multi-state military quick reference

TRANSCRIPT

MULTI-STATE MILITARY QUICK REFERENCE

Survey of State Military Tax Breaks & Filing Rules

FEBRUARY 15, 2021 © H&R BLOCK, INC.

Confidential & Proprietary Work Product

Multi-State Military Quick Reference

© H&R Block, Inc. 1 | P a g e

Table of Contents Servicemembers’ Civil Relief Act (SCRA) ....................................................................................................... 3

Military Spouses Residency Relief Act (MSRRA) ........................................................................................... 5

SCRA / MSRRA Tax Protections Chart ........................................................................................................... 6

Home of Record v. State of Legal Residence (DD2058) ................................................................................ 7

Community Property States/U.S. Possessions .............................................................................................. 8

States with the Most Military Personnel or Bases ........................................................................................ 9

States with the Largest Military Bases .......................................................................................................... 9

Federal Extension Rules ................................................................................................................................ 9

Alabama ...................................................................................................................................................... 10

Arkansas ...................................................................................................................................................... 11

Arizona ........................................................................................................................................................ 13

California ..................................................................................................................................................... 15

Colorado ...................................................................................................................................................... 18

Connecticut ................................................................................................................................................. 20

District of Columbia .................................................................................................................................... 23

Delaware ..................................................................................................................................................... 24

Georgia ........................................................................................................................................................ 25

Hawaii ......................................................................................................................................................... 27

Iowa ............................................................................................................................................................. 29

Idaho ........................................................................................................................................................... 31

Illinois .......................................................................................................................................................... 33

Indiana ........................................................................................................................................................ 35

Kansas ......................................................................................................................................................... 37

Kentucky ...................................................................................................................................................... 39

Louisiana ..................................................................................................................................................... 41

Maine .......................................................................................................................................................... 43

Massachusetts ............................................................................................................................................ 46

Michigan ...................................................................................................................................................... 50

Minnesota ................................................................................................................................................... 52

Missouri ...................................................................................................................................................... 55

Mississippi ................................................................................................................................................... 57

Montana ...................................................................................................................................................... 58

Multi-State Military Quick Reference

© H&R Block, Inc. 2 | P a g e

Nebraska ..................................................................................................................................................... 60

New Hampshire........................................................................................................................................... 62

New Jersey .................................................................................................................................................. 63

New Mexico ................................................................................................................................................ 65

New York ..................................................................................................................................................... 67

North Carolina ............................................................................................................................................. 70

North Dakota............................................................................................................................................... 72

Ohio ............................................................................................................................................................. 74

Oklahoma .................................................................................................................................................... 76

Oregon ........................................................................................................................................................ 78

Pennsylvania ............................................................................................................................................... 81

Rhode Island................................................................................................................................................ 83

South Carolina ............................................................................................................................................. 85

Tennessee ................................................................................................................................................... 87

Utah ............................................................................................................................................................. 88

Vermont ...................................................................................................................................................... 90

Virginia ........................................................................................................................................................ 92

West Virginia ............................................................................................................................................... 94

Wisconsin .................................................................................................................................................... 96

Appendix ..................................................................................................................................................... 99

Note that the following states have no individual state income tax and are intentionally excluded from this document:

• Alaska • Florida • Nevada • South Dakota • Texas • Washington • Wyoming

Multi-State Military Quick Reference

© H&R Block, Inc. 3 | P a g e

Servicemembers’ Civil Relief Act (SCRA)

On December 19, 2003, President Bush signed the Servicemembers Civil Relief Act (SCRA)1 to help ease the economic and legal burdens on military personnel called to active duty status in Operation Iraqi Freedom. The Act expands many of the previous law’s civil protections under the Soldiers & Sailors Civil Relief Act of 1940 and covers all active duty service members, reservists, and members of the National Guard while on active duty.

The protection begins on the date of entering active duty and generally terminates within 30 to 90 days after the date of discharge from active duty. Jurisdiction of the Act reaches the United States, all states therein including political subdivisions, and all territory subject to the jurisdiction of the United States.

Provisions under § 4001 of the Act address income tax and residency issues for tax purposes. Considered together, the provisions of § 4001 outlined below are meant to preclude the possibility that service members will have their income taxed by both their home state and by the state where they are stationed.

50 U.S.C. § 4001(a) - RESIDENCE OR DOMICILE- A servicemember shall neither lose nor acquire a residence or domicile for purposes of taxation with respect to the person, personal property, or income of the servicemember by reason of being absent or present in any tax jurisdiction of the United States solely in compliance with military orders. 50 U.S.C. § 4001(b) - MILITARY SERVICE COMPENSATION- Compensation of a servicemember for military service shall not be deemed to be income for services performed or from sources within a tax jurisdiction of the United States if the servicemember is not a resident or domiciliary of the jurisdiction in which the servicemember is serving in compliance with military orders. 50 U.S.C. § 4001(e) - INCREASE OF TAX LIABILITY- A tax jurisdiction may not use the military compensation of a nonresident servicemember to increase the tax liability imposed on other income earned by the nonresident servicemember or spouse subject to tax by the jurisdiction.

Federal law states that the service member “neither loses nor acquires a residence or domicile” for tax purposes by reason of his military orders and station; the service member’s residency will remain the same as when he entered the military unless he takes proactive and intentional steps to change it.

Often, a change in domicile occurs when the service member files the necessary paperwork with the military, local, or municipal government office to establish a new state of legal residence. Absent these proactive steps, the service member remains domiciled in his state of residence when he entered military service and his active duty military pay does not become subject to tax in the active duty state. The service member will continue to file a resident state income tax return in his home state and his active duty military income is subject to tax on the home state tax return as dictated by that state’s laws.

1 50 U.S.C. § 4001, Pub. L. No. 108–189 (2003)

Multi-State Military Quick Reference

© H&R Block, Inc. 4 | P a g e

If a servicemember is in another state due to military assignment or orders, he generally does not have to file a nonresident return in that state unless he earns income in the nonresident state from non-military sources, such as from a second job. The service member will be subject to tax in the nonresident state on any nonresident source income earned other than from active duty military sources. Thus, income from a second job in the nonresident state is taxable in the nonresident state because that is where it’s earned.

SCRA, however, introduces a change in how this other income is taxed in the nonresident state; the service member’s active duty military income cannot have the effect of increasing the tax liability assessed on the other non-military state income.

In most states, tax liability is calculated using a nonresident income allocation ratio. States typically calculate a nonresident ratio by dividing the nonresident source income by the total federal income as follows:

NR Ratio = Nonresident state sourced income Total federal income

Calculation of this ratio will be defined by each state and is often calculated directly on the nonresident state’s base form or a supplemental schedule based on the state’s accounting method. This ratio is used to prorate various state tax calculations for the nonresident taxpayer, such as additions, subtractions, personal exemptions, dependent exemptions, state tax credits, and most importantly, state tax liability.

To properly calculate the tax liability on the service member’s nonresident income and ensure the military income does not increase the nonresident tax liability, a practitioner must subtract the military wages from the nonresident state income amount (numerator) and sometimes from the federal income amount (denominator) of the equation. See the Tax Institute’s separate guide, State Nonresident Servicemember & Civilian Spouse Adjustments - SCRA/MSRRA, for specific details relating to these adjustments on each state’s nonresident income tax return.

Multi-State Military Quick Reference

© H&R Block, Inc. 5 | P a g e

Military Spouses Residency Relief Act (MSRRA)

The Military Spouses Residency Relief Act of 2009 (MSRRA)2 amends SCRA to offer the same residency retention protections to a servicemember’s spouse who leaves his or her home state to accompany his or her spouse on military orders as SCRA offers to servicemembers. Additionally, a servicemember’s nonmilitary spouse may elect to use the servicemember’s home state for tax purposes even if the two did not previously share the same residence or domicile prior to a military move3.

