to the Fund’s absolute return target.

Log on to keep on top of your pension account by checking your fund value and investments choices. You can also use the new MyPlanner to model a whole range of scenarios for funding your future. The MyPension App is also available to download on your smartphone.

MyPension Fund factsheets

MyPensionTools

Visit www.mypensiontools.co.uk to access a number of useful tools, such as the Contribution Calculator, to help you to work out the net cost of increasing your contributions. With savings in tax and National Insurance, it might cost you much less than you think.

In addition to My Fund Range, which summarises the performance of all funds available in the Plan over the courses of the quarter, you can also access a more detailed 2-page fund factsheet on each of the individual funds on MyPension. These are updated annually.

Our 3 short films, available on MyPensionTools, will help you understand why it’s important to consider your retirement savings as early as you can, no matter what your age. They are designed around 3 simple steps: Know how much you’ll need, Contribute as much as you can, and Make your money work harder.

Films

My Quick Guide gives an overview of the Plan to help you make the most of your membership. It’s particularly useful if you’re a new joiner, as it summarises:

h how the Plan works;

h what to expect when you first join;

h information about how Company and employee contributions work; and

h details of the benefits provided to you and your dependants by the Plan.

My Default Strategy guide provides an in-depth explanation of the Default Strategy, providing more detail on:

h the different phases, funds and switching processes;

h the Alternative Endpoints available;

h choosing your Target Retirements Age and reviewing your choices.

My Handbook covers many of the same themes as My Quick Guide, but gives you further details around:

h how the Plan works;

h the types of contributions you can make to your pension account;

h what happens when you retire, including all the options available to you;

h what happens if you die while in service, or after you retire; and the State Pension benefits.

My Quick Guide

My Default Strategy

My Handbook

Contents

J.P. Morgan UK Pension Plan4

Welcome to the J.P. Morgan UK Pension Plan Fund Range guide ....................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 5

What should I do now? ................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 6

Risk ........................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................ 8

Risk rankings ............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................ 9

Risk vs return ................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 10

The components of risk ............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................. 11

Risk factor table .............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................. 12

Switching processes ............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................. 14

How to make your investment choices on MyPension ................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................. 16

The fund range .......................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 18

Individual fund summaries ........................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................ 20UK/Global/Regional Equities ........................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 21Balanced/Diversified Growth .................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 30Bonds/Liquidity/Other ............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................. 33

Default Strategy Portfolios ............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 38

Fund manager information ............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................. 39

Range of returns ............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 40

Glossary of terms ...................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................... 42

Here to help ............................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................................ 44

This guide helps you consider the last two points above

in relation to the J.P. Morgan UK Pension Plan (the Plan).

It includes details of the range of investment options you

can choose from and will help you understand the important

features of those options. In particular you will find:

h What you need to think about when considering risk

(page 8)

h The risk rankings for each fund (page 9)

h A fund performance table to compare all the funds’

historic performance (pages 18 to 19)

h Individual fund summaries, including fund charges and

performance against benchmark (pages 20 to 36)

Important: the Company meets the administration costs

associated with the Plan, but it’s important you understand

the underlying investment charges as these are met by you

from your pension account.

There are four key elements to pension saving that you need to consider in order to maximise your retirement income:

1. How much you contribute

2. How you invest your pension account

3. How you plan to take your savings in retirement

4. The costs and charges your account faces over the period to your retirement.

We update this detailed guide six weeks after the end of every quarter and you can find the latest version on MyPension or MyPensionTools.

Regular updates

The value of your investments can go down as well as up and past performance is not a guide to future performance. If you are unsure of what investment decisions to make, you should seek impartial financial advice. For more details visit:

www.moneyadviceservice.org.uk/en/articles/choosing-a-financial-adviser

Neither the Trustee nor the Company are authorised to give you investment advice, nor are they responsible for the performance of the investment funds.

Welcome to the J.P. Morgan UK Pension Plan Fund Range guide

Before making your choices, you should read the

My Investments and My Default Strategy guides.

