multinational companies and china: what future? · market for cars, air conditioners and lcd-tvs,...

TRANSCRIPT

Multinational companies and China: What future?

An Economist Intelligence Unit report

Sponsored by:

© The Economist Intelligence Unit Limited 2011 1

Multinational companies and China: What future?

Contents

Preface 2

Executive summary 3

Introduction 6

Chapter 1: The big picture 9 Hope, hype and reality 10

Justifiedoptimism? 12

Chapter 2: The consumption story 13

Chapter 3: The perils of success 16 Is it enough 16

Onestrategy,ortwo? 19

Isittoomuch? 20

Lacoste: Who’s your benchmark? 22

Chapter 4: Whose hubris? 23 Suddenly uncertain 25

Chapter 5: The invisible hand 28 Aiming high 29

The real issue 30

A non-standard approach 32

Atwhatprice? 32

High-speed trains: A series of unfortunate events 33

Getting on with it 34

Chapter 6: Honour thy master 36 The renminbi 38

By other means 41

Nissan: According to plan 42

Investing in R&D 43

Chapter 7: Gearing up to play the game 44 Overcoming the fear factor 46

Appendix: Survey results 48

© The Economist Intelligence Unit Limited 20112

Multinational companies and China: What future?

Multinational companies and China: What future? is an Economist Intelligence Unit report, sponsored by CICC. The EIU conducted the survey and interviews independently and wrote the report. Gaddi Tam was responsible for layout. The cover design is by Harry Harrison.

ThefindingsandviewsexpressedherearethoseoftheEIUaloneanddonotnecessarilyreflecttheviews of the sponsor.

Many interviewees for this report have asked to remain anonymous and we have respected their wishes. We would like to thank all interviewees for their time and insights.

November 2011

Preface

© The Economist Intelligence Unit Limited 2011 3

Multinational companies and China: What future?

Executive summary

W ith leading economies of the world in dire shape, China now has become a crucial engine of global growth—sooner than anyone had imagined. While developed countries remain in a quagmire,

Chinakeepsroaringahead.Whileconsumerselsewhereworryabouttheirjobsandfinancialfuture,manyin China are getting rich, and about to get even more so.

Beyond the headlines about China’s growing weight in the world—whether in purchasing power or otherwise—what does China now mean for multinational companies (MNCs; unless otherwise noted, this termreferstonon-Chinesemultinationals)?AretheybackinguptheirtalkabouttheimportanceofChinawithrealinvestment?Aretheybeingrewardedinreturn?Equallyimportant,andnotunrelated,whatdoMNCsmeanforChina?Willtheybeallowedtorealisetheirdreams?Orwilltheybeheldincheckwhilelocalcompaniesimprovetheircapabilities?

This report, Multinational companies and China: What future?,outlineswhereChinacurrentlyfitsonthe agenda of MNCs and shows how global companies are recalibrating their China operations in reaction tonewrealities.Itsfindingsarebasedonasurveyof328seniorexecutivesconductedinJuneandJuly20111,aswellasin-depthinterviewswithexecutivesofmajorforeignmultinationals,businessscholarsand market analysts.

Amongthekeyfindings:

• Multinationals, large companies in particular, are clearly counting on China to deliver more. Almosthalf(49%)ofallthesurveyrespondentssaidthatthefalloutfromtheglobalfinancialcrisishasraisedtheircompanies’expectationsforChina.Amongthelargercompanies(globalrevenuesofmorethanUS$5bn)thefigureis73%.Butnotallcompaniesareplanningtoinvestmoreinordertoincreasereturns.AmongthelargercompaniescountingonChinatodelivermore,halfarecountingonexistingoperations to bring more growth.

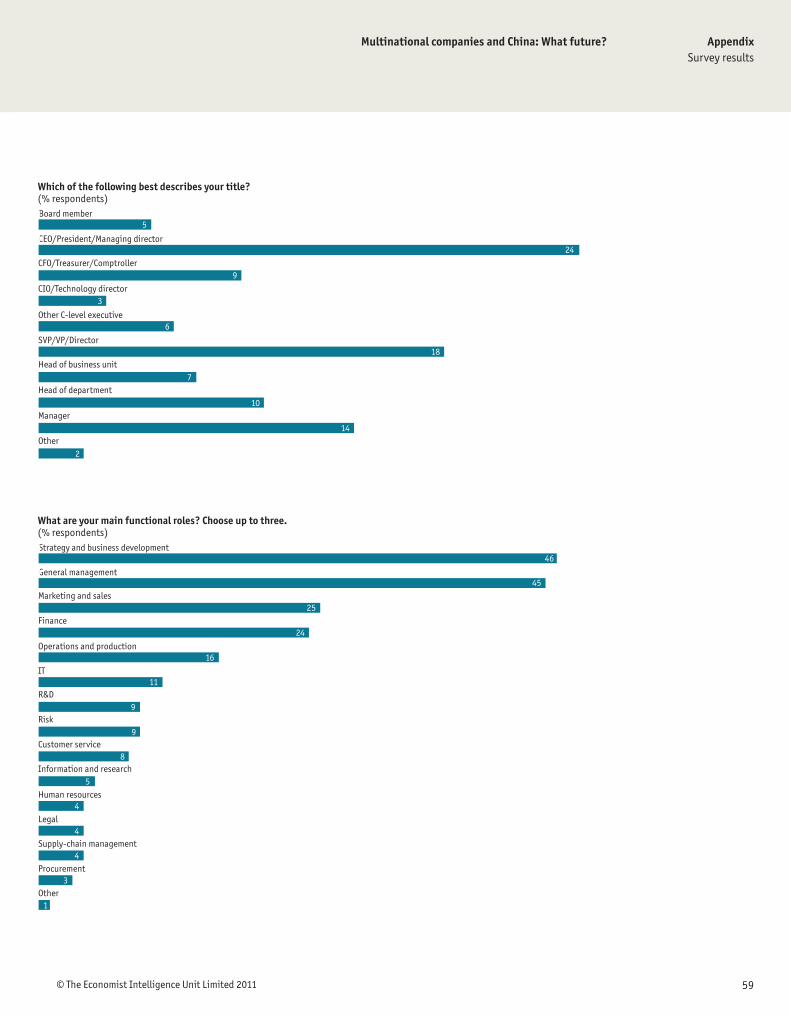

1 The survey covered 328 companies from a range of industries. The respondents came equally from companies headquartered in Europe, North America and Asia-Pacific.Intermsofsize,55%had global revenues of more thanUS$500m,with44%having more than US$1bn in revenues. For more details see appendix.

© The Economist Intelligence Unit Limited 20114

Multinational companies and China: What future?

• While MNCs are bullish, there are signs they are hedging their bets.Theexuberanceofconsumergoodsfirmsaside,Chinaseemstohavestalled,ratherthanrisen,onMNCs’agendas.Amongtherespondents to our survey, the share reporting that their headquarters view China as “critical to global strategy”was37%.Thisisdownfrom53%reportedinasimilarsurveyconductedin2004.2 But this does notmeanthatChinaisnotanimportantmarketformanyfirms.Afurther33%ofrespondentssaidthatwhile it is not critical, it is strategically important.

• Today, China is still a relatively small market for many multinationals, but this is expected to change quickly.Analysisofthefinancialresultsof70MNCs3 showed that in 2010 only ten had China revenuesthataccountedformorethan20%oftheirglobalrevenues.Formorethanhalf,Chinaaccountedforlessthan10%ofglobalrevenues.Companiesdoexpectthistochange.Only8%ofoursurveyrespondentssaidChinaisalreadytheirbiggestmarket,but17%expectittobecomesoinlessthanfiveyears,whileanother21%expectthistohappenin5-10years.

• China’s consumption story is driving MNCs’ strategy. The Chinese government’s drive to raise incomes and shift growth towards domestic consumption is likely to have a profound impact on most companies. Amongsurveyrespondents,58%saidthatthispolicyisthefactorthatwillhavethebiggestimpactontheirChinastrategy,while56%saidthatgrowthprospectsfortheirindustrywasthekeydriveroftheirChinastrategy.

• One of the greatest challenges facing multinationals is achieving “China speed”, while maintaining a low profile. Multinational companies tend to want to build more slowly and solidly than their local counterparts,butiftheydosoinChinatheircompetitorsarelikelytofillthegaps.Overall,59%ofoursurvey respondents remain focused on “improving penetration in wealthier coastal cities/southern region”,andonly33%ofthemare“currentlymovingintosecond-andthird-tiercities”.Atthesametime, companies worry about getting too far ahead of the local competition, lest they attract unwanted attention.ThiscouldexplaintheseeminglylowexpectationsofoursurveyrespondentsintermsofusingacquisitionsasaroutetogrowthinChina:only20%choseacquisitionsasthemostimportantstrategyforgrowthinChina,while63%choseorganicgrowthand46%saidjointventures.

• There are signs that multinationals’ traditional competitive advantages are beginning to erode in China. It is often taken as fact that multinationals have superior technology and better brand management, and hold more appeal for talented workers. There are signs that all of these advantages are beginning to erode in China. Even among the large companies surveyed for this report (global revenues of more than US$5bn), only one-quarter felt they have superior technology or a stronger brand, with these figuresevenlowerforthesampleasawhole.Human-resourcesconsultanciesreportthatlocaltalentisincreasingly gravitating towards mainland companies.

• China’s policies aimed at encouraging local innovation are causing a great deal of ill will among multinationals.Amongoursurveyrespondents,49%wereconcernedorveryconcernedthattheywould

2 Coming of age? Multinational companies in China, Economist Intelligence Unit, 2004. The demographic for the 2004 survey was similar to the 2011 survey,thoughnearly70%ofthe217respondentsin2004were from corporations with global revenues of US$1bn or more; in the 2011 survey, 44%ofthe328respondentshad US$1bn in revenues or more. Focusing only on the responses of companies with more than US$1bn in globalrevenues,thefigureis still down in the 2011 survey—48%viewthecountryas critical.

3 In compiling our list we examinedInterbrand,S&P100Global,andS&P500companiestofindthosethatdisclosed their China revenues in their latest published annual reports or other reliable sources.

© The Economist Intelligence Unit Limited 2011 5

Multinational companies and China: What future?

beforcedtogiveuptheirIPinexchangeformarketaccess.Amongbigcompaniesthefigurewas52%.Whilesomeofthemoreobjectionablemeasureshavebeensoftenedbythecentralgovernment,executivesstillworryaboutlocalprotectionism.And46%ofrespondentssaidthatChina’sregulatoryenvironmentandindustrialpolicieswerelikelytohaveabigimpactontheirChinastrategyinthenextfiveyears.

• Multinationals need to reorganise to match the importance being placed on China. Among large companiesrespondingtooursurvey,only8%saidthattheirChinaCEOsitsonthecompanyboard(for45%,theChinaCEOreportsintoregionalheadquarters).However,40%oflargecompaniessaidthattheyhadpostedveryseniorexecutivestogreaterChina,amoveaimedatimprovingunderstandingofChinaandspeeding decision making at headquarters.

• While planning how to win in China, multinationals are beginning to think how they can leverage their relationships there to compete elsewhere in the world. While most arrangements seem to involve cooperativeagreementswithChinesepartnersontheuseofspecificproductsinothermarkets,therearesigns that this could be taken a step further to include joint ventures in third countries.

© The Economist Intelligence Unit Limited 20116

Multinational companies and China: What future?

