mutual fund style drift and market conditions

TRANSCRIPT

Mutual Fund Style Drift and Market Conditions 2000 - 2015

Robert Holland, Hongyuan Wang,

Peiyi Zhang & Quentin Robert

ABSTRACT

Much work has been done on identifying style drift in mutual funds but there appears to be

a lack of evidence regarding how style drift changes as market conditions change. Using a

method which uses 12 and 24 month rolling regressions we examine R-squared values for

funds against their reported category and against the other 8 Morningstar style categories

using a range of constrains. We find that there have been significant periods of style drift

over parts of the sample period but were unable to find evidence of shift direction and could

not match many of the variations in style drift to changes in market condition. The most

significant drifts occur around the time of the 2008 financial crisis, and since this time we

show there that has been a dramatic reduction in the amount of style drift across all fund

styles. Over the whole period, funds which are core in their style appear to drift more than

other fund types. We conclude that style drift has changed over the period and that since

2008 there has been significantly less drift in mutual funds.

I Introduction

Style drift, is defined as the evolution in investment strategies over time. In the past it has been most

commonly measured by running return-based analysis to obtain resulting Style Drift Score.1 There are

many reasons why fund managers consciously diverge from stated investment strategies, one of which

is to chase outperforming rankings among their peers. In doing so, fund managers expose investors to

different risk factors than advertised, potentially impairing their ability to efficiently construct well

diversified portfolios. As we will discuss further in this paper this is a topic that has been vastly studied

in the past. However, none of the studies we have read have tried to link U.S. mutual funds style drifts

with overall market performance. For example, do mutual funds tend to drift more or less during Bearish

and Bullish market and if so what types of mutual funds drift more and where do they drift to?

Motivated by these issues, we examined the relationship between U.S. mutual funds style drift and

different market conditions based on monthly data ranging from June 2000 to December 2015. We

attempt to answer the following questions:

1. Do mutual funds’ style drift significantly during the period covered?

2. Do certain styles drift more than others?

3. Where do funds from the same category tend to drift?

4. Is there a significant relationship between market conditions and style drift?

We anticipated that certain types of funds would have a tendency of drifting more frequently during

specific market conditions. For example, Small-Cap funds were expected to drift more frequently

during Bearish markets and Large-Cap funds were expected to drift more during Bullish markets.

Furthermore, we believed that the direction of the drifts would be dictated by the specific fund’s style

within each market environment. For instance, we anticipated that a Small-Cap Growth fund would

drift to a ‘safer’ type perhaps towards Mid-Cap Core during Bearish markets and that a Mid-Cap Core

fund would drift towards a ‘riskier’ type such as Small-Cap Core during Bullish markets.

1 The Style Drift Score. By Thomas M. Idzorek and Fred Bertsch

In order to measure style drift, we conducted rolling regressions (12/24 months) on each fund against

the average monthly returns of each fund types. We identified funds that had drifted through various

conditions based around R2. We then created a market ‘index’ to measure the varying degrees of

bearishness and bullishness to link the observed style drift and market conditions.

Although we did not succeed in showing a significant link between the two, we did find a radical shift

in fund managers’ willingness to let their funds drift after the financial crisis of 2008.

II Literature Review

The importance of style drift among the investment community has increased significantly over the past

20 years and as such the amount of research has increased to meet demand for this type of analysis.

Many different sources of literature have found style drift in their studies. However, the cause of drift

is still debated among the academic community. Since the first study, a number of methods have been

used to measure the impact of various factors on style changes or ‘drift’ and the bearing they may have

on fund performance.

Many of the papers that focus on style drift have examined the movements in Style Factors (commonly

the Fama-French factors) and how a shift in these factors over time changes the sources of risk and

return for funds. Returns-based measures for measuring style changes has commonly been used since

Sharpe (1988,1992). For example, diBartolomeo & Witkowski (1997) used the returns-based method

to examine the number of funds which were misclassified. In their study, 40 percent of funds were

misclassified as a result of a poor classification system or a lack of guidelines governing managers

which allowed shifting of styles in order to increase their relative performance. Idzorek & Bertsch

(2004) expanded on this returns-based measure for finding misclassified funds by assigning ‘Style Drift

Scores’ which measure a portfolio's asset mix compared to the average asset mix, based on its volatility.

An alternative method for calculating style drift was developed by Wermers (2010) in which he uses a

‘holdings-based’ measure to assess style drift, which has the advantage of being able to track portfolios

drift when holdings are reported as well as separating active and passive drift. This distinction between

passive and active drift is derived from changes in the market capitalization of holdings, the style of the

holdings and their momentum factor. Wermers (2010) concludes that both passive and active drift

‘contribute significantly’ to total drift. Using the holdings-based method, Wermers finds that managers

who have high levels of active style drift produce superior returns. This is in contrast to Brown &

Harlow (2005), who find that funds with higher style consistency have higher returns during periods

when the benchmark is positive.

There is also widespread discussion as to the causes of style drift. According to Holmes & Faff (2008),

during 1990 and 1999, mutual funds style drifts are influenced by selectivity performances in up-market

and by flow volatility in down-market. However, the article didn’t conclude on how mutual funds may

drift investment styles in different market conditions. Fund flow has also been widely linked to style

drift. Funds both change their styles to attract new investment and change their styles as a result of new

investment (Yuhong & Wenwei, 2013). As there are often large changes in fund flows during bearish

and bullish markets, this may be cause for increased style drift in these periods (Yuhong & Wenwei,

2013). Indeed, these authors find that during bear markets, style drift increases the market timing of

funds whereas during bull markets, market timing is weakened.

Blanchett (2011) states in his paper that drifting funds see a significant increase in fund flows following

the change in Morningstar category following a returns-based style shift. Concurrently, funds tend to

drift to categories that underperform their previous category, and the drift will improve their relative

percentile ranking but remain below-average level in their new category, with no performance boost.

Despite many papers already covering style drift over significant periods, there is still no conclusive

research regarding the cause of style drift over time on U.S. mutual funds. As such, this paper will look

at the market environment throughout the last 15 years and analyze how wider market changes affect

individual fund drift. This will be done using a method of returns-based style analysis.

III Data

Creating a returns dataset for mutual funds

The data for this study came from the CSRP data set and data was collected for the period January 2000

to December 2015. The entire set of U.S mutual funds was amassed with Lipper classification names

and CUSIP IDs for each fund. Data was then filtered so only one Lipper class for each fund remained

and we then removed all funds that did not have a Lipper classification that’s fits in the Morningstar

3x3 style box (Exhibit 1). These funds are categorized (and hereby called) as Large-Cap Growth (LG),

Large-Cap Core (LC), Large-Cap Value (LV), Mid-Cap Growth (MG), Mid-Cap Core (MC), Mid-Cap

Value (MV), Small-Cap Growth (SG), Small-Cap Core (SC) and Small-Cap Value (SV). There were a

total of 9,202 funds which fitted these criteria.

