municipal dc plans: the evolving fiduciary landscape

TRANSCRIPT

Municipal DC Plans:The Evolving Fiduciary Landscape

One Hundred Northfield Drive, Windsor, CT 06095 Toll Free: 866.466.9412 www.fiallc.com

Important Disclosure Information: Please remember that different types of investments involvevarying degrees of risk, and there can be no assurance that the future performance of any specificinvestment, investment strategy, or product (including the investments and/or investment strategiesrecommended or undertaken by Fiduciary Investment Advisors), or any non-investment related content,made reference to directly or indirectly in this report, will be profitable, equal any corresponding indicatedhistorical performance level(s), be suitable for your portfolio or prove successful. In preparing this report,Fiduciary Investment Advisors, LLC has relied upon information provided by third parties. Due to variousfactors, including changing market conditions and/or applicable laws, the content may no longer bereflective of current opinions or positions. Fiduciary Investment Advisors is neither a law firm nor acertified public accounting firm and no portion of the content should be construed as legal or accountingor tax advice. Please remember to contact Fiduciary Investment Advisors, in writing, if there are anychanges in your financial situation or investment objectives for the purpose ofreviewing/evaluating/revising our previous recommendations and/or services. A copy of FiduciaryInvestment Advisors' current written disclosure statement discussing our advisory services and fees isavailable for review upon request.

2

The following information is intended to be used as a general framework to establish best practice policies for the committee and plan.The committee should consult with legal counsel for advice specific to the plan.

3

Today’s Speakers

Virginia McGarrityPartner,

860.275.8291

Michael GossExecutive Vice President,

Fiduciary Investment [email protected]

4

The Changing Fiduciary Landscape

• Governmental plans are not subject to ERISA, but…

o Plan fiduciaries are often held to similar standards of conduct!

• Essential to understand which plan functions are performed as an employer versus those performed as a plan fiduciary

• Numerous lawsuits filed by participants against plan sponsors highlight the important and difficult responsibilities plan fiduciaries are charged with

• This session sets out the basic standards of conduct, the lessons to be learned from participant lawsuits, and ways to minimize fiduciary liability

5

• Connecticut Reporting Requirement for Section 403(b) Planso Enacted June 27, 2017; effective January 1, 2019o Resulted from issues raised by Connecticut teachers that they were not properly

advised of fees and regretted their investment selectionso Political subdivisions (e.g., municipal school districts) administering a 403(b) plan

must provide employees with a disclosure that sets forth certain information regarding fees

o Still awaiting further guidance from the State, however a disclosure similar to the ERISA Section 404(a) notice is likely sufficient

• Connecticut Fiduciary Duties Applicable to Certain Financial Plannerso Enacted July 5, 2017; effective immediatelyo Generally applies to financial planners that are not already regulated by some other

state or federal law o Requires covered financial planners to provide disclosures to consumers, upon

request, each time they make a recommendation to the consumer, whether the financial planner has a fiduciary duty to the consumer

Connecticut Focuses on Fiduciary Standards

6

• Recent lawsuits brought by plan participants against plan sponsors are very instructional

• 401(k) plan litigation – at issue is whether plan fiduciaries:o Acted prudently in selecting and monitoring plan investments and making

changes when warrantedo Understood service agreement, compensation arrangementso Ensured plan fees are reasonable, and properly disclosed

• 403(b) plan litigation – at issue is whether plan fiduciaries acted in the best interest of participants when they allowed:

o Multiple recordkeeperso Included too many and/or duplicative investment choiceso Paid asset-based recordkeeping fees (vs. per participant charge)o Offered funds with high fees and/or restrictions

• Court decisions are based more on the process fiduciaries use rather than the particular result obtained

