mortgages. home loans home loans are referred to as mortgages first home loans offered were in to...

TRANSCRIPT

Mortgages

Home Loans

• Home Loans are referred to as mortgages

• First home loans offered were in to 1930’s

• 67% of all American own their homes

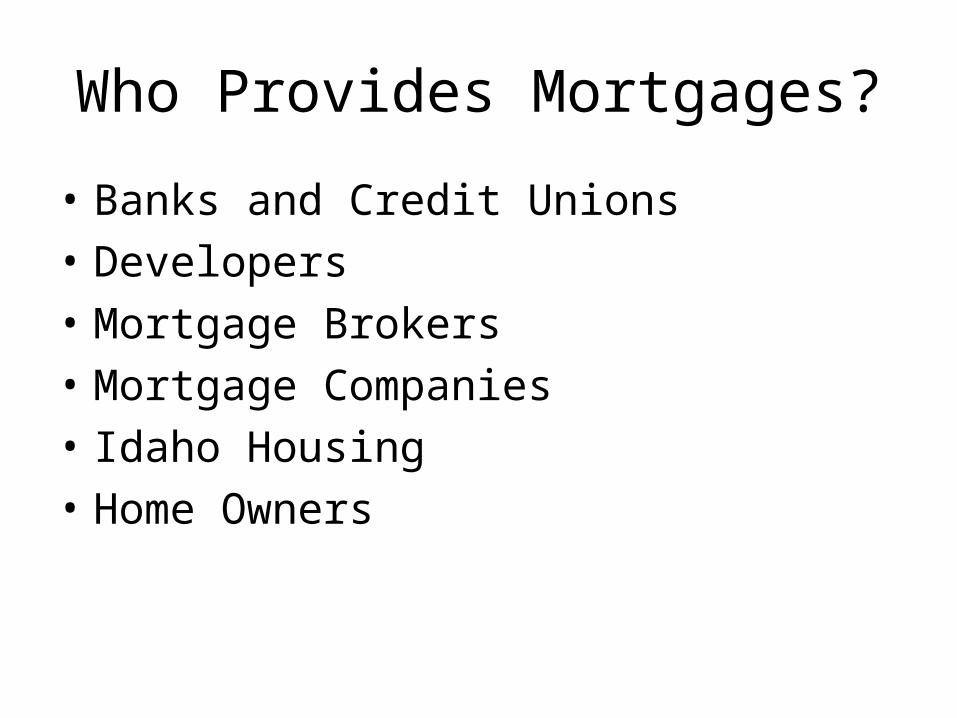

Who Provides Mortgages?

• Banks and Credit Unions

• Developers

• Mortgage Brokers

• Mortgage Companies

• Idaho Housing

• Home Owners

Prequalification

• Preapproved for a mortgage before you begin looking for a home– Let’s you know a head of time how much

house you can afford– Tailors your search for houses in the right

price range– Strengthens your bargaining position – less

contingencies, the easier the offer is to accept– Can lock you in to a good interest rate

Down Payment

• Amount required to put up to purchase a home– Conventional loans are given through

commercial banks and require a 20% down payment

– VA are given through the Veteran’s Administration and require no down payment

– HUD requires a 3% down payment – FHA varies in the amount down

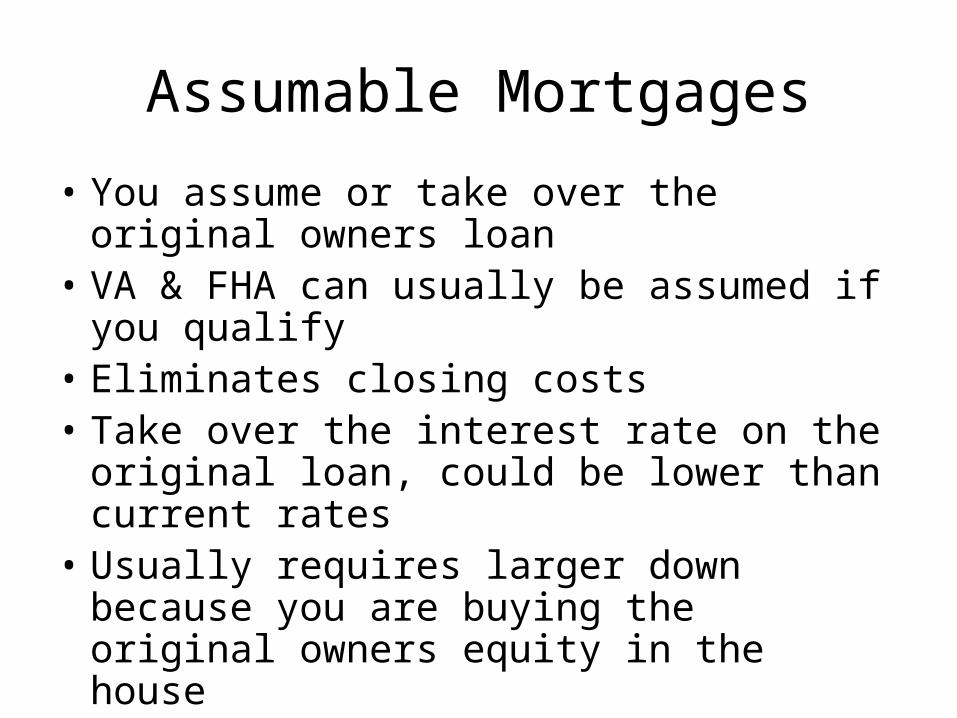

Assumable Mortgages

• You assume or take over the original owners loan

• VA & FHA can usually be assumed if you qualify

• Eliminates closing costs • Take over the interest rate on the original

loan, could be lower than current rates• Usually requires larger down because you