You may also want to read the individual fund fact sheets.

Both are available on MyPension and MyPensionTools;

access details can be found on the back page.

Remember that pension investments are long term. Over time,

as and when your circumstances change, make sure you

regularly check that your investment choices remain appropriate.

Your future. Your choice. 5

How you invest will depend on your personal circumstances and attitude to risk.

Read this guideYou can also find out more about:

h investing in general and what to consider,

in the My Investments guide

h how the Default Strategy works, in the

My Default Strategy guide

h the funds available in the individual fact sheets

h the main benefits of the Plan in the guides,

My Handbook and My Quick Guide.

All of these items are available on MyPension.

Learn

J.P. Morgan UK Pension Plan6

Watch the filmsWe have developed 3 films that focus on each of the key

steps you need to consider for your retirement savings.

An overview of these steps is in your guide, My Handbook,

but here we’ve focused on step 3:

Step 3: Make your money work harderYour investment decisions will have a direct

effect on the value of the benefits you build up.

The film Investments: adding value to your

pension account gives an overview of the

Plan’s investments and what you should

consider when making your choices.

What should I do now?

To view any of these films, or to download the supplementary guides to the films visit MyPensionTools at www.mypensiontools.co.uk

Accessing the tools

Act ReviewDecide how to invest your pension accountThink about your own circumstances and your

financial preferences:

h How much risk do you want to take?

Remember to take into account all the various types

of risk that can influence investments and other factors

such as your other savings and any other sources of

income you will have in your retirement.

h How long until you plan to retire?

The further you are from retiring the longer you have

for your investments to recover their value if they fall

in the short term.

h How will you take your benefits when you retire?

When you retire, you can use your pension account

to buy your choice of retirement benefits. Make sure

your investment choices match your plans.

h Who else do you want to provide for?

You may wish to choose benefits, for example a pension,

that allows you to provide for your spouse, dependants

or registered civil partner, in case you die before them.

Your answers to these types of questions will help

make your investment choices appropriate for you.

Visit MyPension to submit your choices and, if appropriate,

you should seek impartial financial advice to help you.

If you have selected any Lifestyle funds or are in the Default Strategy, it is important you review your Target Retirement Age, as this determines when your investments will begin automatically switching in preparation for your retirement (see My Investments and My Default Strategy guides for more information).

Get onlineMyPension has all your personal Plan details and you can

use it to review your savings and make changes to your

investment choices or find out more.

See the back page for details of how to access MyPension.

You can also monitor investment performance

on your smartphone with our MyPension App.

Your future. Your choice. 7

Action

Check in regularly

Although your pension account is a long-term investment and it is generally not a good idea to trade your investments frequently, you should review at least once a year (or if your plans or circumstances change) and make sure your choices are still appropriate.

Remember to also look out for your benefit statement which we produce every year, for an overview of your Plan benefits and choices.

RiskWhat you need to think about

CapacityIf you are a long way from accessing your retirement benefits,

you will normally have more capacity for risk. For example,

if your investments fall in the short term you still have plenty of

time for their value to potentially recover, and in the meantime,

if you are still contributing to a pension scheme, you will

be purchasing more units and benefiting from additional

compound returns. If you are nearer retirement your capacity

for risk is normally lower as your investments may not recover

in time for your retirement.

ToleranceThis sums up your own feelings and is a personal measure

of the amount of risk you are willing to take with your

investments and how you would feel if your investments

were to fall in value at any point in time.

Between different types of assets (or asset classes), there are

different levels of risk and potential return. Even within an asset

class, there are different levels of risk and potential return that

depend on what the fund manager is trying to achieve.

To help you decide which funds to invest in, each fund has

been assigned a risk ranking (see page 9).

What does the risk ranking represent?

h The risk rankings will help you understand the

different levels of risk when investing your money

compared to other funds within the fund range.