Participant Lawsuits

Fiduciaries & Their Duties

FIA’s New Partnership

Needs Assessment Analysis

Best Practices in Carrying out Fiduciary Oversight

Establishing & Following a Process for

Proper Oversight

Fiduciary Oversight & Responsibilities

7

• Anyone who exercises discretion or control with regard to the plan may be a Fiduciary, which may include:

o Towno Board of Selectmeno Plan Investment Committeeo Individuals Identified in the Plan as a “Named Fiduciary”o Third Parties (e.g., Investment Consultants)o Individuals/Committee Members who Appoint Fiduciaries

• Each plan must have a named Fiduciary identified in the plan document

Types of Fiduciaries

8

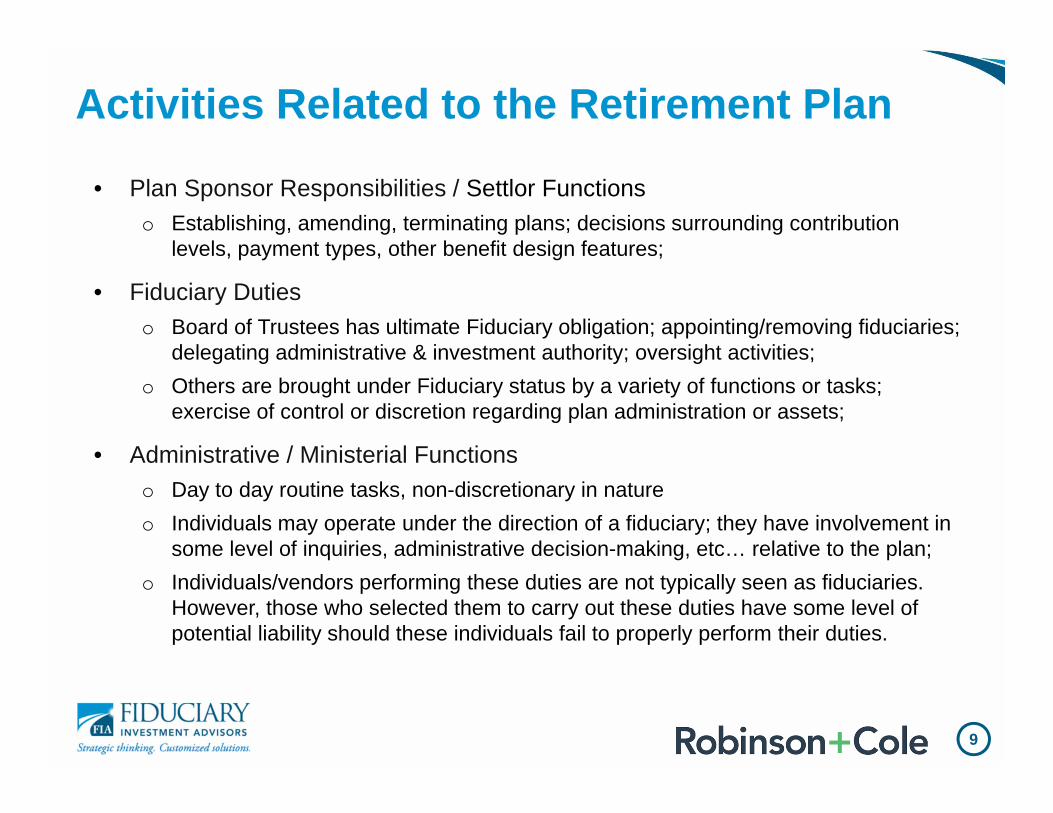

Activities Related to the Retirement Plan

• Plan Sponsor Responsibilities / Settlor Functions o Establishing, amending, terminating plans; decisions surrounding contribution

levels, payment types, other benefit design features;

• Fiduciary Dutieso Board of Trustees has ultimate Fiduciary obligation; appointing/removing fiduciaries;

delegating administrative & investment authority; oversight activities;o Others are brought under Fiduciary status by a variety of functions or tasks;

exercise of control or discretion regarding plan administration or assets;

• Administrative / Ministerial Functionso Day to day routine tasks, non-discretionary in natureo Individuals may operate under the direction of a fiduciary; they have involvement in

some level of inquiries, administrative decision-making, etc… relative to the plan;o Individuals/vendors performing these duties are not typically seen as fiduciaries.

