multi state sales tax compplexities for service...

TRANSCRIPT

Presenting a live 110‐minute webinar with interactive Q&A

Multi‐State Sales Tax Complexities for pService TransactionsResponding to Different State Approaches to Exemptions, True Object Tests, and Other Challenges

T d ’ f l f

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

TUESDAY, OCTOBER 26, 2010

Today’s faculty features:

Matthew Schaefer, State and Local Tax Partner, Brann & Isaacson, Lewiston, Maine

Joe Hatfield, Senior Manager, BDO USA, Dallas

Peter Stathopoulos, Managing Director, State and Local Tax Group, Bennett Thrasher, Atlanta

David Yerkes, Tax Principal, State and Local Taxes, Grant Thornton, Dallas

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers.Please refer to the instructions emailed to registrants for additional information. If you have any questions,please contact Customer Service at 1-800-926-7926 ext. 10.

Tips for Optimal Sound Quality

If you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory and you are listening via your computer speakers, you may listen via the phone: dial 1-866-873-1442 and enter your PIN when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Continuing Education Credits FOR LIVE EVENT ONLY

For CLE and/or CPE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• Close the notification box

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the blue icon beside the box to send

M lti St t S l T C l iti F Multi‐State Sales Tax Complexities For Service Transactions

Oct. 26, 2010

Peter Stathopoulos, Bennett [email protected]

Joe Hatfield, BDO [email protected]

Matthew Schaefer, Brann & [email protected]

Joseph Schmidt, Grant [email protected]

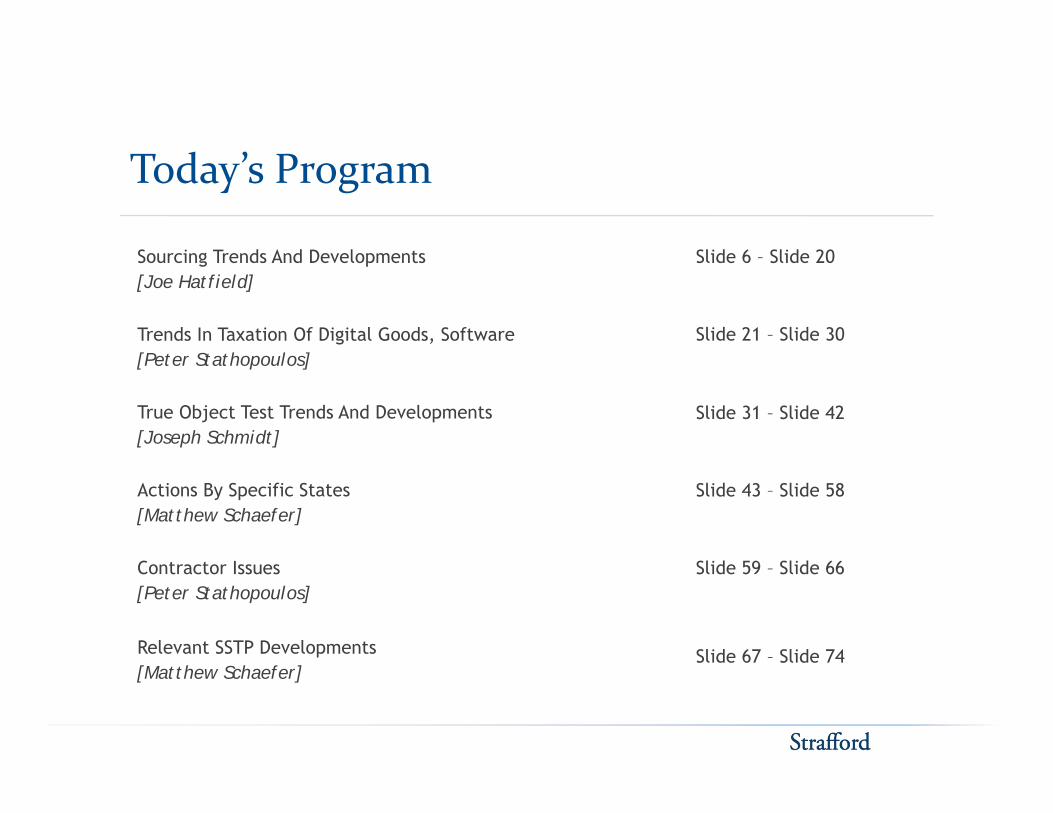

Today’s Program

S i g T d A d D l t Slid 6 Slid 20Sourcing Trends And Developments[Joe Hatfield]

Trends In Taxation Of Digital Goods, Software[P t St th l ]

Slide 6 – Slide 20

Slide 21 – Slide 30[Peter Stathopoulos]

True Object Test Trends And Developments[Joseph Schmidt]

Slide 31 – Slide 42

Actions By Specific States[Matthew Schaefer]

l d l d

Slide 43 – Slide 58

Contractor Issues[Peter Stathopoulos]

Relevant SSTP Developments

Slide 59 – Slide 66

Slide 67 – Slide 74[Matthew Schaefer]

SOURCING TRENDS AND Joe Hatfield, BDO USA

SOURCING TRENDS AND DEVELOPMENTS

Sourcing - GeneralSourcing - General

• The sales of tangible personal property are generally taxed by one of two methodstwo methods Destination Origin

• The ship-to and ship-from addresses are used to determine destination and origin.

BDO USA, LLP Nexus UpdatePage 7

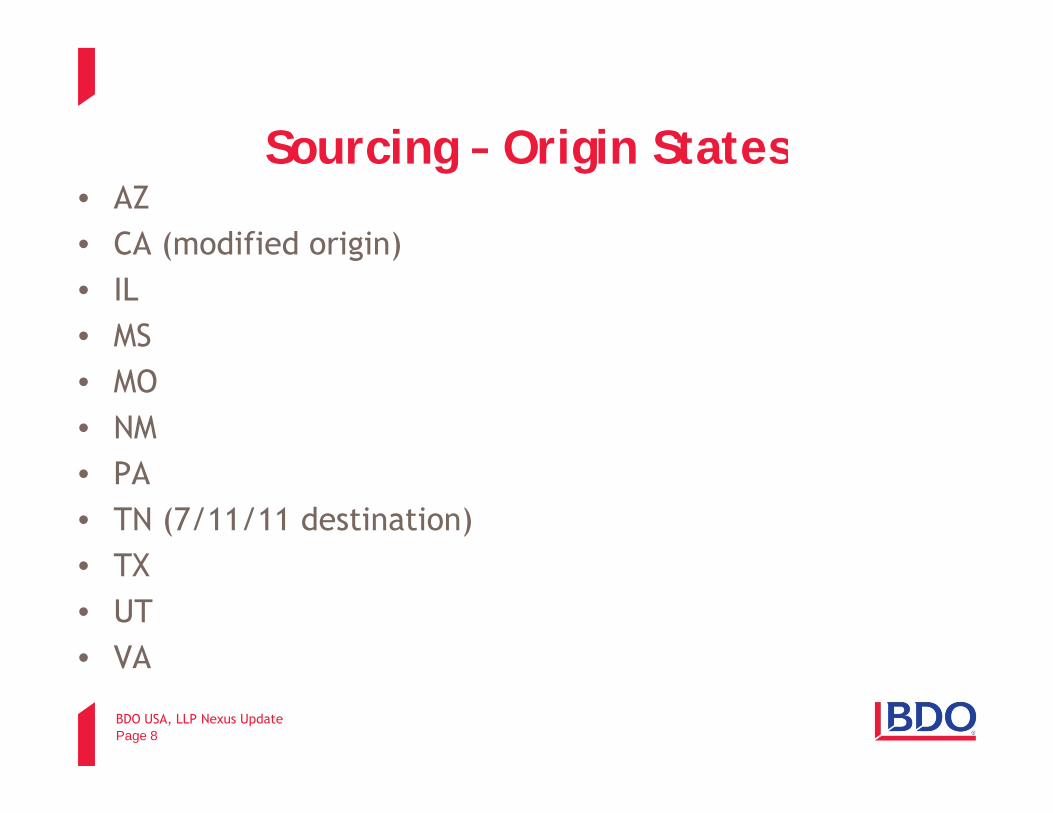

Sourcing – Origin StatesSourcing – Origin States• AZ• CA (modified origin)CA (modified origin)• IL• MS• MO• NM• PA• TN (7/11/11 destination)