The risk rankings are only meant to be a guide

and are for comparison only.

h The risk rankings are based on the Trustee’s

assessment of investment risk, and reflect advice

from their investment advisers.

h The number reflects the Trustee’s assessment

of the total risk level of each fund, taking into

account the individual components of risk

which the Trustee has considered and to which

each fund is exposed. The component risks

considered are set out on page 11.

h The scale runs from 1 to 13, where ‘1’ represents

the lowest level of risk amongst the funds available

via the Plan, and ‘13’ represents the highest.

h Generally, funds with a lower risk ranking will tend

to have lower potential returns and lower volatility of

the investment returns, while funds with a higher risk

ranking will tend to have higher potential returns and

higher volatility of investment returns, although there

is no guarantee that this will be the case in practice.

What does the risk ranking not represent?

h A fund with a risk ranking of 6 is likely to be more

risky than a fund rated 5, but less risky than a fund

rated 7, but this does not mean it will have half the

risk of a fund with a ranking of 12.

h There may be times when a lower ranked fund could

experience losses in excess of a higher ranked fund.

This could be the result of a fund having a high

exposure to a particular risk that causes it to lose

money for an extended period.

h There is no guarantee that investors in a fund with

a high risk ranking will be compensated for the risk

they are taking on. The levels of investment risk

may change in the future.

h The rankings do not necessarily show the ‘best’

or ‘worst’ investment for you. It is important to

make investment decisions on the basis of your

own circumstances and level of risk tolerance.

You may wish to consider taking your own

impartial financial advice.

J.P. Morgan UK Pension Plan8

Risk means different things to different people. When choosing your investments, you should think about how much risk you are prepared to take. In particular, it is important to consider your capacity and tolerance for risk:

Risk rankings

Your future. Your choice. 9

The following table shows the risk ranking applied to each fund and allows you to see how the risk rankings vary between funds in the same asset class. To understand the individual component risks to which each fund is exposed, please turn to page 11.

Fund Risk ranking

UK Equities (see pages 21 to 23)

LGIM UK Equity (5% Capped) Index 8

Baillie Gifford UK Equity Focus Pension 10

JPM Life UK Specialist Equity 9

Aberdeen Standard Investments UK Equity 9

JPM Life UK Dynamic 10

Global Equities (see pages 23 to 25)

LGIM Global Equity Market Weight (30:70) Index 9

JPM Life Diversified Equity 10

JPM Life Global Dynamic All Countries 11

Baillie Gifford Global Alpha Pension 11

LGIM MSCI World Minimum Volatility Equity Index 8

LGIM FTSE Global Developed Small Cap Equity Index 12

Regional Equities (see pages 26 to 29)

LGIM North America Equity Index 10

LGIM Europe (ex UK) Equity Index 10

LGIM Japan Equity Index 10

LGIM Asia Pacific (ex Japan) Developed Equity Index 11

LGIM World Emerging Markets Equity Index 12

Baillie Gifford Emerging Markets 12

JPM Life All-Emerging Markets Equity 13

*Underlying fund in the default portfolios and not currently available as a self-select option.

Fund Risk ranking

Balanced Funds (see pages 29 to 32)

LGIM Consensus Blended 7

Baillie Gifford Managed Pension 7

JPM Life Balanced 7

Diversified Growth Funds (see pages 29 to 32)

LGIM Diversified 6

Aberdeen Standard Investments Global Absolute Return Strategies 6

Baillie Gifford Diversified Growth Pension 6

Nordea Diversified Returns Strategy 6

Bonds (see pages 32 to 34)