MSRRA thus modifies some basic rules of taxation with respect to military spouses when:

• The spouse earns income from services performed in a state where the spouse is present solely to be with the servicemember pursuant to military orders and

• The state is not the spouse’s legal domicile

Under these circumstances, and pursuant to 50 U.S.C. §§ 4001(a)(2) and (c), the civilian spouse will not be required to pay income taxes to the nonresident state on income earned for services rendered in the nonresident state. These two provisions create a legal fiction for the spouse: even though the spouse actually may earn income in the nonresident state, the spouse’s income will be taxed in the spouse’s home state. Individual state laws will govern the taxability of home state source income. Practitioners should note, however, that income from sources other than for personal services of the civilian spouse may remain taxable to the nonresident state according to the state’s rules of taxation as they apply to nonresidents.

Many states require nonmilitary spouses of military servicemembers to provide proof that they meet the criteria for state personal income tax exemptions as set forth in the MSRRA.

See the Tax Institute’s separate guide, State Nonresident Servicemember & Civilian Spouse Adjustments - SCRA/MSRRA, for specific details relating to military spouse adjustments on each state’s nonresident income tax return.

2 50 U.S.C. § 4001(a)(2), Pub. L. No. 111-97 (2009), amended by The Veterans Benefits and Transitions Act of 2018 (VBTA), Pub. L. No. 115-407 (Dec. 31, 2018) 3 Under MSRRA of 2009, a spouse who did not have the same domicile as the servicemember prior to moving to a new state on military orders was not afforded protection under the MSRRA. The Veterans Benefits and Transitions Act of 2018 (VBTA), Pub. L. No. 115-407 (Dec. 31, 2018), § 302(a)(2)(B) amends SCRA and MSRRA as it relates to the servicemember’s spouse by adding: “For any taxable year of the marriage, the spouse of a servicemember may elect to use the same residence for purposes of taxation as the servicemember regardless of the date on which the marriage of the spouse and the servicemember occurred.” This amendment removed the “same state” requirement under prior MSRRA.

Multi-State Military Quick Reference

© H&R Block, Inc. 6 | P a g e

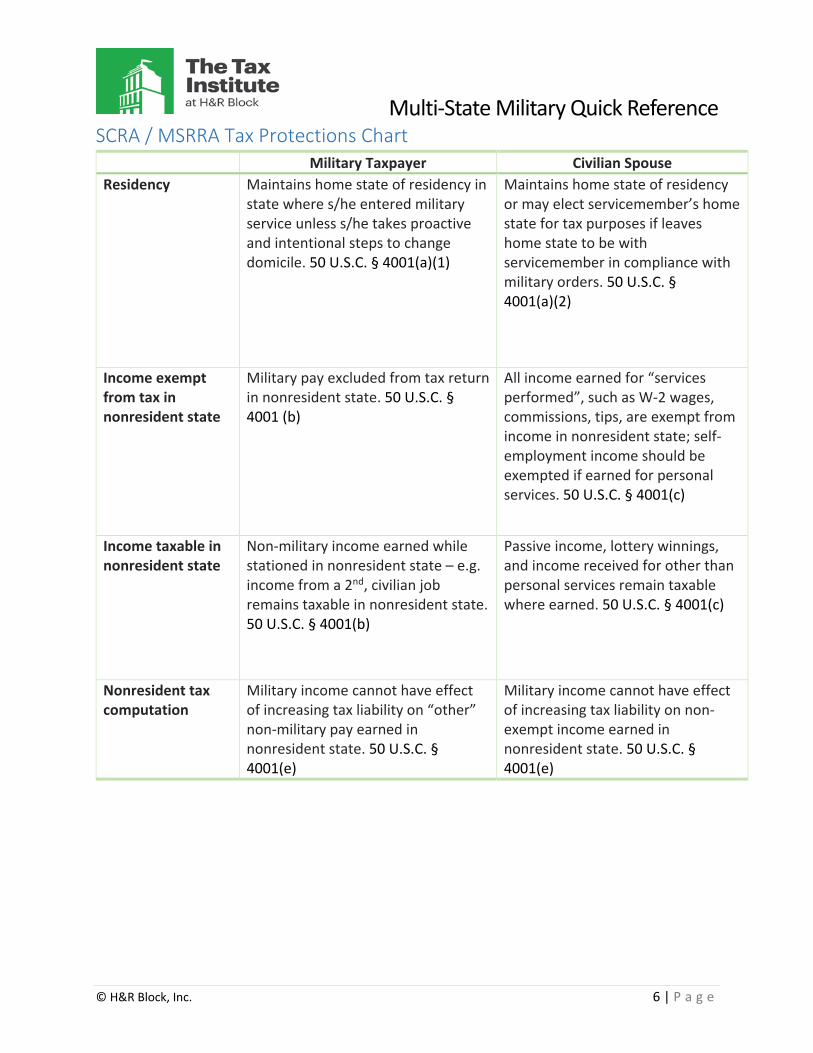

SCRA / MSRRA Tax Protections Chart Military Taxpayer Civilian Spouse Residency Maintains home state of residency in

state where s/he entered military service unless s/he takes proactive and intentional steps to change domicile. 50 U.S.C. § 4001(a)(1)

Maintains home state of residency or may elect servicemember’s home state for tax purposes if leaves home state to be with servicemember in compliance with military orders. 50 U.S.C. § 4001(a)(2)

Income exempt from tax in nonresident state

Military pay excluded from tax return in nonresident state. 50 U.S.C. § 4001 (b)

All income earned for “services performed”, such as W-2 wages, commissions, tips, are exempt from income in nonresident state; self-employment income should be exempted if earned for personal services. 50 U.S.C. § 4001(c)

Income taxable in nonresident state

Non-military income earned while stationed in nonresident state – e.g. income from a 2nd, civilian job remains taxable in nonresident state. 50 U.S.C. § 4001(b)

Passive income, lottery winnings, and income received for other than personal services remain taxable where earned. 50 U.S.C. § 4001(c)

Nonresident tax computation

Military income cannot have effect of increasing tax liability on “other” non-military pay earned in nonresident state. 50 U.S.C. § 4001(e)

Military income cannot have effect of increasing tax liability on non-exempt income earned in nonresident state. 50 U.S.C. § 4001(e)

Multi-State Military Quick Reference

© H&R Block, Inc. 7 | P a g e

Home of Record v. State of Legal Residence (DD2058) Preparing taxes for a military servicemember can present several unique challenges. Correctly ascertaining where the servicemember should file his or her taxes is paramount. The only way to determine if a civilian spouse is eligible for the protections of the MSRRA is to ascertain both the servicemember and the spouse’s correct state of legal residence.

The first question should always be: Where was your permanent duty station during the tax year – in what state?

The second question should always be: “Have you ever filled out a DD2058 and filed it with your payroll department? If so, what state did you list? If no DD2058 has ever been filed, then from what state did you join the military (home of record)?

The answer to the second question tells you the servicemember’s state of legal residence – the state in which they will be filing a resident tax return. The first question, if listing a different state, tells you in which state the servicemember may be required to file a nonresident tax return.

When completing the interview section in our digital/DIY software, the software uses the term “home of record” to designate a taxpayer’s residency rather than “state of legal residence”. The terms can become conflated and misunderstood.

Every tax professional needs to know the following:

The term “home of record” is defined as the state where the individual first enlisted or from where he/she received a commission from one of the branches of armed services. A servicemember’s home of record determines certain benefits, such as travel allowance back to a location when the servicemember is discharged from the military. This designation never changes and is NOT what determines where the servicemember pays taxes.