TX• TX• UT• VA

BDO USA, LLP Nexus Update

VA

Page 8

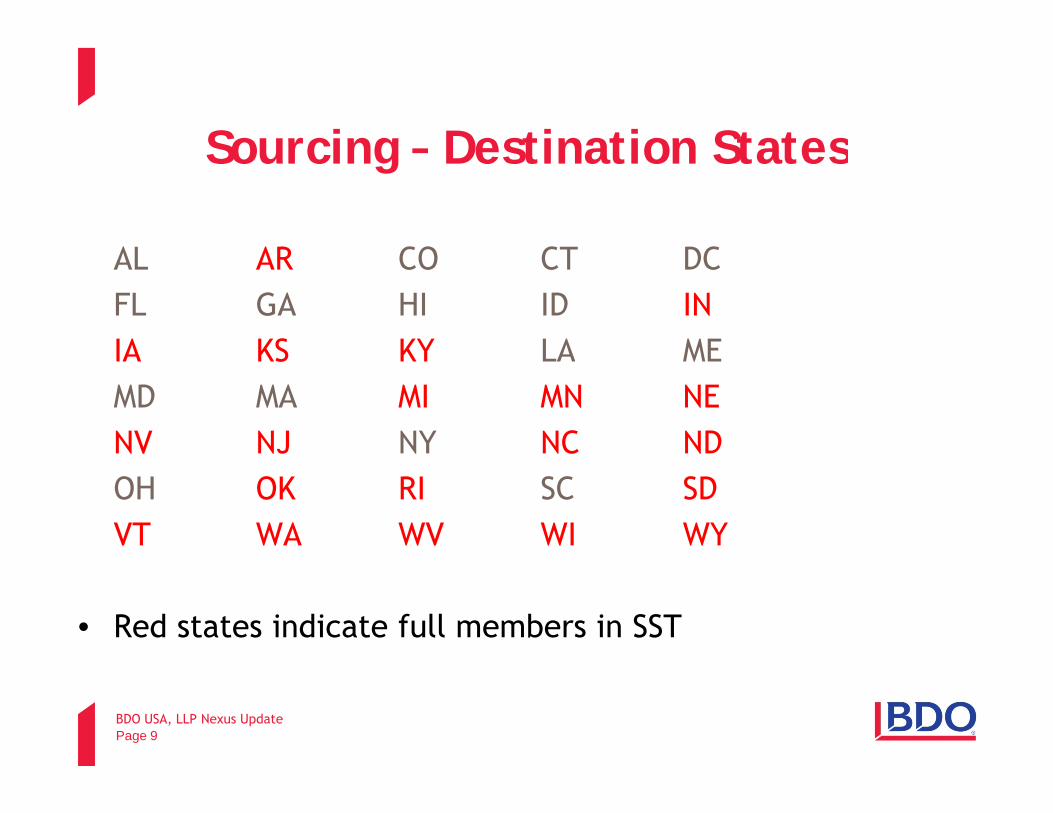

Sourcing – Destination StatesSourcing – Destination States

AL AR CO CT DCAL AR CO CT DCFL GA HI ID INIA KS KY LA MEIA KS KY LA MEMD MA MI MN NENV NJ NY NC NDOH OK RI SC SDVT WA WV WI WY

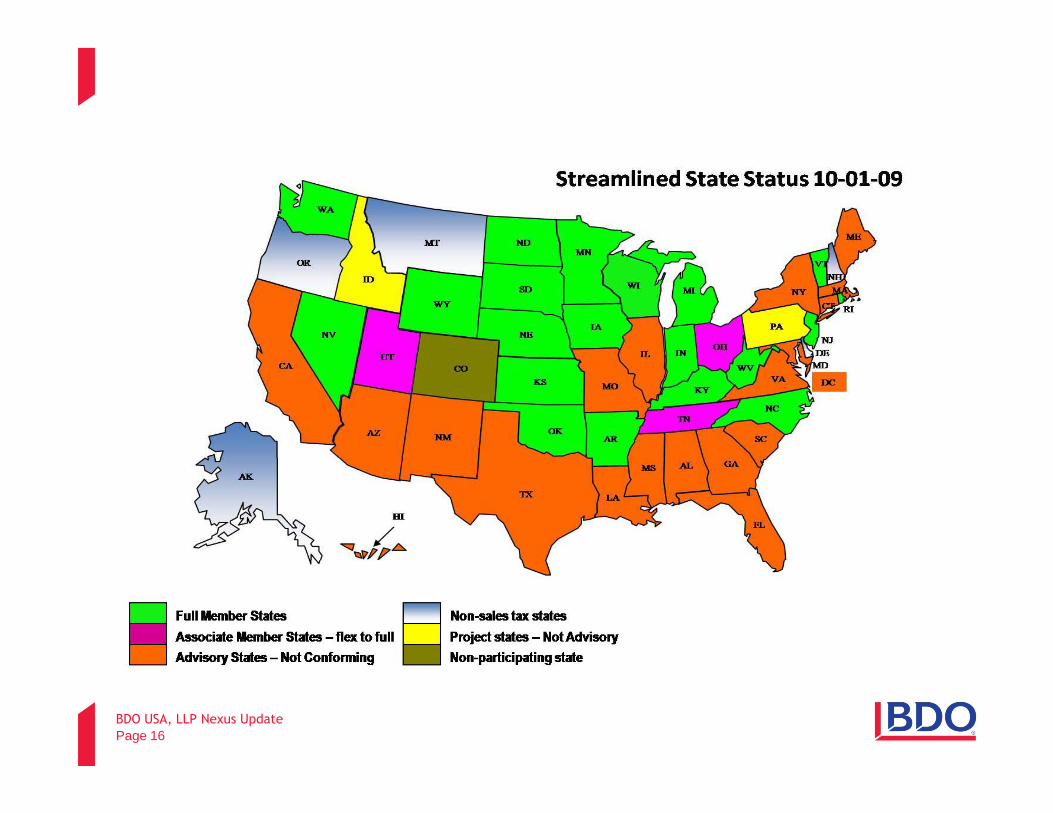

• Red states indicate full members in SST

BDO USA, LLP Nexus UpdatePage 9

Sourcing Of Services OptionsSourcing Of Services Options

• Origin: Location of where services are performedOrigin: Location of where services are performed

• Destination: Location that services are received (benefit)( )

BDO USA, LLP Nexus UpdatePage 10

Sourcing Of Services IssuesSourcing Of Services Issues

• Multiple points of provision

• Multiple points of use

• Multiple taxing jurisdictions

BDO USA, LLP Nexus UpdatePage 11

Multiple Points Of ProvisionMultiple Points Of Provision

• Services are being performed in multiple locations

• Potential for double-taxation

• Should only be services are performed in an origin state and received in a destination state

BDO USA, LLP Nexus UpdatePage 12

Multiple Points Of UseMultiple Points Of Use

Services are received by a customer at multiple locations• Services are received by a customer at multiple locations

• Seller may not know where the customer is receiving Seller may not know where the customer is receiving services.

• Seller may not be licensed to collect tax in all jurisdictions for which services are being provided.

• Some states allow issuance of a multiple-points-of-use certificate.

BDO USA, LLP Nexus UpdatePage 13

Multiple Taxing JurisdictionsMultiple Taxing Jurisdictions

• Taxability of services vary from one state to anotherTaxability of services vary from one state to another.

• Tax rates will vary among jurisdictions.y g j

BDO USA, LLP Nexus UpdatePage 14

Streamlined Sales Tax Sourcing RulesStreamlined Sales Tax Sourcing Rules

• Requires destination-based sourcing in most cases.O i i b d i i ll d i t t th t h l l • Origin-based sourcing is allowed in states that have local sales taxes.

• Product is defined as TPP, digital product or service.Product is defined as TPP, digital product or service.• Sourced to seller’s place of business if received by

purchaser at that location, or• Sourced to location of receipt by purchaser, or • If location of receipt is not known, sale is sourced to a

known address of the purchaserknown address of the purchaser.• Multiple-points-of-use exemption is not allowed

BDO USA, LLP Nexus UpdatePage 15

BDO USA, LLP Nexus UpdatePage 16

Sourcing – Specific ServicesSourcing – Specific Services

• Information services

• Data processing

• Application service providers/cloud computing

BDO USA, LLP Nexus UpdatePage 17

Information ServicesInformation Services• Collecting, compiling or analyzing information of any kind

and the furnishing of reports to other personsand the furnishing of reports to other persons• Web surveys and tax research sites are information services• Sourcing can be determined by location of seller or of

purchaser.• Potential for taxation in multiple jurisdictions or no

jurisdictionsjurisdictions• Multiple-points-of-use exemption is allowed in many

jurisdictions.• This exemption allows seller to not collect tax.• Purchaser is required to pay use tax based upon allocation.

BDO USA, LLP Nexus UpdatePage 18

Data ProcessingData Processing

• Processing of others’ data, including key-punching or g , g y p gsimilar data entry services

• Payroll processing is an example.• Sourcing can be determined by location of seller or of

purchaser.• Potential for taxation in multiple jurisdictions or no • Potential for taxation in multiple jurisdictions or no

jurisdictions• Multi-point-of-use exemption allowed in many jurisdictions• This exemption allows seller to not collect tax.• Purchaser is required to pay use tax based upon allocation.