However, those who selected them to carry out these duties have some level of potential liability should these individuals fail to properly perform their duties.

9

10

You’re a Fiduciary: Now What?

• While governmental plans are not subject to ERISA , they are subject to the applicable provisions of the Internal Revenue Code (the “Code”)

o Section 401(a)(2) requires the exercise of prudence in the investment of plan assets (derived from the “exclusive benefit rule”)

o Many municipalities look to ERISA for guidance and best practices

• State law considerationso Conn. Gen. Stat. § 7-400 et seq. generally not applicable

• Common law of trusts as guidanceo ERISA borrows heavily from common law

• Plan documents

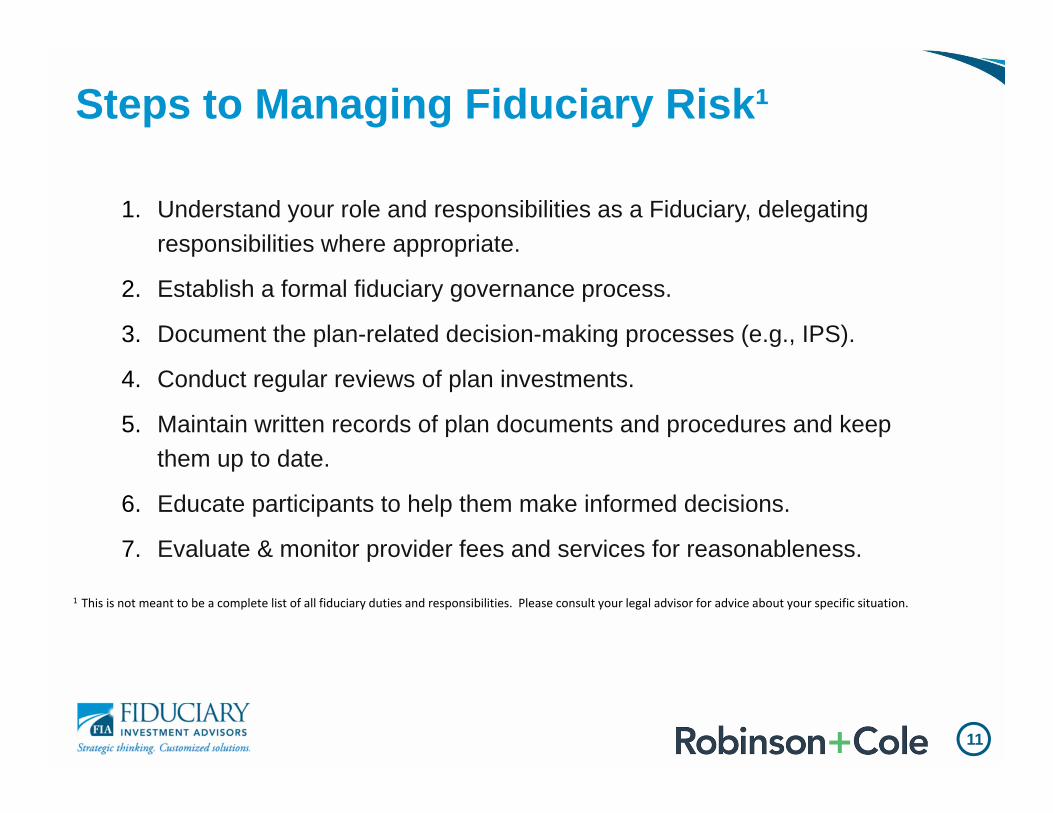

1. Understand your role and responsibilities as a Fiduciary, delegating responsibilities where appropriate.

2. Establish a formal fiduciary governance process.

3. Document the plan-related decision-making processes (e.g., IPS).

4. Conduct regular reviews of plan investments.

5. Maintain written records of plan documents and procedures and keep them up to date.

6. Educate participants to help them make informed decisions.

7. Evaluate & monitor provider fees and services for reasonableness.

1 This is not meant to be a complete list of all fiduciary duties and responsibilities. Please consult your legal advisor for advice about your specific situation.

