multimedia & hi tech investments – a „cutting edge” for innovation kocice invest 2010,...

TRANSCRIPT

Multimedia & Hi Tech Investments – a „cutting edge” for innovation

KOCICE INVEST 2010, October 19th

PwC

Interactive multimedia systems may

allow the developing countries to

overpass the industralisation age

Stan Shih, General Director Acer Group

1. A recognised academic/research center, similar to Stanford University, Cambridge or MIT.

2. A success story like Microsoft, Apple or Google history.

3. A right competence/talent in advanced technology and the ability to acquire it.

4. Financial capital accepting high risk investments, exemple Israel and Taiwan.

5. Infrastructure – South Korea, Singapur.

6. Right behavior – confidence with an appetite for risk.

What we need to create a new Silicon Valley?

What is an Innovation in the interactive multimedia space?

@

Agenda

• What are the innovation drivers

• Where we stand in Hi Tech „cutting edge” innovation

• How to turn knowledge, capital and infrastructure into the development of a Region

• Multimedia City of Nowy Sącz – Case Study

Agenda

• What are the innovation drivers• Where we stand in Hi Tech „cutting edge” innovation

• How to turn knowledge, capital and infrastructure into the development of a Region

• Multimedia City of Nowy Sącz – Case Study

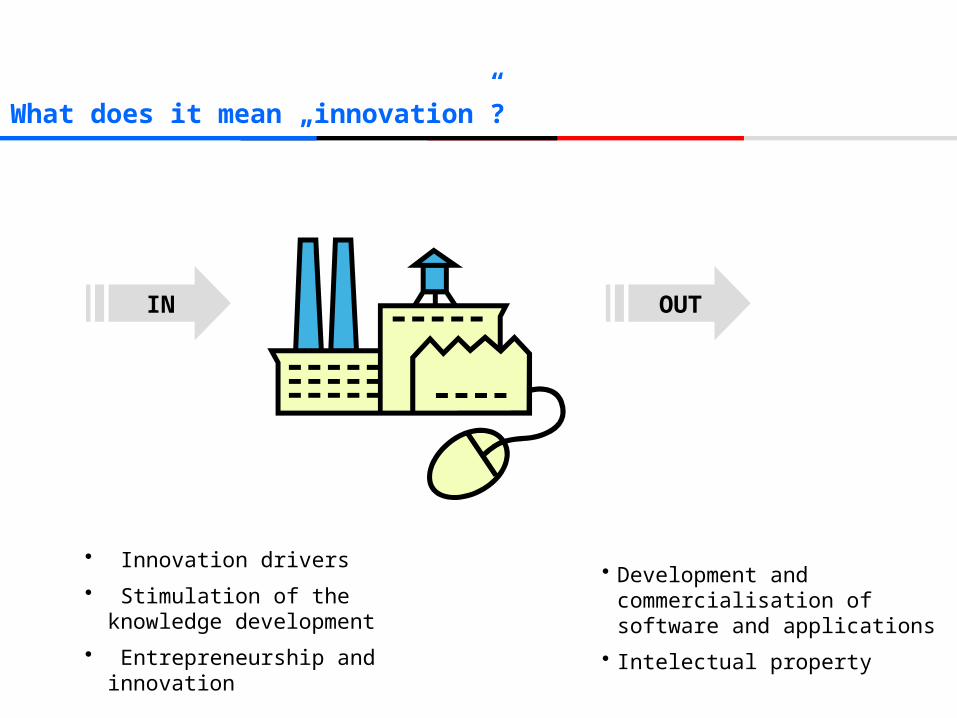

What does it mean „innovation”?

