mortality rates and improvement over …...actuarial society 2016 convention 23 –24 november...

TRANSCRIPT

Actuarial Society 2016 Convention 23 – 24 November 2016

MORTALITY RATES AND IMPROVEMENT OVER

TIME AT ADVANCED AGES IN SOUTH AFRICA

Ronald Richman and Rob Dorrington

Actuarial Society 2016 Convention 23 – 24 November 2016

Agenda

1. Background

2. Method

3. Results

4. Conclusion

2

Actuarial Society 2016 Convention 23 – 24 November 2016

Background• Why should actuaries care about population mortality rates at

the older ages?

• Data on insured lives not always sufficient to estimate:

• level and trend at older ages

• stochastic models of mortality

• Valuation of cashflows for damages use population mortality

rates

• In South Africa actuaries need to use professional/expert

judgement:

• Data for SAIML/SAIFL98 not robust after age 85 and rates

approximated

• Mortality improvement rates from other countries often used as a

proxy

• SCR Longevity in SAM relies on work performed for SII

• Reliant on old population lifetables (SALT85) for damages

• Why not use the population data to calculate rates?3

Actuarial Society 2016 Convention 23 – 24 November 2016

Use census data to estimate mx

• log mx for

males

• Flat or

decreasing

with age

• Expect straight line

on log

scale if

follows

Gompertz

• Similar for

females

• What has

gone

wrong?4

0.02

0.20

2.00

70

73

76

79

82

85

88

91

94

97

10

0

10

3

10

6

mx

Age last birthday on 10 October

Males

1996 raw

2001 raw

2011 raw

Actuarial Society 2016 Convention 23 – 24 November 2016

Census data are messy• Misreporting at

older ages

• Heaping on

years of birth

ending on ‘0’,

1914 & 1918

• Often, too many

enumerated at

older ages (183 at 115+)

producing rates

that may be too

low

• Population

estimates

uncertain5

Actuarial Society 2016 Convention 23 – 24 November 2016

Agenda

1. Background

2. Method

3. Results

4. Conclusion

6

Actuarial Society 2016 Convention 23 – 24 November 2016

The plan• Death data often reported with greater accuracy than

population data (ID number)

• Deaths are not fully reported in South Africa so correct

the data before use – death distribution methods (see

paper for details and references)

• Reconstruct the population using only the death data –

the method of extinct generations (EG):

• Not feasible to wait for deaths to occur, so project the

future deaths based on the past deaths – How?

7

xi

ciDcxN ),(),(

Actuarial Society 2016 Convention 23 – 24 November 2016

Similar problems, similar solutions

1. Predict future deaths occurring for each

cohort based only on past death information

2. Predict outstanding claims to be reported in

the future for each accident period based

only on past claim payments

• Demographic solution: NEG Methods (NEG)

• Actuarial solution: Chain ladder and

extensions

Actuarial Society 2016 Convention 23 – 24 November 2016

Triangles

9

Actuarial Society 2016 Convention 23 – 24 November 2016

GAM Model

10

txfxfxtf

eODPD

txt

txtxt

*)()()(

)(~

,

,,

• Chain ladder = ODP

GLM

• Use GAM (GLM plus

smoothing) to model the deaths directly

(NEG-GAM)

• Implicitly model

mortality as the

percentage of the

cohort dying at

each age

• Insight into chain

ladder method

• Period trend

)(| xfqxt )(),( xtfcxN

txf *)(

Actuarial Society 2016 Convention 23 – 24 November 2016

Control variables

11

txxt

txt

tx

txfxfxtf

eODPD txt

*)()()(

)(~

,

,,

Legend

Year of birth heaping -

Age heaping -

Completeness -

xt

x

t

Actuarial Society 2016 Convention 23 – 24 November 2016

Agenda

1. Background

2. Method

3. Results

4. Conclusion

12

Actuarial Society 2016 Convention 23 – 24 November 2016

National Completeness• (1) – Logistic

curve fit

through point

estimates of

completeness

• (2) – Peaks at

87%

• (3) – Falls

mainly due to late reported

deaths

• Warning – do

not use death

data unless

corrected!

13

(1)

(2)

(3)

50%

55%

60%

65%

70%

75%

80%

85%

90%

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

National

Actuarial Society 2016 Convention 23 – 24 November 2016

National Population 70+• Sensible

trajectory

• Higher than

earlier censuses

– expected since these

were

undercounted

relative to 2011

Census

• Too low

compared to

Census 2011?

• Modelling

issue

• Census

overcount14

-

500 000

1 000 000

1 500 000

2 000 000

2 500 000

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

20

15

Po

pu

lati

on

est

ima

tes i

n i

nte

rva

l 7

0+

Year

National

Census

Survey

AltMYE

ASSA

StatSA

UNPD

USCB

NEG - GAM

Actuarial Society 2016 Convention 23 – 24 November 2016

Age exaggeration• Ratio of

estimated

population to

census

population in

increasing

open intervals

• Age

exaggeration from around

79

• Explains

“flattened” mortality rates

15

0%

20%

40%

60%

80%

100%

120%

72

75

78

81

84

87

90

93

96

99

10

2

10

5

10

8

11

1Rat

io o

f N

EG-G

AM

to

Ce

nsu

s at

age

s x+

Age last birthday on 10 October

National

1996

2001

2011

Actuarial Society 2016 Convention 23 – 24 November 2016

mx - Males• Sensible

ranking of

mortality rates

at younger

ages

• Cross-over at

ages 86-88

• High rates at

younger ages should imply

high rates at

older ages

• Unless select

effect (little

evidence)

