msc investment management programme design … investment management.… · the msc investment...

TRANSCRIPT

MSc Investment Management Programme Design

Academic Year 2014-15

MSc Investment Management

The MSc Investment Management programme is closely designed around preparing students for CFA examinations. The programme is divided into three distinct sections:

The first semester of taught courses or modules (that runs from September to December with examinations in January) worth 60 credits

The second semester of taught modules (that runs from February to April with examinations in May) worth 60 credits

An independent study project (completed over the summer period) worth 60 credits

The specific modules that you take will use a wide range of different assessment methods that may include coursework, essays, multiple-choice tests, presentations and formal unseen examinations. In the second semester students have the freedom to pick an optional module from our extensive module catalogue. The School of Management is continually revising and seeking to improve the module and programme catalogue on offer. As such, this document should be taken as indicative rather than definitive and modules may be altered or withdrawn at any time.

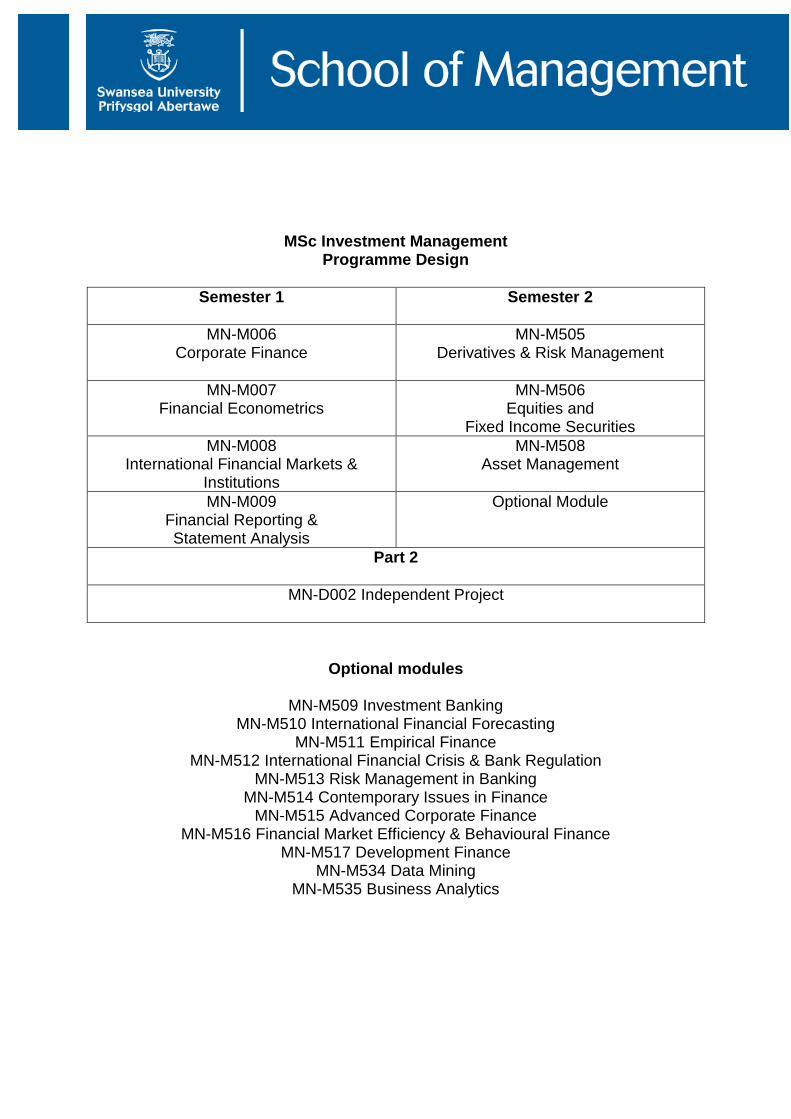

MSc Investment Management Programme Design

Semester 1

Semester 2

MN-M006 Corporate Finance

MN-M505 Derivatives & Risk Management

MN-M007 Financial Econometrics

MN-M506 Equities and

Fixed Income Securities

MN-M008 International Financial Markets &

Institutions

MN-M508 Asset Management

MN-M009 Financial Reporting & Statement Analysis

Optional Module

Part 2

MN-D002 Independent Project

Optional modules

MN-M509 Investment Banking MN-M510 International Financial Forecasting

MN-M511 Empirical Finance MN-M512 International Financial Crisis & Bank Regulation