Introduction

M any foreign multinational companies4 (MNCs) have long viewed China, with its 1.3bn people, as a dream market, with the emphasis on “dream”. With leading economies of the world in

dire shape, China now has also become a critical engine of global growth—sooner than anyone had imagined. While developed countries remain in a quagmire, China keeps roaring ahead. Consumers elsewhereworryabouttheirjobsandfinancialfuture,butmanyinChinaaregettingrich,andabouttoget even more so.

In many sectors, China is now an emerged, rather than an emerging, market. It is the world’s largest market for cars, air conditioners and LCD-TVs, to name just a few products. No doubt, China will soon be the greatest consumer of a whole host of other goods from medicines to designer handbags.

Beyond the headlines about China’s growing weight in the world—whether in purchasing power or otherwise—whatdoesChinanowmeanforMNCs?AretheybackinguptheirtalkabouttheimportanceofChinawithrealinvestment?Andaretheybeingrewardedinreturn?Equallyimportant,andnotunrelated,whatdoMNCsmeanforChina?Willtheybeallowedtorealisetheirdreams?Orwilltheybeheldincheckwhilelocalcompaniesimprovetheircapabilities?

This report, Multinational companies and China: What future?,assesseswhereChinacurrentlyfitson the agenda of MNCs, and discusses how some are recalibrating their China operations in reaction to newrealities.Itsfindingsarebasedonasurveyof328seniorexecutivesatnon-ChinesemultinationalsconductedinJuneandJuly2011,aswellasin-depthinterviewswithexecutivesofmajorforeignmultinationals,businessscholarsandmarketanalysts,andotherpublishedreportsonspecificindustries.

Multinationals’futureinChinavariesgreatlydependingonindustry,companysizeandindeedonthe individual company concerned. But some general observations can be made. First, companies are counting on China to deliver more. But not all are planning to plough in more investment in the name ofhigherreturns.Almosthalf(49%)ofallthesurveyrespondentssaidthatthefalloutfromtheglobal

4 Throughout this report, unless otherwise noted, “MNCs” refers to non-Chinese multinational companies.

© The Economist Intelligence Unit Limited 2011 7

Multinational companies and China: What future?

financialcrisishasraisedtheircompanies’expectationforChina.Butwhile21%are“investingmoreinChinainthehopethatitwillmakeupfordeterioratingmarketselsewhere”,28%are“countingonexistingoperationsinChinatodelivermoreof[their]globalrevenue”.Largercompanies(revenuesofmorethanUS$5bn)aremorewilling—andpresumablyable—tospend:73%arecountingonChinatodelivermore,buttheyarealmostevenlysplitbetweeninvestingmoreandcountingonexistingoperations to deliver growth.

YetChinaisnotascrucialtoforeigncompaniesasmaybeexpected,givenwidespreadhypeaboutitsgrowth. The share of respondents reporting that their headquarters views China as “critical to global strategy”was37%inour2011survey,downfrom53%reportedinasimilarsurveyconductedin2004.5 Although the survey sample from 2004 had a higher percentage of larger companies, when we look only at theresponsesofcompanieswithmorethanUS$1bninglobalrevenues,thefigureisstilldowninthe2011

Counting on ChinaHow has the fallout from the global financial crisis affected your company’s expectation for China? Choose the one answer that best applies.(% respondents)We are counting on our existing operations in China to deliver more of our global revenue

We are investing more in China in the hope that it will make up for deteriorating markets elsewhere

We are postponing further investment in China because of deterioration in our main markets

We are repatriating more profits from China to shore up balance sheets at headquarters

Our expectation has not changed

Source: Economist Intelligence Unit survey

2836

2137

94

21

4022

Big companiesAll respondents

2004 total2011 total 2011 big companies

Critical, or just important?From the perspective of your global headquarters, which statement best describes China?(% respondents)It is critical to global strategy

It is strategically important, but not critical

It is on a par with other emerging markets

We are still exploring the market

It will be a niche market for us

Don’t know

n.a.

Source: Economist Intelligence Unit survey

3748

52.5

3336

40.6

95

5.5

139

1.4

5

21

5 Coming of age? Multinational companies in China, Economist Intelligence Unit, 2004. The demographic for the 2004 survey was similar to the 2011 survey,thoughnearly70%ofthe217respondentsin2004were from corporations with global revenues of US$1bn or more;inthe2011survey,44%of the 328 respondents had US$1bn in revenues or more.

© The Economist Intelligence Unit Limited 20118

Multinational companies and China: What future?

survey—48%viewthecountryascritical.Still,thatisafairlylargepercentageofcompaniesbankingonChina. And even those for whom China is not critical view it as important.

Indeed,basedonourqualitativeinterviewswithmultinationalexecutivesandserviceprovidersworking with them, it seems that foreign companies that have so far only dipped their toes in China are seriously considering taking a headlong dive. Many that had been to China and left in failure are now returning.EventhosethathavebeenaggressivelyexpandinginthecountryforyearsarerecalibratingtoseizethehistoricopportunitythatChinapresents—thosewithvaluabletechnologyaretryingtofigureout how to do so without losing their shirts. At the same time China is presenting new opportunities in areassuchascapitalraisingandresearchanddevelopment(R&D).

ButChinafromhereonisgoingtobecomemoredifficult(notthatitwasevereasy).Thepost-crisisself-confidenceoftheChinesegovernment,companiesandpeopleissoaringtothepointwhereitstrikesmany outsiders as hubristic. Today, some foreign companies in China wonder how long they will be welcome. While smaller foreign consumer-goods makers, retailers and lower-tech companies seem largely toflybelowtheradar,othersfeeltheyarebeingwatchedcarefully.Chinaismakinggreaterdemands—especially on foreign companies with proprietary knowhow and cutting-edge technologies. Competition is already brutal. To build a winning business in China, foreign multinationals must now plan even more meticulously—as well as make tangible contributions to the host country’s continued economic development.

TheimageofChinathatemergesfromthisresearchisacountryofoutsizedpotential,boundlessambitionandincreasingcomplexity.TherelentlessriseoftheChinamarketremainsoneofthemostimportant global business stories today. But how this story ends will not be the same for all MNCs. That will depend on how well each company writes its own subplot.

© The Economist Intelligence Unit Limited 2011 9

Multinational companies and China: What future?

Chapter 1: The big pictureThe role China now plays in the world economy is pivotal. But its role in the global revenues of multinational companies is, for the moment, less so.

TheglobalfinancialcrisishasundeniablyraisedChina’sstatureintheworld.Thankstoitsabilitytomaintainneardouble-digitannualGDPgrowththroughthetumultof2008-09,Chinaovertook

Japanastheworld’ssecond-largesteconomyin2010.Beforetheglobalfinancialcrisiserupted,GoldmanSachshadexpectedChinatosurpasstheUSastheworld’sbiggesteconomyaround2041.But now, the Wall Street bank projects that the Chinese economy will overtake that of the US by as earlyas2027.6 The Economist Intelligence Unit (EIU) forecasts that on a purchasing power parity (PPP)basisitwilldosoby2017.

China’s growth prospects look good in the short to medium term as well. During 2012-15 the EIU forecastsChina’sGDPtoexpandbyanannualaverageof8.4%.Thatwouldbeonlymarginallylowerthanthe9%growthexpectedin2011.

This dramatic reversal of fortunes between the West and the rest has transformed the way many MNCslookatChina(aswellasotherlargeemergingmarkets,suchasIndiaandBrazil).Simplyput,itis no longer seen as a major market for the future but a place to make big money now. While it may not becrucialtoallcompanies,Chinacertainlyrankshighlyontheglobalagenda.Inadditiontothe37%ofsurveyrespondentswhosaidtheirheadquartersviewedChinaascritical,another33%vieweditas“strategicallyimportant,butnotcritical”(thoughthisfigurewasalsodownfromthe2004survey,where41%ofrespondentssaidthis).Only13%saidtheywere“stillexploringthemarket”.

Thelatestfiguresforforeigndirectinvestment(FDI)alsosuggestrisinginterest.Thoughin2009,intheimmediateaftermathoftheglobalfinancialcrisis,inwardFDIdroppedtoUS$114bnfromUS$175bnthe year before, it bounced back to an estimated US$185bn in 2010 as crisis-stricken economies began torecover.(ItisworthnotingthatthesefiguresmaybeinflatedbyprivateChinesecompaniesraising

6Intermsofconstant2007US dollars. See Goldman Sachs, “The Long-Term Outlook for the BRICs and N-11 Post Crisis”, December 4th2009.

© The Economist Intelligence Unit Limited 201110

Multinational companies and China: What future?

money through offshore companies and then repatriating the funds back to China as FDI. It is estimated by Dealogic that such funds accounted for US$36bn in the 18 months to end-June 2011.)

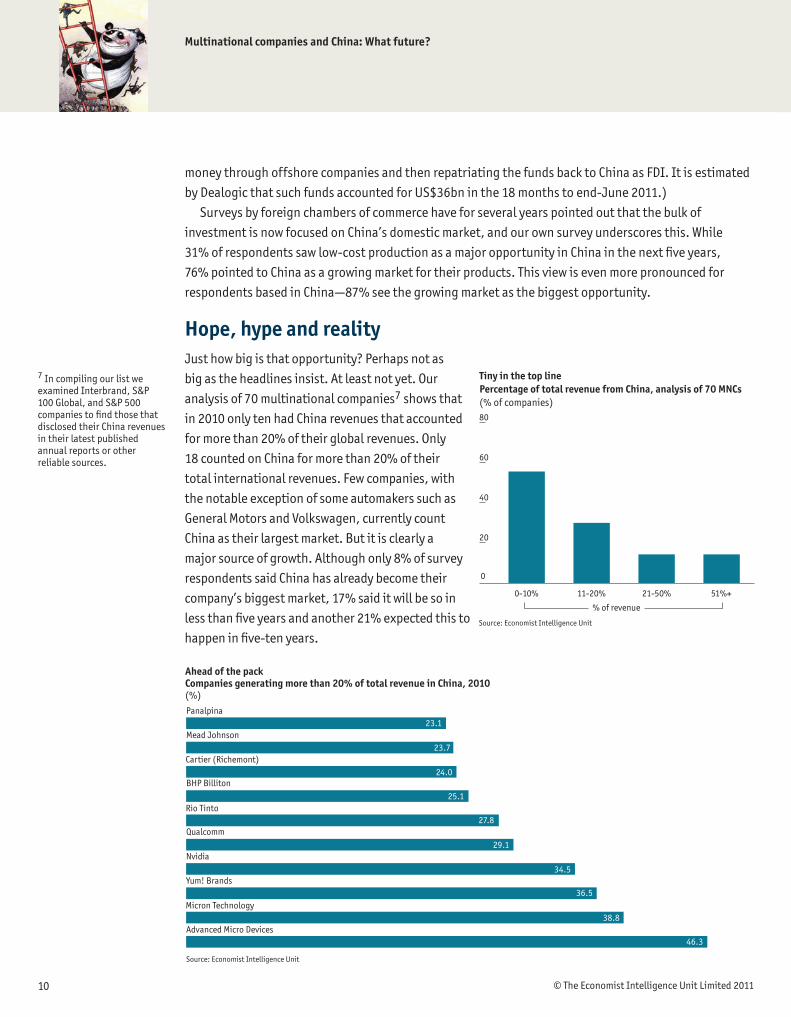

Surveys by foreign chambers of commerce have for several years pointed out that the bulk of investment is now focused on China’s domestic market, and our own survey underscores this. While 31%ofrespondentssawlow-costproductionasamajoropportunityinChinainthenextfiveyears,76%pointedtoChinaasagrowingmarketfortheirproducts.ThisviewisevenmorepronouncedforrespondentsbasedinChina—87%seethegrowingmarketasthebiggestopportunity.