16

0.02

0.20

2.00 7

0

73

76

79

82

85

88

91

94

97

100

103

106

109

mx

Age last birthday

Males

African

Indian

Coloured

White

National

Actuarial Society 2016 Convention 23 – 24 November 2016

mx - Females• Similar points to

males

• White Female

mortality seems

too high at

highest ages

• Crosses over

rates for

males at age

101

• Would expect

rates to

remain lower

than males

over whole

age range

17

0.02

0.20

2.00 7

0

73

76

79

82

85

88

91

94

97

100

103

106

109

mx

Age last birthday

Females

African

Indian

Coloured

White

National

Actuarial Society 2016 Convention 23 – 24 November 2016

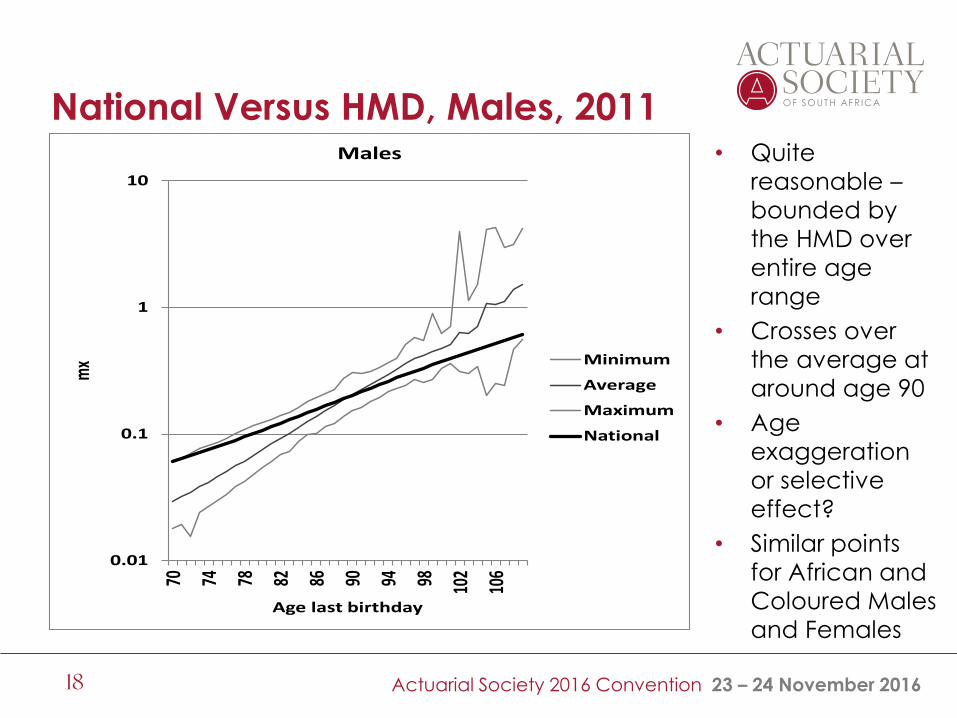

National Versus HMD, Males, 2011• Quite

reasonable –

bounded by

the HMD over

entire age

range

• Crosses over

the average at

around age 90

• Age

exaggeration

or selective

effect?

• Similar points

for African and

Coloured Males

and Females

18

0.01

0.1

1

1070 74 78 82 86 90 94 98 10

2

106

mx

Age last birthday

Males

Minimum

Average

Maximum

National

Actuarial Society 2016 Convention 23 – 24 November 2016

Indian Versus HMD, Females, 2011• Reasonable –

rates remain

high until oldest

ages

• Tends towards

and crosses

over average

rates in HMD at

oldest ages

• Similar

comments for

Whites and

Indian males

19

0.01

0.1

1

1070 74 78 82 86 90 94 98 10

2

106

mx

Age last birthday

Females

Minimum

Average

Maximum

Indian

Actuarial Society 2016 Convention 23 – 24 November 2016

Preliminary mortality improvement• Please do not use

without permission

• Rates appear

reasonable for all

groups at ages 70-

79

• Improvements since

1985 shown at these

ages

• Only a marginal

decline in mortality

nationally

• Improvements for

males and females

comparable,

except for white

males vs females –

needs more

investigation20

Group SexRate of

improvement per annum

African Male -0.30%

African Female -0.30%

Asian Male 1.70%

Asian Female 1.30%

Coloured Male 2.10%

Coloured Female 2.20%

White Male 1.40%

White Female 0.70%

National Male 0.50%

National Female 0.00%

Weighted Average Male 0.21%

Weighted Average Female 0.13%

Actuarial Society 2016 Convention 23 – 24 November 2016

White Versus Insured, Males, 2011• Significantly higher

than SAIML98

• Lower than PA(90)

rates until age 79

• Lower than (but

quite close to) the

rates in Table 1 of

Koch (2016) at all

ages

• Population rates

lower/close to

rates used by

actuaries to value

retirement benefits

and damages for

“select”

populations

21

0.01

0.10

1.00

70

73

76

79

82

85

88

91

94

97

10

0

10

3

10

6

mx

Age last birthday

Males

NEG-GAM 2011

D&T

PA90

Koch - Table 1

Actuarial Society 2016 Convention 23 – 24 November 2016

Agenda

1. Background

2. Method

3. Results

4. Conclusion

22

Actuarial Society 2016 Convention 23 – 24 November 2016

Conclusion• SA death data provide valuable information to actuaries

once corrected using demographic methods

• NEG or “Exposure free” modelling in regression framework provides a powerful framework for modelling mortality at

the older ages in South Africa…

• … and perhaps for developed countries as well?

• Issues requiring more investigation:

• Population estimates perhaps too low

• Rates crossing over

• Professional need to acknowledge uncertainty/expert

judgement:

• Uncertainty around level and trend

• 1-in-200 Longevity risk capital

23