morgan stanley tmt conference - capgemini · 1 morgan stanley tmt conference – nov 06 agenda...

TRANSCRIPT

Morgan Stanley TMT Conference Barcelona, November 17, 2006

Paul Hermelin, CEO

1

Morgan Stanley TMT Conference – Nov 06

Agenda

Business Momentum end of 06

Outsourcing margin recovery plan

Investing for the future (I3)

Kanbay acquisition

2

Morgan Stanley TMT Conference – Nov 06

Business Momentum end of 06

3

Morgan Stanley TMT Conference – Nov 06

We finish the year with a strong momentum

9.0%

8.7%

3 784

H1 2006

13.5%

12.4%

- 1.9%

- 1.8%

1 881

Q3 2006

11.0%

8.6%

3.3%

2.5%

1 915

Q2 2006

1 8696 9543 4821 8081 6743 4721 7641 708Amount in M€ (Published)

10.0%

9.4%

4.3%

3.3%

Q1 2006FY 2005

0.3%

H2 2005

7.4%

8.0%

Q4 2005

- 4.0%

- 5,1%

Q3 2005Q1 2005

2.3%

3.3%

Q2 2005 H1 2005

Year-on-Year Organic Growth

Year-on-Year Current Growth

Sequential Organic Growth

Sequential Current Growth

Revenue quarterly evolution in M€

1708

1764

1674

1808

18691915 1881

1400

1600

1800

2000

Q1 05 Q2 05 Q3 05 Q4 05 Q1 06 Q2 06 Q3 06

At constant rates and perimeter

4

Morgan Stanley TMT Conference – Nov 06

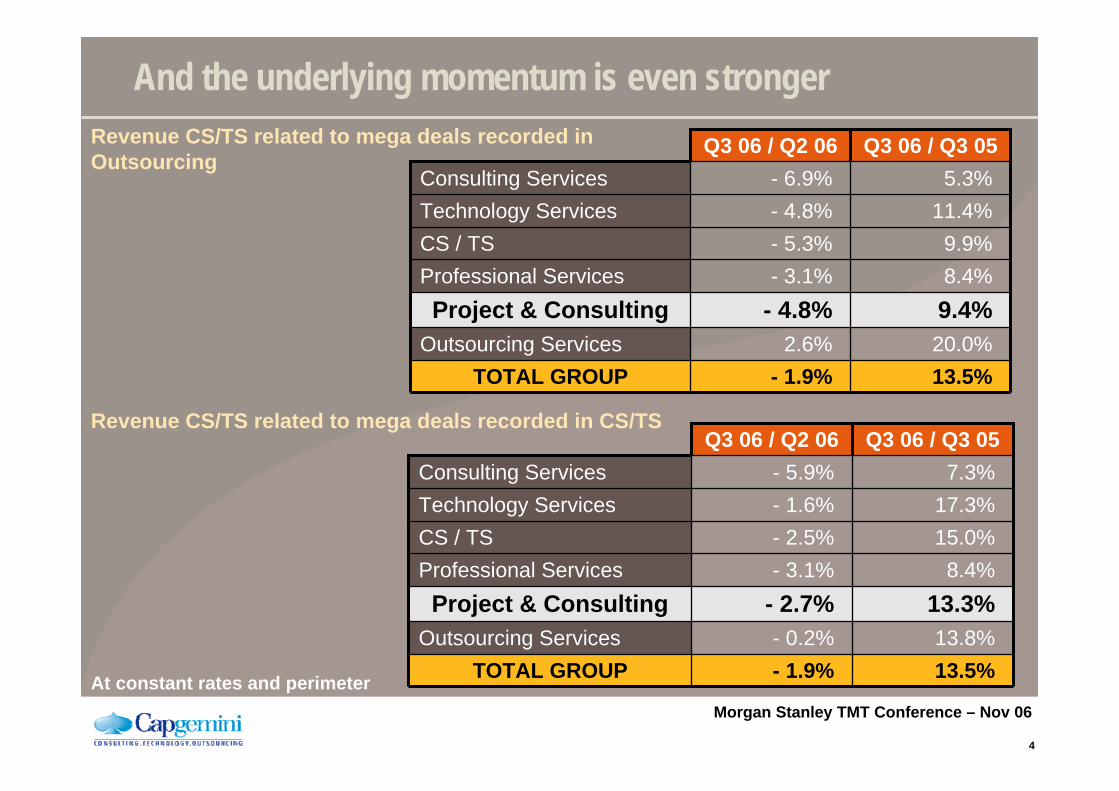

9.9%- 5.3%CS / TS

- 1.9%2.6%

- 4.8%- 3.1%

- 4.8%- 6.9%

Q3 06 / Q2 06

13.5%TOTAL GROUP20.0%Outsourcing Services9.4%Project & Consulting8.4%Professional Services