Monthly returns data for the same period were then gathered and the CUSIPs were matched against

those from the Lipper classification dataset. Funds were only kept where there were greater than 60

months of returns so that future analysis would be statistically significant. Other than this our data is

free of survivorship bias. This gave us a total of 1,501 funds, distributed as follows:

Table 3.1 Number of Funds by Style

Fund Type Total Number of Funds

Large-Cap Growth 266

Large-Cap Core 339

Large-Cap Value 171

Mid-Cap Growth 143

Mid-Cap Core 107

Mid-Cap Value 28

Small-Cap Growth 179

Small-Cap Core 184

Small-Cap Value 84

Total 1501

We then removed the first 6 months of data as for Mid-Cap Value there were no funds which had returns

in this period which skewed our dataset. The number of funds in each category varied over time with

the lowest total number of funds being 613 in June 2000 and the highest being 1,205 in February/March

2007. We take account for this variation in our methodology.

Creating a market type dataset

To determine market type we used daily and monthly data from the S&P 500 for the period January

2000 – December 2015. This data was retrieved from Yahoo Finance.

IV Methodology

Creating benchmarks and testing for misclassification

With the data now collected and organized we calculated the average monthly returns per fund class

and used them as benchmarks against which we ran regressions to analyse style drift. Before going

ahead and running regressions to measure drift, we checked to see whether or not some of the funds in

our dataset were misclassified as of January 2000. We did so by calculating the average of the first 12

consecutive months of returns for each benchmark and each fund as well as the standard deviation of

returns for each benchmark over that period. We defined funds as having been misclassified if their

average returns over their first 12 months were more than 1.5 standard deviations away from their

respective benchmark’s average. We found that none of the funds in the sample had been misclassified.

Deciding how to measure drift

In order to measure drift, and more specifically the instance at which the fund had drifted away from

its style, we ran rolling regressions for each fund against all benchmarks previously mentioned shifting

down by one month each time. The time period over which the regressions were run was a topic of

much discussion. Since our ultimate goal was to be able to overlap drift and market conditions (bull,

bear or neutral), we needed a time period short enough to compare with often short global market trends

but long enough to reduce the amount of noise around our results. With that in mind we ran our rolling

regressions over two distinct periods, 12 months and then 24 months. Once we ran regressions for each

funds (1501) against all benchmarks (their own and the 8 remaining), for both time periods (12 months

rolling and 24 month rolling), we turned our attention to selecting the funds that had drifted to other

styles.

Identifying periods during which funds had drifted was a pain-point for our group. We had to try a few

different methods before settling for our final one. We will now discuss each method we used and why

we ultimately did or did not pick them.

1. Betas and p-values.

We first regressed each fund against their own benchmark (using the linest function in excel), calculated

the standard deviations of the betas for each period and class type. Assuming that a fund that hadn’t

drifted would have a beta equal to or close to 1 (i.e. positively correlated with the average returns of its

own class), we identified funds that had drifted by selecting those who’s betas were significantly

different from 1 at the 10% level and who’s betas were more than 1.5 standard deviations away from 1.

In order to differentiate between drift and out/underperformance, we took the resulting funds and

regressed them against all other benchmarks. We defined funds that had drifted as those whose betas

(when regressed a second time) were between 0.9 and 1.1, i.e. had not drifted against benchmarks other

than its own.

However, after further discussion we realized that this might not be the best way to measure drift as a

fund could have a beta significantly different than 1 against its own class type if it was over or under

levered. Therefore, the results we got using this method weren’t a reliable measure of drift.

2. R2

After deliberation we opted to look at R2 as an indication of drift. The intuition behind it was that the

larger the R2, the better the model fits our data, therefore, the higher the R2 the better the benchmark

used in the regression fits the fund returns it is regressed against. For example, if a LC fund is regressed

against its own benchmark and had an R2 of 0.75 and an R2 of 0.95 when regressed against the LV

benchmark, over the same period of time, we conclude that the LC fund drifted to LV.

Within this method we decided to test two different constraints in order to differentiate between

intentional and unintentional drifts.

a. Two conditions (Two-CC)

The first test required the fund to have an R2 smaller than 0.75 when regressed against its own

benchmark and an R2 larger than 0.75 when regressed against other benchmarks. However, we often

found under this condition the same fund could have shifted towards more than one new fund type

during the same period of time. When this was the case we elected picked the class type that generated

the highest R2.

b. One condition (One CC)

This observation led us to conclude that we might not need the first condition but simply select the fund

class that generated the highest R2 when used in our regressions.

Our results section will be using the output generated from 2a. and 2b. for both 12 and 24 months rolling

regressions.

Matching periods of drift with market conditions

Once we had identified the funds that had drifted and the 12/24 months’ periods during which the drifts

had occurred, we turned our attention to matching said periods with corresponding market conditions.

This also caused the group some difficulties and we attempted various methods before settling for our

final one.

1. Dummy variable regressions

At first we attempted to regress the percentage of funds that had drifted in each period against dummy

variables Bull (1 when Bull Market, 0 otherwise), Bear (1 when Bear Market, 0 otherwise) and Neutral

(1 when Neutral Market, 0 otherwise). We defined a Bull market when the daily market value was

greater than the 200 day moving average, a Bear market when the daily market value was smaller than

the 200 day moving average and a Neutral market when there wasn’t a Bull or Bear market for 60

consecutive days.

Although our results (which we will not discuss in the next section) where significant on some of our

tests, we realized that it was practically impossible to know the exact point in time where the drift had

occurred and therefore what the true market condition was at the time of the drift. Furthermore, this

method did not take into consideration the magnitude of the Bear or Bull markets which we felt would

have a significant impact on drift. We therefore decided to discount this method.

2. 12/24 months rolling market conditions

In order to better reflect the magnitude of market conditions, we calculated the mean and standard

deviation of the S&P 500’s monthly returns between January 2000 and December 2015. We then

attributed various values to each month depending on how many standard deviations away from the