The term “state of legal residence” refers to a servicemember’s permanent home or domicile, (the state the servicemember considers his/her permanent residence and where they intend to live after being discharged from the military). The “state of legal residence” is considered by the military (“DFAS”) to be the servicemember’s residence for state income tax purposes. In addition, state of legal residence is used to determine qualification for in-state tuition rates, eligibility to vote for federal and state elections and for a will to be probated.

While a servicemember’s “state of legal residence” can be changed in the same manner as any individual can change their domicile, the home of record can only be changed to correct an error, or after a break in military service. Thus, for tax purposes, the term “state of legal residence” should be used rather than “home of record”.

Servicemembers can change their state of legal residence by use of a Form DD2058, State of Legal Residence Certificate.

Practice Tip: Ask the servicemember if s/he has a DD2058 on file and if so, what state it lists as the servicemember’s home of legal residence. This should be the starting point for determining the servicemember’s tax situation.

Multi-State Military Quick Reference

© H&R Block, Inc. 8 | P a g e

Community Property States/U.S. Possessions Married taxpayers domiciled in a community property state, U.S. possession, or foreign country are subject to community property rules. Community property laws affect how taxpayers calculate income for federal income tax purposes. Spouses who are domiciled in community property states and filing separate federal income tax returns must split community income, treating half as earned by each spouse, even if one spouse earns all the community income.

State community property laws apply to military retirement pay. Generally, the pay is either separate or community income based on the servicemember’s marital status and the couple’s domicile while the servicemember was in active military service. For example, the military retirement income that a servicemember receives for services performed during marriage and while the couple was domiciled in a community property state is community income. Active military pay earned while married and domiciled in a community property state is also community income. Under the federal tax rules for community income, the servicemember is treated as having received half of the income and the servicemember’s spouse is treated as receiving the other half.

Spouses who maintain separate residences due to temporary absences (such as an absence due to military service where the spouses intend to live together when the spouse in the military returns) are not considered to be living apart for purposes of determining whether the special treatment under IRC §66(a) and Reg. §1.66-2 for spouses living apart all year.

The following states and U.S. possessions follow community property rules:

Arizona Texas

California Washington

Louisiana Wisconsin

Idaho Guam

New Mexico Puerto Rico

Nevada Northern Mariana Islands

*Alaska has a community property “election”

See IRS Publication 555, Community Property

Multi-State Military Quick Reference

© H&R Block, Inc. 9 | P a g e

States with the Most Military Personnel or Bases • Alaska • California

• Colorado • Florida

• Maryland • New York

• Oklahoma • Virginia

• South Carolina

States with the Largest Military Bases • Georgia (Fort Benning) • Kentucky (Fort Campbell) • North Carolina (Fort Bragg) • Texas (Fort Hood) • Washington (Joint Base Lewis-McChord)

Federal Extension Rules Many states follow the federal military extension filing rules. Under federal rules, servicemembers who are serving in a combat zone (CZ), contingency operation, or who have been hospitalized because of such service, have at least 180 days after leaving the designated CZ, contingency operation, or hospital discharge to file and pay federal taxes. The IRS will not assess or charge interest and penalties attributable to the extension period.

• In collaboration with the Department of Defense, the IRS identifies taxpayers who are serving in a combat zone to suspend compliance action until 180 days after the taxpayer has left the CZ.

• Servicemembers qualifying for CZ relief may notify the IRS of their status via email at [email protected]. The e-mail should contain:

o Official document that indicates their area of military operation o If civilian, Letter of Authorization stating service in “tax-free zone” or “Combat Zone Tax

Exclusion Area” (CZTE) o Do not include SSN

• Deadline extension provisions apply to most tax actions required to be performed on or after the beginning date for the CZ, or the date service began, whichever is later.

• In general, the deadline is extended for the period of service in a CZ plus 180 days after the last day in a CZ.

• For hospitalizations, the 180-day extension period begins upon discharge. For hospitalization inside the U.S., the extension period cannot be more than 5 years.

Additional Resources IRS Publication 3, Armed Forces’ Tax Guide Extension of Deadlines – Combat Zone Service FAQ

Multi-State Military Quick Reference

© H&R Block, Inc. 10 | P a g e

Alabama Filing Status General rule: Taxpayers, including servicemembers may use a different status on the AL return than

used on the federal return. Married Split Residency: Use “married filing separate” if one spouse is a resident of AL and the

other is a resident of another state.

Extensions No special provisions

Resident Military AL taxes resident servicemembers on military compensation except for:

o military compensation received while serving in a combat zone. o active duty military allowances for quarters, substance, uniforms, and travel.

Servicemembers exclude dividends received on veteran’s life insurance from AL taxable income. AL exempts from tax any payment made by the U.S. Dept. of Defense for any servicemember killed

in action in a designated combat zone in the year s/he is declared deceased. The deceased service-member’s spouse may also claim the exemption for any income s/he earned in the same year.

Nonresident Military Under SCRA, a nonresident servicemember’s active duty military service pay is not taxable by AL. A

servicemember who earns only active duty military pay is not required to file an AL tax return. A nonresident servicemember who earns any non-military income in AL or from AL sources is

required to file AL Form 40NR.

Reservist/National Guard Reservists and National Guard members are not taxed on any military allowances received for

quarters, subsistence, uniforms, and travel.

Tax Credits No special provisions

Retirement AL exempts military retirement pay from AL income tax. Retired servicemembers should not include

this pay on Form 40, Part I lines 5a and 5b. AL exempts disability retirement payments (and other benefits) paid by the Veterans Administration

from AL income tax.

Special Filing Rules/Restrictions No special provisions

Additional Resources No additional resources

Multi-State Military Quick Reference

© H&R Block, Inc. 11 | P a g e

Arkansas

Filing Status General rule: Servicemembers may use a different status on the AR return than used on the federal

return.

Extensions If a servicemember’s ability to file and pay income tax is affected by military service and the

servicemember notifies the IRS or state authority, the servicemember may defer paying tax up to 180 days after the servicemember’s termination of military service.

o No interest of penalty shall accrue for the period of deferment. o Statute of Limitations – Collections by seizure or otherwise shall be suspended for the

period of military service of the servicemember and for an additional 270 days thereafter.

Resident Military AR resident servicemembers are exempt from AR tax on all service pay and allowances received

while on active duty. Servicemembers must file Form AR1000F and enter excludable income on line 9.

AR resident servicemembers claiming an exclusion for military compensation may not use the low-income tax tables.

Nonresident Military Under SCRA, a nonresident servicemember’s active duty military service pay is not taxable by AR. Nonresident servicemembers complete Form AR-NR MILITARY to indicate they are not required to

file AR return. Servicemembers complete and file the Form AR-NR MILITARY one time only to claim this permanent exemption.

A nonresident servicemember’s spouse who meets the requirements of MSRRA requirements is not subject to AR tax and may receive a refund of AR tax withheld by attaching a completed Form AR-MS, along with a copy of servicemember’s Leave and Earning Statement (LES), to Form AR1000NR with “Military Spouse” notated at the top of the return. Enter the total amount of AR withholding on AR1000NR but do not include the exempt income.

A MSRRA qualified spouse should submit a completed payroll withholding form, ARW-4MS to his or her employer yearly to prevent future AR tax withholding.

Reservist/National Guard Reservists and National Guard members are not subject to AR tax on service pay or allowance they

earn. Reservists and National Guard members must file Form AR1000F and enter the exempt income on line 9.

Reservists and National Guard members may deduct expenses, including overnight travel expenses, incurred from participating in the reserves on Form AR1000ADJ.

Multi-State Military Quick Reference

© H&R Block, Inc. 12 | P a g e

Tax Credits Servicemembers may not use the Low-Income Tax Tables if claiming an exclusion for military

compensation or retirement.