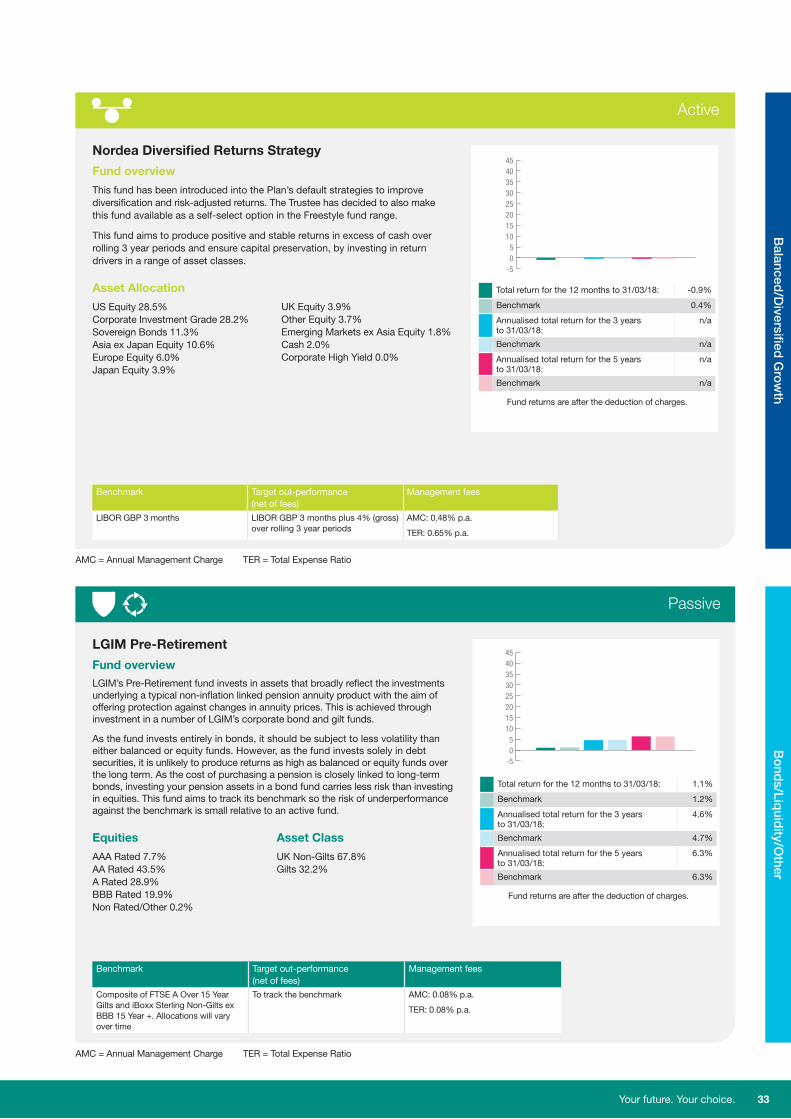

LGIM Pre-Retirement 3

LGIM Over 5 Year Index-Linked Gilts Index 2

Fidelity Aggregate Bond 4

JPMAM Flexible Credit 5

Insight Bonds Plus 300 6

Liquidity (see page 35)

JPM Life UK Liquidity 1

LGIM Euro Liquidity 5

Other (see pages 35 to 36)