Steps to Managing Fiduciary Risk¹

11

12

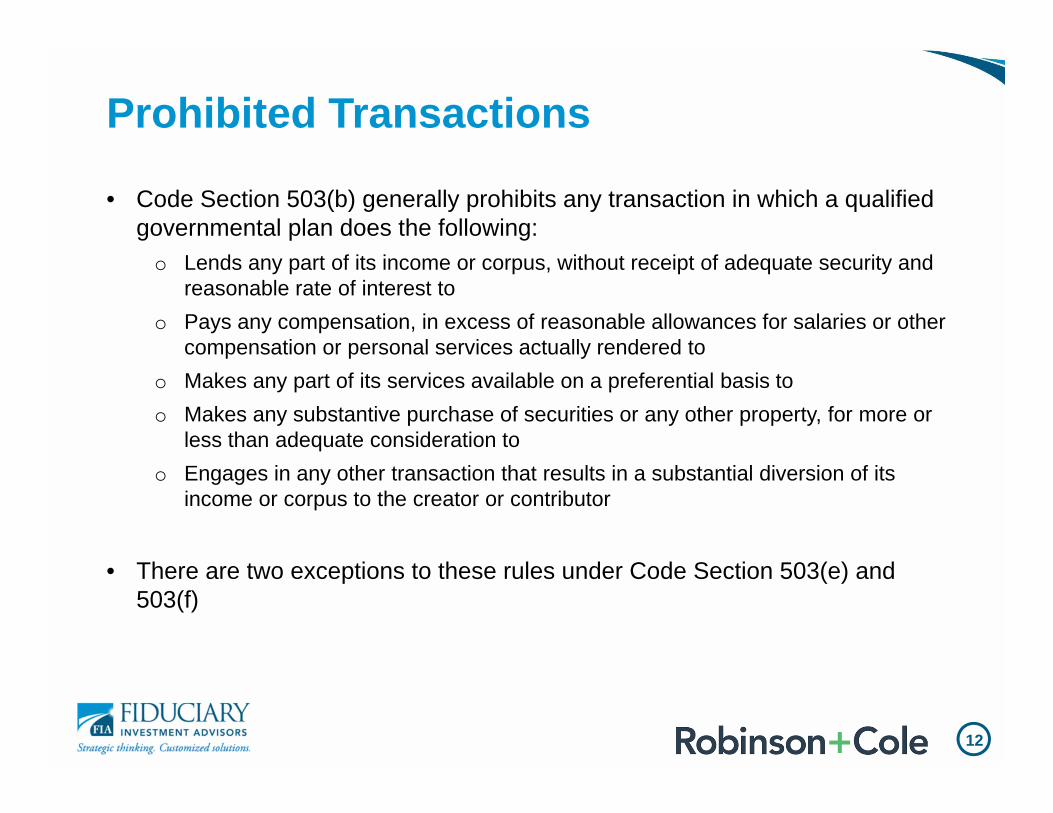

• Code Section 503(b) generally prohibits any transaction in which a qualified governmental plan does the following:

o Lends any part of its income or corpus, without receipt of adequate security and reasonable rate of interest to

o Pays any compensation, in excess of reasonable allowances for salaries or other compensation or personal services actually rendered to

o Makes any part of its services available on a preferential basis too Makes any substantive purchase of securities or any other property, for more or

less than adequate consideration too Engages in any other transaction that results in a substantial diversion of its

income or corpus to the creator or contributor

• There are two exceptions to these rules under Code Section 503(e) and 503(f)