MN-M513 Risk Management in Banking MN-M514 Contemporary Issues in Finance

MN-M515 Advanced Corporate Finance MN-M516 Financial Market Efficiency & Behavioural Finance

MN-M517 Development Finance MN-M534 Data Mining

MN-M535 Business Analytics

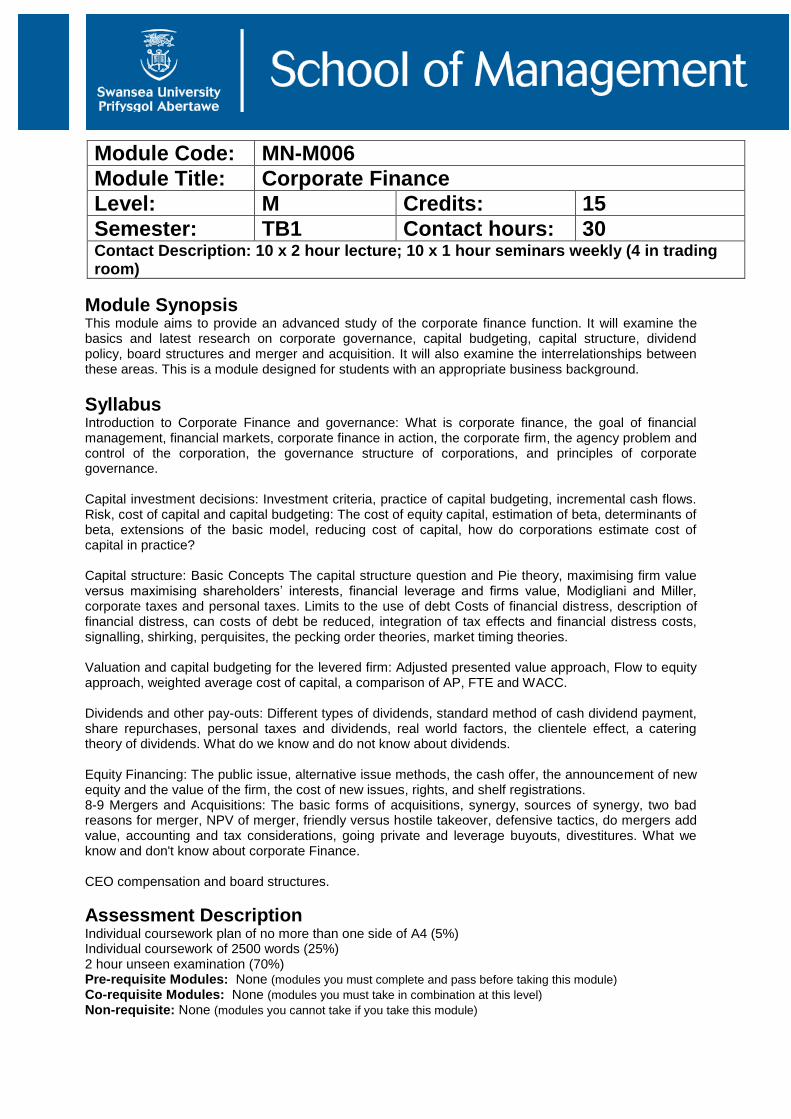

Module Code: MN-M006

Module Title: Corporate Finance

Level: M Credits: 15

Semester: TB1 Contact hours: 30 Contact Description: 10 x 2 hour lecture; 10 x 1 hour seminars weekly (4 in trading room)

Module Synopsis This module aims to provide an advanced study of the corporate finance function. It will examine the basics and latest research on corporate governance, capital budgeting, capital structure, dividend policy, board structures and merger and acquisition. It will also examine the interrelationships between these areas. This is a module designed for students with an appropriate business background.