Hope, hype and realityJusthowbigisthatopportunity?Perhapsnotasbig as the headlines insist. At least not yet. Our analysisof70multinationalcompanies7 shows that in 2010 only ten had China revenues that accounted formorethan20%oftheirglobalrevenues.Only18countedonChinaformorethan20%oftheirtotal international revenues. Few companies, with thenotableexceptionofsomeautomakerssuchasGeneral Motors and Volkswagen, currently count China as their largest market. But it is clearly a majorsourceofgrowth.Althoughonly8%ofsurveyrespondents said China has already become their company’sbiggestmarket,17%saiditwillbesoinlessthanfiveyearsandanother21%expectedthistohappeninfive-tenyears.

Tiny in the top linePercentage of total revenue from China, analysis of 70 MNCs (% of companies)

0

20

40

60

80

51%+21-50%11-20%0-10%

Source: Economist Intelligence Unit

% of revenue

7 In compiling our list we examinedInterbrand,S&P100Global,andS&P500companiestofindthosethatdisclosed their China revenues in their latest published annual reports or other reliable sources.

Ahead of the packCompanies generating more than 20% of total revenue in China, 2010 (%)Panalpina

Mead Johnson

BHP Billiton

Qualcomm

Cartier (Richemont)

23.1

24.0

25.1Rio Tinto

Nvidia

Yum! Brands

Advanced Micro Devices

Source: Economist Intelligence Unit

Micron Technology

27.8

34.5

29.1

36.5

38.8

46.3

23.7

© The Economist Intelligence Unit Limited 2011 11

Multinational companies and China: What future?

It’s the growth ...China as % of total revenues 2005 and 2010(%)Adidas

Advanced Micro Devices

BHP Billiton

Boeing Co

Bombardier

Bosch

Carrefour

Corning

DuPont

Intel

LG Electronics

LM Ericsson Telephone Co

Micron Technology

Motorola

Nvidia

Philips

Qualcomm

Siemens

Xilinx

Yum! Brands

Source: Economist Intelligence Unit

20102005

Astra Zeneca

8.33.0

14.5

3.2

12.325.1

4.86.1

1.35.9

8.8

4.72.4

2.4

13.8

15.58.3

7.612.8

15.938.8

13.67.0

16.934.5

9.97.8

7.029.1

4.27.7

10.219.3

13.8636.5

16.5

3.1

4.58.4

12.5

0.8

46.3

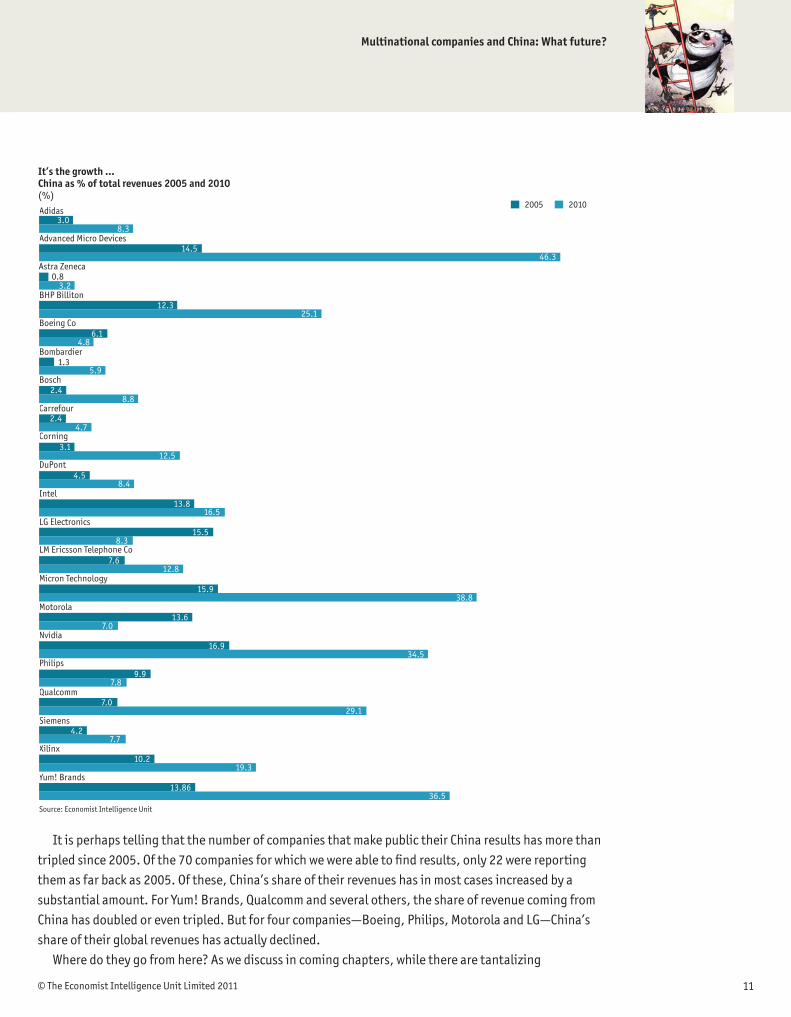

It is perhaps telling that the number of companies that make public their China results has more than tripledsince2005.Ofthe70companiesforwhichwewereabletofindresults,only22werereportingthem as far back as 2005. Of these, China’s share of their revenues has in most cases increased by a substantial amount. For Yum! Brands, Qualcomm and several others, the share of revenue coming from China has doubled or even tripled. But for four companies—Boeing, Philips, Motorola and LG—China’s share of their global revenues has actually declined.

Wheredotheygofromhere?Aswediscussincomingchapters,whiletherearetantalizing

© The Economist Intelligence Unit Limited 201112

Multinational companies and China: What future?

opportunities in China, the operating environment is tough and getting tougher. Nearly half of the executivessurveyedsaidtheywereconcernedabout“beingforcedtogiveourIP(intellectualproperty)inexchangeformarketaccess”,withmorethanone-quarter“veryconcerned”.Theshifttoahigher-wage economy will put pressure on business models. Indeed, although surveys by business chambers indicatethatmanycompaniesaremakinghealthyprofitsinChina,someobserversareoftheopinionthatsinceChinaisnolongeran“emerging”marketinmanysectors,thedaysofheftyprofitmargins—intherangeof15-20%—areover.

Onamacrolevel,Chinafacessomeseriousriskstoo.Aninflationratethathasbeenpushedtoathree-year high by multiple factors (ample liquidity, booming demand, high commodity prices and upward wage pressures) has become the biggest headache for Chinese policymakers. Rising prices disproportionately affect China’s still-relatively-poor masses, and in the past have triggered social unrest. There is also the growing possibility that China’s huge investment drive—especially at the localgovernmentlevel—anditsownexuberanthousingmarketcouldendinabust,triggeringasharpeconomicslowdowninthenextfewyears.Atimelypolicyresponsecannotbetakenforgranted,sincethegovernmentisincreasinglypreoccupiedwithpoliticalmanoeuvringaheadofthenextleadershiptransition,expectedatthe18thChineseCommunistPartycongressinlate2012.

Justified optimism?MNCexecutivesarenotoverlyconcernedaboutamajorcrisisintheChineseeconomy,buttheyarenotrulingitout.Justunder40%saidtheywereconcerned(18%veryconcerned)aboutacrisis.More—44%—wereconcernedaboutmajorsocialunrest.Butmanydoexpectaslowdowningrowth—40%expectChina’sgrowthratetoslowtomoredevelopedcountrylevels,whichwesuggestedwere3-5%,withinthenextfiveyears.

Ameasureofoptimismmaybejustified,becauseChinahasprovenscepticswrongtimeandagainduring its three-decade-long pursuit of national economic development. It is also important to distinguishbetweeninevitablecyclicaldownturnsthataffectalleconomiesandtheinexorablestructural upgrading of the Chinese economy. To understand the full implications of the latter, one only has to look at the immense collective purchasing power of Chinese consumers today.

© The Economist Intelligence Unit Limited 2011 13

Multinational companies and China: What future?

Chapter 2: The consumption story China’s determination to make consumption a more important driver of economic growth will have profound implications for many companies. Wage increases are only part of the story. Taken together with policies to provide universal healthcare, to draw more people into cities and to clean up the environment, they create opportunities galore and the potential for explosive growth.

Only a few years ago, foreign businessmen who scoffed at the notion of China’s “one billion customers” as a headline writers’ fancy were as common as those who believed that such a market has always

existedandwassimplywaitingtobefloodedwithsuperiorforeigngoods.Today,thedoubtersareinretreat. Take Arthur Kroeber, who edits the China Economic Quarterly, a publication which he admits has “longpouredscepticalcoldinkonextravagantclaimsthatthequasi-mythicalbeastknownasthe‘Chineseconsumer’ will take over the universe”. He now declares that “as facts change, we change our minds, and the facts now clearly say that the Chinese consumer has arrived”.

Whatarethesenewfacts?Inhislatestanalysis,using2009data,MrKroeberestimatesthatChinanowhasabout100mhouseholds(or300mpeople)withaverageannualhouseholdexpenditureofsomeUS$7,500.IntermsofsizethisarmyofChineseconsumers,withpowertospendattheirdiscretion,rivals that of the US. Of course, the typical American consumer spends far more than his or her Chinese counterpart and will continue to do so for many more years to come. But at an aggregate level, Chinese householdconsumptionisalreadyaboutUS$800bnayear,whichismorethanthecombinedfiguresin South Korea and Taiwan, where per-capita incomes are about twice as high as in China. “Chinese household consumption has crossed a critical threshold,” Mr Kroeber concludes.

His views are supported by the EIU’s macroeconomic forecasts. We project China’s GDP per head to rise to just under US$10,000 a year by 2015, more than double the 2010 level of around US$4,500. During2011-15,totaldisposableincomeisexpectedtogrowbywellover10%ayear.Oursurveyrespondentscertainlybelievethatconsumptionissettotakeoff:58%saidthatChina’seffortstoraise

© The Economist Intelligence Unit Limited 201114

Multinational companies and China: What future?

incomes and boost consumption is the factor that would have the biggest impact on their China strategy, and56%saidthatgrowthprospectsfortheirindustrywasthekeydriveroftheirChinastrategy.

Efforts to raise incomes could have a very big impact indeed. The Chinese government is eager to rebalanceeconomicgrowthdriversawayfrominvestmentandexportstowardsconsumption,anditisespeciallykeentoraiseincomesofthelesswell-off.Itplanstoraiseminimumwagesbyatleast13%ayearforthefiveyearscoveredbythegovernment’s12thFive-YearPlan(FYP)for2011-15.Marketforcesarealreadydrivingupwagesatanevenquickerpaceinsomeareas:since2010,30Chineseprovinceshaveraisedtheirminimumwages,byanaverageof23%,andfactoryownersinthePearlRiverDeltaexportbeltsurroundingHongKongareincreasingpaybymuchmorethanthattokeeptheirassemblylinesrunning.In2010theminimumwageinBeijingwentupbyover45%,thankslargelytothegalloping economy and tightening labour supply.

Whilecompaniesareintheshorttermscramblingtofindefficienciestooffsetrisingwages,theyarekeenly aware of the opportunity the creation of a new consumer class represents. This class will not be limitedtothefirst-tiercitiesofBeijingandShanghai,butwillemergeallacrossChinaanddeepintoitspoorerinteriorregions.Bytheendofthegovernment’s12thFYP,theEIUexpectseventhetraditionallybackwater provinces of Henan, Anhui and Sichuan to have disposable incomes per head of over US$3,660(Rmb25,000).TheNielsenCompany,amarketresearchandconsultingfirm,believesthenextbigprizearethe161mhouseholdsinthethird-andfourth-tiercitiesattheprefecturalandcountylevelsin such central and western regions.