• Innovation drivers

• Stimulation of the knowledge development

• Entrepreneurship and innovation

IN OUT

• Development and commercialisation of software and applications

• Intelectual property

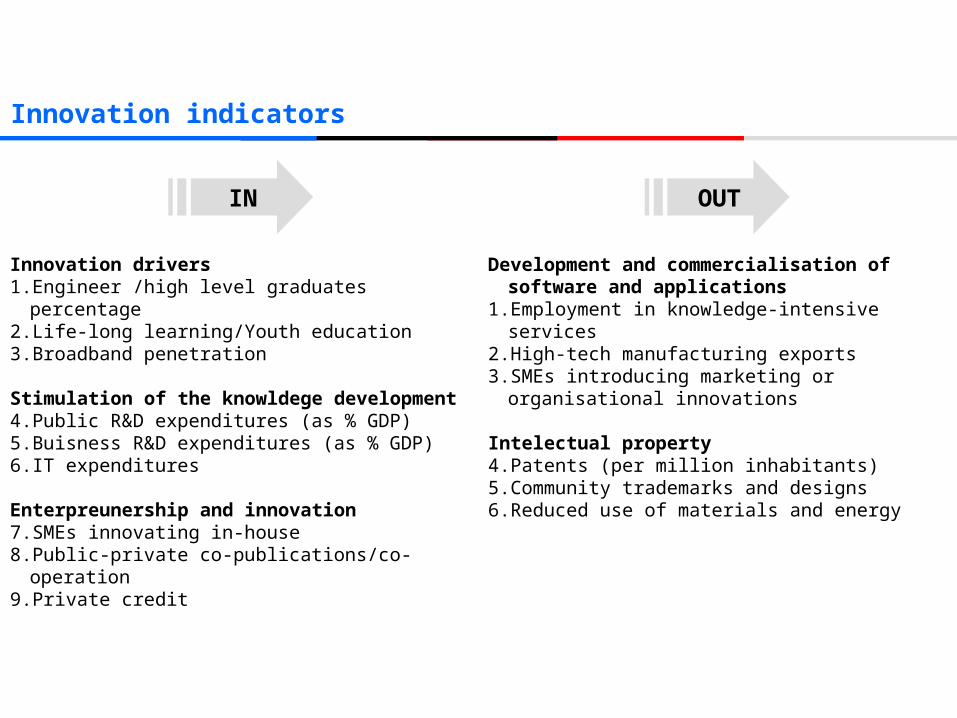

Innovation indicators

Innovation drivers1. Engineer /high level graduates percentage2. Life-long learning/Youth education3. Broadband penetration

Stimulation of the knowldege development4. Public R&D expenditures (as % GDP)5. Buisness R&D expenditures (as % GDP)6. IT expenditures

Enterpreunership and innovation7. SMEs innovating in-house8. Public-private co-publications/co-operation9. Private credit

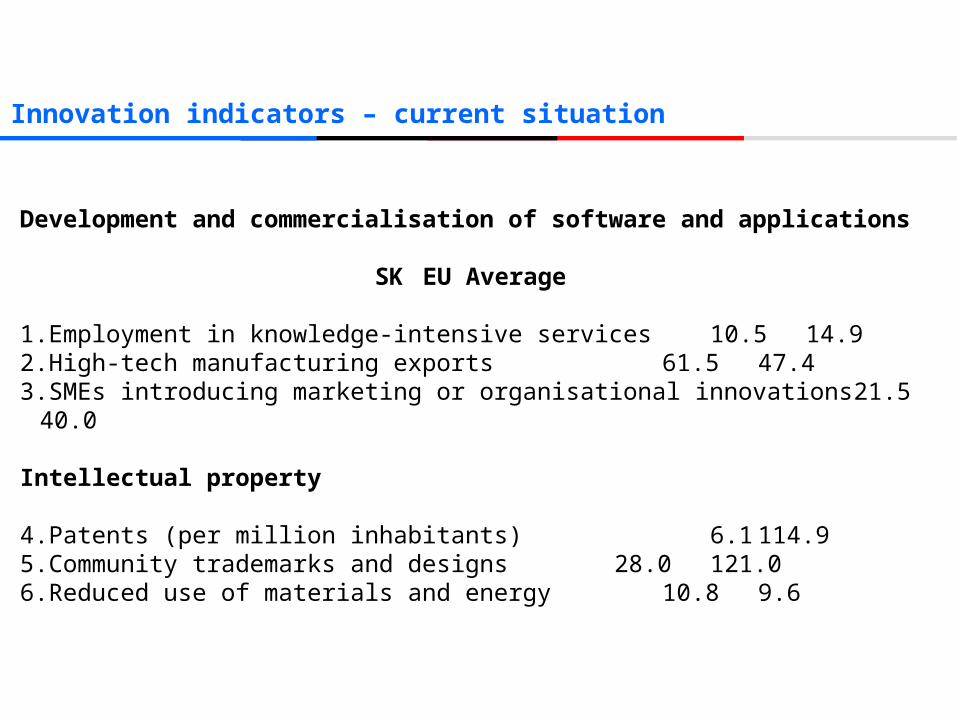

Development and commercialisation of software and applications

1. Employment in knowledge-intensive services2. High-tech manufacturing exports3. SMEs introducing marketing or organisational

innovations

Intelectual property4. Patents (per million inhabitants)5. Community trademarks and designs6. Reduced use of materials and energy