Syllabus Introduction to Corporate Finance and governance: What is corporate finance, the goal of financial management, financial markets, corporate finance in action, the corporate firm, the agency problem and control of the corporation, the governance structure of corporations, and principles of corporate governance. Capital investment decisions: Investment criteria, practice of capital budgeting, incremental cash flows. Risk, cost of capital and capital budgeting: The cost of equity capital, estimation of beta, determinants of beta, extensions of the basic model, reducing cost of capital, how do corporations estimate cost of capital in practice? Capital structure: Basic Concepts The capital structure question and Pie theory, maximising firm value versus maximising shareholders’ interests, financial leverage and firms value, Modigliani and Miller, corporate taxes and personal taxes. Limits to the use of debt Costs of financial distress, description of financial distress, can costs of debt be reduced, integration of tax effects and financial distress costs, signalling, shirking, perquisites, the pecking order theories, market timing theories. Valuation and capital budgeting for the levered firm: Adjusted presented value approach, Flow to equity approach, weighted average cost of capital, a comparison of AP, FTE and WACC. Dividends and other pay-outs: Different types of dividends, standard method of cash dividend payment, share repurchases, personal taxes and dividends, real world factors, the clientele effect, a catering theory of dividends. What do we know and do not know about dividends. Equity Financing: The public issue, alternative issue methods, the cash offer, the announcement of new equity and the value of the firm, the cost of new issues, rights, and shelf registrations. 8-9 Mergers and Acquisitions: The basic forms of acquisitions, synergy, sources of synergy, two bad reasons for merger, NPV of merger, friendly versus hostile takeover, defensive tactics, do mergers add value, accounting and tax considerations, going private and leverage buyouts, divestitures. What we know and don't know about corporate Finance. CEO compensation and board structures.

Assessment Description Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 2500 words (25%) 2 hour unseen examination (70%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level) Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M007

Module Title: Financial Econometrics

Level: M Credits: 15

Semester: TB1 Contact hours: 30 Contact Description: 14 hours lectures, 6 hours tutorials, 10 hours computer workshops

Module Synopsis Financial Econometrics aims to provide students with both a theoretical and a practical knowledge of econometric techniques required in the analysis of financial data. This is intended to help students develop the skills required to perform advanced financial analysis. Practical examples and practical sessions are used to illustrate the concepts involved, and particular emphasis is given to using real data in examining and testing hypotheses concerning the properties of, and relationships between, financial series.

Module Aim This module aims to provide students with a state-of-the-art understanding of econometric tools and their applications to real world problems.

Syllabus Descriptive statistics, distributions and hypothesis testing;

The simple and multiple linear regression model: Hypothesis testing and diagnostic testing;

Dynamic modelling;

Unit root and cointegration analysis;

Causality;

Modelling volatility

Assessment Description 2 x Individual coursework - data-based exercises and short report (20% each) 2 hour unseen examination (60%) - Two questions to be answered from a choice of five. Questions include a mixture of responses to output, data manipulation, and short responses. Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