LGIM Ethical UK Equity Index 8

Aberdeen Standard Investments Pooled Property Fund 5

Partners Group Generations* 6

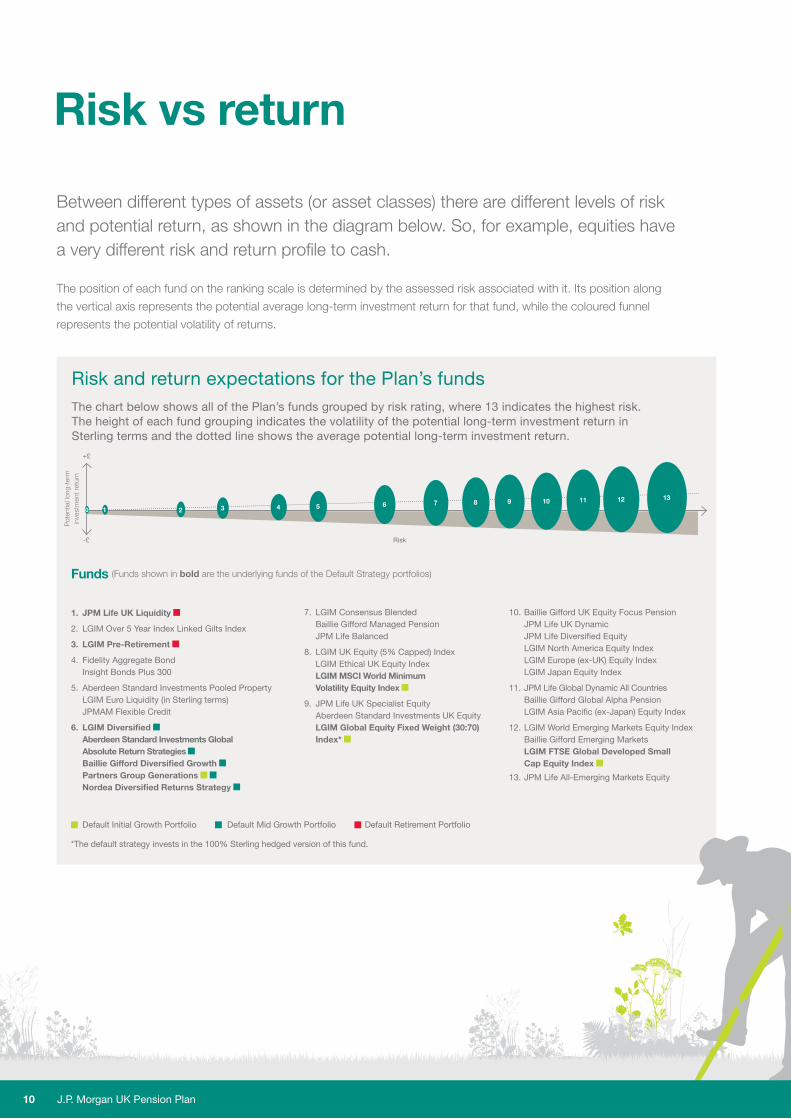

Risk and return expectations for the Plan’s fundsThe chart below shows all of the Plan’s funds grouped by risk rating, where 13 indicates the highest risk. The height of each fund grouping indicates the volatility of the potential long-term investment return in Sterling terms and the dotted line shows the average potential long-term investment return.

Risk vs return

Between different types of assets (or asset classes) there are different levels of risk and potential return, as shown in the diagram below. So, for example, equities have a very different risk and return profile to cash.

The position of each fund on the ranking scale is determined by the assessed risk associated with it. Its position along

the vertical axis represents the potential average long-term investment return for that fund, while the coloured funnel

represents the potential volatility of returns.

Pot

entia

l lon

g-te

rm

inve

stm

ent

retu

rn

+£

-£

3 4 5 6 7 8 9 10 11 12 13

10 2

Risk

Funds (Funds shown in bold are the underlying funds of the Default Strategy portfolios)

Default Initial Growth Portfolio

*The default strategy invests in the 100% Sterling hedged version of this fund.

Default Mid Growth Portfolio Default Retirement Portfolio

J.P. Morgan UK Pension Plan10

1. JPM Life UK Liquidity

2. LGIM Over 5 Year Index Linked Gilts Index

3. LGIM Pre-Retirement

4. Fidelity Aggregate Bond Insight Bonds Plus 300

5. Aberdeen Standard Investments Pooled Property LGIM Euro Liquidity (in Sterling terms) JPMAM Flexible Credit

6. LGIM Diversified Aberdeen Standard Investments Global Absolute Return Strategies Baillie Gifford Diversified Growth Partners Group Generations Nordea Diversified Returns Strategy

7. LGIM Consensus Blended Baillie Gifford Managed Pension JPM Life Balanced

8. LGIM UK Equity (5% Capped) Index LGIM Ethical UK Equity Index LGIM MSCI World Minimum Volatility Equity Index

9. JPM Life UK Specialist Equity Aberdeen Standard Investments UK Equity LGIM Global Equity Fixed Weight (30:70) Index*

10. Baillie Gifford UK Equity Focus Pension JPM Life UK Dynamic JPM Life Diversified Equity LGIM North America Equity Index LGIM Europe (ex-UK) Equity Index LGIM Japan Equity Index