In addition to wage rises, China’s galloping urbanisation will help push up consumption and reduce the income gap. It will, in turn, further spur economicgrowthandsupportconsumptionbyexistingcitydwellersandnewmigrants, as well as making it easier to reach more consumers, creating huge potentialopportunitiesfortheworld’sindustrialfirms.Weforecastthatby2025around1bnofChina’spopulation(or70%ofthetotal)willliveincities.Betweennowandthen170newmasstransitsystemsand40bnsquaremetresoffloorspacewillbebuilt.China’scompaniesarenotlikelytobeabletomanage all this on their own.

In the year 2025Forecasts for urbanisation

• Around1bnlivinginChina’scities

• 15citieswith25m+population

• 200+citieswith1m+population

• 170newmasstransitsystemsbuilt

• 40bnsqmoffloorspacebuilt

China urban inflows, 2010-20.

Source:ChinaRegionalForecastingService,EconomistIntelligenceUnit

On the horizonWhich of the following factors are likely to have the biggest impact on your China strategy in the next five years? Choose up to three.(% respondents)China’s efforts to raise incomes and boost consumption

The regulatory environment/industrial policies (eg, indigenous innovation)

Renminbi convertibility, if it happens

Urbanisation

Competition from Chinese companies

58

43

32Improved infrastructure (as a result of stimulus spending)

25

21

Other, please specify

Source: Economist Intelligence Unit survey

5

46

© The Economist Intelligence Unit Limited 2011 15

Multinational companies and China: What future?

8 A better life? The wants and worries of China’s consumers, Economist Intelligence Unit, 2010.

Healthcare reform, a key Chinese government initiative, will be vital in unleashing the full potential of the country’s consumption power. With no social safety net, many Chinese households continue to save an inordinate amount of their incomes against medical emergency, or to fund their retirement. Evenrelativelywell-offcitydwellersreportthattheysavemorethan30%oftheirannualhouseholdincome, in part to cover medical emergencies.8 There is an urgent need to overhaul China’s patchy healthcare system to prepare for the coming upsurge in the elderly population, and also to bring a much-neededboosttothequalityoflifeofmanyofitscitizens.Patientsinmanyruralareascurrentlyhave only limited access to clinics, drugs and health insurance. And city dwellers often must cope with overcrowded hospitals and overstretched doctors. Rural and urban residents alike must pay a big portion of medical bills themselves.

The Chinese government is now trying to restore the public healthcare system, after allowing it to decay for most of the modern era of economic reform. With the goal of providing “safe, effective, convenient andaffordable”healthcaretoallcitizensby2020,in2008thegovernmentintroducednationalhealthinsurance.(Thiswasfiveyearsafteritlaunchedaseparateruralcooperativemedicalinsuranceschemethat partially covers healthcare costs.) As Chinese people stop losing sleep over their ability to pay medical bills, they are likely to save less and spend more in their daily life, boosting consumption.

To be sure, this may still be a distant prospect. Many parts of the healthcare reform plan, such as the role of the private sector and drug pricing, have yet to be decided or put into place. Moreover, current healthcare insurance rarely covers the cost of the level of care demanded by middle-class consumers. It is estimated that about 200m people still have no health insurance at all.

Nonetheless, the healthcare market is already huge and can only get bigger. Health insurance and the provision of more healthcare facilities across the country will bring more consumers into the system. There are an estimated 13,000 hospitals in China, many of which are likely to need new equipment. Beijing has also announced plans to encourage more foreign investment in this sector, though guidelines have yet to be issued (there are already about 100 foreign-invested clinics and hospitals in China). China is a top-ten market for pharmaceuticals in the world, with US$42bn-worth of drugs sold in 2010 according to IMS, a healthcare consultancy. Though much of the spending was on cheap, domestically made generic drugs, the marketgrewatanannualaverageofaround6%during2006-10.Thispaceisexpectedtocontinuethrough2015, as incomes rise, the government spends more and the ranks of the elderly swell. By then, some forecasters project China to be the world’s second-largest pharmaceutical market, after the US.

Another area with seemingly huge implications for consumption is China’s determination to clean up its environment. In a country where studies estimate air pollution kills up to 1.3m people a year9, a potentialbonanzaawaits,forexample,globalcarmakersthatdevelopgreenervehiclesforthemasses.Havingpledgedtoreducethecountry’scarbonintensity(carbonemittedperunitofGDP)by40-45%by2020comparedwiththe2005level,thegovernmentplanstoinvestmorethanRmb100bn(US$15.7bn)inthegreen-vehiclesectorinthecomingdecadetocurbtheexplosiveupsurgeinvehicleemissions.Itsgoal is to turn China into the world’s largest producer of clean-energy cars, with emphasis on electric vehicles (EVs), a category that includes hybrid-electric and battery-powered vehicles.

HowdoMNCsplantocapitaliseonthisconsumptionstory,andwhatobstaclesdotheyface?Perhapsmoreimportantly,howdoesChinaviewtheirsuccess?

9 “The China Greentech Report 2011”, The China Greentech Initiative, 2011.

© The Economist Intelligence Unit Limited 201116

Multinational companies and China: What future?

Chapter 3: The perils of successNow that the mythical China consumer has materialised, companies could struggle to keep pace with rising demand. They also worry that too much success will attract unwanted attention.

M any multinationals are now turbo-charging their China plans to keep pace with demand. The words“doublinginsize”arecommonlyheard,whetherreferringtotheoverallsizeofamarket,

ortoanindividualcompany’srevenueexpectations.Forexample,AkzoNobel,achemicalcompany,planstodoubleitsrevenuetoUS$3bninthenextfiveyears.Ithasploughed€275m(US$383m)intoacomplexinNingbotomakenumerousproductsthatwillbesoldtothebuildingandconstruction,cleaning and detergents, food preservation, oil, personal care and pulp industries. The company also recently bought a local automotive paint maker.

Some companies are even more ambitious. Coach, a premium US accessory maker that saw its sales in China double in 2010 to US$100m, says it aims to raise its revenue in the country to US$500m by 2014andsecurea10%marketshareinitssector.Unileverisaimingtoboostsalesfive-foldtoUS$10bnby2020.Volkswagenwillopentwonewplantsby2013(bothtobefinancedbyrevenuesfromitsChinaventures)andFordwillopenthreeby2014.Coca-ColaisjustfinishingupaUS$3bninvestmentprogrammeandisplanningtospendUS$4bnmoreoverthenextthreeyears.Thelistgoeson.

Is it enough?Ironically,amidallthefantasticexpansionplans,oneofthebiggestquestionsfacingmultinationalsis,isitenough?Whilecompaniesareputtingincreasingamountsintomarket-sizingresearchandsqueezingasmuch investment out of headquarters as they can, in interviews for this report some admit that they really arenotveryconfidentintheresults—ifanything,theyworrytheyarebeingtoocautious.

Nissan,whichhasjustunveiledamajorexpansionplan(seeNissan:Accordingtoplan,p42),has

© The Economist Intelligence Unit Limited 2011 17

Multinational companies and China: What future?

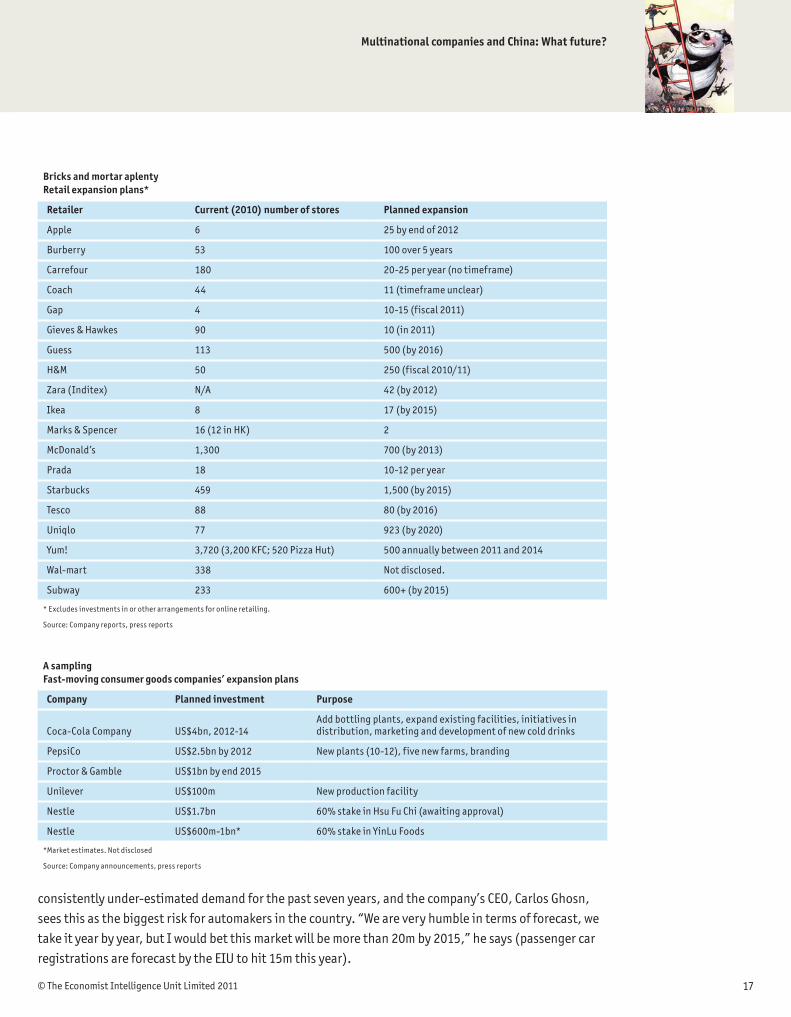

Bricks and mortar aplentyRetail expansion plans*

Retailer Current (2010) number of stores Planned expansion

Apple 6 25 by end of 2012

Burberry 53 100 over 5 years

Carrefour 180 20-25 per year (no timeframe)

Coach 44 11 (timeframe unclear)

Gap 4 10-15 (fiscal 2011)

Gieves&Hawkes 90 10 (in 2011)

Guess 113 500 (by 2016)

H&M 50 250 (fiscal 2010/11)

Zara(Inditex) N/A 42 (by 2012)

Ikea 8 17(by2015)

Marks&Spencer 16 (12 in HK) 2

McDonald’s 1,300 700(by2013)

Prada 18 10-12 per year

Starbucks 459 1,500 (by 2015)

Tesco 88 80 (by 2016)

Uniqlo 77 923(by2020)

Yum! 3,720(3,200KFC;520PizzaHut) 500 annually between 2011 and 2014

Wal-mart 338 Not disclosed.

Subway 233 600+(by2015)

*Excludesinvestmentsinorotherarrangementsforonlineretailing.

Source:Companyreports,pressreports

A samplingFast-moving consumer goods companies’ expansion plans

Company Planned investment Purpose

Coca-Cola Company US$4bn, 2012-14Addbottlingplants,expandexistingfacilities,initiativesindistribution, marketing and development of new cold drinks

PepsiCo US$2.5bn by 2012 New plants (10-12), five new farms, branding

Proctor&Gamble US$1bn by end 2015

Unilever US$100m New production facility

Nestle US$1.7bn 60%stakeinHsuFuChi(awaitingapproval)

Nestle US$600m-1bn* 60%stakeinYinLuFoods

*Market estimates. Not disclosed

Source:Companyannouncements,pressreports

consistently under-estimated demand for the past seven years, and the company’s CEO, Carlos Ghosn, sees this as the biggest risk for automakers in the country. “We are very humble in terms of forecast, we take it year by year, but I would bet this market will be more than 20m by 2015,” he says (passenger car registrations are forecast by the EIU to hit 15m this year).

