multifamily market steve woodyard woodyard realty corp woodyard realty corp

TRANSCRIPT

Multi family Market

Steve WoodyardWoodyard Realty Corp.

Jobs

Interest Rates

Financing

Low supply of new housing

New home owner credit and desire

Changing demographics

Technology

What drives the market?

Timeline of Woodyard Realty Corp.’s Sales to Out-of-State Investors Versus Local Investors

Out of State10% Out of State

Investors

53%

LocalInvestors

47%

Local Investors

90%

1984 – 20002001 – Oct 5, 2014

Memphis SubmarketsBartlett 38134, 38135, 38133 Collierville/Germ 38017, 38138, 38139Cordova/Lakeland 38016, 38018, 38002Downtown 38103, 38105, 38157 East 38119, 38120, 38122, 38117 Frayser 38127 Midtown 38104, 38107, 38111, 38112 North Mississippi 38632, 38637, 38654, 38671,

38664, 38680, 38676Raleigh 38108, 38128Southeast 38115, 38118, 38125, 38141 Southwest 38106, 38109, 38114, 38116,

38126,38132, 38131

as defined by Apartment Association of Greater Memphis

*Distressed assets are defined as properties with unusually low occupancy (less than 65% occupancy).

June 30, 2013; Information not been verified

Sub Market # Prop Units Occ % Units Occ % Rent Sq.ft Avg Sq.ftMarket

RentEffective

Rent

Bartlett 17 4,409 94.83% 0 94.83% $0.67 962 $645 $673

Collierville/Germantown 11 2,357 92.15% 252 95.72% $0.98 1042 $1,026 $1,027

Cordova/Lakeland 20 8,115 94.05% 0 94.05% $0.85 1022 $873 $853

Downtown 22 3,934 92.25% 199 93.73% $1.13 901 $1,017 $1,017

East 17 3,058 93.98% 0 93.98% $0.81 992 $799 $788

Frayser 13 1,805 87.92% 252 95.17% $0.64 839 $536 $536

Jackson, TN 6 753 93.89% 0 93.89% $0.69 966 $671 $671

Mid-town 34 3,814 89.77% 272 92.21% $0.80 790 $633 $633

North Mississippi 15 3,653 94.39% 0 94.39% $0.79 1034 $816 $804

Raleigh 10 2,208 83.29% 335 86.60% $0.71 844 $600 $554

Southeast 33 9,139 92.64% 134 93.46% $0.77 972 $747 $728

Southwest 18 3,000 91.60% 12 91.73% $0.58 955 $551 $744

Total 216 46,245 92.35% 1456 93.51% $0.80 956 $767 $771

Including Distressed*

Excluding Distressed*

Overall

Local Multifamily Market: 2014 Review (Jan-Oct 5, 2014)

Normal 22

REO/Distressed6

Type of Transaction28 Sales plus 7 Foreclosures

Frayser - 3

Raleigh - 1

Southwest- 1

Foreclosures by Submarket 7 Foreclosures

Foreclosures7East - 2

30+ apartment units in Greater Memphis Metropolitan Area

Local Multifamily Market: 2014 Sales (Jan-Oct 5, 2014)