IN OUT

Innovation Index– current situation

Ind

eks

Inn

ow

acyj

no

ści

Source: European Innovation Scoreboard 2009

Innovation indicators

Innovation drivers SK EU Average

1.Engineer /high level graduates percentage 28.1 40.52.Life-long learning/Youth education 3.3 9.63.Broadband penetration 79.0 81.0

Stimulation of the knowledge development

4.Public R&D expenditures (as % GDP) 0.26 0.675.Business R&D expenditures (as % GDP) 0.20 1.216.IT expenditures 2.5 2.7

Entrepreneurship and innovation

7.SMEs innovating in-house 17.9 30.08.Public-private co-publications/co-operation 7.0 36.19.Private credit 0.45 1.27

Innovation indicators – current situation

Development and commercialisation of software and applications

SK EU Average

1.Employment in knowledge-intensive services 10.5 14.92.High-tech manufacturing exports 61.5 47.43.SMEs introducing marketing or organisational innovations 21.5 40.0

Intellectual property

4.Patents (per million inhabitants) 6.1 114.95.Community trademarks and designs 28.0 121.06.Reduced use of materials and energy 10.8 9.6

• Slovakia is being seen by investors as a moderate innovator country with a substantial

catching-up potential

• The country’s innovation performance is however below the EU average but at the

same time the rate of improvement exceeds the EU average

• Main growth engines were coming from an increase in broadband access, community

trade marks and design

• Main drawbacks are still in the area of R&D investments/expenditures by firms,

education and access to graduates in high tech areas

Slovakia and innovation viewed by investors

Agenda

• What are the innovation drivers

• Where we stand in Hi Tech „cutting edge” innovation

• How to turn knowledge, capital and infrastructure into the development of a Region

• Multimedia City of Nowy Sącz – Case Study

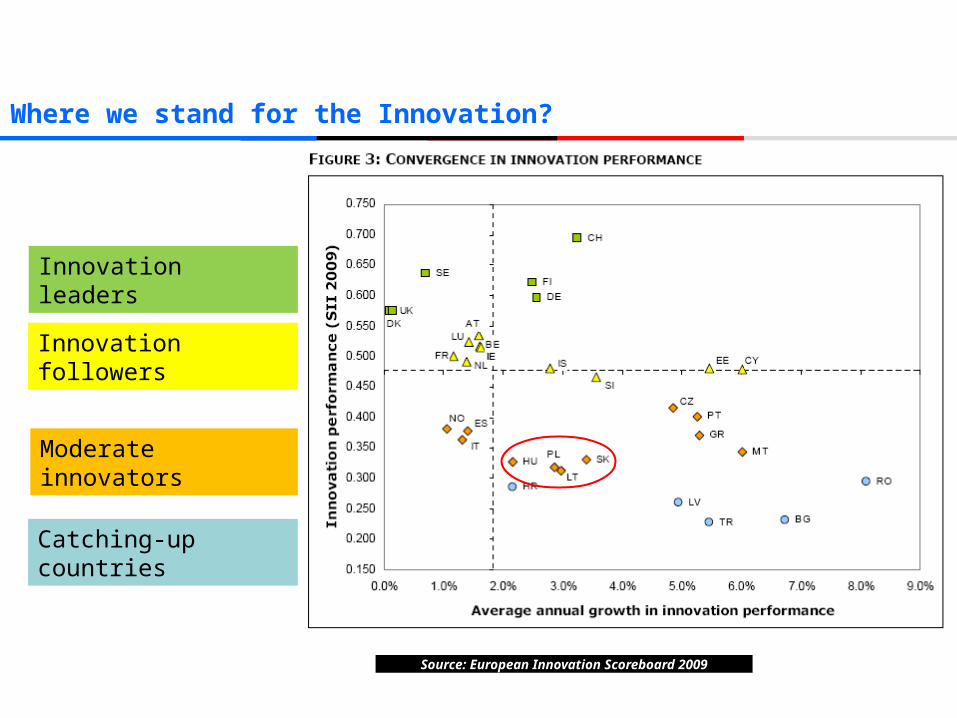

Where we stand for the Innovation?