BDO USA, LLP Nexus UpdatePage 19

Application Service Provider/ Application Service Provider/ Cloud Computing

• Software accessed over the Internet• Examples include online training, sales tax calculation• States argue this is the use of tangible personal property that should be

sourced to user’s location• Very few states have addressed this issue directly

New York Texas Allow allocation based upon user locationAllow allocation based upon user location

BDO USA, LLP Nexus UpdatePage 20

TRENDS IN TAXATION OF Peter Stathopoulos, Bennett Thrasher

TRENDS IN TAXATION OF DIGITAL GOODS, SOFTWARE

Historical Background

• Most states have historically followed the legal fiction that non-customized (canned) software is tangible personal property (vs. acustomized (canned) software is tangible personal property (vs. a taxable service)

• This position was originally based on the presence of a tangible• This position was originally based on the presence of a tangible medium embodying the software (disk) and the previous treatment of films/music recorded on a tangible medium.

22

Historical Background (Cont.)

• For example, in Turner Comm. Corp. v. Chilivis, 236 Ga. 91 (1977), the Georgia Supreme Court held that videotape was TPP for sales tax purposes, because the intangible property contained in a videotape would be valueless if not embodied in a tangible medium.

• Customized software was deemed to be more akin to a service and was therefore excluded from taxation in many states based on a “true object” analysis.

• Nonetheless, many states began to impose tax on information services, database services and information processing.

23

Historical Background (Cont.)

• As software began to be transferred electronically (via load-and-leave or download over the Internet), many states did not impose sales tax on such transactions due to a lack of a physical medium being transferred.

• Accordingly, many states have continued to define software as TPP but now tax its sale or license, regardless of the means of delivery to the customer.

• However, most of these states do not specifically address software as a service or application service provider models. Further, sales sourcing issues have not been explored.

24

Problems Inherent In Taxing Software

• Tangible personal property vs. service• Defining canned vs. customer software• Substance over form in SAAS/ASP customer agreements• Substance over form in SAAS/ASP customer agreements• If the legal fiction is maintained that software is TPP, how is remote

license of software sourced?H i ll d t d t i h it ft i b i d• How is a seller supposed to determine where its software is being used on a terminal-by-terminal basis?

• Taxation of software maintenance contracts• Bundled transactions

25

Current Status• Twenty two states currently claim to impose tax on digital goods• Twenty-two states currently claim to impose tax on digital goods,

including canned software, regardless of means of transmission.• Thirty-four states currently claim to impose tax on downloads of

canned softwarecanned software.• Fourteen states currently claim to impose tax on custom software

delivered via a tangible medium.O l th j i di ti (CT D C HI) l i t i t• Only three jurisdictions (CT, D.C., HI) claim to impose tax on downloads of custom software.

• Only four states directly address remotely hosted licensing (NY, MA, IN WA)IN, WA).

26

Current Status (Cont.)

• Nine states claim to impose tax on information services.

• However most of these states provide an exclusion for personalized• However, most of these states provide an exclusion for personalized information or for information used by businesses.

E i t t th t l i t i t t l h t d ft• Even in states that claim to impose tax on remotely hosted software, most have not specifically addressed sourcing issues (where does transfer of possession of software take place? At host server or where buyer accesses software via terminal?)buyer accesses software via terminal?).

27

SSUTA Definitions• Twenty-three states have enacted conforming SSUTA legislation.Twenty three states have enacted conforming SSUTA legislation.• “Pre-written software” is defined to mean software not designed and

developed to the specifications of a specific purchaser; subsequent sale of specifically-designed software to non-original user is no longerof specifically designed software to non original user is no longer custom.

• Pre-written software is included in definition of TPP.• Modifications of pre-written software do not change character of• Modifications of pre-written software do not change character of

software as pre-written ,but charges therefore may be excluded if separately stated.

• Member states may exempt software “delivered electronically” or by• Member states may exempt software delivered electronically or by “load and leave.”

28

SSUTA Definitions (Cont.)

• SSUTA definitions do not specifically address remotely hosted software, ASP or SAAS models.

• All sales are sourced based on destination, regardless of whether TPP, digital good or service (unless origin destination election made)

• Digital goods may not be included in the definition of tangible personal property.

• Computer software is excluded from the definition of “products transferred electronically.”

29

Problems Inherent In TaxingProblems Inherent In Taxing ASP/SAAS/Cloud Models

• No software is ever “transferred” to user; user accesses software remotely via Internet

• Software may be hosted on servers in a different state than where userSoftware may be hosted on servers in a different state than where user is situated.

• User can’t modify software (raises issue of whether user ever really has possession or control of software)has possession or control of software)

• User agreement may not even include license of software.• Who is using software: service provider or end user?

D b t f ?• Does substance govern over form?• If software is TPP, where does user first take possession?

30

TRUE OBJECT TEST TRENDS Joseph Schmidt, Grant Thornton

TRUE OBJECT TEST TRENDS AND DEVELOPMENTS

Bundled Transactions

• “Bundled transactions” refers to:

– The sale of taxable goods together with non-taxable elements (typically services or intangibles) in a single transaction

• Not separately priced• Taxable and non-taxable elements may be either commingled or

separately identifiable

– Problem: “Bundling” exposes otherwise non-taxable items to sales or use tax.

© Grant Thornton LLP. All rights reserved. 32

Examples

• Phones given as an inducement to sign up for cellular telephone service

• Maintenance included in the price of automobiles

© Grant Thornton LLP. All rights reserved. 33

What Makes True Object Test Unique, For Sales Tax Purposes

• Tension – Reality behind the underlying economics of the transaction vs. sales

tax unique default is the possibility of classifying the entire transaction as taxable or non-taxable, based on the “true object” test

• Involves an inquiry into:– Buyer’s intenty– Relative values of disparate elements– Ability to identify and separate elements

© Grant Thornton LLP. All rights reserved. 34

Variations Of The True Object Test

• Functional consequences:– Involves an inquiry into the relative values and asks whether the

“taxable” element of the transaction is inconsequential to what was purchased

• Economic consequences– Involves an inquiry into the relative values of the elements of the q y

transaction and considers the significance of the “taxable” portion

© Grant Thornton LLP. All rights reserved. 35

Common Problem Areas

• Warranty services• Installation and/or maintenance agreements• Delivery and transportation servicesy p• Property “leased” in a manner that qualifies as services• “Off the shelf” software vs. customized software• Separately stated charges• Separately stated charges

© Grant Thornton LLP. All rights reserved. 36

Recent Developments

– Utah• Various regulations (effective Sept. 23, 2010)

– The entire purchase in a bundled transaction is subject to tax, unless the seller separately states the exempt items on the invoice or is able to identify the items exempt from sales tax.

– When a purchase contains items taxed at different rates, the entire purchase is subject to the higher rate, unless the seller separately states the items subject to different rates or is able to identify the items subject to the lower rate.

© Grant Thornton LLP. All rights reserved. 37

Recent Developments (Cont.)

– New Jersey• Notice to cable television service providers (Sept. 3, 2010)

– Bundled cable service providers are required to collect sales tax on equipment used at the customer’s location.

» Examples of such equipment are converters, remote controls, adapters and modems.

– The tax is based on the consideration for the equipment, as q preflected in the provider’s books and records when bundled with non-taxable cable television service.

© Grant Thornton LLP. All rights reserved. 38

Recent Developments (Cont.)

– Massachusetts• Letter Ruling 09-2 (March 23, 2009)

– When cell phones are sold in a bundled transaction with pcommunications services, sales tax is based on “fair retail selling price.”

© Grant Thornton LLP. All rights reserved. 39

Recent Developments (Cont.)

– Missouri• Letter Ruling LR4593 (Feb. 27, 2008)

– Service of converting customer’s VHS tapes onto DVD is g psubject to sales tax

– Concluded that true object of transaction is to obtain DVD

© Grant Thornton LLP. All rights reserved. 40

Recent Developments (Cont.)

– California• Dell Inc. v. Superior Court (Jan. 31, 2008)

– Computers and service contracts bundled and not separately stated on invoice

– Court held that the two components could be separated and that service contract would not be subject to sales tax.

– Court reasoned that service contracts were separate objects p jof the transaction.

© Grant Thornton LLP. All rights reserved. 41

Forward-Looking Approach

• Things to consider– Viability of “un-bundling” the transaction on a go-forward basis

• More likely in commercial settings• Ideally separately transact between “persons” providing the

goods and those delivering services or intangibles– ExampleExample

• Bank purchases ATM installed • Work with operations to remap the ATM purchase and

installation process by:installation process by:– Procuring uninstalled ATM by transacting with bank

management services affiliateBank operating company entering into an installation and

© Grant Thornton LLP. All rights reserved. 42

– Bank operating company entering into an installation and maintenance agreement

ACTIONS BY SPECIFIC STATESMatthew Schaefer, Brann & Isaacson

ACTIONS BY SPECIFIC STATES

Trends In State Sales/Use TaxTreatment Of Services

Traditionally, services have not been broadly subject to transaction taxes, with certain exceptions; but, many states are seeking to expand the range of taxable servicesthe range of taxable services.