© The Economist Intelligence Unit Limited 201118

Multinational companies and China: What future?

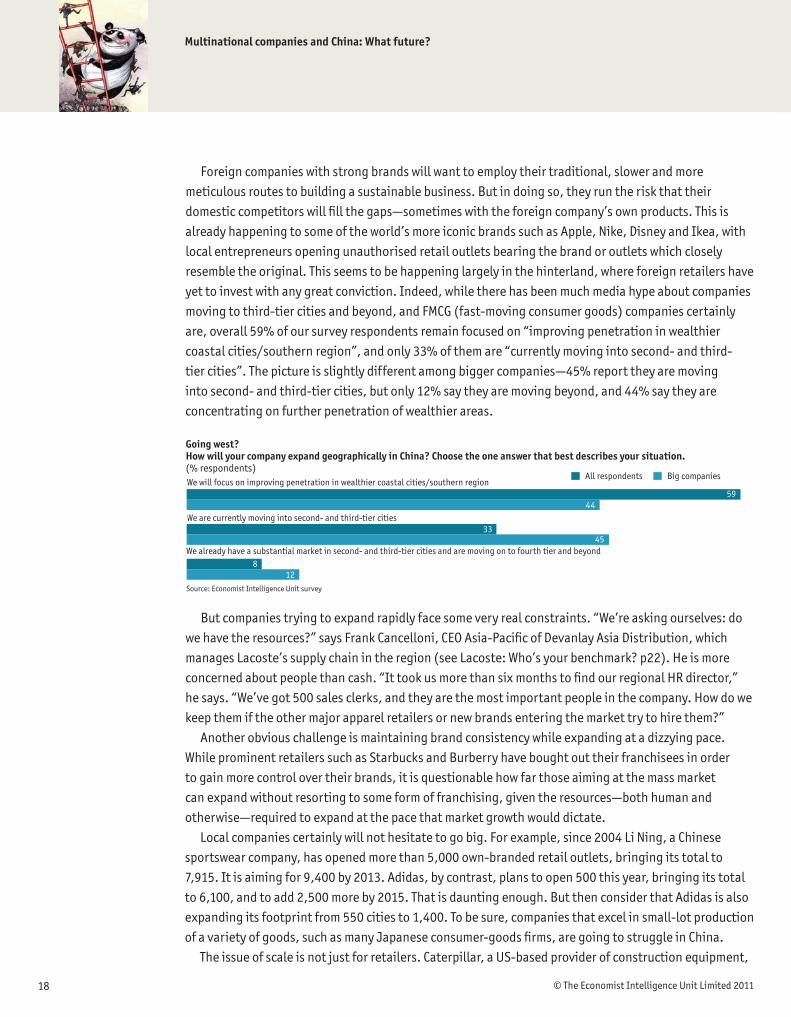

Foreign companies with strong brands will want to employ their traditional, slower and more meticulous routes to building a sustainable business. But in doing so, they run the risk that their domesticcompetitorswillfillthegaps—sometimeswiththeforeigncompany’sownproducts.Thisisalready happening to some of the world’s more iconic brands such as Apple, Nike, Disney and Ikea, with local entrepreneurs opening unauthorised retail outlets bearing the brand or outlets which closely resemble the original. This seems to be happening largely in the hinterland, where foreign retailers have yet to invest with any great conviction. Indeed, while there has been much media hype about companies moving to third-tier cities and beyond, and FMCG (fast-moving consumer goods) companies certainly are,overall59%ofoursurveyrespondentsremainfocusedon“improvingpenetrationinwealthiercoastalcities/southernregion”,andonly33%ofthemare“currentlymovingintosecond-andthird-tiercities”.Thepictureisslightlydifferentamongbiggercompanies—45%reporttheyaremovingintosecond-andthird-tiercities,butonly12%saytheyaremovingbeyond,and44%saytheyareconcentrating on further penetration of wealthier areas.

Going west?How will your company expand geographically in China? Choose the one answer that best describes your situation.(% respondents)We will focus on improving penetration in wealthier coastal cities/southern region

We are currently moving into second- and third-tier cities

We already have a substantial market in second- and third-tier cities and are moving on to fourth tier and beyond

Source: Economist Intelligence Unit survey

5944

812

3345

Big companiesAll respondents

Butcompaniestryingtoexpandrapidlyfacesomeveryrealconstraints.“We’reaskingourselves:dowehavetheresources?”saysFrankCancelloni,CEOAsia-PacificofDevanlayAsiaDistribution,whichmanagesLacoste’ssupplychainintheregion(seeLacoste:Who’syourbenchmark?p22).Heismoreconcernedaboutpeoplethancash.“IttookusmorethansixmonthstofindourregionalHRdirector,”he says. “We’ve got 500 sales clerks, and they are the most important people in the company. How do we keepthemiftheothermajorapparelretailersornewbrandsenteringthemarkettrytohirethem?”

Anotherobviouschallengeismaintainingbrandconsistencywhileexpandingatadizzyingpace.While prominent retailers such as Starbucks and Burberry have bought out their franchisees in order to gain more control over their brands, it is questionable how far those aiming at the mass market canexpandwithoutresortingtosomeformoffranchising,giventheresources—bothhumanandotherwise—requiredtoexpandatthepacethatmarketgrowthwoulddictate.

Localcompaniescertainlywillnothesitatetogobig.Forexample,since2004LiNing,aChinesesportswear company, has opened more than 5,000 own-branded retail outlets, bringing its total to 7,915.Itisaimingfor9,400by2013.Adidas,bycontrast,planstoopen500thisyear,bringingitstotalto 6,100, and to add 2,500 more by 2015. That is daunting enough. But then consider that Adidas is also expandingitsfootprintfrom550citiesto1,400.Tobesure,companiesthatexcelinsmall-lotproductionofavarietyofgoods,suchasmanyJapaneseconsumer-goodsfirms,aregoingtostruggleinChina.

The issue of scale is not just for retailers. Caterpillar, a US-based provider of construction equipment,

© The Economist Intelligence Unit Limited 2011 19

Multinational companies and China: What future?

has been making headlines recently over the new priority it places on China—even factoring in the considerable (and early) investments it has already made in the country. According to analysis from Off-HighwayResearch,aconsultancy,Caterpillar’smarketshareinChinahasfallenfrom11%in2005to7%in2010,despitethefactthatitssaleshavequadrupledinthattime.Themarketshareisnotgoingtoarch-rival Komatsu of Japan, but to local players.

One strategy, or two?Those on the front-lines of the consumption story are also grappling with how to keep up with consumer needs that at one end of the spectrum are becoming very sophisticated, while at the other remain very basic. As an analyst once quipped, “In China you have both Africa and the EU.” Today, people living in coastal provinces of the eastern and southern seaboards, as well as in some large cities in the interior, are much richer and more discerning than the national average. Rollouts of nationwide distribution networks remain works in progress. But what is more, regional disparities in tastes, preferences and shopping habits, apart from incomes, are simply too great. “If you compare Guangdong in the south and Shandong in the east, less than half of the leading brands are common between the two provinces,” says Karthik Rao, managing director for Greater China at Nielsen.

While most foreign companies have in the past chosen to play in the higher end of the market, leaving the lower-end to local players, there are signs that they are now reassessing that strategy, with some aiming to play in the middle, if not the low-end, of the pyramid.

“As incomes rise, people become hungry for choice,” notes Mr Rao. “Tastes are constantly changing and companies have to stay on top of that. They even have to segment their product line to cater for different tastes as they evolve. That’s what a lot of companies have now realised.”

Thisappliestoeverythingfromdenimjeanstocars.LeviStrauss,forexample,hasdevelopedanewrange of jeans called dENiZEN, which retail for about US$40-60 compared with the US$100 for a regular pairofLevi’s.GMisdevelopingamarquespecificallyforChinatotargettheaspiringcar-ownerwhocannot afford a Chevrolet but wants a lot of the features the brand would offer. The company estimates thatthereare4msuchconsumers.WhyleavethatmarkettolocalmakerslikeCheryorBYD?

The issue will also confront the pharmaceutical industry. China’s growing middle class is willing to pay out of its own pocket for branded Western drugs that they are sure will not harm them. This seems unlikely to change any time soon, given numerous scandals over product quality in China. But at the same time foreign companies will need to align themselves with the Chinese government’s goal of improving access to healthcare for all, including the lowest-income groups. While the government’s ultimate policy on drug pricing remains to be set, it seems a fair bet that price caps will drive the market towards generics.

In the view of George Baeder, who leads the Asia life science practice of Monitor Group, a consultancy, “The government must meet the needs of 1.3bn people. It can’t just follow the broken models in the West,wheredrugsaretooexpensive.Theyneedtodrivecostsdowntothelowestlevel.MostMNCsarenot particularly strong at playing here.”

Most big pharma companies face declining prospects as their major drugs come off patent. Unlike othertypesofconsumergoods,pharmacompaniescannottailorproductstothelowendofthemarket:

© The Economist Intelligence Unit Limited 201120

Multinational companies and China: What future?

they may need to offer the same products at lower cost to poorer segments of society. Can or should they dothis?Thereisnoclearanswerandonlyoneprecedent,whichdoesnotreallyapply:themovesbyfivebigcompaniestoofferAIDSdrugsatlowcostinAfrica.WhilethishadnoramificationsforglobalpricingofAIDSdrugs,thesamecannotbeexpectedfordrugsthathaveawiderapplicationandareproducedinChina, which has problems with cross-border leakages of both real and counterfeit goods.

Is it too much?WhatdoestheChinesegovernmentmakeofthismadscramble?Mostsmallerandlower-profilefirmsfeelthey are too unimportant in China’s overall priorities to warrant much attention. They are probably right. But the larger players are mindful of their steps.

“Ioftenjokewithgovernmentofficials—howmanystoresaretoomany?”saysaseniorexecutiveatoneforeignretailer.“Imean,isUS$50bninsalestoomuch?Therecouldbeatippingpointwhentheysay‘toomuch’.Butthemarketisgrowingsofastthatitisnotinconceivablethatourmarketsharecouldeven decline while our business continues to grow enormously.”

This nagging worry about somehow being punished for treading on the local competition could explaintheseeminglylowexpectationsofoursurveyrespondentsintermsofusingacquisitionsasaroutetogrowthinChina:only20%choseacquisitionsasthemostimportantstrategyforgrowthinChina,while63%choseorganicgrowthand46%saidjointventures.

TherehasbeenanairofuncertaintyhangingoverChina’sM&AmarketsinceregulatorsrejectedCoca-

Cola’splannedpurchaseofChinaHuiyuanJuiceforUS$2.3bnin2009overcompetitionconcernsthatwere viewed as questionable. The deal would have boosted Coca-Cola’s share of the fruit and vegetable juicemarkettoaround20%.TheAmericangianthassincegivenuponbuyinganythinginChina.MuhtarKent,chairmanandCEOofCoca-Cola,toldreportersinAugust,“It’s[acquisitions]nolongeronourradar screen because we’re seeing so much potential for organic growth.10“

The Ministry of Commerce has since shown a keenness to improve the transparency of its decisions

10 “Coca-Cola Plans $4bn China Investment”, wsj.com, August19th2011

Putting on weightWhich of the following growth strategies will be most important to your company’s expansion plans in China? Choose up to two.(% respondents)Organic growth

Joint ventures

Acquisitions of Chinese companies

Acquisitions of foreign competitors’ operations

We are not planning to expand

Don’t know

Source: Economist Intelligence Unit survey

6380

2023

67

93

11

4643

Big companiesAll respondents

© The Economist Intelligence Unit Limited 2011 21

Multinational companies and China: What future?

and to be a more sophisticated regulator. But the fact remains that China’s law does allow it to consider non-competition issues, such as security of supply and its own industrial policies, in making its rulings.