Source: European Innovation Scoreboard 2009

Innovation leaders

Innovation followers

Moderate innovators

Catching-up countries

Kosice region

Source: European Innovation Scoreboard 2009

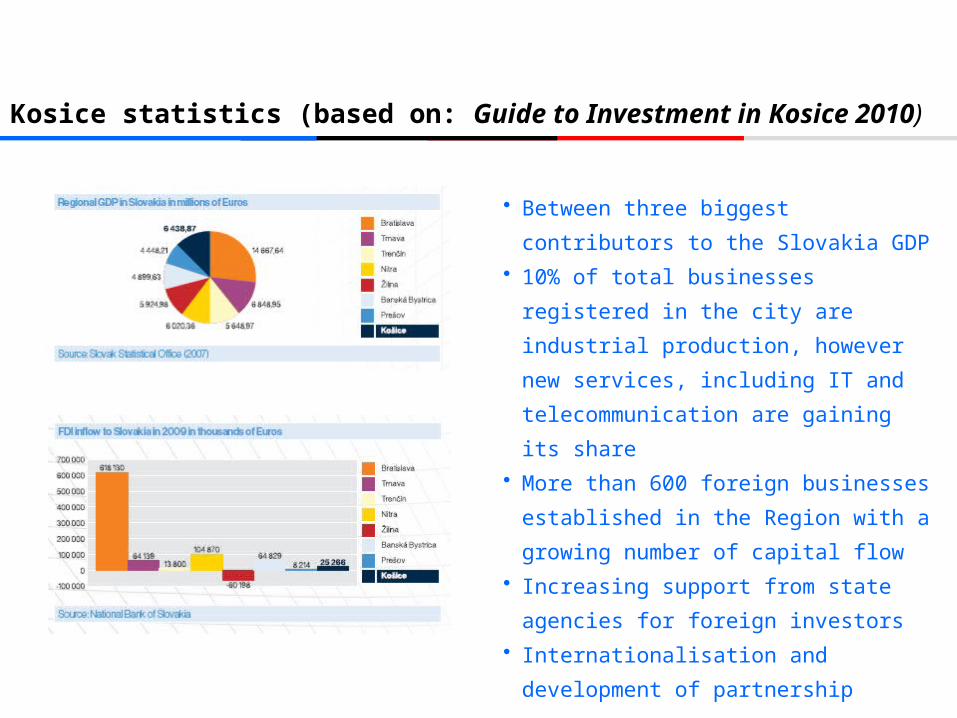

Kosice statistics (based on: Guide to Investment in Kosice 2010)