11. JPM Life Global Dynamic All Countries Baillie Gifford Global Alpha Pension LGIM Asia Pacific (ex-Japan) Equity Index

12. LGIM World Emerging Markets Equity Index Baillie Gifford Emerging Markets LGIM FTSE Global Developed Small Cap Equity Index

13. JPM Life All-Emerging Markets Equity

The components of risk

When preparing the risk rankings the following types or ‘components’ of risk have been considered:

Asset class risks h Market risk: this is the risk that the value of your

investments will fall. It’s what most of us think of

when we think of ‘risk’.

h Volatility risk: is the variability of returns relative to their

expected return, which means it relates to how often and

how sharply the market price of an investment changes.

h Inflation risk: if your investment returns are lower than

inflation then the purchasing power of your pension

account goes down. This is inflation risk.

h Currency risk: is the risk of the potential loss in an

investment’s value following a change in price of one currency

against another. It’s also known as exchange rate risk.

h Interest rate risk: relates to the change in the value of an

investment asset as a result of a change in interest rates.

This type of risk is greater in assets like bonds where if

interest rates rise, bond prices fall and vice versa.

h Credit risk: is the risk of default. Again, this is more relevant

to investments like bonds where there is the risk that the

issuer (the company or government offering the bonds)

may be unable or unwilling to make further income and/or

principal payments. UK Government bonds or gilts, for

example, are usually considered to have very low credit risk.

h Emerging market risk: are country specific risks that

could affect the value of an investment in an emerging

market. Risks include changes in the political climate,

natural disasters, currency risk and the risk that you will

have difficulties buying and selling in that market if it is

relatively small (known as illiquidity risk).

Fund specific risks h Smaller company risk: is the potential, increased risk

of investing in a smaller company which may not have

the same level of market information or quality assurance

available as for a larger company. They are also more

susceptible to volatility, because being smaller, it takes

lower transaction volumes (buying and selling of shares)

to move prices.

h Illiquidity risk: relates to how easily an asset can be

bought or sold. If an asset is illiquid, it can’t easily be sold or

exchanged for cash quickly without a substantial loss in value.

h Derivatives risk: a derivative is a type of contract

between two parties (like a future or a swap) where its

value is based on or derived from an underlying asset,

index or interest rate. These types of assets can change

dramatically in value as a result of small changes in the

value of the underlying asset. There is also a potential

risk that the other party may default on the contract,

known as counterparty risk (a type of credit risk).

h Active manager risk: there is a risk that the decisions

taken by an investment manager may have a detrimental

impact on the returns of a fund. A passive manager will not

make many investment decisions other than how to best

track the performance of an index. Active managers will

buy and sell investments with the intention of out-performing

a specific benchmark. The benchmark may be:

• a specific index (for example, FTSE All-Share Index for

UK equity);

• other investment managers (for example, a median

return of investment funds investing in the same sector);

• referenced against cash (for example, UK base rate)

The degree of active decisions made by a manager will vary

by fund and will, in part, be dependent on the investment

objective of the investment fund. If successful, active

management can out-perform relative to the benchmark.

However, if the manager’s decisions prove unsuccessful,

they can under-perform relative to the benchmark.

Other risks h Benefit matching risk: this is the risk that your investments

are not aligned with your preferred method of funding your

retirement, and may therefore result in a lower income in

retirement. If you choose to buy an annuity, the cost of

converting your pension account from a pot of money into

an annual income (annuity) is linked in part to the price of

government and corporate bonds. If you decide to take

benefits through income drawdown, there is also the risk

that your investment strategy may not be suitable for the

way you intend to take benefits in retirement.