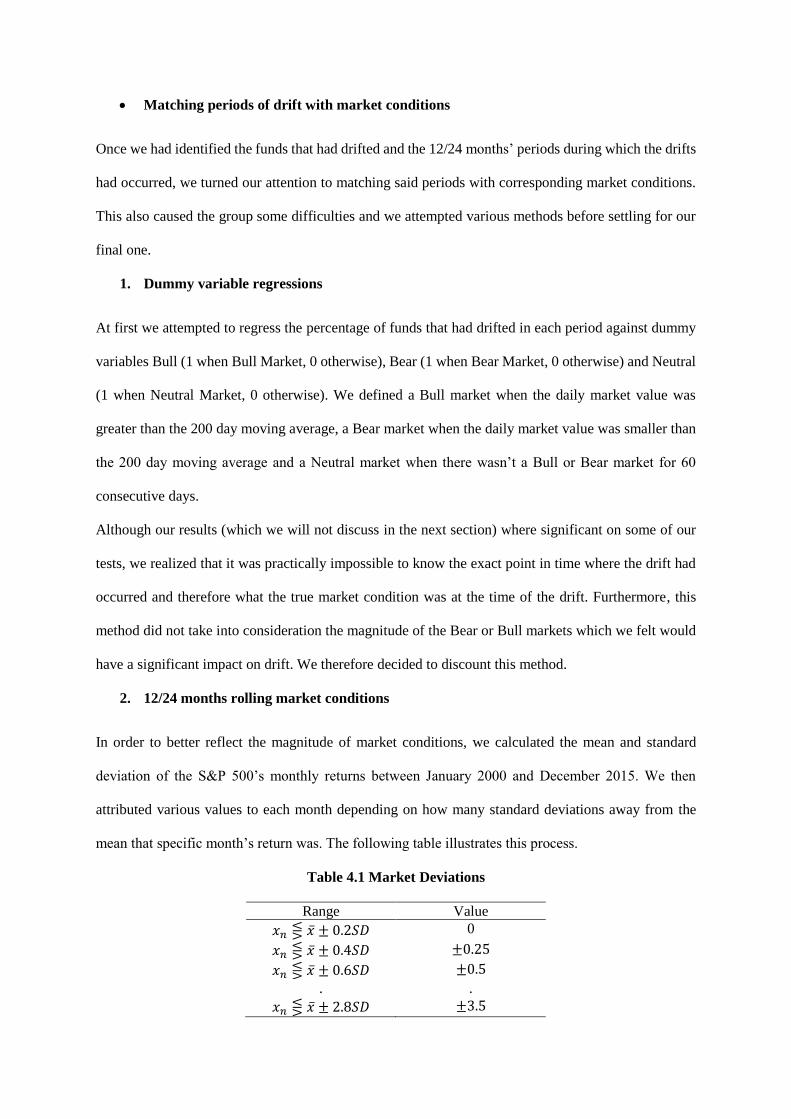

mean that specific month’s return was. The following table illustrates this process.

Table 4.1 Market Deviations

Range Value

𝑥𝑛 ⋚ �̅� ± 0.2𝑆𝐷 0

𝑥𝑛 ⋚ �̅� ± 0.4𝑆𝐷 ±0.25

𝑥𝑛 ⋚ �̅� ± 0.6𝑆𝐷 ±0.5

. .

𝑥𝑛 ⋚ �̅� ± 2.8𝑆𝐷 ±3.5

By attributing more extreme values to more extreme market conditions and less extreme values to less

extreme market conditions we were able to get a more accurate representation of the market conditions.

We then calculate the 12/24 month rolling average market condition which we matched with our

previously calculated drift in graphs.

We will now discuss and interpret the results of our study.

V Results

Drift Percentage

Under the 4 circumstances mentioned above, we calculate the final style drift as a percentage of different

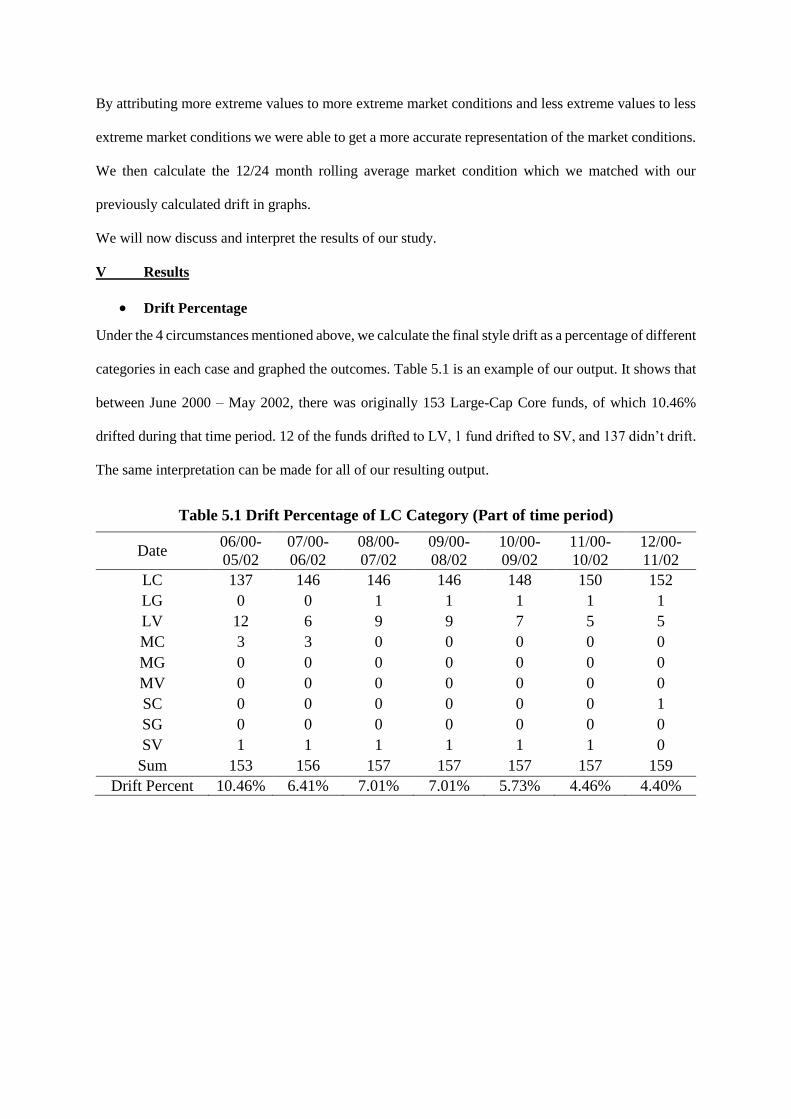

categories in each case and graphed the outcomes. Table 5.1 is an example of our output. It shows that

between June 2000 – May 2002, there was originally 153 Large-Cap Core funds, of which 10.46%

drifted during that time period. 12 of the funds drifted to LV, 1 fund drifted to SV, and 137 didn’t drift.

The same interpretation can be made for all of our resulting output.

Table 5.1 Drift Percentage of LC Category (Part of time period)