• Between three biggest contributors to the

Slovakia GDP

• 10% of total businesses registered in the

city are industrial production, however new

services, including IT and

telecommunication are gaining its share

• More than 600 foreign businesses

established in the Region with a growing

number of capital flow

• Increasing support from state agencies for

foreign investors

• Internationalisation and development of

partnership

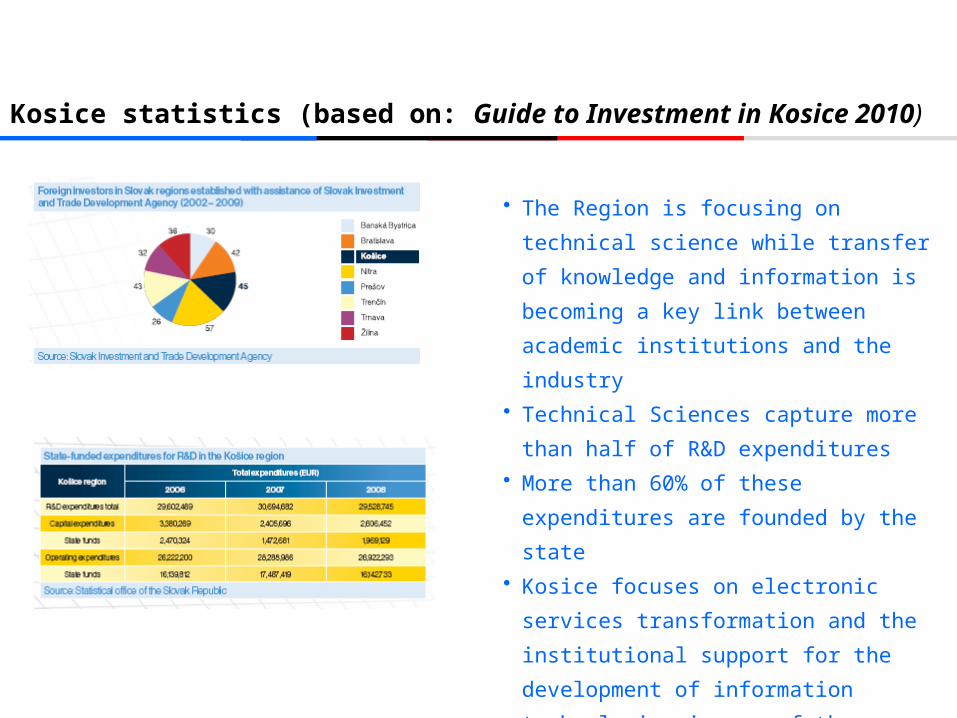

• The Region is focusing on technical

science while transfer of knowledge and

information is becoming a key link between

academic institutions and the industry

• Technical Sciences capture more than half

of R&D expenditures

• More than 60% of these expenditures are

founded by the state

• Kosice focuses on electronic services

transformation and the institutional support

for the development of information

technologies is one of the priority

Kosice statistics (based on: Guide to Investment in Kosice 2010)

Agenda

• What are the innovation drivers

• Where we stand in Hi Tech „cutting edge” innovation

• How to turn knowledge, capital and infrastructure into the development of a Region

• Multimedia City of Nowy Sącz – Case Study

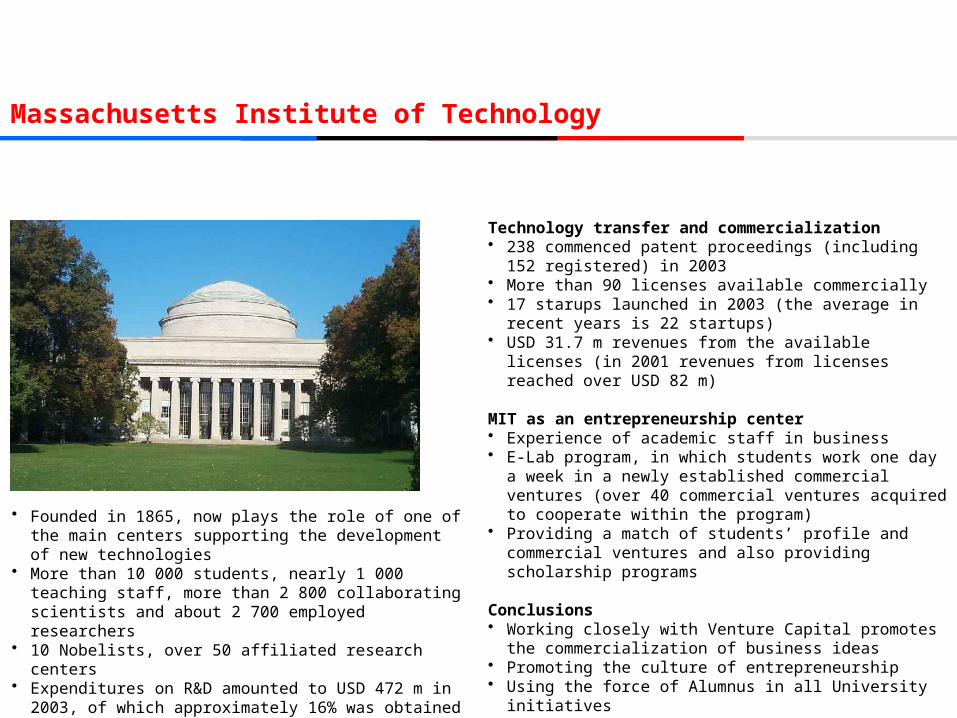

Massachusetts Institute of Technology

Technology transfer and commercialization• 238 commenced patent proceedings (including 152

registered) in 2003• More than 90 licenses available commercially• 17 starups launched in 2003 (the average in recent years is