Retirement Servicemember military retirement income and survivor benefits are completely exempt from AR

income tax for tax years beginning January 1, 2018. Servicemembers enter the gross amount of military pension income on Form AR 1000F / AR1000NR line 17. Beginning with tax year 2018, servicemembers receiving this military pension exemption are disallowed the $6,000 maximum exemption allowed to AR taxpayers for retirement income.

Servicemembers may exempt from AR income tax a military disability pension that falls under IRC § 104(a)(4) if the pension was for personal injuries or sickness due to active service. Retired servicemembers may exempt military retirement pay from active service above and beyond the $6,000 cap to the extent it is based upon a military related disability. Servicemembers claiming an exclusion for military retirement may not use the Low-Income Tax Tables.

Special Filing Rules/Restrictions AR-MS Tax Exemption Certificate for Military Spouse AR applies the federal provision excluding gain from the sale of personal residence for purposes of

computing servicemembers’ AR taxable income.

Additional Resources Arkansas Military Spouses Residency Relief Act Information

Multi-State Military Quick Reference

© H&R Block, Inc. 13 | P a g e

Arizona

Filing Status General Rule: Servicemembers may use a different filling status on the AZ return than used on the

federal return. Caution, Community Property States: AZ requires servicemembers domiciled in AZ (or another

community property state filing separate returns) to report their own income taxable to AZ and half of community income taxable to AZ. AZ does not tax military income and servicemembers should not report this income as separate or community income.

Extensions AZ may waive any interest and penalties for late payment or extension underpayment penalty

assessed to a servicemember when the servicemember is outside the U.S. and it is impossible or impractical to file or pay AZ taxes. Servicemembers should submit a written request to the tax audit section of the AZ Department of Revenue explaining the circumstances and requesting a waiver of any interest or penalties. Servicemembers should make this request as soon as possible upon their return to the U.S.

Servicemembers file the return and request for a waiver of interest and penalties separately; but a copy of the request must be attached to the return.

Resident Military AZ does not tax a resident servicemember’s active duty military pay. An AZ resident servicemember and his or her resident spouse must file an AZ return if either spouse

has AZ income other than military pay. Servicemembers filing an AZ return report all income, including military pay, and subtract military pay to the extent it is included in federal AGI by using AZ Form 140, line 32. Full year resident servicemembers may not subtract active duty military pay on Forms 140A or 140EZ. Part year resident servicemembers may subtract active duty military pay on Form 140PY.

AZ resident servicemembers should not file an AZ return if the servicemember: o is an active duty member of armed forces; o earned income only for active duty military service; and o had no AZ tax withheld from active duty military pay.

Nonresident Military Nonresident servicemembers are not subject to AZ income tax on active military pay. A nonresident servicemember who earns non-military income from AZ sources reports such income

on AZ Form 140NR. A nonresident servicemember who is required to file Form 140NR should check box 12 on AZ Form 140NR to exclude active military wages on line 15, Form 140NR.

A nonresident servicemember’s civilian spouse who meets the MSRAA requirements should exclude his/her income in AZ income on Form 140NR line 15 by checking the box on line 14, if they are otherwise required to file an AZ income tax return.

Multi-State Military Quick Reference

© H&R Block, Inc. 14 | P a g e

A nonresident servicemember who is required to file an AZ income tax return must prorate dependency exemptions by the portion that represents the proration of AZ AGI to federal AGI. However, a nonresident servicemember is not required to prorate the personal exemption.

Reservist/National Guard Reservists and National Guard members should not file an AZ income tax return if the Reservist or

National Guard member: o is an active service Reservists or National Guard member; o earns income only from active service; and o had no AZ tax withheld from active Reserve/Guard pay.

Reservists or National Guard members required to file AZ Form 140 must include all income, including military pay, and subtract active service compensation on Form 140, line 32, to the extent such pay is included in federal AGI.

Active service compensation includes all pay received for services performed as a Reservist or National Guard members including weekend duty and two weeks a year active duty. However, compensation received by a “military technician (dual status)” for federal civil service employment for the National Guard or for the United States Reserves, is not income received for active service as a National Guard member for a Reserve member even though the employee may be required to wear a military uniform while at work. Additionally, a member of the U.S. Public Health Service or National Oceanic and Atmospheric Administration does not qualify as a servicemember earning active service compensation.

Retirement Servicemembers receiving U.S. government military pension can subtract the lessor of the amount

of the pension received or $3,500 using AZ Form 140, line 29b.

Credits No special provisions

Special Filing Rules/Restrictions No special provisions

Additional Resources AZ Pub 704, Taxpayers in the Military AZ Pub 705, Spouses of Active Duty Military Members

Multi-State Military Quick Reference

© H&R Block, Inc. 15 | P a g e

California Filing Status General Rule: Servicemembers use the same filing status for California as they use on the federal

income tax return. Nonresident Spouse Exception: A servicemember or auxiliary military branch member may file

separately for California if either spouse was: o An active duty member of U.S. armed forces or auxiliary military branch during tax year; or o A nonresident for the entire year who has no California source income.

Caution, Community Property States: If the spouse earning the California source income is domiciled in a community property state or territory, the spouses must equally split the community income. Consequently, both spouses will have California sourced income and they will not qualify for the nonresident spouse exception to filing status rules.

Extensions CA allows servicemembers an additional 180 days to file their state tax return and pay tax, without

interest or penalties, after they return from overseas in a noncombat assignment or after they return from a combat zone (CZ) or qualified hazardous duty area (QHDA): o Servicemembers who served in a CZ or QHDA can receive an additional extension (up to 106 days)

for the number of days they were in a CZ or QHDA during the filing period. This is in addition to the 180-day extension.

o Servicemembers serving overseas write “MILITARY OVERSEAS” at the top of the tax return in RED INK. Servicemembers serving in a designated CZ or QHDA write “COMBAT ZONE” and the area serving at the top of the tax return in RED INK.

o Servicemembers serving overseas or serving in a designated CZ or QHDA write the date deployed overseas or the date they entered a designated CZ or QHDA and the date they returned from overseas or from a designated CZ or QHDA. Attach copies of military orders documenting the deployment.

o If both the servicemember and the servicemember’s spouse are in the military, write the information for both spouses and indicate which information belongs to which spouse. The extensions apply to the both spouses regardless of whether they file joint or separate tax returns.

Resident Military CA resident servicemembers stationed in CA are taxed on their military income. CA provides no

exclusions, subtractions, or credits exempting military active duty pay. CA resident servicemembers stationed outside of CA on TDY remain residents of CA. CA resident servicemembers whose permanent duty station is outside of CA are treated as

nonresidents of CA for tax purposes. CA taxes all income received prior to departure. CA taxes CA sourced income earned after departure (excluding such intangibles like interest and dividends). This applies only to PCS and not TDY or sea duty from a CA homeport.

American Indian tribal servicemembers living on an Indian reservation are not taxed on military pay. These servicemembers subtract exempt income on Sch. CA (540 or 540NR), line 1, Column B.

Multi-State Military Quick Reference

© H&R Block, Inc. 16 | P a g e

Servicemembers may continue to deduct moving expenses using federal Form 3903. No California adjustment is required.

Nonresident Military Military servicemembers domiciled outside of CA are considered nonresidents for tax purposes when

stationed in CA on PCS orders. A nonresident servicemember’s military pay is not taxed in CA under SCRA, and a servicemember who

earns only military pay is not required to file a CA return. A nonresident servicemember who earns any non-military income in California or from California

sources is required to file and pay California taxes on that California income. Such servicemembers file Form 540NR and report all income, including military income, on Sch. CA (540NR) in column A. These servicemembers exclude military income on Sch. CA (540NR) columns B or E. These servicemembers exclude their military compensation and other non-California sourced income from Sch. CA (540NR), column E.