11.4%Technology Services5.3%Consulting Services

Q3 06 / Q3 05Revenue CS/TS related to mega deals recorded in Outsourcing

And the underlying momentum is even stronger

15.0%- 2.5%CS / TS

- 1.9%- 0.2%

- 2.7%- 3.1%

- 1.6%- 5.9%

Q3 06 / Q2 06

13.5%TOTAL GROUP13.8%Outsourcing Services

13.3%Project & Consulting8.4%Professional Services

17.3%Technology Services7.3%Consulting Services

Q3 06 / Q3 05

At constant rates and perimeter

Revenue CS/TS related to mega deals recorded in CS/TS

5

Morgan Stanley TMT Conference – Nov 06

Utilisation has not peaked yet but is already quite good

50

60

70

80

90

62

67 6665

66

69

66

Q1 Q2 Q3 Q4 Q1 Q2 Q3

807978 79 7979

80

Q1 Q2 Q3 Q4 Q1 Q2 Q3

86 86 85 8685

8685

Q1 Q2 Q3 Q4 Q1 Q2 Q3

Consulting Services Technology Services Professional Services

2005 2006

At constant rates and perimeter – with India

2005 2006 2005 2006

6

Morgan Stanley TMT Conference – Nov 06

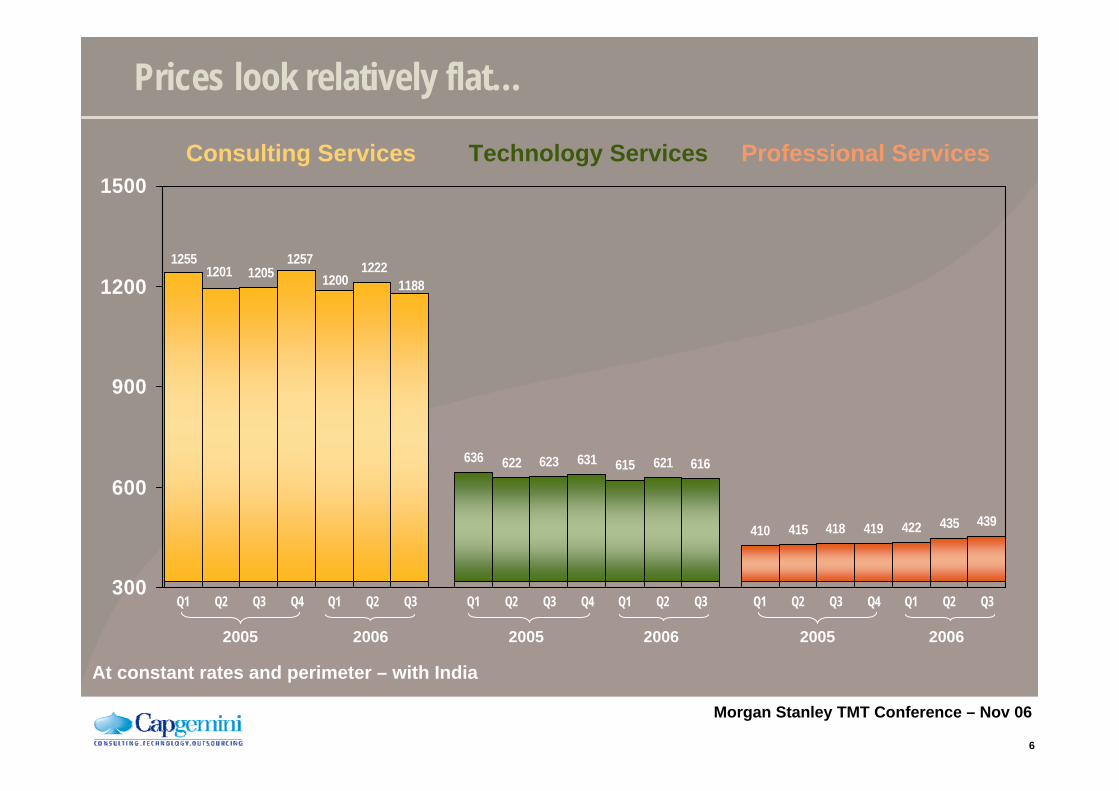

Prices look relatively flat…

300

600

900

1200

1500

1200 118812221257

1201 12051255

Q1 Q2 Q3 Q4 Q1 Q2 Q3

636 622 623 631 615 621 616

Q1 Q2 Q3 Q4 Q1 Q2 Q3

410 415 418 419 422 435 439

Q1 Q2 Q3 Q4 Q1 Q2 Q3

Consulting Services Technology Services Professional Services