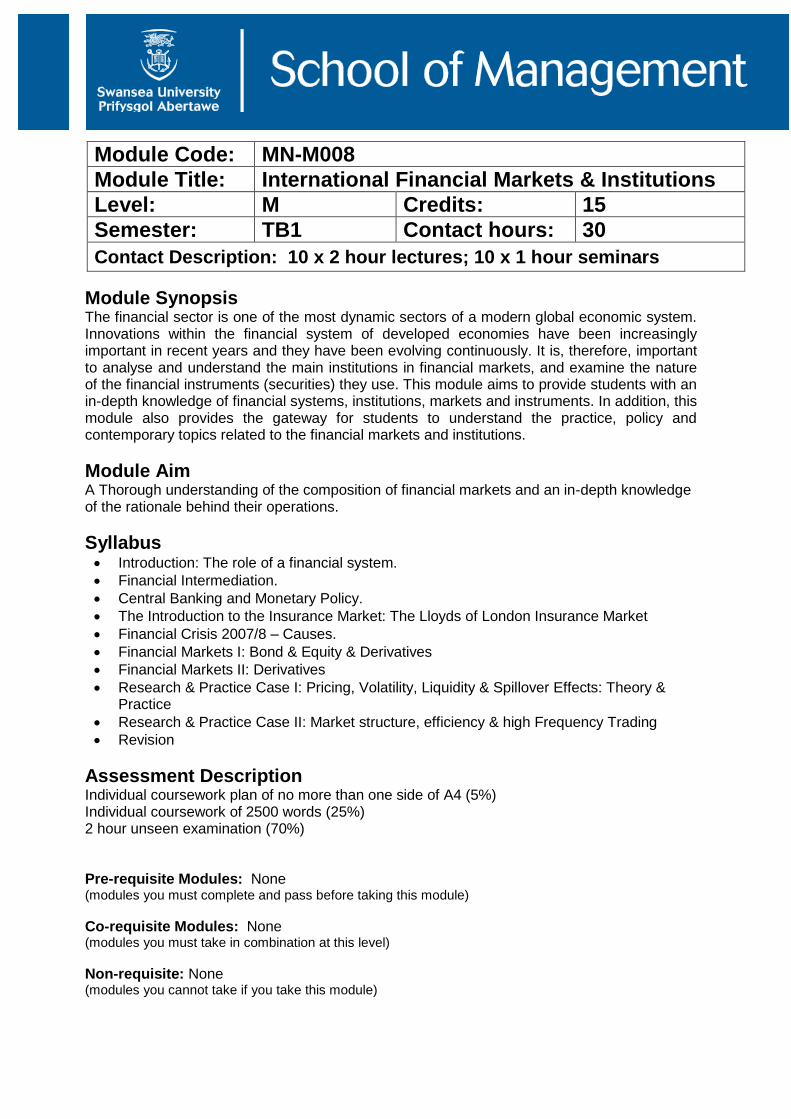

Module Code: MN-M008

Module Title: International Financial Markets & Institutions

Level: M Credits: 15

Semester: TB1 Contact hours: 30

Contact Description: 10 x 2 hour lectures; 10 x 1 hour seminars

Module Synopsis The financial sector is one of the most dynamic sectors of a modern global economic system. Innovations within the financial system of developed economies have been increasingly important in recent years and they have been evolving continuously. It is, therefore, important to analyse and understand the main institutions in financial markets, and examine the nature of the financial instruments (securities) they use. This module aims to provide students with an in-depth knowledge of financial systems, institutions, markets and instruments. In addition, this module also provides the gateway for students to understand the practice, policy and contemporary topics related to the financial markets and institutions.

Module Aim A Thorough understanding of the composition of financial markets and an in-depth knowledge of the rationale behind their operations.

Syllabus Introduction: The role of a financial system.

Financial Intermediation.

Central Banking and Monetary Policy.

The Introduction to the Insurance Market: The Lloyds of London Insurance Market

Financial Crisis 2007/8 – Causes.

Financial Markets I: Bond & Equity & Derivatives

Financial Markets II: Derivatives

Research & Practice Case I: Pricing, Volatility, Liquidity & Spillover Effects: Theory & Practice

Research & Practice Case II: Market structure, efficiency & high Frequency Trading

Revision

Assessment Description Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 2500 words (25%) 2 hour unseen examination (70%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M009

Module Title: Financial Reporting & Statement Analysis

Level: M Credits: 15

Semester: TB1 Contact hours: 30

Contact Description: 10 x 2 hour lectures; 10 x 1 hour seminars

Module Synopsis The module is designed to give students an understanding of financial reporting and how financial statements are prepared. Students will consider the usefulness of financial statements and financial statement analysis in decision making.

Module Aim The module aims to give students the knowledge and skills necessary to read a set of financial statements and to draw meaningful conclusions about the financial performance and position of a company. Students will study the tools and techniques of financial analysis which allows users to compare financial performance over time and between companies.

Syllabus Introduction to the Principles of Finance Reporting and to the Conceptual Framework

Introduction to financial analysis and its role in decision making

The primary financial statements – their purpose and content

Financial reporting standards in relation to non-current assets

Financial reporting standards relating to non-current liabilities

Financial reporting standards relating to revenue, inventory and taxes

Financial analysis – tools and techniques

Financial analysis – evaluating trends

Financial analysis – predicting future performance

Financial statements – manipulation, fraud and the limitations of financial statements and of financial analysis as a tool in decision making.

Assessment Description Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 2500 words (25%) 2 hour unseen examination (70%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M505

Module Title: Derivatives & Risk Management

Level: M Credits: 15

Semester: TB2 Contact hours: 30 Contact Description: 10 x 2 hour lectures; 10 x 1 hour weekly seminars

Module Synopsis This module aims to provide an understanding of how companies and financial institutions can manage risk through the use of financial derivatives and covers the role of hedging and risk management in business organisations. Different types of financial derivative will be introduced and their roles in financial markets in terms of trading and hedging will be covered. Basic pricing theories and techniques will also be covered in this module. This module is sponsored by Admiral Insurance Group (Cardiff) with a module prize.

Module Aim This module aims to provide an understanding of how companies and financial institutions can manage risk through the use of financial derivatives and covers the role of hedging and risk management in business organisations. The students are expected to understand derivatives products, pricing and strategic trading and hedging through using derivatives.