Date 06/00-

05/02

07/00-

06/02

08/00-

07/02

09/00-

08/02

10/00-

09/02

11/00-

10/02

12/00-

11/02

LC 137 146 146 146 148 150 152

LG 0 0 1 1 1 1 1

LV 12 6 9 9 7 5 5

MC 3 3 0 0 0 0 0

MG 0 0 0 0 0 0 0

MV 0 0 0 0 0 0 0

SC 0 0 0 0 0 0 1

SG 0 0 0 0 0 0 0

SV 1 1 1 1 1 1 0

Sum 153 156 157 157 157 157 159

Drift Percent 10.46% 6.41% 7.01% 7.01% 5.73% 4.46% 4.40%

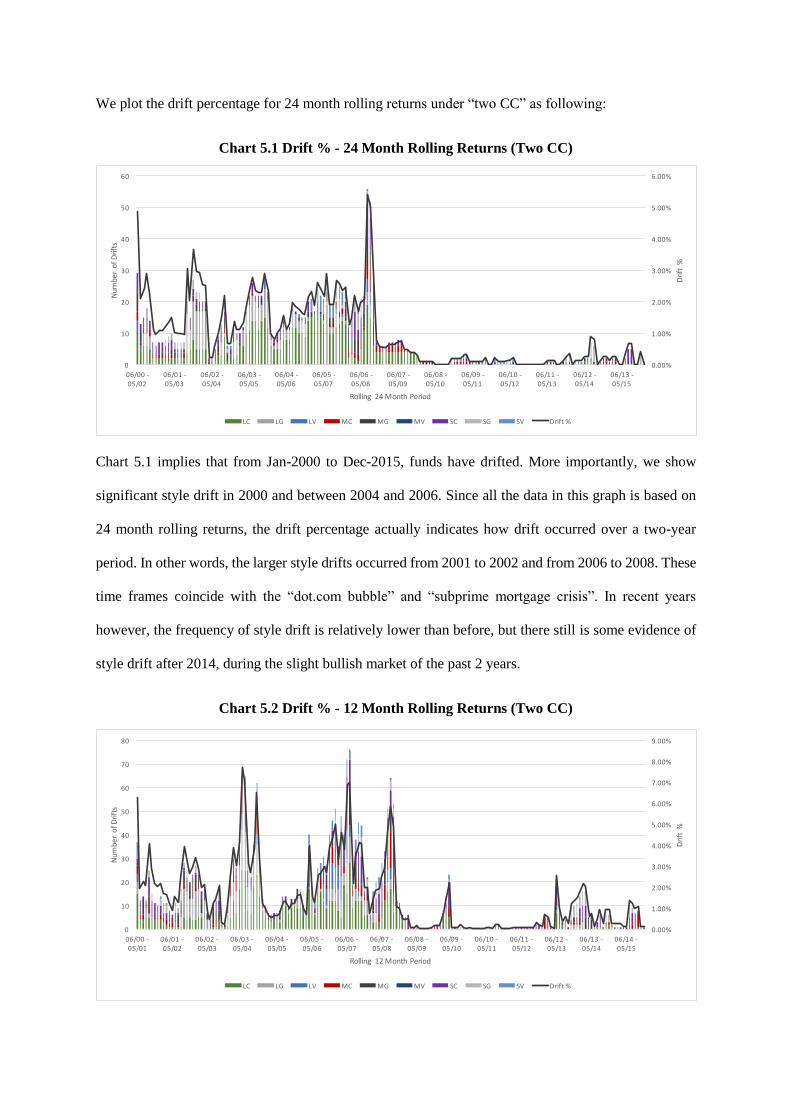

We plot the drift percentage for 24 month rolling returns under “two CC” as following:

Chart 5.1 Drift % - 24 Month Rolling Returns (Two CC)

Chart 5.1 implies that from Jan-2000 to Dec-2015, funds have drifted. More importantly, we show

significant style drift in 2000 and between 2004 and 2006. Since all the data in this graph is based on

24 month rolling returns, the drift percentage actually indicates how drift occurred over a two-year

period. In other words, the larger style drifts occurred from 2001 to 2002 and from 2006 to 2008. These

time frames coincide with the “dot.com bubble” and “subprime mortgage crisis”. In recent years

however, the frequency of style drift is relatively lower than before, but there still is some evidence of

style drift after 2014, during the slight bullish market of the past 2 years.

Chart 5.2 Drift % - 12 Month Rolling Returns (Two CC)

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

0

10

20

30

40

50

60

70

80

06/00-05/01

06/01-05/02

06/02-05/03

06/03-05/04

06/04-05/05

06/05-05/06

06/06-05/07

06/07-05/08

06/08-05/09

06/09-05/10

06/10-05/11

06/11-05/12

06/12-05/13

06/13-05/14

06/14-05/15

Drift%

Num

berofDrifts

Rolling12MonthPeriod

LC LG LV MC MG MV SC SG SV Drift%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

0

10

20

30

40

50

60

06/00-05/02

06/01-05/03

06/02-05/04

06/03-05/05

06/04-05/06

06/05-05/07

06/06-05/08

06/07-05/09

06/08-05/10

06/09-05/11

06/10-05/12

06/11-05/13

06/12-05/14

06/13-05/15

Drift%

NumberofDrifts

Rolling24MonthPeriod

LC LG LV MC MG MV SC SG SV Drift%

While the graph a similar pattern from that of the 24 month rolling returns, the frequency of style drift

increases slightly, which is to be expected as the regression for 12 month rolling returns contributes to

pinpoint more specifically the periods in which style drifts happened.

Based on the results above, we then loosen our conditions to “one CC” and get the following drift

percentages.

Chart 5.3 Drift % - 24 Month Rolling Returns (One CC)

Chart 5.4 Drift % - 12 Month Rolling Returns (One CC)

As we can see, the graph for “one CC” highlights a higher frequency in style drift than their

corresponding “two CC” graphs. This suggests that eliminating the criterion that the R2 of the regression

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

0

10

20

30

40

50

60

70

80

90

06/00-05/02

06/01-05/03

06/02-05/04

06/03-05/05

06/04-05/06

06/05-05/07

06/06-05/08

06/07-05/09

06/08-05/10

06/09-05/11

06/10-05/12

06/11-05/13

06/12-05/14

06/13-05/15

Drift%

NumberofD

rifts

Rolling24MonthPeriod

LC LG LV MC MG MV SC SG SV Drift%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

0

20

40

60

80

100

120

140

160

180

06/00-05/01

06/01-05/02

06/02-05/03

06/03-05/04

06/04-05/05

06/05-05/06

06/06-05/07

06/07-05/08

06/08-05/09

06/09-05/10

06/10-05/11

06/11-05/12

06/12-05/13

06/13-05/14

06/14-05/15

Drift%

NumberofDrifts

Rolling12MonthPeriod

LC LG LV MC MG MV SC SG SV Drift%

of a fund to its own category average return must be less than 0.75 increases the amount of style drift

observed.