• What states impose transaction taxes on many services?• What are some types of services that are more commonly taxed ?• Is there a trend toward increased taxation of services?• Are there particular developments during 2010 that may affect a

number of companies?

44

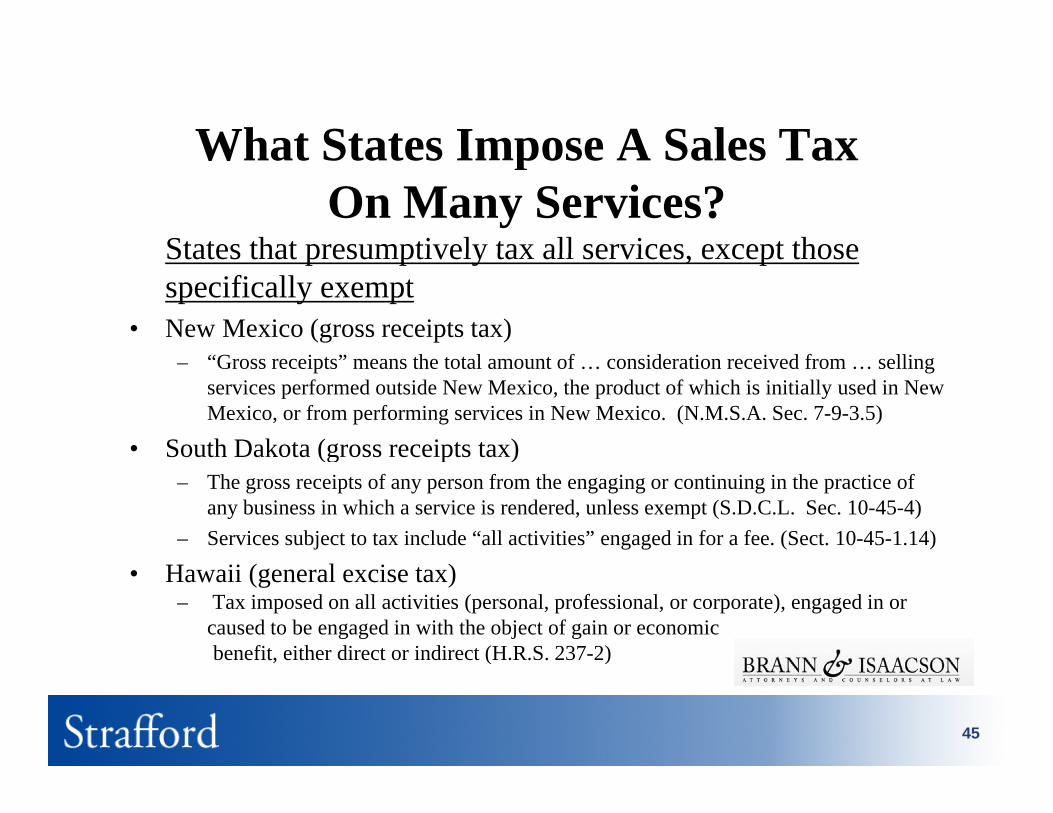

What States Impose A Sales TaxWhat States Impose A Sales Tax On Many Services?

States that presumptively tax all services except thoseStates that presumptively tax all services, except those specifically exempt

• New Mexico (gross receipts tax)“G i ” h l f id i i d f lli– “Gross receipts” means the total amount of … consideration received from … selling services performed outside New Mexico, the product of which is initially used in New Mexico, or from performing services in New Mexico. (N.M.S.A. Sec. 7-9-3.5)

• South Dakota (gross receipts tax)(g p )– The gross receipts of any person from the engaging or continuing in the practice of

any business in which a service is rendered, unless exempt (S.D.C.L. Sec. 10-45-4)– Services subject to tax include “all activities” engaged in for a fee. (Sect. 10-45-1.14)

• Hawaii (general excise tax)– Tax imposed on all activities (personal, professional, or corporate), engaged in or

caused to be engaged in with the object of gain or economicbenefit, either direct or indirect (H.R.S. 237-2), ( )

45

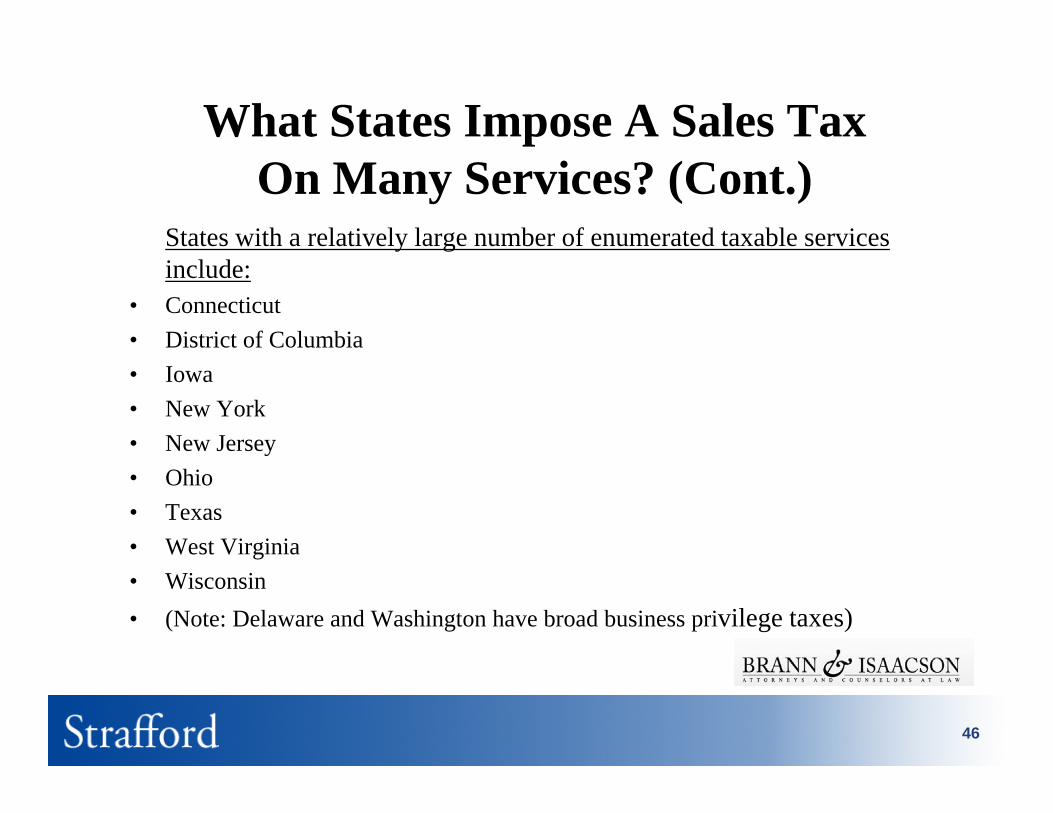

What States Impose A Sales Tax On Many Services? (Cont.)

States with a relatively large number of enumerated taxable services include:

• Connecticut • District of Columbia• Iowa • New York • New Jersey • Ohio• Texas• West Virginia• Wisconsin• (Note: Delaware and Washington have broad business privilege taxes)

46

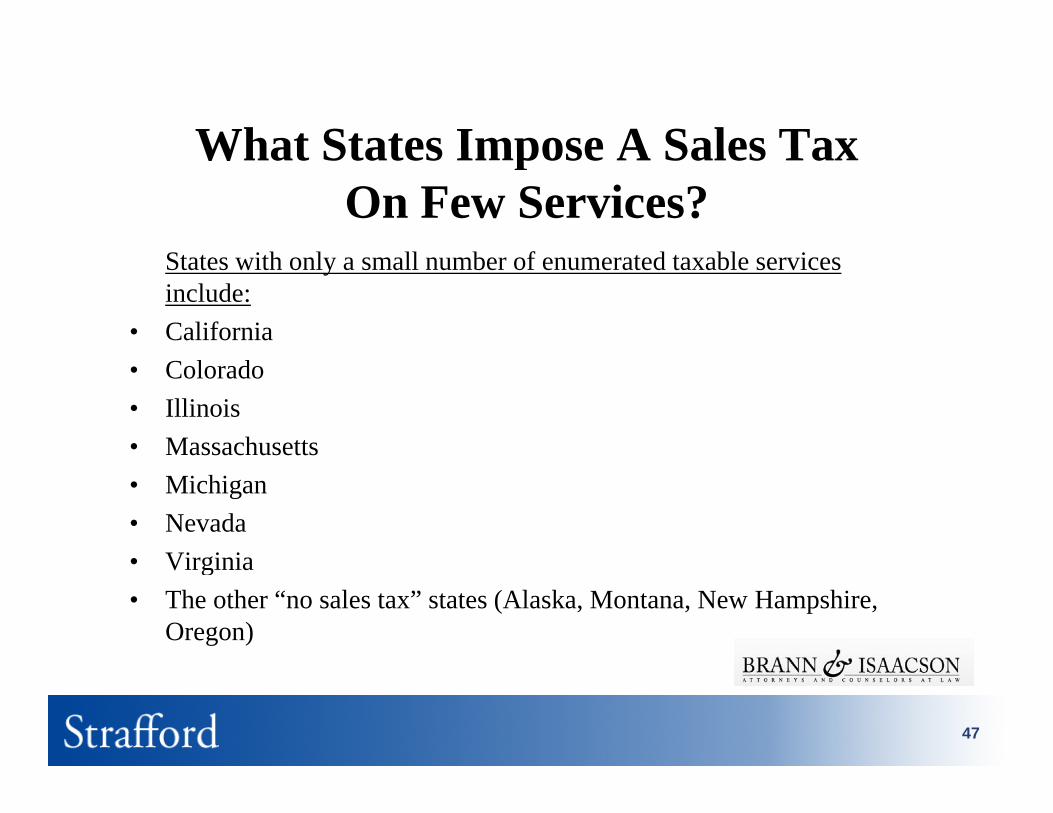

What States Impose A Sales TaxWhat States Impose A Sales Tax On Few Services?