Syllabus Introduction to Risk Management and Derivatives Markets

Hedging interest rate risk with futures and forward rate agreements

Swaps and other OTC hedging instruments

Introduction to options

Arbitrage bounds for option prices

Binomial Option Pricing Model

Black-Scholes option pricing model

Option strategies 1

Option strategies 2

Case Studies of Uses and Abuses of Derivative

Assessment Description Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 2500 words (25%) 2 hour unseen examination (70%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M506

Module Title: Equities & Fixed Income Securities

Level: M Credits: 15

Semester: TB2 Contact hours: 30

Contact Description: 10 x 2 hour lectures; 5 x 2 hour seminar fortnightly

Module Synopsis The module is designed to develop an awareness of the two main asset classes of equities and fixed-income securities.

Module Aim The module covers the two main asset classes of equities and fixed-income securities and covers their characteristics and valuation. The module covers the required material for CFA level 1.

Syllabus Types of Equity Securities and Their Characteristics

Equity Markets: Characteristics, Institutions, and Benchmarks

Fundamental Analysis (Sector, Industry, Company)

Valuation of Individual Equity Securities

Equity Market Valuation and Return Analysis

Types of Fixed-Income Securities and Their Characteristics

Fixed-Income Markets: Characteristics, Institutions, and Benchmarks

Fixed-Income Valuation (Sector, Industry, Company) and Return Analysis

Term Structure Determination and Yield Spreads

Analysis of Interest Rate Risk

Analysis of Credit Risk

Valuing Bonds with Embedded Options

Structured Products

Assessment Description Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 2500 words (25%) 2 hour unseen examination (70%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M508

Module Title: Asset Management

Level: M Credits: 15

Semester: TB2 Contact hours: 30 Contact Description: 10 x 2 hour lectures; 5 x 2 hours seminar fortnightly - all in trading room

Module Synopsis This module is concerned with recent advances in asset and portfolio management. It seeks to provide a systematic understanding of the portfolio management concepts and its components. Emphasis is given on the asset allocation process, the equity and fixed-income portfolio management strategy and performance evaluation. Students will have an opportunity to learn how to make use of the database, DATASTREAM. This database provides information on a variety of assets, macro-economic data and financial statements of companies around the world.

Module Aim This module is concerned with recent advances in asset and portfolio management. It seeks to provide a systematic understanding of the portfolio management concepts and its components. Emphasis is given on the asset allocation process, the equity and fixed-income portfolio management strategy and performance evaluation.

Syllabus Introduction to Asset Management

Investment policy statement (IPS)

Equity Portfolio Management

Fixed-income Portfolio Management

Passive and Active Investment Management

Alternative Investment Management (AIM)

Portfolio Monitoring and Performance Evaluation

Assessment Description Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 2500 words (25%) 2 hour unseen examination (70%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M509

Module Title: Investment Banking

Level: M Credits: 15

Semester: TB2 Contact hours: 30 Contact Description: 10 x 2 hour lectures; 10 x 1 hour seminar weekly - PC LAB

Module Synopsis The module is designed to develop an awareness of how investment banking operates.

Module Aim This module aims to provide students with an insight into the major features of the investment banking business. The module will examine the key activities of investment banks including mergers and acquisitions, facilitating capital raising and proprietary trading.

Syllabus The role of investment banks in the global financial system

Investment banks role in facilitating capital raising for companies

Investment banks role in mergers and acquisition activity

The proprietary trading of investment banks

Regulatory issues relating to investment banks including Dodd Frank Act and ring fencing

Risks facing investment banks and risk management practices

The impact of 2008 on the investment banking industry

Assessment Description Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 2500 words (25%) 2 hour unseen examination (70%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M510

Module Title: International Financial Forecasting

Level: M Credits: 15

Semester: TB2 Contact hours: 30

Contact Description: 10 x 2 hour lecture; 10 x 1 hour computer lab

Module Synopsis This module aims to familiarize students with the key concepts used in the forecasting of time series data and financial data. The module exposes students to both the practical and theoretical aspects of time series forecasting, dealing with the application and consideration of a range of forecasting methods and forecast evaluation techniques.

Module Aim This module aims to present the theory and practice of forecasting, and to provide an introduction to the practical application of these techniques in the forecasting of financial data.

Syllabus Broader issues in forecasting: An introduction to forecasting methods; understanding and

interpreting forecasts; quantitative and judgmental forecasts; the basic steps in forecast construction; measures of forecast accuracy; prediction intervals; forecast combination and forecast encompassing.