are buying the original owners equity in the house

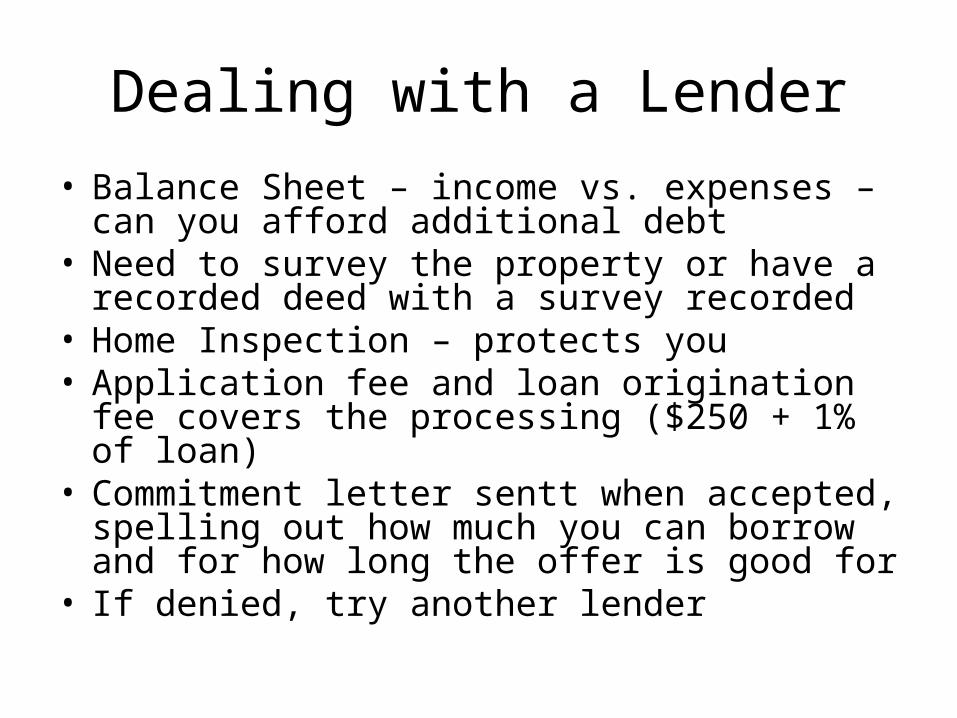

Dealing with a Lender

• Balance Sheet – income vs. expenses – can you afford additional debt

• Need to survey the property or have a recorded deed with a survey recorded

• Home Inspection – protects you• Application fee and loan origination fee covers

the processing ($250 + 1% of loan)• Commitment letter sentt when accepted, spelling

out how much you can borrow and for how long the offer is good for

• If denied, try another lender

Closing • You will write many checks, sign your name

countless times, and sift through mounds of paper

• But when you walk away with the keys to your house – the American dream is realized for you

• You will receive a good faith estimate a couple days before the closing

• Title Insurance• Proof of Insurance• Points• Filing Fees• Real Estate Taxes• Escrow for taxes and insurance

Mortgage Rates

• Fixed or Conventional – set at closing– Don’t benefit from change in interest rates

over time– Principal and interest are paid in equal

monthly payments over installments of 15-30 years

– Pay one extra payment a year at the same time every year – 30 year loan paid off in 15 years

ARM

• Adjustable Rate Mortgage– Rates change on a regular basis – usually

once a year– Why we have foreclosure problem today– Tied to index like Treasury Bills– Get you with teaser rates of 5%, then raise up

to 14.5% over time– Hard to budget for

Refinancing

• When interest rates go down – may want a lower rate

• Needs to be at least 2% lower than current rate

• Can help you consolidate if you have equity – but don’t roll credit card into this unless you are stupid, desperate, or have no brain left in your head

Foreclosure

• When you fall behind in your mortgage and the bank is repossessing your home

• Usually you are six months in arrears

• Don’t ignore the problem - it is an elephant in your living room

• Contact your lender right away and try to work something out with your lender

• Don’t fall for some foreclosure scam artist

• You will feel vulnerable – seek help – liquidate assets if you can first

Second Mortgage

• Use your home as collateral for a loan for other things– Home Improvements– Consolidate credit card loans– Car loan – deductible on taxes – car loans are

not– Usually not for as long as a mortgage– Can be very expenses – add to your debt

Reversible Mortgage

• The RAM is a special type of loan that works in reverse — the lender makes monthly payments to you based on the equity of your home.

• These instruments are gaining popularity with older homeowners who want to use the equity in the home to supplement their income.

• The lender will appraise the home value and make a home loan based upon a percentage of the current value.

• The homeowner retains ownership. The lender will then allow you one of four payment options:– Lump-sum payment– Equal monthly annuity payments to the homeowner

for up to the amount of equity in the home. The number and schedule payments depend on the equity in the home and age of the recipient.

– An equity line of credit that the borrower can draw upon as needed

– Combination of annuity payments and equity line

• No payments will be required as long as the borrower remains in the home.– Payments are made when the homeowner dies,

sells, refinances, or moves.

Selling Your Home

– Average person stays in home from 5-7 years– Find out what your house is worth – free

market estimates– Make it look good inside and out– If it doesn’t sell within the first month – you’re

too high

• Profit or Loss – Profit (Capital Gains)– Basis – what you paid for your house,

including improvements, etc.– Selling Price