S i h l ll b f d bl iStates with only a small number of enumerated taxable services include:

• California• Colorado• Illinois• Massachusetts• Michigan• Nevada• Virginia• Virginia• The other “no sales tax” states (Alaska, Montana, New Hampshire,

Oregon)

47

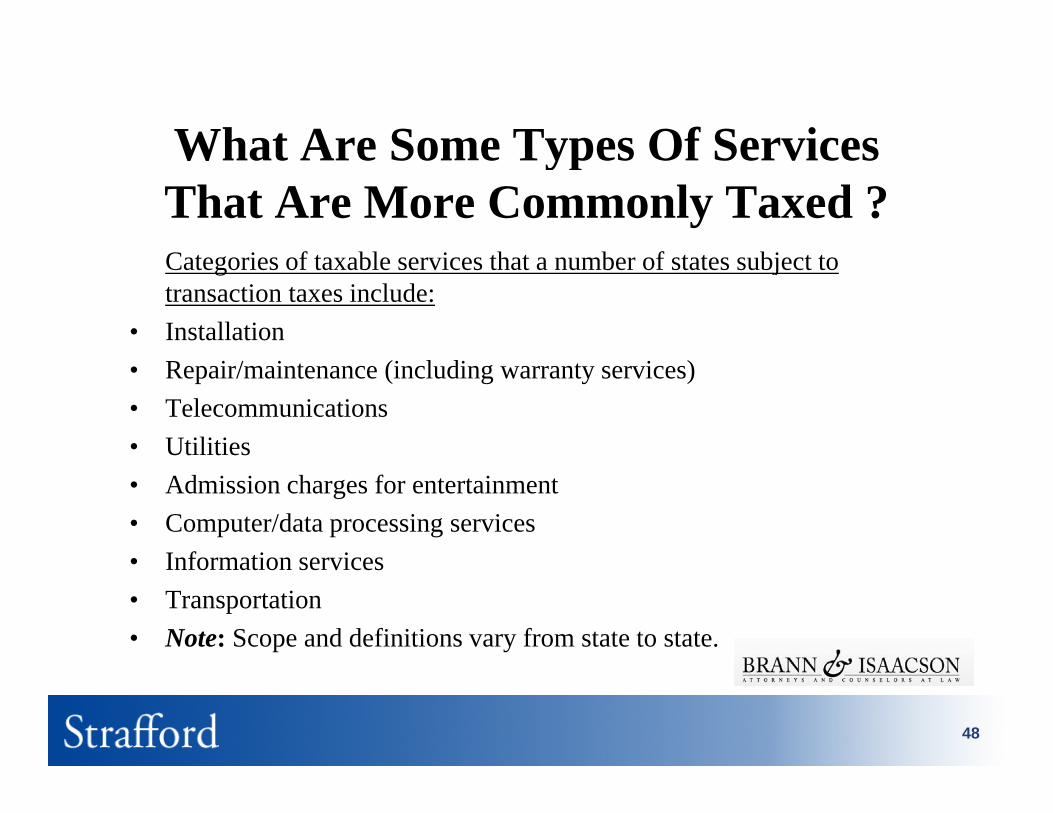

What Are Some Types Of ServicesWhat Are Some Types Of Services That Are More Commonly Taxed ?C i f bl i h b f bjCategories of taxable services that a number of states subject to transaction taxes include:

• Installation• Repair/maintenance (including warranty services)• Telecommunications• Utilities• Admission charges for entertainment• Computer/data processing services• Information services• Information services• Transportation• Note: Scope and definitions vary from state to state.

48

What Are Some Types of Services ThatWhat Are Some Types of Services That Are More Commonly Taxed? (Cont.)

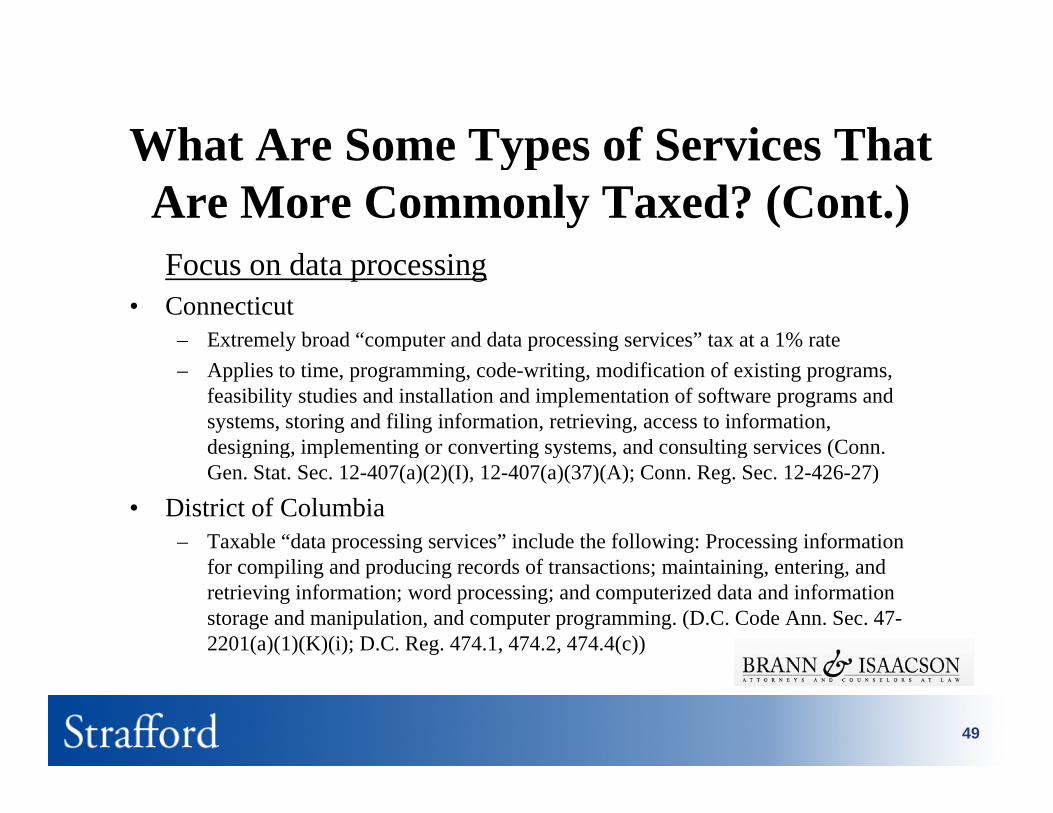

d iFocus on data processing • Connecticut

– Extremely broad “computer and data processing services” tax at a 1% rate– Applies to time, programming, code-writing, modification of existing programs,

feasibility studies and installation and implementation of software programs and systems, storing and filing information, retrieving, access to information, designing, implementing or converting systems, and consulting services (Conn. g g p g g y g (Gen. Stat. Sec. 12-407(a)(2)(I), 12-407(a)(37)(A); Conn. Reg. Sec. 12-426-27)

• District of Columbia– Taxable “data processing services” include the following: Processing information

f ili d d i d f i i i i i dfor compiling and producing records of transactions; maintaining, entering, and retrieving information; word processing; and computerized data and information storage and manipulation, and computer programming. (D.C. Code Ann. Sec. 47-2201(a)(1)(K)(i); D.C. Reg. 474.1, 474.2, 474.4(c))