22 startups)• USD 31.7 m revenues from the available licenses (in 2001

revenues from licenses reached over USD 82 m)

MIT as an entrepreneurship center• Experience of academic staff in business• E-Lab program, in which students work one day a week in a

newly established commercial ventures (over 40 commercial ventures acquired to cooperate within the program)

• Providing a match of students’ profile and commercial ventures and also providing scholarship programs

Conclusions• Working closely with Venture Capital promotes the

commercialization of business ideas• Promoting the culture of entrepreneurship• Using the force of Alumnus in all University initiatives

• Founded in 1865, now plays the role of one of the main centers supporting the development of new technologies

• More than 10 000 students, nearly 1 000 teaching staff, more than 2 800 collaborating scientists and about 2 700 employed researchers

• 10 Nobelists, over 50 affiliated research centers• Expenditures on R&D amounted to USD 472 m in 2003, of

which approximately 16% was obtained from private sponsors

Georgia Institute of Technology

Technology transfer and commercialization• 53 commenced patent proceedings in 2003, including 41

registered patents• More than 70 commercially available licenses• 12 startup ventures launched

Venture Lab• Georgia Institute of Technology has created an initiative called

Venture Lab to facilitate the commercialization process of technology solutions developed at the university

• The initiative allows to make funds available for the development of commercial ventures, while ensuring control of university over their development by maintaining ownership of the developed solutions (patents)

• More than 100 comapnies formed (including 2 sold for more than USD 60 m each in 2003)

Conclusions• Very strong regional relations promoting local

entrepreneurship, together with the financial commitment on the part of state institutions

• Well-established and proven financial support program (incubator)

• University with achievements of 16 000 students and approximately 900 teaching staff

• Excellent example of cooperation with institutions of the state of Georgia

Stanford University

Technology transfer and commercialization• 334 commenced patent proceedings, including 117 obtained

patents in 2003• In 2003 over 123 licenses were made commercially available

with the revenue accounting to USD 45.4 m• More than 170 startup ventures launched in 1999-2001

Stanford Technology Venture Program• Promoting entrepreneurship in business, both through

educational programs and above all support in the development of the most interesting and promising research

• Many initiatives promoting and supporting the commercialization of scientific ventures (Entrepreneur Club, Venture Capital Club, High-Tech Club)

Conclusions• Use of government financial support in the early development

works (doctoral programs)• Relations with funds like Venture Capital• Proximity of Silicon Valley

• The University was founded in 1891, almost 15 000 students• 17 Nobelists and 133 members of the National Academy