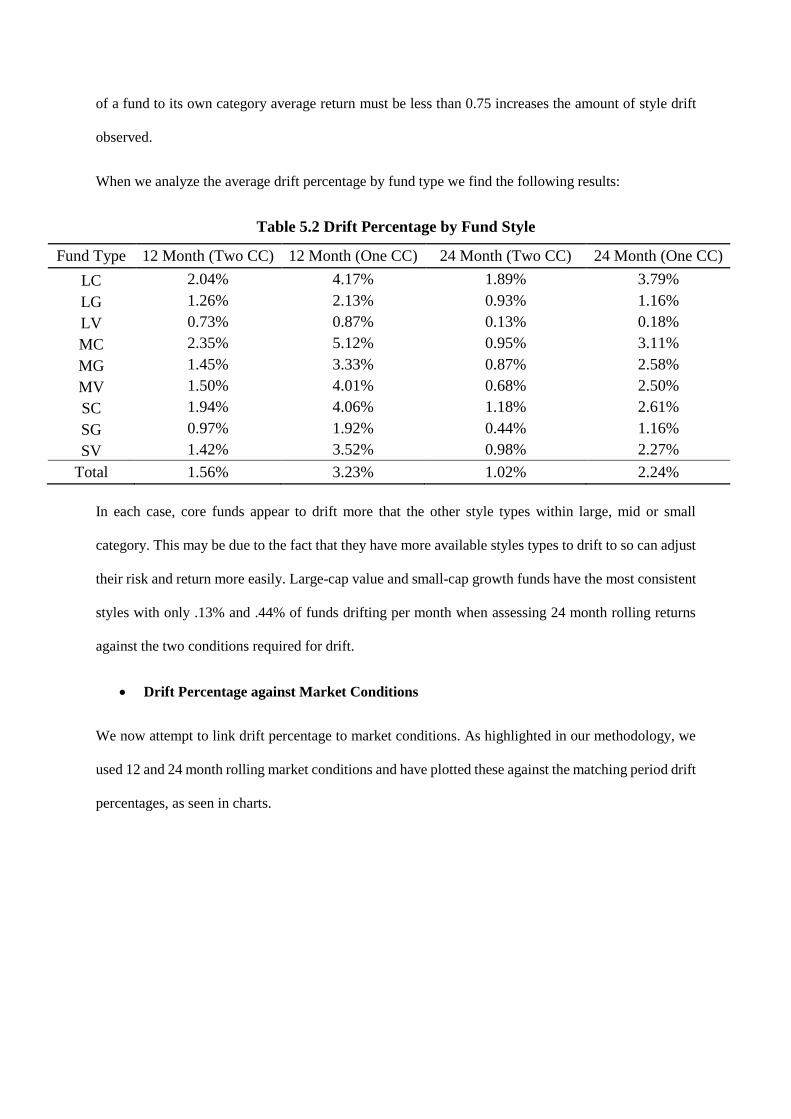

When we analyze the average drift percentage by fund type we find the following results:

Table 5.2 Drift Percentage by Fund Style

Fund Type 12 Month (Two CC) 12 Month (One CC) 24 Month (Two CC) 24 Month (One CC)

LC 2.04% 4.17% 1.89% 3.79%

LG 1.26% 2.13% 0.93% 1.16%

LV 0.73% 0.87% 0.13% 0.18%

MC 2.35% 5.12% 0.95% 3.11%

MG 1.45% 3.33% 0.87% 2.58%

MV 1.50% 4.01% 0.68% 2.50%

SC 1.94% 4.06% 1.18% 2.61%

SG 0.97% 1.92% 0.44% 1.16%

SV 1.42% 3.52% 0.98% 2.27%

Total 1.56% 3.23% 1.02% 2.24%

In each case, core funds appear to drift more that the other style types within large, mid or small

category. This may be due to the fact that they have more available styles types to drift to so can adjust

their risk and return more easily. Large-cap value and small-cap growth funds have the most consistent

styles with only .13% and .44% of funds drifting per month when assessing 24 month rolling returns

against the two conditions required for drift.

Drift Percentage against Market Conditions

We now attempt to link drift percentage to market conditions. As highlighted in our methodology, we

used 12 and 24 month rolling market conditions and have plotted these against the matching period drift

percentages, as seen in charts.

Charts 5.5 -5.8 Rolling Period Shifts against market conditions

The results appear to be distinct in some cases. Firstly, it is obvious that since 2008, there has been low

levels of drift in all of our categories. This is despite large swings in market conditions during which

we would expect to see fund managers change their styles to reflect these more bearish or bullish

markets, either seeking higher returns or safety. Prior to 2008 we see large levels of drift across time

but there appears to be very little correlation with the market type. However, it should be noted that in

each case there appears to be a large increase in style drift in the months preceding the financial crisis.

Further analysis is required to determine the nature of this shift and whether it was fund managers

seeking safety in fear of a market collapse or whether it was market confidence prompting managers to

take on additional risk and move to more aggressive investing styles.

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

-1.5

-1

-0.5

0

0.5

1

06/00-05/01

06/01-05/02

06/02-05/03

06/03-05/04

06/04-05/05

06/05-05/06

06/06-05/07

06/07-05/08

06/08-05/09

06/09-05/10

06/10-05/11

06/11-05/12

06/12-05/13

06/13-05/14

06/14-05/15

FundDrift(%)

12M

onthRollingMarketConditions

Rolling12MonthPeriod

12MonthFundDriftvMarketCondition

Rolling12monthMarketCondition Rolling12month%FundDrift(OneCC)

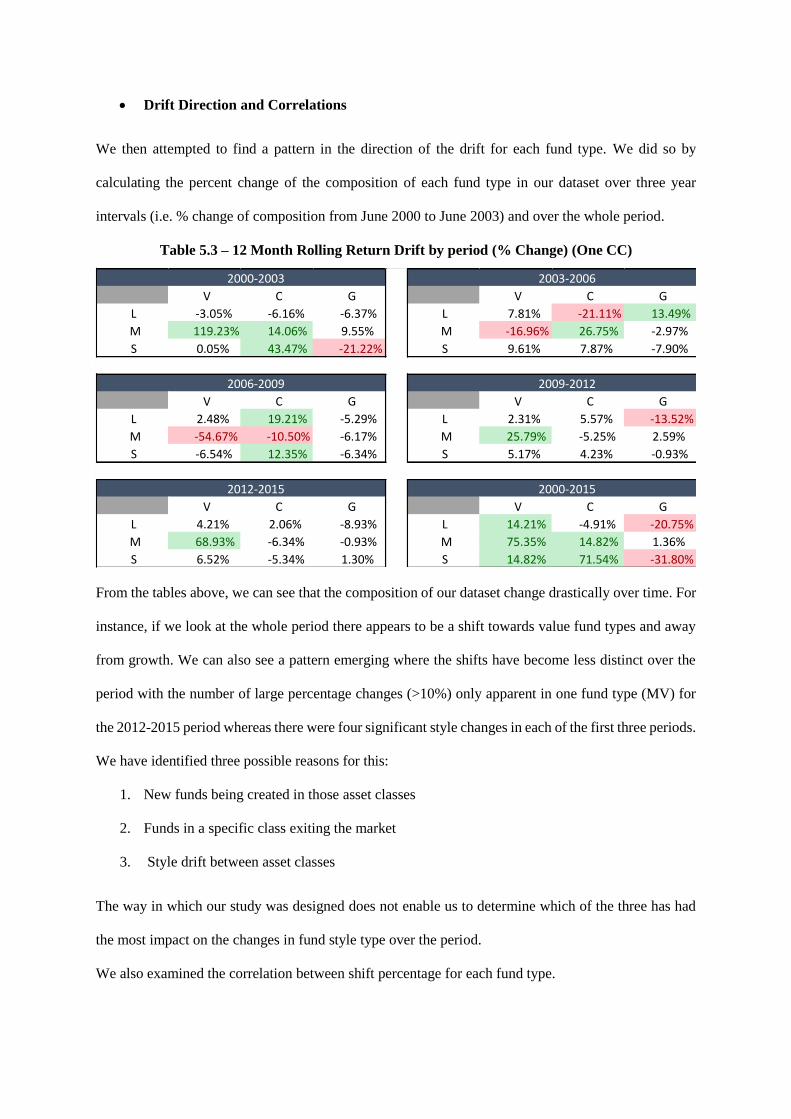

Drift Direction and Correlations

We then attempted to find a pattern in the direction of the drift for each fund type. We did so by

calculating the percent change of the composition of each fund type in our dataset over three year

intervals (i.e. % change of composition from June 2000 to June 2003) and over the whole period.