To claim the adjustment, nonresident servicemembers write “MPA” (Military Pay Adjustment) on Sch. CA (540NR), Part II, line 1 to the left of column A or per their tax software’s instructions.

IRA Adjustment – Nonresident active duty servicemembers whose IRA deduction was subject to the federal AGI limitation should recompute their IRA deduction reported on Sch. CA (540NR), line 19 by removing their active duty military pay. Servicemembers calculate the adjustment on Sch. CA (540NR), line 22 and write “MPA Adjustment” on the dotted line next to line 22.

A servicemember’s civilian spouse who meets the MSRRA requirements will not include his/her income in CA income on Sch. CA (540NR), line 1 column E. However, the spouse must include his/her income in total income on Sch. CA (540NR), line 1 column D.

The Veterans Benefits and Transition Act of 2019 allows the spouse of a servicemember to make the election to use the same residence for tax purposes, as the servicemember (regardless of the marriage date). If the spouse makes the election write “VBTA” at the top of the tax return in RED INK.

Reservist/National Guard Reservists and National Guard members who stay overnight more than 100 miles away from their

home while in service can deduct unreimbursed travel expenses on Sch. CA (540), Section C, Line 11. California National Guard Surviving Spouse & Children Relief Act of 2004 - California exempts from

gross income any death benefits received from the State of California by a surviving spouse, registered domestic partner, or member-designated beneficiary of certain military personnel killed in the performance of duty. “Military personnel” includes the California National Guard, State Military Reserve, or the Naval Militia. Taxpayers who reported a death benefit in “other income” on Sch. CA (540), line 8, column A may subtract the death benefit amount in column B.

Deployed Military Exemption – Deployed servicemembers who are the sole owner of a small business are eligible for the Deployed Military Exemption. The business is not subject to the minimum franchise tax or the annual tax if the servicemember owner was deployed during the tax year operated at a loss or ceased operation. To claim the exemption, servicemembers should write “Deployed Military” in black or blue ink in the top margin of the corporation or LLC’s tax return.

Multi-State Military Quick Reference

© H&R Block, Inc. 17 | P a g e

Retirement Military Retirement Pay: CA taxes military retirement pay received by CA residents. This applies to

all military pension income received while the retiree is a CA resident regardless of where the retiree was stationed or domiciled while on active duty.

o Exception: California does not tax military retirement pay received by an American Indian tribal member residing on his/her tribal reservation.

Servicemembers receiving Combat-Related Special Compensation (CRSC), a special compensation for qualified combat-related disabilities, exempt CRSC payments from California tax.

Tax Credits CA Earned Income Tax Credit: Servicemembers may elect to include all (and/or all the spouse’s or

registered domestic partner’s, if filing jointly) nontaxable military combat pay in earned income for purposes of calculating the California EITC, regardless if s/he elected not to include it for federal purposes. Servicemembers making this election must include all nontaxable military combat pay.

Child & Dependent Care Credit: Resident and nonresident servicemembers include in earned in come all military compensation (including combat zone pay) in earned income when calculating this credit. However, income earned by a servicemember’s spouse that is not taxed pursuant to MSRAA is not considered earned income from CA sources. Both spouses must have CA earned income to qualify for this credit.

Renter’s Credit: Nonresident servicemembers do not qualify for this credit. The servicemember’s spouse or registered domestic partner may claim this credit if s/he a California resident, did not live in military housing during tax year, and is otherwise qualified.

o Servicemembers, and other taxpayers, do not qualify for this credit if their rented property is exempt from property taxes. Exempt property includes most government-owned buildings, including military barracks.

Special Filing Rules/Restrictions E-filing Restrictions – none Paper Filing – none (see Extensions for special processing for military extensions)

Additional Resources FTB Pub 10324, Tax Information for Military Personnel FTB Pub 1001, Supplemental Guidelines to California Adjustments FTB Military

4 At the time of this publication the 2020 FTB Pub 1032 was not available.

Multi-State Military Quick Reference

© H&R Block, Inc. 18 | P a g e

Colorado

Filing Status General Rule: Servicemembers and spouses (joint or separate) must use the same filing status for

CO as used on the federal return.

Extensions CO allows servicemembers stationed in a combat zone to postpone filing and paying state income

taxes until 180 days after their assignment in the combat zone ends. Interest and penalties are deferred during this period. If the return is filed under this 180-day extension, servicemembers should write the name of the applicable combat zone across the top of CO Form 104.

Resident Military CO full year resident servicemembers are taxed in the same manner as all other CO residents.

Resident servicemembers are taxed on all income regardless of source, unless an exception applies. Combat Zone: CO does not tax military pay earned in a combat zone that qualifies for the federal

tax exemption. However, CO taxes combat zone income that does not qualify for the federal exemption. Servicemembers whose only source of income is federally exempt military compensation are not required to file a CO return.

Colorado is HOME Act: An active duty servicemember (1) whose home of record is CO and (2) who loses CO residency after January 1, 2016 (i.e. chooses residency elsewhere), may reacquire CO legal residency, even without a physical presence in CO, if the servicemember does one of the following:

• Registers to vote in CO.; • Purchases residential property or an unimproved lot in CO; • Titles and registers a motor vehicle in CO; • Notifies the state of previous legal residence of the intent to make CO the state of legal

residence; or • Prepares a new last will and testament declaring that CO is the state of legal residence.

Servicemembers who reacquire residency may: • Subtract active duty service pay to the extent included in federal taxable income on DR

0104AD, line 16; • Not file CO taxes if their only source of income is federally exempt military income; and • Not have CO taxes withheld taxes on federally exempt military income.

Servicemembers and spouses who are full-year CO residents and who spend at least 305 days outside of the 50-state boundary of the U.S. for active duty service may file as a nonresident on their CO return by marking the “nonresident 305-day rule Military” indicator on Form 104PN.

Nonresident Military Under SCRA, a nonresident servicemember’s active duty military pay is not taxable by CO. Nonresidents are taxed by CO only on non-military income derived from CO sources (e.g. wages

from a nonmilitary job, rental income from property located in CO, etc.). Servicemembers earning non-military income must pay CO tax and Form 104PN.

Multi-State Military Quick Reference

© H&R Block, Inc. 19 | P a g e

MSRRA qualified spouses can prevent CO withholding on wages earned in Colorado by submitting a completed DR 1059 to the employer when hired. Additionally, MSRRA qualified spouses must submit a completed DR 1059 to the CO DOR, along with a copy of their military ID card with Form 104PN yearly.

Reservist/National Guard No special provisions

Tax Credits No special provisions

Retirement Retired servicemembers under age 55 at the end of the tax year may claim the military retirement

subtraction of $7,500 on Form DR 0104AD line 5 or 6, subject to limitations. Retired servicemembers at least 55 at the end of the tax year may claim the regular pension and

annuity subtraction on line 3 or 4 of Form DR 0104AD for retirement benefits included in federal taxable income, subject to limitations.

• Retirees 55 – 64 may deduct up to $20,000 • Retirees 65+ may deduct up to $24,000

Special Filing Rules/Restrictions CO will not accept a military power of attorney. Taxpayers must use Form DR 0145, Power of

Attorney.