Prohibited Transactions

Diversify the investment

options to allow participants to manage risk

FIA’s New Partnership

Needs Assessment Analysis

Act exclusively in the interest of

plan participants and beneficiaries

Act in accordance with the “prudent expert rule”

Duty of Loyalty:Act exclusively in the interest of plan participants and beneficiaries

Duty of Prudence: Act in accordance with the “prudent expert rule”

Duty to Diversify Investments:Diversify the investment options to allow participants to manage risk

Duty to Follow Plan Documents:Follow the plan documents and instruments governing the plan

Duty to Avoid Prohibited Transactions:Ensure legal and appropriate transactions and be free from conflict

“Five Key Duties”

ERISA Fiduciary Responsibilities

13

Prudence focuses on the process, not results, surrounding fiduciary decision-making.

1. Select and Monitor Plan Investments2. Analyze Investment & Service Provider Fees3. Evaluate Practice and Policy4. Focus on Participant Outcomes

Fiduciary Best

Practice

Participants

Practice/Po

licy

Fees

Investments

Establishing & Following a Process

14

Investment Options: The fund menu should offer options with differing risk/return characteristics in order to minimize the potential risk of large investment losses (and provide for the ability to create a well diversified portfolio).

Principal areas of oversight: menu design (asset category selection); procedural process (fund selection and oversight); and on-going monitoring (performance benchmarking).

Fund Menu Design: Periodically reviewing menu design is a way for sponsors to strengthen investment offerings and improve overall participant engagement.

Default Investment Alternative: The Committee may designate this option for the plan for participants who have not made an investment election.

Select & Monitor Plan Investments

The plan fiduciary has an obligation to prudently select such vehicles [for example, mutual funds], as well as a fiduciary obligation to periodically evaluate their performance to determine whether the vehicles should continue to be available as participant investment options.

15

“The Employee Retirement Income Security Act of 1974, as amended (ERISA), requires employee benefit plan fiduciaries to act solely in the interests of, and for the exclusive benefit of, plan participants and beneficiaries. As part of that obligation, plan fiduciaries should consider cost, among other things, when choosing investment options for the plan and selecting plan service providers.”¹*

¹ Source: Department of Labor 401(k) Plan Fee Disclosure Form*Do not apply to government plans but are considered best practices for Fiduciaries

Analyze Investment & Service Provider Fees

Plan fiduciaries have a responsibility to understand and benchmark all fees and services associated with the plan. Quantify all plan fees, both direct and indirect Determine who is paying the fees (sponsor, participants, combination.) Compare and benchmark fees to determine reasonableness Evaluate which services are being paid for with plan assets Negotiate with plan service providers, if needed, to improve plan costs Document discussions surrounding the review of plan fees, new pricing trends, etc.

Sponsors must provide plan participants with sufficient information about fees to enable them to make informed investment decisions.

Sponsors should ensure that the required fee disclosures under 408(b)(2) and 404(a)(5) (service provider and participant level disclosures) are accurate and distributed. They should be prepared to produce such documentation in the event of an audit.*

16

Evaluate Practice & Policy

Evolving Environment: The regulatory and legislative landscape surrounding retirement plans is constantly evolving. Staying informed on new initiatives and marketplace trends is critical for plan sponsors and oversight committees.

Investment Policy Statement: Helps define the plan’s goals and objectives and provides a guideline to aid with investment decisions. A well-written IPS serves to: Create the first step in establishing the Fiduciary Trail SM

Clearly articulate the plan’s long range investment framework Define Roles and Responsibilities of the Fiduciaries Describe the plan’s long range investment framework Outline process for investment selection, monitoring and replacement

Other Committee Best Practices: Periodically verify fiduciaries understand their responsibilities Implement Fiduciary Governance documents Schedule periodic meetings, establish a quorum, approve minutes Document all investment and plan related decisions

Plan sponsors must understand and be in compliance with regulations (ERISA, DOL, IRS,…). Sponsors and oversight committees should also stay informed on trends and best practices in the retirement marketplace.