49

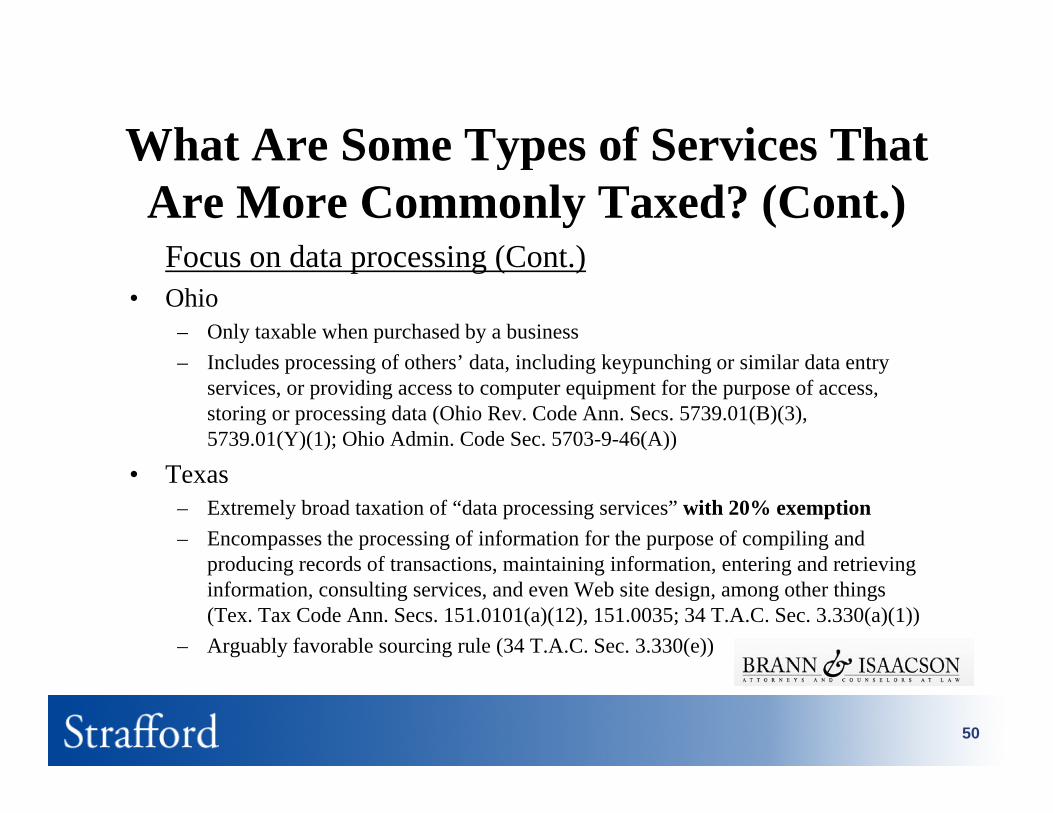

What Are Some Types of Services ThatWhat Are Some Types of Services That Are More Commonly Taxed? (Cont.)

Focus on data processing (Cont )Focus on data processing (Cont.) • Ohio

– Only taxable when purchased by a businessI l d i f h ’ d i l di k hi i il d– Includes processing of others’ data, including keypunching or similar data entry services, or providing access to computer equipment for the purpose of access, storing or processing data (Ohio Rev. Code Ann. Secs. 5739.01(B)(3), 5739.01(Y)(1); Ohio Admin. Code Sec. 5703-9-46(A))

• Texas– Extremely broad taxation of “data processing services” with 20% exemption– Encompasses the processing of information for the purpose of compiling and

d i d f t ti i t i i i f ti t i d t i iproducing records of transactions, maintaining information, entering and retrieving information, consulting services, and even Web site design, among other things (Tex. Tax Code Ann. Secs. 151.0101(a)(12), 151.0035; 34 T.A.C. Sec. 3.330(a)(1))

– Arguably favorable sourcing rule (34 T.A.C. Sec. 3.330(e))

50

What Are Some Types of Services ThatWhat Are Some Types of Services That Are More Commonly Taxed? (Cont.)

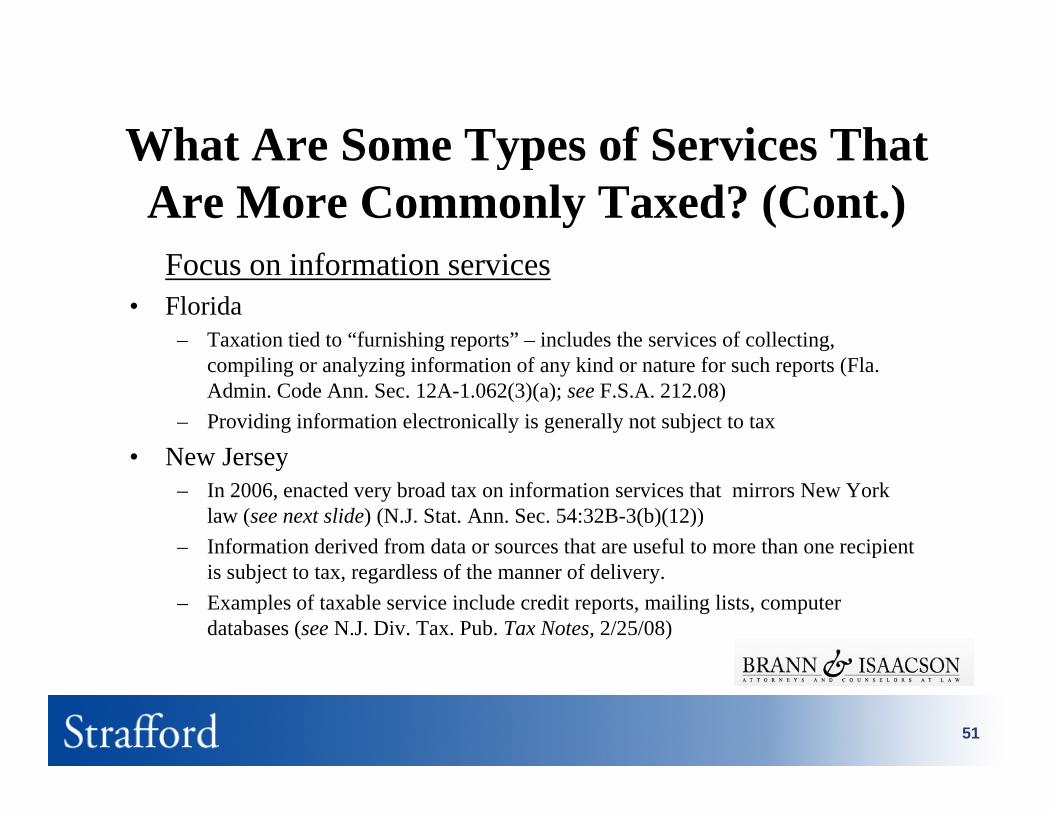

i f i iFocus on information services • Florida

– Taxation tied to “furnishing reports” – includes the services of collecting, compiling or analyzing information of any kind or nature for such reports (Fla. Admin. Code Ann. Sec. 12A-1.062(3)(a); see F.S.A. 212.08)

– Providing information electronically is generally not subject to tax

• New Jersey• New Jersey– In 2006, enacted very broad tax on information services that mirrors New York

law (see next slide) (N.J. Stat. Ann. Sec. 54:32B-3(b)(12))– Information derived from data or sources that are useful to more than one recipient

is subject to tax, regardless of the manner of delivery.– Examples of taxable service include credit reports, mailing lists, computer

databases (see N.J. Div. Tax. Pub. Tax Notes, 2/25/08)

51

What Are Some Types of Services ThatWhat Are Some Types of Services That Are More Commonly Taxed? (Cont.)