Chinahasrecentlyshownsignsthatitwillallowpurchasesinrelativelyhigh-profilelocalcompanies—albeitwithconditions.Forexample,Diageo,aUKdrinksgiant,receivedapprovalthisyeartotakeacontrollingstakeinitsexistingChinesejointventure,SichuanChengduQuangxingGroup,therebygainingindirectcontrolofShuijingfang,ownerofthefamousQuanxingbrandofthelocalspiritbaijiuthataccountsformorethan30%ofChina’salcoholicdrinksmarket.Approvaloftheacquisitionreportedlytook16monthsand,asacondition,ShuijingfanghadtodivesttheQuanxingbrand.Nestléthisyearannounceddealstotake60%stakesintwolocalcompanies,YinLuFoods,amakerofpeanutmilk, and Hsu Fu Chi International, a confectioner. The former has been approved, but the latter is still awaiting the green light.

It is notable that all of these deals have involved keeping a substantial stake with local shareholders. Indeed, the byword remains caution. “MNCs need to choose targets carefully and manage growth,” says Ninette Dodoo, a lawyer with Clifford Chance in Beijing. “By that we mean, do not overshadow the Chinese business target.”

© The Economist Intelligence Unit Limited 201122

Multinational companies and China: What future?

Lacoste: Who’s your benchmark?

Devanlay, which is responsible for the production and distribution of Lacoste brand apparel globally, is illustrative of what is no doubt happening in many companies around the world. Until around 2008 the company paid no special attention to China. Revenues from the countryweregrowingat10-15%ayearanditwasopening20-30newpoints of sale (boutique, a corner within a department store, or a franchise operation) annually. This was fabulous when benchmarked against France or the US. But the company never benchmarked againstotherbrandsinChina.Haditdoneso,itwouldhaverealizedthateven20%growthwasnothingtogetexcitedabout.

Enter a new CEO, Jose Luis Duran, formerly the global head of French hypermarket chain Carrefour. Mr Duran knew China. Suddenly the possibilities became clear. Mr Duran understood the need for higher investment in a market featuring intense competition in the so-called“accessibleluxury”spaceaswellastheneedtomarchforward into second and third-tier cities where no one had ever seen the iconic Lacoste crocodile logo (or at least the real thing).

Since Mr Duran took over Devanlay has beefed up its management in China, including sending a new CFO from Europe. It has been increasing investments in new store openings and renovations and essential infrastructure such as information systems.

DevanlaydoesnotrevealinvestmentfiguresbutFrankCancelloni,thecompany’sAsia-PacificCEO,saysthatcapitalexpenditureforthe region (Japan, China and South Korea) will double in 2011, with China accounting for more than half the total. “We are now growing atabout30%ayear,andIthinkcompoundannualgrowthof30-35%isachievable,”hesays.TodayChinaaccountsforlessthan5%ofLacoste’stotalapparelsalesworldwide,afigurewhichMrCancellonisayscouldriseto10%inthefutureoncurrentgrowthprojections.

Keeping upDevanlay’s current challenge is deciding what it can reasonably do in termsofthepaceofexpansion.“Twoyearsagoweopened20doors[pointsofsale]ayearandnowwe’retalkingabout100-150,”saysMrCancelloni.“Butnowwe’reasking,‘dowehavetheresources?’”Heismost concerned about staff retention and has hired an HR consultancy to survey retail staff on what motivates them to stay with a company. ThecompanyalsospentsixmonthsfindingtherightHRdirector.

While others in the apparel retail industry are moving towards directly owned stores, Devanlay is likely to continue to use dealers in second and third-tier cities as a means to achieve scale. It currently operates 100 points of sale directly in Shanghai, Beijing, ShenzhenandGuangzhou,amixtureofboutiquesandcornerswithindepartment stores, and 250 franchised points of sale. “Franchising ismoreprofitable,thereisnodoubtaboutit,”saysMrCancelloni.“Ifyouopeninacertaincitythenyouhavetosetupanofficeandhiremanagers, etcetera. Again, it’s people. So I think we would rather make sure the people at headquarters are very good at training and working with franchisees.”

Crocodile-infested watersLacoste, like many companies operating in China, has its share of problems with counterfeiting. Lacoste’s problems in Asia actually go backtothe1950swhentwobrotherssetupcompaniesinHongKongand Singapore making polo shirts and using a crocodile logo. Lacoste assumesthattheywereexposedtothebrandaftertheyfledChinafollowing the communist revolution and went to Vietnam, which was stillaFrenchcolonyandwhereFrenchexpatriateswouldbewearingLacoste shirts.

Over the years there have been numerous legal disputes with the companies spawned by the brothers, including in China. The battle with Singapore-based Crocodile International, known as Cartelo in China, continues. There are also numerous small groups who make exactcopiesofLacosteproducts,orproductsclearlyinspiredbyLacoste.

Counterfeiting has not prevented Lacoste from growing rapidly in China. According to Jerome Bachasson, regional director for Asia-PacificatLacoste,whooverseestrademarkprotection,brandingandsponsorship,itisunrealistictoexpectthecounterfeitingindustrytogo away soon given that so many livelihoods in China still depend on it. While it is important to take legal action against the factories or wholesalers involved in counterfeiting, the only real solution is to stay one step ahead of them.

“Wewillfightcounterfeitingbyhavingfantasticstores,creatingthat gap between us and the locals,” he says. “Consumers want to know how to tell the difference between originals and fakes. In fact I’d say consumers are going faster than the Chinese authorities in dismissing fakes.”

© The Economist Intelligence Unit Limited 2011 23

Multinational companies and China: What future?

Chapter 4: Whose hubris? It is often taken for granted that multinationals possess superior technology, better brand management and a stronger appeal for talented workers. There are signs that all of these advantages are beginning to erode in China.

A chieving‘Chinaspeed’,asithascometobeknown,isbutonefactorinstayingaheadofthecompetition.“Itisaglobalplayingfieldalmostunlikeanyother,”notesTorstenStocker,a

consultantwithMonitorGroup.Hepointstotheexampleofplasticcontainers,whichinmanycountries around the world are synonymous with Tupperware or Rubbermaid. In China, the market leaderisLock&Lock,aSouthKoreancompanythatisalmostunknownoutsideAsia.

Competition in China comes in many forms. There are foreign companies that have been in the market for years and are now upping their game, as well as new entrants and companies returning to China for a second time. Then there are the locals, who by all accounts are rapidly improving in many segments.

Our survey suggests that competition from local companies is perhaps being underestimated by MNC headquarters.RespondentsbasedinChinarankcompetitionfromlocalfirmsatthetopoftheirlistof obstacles, while the sample as a whole ranked it second, behind IPR (intellectual-property rights) protection. Studies suggest that foreign companies ignore the threat of local competition at their peril.Aformerexecutiveatonemultinationaldisparaginglynotesthatmanagementathisformeremployer would track the market share of the usual global competitors on a weekly basis, ignoring the localcompetition,untilonedaythe“other”categoryexceeded50%.Whoisthis‘other’?theysuddenlywanted to know. By then it was too late.

NimblelocalcompetitorsarechallengingthelikesofP&GandUnilever.Inarecentreport,Booz&Co,aconsultancy,highlightedtheriseoffoursuchcompanies:Wanglaoji(herbaltea);FoshanJingxingHealth(sanitarynapkins);BawangInternational(shampoo)andHangzhouHancaoBiotechnology (non-tobacco cigarettes)11. The authors wrote that for foreign multinationals, “the warningsignsshouldbeapparent”.Theywentontoconclude:“Chinaisgeneratingahostofpowerful

11 “China’s Local Champions”, Booz&Co,2011

© The Economist Intelligence Unit Limited 201124

Multinational companies and China: What future?

Getting in the wayWhat do you see as the biggest operational obstacles standing in the way of seizing opportunities in China? Choose up to three.(% respondents)Lack of intellectual property (IP) protection

Competition from domestic companies

Discrimination against foreign companies

Competition from other foreign companies

Lack of legal protection in general

Lack of available local talent

Risk of trade and economic disputes between China and other countries

Lack of autonomy to make the right decisions for the China market

Source: Economist Intelligence Unit survey

Respondents based in China

Unpredictable nature of Chinese government

4135

3221

31

Corruption28

29

27

27

23

14

13

15

33

11

813

13

3548

Cleaning upMarket share by retail value for selected consumer goods (%)

0

10

20

30

40

50

OthersWhiteCat

BlueMoon

NafineUnileverP&GLibyNice

Source: Euromonitor 2009 report; Booz & Company

DomesticMNCOther

40

225

91014

18

OthersAmwayReckittBenckiser

KaimiWhiteCat

LohmannHaas

BlueMoon

SCJohnson

47

466671212

Laundry Surface Care

0

10

20

30

40

50

OthersReckittBenckiser

LonkeyNafineAmwayWhiteCat

NiceLiby

24

44510

171719

OthersKaimiReckittBenckiser

Saa LeeLonkeyWhiteCat

BlueMoon

SCJohnson

31

666910

1418

Dishwashing Toilet Care

© The Economist Intelligence Unit Limited 2011 25

Multinational companies and China: What future?

local champions—and competing against them is the new reality. Close to their customers, focused on developing lower-cost alternatives, marketing and distribution strategies, these businesses are developing new goods and innovative ways of selling them that are well attuned to the needs of Chinese consumers.”

Therisingcompetitivestrengthoflocalcompaniesisalsoreflectedinthetalentmarket.Althoughoursurvey respondents as a whole ranked “lack of available local talent” pretty far down the list of obstacles standing in the way of market success, a mounting array of evidence suggests they should be concerned. Those on the ground already are—respondents from China ranked the lack of talent third on their list of obstacles (respondents as a whole ranked it eighth).

WithmanyChinesecompaniesflourishingandexpandingatafasterpacethanMNCs,thesamepoolofbilingual and bicultural local talent who can straddle the Chinese and international business worlds are beingchasedbyboth.Forexample,in2010DeutscheBanklostitsChinaheadtoIndustrialandCommercialBankofChina.AfewyearsearlierB&QandMicrosoftsawhigh-profileexecutivesjumptoChinesecompetitors (to Alibaba and Shanda Interactive Entertainment respectively). Ante and Li Ning, the two leading sportswear makers, also have managed to attract talent away from Nike, Adidas and Puma.

HRandexecutive-searchfirmssaythisreverseflowoflocaltalentfromMNCstoChinesecompanieswill increase in the future. According to Manpower Inc, a comparison of its surveys done in 2006 and 2010showsthatjobseekerswhopreferredtoworkforaprivateChinesecompanyjumpedbyfivepercentagepointsduringtheperiod,whilethefigureforthosewhopreferredaforeigncompanydropped by ten percentage points.

The rising attraction of local companies is manifold. Thanks to rapid growth, more of them can match orexceedsalariesatMNCs.Manycompaniesareexpandingoverseas,providingattractivepostings.AndemployeescanexpectquickerpromotionatmanysuccessfulChinesecompanies,whicharelessrigidandformal,allowingmanagerialemployeesmoreflexibilitytodefinetheirresponsibilitiesandworkingconditions.