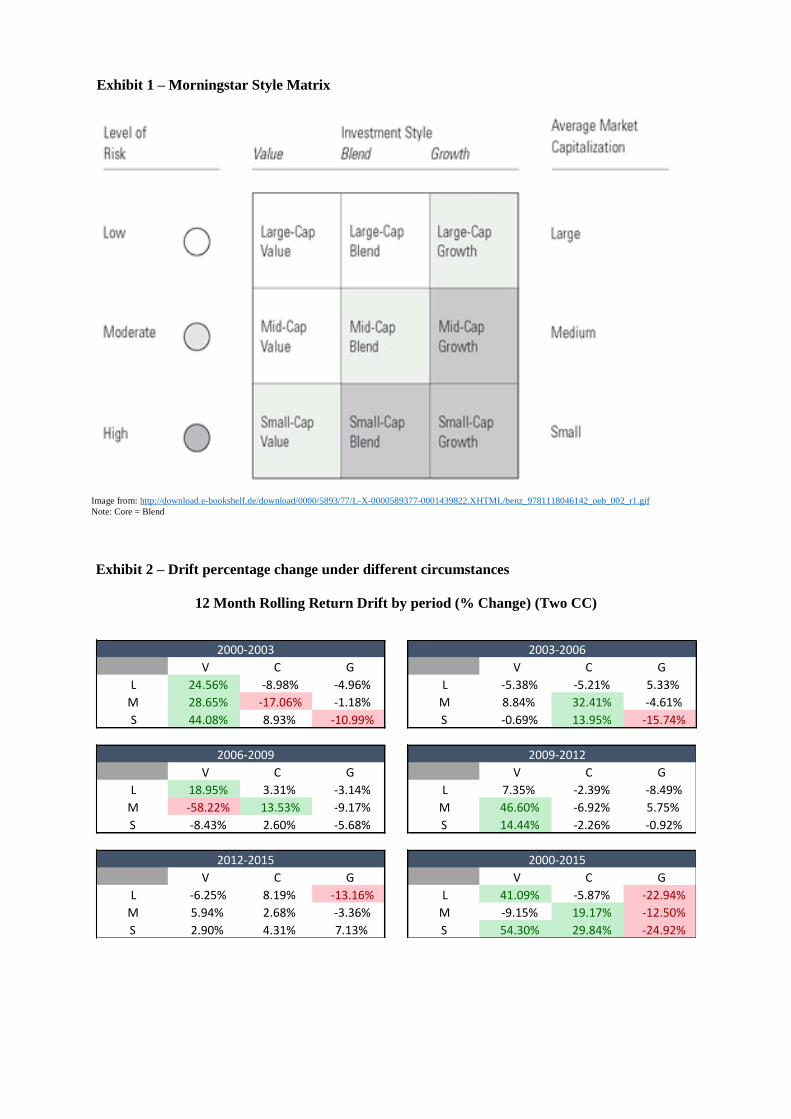

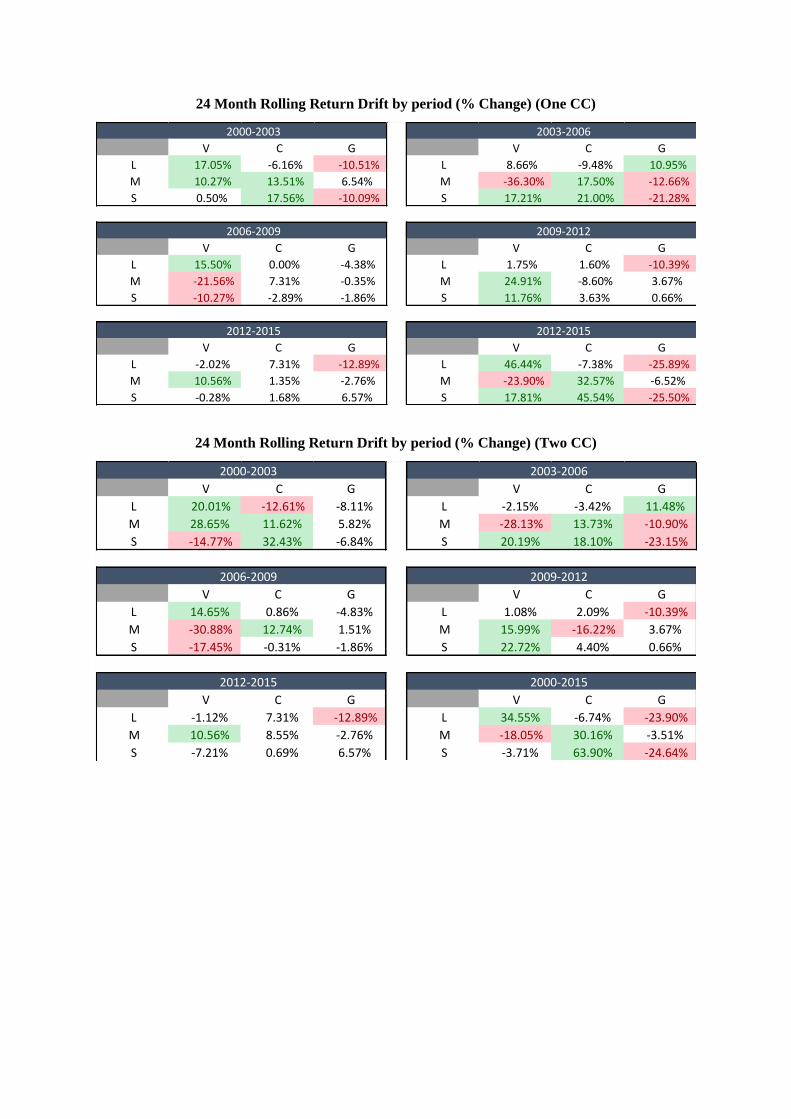

Table 5.3 – 12 Month Rolling Return Drift by period (% Change) (One CC)

From the tables above, we can see that the composition of our dataset change drastically over time. For

instance, if we look at the whole period there appears to be a shift towards value fund types and away

from growth. We can also see a pattern emerging where the shifts have become less distinct over the

period with the number of large percentage changes (>10%) only apparent in one fund type (MV) for

the 2012-2015 period whereas there were four significant style changes in each of the first three periods.

We have identified three possible reasons for this:

1. New funds being created in those asset classes

2. Funds in a specific class exiting the market

3. Style drift between asset classes

The way in which our study was designed does not enable us to determine which of the three has had

the most impact on the changes in fund style type over the period.

We also examined the correlation between shift percentage for each fund type.