17

Focus on Participant Outcomes

Communication & Education Programs Focused on “Preparedness”: Sponsors have an obligation to make available education materials for participants on retirement

investments Strategies include general education, targeted topics, one-on-one guidance

Evaluation of the Retirement Readiness of plan participants: Can help determine overall health of the plan and whether goals are being accomplished. Assessment at

the subgroup level can help focus the effort.

Plan Design Features: Automatic enrollment Automatic escalation Other features that engage participants & promote positive outcomes

Selection/Monitoring of Recordkeeping services: Leverage the tools, resources and capabilities available Consider RFI/RFP to periodically benchmark vendor services & costs

Sponsors should recognize they play an important role in promoting retirement readiness and improving participant outcomes. Many are taking on more responsibility for assisting employees in their transition from work to retirement.

18

Prudence focuses on the process surrounding fiduciary decision-making, not the results.

1st Quarter: Fee Focus Investment Review Administrative Fee Review Investment Expense Analysis Benchmarking and Trends Recordkeeper Negotiations

2nd Quarter: Practice & Policy Focus Investment Review Investment Policy Statement Review Regulatory and Legislative Update Committee Best Practices Bonding and Fiduciary Insurance

3rd Quarter: Participant Focus Investment Review Recordkeeper Services Update Plan Demographic Review Education & Advice Plan Plan Design Benchmarking

4th Quarter: Investment Focus Investment Review Default Investment Analysis Asset Class Updates Trends and Best Practices Investment Menu Review