28 Sales Transactions32 total sales in 2013

$219.4 Gross Sales Volume (in Millions) $239.3 total gross sales volume in 2013

5,487 Units Sold6,513 total units sold in 2013

$39,977 Average Price per Unit$36,757 total avg. price/unit in 2013

Southwest - 14%

Bartlett7% Cordova/

Lakeland 7%

East 7%

Midtown -39%

Southeast - 14%

Raleigh 4%

Germ./Collierville 4%

Frayser 4%

30+ apartment units in Greater Memphis Metropolitan Area

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 Jan-Oct 5, '14

$0

$50

$100

$150

$200

$250

$300

$350

$400

24 35 33 41 59 68 61 27 28 29 38 40 32 28

Vol

ume

in M

illio

ns

Local Multifamily Market: 2001-Oct. 5, 2014 Sales in Review

$59

$125

$188

$293

$370$345

$105

$65 $55

13-Yr Average*$195.9 Million

13-Yr Average*40 Transactions

$174

$323

$206$219

30+ apartment units in Greater Memphis Metropolitan Area * Does not include 2014

$239

2010 2011 2012 2013$0

$50

$100

$150

$200

$250

$300

$350

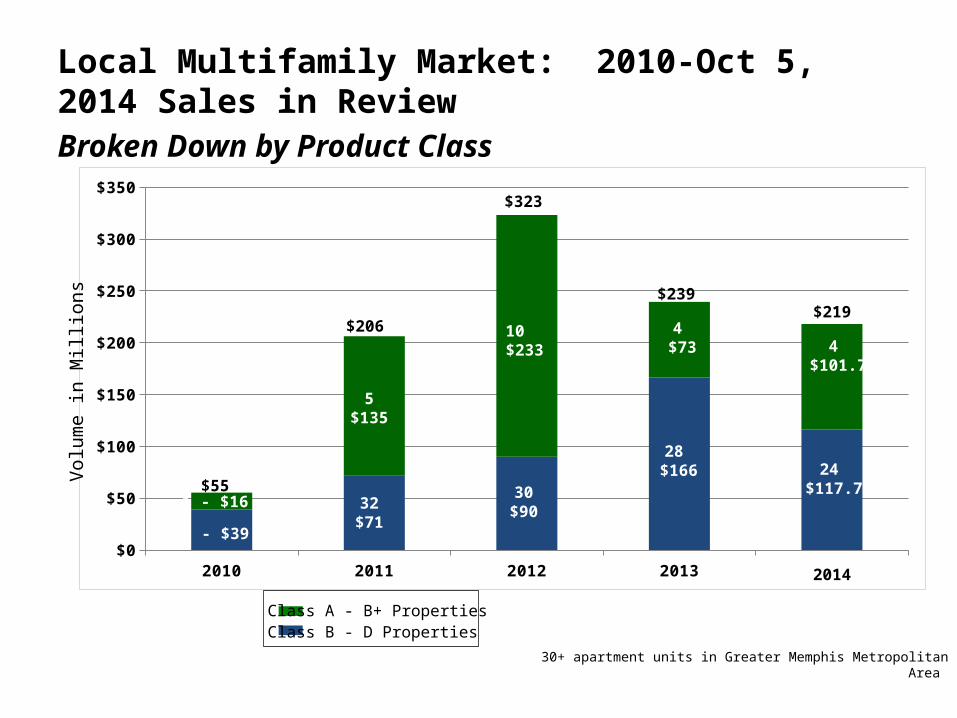

Local Multifamily Market: 2010-Oct 5, 2014 Sales in ReviewBroken Down by Product Class

$55

$323

$206

$239

28 - $39

1 - $16 32$71

5$135

30$90

10$233

28 $166

4 $73

Volu

me

in M

illio

ns

Class A - B+ Properties Class B - D Properties

30+ apartment units in Greater Memphis Metropolitan Area

$219

24 $117.7

4 $101.7

2014

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 20150

500

1000

1500

2000

2500

3000

3500

4000

4500

Local Multifamily Market: 2001 – 2014 Construction

14-Yr Average1176 Units

# of

Uni

ts

30+ apartment units in Greater Memphis Metropolitan Area

Local Multifamily Market: New Construction

University of Memphis AreaGather on Southern 74 CP3595 Southern 64 UCHighland Row 354 PLMidland Apts 120 PLDoyle Apts 127 PL

Downtown AreaPrinter’s Alley & Annex 54 UCSouth Junction Apts 197 UCToof Apts 50 UCThe Chisca Apts 165 UCCrescent Bluff 172 UCHarbor Isle 134 UCArtspace Memphis 44 PLUptown Apts 90 PL362 S Second 64 PLFrench Fort 67 PL

Collierville AreaWestbrook Crossing 227 CPCarrington Apts 112 CPSignature Apts 251 UC

Under Construction

Apts – Planning Stages

CP – Completed ProjectUC – Under ConstructionPL - Planned

Trends Improving the Rental DemandBaby Boomers Scaling Down, Entering Rental Market

In the United States, the baby boom generation represents 76 million people.

On January 1, 2011, as the baby boomers began to celebrate their 65th birthdays, 10,000 people turned 65 every day— this will continue for next 16 years.

Trends Improving the Rental DemandMore Renters Entering the Market - Generation Y

• Generation Y, the echo boom of the baby boomers, born from 1977-2001 (estimated majority are between 18-30 years old)

• Nearly 80 million in population (larger than the baby boomer population of 72 million)

27%Live withRelatives 60% Rent

13%Own

2006 2007 2008 2009 2010 2011 2012 2013 Mid Year 2014

86%

88%

90%

92%

94%

91%90%

89% 89%90% 90%

91% 92%

94%

2006 2007 2008 2009 2010 2011 2012 2013 Mid Year 2014

$600

$650

$700

$750

$800

$685 $690 $689 $694 $693 $713

$728 $748

$771

Local Multifamily Market: Mid Year 2014

*

* Apartment Association of Greater Memphis includes foreclosures and out of service apartments for the first time

Rent Trend

Occupancy Trend

*

Market Cycle as Projected by Integra Realty Resources

Out of State

LocalInvestors

Local Investors

2

1

3

2

1

3

2

1

3

2

1

3

Recovery PhaseDecreasing Vacancy RatesLow New ConstructionModerate AbsorptionLow/Moderate Employment GrowthNeg/Low Rental Rate Growth

Expansion PhaseDecreasing Vacancy RatesModerate/High New ConstructionHigh AbsorptionModerate/High Employment GrowthMed/High Rental Rate Growth

Hyper Supply PhaseIncreasing Vacancy RatesModerate/High New ConstructionLow/Negative AbsorptionModerate/Low Employment GrowthMed/Low Rental Rate Growth

Recession PhaseIncreasing Vacancy RatesModerate/Low New ConstructionLow AbsorptionLow/Neg Employment GrowthLow/Neg Rental Rate Growth

Recovery Expansion Hyper Supply Recession

2

1

3

1st Stage of the Phase

2nd Stage of the Phase

3rd Stage of the PhaseIntegra

Memphis

IRR - Memphis Metro- Decreasing Vacancy- Moderate/High New Construction- High Absorption- Moderate/High Employment Growth- Medium/High Rental Rate Growth

WRC30+ units

Woodyard Realty - Memphis Metro- Decreasing Vacancy- Low to Moderate New Construction- Moderate/High Absorption- Low/Moderate Employment Growth- Low/Medium Rental Rate Growth

Woodyard Realty Corp.’s 2015 Forecast

Each submarket will have improving conditions

Similar and slightly declining levels of foreclosures

Increasing levels of new construction

Modestly increasing rents that are gaining momentum

Improving Occupancy

Prices have hit bottom and are improving

Two possibly three years left to find value-add opportunities