Time series decomposition: Detrending; seasonal adjustment; alternative moving averages; the classical decomposition; forecasting and decomposition.

Smoothing methods: Exponential smoothing methods; Holt's method; Holt-Winters' method; Pegel's classification.

ARIMA time series modelling: Moving average (MA) models; Autoregressive (AR) models; Autoregressive-moving average (ARMA) models; Stationarity, non-stationarity, and integrated autoregressive-moving average (ARIMA) models; Model estimation and initialization; Nonlinear estimation; Diagnostic checking; Forecasting with ARIMA models.

Forecasting movements in financial data; Specific techniques and alternative forecast evaluation criteria.

Assessment Description Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 2500 words (25%) 2 hour unseen examination (70%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None

(modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M511

Module Title: Empirical Finance

Level: M Credits: 15

Semester: TB2 Contact hours: 30 Contact Description: 10 x 2 hour lectures; 5 x 2 hours seminar fortnightly

Module Synopsis This module aims to provide students with an understanding and appreciation of recent developments in empirical finance. The module is topical in nature, exposing students to the recent empirical studies and econometric methods employed in the analysis of range of financial issues.

Module Aim This module aims to provide an appreciation of topical methods and studies in empirical finance.

Syllabus The syllabus will subject to variation to ensure topicality, but will be expected to include:

The modelling of volatility: GARCH and its extensions

Examining market efficiency

Asset Pricing and Factor Models

Empirical analysis of risk

Panel data analysis

Logit and Probit analysis for corporate finance

The econometrics of regime shifts (inc. Markov switching)

The empirical analysis of returns

Empirical analysis of finance-macroeconomics nexus: interest rates, inflation, the housing market

Assessment Description Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 2500 words (25%) 2 hour unseen examination (70%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M512

Module Title: International Financial Crises & Bank Regulations

Level: M Credits: 15

Semester: TB2 Contact hours: 30

Contact Description: 10 x 2 hour lectures; 10 x 1 hour seminar weekly

Module Synopsis Bank crises occur frequently in many countries and across many time periods. Many go beyond the distress of individual banks and have systemic effects, threatening the banking system as a whole. Although regulators have developed increasingly sophisticated methods to regulate banks they have not been able to prevent further crises. Indeed many changes in the regulatory system are often in response to the effects of financial crises. Thus there is a close and often circulatory relationship to financial crises and regulation. This course examines the causes of financial crises (in particular the 2007/8 global banking crisis), the relationship between crises and bank regulation, the reasons for regulation and the technical aspects of regulation including Basel 3, macroprudential regulation and resolution regimes.

Module Aim This module aims to provide an understanding of the interconnections between financial crises and bank regulation.

Syllabus History of banking Crises; The global banking crisis of 2007/8 – was it so different?

The relationship between banking crises and bank regulation.

Minsky’s instability hypothesis;

The reasons for and against bank regulation;

Free Banking and the New Zealand Model of Regulation;

Regulating Bank Capital Adequacy – Basel 1, 2 and 3;

Regulation of liquidity, Market risk and Operational Risk;

Lender of Last Resort, Deposit Insurance and other safety net provisions;

Too Big to Fail problem and some solutions

Macroprudential regulation.

Assessment Description Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 2500 words (25%) 2 hour unseen examination (70%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M513

Module Title: Risk Management in Banking

Level: M Credits: 15

Semester: TB2 Contact hours: 30

Contact Description: 10 x 2 hour lectures; 10 x 1 hour weekly - PC LAB

Module Synopsis Banks are subject to various risks because of their role as intermediaries, because of business models adopted and because they operate in volatile markets. The risks banks are exposed to through acting as intermediaries are primarily credit risk, liquidity risk and interest risk. Banks are also exposed to market risk through their proprietary trading activities. This course examines the sources of risk facing banks and the methods that banks can adopt to evaluate and control these risks. This module includes the conceptual, technical and computational aspects of risk management in Banking and Financial Institutions. In addition, the module covers topics on how to manage the risk financial institutions are facings such as futures, forwards, options, and swaps. Finally, the module covers the latest innovations in risk management in banking following the lessons from the financial crisis of 2007-08.

Module Aim The aim of the module is to examine the main risks faced by banks and evaluate the main techniques used by banks to manage these risks.