Additional Resources Colorado Publication FYI Income 21 – Military Service Members Military Service Members FYI - Income 21: Military Servicemembers

Multi-State Military Quick Reference

© H&R Block, Inc. 20 | P a g e

Connecticut

Filing Status General Rule: Use the same filing status for CT as used on federal income tax return. Married Non-MSRRA Qualified Spouse: If the servicemember and spouse reside together, and the

non-military spouse does not qualify for the MSRRA exemption, the residency or nonresidency, and filing status, may be affected. If the servicemember’s spouse does not qualify for the exemption under the MSRRA, the filing status is as noted below:

o Married Filing Jointly if: the servicemember is a resident of CT and the spouse is a nonresident of CT, and

both spouses elect to be treated as residents of CT for the entire taxable year; or the servicemember and spouse are both nonresidents of CT and only one spouse

has non-military income derived from or connected with sources within CT, and both spouses elect to file a joint CT income tax return; or

the servicemember and spouse are both part-year residents of CT and have the same period of residency; or

the servicemember and spouse are both CT residents and the filing status for federal income tax purposes is married filing jointly.

o Married Filing Separately if: the servicemember is a resident or nonresident of CT and the spouse is a part-year

resident of CT; or the servicemember and spouse are both part-year residents of CT but do not have

the same period of residency; or the servicemember is a resident of CT and the servicemember’s spouse is a

nonresident of CT, and both spouses do not elect to be treated as CT residents; or the servicemember and spouse are both nonresidents of CT, only one spouse has

CT-sourced income (other than military pay) with sources within CT, and the couple elects not to file a joint return.

Extensions Servicemembers who serve in a combat zone or contingency operation file their CT income tax

return no later than 180 days after the later of: o The last day of service in a combat zone or contingency operation or the last day the area is

designated as a combat zone or contingency operation; or o The last day of continuous hospitalization inside or outside CT because of wounds, disease,

or injury incurred while serving in a combat zone or contingency operation. Spouses of servicemembers and civilians supporting the armed forces in a combat zone or

contingency operation who are away from their permanent duty stations but are not within the designated combat zone or contingency operation, are also eligible for the extension.

Qualifying individuals requesting an extension should print both the name of the combat zone or contingency operation and the operation they served with at the top of their CT return. This is the same combat zone or contingency operation name printed on the federal income tax return.

Multi-State Military Quick Reference

© H&R Block, Inc. 21 | P a g e

Resident Military CT resident servicemembers stationed in CT include base military pay in CT taxable income and file

CT Form 1040 Combat Zone: CT does not tax combat pay and hostile fire or imminent danger special pay. CT resident servicemembers who are assigned to another state or country may file as nonresidents

if they meet the specific requirements for the “Group A exception” or “Group B exception” as outlined on pages 6-9 of Informational Publication 2019(5) (extensive examples are provided). A military or non-military resident may file as a nonresident if the taxpayer meets all of the conditions for either the Group A exception or Group B exception as set forth below:

Group A exception, the taxpayer: o did not maintain a permanent place of abode in CT for entire taxable year; o did maintain a permanent place of abode outside of CT for the entire taxable year; and o did not spend more than an aggregate of 30 days in CT during the taxable year Group B exception, the taxpayer, during any period of 548 consecutive days: o is present in a foreign country, or countries, for at least 450 days; o did not spend more than 90 days in CT and did not maintain a permanent place of abode in

CT at which spouse (unless legally separated from spouse) or minor children spent more than 90 days; and

o is not present in CT for a number of days which does not exceed an amount that bears the same ratio to 90 as the number of days contained in the nonresident portion of the taxable year bears to 548 during a taxable year in which the 548-day period either began or ended.

Number of days in the nonresident portion/548 X 90 = maximum number of days allowed in CT.

Nonresident Military Under SCRA, a nonresident servicemember’s active duty military pay is not taxable by CT.

Nonresident servicemembers with no income other than active duty military pay are not required to file a CT income tax return.

Nonresident servicemembers are taxed on non-military CT sourced income and must file CT Form 1040NR/PY. Subtract military pay on line 51 of CT Form 1040NR/PY.

A nonresident servicemember’s armed forces pension is not CT-sourced income.

Reservist/National Guard No special provisions. See “Retirement” below.

Tax Credits No special provisions

Retirement Veterans receiving disability pensions and any other benefits are treated the same for CT tax

purposes as for federal income tax purposes. Veterans exclude these benefits from CT income tax if these amounts are excludable from gross income for federal income tax purposes.

Multi-State Military Quick Reference

© H&R Block, Inc. 22 | P a g e

Retired servicemembers, including retired National Guard members, subtract retirement pay received from the U.S. government from federal AGI when computing CT AGI. To the extent the retirement paid is included in federal AGI, the retired servicemember subtracts military retirement pay on Form CT-1040, Line 44 (resident) or Form CT-1040NR/PY, Line 46 (non-resident, or part-year resident).

o Survivor benefits received by a beneficiary under an option or election made by a retired member, and that began upon the member’s death, are also excluded from CT AGI.

o A former spouse of a retired servicemember that receives payments as part of a divorce or dissolution decree does not qualify for the retirement pay exclusion.

CT does not treat Armed Forces pension as CT sourced income earned by CT nonresidents

Special Filing Rules/Restrictions A servicemember’s MSRRA qualified spouse who had CT income tax withheld from his/her wages

may file a claim for refund of any amount withheld from wages by paper filing Form CT-1040NR/PY, Connecticut Nonresident and Part-Year Resident Income Tax Return, and writing “Military Spouse” across the top of the return. Attach the following documents:

o A letter signed by the military spouse stating that he or she is claiming the MSRRA exemption on the wages earned in CT and that he or she meets all the requirements to claim the exemption under the MSRRA;

o A copy of the servicemember’s Leave and Earnings Statement; and o A copy of the military ID issued to the military spouse.

If a servicemember dies while on active duty in a combat zone or because of injuries received in a combat zone:

o No income tax or return is due for the year of death or for any prior taxable year on or after the first day serving in a combat zone.

o Any tax due for those years which is unpaid at the date of death, including interest, additions to tax, and penalties, if any, will not be assessed. If assessed, the assessment will be abated, and if collected, it will be refunded to the legal representative of the estate.

o If any tax was previously paid for those years, the tax will be refunded to the legal representative of the estate or to the surviving spouse upon the filing of a return on behalf of the decedent.

o When filing on behalf of a deceased servicemember, enter zero tax due and attach a statement to the return along with a copy of the death certificate.

Additional Resources Military Information, CT DRS website Information Publication 2019(5), CT Income Tax Information for Armed Forces Personnel and

Veterans

Multi-State Military Quick Reference

© H&R Block, Inc. 23 | P a g e

District of Columbia

Filing Status General Rule: Taxpayers, including servicemembers, use the same filing status on the DC return as

used on the federal return. If more than one filing status applies, the servicemember should use the filing status that will result in the lowest tax.

Extensions Servicemembers who are serving in a designated CZ may receive an extension of up to an additional

6 months to file their D.C. income taxes as well as pay any amounts that are due. Mark the “Military Combat Zone” indicator at the top of Form FR-127. During the period of extension, assessment and collection deadlines are extended and no penalty and interest will be charged. The extension also applies to spouses, whether they file joint or separate returns.

Resident Military Active duty military income earned by D.C. residents is taxable and reported on Form D-40.

Nonresident Military Under SCRA, a nonresident servicemember’s active duty military pay is not taxable by DC.

Nonresident servicemembers that are otherwise required to file a DC return, deduct military compensation on Schedule I, line 14.

MSRRA-qualified spouses are not subject to tax on income earned in the District. The spouse may file Form D-4A, Certificate of Nonresidence in the District of Columbia, with his/her employer to claim exemption from D.C. withholding.

Keep a copy of the Dept. of Defense form providing the servicemember’s legal residence with the nonresident servicemember’s tax records.

Reservist/National Guard No special provisions

Tax Credits No special provisions

Retirement No special provisions

Special Filing Rules/Restrictions No special provisions

Additional Resources No additional resources

Multi-State Military Quick Reference

© H&R Block, Inc. 24 | P a g e

Delaware

Filing Status General Rule: Taxpayers, including servicemembers, may use a different filling status on the DE return

than used on the federal income tax return.