Your future. Your choice. 11

Ris

k Fa

cto

rs

Mar

ket r

isk

Vola

tility

ris

k

Infla

tion

risk

Cur

renc

y ris

k

Inte

rest

rat

e ris

k

Cre

dit r

isk

Em

ergi

ng m

arke

ts r

isk

Sm

alle

r co

mpa

ny r

isk

Illiq

uidi

ty r

isk

Der

ivat

ives

ris

k

Inve

stm

ent m

anag

er r

isk

Ann

uity

con

vers

ion

risk

UK Equities

LGIM UK Equity (5% Capped) Index

Baillie Gifford UK Equity Focus Pension

JPM Life UK Specialist Equity

Aberdeen Standard Investments UK Equity

JPM Life UK Dynamic

Global Equities

LGIM Global Equity Market Weight (30:70) Index

JPM Life Diversified Equity

JPM Life Global Dynamic All Countries

Baillie Gifford Global Alpha Pension

LGIM MSCI World Minimum Volatility Equity Index

LGIM FTSE Global Developed Small Cap Equity Index

Regional Equities

LGIM North America Equity Index

LGIM Europe (ex UK) Equity Index

LGIM Japan Equity Index

LGIM Asia Pacific (ex Japan) Developed Equity Index

LGIM World Emerging Markets Equity Index

Baillie Gifford Emerging Markets

JPM Life All Emerging Market Equity

Risk factor table

J.P. Morgan UK Pension Plan12

Your future. Your choice. 13

High Exposure

Moderate Exposure

Some Exposure

Minimal Exposure

Ris

k Fa

cto

rs

Mar

ket r

isk

Vola

tility

ris

k

Infla

tion

risk

Cur

renc

y ris

k

Inte

rest

rat

e ris

k

Cre

dit r

isk

Em

ergi

ng m

arke

ts r

isk

Sm

alle

r co

mpa

ny r

isk

Illiq

uidi

ty r

isk

Der

ivat

ives

ris

k

Inve

stm

ent m

anag

er r

isk

Ann

uity

con

vers

ion

risk

Balanced

LGIM Consensus Blended

Baillie Gifford Managed Pension

JPM Life Balanced

Diversified Growth Funds

LGIM Diversified

Aberdeen Standard Investments Global Absolute Return Strategies

Baillie Gifford Diversified Growth

Nordea Diversified Returns Strategy

Bonds

LGIM Pre Retirement

LGIM Over 5 Year Index-Linked Gilts Index

Fidelity Aggregate Bond

JPMAM Flexible Credit

Insight Bonds Plus 300

Liquidity

JPM Life UK Liquidity

LGIM Euro Liquidity

Other

LGIM Ethical UK Equity Index

Aberdeen Standard Investments Pooled Property

Partners Group Generations*

* Underlying fund in the default portfolios and not currently available as a self-select option.

If you have selected Lifestyle funds in the Freestyle strategy, you can choose your switching period from 3, 5, or 10 years before your Target Retirement Age. Your investments will be progressively moved out of your chosen Lifestyle funds into the LGIM Pre Retirement Fund and the Liquidity fund in the same percentages as for the Default Strategy.

How quickly your investments move depends on the switching period you choose, as illustrated below.