Syllabus Introduction to the main risks faced by banking and insurance institutions

Liquidity and Operational Risk - Asset liability management

Off balance sheet (OBS) and Credit risk

Interest rate Risk

Managing Risk 1 – Futures, Forwards and Swaps

Managing Risk 2 – Options

Understanding and measuring market risk, Value at Risk (VaR) and its shortcomings

Stress Tests, Rating Agencies, Sovereign Risk and Capital Adequacy (Basel Accord)

Originate and Distribute, ABSs, CDOs, and the 2007-08 credit crunch.

Case study: Northern Rock & Revision

Assessment Description Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 2500 words (25%) 2 hour unseen examination (70%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M514

Module Title: Contemporary Issues in Finance

Level: M Credits: 15

Semester: TB2 Contact hours: 30 Contact Description: 10 x 2 hour lectures; 5 x 2 hour seminar fortnightly

Module Synopsis The focus will be on researching important but unresolved issues/puzzles in finance and financial management. The course will help to identify and explain how such financial phenomena exist and persist in financial markets and organisations. The students are trained with knowledge and understanding on contemporary issues in finance as well as key research and presentation skills. Both academic and institutional knowledge at theory and empirical levels will be enhanced through this module.

Module Aim The aim of the module is to identify and explain unresolved puzzles in finance through both lectures, presentations and group paper, and Q&A. Multiple skills and varieties of knowledge will be developed for students. This also aims to create opportunities for students to experience and enhance their ability to professionally communicate and apply what they have learned from the module in providing critical valuation or solution to the contemporary finance issues.

Syllabus The finance puzzles examined change from year to year depending on staff/student interests. The following are representative:

Is the CAPM still a useful model for explaining the variation in stock returns?

Does a firm’s dividend policy matter?

How useful is the theory of agency costs for helping us to understand the use of performance related pay by firms?

Is there any evidence that performance related pay works?

To what extent are the behavioural finance studies a challenge to the efficient markets hypothesis?

Discuss the closed-end fund puzzle

Why do speculative bubbles continue to occur?

Discuss the effects of greater world financial market integration.

Discuss the mini flash crash occurrence and impact to financial markets.

Assessment Description 3 x group presentations (15% each) Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 3000 words (55%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M515

Module Title: Advanced Corporate Finance

Level: M Credits: 15

Semester: TB2 Contact hours: 30

Contact Description: 10 x 2 hour lectures; 5 x 2 hour seminars

Module Synopsis The module is designed to build on the Corporate Finance in semester 1 and examine some of the latest theoretical and empirical contributions to our understanding of corporate finance.

Module Aim The module builds on the foundations laid in the Corporate Finance module in semester 1 and examines some of the latest theoretical and empirical contributions in this subject. The aim will be to understand the contribution to our understanding of corporate finance from latest research published in academic journals.

Syllabus A primer on the main themes of Corporate Finance

Arbitrage and Financial Decision Making

Valuation

Risk

Capital Structure

Financial Distress, Managerial Incentives and Information

Payout policy

Capital budgeting and valuation with leverage

Risk management

International Corporate Finance

Assessment Description Group plan of no more than one side of A4 (5%) Group Presentation (10%) Group Report of 3500 words (25%) 2 hour unseen examination (60%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M516

Module Title: Financial Market Efficiency & Behavioural Finance

Level: M Credits: 15

Semester: TB2 Contact hours: 30 Contact Description: 10 x 2 hour lectures; 5 x 2 hour seminars

Module Synopsis The module is designed to develop an awareness of the hypothesis of financial market efficiency and the challenges to this hypothesis from behavioural finance.

Module Aim This module examines the nature of the efficient market hypothesis and the evidence relating to this hypothesis. A challenge to the efficient market hypothesis has come from the application of psychological concepts to investor decision making – termed behavioural finance. The conflict between these two approaches to understanding the way financial markets operate is the main focus of this module

Syllabus The concept of efficient markets and the Fama classification of EMH tests

Evidence on weak form tests

Evidence on semi-strong form tests

Evidence on strong form tests

Criticisms of the EMH: rationality, joint-hypothesis etc

Psychological biases in decision making – prospect theory, overconfidence, narrow framing, limits to arbitrage etc

Overreaction and underreaction

Herding

Bubbles

Criticisms of behavioural finance and comparison with EMH

Assessment Description Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 2500 words (25%) 2 hour unseen examination (70%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M517

Module Title: Development Finance

Level: M Credits: 15

Semester: TB2 Contact hours: 30 Contact Description: 10 x 2 hour lectures; 10 x 1 hour seminars

Module Synopsis Module aims to cover some key aspects of financial sector policies, financial development, financial structure and economic growth. It then discusses the models of financial repression and financial liberalization, and the theoretical and empirical determinants of private savings. This is followed by an in-depth discussion of the role of foreign aid and remittances in economic development. The debt and financial crises of the 1990s are thoroughly analysed, as well as examining the importance of informal markets in LDCs.