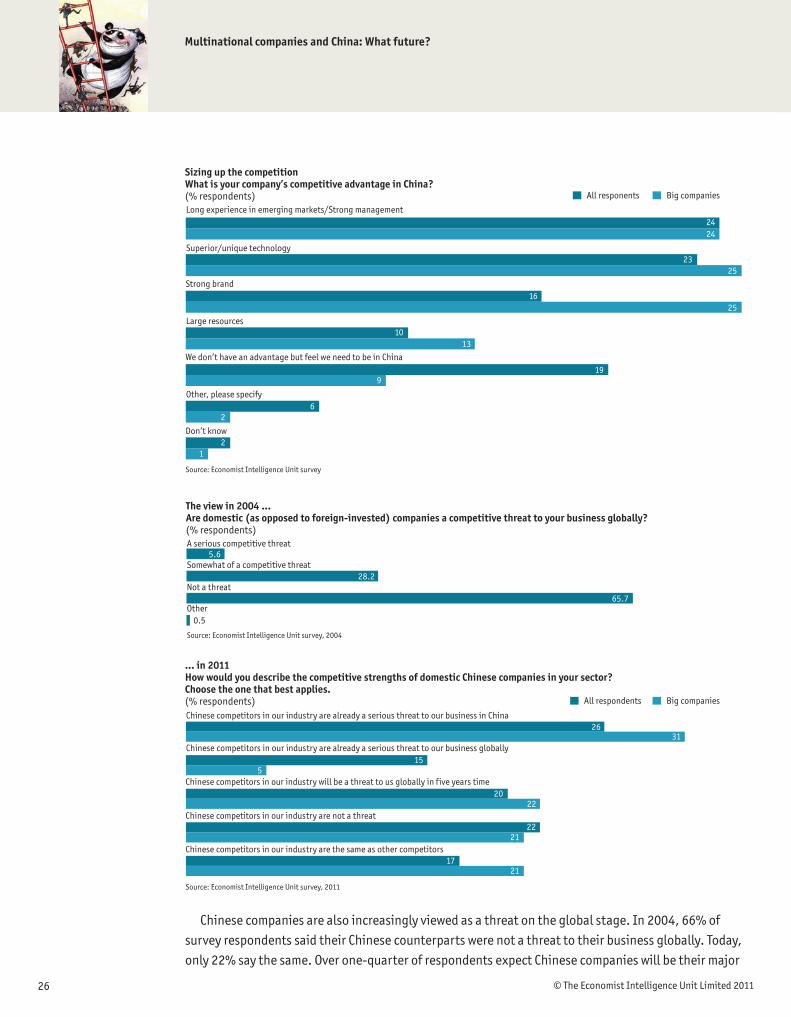

Suddenly uncertainEven though headquarters may be underestimating the power of local brands and Chinese companies’ growing attractiveness to the country’s shallow pool of talent, multinationals do not seem overly confident.Askedtoidentifytheircompany’scompetitiveadvantageinChina,justunder20%ofsurveyrespondents reported that they don’t have an advantage but feel they need to be in the market. Among large companies, only one-quarter felt they have superior technology or a stronger brand, with these figuresevenlowerforthesampleasawhole.

Indeed, the competitive prowess of Chinese companies has surged since our last report in 2004. Then,68%ofsurveyrespondentssawforeign-investedcompaniesasthebiggestcompetitivethreattotheirbusinessinChina,while44%sawathreatfromprivateChinesecompaniesand27%fromstate-ownedenterprises.In2011foreignersdonotseemtoworrymuchabouteachother—only27%pointedtocompetitionfromotherforeignersasathreat,rankingsixthonthelistofobstaclesinthewayofopportunity. Competition from domestic companies, by contrast, ranks second behind IP protection as thebiggestthreat,anditranksfirstamongrespondentsbasedinChina.

© The Economist Intelligence Unit Limited 201126

Multinational companies and China: What future?

Sizing up the competitionWhat is your company’s competitive advantage in China?(% respondents)Long experience in emerging markets/Strong management

Superior/unique technology

Large resources

Other, please specify

Strong brand

2424

1625

25

1013

9

We don’t have an advantage but feel we need to be in China19

6

Don’t know2

2

1

23

Source: Economist Intelligence Unit survey

Big companiesAll responents

Chinesecompaniesarealsoincreasinglyviewedasathreatontheglobalstage.In2004,66%ofsurvey respondents said their Chinese counterparts were not a threat to their business globally. Today, only22%saythesame.Overone-quarterofrespondentsexpectChinesecompanieswillbetheirmajor

... in 2011How would you describe the competitive strengths of domestic Chinese companies in your sector? Choose the one that best applies.(% respondents)Chinese competitors in our industry are already a serious threat to our business in China

Chinese competitors in our industry are already a serious threat to our business globally

Chinese competitors in our industry will be a threat to us globally in five years time

Chinese competitors in our industry are not a threat

Chinese competitors in our industry are the same as other competitors

Source: Economist Intelligence Unit survey, 2011

2631

2022

22

1721

21

155

Big companiesAll respondents

The view in 2004 ...Are domestic (as opposed to foreign-invested) companies a competitive threat to your business globally? (% respondents)A serious competitive threat

Somewhat of a competitive threat

Not a threat

Other

Source: Economist Intelligence Unit survey, 2004

5.6

28.2

65.7

0.5

© The Economist Intelligence Unit Limited 2011 27

Multinational companies and China: What future?

globalcompetitorsinfiveyears’time(9%saytheyalreadyare),while47%saytheywillbeseriouscompetitorswithintenyears.Bigcompaniesaresomewhatmoreconfident—only16%expecttheirChinesecounterpartstochallengethemgloballywithinfiveyears(only5%dosonow),withthefigurerisingto38%withintenyears.ButlargercompaniesaremoreconcernedabouttheimpacteventsinChinawillhaveontheirindustry—38%saidthatdevelopmentswillhaveadisruptiveimpactontheirindustrywithinfiveyears,andmorethanhalfexpectthistohappenwithintenyears.Thisthreatismostlikely to come from lower-cost competition on the global stage.

Still,executivesthinkthatChina’seffortstoboostconsumption,andtheuncertainregulatoryenvironment(discussedinthenextchapter),willhaveabiggerimpactthanlocalcompetitionontheirChinastrategyinthenextfiveyears.

© The Economist Intelligence Unit Limited 201128

Multinational companies and China: What future?

Chapter 5: The invisible hand China’s use of protectionism as a means of encouraging innovation is causing a great deal of ill will among technology-rich multinationals. The role of vested interests is as much, if not more, of a problem than policy. Rather than counting on an official solution, companies are probably better off seeking a way to work around the risks.

Amid all the chatter about China in boardrooms around the world, there are a couple of basic questionsthatexecutivesshouldbeasking:doesChinareallywantMNCs?Andifso,whatexactly

doesitwantfromthem?AtthemomentChina’spoliciestowardsforeigncompaniesinsomesectorsare generating an awful lot of ill will.

Thegovernment’sbroadeconomicagendaisnosecret,althoughitisrathermoredifficulttokeeptrackofallthevariousprioritylists(seep29).Its12thFive-YearPlan(FYP)aimstopursue“scientificdevelopment” as a top priority by fostering “strategic emerging industries” with a view to upgrading the Chinese economy from low-cost manufacturing to higher-value-added industries and services.

Foreign companies worry that China’s emphasis on having local companies lead the charge up the valuechainwillcomeattheirexpense.Overthenextfewyearsthestrategicsectorswillbeshoweredwithvariousformsofofficialassistance,frompriorityfundingtotaxbreaks,inordertoensurethattheymeetthegovernmenttargetofgenerating8%ofGDPby2015.Inthepast,similarpreferentialpolicieswere deployed to nurture a group of domestic corporate powerhouses in such sectors as railways and telecoms. China is determined to create more such “national champions” in other industries—especially in newly emerging sectors where no country has much of a head start and where there is a real chance to take the lead. In the previous FYP, the government targeted solar and wind energy, and in both sectors Chinese companies now lead the markets globally. This lead has been based more on low costs than technological prowess. Some observers point out that it is Chinese companies’ ability to drive down pricesthathasfuelledmarketgrowthintheseindustriesinthefirstinstance.

© The Economist Intelligence Unit Limited 2011 29

Multinational companies and China: What future?

Aiming high

Sectors in which China hopes to take leadership From the Medium and Long-term Plan for Science and Technology Development (MLP):11 key sectors for employing technology development and innovation to solve China’s problems (with a sampling of the 68 priority areas withclearlydefinedmissions)• Energy,waterandmineralresources(coalliquefactionand

gasification,renewableenergy,explorationandextractiontechnology, power grids, etc)

• Environment(environmentally-friendlyfertilizers,herbicidesandpesticides, waste recycling)

• Agriculture(amoderndairyindustry,geneticallymodifiedcrops)• Manufacturing(robotics)• Transportation(high-speedrailandelectriccars)• Informationandservices• Populationandhealth(drugsandreproductivehealthproducts)• Urbanization(energy-efficientbuidings)• Publicsecurityandnationaldefence

8fieldsoftechnologyinwhich27breakthroughtechnologiesaretobepursued• Biotech(stemcell-basedtissueengineering)• IT(next-generationinternetandsupercomputers)• Advancedmaterials• Advancedmanufacturing• Advancedenergytechnology(fastneutronnucleartechnology)• Marinetechnology(deepseaexploration)• Lasertechnology• Aerospacetechnology

4 basic research programmes• Proteinscience• Nanotechnology

• Quantumphysics• Developmentalandreproductivescience

From the 11th Five-Year Plan for High-Technology Industries (2006-2010)16 Special Projects aimed at import substitution• Coreelectroniccomponents,high-endgeneralusechipsand

basic software products• Large-scaleintegratedcircuitmanufacturingequipmentand

techniques• Newgenerationbroadbandwirelessmobilecommunication

networks• Advancednumeric-controlledmachineryandbasic

manufacturing technology• Large-scaleoilandgasexploration• Largeadvancednuclearreactors• Waterpollutioncontrolandtreatment• Breedingnewvarietiesofgeneticallymodifiedorganisms• Pharmaceuticalinnovationanddevelopment• ControlandtreatmentofAIDS,hepatitisandothermajor

diseases• Largeaircraft• High-definitionearthobservationsystem• Mannedspaceflightandlunarprobe• Threeothersthatremainclassified

From the 12th Five-Year PlanStrategicemergingindustries(whicharetoaccountfor8%ofGDPby2015,upfrom3%today)• Energysavingandenvironmentalprotection• Newgenerationofinformationtechnology• Biotechnology• High-endequipmentmanufacturing• Newenergy• Newmaterial• Newenergyvehicles

Perceived favouritism towards domestic companies is a major sore point with MNCs, which accuse theChinesegovernmentofcreepingprotectionism.Topexecutivesfromthreeoftheworld’sleadingcompanies have been captured on record in the past two years openly questioning China’s intentions12. In its 2011 “American Business in China” white paper, the American Chamber of Commerce in China for thefirsttimehasdedicatedasectiononindustrialpolicyandmarketaccessfocusingonregulatorybarriers. The paper describes a pattern of discrimination created by a host of labyrinthine regulations—including on licensing, government procurement and competition law—as impeding fair competition

12 The heads of Siemens and BASF in 2010 told the Chinese premier, Wen Jiabao, directly in public that they were unhappy with the change in the business climate for foreign companies operating in China, pointing particularly to the issues of forced technology transfer and unfair public-procurement systems.