V C G V C G

L -3.05% -6.16% -6.37% L 7.81% -21.11% 13.49%

M 119.23% 14.06% 9.55% M -16.96% 26.75% -2.97%

S 0.05% 43.47% -21.22% S 9.61% 7.87% -7.90%

V C G V C G

L 2.48% 19.21% -5.29% L 2.31% 5.57% -13.52%

M -54.67% -10.50% -6.17% M 25.79% -5.25% 2.59%

S -6.54% 12.35% -6.34% S 5.17% 4.23% -0.93%

V C G V C G

L 4.21% 2.06% -8.93% L 14.21% -4.91% -20.75%

M 68.93% -6.34% -0.93% M 75.35% 14.82% 1.36%

S 6.52% -5.34% 1.30% S 14.82% 71.54% -31.80%

2000-2015

2000-2003 2003-2006

2006-2009 2009-2012

2012-2015

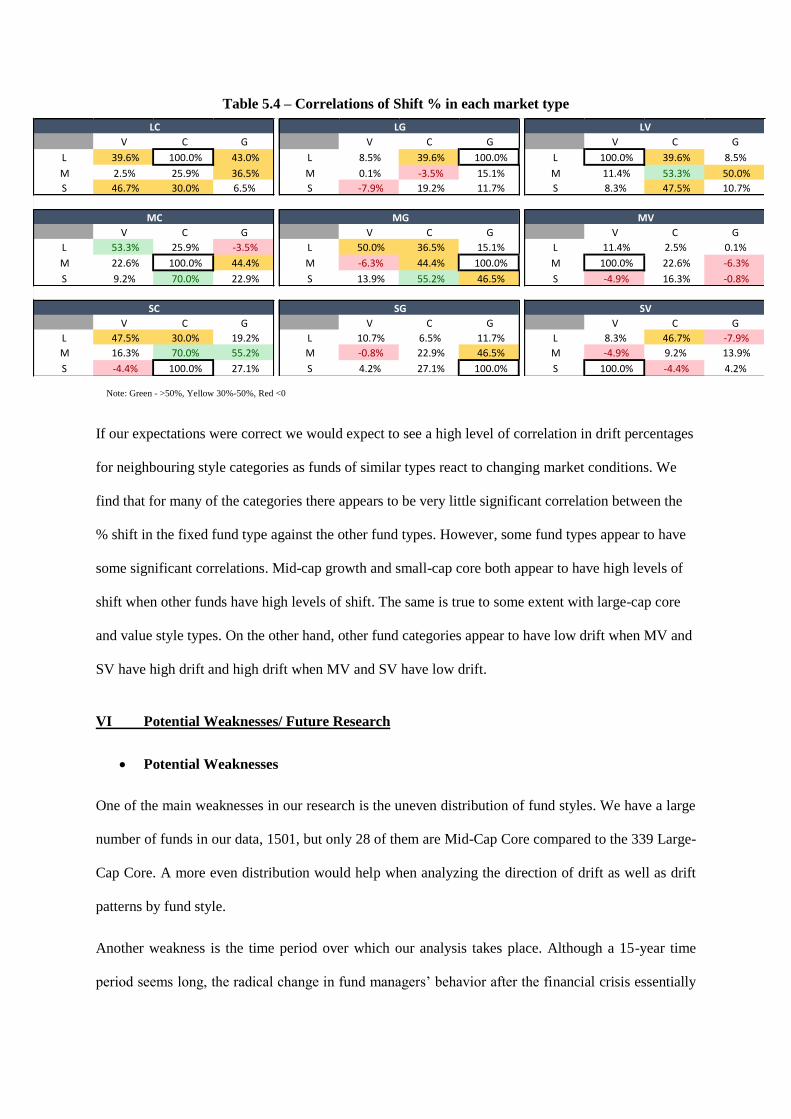

Table 5.4 – Correlations of Shift % in each market type

If our expectations were correct we would expect to see a high level of correlation in drift percentages

for neighbouring style categories as funds of similar types react to changing market conditions. We

find that for many of the categories there appears to be very little significant correlation between the

% shift in the fixed fund type against the other fund types. However, some fund types appear to have

some significant correlations. Mid-cap growth and small-cap core both appear to have high levels of

shift when other funds have high levels of shift. The same is true to some extent with large-cap core

and value style types. On the other hand, other fund categories appear to have low drift when MV and

SV have high drift and high drift when MV and SV have low drift.

VI Potential Weaknesses/ Future Research

Potential Weaknesses

One of the main weaknesses in our research is the uneven distribution of fund styles. We have a large

number of funds in our data, 1501, but only 28 of them are Mid-Cap Core compared to the 339 Large-

Cap Core. A more even distribution would help when analyzing the direction of drift as well as drift

patterns by fund style.

Another weakness is the time period over which our analysis takes place. Although a 15-year time

period seems long, the radical change in fund managers’ behavior after the financial crisis essentially

V C G V C G V C G

L 39.6% 100.0% 43.0% L 8.5% 39.6% 100.0% L 100.0% 39.6% 8.5%

M 2.5% 25.9% 36.5% M 0.1% -3.5% 15.1% M 11.4% 53.3% 50.0%

S 46.7% 30.0% 6.5% S -7.9% 19.2% 11.7% S 8.3% 47.5% 10.7%

V C G V C G V C G

L 53.3% 25.9% -3.5% L 50.0% 36.5% 15.1% L 11.4% 2.5% 0.1%

M 22.6% 100.0% 44.4% M -6.3% 44.4% 100.0% M 100.0% 22.6% -6.3%

S 9.2% 70.0% 22.9% S 13.9% 55.2% 46.5% S -4.9% 16.3% -0.8%

V C G V C G V C G

L 47.5% 30.0% 19.2% L 10.7% 6.5% 11.7% L 8.3% 46.7% -7.9%

M 16.3% 70.0% 55.2% M -0.8% 22.9% 46.5% M -4.9% 9.2% 13.9%

S -4.4% 100.0% 27.1% S 4.2% 27.1% 100.0% S 100.0% -4.4% 4.2%

SVSGSC

LC LG LV

MC MG MV

Note: Green - >50%, Yellow 30%-50%, Red <0

means that we have two separate time periods, one ranging from 2000-2008 and one ranging from 2009-

2015. Neither of these time frames are truly long enough for us to determine a strong pattern in drift.

Our results would have been significantly different had we spanned back to the early 1990s.

Furthermore, we failed to update the benchmarks for each fund style as funds drifted. This slightly

skewed our data in regards to determine the direction of style drift. If we had had more time we would

go back and adjust the composition of each fund class as we moved along.

Future Research

As we have shown in the results section, we have found a significant change in fund managers’

behaviors in regards to fund drift. This could be explained a number of ways. For instance, this could

be due to the fact that the funds that drifted before the financial crisis tended to underperform those that

didn’t. This realization might have increased their discipline in maintain a consistent style in order to

avoid the negative impact of style drift on their performance. Furthermore, since the financial crisis

regulations imposed on mutual funds have increased significantly. The majority of these regulatory

changes have targeted the disclosure of the funds holding as well as risk/returns profile. This increase

in transparency makes fund managers more accountable to current investors as well as highlights their

inconsistencies to potential investors. It could be interesting to explore the impact of these changes of

regulations on fund style drift.