Module Aim To provide students with a detailed analysis of the major explanations for the nature and patterns of the impact of finance and financial development on growth and the consequences of intervention (financial repression or liberalization, foreign aid) and the impact of capital flows in the form of Foreign Direct Investment (FDI). Additionally, the course will also analyse the informal financial markets.

Syllabus 1.An introduction to development finance The Finance-Growth Nexus 2.Financial Repression 3.Financial Liberalization 4.Determinant of Savings 5.Foreign Direct Investment 6.Foreign Aid 7.International Debt crisis 8.The Asian Crisis 9.Informal Financial Markets

Assessment Description Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 2500 words (25%) 2 hour unseen examination (70%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

Module Code: MN-M534

Module Title: Business Analytics

Level: M Credits: 15

Semester: TB2 Contact hours: 30

Contact Description: 10 x 2 hour lectures; 10 x 1 hour seminars

Module Synopsis Business analytics as applied to big data is a game-changing opportunity for business practice. The last decade has seen an explosion in the volume of data collected by business and government – providing opportunities to analyse behaviours at individual and macro- levels. The purpose of this module is to inform students as to the major concepts of business analytics – both in theory and in practice from a strategic perspective.

Module Aim The module aims to prepare students for the analysis of large data sets in business organisations.

Syllabus What is big data and why is it important Big data technology Business analytics models Business analytics at the strategic level Development and deployment at the functional level Business analytics at the analytical level Data sourcing and collection Embedding an analytic approach across the organisation Information management Business analytics modelling in practice Data privacy and ethics

Assessment Description Individual coursework plan of no more than one side of A4 (5%) Individual coursework of 2500 words (25%) 2 hour unseen examination (70%) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

2

Module Code: MN-M535

Module Title: Data Mining

Level: M Credits: 15

Semester: TB2 Contact hours: 30

Contact Description: 10 x 2 hour lecture; 10 x 1 hour seminar

Module Synopsis The module is designed to provide students with practical and applied knowledge of how to conduct data mining activities for business and management purposes. This includes conceptual approaches and key concepts in data mining as well as the statistical and modelling techniques necessary to analyse large data sets to generate meaningful business intelligence. The module takes a data driven approach to operation of data analysis.

Module Aim The module aims to prepare students for undertaking analysis of large data sets, and to make students aware and informed on the benefits and applications of data mining for business or management.

Syllabus Introduction to data mining Data Input: concepts, instances and attributes Data output: knowledge representation (linear models, rules, trees) Simple Algorithms Statistical modelling Validation and evaluating output Applied data mining: decision trees, classification rules, association rules Extended linear modelling and prediction Data transformation

Assessment Description 2 x Individual coursework plans of no more than one side of A4 - project report on data mining exercise (5% each) 2 x Individual coursework project report on data mining exercise (45% each) Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: None (modules you cannot take if you take this module)

3

Module Code: MN-D002

Module Title: Independent Project

Level: D Credits: 60

Semester: TB3 Contact hours: 9 Contact Description: 4 x 1-hour briefing session; 6 x 30 minute individual supervision meetings

Module Synopsis The report documents the result of an independently researched analysis of a finance related topic or issue. It is intended to provide a degree of synthesis of the various course components. The student should be able to demonstrate he/she is able to apply knowledge and skills gained and that he/she has an understanding of the wider context of the programme of study undertaken.

Module Aim The project provides students with an opportunity to engage in independent study.

Syllabus Briefing/introduction The project structure/process Conducting a literature review Report writing

Assessment Description 5% Project proposal. 95% individual report of 15,000 words; this is a maximum limit and solely for the main text. The word limit excludes appendices (if any), and essential footnotes, but includes introductory parts and statements, a bibliography and index. Pre-requisite Modules: None (modules you must complete and pass before taking this module)

Co-requisite Modules: None (modules you must take in combination at this level)

Non-requisite: MN-D001 (modules you cannot take if you take this module)