© The Economist Intelligence Unit Limited 201130

Multinational companies and China: What future?

between American and Chinese companies13. The European Union Chamber of Commerce in China strikes the same note in its 2010/2011 Position Paper14. “More than anything else, European companies wish to have equal access to China’s markets,” it said. “Despite China’s 30 years of reform, it still remains excessivelyregulatedandlessopentocompetitioncomparedtoothermajoreconomies.”Eventhenormally more discreet Japanese chamber began issuing an annual white paper in 2010, citing many of the same complaints15.

The real issueChinahardlyinventedindustrialnationalism,andthiswouldnotbethefirsttimemultinationalshave encountered it. But China’s attempt to link access to its markets with requirements that foreign investors share more of their intellectual property—including developing and registering it in China—is something new. Depending on which analysis one subscribes to, China’s policies are either “a blueprint for technology theft on a scale the world has never seen before”,16 with the ultimate aim of overtaking the Western world in technology leadership, or a more understandable attempt to bolster China’s capabilities17, albeit with reckless disregard for the impact on foreign companies. Regardless of the intention,theresultisthesame—foreigninvestorsarespooked.Amongoursurveyrespondents,49%wereconcernedorveryconcernedthattheywouldbeforcedtogiveuptheirIPinexchangeformarketaccess.Amongbigcompaniesthefigurewas52%.Whilethegovernment’seffortstoraiseincomesandspur consumption were seen by respondents as having the biggest impact on their China strategy, the regulatory environment and industrial policies ranked second.

The reason China is demanding more from technology-rich foreign companies is not hard to fathom. What was initially a desire to move up the value chain has suddenly become a need, as China faces rising labourcosts,anageingpopulationandunstabledemandfromitstraditionalexportmarkets,forcingitto keep growth going with fewer resources and to stoke demand in its own domestic market. Yet previous policies aimed at improving technological prowess have produced little. While a handful of companies has become globally competitive—Huawei, a telecoms-equipment maker, is universally held up as the poster child—in the main Chinese manufacturers have remained low-end assemblers in the global supply chain.

Apple’siPhoneisoftencitedasanexample.OftheUS$500pricetagforaphone,ChinagetsaboutUS$7foritsassemblyjob,whileJapanesecompaniesgetUS$60andGermanfirmsUS$30(Appleitselfmakes US$321).18

Effortstochangeallofthisbeganfiveyearsago,withtheMediumandLong-TermPlanforScienceand Technology Development (MLP), issued by the State Council. It stands at the core of what has becomeknownasthe‘indigenousinnovationpolicy’.TheMLP,towhichfewpaidattentionwhenitwasannounced, was really more of a sweeping mission statement. But subsequent implementing regulations and other policies have been issued seemingly in line with the mission and, as they are now being implemented, the impact is beginning to be felt. Some analysts believe that this confusing labyrinth is a co-ordinated effort.19 Others are doubtful that even the Chinese government could pull together so many moving parts, citing inter-agency battles and what seems to be a diminishing will among provinces andmunicipalitiestofollowthecentralgovernment’sorders.Ifanythingisclear,itistheexpected

16 James McGregor, “China’s Drive for Indigenous Innovation, A Web of Industrial Policies”, American Chamber of Commerce, 2010

17 Dieter Ernst, “China’s Innovation Policy is a Wake-up CallforAmerica”,AsiaPacificIssues, East-West Centre, May 2011

18 Yuqing Xing and Neal Detert, “How the iPhone Widens the United States TradeDeficitwiththePeople’sRepublic of China”, Asian Development Bank Institute, 2010

19 In addition to McGregor’s work cited above, another excellentefforttopulltogether all of the policies into a coherent picture is “ChinavsTheWorld:WhoseTechnologyisit?”byThomasM Hout and Pankaj Ghemawat, Harvard Business Review, December 2010

13 www.amchamchina.org/businessclimate2011

14 www.europeanchamber.com.cn

15www.cjcci.biz/public_html/whitepaper/2011

© The Economist Intelligence Unit Limited 2011 31

Multinational companies and China: What future?

roleofforeigncompanies.TheMLPdefinesindigenousinnovationas“enhancingoriginalinnovationthrough co-innovation and re-innovation based on the assimilation of imported technologies”.

Co-ordinated or not, the policies that are now commonly referred to in totoas‘indigenousinnovation’arealreadyhavingasignificantimpactonforeignbusiness.TheAmericanChamberofCommerceinChinareportedinits2011BusinessClimateSurveythat26%ofrespondentswerealreadylosingbusinessand40%expectedtheywouldlosebusinessinfuture.Thepoliciescombinerun-of-the-milltaxbreaksandincentivesforlocalcompaniesinvolvedininnovation,withmoreprotectionistmeasuressuch as requiring state-owned entities to favour locally-developed IP in their purchasing, or for foreign companies to reveal sensitive information in order to sell their products in China. In the background isarenewedemphasis,notalwaysspeltoutinofficialpolicy,onjointventures.Notsurprisingly,theAmerican Chamber’s survey showed that the biggest concern was the loss of sales to state-owned entities.

China has softened some of the more egregious measures, especially where they amounted to outrightprotectionism.Forexample,thegovernmenthadoriginallystatedthatitwouldsupportindigenous innovation by using the public-procurement process to favour products from Chinese companies and containing IP owned by China. It drafted a catalogue of products that would qualify for procurement. But after protests from no less than 34 international trade associations, the requirements on IP ownership were watered down, and in January 2011 the Chinese president, Hu Jintao, vowed to delink indigenous innovation from public procurement altogether.

Yet the US-China Business Council issued a circular in July 2011 stating that 22 provincial- and municipal-level governments (including the Beijing municipal government) had issued their own catalogues, with three being issued since Mr Hu’s statement.20ManycontainexplicitreferencestoIPownership and import substitution.

Thisdevelopmentexplainswhysurveyrespondentsarejustasconcerned—moresointhecaseofbigcompanies—with protectionism at the local level as they are about the national level. There has been a discernable trend in recent years for multinationals to align more closely with local governments, making themselves indispensible to the local administration by providing investments in infrastructure, education and so on. In return, the local administration helps them to deal with issues like IPR infringements,unauthorisedtaxesandgeneraldirtytricksbycompetitors.“Itisoddandalittlemafia-like, but they are doing the best they can,” notes one consultant.

20 Provincial and Local Indigenous Innovation Catalogues, US-China Business Council, July 2011

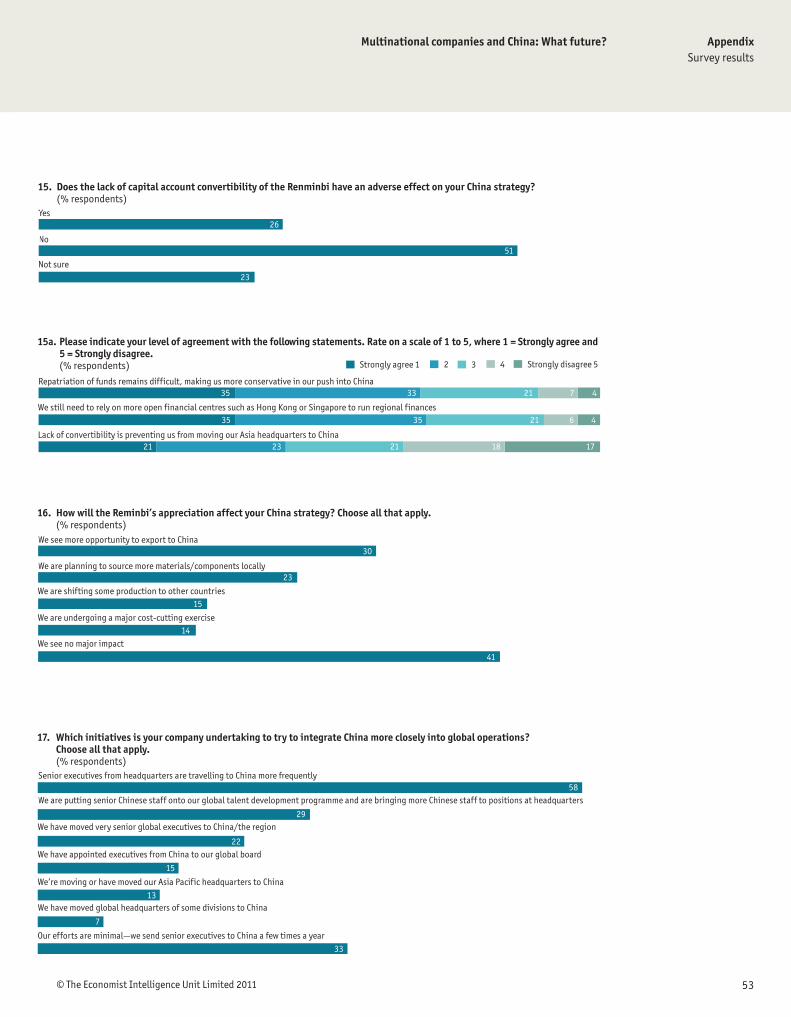

Who cares about the yuan?How will the reminbi’s appreciation affect your China strategy? Choose all that apply.(% respondents)We see more opportunity to export to China

We are planning to source more materials/components locally

We are shifting some production to other countries

We are undergoing a major cost-cutting exercise

We see no major impact

Source: Economis Intelligence Unit survey

30

15

14

41

23

© The Economist Intelligence Unit Limited 201132

Multinational companies and China: What future?

Somedoubtthattheeliminationofofficialpolicieswouldmakemuchdifference.AccordingtoJohnChiang,aformerITindustryexecutivewhonowteachestechnologymanagementatPekingUniversity, parochialism is an acceptable way of thinking in China, which is still coming off a surge of nationalistpridefollowingtheglobalfinancialcrisis.“Nomatterwhattheofficialpolicyis,MNCswillbehandicapped by this patriotism,” he says.

A non-standard approachChina’s efforts to develop its own industrial standards are also related to the indigenous innovation strategy. While the development of proprietary standards is understandable, the way in which China is going about it, and the lack of transparency in its approach, has led foreign companies to believe that these standards will be used as protectionist weapons.21 In many other countries standards are set by industry consensus and then ultimately judged by markets. China’s efforts, however, are being led by the government and are not subject to industry review or market scrutiny.

The most well-known cases involve China’s attempts to set its own wireless networking and 3G standards, known as WAPI and TD-SCDMA respectively. To cut a long story short, most mobile phone users in China today use the international Wi-Fi standard. But mobile phones sold in China today must still support WAPI, the Chinese standard, and their makers such as Nokia must pay a royalty to WAPI’s creators. TD-SCDMA is also in use, by China Mobile, though it is reportedly still plagued by bugs. Other operators rely on the international-standard CDMA.

Even without government direction, the standards-setting process is all too often hijacked by vested interests and used to keep out of the market foreign products with which Chinese producers cannot compete.Foreignfirmsarerarelyallowedtoparticipateinstandards-formingcommitteesand,whentheyare,itisusuallyonlyas“observers”.Askedwhatwastheexcusefornotallowingtheirparticipationin a standards committee, one foreign equipment maker said, “They said it’s only for Chinese companies. Itwasassimpleasthat.We’vefinallymanagedtoget‘observer’statussoweknowabitmorewhat’sgoing on. We used to have cases where we were knocked off the list because we weren’t informed of the requirements.”

Many standards are what has come to be known as “voluntary, yet compulsory”. WAPI is a classic example.Anotherisfarmequipment,wherecompaniesmustmeetthestandards(onwhichonlylocalmanufacturers have input) or be left off the list for government subsidies for equipment purchase, which are the key driver of the market.