Fiduciary Governance Calendar

19

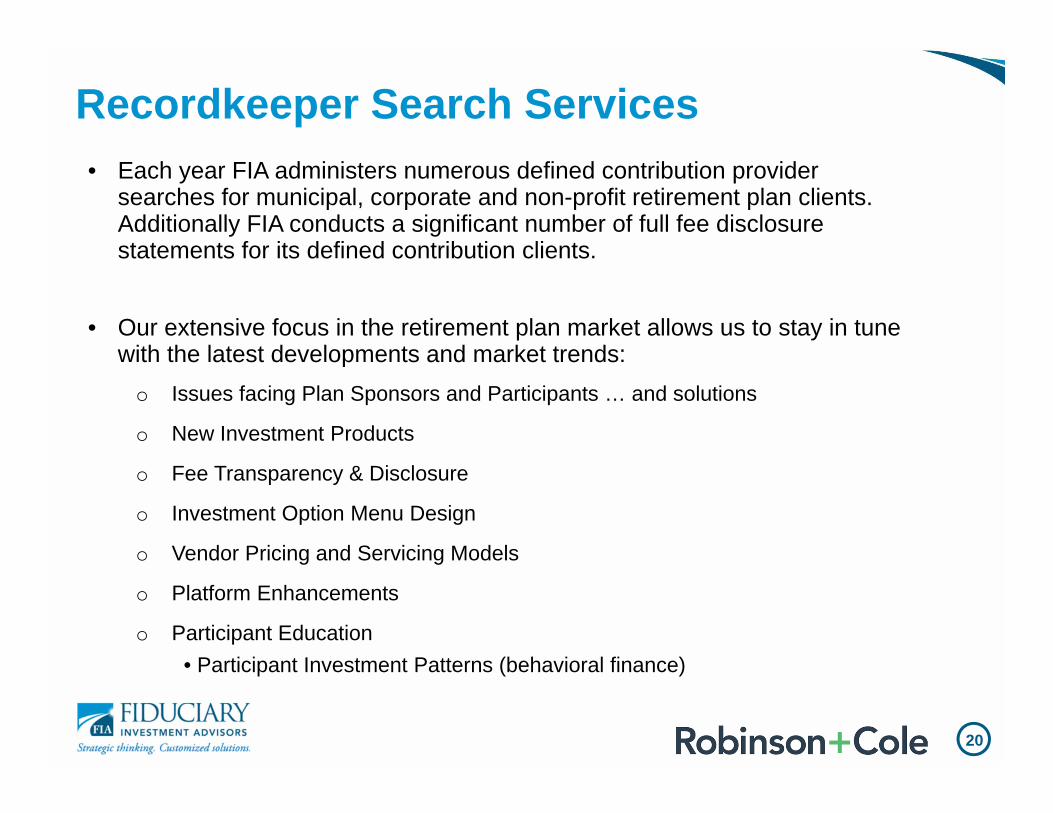

• Each year FIA administers numerous defined contribution provider searches for municipal, corporate and non-profit retirement plan clients. Additionally FIA conducts a significant number of full fee disclosure statements for its defined contribution clients.

• Our extensive focus in the retirement plan market allows us to stay in tune with the latest developments and market trends:

o Issues facing Plan Sponsors and Participants … and solutions

o New Investment Products

o Fee Transparency & Disclosure

o Investment Option Menu Design

o Vendor Pricing and Servicing Models

o Platform Enhancements

o Participant Education• Participant Investment Patterns (behavioral finance)

Recordkeeper Search Services

20

Client

• Connecticut City• Committee in place• RFP to transition from a broker‐led model to a flat fee advisory structure• $117 million across 3 plans with MetLife

• 401(a), 403(b), 457(b)• 18 investment options• Large holding in Guaranteed Interest Account

• Payout options: $280,000 Market Value Adjustment or 5 year installments• Weekly in person education being provided by recordkeeper• Bundled Pricing Model

Scope of Project

• Conduct a plan diagnostic to streamline fund menu and review options for plan enhancements• Conduct a Request For Proposal to review current and potential replacement recordkeepers (10 total respondents)Outcomes

• Streamlined fund menu from 18 funds to 14 while reducing share classes where applicable• Moved all assets to a new recordkeeper

• The new stable value investment covered the Market Value Adjustment and reduced the return on the stable value by 45bps untilthe MVA is recouped

• Reduced recordkeeping fees by 80% ($283,335 annually); reduced advisory by ~50%• Eliminated all revenue sharing, assessing fees equally across all participant accounts• Maintained weekly education schedule, and enhanced communication capabilities• Greatly enhanced administrative support and participant experience

Municipal RFP Case Study 1

21

Client

• Connecticut City• Committee in place• Approximately $54 million across 2 plans with Voya

• 401(a), 457(b)• 18 investment options• Large holding in Fixed Account

• Weekly in person education being provided by recordkeeper• Bundled Pricing Model within Group Annuity Contracts

Scope of Project

• Conduct a plan diagnostic to streamline fund menu, on Voya’s mutual fund platform, and review options for plan enhancements

Outcomes

• Streamlined fund menu from 18 funds to 12 mutual funds while reducing all share classes• Reduced recordkeeping fees by 65% ($39,386 annually); reduced investment expenses by 60% ‐ savings of ~$150,000 annually• Eliminated all revenue sharing, assessing fees equally across all participant accounts• Maintained weekly education schedule, and enhanced communication capabilities• Greatly enhanced administrative support and participant experience

Municipal RFP Case Study 2

22

23

• Eligible 457(b) plans enacted in 1979o For 20 years, there was limited fiduciary responsibility because plan assets did not

have to be held in trust (“hands off” approach)

• As of January 1, 1999, all assets in governmental 457(b) plans must “be held in trust for the exclusive benefit of participants and their beneficiaries”

o Trust requirement imposed additional fiduciary responsibilityo This language is identical to the language in Section 401(a)(2)

• The following factors should be considered under the exclusive benefit rule:o Investment costs do not exceed fair market value at the time of purchaseo Investment provides a fair return commensurate with the prevailing rateo Plan maintains sufficient liquidity to permit distributions in accordance with the terms

of the plano Safeguards and diversity that a prudent investor would adhere to are present

What About 457(b) Plans?