Extensions No special provisions

Resident Military DE resident servicemembers may exempt combat pay from DE income tax to the extent that the

combat pay is excludable from federal gross income.

Nonresident Military A nonresident servicemember’s military pay is not taxed in DE under SCRA, and a servicemember

who earns only military pay is not required to file a DE return. A nonresident servicemember who earns any non-military income from DE sources must file and

pay DE taxes on that income. Nonresident servicemembers who are required to file a return must include all income on Form 200-

02 in Column 1, lines 1 to 14 and subtract military compensation in Column 1, line 16. MSRRA-qualifying spouses are not subject to tax by DE and can file an Annual Withholding Tax

Exemption Certification, Form W-4DE, to be exempted from DE withholding on their paychecks.

Reservist/National Guard No special provisions

Tax Credits No special provisions

Retirement No special provisions

Special Filing Rules/Restrictions Tax relief for death related to service in combat zone, terroristic, or military action:

o DE does not tax the servicemember in the tax year of his/her death if the death occurred while serving in a CZ or was due to wounds, disease, or injury while serving in a CZ.

o DE does not impose income tax in the tax year of the death of a servicemember if the death occurred because of wounds or injury incurred while serving outside the U.S. during a terroristic or military action.

Additional Resources Personal Income Tax FAQs (Military)

Multi-State Military Quick Reference

© H&R Block, Inc. 25 | P a g e

Georgia

Filing Status General Rule: Servicemembers use the same filing status for GA as used on the federal income tax

return. Nonresident Spouse Exception: A servicemember may file jointly or separately, regardless of federal

filing status, if one spouse is a resident and the other is a nonresident without any GA-source income.

Extensions GA allows resident servicemembers serving outside of the continental U.S. an automatic extension

to file their GA return of six months after returning to continental U.S. No penalties or interest will accrue during this period.

Servicemembers who are hospitalized because of injuries sustained while serving in a designated combat zone or who are imprisoned by forces opposing the United States while serving in a combat zone receive an extension for filing their GA income tax return for the period of service in the combat zone, plus the period of continuous hospitalization attributable to an injury, plus any period of confinement, and the next 180 days.

Resident Military GA taxes resident servicemembers on all income, regardless of source, including military pay, unless

otherwise specifically exempt by GA law. Servicemembers who are killed in combat or deceased because of injuries incurred in combat are

exempt from all GA income taxes in the year of their death. This exemption applies to any prior taxable year ending on (or after) the first day the servicemember served in the combat zone.

Nonresident Military Under SCRA, a nonresident servicemember’s active duty military pay is not taxable by GA.

Nonresident servicemembers must file a GA return only if they receive non-military GA sourced income.

If a nonresident servicemember is required to file a GA return, the nonresident servicemember files GA Form 500 and completes Schedule 3 to calculate GA taxable income.

MSRRA qualified spouses can prevent GA withholding from their pay by checking the applicable box in Section 8 of GA Form G-4 and returning Form G-4 to the employer. The employer must submit Form G-4 to the GA Dept. of Revenue as provided on Form G-4.

Reservist/National Guard National Guard members and Reservist serving in a combat zone or stationed in defense of the

borders of the U.S. pursuant to military orders may exclude, to the extent included in federal AGI, military compensation earned the during the period covered by the military orders. The servicemember claims the exclusion by attaching a copy of the federal return with the GA return.

Multi-State Military Quick Reference

© H&R Block, Inc. 26 | P a g e

National Guard and Air National Guard members who are on active duty for more than 90 consecutive days can claim a tax credit for the cost of qualified life insurance premiums paid through the servicemember’s group life insurance program. The servicemember claims the credit on Form IND-CR.

Tax Credits See “Reservist/National Guard” above.

Retirement A resident who is a “disabled veteran” is exempt from tax on disability income received from the

U.S. Dept. Of Veterans Affairs if the payment is for: (i) Loss or permanent loss of use of one or both feet; (ii) Loss or permanent loss of use of one or both hands; (iii) Loss of sight in one or both eyes; or (iv) Permanent impairment of vision of both eyes

A “disabled veteran” is any wartime veteran discharged under honorable conditions and who is at least 90 percent totally and permanently disabled.

Special Filing Rules/Restrictions No special provisions

Additional Resources Withholding and Taxation of Certain Nonresident Military Spouses (Policy Statement IT-2019-01)

Multi-State Military Quick Reference

© H&R Block, Inc. 27 | P a g e

Hawaii

Filing Status General Rule: Taxpayers, including servicemembers, may use a different HI filing status than used

on the federal income tax return. Married Split Residency:

o Joint Resident Income Tax Return: The taxpayer may file a joint HI resident tax return. However, all the income of both spouses must be included on the HI income tax return, regardless of source, from the date the resident spouse establishes residence in HI.

o Married Filing Separate Resident Tax Return: The taxpayer may file a separate HI resident income tax return, instead of a joint resident income tax return. The resident spouse is taxed on all regardless of source, at the rates applicable to married individuals filing separate income tax returns

Extensions Servicemembers serving in a combat zone may receive an extension of 180 days after the date the

servicemember leaves the combat zone.

Resident Military HI does not tax military pay received by servicemembers while in a combat zone. HI forgives income tax for servicemembers who die while on active duty in a combat zone or

because of wounds, diseases, or injuries incurred while serving in a combat zone. Servicemembers who are not eligible for combat zone benefits may defer collection action for up to

six months after the period of military service if the servicemember’s ability to pay is materially impaired because of the member’s military service. Servicemembers may request deferral by sending to the Department of Revenue a copy of the notice of tax due and attaching a written request with the servicemember’s name, social security number, monthly income and source of income before military service, and date they are eligible for discharge (and, if possible, a copy of their orders).

HI imposes an interest rate of 8% per year on outstanding tax liabilities. To use the 6% interest rate under the SCRA, active duty servicemembers must send a written request for relief to the HI Dept. of Revenue, along with a copy of their orders or reporting instructions detailing their call to active duty.

Nonresident Military Under SCRA, a nonresident servicemember’s active duty military pay is not taxable by HI. Nonresident servicemembers are not required to file a HI income tax return unless they receive non-

military HI sourced income such as rental income or non-military wages. Nonresident’s receiving non-military HI sourced income must file Form N-15.

A servicemember’s nonresident spouse who does not qualify for protections under MSRRA is taxed on HI sourced income and must file Form N-15.

Multi-State Military Quick Reference

© H&R Block, Inc. 28 | P a g e

Reservist/National Guard Reservist and National Guard members may exclude up to $6,943 (for tax years beginning after

2019) of military pay received from taxable income. • Servicemembers should enter on Form N-11, line 15 the smaller of (a)$6,943, or (b) the

amount of the servicemember’s pay Form W-2, box 16. • If the servicemember is married and filing a joint return, and both spouses qualify, the

exclusions for both spouses should be added and the total should be entered on line 15.

Tax Credits No special provisions

Retirement HI does not tax qualifying distributions from military pensions. Retired servicemembers subtract

qualifying distributions from a military pension by using Form N-11, line 13.

Special Filing Rules/Restrictions No special provisions

Additional Resources Tax Information Release No. 90-10: Clarification of Taxation and the Eligibility for Personal

Exemptions and Credits of Residents and Nonresidents in the Military and Spouses and Dependents of Persons in the Military.