of Science• More than USD 639 m spending on R&D, including about

83% funds obtained from government grants

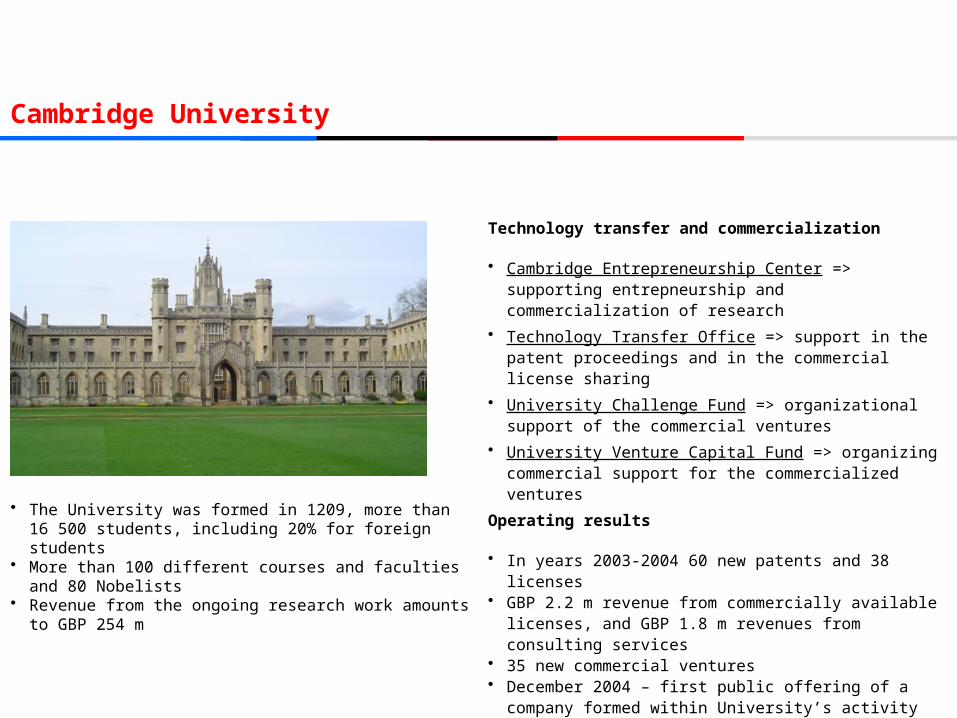

Cambridge University

Technology transfer and commercialization

• Cambridge Entrepreneurship Center => supporting entrepneurship and commercialization of research

• Technology Transfer Office => support in the patent proceedings and in the commercial license sharing

• University Challenge Fund => organizational support of the commercial ventures

• University Venture Capital Fund => organizing commercial support for the commercialized ventures

Operating results

• In years 2003-2004 60 new patents and 38 licenses• GBP 2.2 m revenue from commercially available licenses, and

GBP 1.8 m revenues from consulting services• 35 new commercial ventures• December 2004 – first public offering of a company formed

within University’s activity

• The University was formed in 1209, more than 16 500 students, including 20% for foreign students

• More than 100 different courses and faculties and 80 Nobelists

• Revenue from the ongoing research work amounts to GBP 254 m

Agenda

• What are the innovation drivers

• Where we stand in Hi Tech „cutting edge” innovation

• How to turn knowledge, capital and infrastructure into the development of a Region

• Multimedia City of Nowy Sącz – Case Study

1. An academic/research center

2. A success story

3. A right competence/talent in advanced technology

4. Financial capital accepting high risk investments

5. Infrastructure

6. Right behavior

From an idea to the implementation …

KEY POINTS:

State-of-the art infrastructure for multimedia productions,

Entrepreneur-friendly policies and business climate in the city and region,

Very well skilled workforce prepared by the best Business University in Poland,

Multimedia R&D facilities at the world class level,

Knowledge exchange – open structure of the organization,

Business Development services and funding,

A strong brand with international realm,

A permanent focus on INNOVATION!

Multimedia City in Nowy Sącz (Poland) means:

R&D CENTER

TECHNOLOGY PARK

VENTURE CAPITAL

BUSINESS INCUBATOR

MULTIMEDIA CLUSTER

Multimedia City project in Nowy Sącz is an internationational center

of innovation focused on development of multimedia products and

services and information systems. Project is based on the resources

of Nowy Sącz School of Business – National-Louis University

and more than 50 already dedicated partners.

The Multimedia City will consist of state-of-the-art multimedia

laboratories cooperating with information architecture and

application development section – coexisting on the basis of the

most modern servers and solutions in field of data processing and

transfer. Financial (financing) and legal (international law, patent

protection and intellectual property management) support will be

provided to create the „Innovation Management System/Policy”.

Key FACTS about the Project:

Initial investment planned 30+ m euro

Initial knowledge-input partners = more then 50 companies

Full operating capacity – year 2012

Presence – global

Active cooperation with business and education – YES!

PARTNERSHIP POSSIBILITIES – what do we offer and what do we expect?

• Focus on innovation

• Strong brand/market leader in multimedia or associated industry

• R&D budgets and ideas about R&D projects in multimedia

• Ideas about synergies with other companies

• Believer of networks, openness and ability to provide network member benefits

• Strong belief and support from management

• Willingness to relocate/open a branch/ have some activity on MC-grounds

• Provide support to MC-organisation (people, money, time, and others)

• Bring dynamism and entrepreneurship to the project!

Our vision is that the Nowy Sącz Region will become,

and be acknowledged globally,

as one of the most innovative, creative and productive locations in Europe

for Multimedia research, education, business, and investment by 2018 with the success of the Mutimedia City project.

THANK YOU

Piotr BaranowskiPricewaterhouseCoopersDirectorAdvisoryTechnology Information Communication Entertainment