VII Conclusion

In this paper we set-out to establish a clear link between market conditions and style drift. In order to

do so we started by observing and measuring style drift in 1501 U.S. mutual funds between January

2000 and December 2015.

Our initial hypothesis was that certain types of funds would have a tendency of drifting more frequently

during specific market conditions. For example, Small-Cap funds were expected to drift more in Bearish

markets and Large-Cap funds were expected to drift more in Bullish markets. Although we found that

a significant amount of funds drifted across all styles at various points in time, we were unable to show

any significant increase in fund drift during specific market conditions.

Furthermore, we expected that the direction of the drifts would have been dictated by the original fund’s

style as well as the market condition. For instance, a Small-Cap Growth fund was anticipated to drift

towards a ‘safer’ type perhaps Mid-Cap Core during Bearish markets and a Mid-Cap Core fund was

anticipated to drift towards a ‘riskier’ type such as Small-Cap core in Bullish markets. We were able to

find evidence that core funds drifted more that other fund types but could not then link this to market

conditions over the period. However, we could not provide a substantial link between drift in neighbour

fund types which we would expect if funds drifted as a result of market conditions.

Some of the potential reasons behind this ‘failure’ could be linked to the uneven distribution within our

dataset and our late realization that updating rebalancing our dataset composition and benchmarks after

each regression was run may increase the reliability of our results.

Nevertheless, an interesting finding came out of our study. We found that fund managers’ openness to

drifting was greatly influenced by the 2008 financial crisis. Indeed, as mentioned in our results section,

we see a clear cut change in the number of drifts towards the end of 2008. Between 2000-2007, on

average, 2.63% of funds are drifting at any given point in time and we even see drifts upwards of 10%

in some months. However, after 2008, on average, only 0.46% of funds are drifting at any given point

in time and the highest level of drift at any given point in time after that is 2.56%.

As discussed in the previous section future research it would be interesting to analyse the potential

causes of this change in mind-set. We believe that poor performance witnessed by mutual funds that

drifted significantly around 2008 may be one of the causes of such a shift. Another area for further

study could be analysing the impact of the change in regulations after the crisis on mutual funds.

We still remain convinced that a relationship exists between mutual fund style drift and market

conditions and hope that it will be researched further in the years to come.

Bibliography

Blanchett, D. M., 2011. Gaming the System: The Impact of Morningstar Category Changes

on Peer Rankings. Journal of Investing, 20(1), pp. 33-42.

Brown, K. & Harlow, W., 2005. Staying the course: Performance persistance and the role of

investment style consistency in professional asset mangement, Texas: Working Paper.

diBartolomeo, D. & Witkowski, E., 1997. Mutual Fund Misclassifiaction: Evidence Based on

Style Analysis. Financial Analysts Journal, Volume Septmeber/October, pp. 32-43.

Holmes, K. & Faff, R., 2008. Style drift and fund performance in up and down markets:

Australian Evidence. Applied Financial Economics Letters, 4(6), pp. 395-398.

Idzorek, T. M. & Bertsch, F., 2004. The Style Drift Score: A quantitative measure. The

Journal of Portfolio Management, Volume Fall, pp. 75-83.

Sandoval, L., 2012. Correlation of financial markets in times of crisis. Physica A: Statistical

Mechanics and its Applications, 391(1-2), pp. 187-208.

Sharpe, W., 1988. Determining a Fund's Effective Asset Mix. Investment Management

Review, Volume December, pp. 59-69.

Sharpe, W., 1992. Asset Allocation: Management Style and Perfomance Measurement. The

Journal of Portfolio Management, Volume Winter, pp. 7-19.

Wermers, R., 2010. A Matter of Style: The Causes and Consequences of Style Drift in

Institutional Portfolios. [Online]

Available at: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1573410

[Accessed 16 April 2016].

Yuhong, Z. & Wenwei, G., 2013. An Empirical Study on the Relationship between Style

Drift, Fund Flow and Market Timing. International Journal of Digital Content Technology

and its Applications(JDCTA), April, 7(7), pp. 387-395.

Exhibit 2 – Drift percentage change under different circumstances

12 Month Rolling Return Drift by period (% Change) (Two CC)

V C G V C G

L 24.56% -8.98% -4.96% L -5.38% -5.21% 5.33%

M 28.65% -17.06% -1.18% M 8.84% 32.41% -4.61%

S 44.08% 8.93% -10.99% S -0.69% 13.95% -15.74%

V C G V C G

L 18.95% 3.31% -3.14% L 7.35% -2.39% -8.49%

M -58.22% 13.53% -9.17% M 46.60% -6.92% 5.75%

S -8.43% 2.60% -5.68% S 14.44% -2.26% -0.92%

V C G V C G

L -6.25% 8.19% -13.16% L 41.09% -5.87% -22.94%

M 5.94% 2.68% -3.36% M -9.15% 19.17% -12.50%

S 2.90% 4.31% 7.13% S 54.30% 29.84% -24.92%

2000-2015

2000-2003 2003-2006

2006-2009 2009-2012

2012-2015

Exhibit 1 – Morningstar Style Matrix

Image from: http://download.e-bookshelf.de/download/0000/5893/77/L-X-0000589377-0001439822.XHTML/benz_9781118046142_oeb_002_r1.gif

Note: Core = Blend

24 Month Rolling Return Drift by period (% Change) (One CC)

24 Month Rolling Return Drift by period (% Change) (Two CC)

V C G V C G

L 17.05% -6.16% -10.51% L 8.66% -9.48% 10.95%

M 10.27% 13.51% 6.54% M -36.30% 17.50% -12.66%

S 0.50% 17.56% -10.09% S 17.21% 21.00% -21.28%

V C G V C G

L 15.50% 0.00% -4.38% L 1.75% 1.60% -10.39%

M -21.56% 7.31% -0.35% M 24.91% -8.60% 3.67%

S -10.27% -2.89% -1.86% S 11.76% 3.63% 0.66%

V C G V C G

L -2.02% 7.31% -12.89% L 46.44% -7.38% -25.89%

M 10.56% 1.35% -2.76% M -23.90% 32.57% -6.52%

S -0.28% 1.68% 6.57% S 17.81% 45.54% -25.50%

2012-2015

2000-2003 2003-2006

2006-2009 2009-2012

2012-2015

V C G V C G

L 20.01% -12.61% -8.11% L -2.15% -3.42% 11.48%

M 28.65% 11.62% 5.82% M -28.13% 13.73% -10.90%

S -14.77% 32.43% -6.84% S 20.19% 18.10% -23.15%

V C G V C G

L 14.65% 0.86% -4.83% L 1.08% 2.09% -10.39%

M -30.88% 12.74% 1.51% M 15.99% -16.22% 3.67%

S -17.45% -0.31% -1.86% S 22.72% 4.40% 0.66%

V C G V C G

L -1.12% 7.31% -12.89% L 34.55% -6.74% -23.90%

M 10.56% 8.55% -2.76% M -18.05% 30.16% -3.51%

S -7.21% 0.69% 6.57% S -3.71% 63.90% -24.64%

2000-2015

2000-2003 2003-2006

2006-2009 2009-2012

2012-2015