Tax Information Release No. 2003-2: Extension of Deadlines and Other Tax Relief for Members of the Armed Forces, Reserves, and Hawaii National Guard

Tax Information Release No. 2010-01: Military Spouses Residency Relief Act (“MSRRA”) Tax Facts 97-2: Income Tax Information for Nonresident Military Servicemembers

Multi-State Military Quick Reference

© H&R Block, Inc. 29 | P a g e

Iowa

Filing Status General Rule: Servicemembers use the same filing status for IA as they used on the federal income

tax return. Married Taxpayers: A taxpayer, including a servicemember, and spouse filing a joint federal return

can file separately using either (a) Status 3, married filing separately on a combined return, or (b) Status 4, married filing separate returns: o If a nonresident servicemember’s resident spouse has IA-source income it may be beneficial to

use filing status 3 (married filing separately on the combined return form). o Nonresident spouses without IA sourced income may use filing status 3 or 4 (married filing

separately on the combined return or married filing separate returns).

Extensions IA grants all active duty servicemembers in the armed forces (including Reservists and National

Guard members) deployed outside the U.S. an extension of 180 days to file and pay, without interest or penalty, IA income taxes after leaving the combat zone (CZ), the hazardous duty area (HDA) or ceasing to participate in a contingency operation.

Servicemembers hospitalized because of injury or illness in a CZ or HDA have five years to file and pay, without interest or penalty, IA income taxes after leaving the combat zone or hazardous duty area.

The 180-day extension applies to spouses of servicemembers filing a combined return. To claim the extension, servicemembers (or their spouses, authorized agents and taxpayer

representatives) notify the IA DOR by providing: o The servicemember’s name, and spouse’s name, if applicable. o The servicemember’s stateside address, and spouse’s address, if applicable. o The servicemember’s date of birth, and spouse’s date of birth, if applicable. o The date the servicemember was deployed to the CZ or other qualifying area. o An official document that indicates the servicemember’s area of operation.

Resident Military IA excludes active duty military pay from taxable income. Active duty servicemembers (including

Reservists and National Guard members) include active duty pay received from the federal government for military service performed as income on line 1 (wages) of Form IA 1040 and deduct the same active duty pay on line 24 (other adjustments).

When calculating the income threshold to file a tax return, servicemembers do not include income received from excludable active duty service. For example: a married couple, IA residents and under the age of 65, whose combined income totals $50,000 with $40,000 of that income representing pay for active duty may not have to file a tax return. This is because their combined income, without the military pay, is $10,000 which is below the MFJ threshold of $13,500.

IA forgives income tax when a servicemember is killed in a combat zone, missing in action or presumed dead, killed outside the US due to terrorist or military action.

Multi-State Military Quick Reference

© H&R Block, Inc. 30 | P a g e

Nonresident Military Under SCRA, a nonresident servicemember’s active duty military pay is not taxable by IA. If required to file an IA tax return, nonresident servicemembers do not include military pay on line 1

of the IA 1040 and also do not report it as IA income on the IA 126. In general, this applies only to active duty military and does not include the National Guard or Reserve personnel.

MSRRA qualifying spouses report all IA source income report all IA source income on IA 1040, but show no Iowa wages, salaries, tips or Schedule C income on IA 126.

Reservist/National Guard National Guard members who are performing active military service for the military or at the

direction of the federal government can exclude pay received from the federal government for military service performed.

National Guard members employed full-time in the National Guard doing duty for the state are not considered in active duty status and their pay is not excluded from IA tax.

If a Reservist or National Guard member is called to active state or federal duty and makes a withdrawal from a qualified retirement account, the amount of the withdrawal is not subject to IA income tax or state tax penalty. If this income is reported as taxable pension income on line 9 of the IA return, the servicemember enters that amount on line 24 of the IA 1040 (other adjustments).

Tax Credits IA offers property tax credits for servicemembers and veterans including: o The Disabled Veteran Homestead Tax Credit adopted to encourage home ownership for

disabled veterans. The current credit is equal to 100% of the actual tax levy. o The IA Military Exemption reduces the taxable value of property for military veterans. o Military student loan exemption – Servicemembers, Reservists, and National Guard members

may exempt student loan repayments from IA Income tax if the individual is on active duty at the time of the loan repayment. Include the repayment amount on line 1 of the IA 1040 and deduct on line 24 under “other adjustments”.

Retirement IA excludes military retirement benefits from taxation, for both resident and nonresidents, without

age restrictions. Survivor benefits received under U.S.C. 1447 are also excluded. The military retirement benefits exemption is in addition to the general $6,000/$12,000 pension exclusion available to IA taxpayers 55 years of age or older.

Special Filing Rules/Restrictions IA accepts the federal Power of Attorney form or a Military Power of Attorney if it contains a written

statement, initialed by the taxpayer, indicating it is being submitted for use with the IA forms.

Additional Resources Iowa Military Tax information Iowa Tax Responsibilities of Military Personnel Military Loan Exemptions IA § 422.7(42)/IAC § 701-- 40.63 Military Spouse Residency Relief Act

Multi-State Military Quick Reference

© H&R Block, Inc. 31 | P a g e

Idaho

Filing Status General Rule: Servicemembers must use the same filing status for ID as they use on the federal

income tax return. Married, Split Residency: Resident servicemembers on active duty outside ID who are married to a

part year ID resident or nonresident must file ID Form 43. Resident servicemembers on active duty outside ID who are married to ID residents file ID Form 40.

Caution - Community Property State: Resident spouses filing separate returns must divide equally between them the community income, withholdings, and deductions of both spouses. The community property should include only the income earned during the time the couple was married. These spouses must include with the tax return a copy of any written agreement between them regarding the separation of assets and income.

Extensions ID follows the federal rules on 180-day extensions for servicemembers serving in a combat zone.

For a more a more in-depth discussion, see IRS Publication 3. Servicemembers must write "COMBAT ZONE" and the date of deployment in red on top of the ID return.

Resident Military Resident servicemembers stationed in ID report all military and non-military income, regardless of

source, on Form 40, line 7. ID does not tax the military pay earned outside of ID by resident servicemembers on continuous and

uninterrupted active duty for 120 days or more (which do not need to be in the same tax year). A resident servicemember who files Form 40 subtracts this military pay on Form 39R, line 11.

ID exempts military pay earned while serving in a combat zone or hospitalized for injuries or illness sustained in a combat zone.

Nonresident Military Under SCRA, a nonresident servicemember’s active duty military pay is not taxable by ID. A nonresident servicemember who earns more than $2,500 of non-military gross income from ID

sources must file ID Form 43 and pay ID tax. A nonresident servicemember’s civilian spouse who meets the MSRRA requirements can claim an

exemption from withholding on wages by filing Form ID-MS1 with an employer.

Reservist/National Guard ID follows federal guidelines and no tax is owed for enlisted or warrant officer’s military pay

received while serving in a combat zone. Commissioned officer pay exclusion is capped at the highest enlisted pay plus any hostile fire or imminent danger pay.

National Guard members should write "COMBAT ZONE" and the date of deployment in red ink at the top of the return.

Multi-State Military Quick Reference

© H&R Block, Inc. 32 | P a g e

Tax Credits Grocery Credit: Resident servicemembers on active duty military may qualify for a refund of the

grocery credit. Credit for Taxes Paid to Another State: Resident servicemembers on active military duty use Form

39NR, Part D when computing the credit for taxes paid to another state.

Retirement Retired servicemembers may subtract from taxable income on ID Form 39R, line 8 (residents) or ID

Form 39NR, line 22 (nonresidents or part-year residents), any retirement benefits paid by the U.S. if they are (1) at least 65 years old or (2) at least 62 years old and disabled. Married taxpayers filing separate returns cannot claim this subtraction.

Special Filing Rules/Restrictions Spouses of servicemembers serving in a combat zone may sign the joint income tax return for the

servicemember without a power of attorney. The spouse attaches a signed statement to the return that explains the servicemember is serving in a combat zone. Spouses filing an electronic return should keep a copy of the statement with the federal Form 8453.

Additional Resources Idaho Tax Commission Military

Multi-State Military Quick Reference