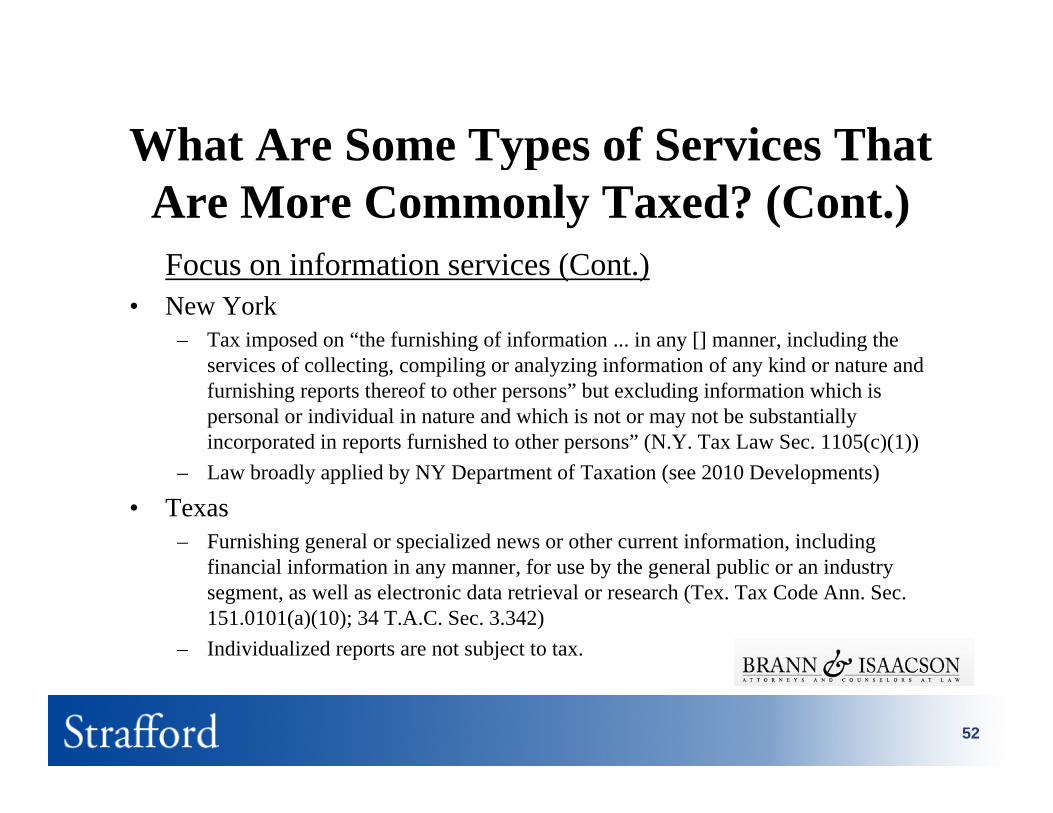

i f i i ( )Focus on information services (Cont.) • New York

– Tax imposed on “the furnishing of information ... in any [] manner, including the services of collecting, compiling or analyzing information of any kind or nature and furnishing reports thereof to other persons” but excluding information which is personal or individual in nature and which is not or may not be substantially incorporated in reports furnished to other persons” (N.Y. Tax Law Sec. 1105(c)(1))

– Law broadly applied by NY Department of Taxation (see 2010 Developments)

• Texas– Furnishing general or specialized news or other current information, including

fi i l i f i i f b h l bli i dfinancial information in any manner, for use by the general public or an industry segment, as well as electronic data retrieval or research (Tex. Tax Code Ann. Sec. 151.0101(a)(10); 34 T.A.C. Sec. 3.342)

– Individualized reports are not subject to tax.

52

Is There A Trend Toward IncreasedIs There A Trend Toward Increased Taxation Of Services?

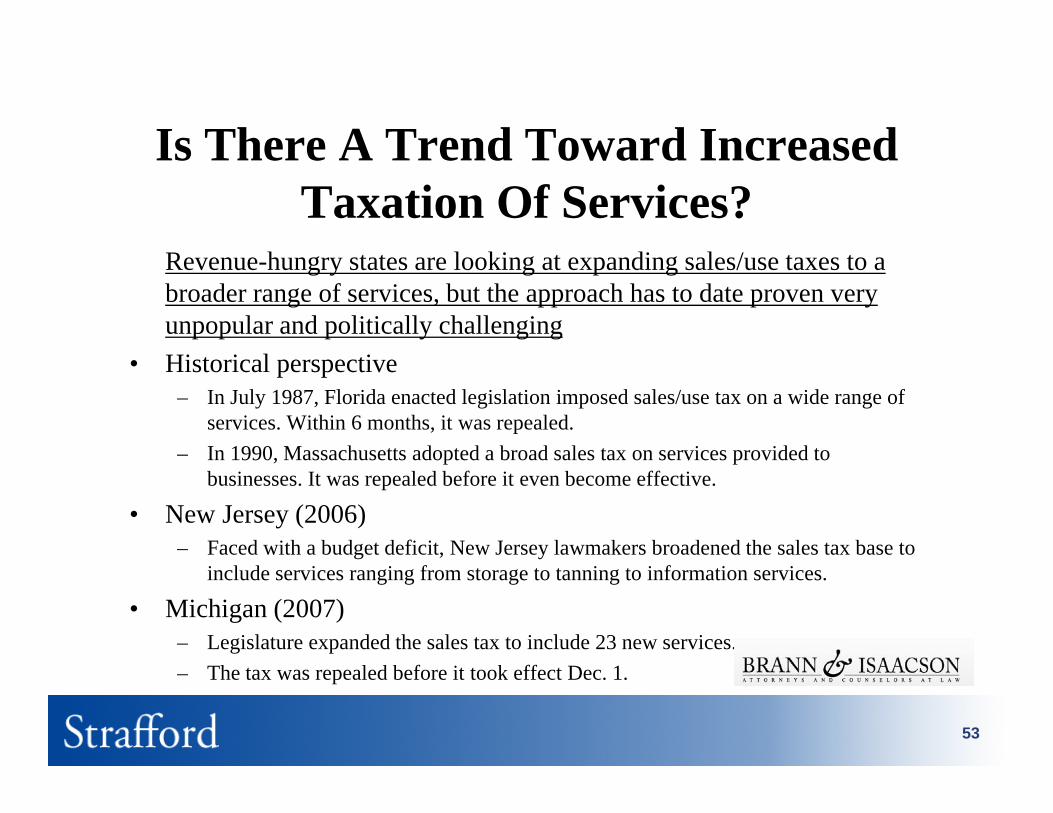

R h l ki di l /Revenue-hungry states are looking at expanding sales/use taxes to a broader range of services, but the approach has to date proven very unpopular and politically challenging Hi i l i• Historical perspective

– In July 1987, Florida enacted legislation imposed sales/use tax on a wide range of services. Within 6 months, it was repealed.

– In 1990, Massachusetts adopted a broad sales tax on services provided toIn 1990, Massachusetts adopted a broad sales tax on services provided to businesses. It was repealed before it even become effective.

• New Jersey (2006)– Faced with a budget deficit, New Jersey lawmakers broadened the sales tax base to

include services ranging from storage to tanning to information services.

• Michigan (2007)– Legislature expanded the sales tax to include 23 new services.– The tax was repealed before it took effect Dec. 1.

53

Is There A Trend Toward IncreasedIs There A Trend Toward Increased Taxation Of Services? (Cont.)

R h l ki di l /Revenue-hungry states are looking at expanding sales/use taxes to a broader range of services, but the approach has to date proven very unpopular and politically challenging (Cont.)M l d (2007)• Maryland (2007)

– Faced with a budget crisis, Maryland’s Legislature in a special session enacted a broad sales tax on computer services that included Web design, customer programming, facilities management, data center support, systems integration, p g g, g , pp , y g ,installation and maintenance, computer training and data entry.

– Maryland’s IT industry argued the law would hurt business, and the tax was repealed in 2008 before its July 1 effective date.

M i (2009)• Maine (2009)– Maine’s Legislature enacted a tax bill intended to restructure the tax base, reducing

the personal income tax rate and imposing sales tax on wide array of new services. – A citizens repeal initiative succeeded in June 2010. p

54

Is There A Trend Toward IncreasedIs There A Trend Toward Increased Taxation Of Services? (Cont.)

Revenue hungry states are looking at expanding sales/use taxes to aRevenue-hungry states are looking at expanding sales/use taxes to a broader range of services, but the approach has to date proven very unpopular and politically challenging (Cont.)

• Michigan (2010)• Michigan (2010)– Governor Granholm proposed expanding the sales tax to services, but later conceded

it would not be adopted.

• Pennsylvania (2010)Pennsylvania (2010)– Governor Rendell proposed a budget that would expand the sales tax to cover data

processing and professional services, but was forced to abandon the plan.

• District of Columbia (2010)– A proposal that the District Council consider taxing a wide range of new services was

met with widespread opposition from citizens.

• California (2010)– Proposals and study of expanding the sales tax to services

55

2010 Developments That May Affect A2010 Developments That May Affect A Number of Companies

N Y k i f i i b b dl li dNew York information services tax to be even more broadly applied; Department makes clear it covers the compiling of information from public sources I J l 2010 h N Y k D f T i d Fi i d• In July 2010, the New York Department of Taxation and Finance issued a “clarification” of its “existing interpretation” concerning the application of New York’s sales and use tax on “information services” to cover reports derived from publicly-available documents. (See TSB-M-10(7)S, July 19, 2010)

• The Department asserts it previously articulated its policy that “the sale of public documents by private entities” does, indeed, constitute the sale of a taxable information service, but acknowledged that it had advised certain companies to the contrary.

• Based on this express mea culpa from the Department, the Department has determined p p p , pthat it “will not assess any sales tax due that was not collected, or any related penalty and interest, for sales of public documents made during” tax periods prior to Sept. 1, 2010, but companies must now collect and remit the tax.

• Could constitute a complete reversal for some companiesCould constitute a complete reversal for some companies

56

2010 Developments That May Affect A2010 Developments That May Affect A Number of Companies (Cont.)

A d h W hi S b i d i (b& )Amendments to the Washington State business and occupation (b&o) tax may subject more non-Washington companies to the tax

• Washington’s b&o tax broadly applies to receipts from the sale of iservices.