J.P. Morgan UK Pension Plan14

Switching processes

3-year switching process

Years to selected retirement age More than 3 3 2 1

Lifestyle Fund(s) 100% 66.5% 33% 0%

LGIM Pre Retirement Fund 0% 25% 50% 75%

JPM Life UK Liquidity Fund 0% 8.5% 17% 25%

Total 100% 100% 100% 100%

5-year switching process

Years to selected retirement age More than 5 5 4 3 2 1

Lifestyle Fund(s) 100% 80% 60% 40% 20% 0%

LGIM Pre Retirement Fund 0% 15% 30% 45% 60% 75%

JPM Life UK Liquidity Fund 0% 5% 10% 15% 20% 25%

Total 100% 100% 100% 100% 100% 100%

10-year switching process

Years to selected retirement age

More than 10

10 9 8 7 6 5 4 3 2 1

Lifestyle Fund(s) 100% 95% 90% 85% 80% 72.5% 60% 45% 30% 15% 0%

LGIM Pre Retirement Fund

0% 5% 10% 15% 20% 27.5% 35% 45% 55% 65% 75%

JPM Life UK Liquidity Fund 0% 0% 0% 0% 0% 0% 5% 10% 15% 20% 25%

Total 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Switching will take place quarterly and will reallocate your contributions and pension account investments towards the target percentages shown in the tables above. Switches for Lifestyle funds do not incur additional administration charges but will include transaction charges.

Target Retirement Age

Your Target Retirement Age is the age at which you aim to take your benefits from your pension account. Currently it can be at any age between age 55 and 75.

You need to select a Target Retirement Age if you have selected any Lifestyle funds or are in the Default Strategy, which you can do by logging into MyPension.

This is because this age determines when your investments begin switching into defensive investments, such as bond and/or liquidity funds, as you approach retirement. It’s important that you review the age you’ve chosen to ensure it’s in keeping with your retirement plans.

If you do not select a Target Retirement Age, it is assumed that you will retire at age 60 for the purpose of your pension within the Plan.

Your future. Your choice. 15

How to make your investment choices on MyPensionOn MyPension you can change your investment choices any time you like. To get started, choose the ‘My Investments’ tab on the home page, then ‘Change My Investments’ and consider the options opposite.

What type of contribution group(ings) do you want to change? You can change your investment choices for all your contributions or edit individual contribution groupings. Select what you want to change, click ‘Change my Investment Strategy’ and proceed to the ‘Investment strategy’ page.

What investment strategy do you want? You can choose between the Freestyle and the Default Strategy. (The icon on MyPension gives a summary of these options.) Make your selection and click ‘Continue’ to move to the ‘Decisions’ page.

If you select the Default Strategy:Select your Default Strategy option and your Target Retirement Age for your selected contribution types. Decide if any of the Alternative Endpoints might be right for you. Choose your preferred Default Strategy option, ‘Continue’ and proceed to the ‘Summary’ page.

Confirm your choiceOn the ‘Summary’ page, review your new selection(s) and ‘Authorise’ to confirm your choices.

If you choose Freestyle funds: If you choose to invest your selected contribution types into Freestyle funds, you will be able to choose where your past assets are invested and where your future contributions will be invested. These choices can be different if preferred. When investing in Freestyle funds you will need to monitor and maintain your choices on an ongoing basis.

…if you’re currently investing in the Default Strategy, you’ll be able to move your selected contribution types to your choice of Freestyle funds. You will need to monitor and maintain your choices on an ongoing basis.

…if you’re already investing in Freestyle, you’ll be able to choose where your current assets are invested and/or where your future contributions will be invested.

Choose your funds, ‘Continue’ and proceed to the ‘Summary’ page.

J.P. Morgan UK Pension Plan16

You can see a more detailed version of the investment choices decision tree in My Investments.

Remember: Current, future, or both?

If you’re already invested in the Freestyle (and Lifestyle) strategy and you want to change your choices, you can make decisions for where your current assets and/or future contributions will be invested.

h To update your future contributions only, tick the box next to ‘Update my Future contributions’,

and then select ‘Continue’.

The next page will allow you to add your chosen funds for future contributions.

Don’t forget if you want a Freestyle fund with a Lifestyle overlay, make sure you select the Lifestyle version of the fund (the one you want will have ‘Lifestyle’ in the name).

h To switch your current holdings only, select the box next to ‘Update my Current assets’.

Here you can either:

IMPORTANT: If you have more than one period of service under the Plan, any switches you instruct only apply to the record for the period of service that you are viewing at that time. You can move between your records by selecting the ‘Benefit records’ icon, which you’ll find in the top right hand corner of your MyPension screen.

Your future. Your choice. 17