• The Washington Legislature in 2010 enacted an amendment to the law eliminating the physical presence requirements and instead adopting an “ i ” d d“economic nexus” standard.

• However, the new economic nexus standard applies only to companies with “apportionable activities,” defined to include royalties and

f i l i d th iprofessional services and other services. • Companies which in the past may not have been subject to the B&O

tax should re-examine their position.• A ballot initiative seeks to repeal parts of the law.

57

Trends In State Sales Tax TreatmentTrends In State Sales Tax Treatment Of Services: Takeaways

F i bj i h j i f• For now, most services are not subject to tax in the majority of states.• Companies should be aware of those states that tax nearly all, or many

services.• Companies that sell, or purchase, particular types of services should

understand where such services are taxable, where they are being performed, etc.

• There is considerable pressure on state budgets, causing lawmakers to consider expanding the sales tax bases to cover more services. But, there is also considerable opposition to such efforts from industry and th blithe public.

• Consult your attorneys and/or tax advisors regarding your particular state tax issues.

58

CONTRACTOR ISSUESPeter Stathopoulos, Bennett Thrasher

CONTRACTOR ISSUES

Issues Associated WithIssues Associated With Taxing Contractors

• Most states do not directly impose tax on construction contractor services.

• Rather, contractor may be deemed to be the end user of all materialsRather, contractor may be deemed to be the end user of all materials incorporated into realty.

• However, many such states distinguish between lump-sum contracts and time-and-materials contracts.and time and materials contracts.

• Such states may deem the contractor to be the end user of materials used in lump-sum contracts, but to be a retailer with regard to materials separately stated in separated contracts.sepa a e y s a ed sepa a ed co ac s.

60

Dual Operator Issues

• If contractor is a dual operator, contractor must self-assess sales/use tax on materials withdrawn from inventory at the retail sales price of such materials (vs. cost of materials).

• For self-manufactured products, the tax on withdrawals from inventory is on the manufactured retail price, not on the cost of the raw materials.is on the manufactured retail price, not on the cost of the raw materials.

• May be difficult to define a dual operator

• Dual operator may be required to track purchases for resale vs. own use

61

Who Used The Materials?

• Contractor may be deemed to be end user of materials, even when materials are purchased by customer and provided to the contractor

• Contractor may be deemed to be the purchasing agent for the end user (and therefore not subject to sales tax on materials).

• Purchasing agent arrangement most commonly attempted where customer is exempt organization

• Retail sales of materials to an exempt organization are exempt from sales/use tax.

62

Leasing Of Equipment By Contractors

• Complications may arise when a contractor also engages in retail leasing activities and then withdraws leased materials from inventoryleasing activities and then withdraws leased materials from inventory for use by the contractor.

• For leased equipment that comes with operators there is an issue as to• For leased equipment that comes with operators, there is an issue as to whether the labor charges for operations personnel are taxable as part of the lease.

63

When Is Contractor A Contractor?

• In a situation where a contractor is a member of a consortium, contractor may really only be supplying materials.contractor may really only be supplying materials.

• Issue of whether materials supplied to general contractor or customer under consortium agreementunder consortium agreement

• Contractor may nonetheless be required to participate in sales taxes d ti tunder a consortium agreement.

64

Contracting Vs Real Estate RepairContracting Vs. Real Estate Repair And Maintenance Services

• Some states distinguish between real estate repair and maintenance services vs. contracting.services vs. contracting.

• Such states usually distinguish between repairs/maintenance and major improvement or modifications.

• May be difficult to distinguish between repair and major alteration of• May be difficult to distinguish between repair and major alteration of modification

• One test involves whether useful life of property is prolonged,S l f i l f t ( b i k hi )• Scale of repair also a factor (e.g., brick vs. new chimney)

65

Taxation Of Contracting Services

• Some states directly tax contracting services• Some states directly tax contracting services

• In such instances, purchase of materials by contractor is usually texempt

66

RELEVANT SSTP Matthew Schaefer, Brann & Isaacson

RELEVANT SSTP DEVELOPMENTS

Treatment Of Services Under The Streamlined Sales And Use Tax Agreement

(SSUTA)Services are not a primary focus of the SSUTA, but the relevant provisions apply in 20-plus member states, so sellers and buyers should be aware of itshould be aware of it

• What is the Streamlined Sales and Use Tax Agreement?• Which states are members of the SSUTA?• What services are specifically addressed under the SSUTA?• How does the SSUTA affect the sale of services?ff f

68

What Is The SSUTA?An agreement adopted by a group of states that prescribes a g p y g p pmodel set of requirements that are intended to simplify state sales and use tax provisions and administration

• In order to join the SSUTA, a state must conform its laws to the provisions of j , pthe Agreement, creating a degree of uniformity among the member states’ sales and use tax systems/

• Member states, however, are NOT required to have a uniform tax base; i.e., goods and services subject to tax may differ from state to state.

• Member states agree to provide amnesty for uncollected sales tax to sellers that register under the Agreement within 12 months of a state’s initial membership (amnesty period has long since expired for many member states)membership (amnesty period has long since expired for many member states).

• Participating seller agrees to collect and remit sales tax on sales sourced to each full-member state, irrespective of whether the seller has nexus.

69

What States Are SSUTA Members?

ll bFull-member states• Arkansas, Indiana, Iowa, Kansas, Kentucky, Michigan, Minnesota, Nebraska,

Nevada, New Jersey, North Carolina, North Dakota, Oklahoma, Rhode Island, South Dakota Vermont Washington West Virginia Wisconsin WyomingSouth Dakota, Vermont, Washington, West Virginia, Wisconsin, Wyoming

• States whose laws purport to be in full conformity with the Agreement

Associate member states• Ohio, Tennessee and Utah• Associate member states have not fully conformed their laws to the Agreement

and do not have the same privileges as full members; participating sellers may, b t t i d t ll t b t t ’ l tbut are not required to, collect member states’ sales tax.

Petition For full membership pending• Georgia

70

What Services Are SpecificallyWhat Services Are Specifically Addressed Under The SSUTA?

V f Th A d fi l i fVery few – The Agreement defines only a variety of telecommunications services, leaving states free to tax

• Perhaps because telecommunications services are widely taxed, the l i i i d h b i l i l d i htelecommunications industry has been very actively involved in the

development of the Agreement, resulting in specific sourcing provisions (see Sect. 314) and extensive definitions (see Sec. 315 and App C Library of Definitions)App. C, Library of Definitions).

• The absence of other, specifically defined services does not mean that SSUTA member states do not tax services. Rather, it means that member states are not required to conform their laws to a uniformmember states are not required to conform their laws to a uniform definitions for services and are free to impose transaction taxes on any service, however the state legislature may define it.

71

How Then Does The SSUTA AffectHow, Then, Does The SSUTA Affect The Sale Of Services?

Th A h f h d il d i l h lThe Agreement, however, sets forth detailed sourcing rules that apply to sales of services

• Sect. 309 of the SSUTA requires member states to source nearly all i ( i i l d l d fl i i ) diservices (exceptions include telecom and florist services) according to

the following hierarchy:– Where the service is received, if at a business location of the seller

Where the service is received as indicated by instructions from the purchaser– Where the service is received, as indicated by instructions from the purchaser– At an address for the purchaser on file with the seller– Any other address obtained at time of purchase, including billing address– Location from which tangible personal property was sent g p p p y

• The terms “receive” and “receipt” mean making first use of a service (see Sect. 311(B))

• Dropped former rule on “multiple points of use”Dropped former rule on multiple points of use

72

How Then Does The SSUTA AffectHow, Then, Does The SSUTA Affect The Sale Of Services? (Cont.)

Th A i ifi f i “b dl dThe Agreement requires specific treatment for certain “bundled transactions” that combine tangible personal property and services

• “Bundled transaction” is defined as the sale of two or more products that “di i d id ifi bl ” d “ ld f i i d i ”are “distinct and identifiable” and “sold for one non-itemized price.”

• Definition excludes combined sales involving services where a service the “true object” of the transaction

• Under the Agreement, member states are free to adopt their own treatment of bundled transactions, with the exception of certain restrictions set forth in the Agreement (see Sect. 330)

– Optional software maintenance contracts addressed– Where taxable portion of a bundled contract is de minimis (under 10%) the

transaction is not taxable.

73

How Then Does The SSUTA AffectHow, Then, Does The SSUTA Affect The Sale Of Services? (Cont.)

I i i f i i SSUTA i i b hIt is important for companies to monitor SSUTA activity, because the SSUTA is continually reviewing issues that may change the laws affecting companies in more than 20 states

• SSUTA has multiple working groups and other committees studying various issues, including certain services issues (specific services,

i )sourcing).• SSUTA is a major proponent of federal legislation – including a bill in

the 2010 congressional session – to allow the imposition of its standards ll i t l th l t il ti i ti i thon all companies, not merely those voluntarily participating in the

SSUTA.

74