At constant rates and perimeter – with India

2005 2006 2005 2006 2005 2006

7

Morgan Stanley TMT Conference – Nov 06

661

652

662

673

663

677

682

640

660

680

700

Q1 Q2 Q3 Q4 Q1 Q2 Q3

Technology Services Excluding India

2005 2006

410

415418 419

422

435439

400

420

440

460

Q1 Q2 Q3 Q4 Q1 Q2 Q3

Professional Services

2005 2006

But onshore prices are up in Technology Services, and scale effects hide the strong Local Professional Svces progress!

At constant rates and perimeter

8

Morgan Stanley TMT Conference – Nov 06

Sustained bookings hint on future growth

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

Q1 04 Q2 04 Q3 04 Q4 04 Q1 05 Q2 05 Q3 05 Q4 05 Q1 06 Q2 06 Q3 06

OutsourcingProject & Consulting

M€

484

2 860

284

1 943

277490

320

1 1171 760

1 078 1 178 929 1 255 1 119 1 226 953 1 274 1 230

329

1 376

At constant rates and perimeter

406

1 117

1 562

4 038

1 213

3 198

1 3961 716

1 273

2 391

2 990

1 7051 523

9

Morgan Stanley TMT Conference – Nov 06

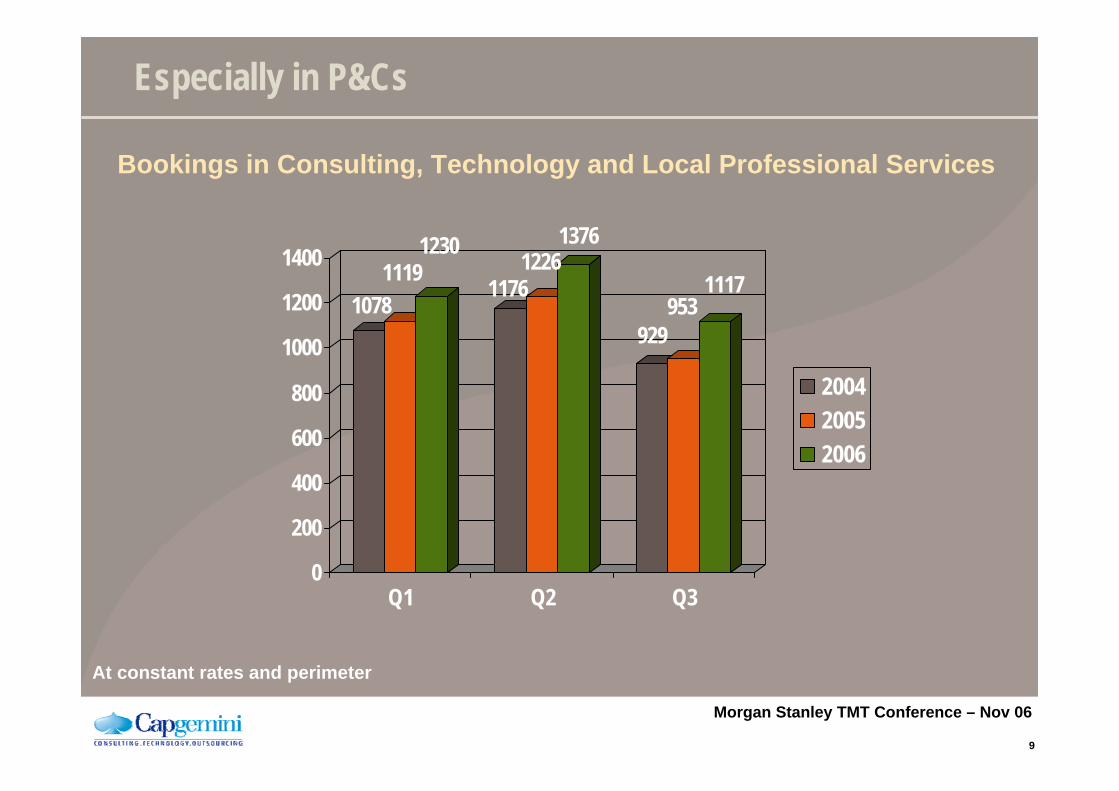

Especially in P&Cs

10781119

1230

11761226

1376

929953

1117

0

200

400

600

800

1000

1200

1400

Q1 Q2 Q3

200420052006

At constant rates and perimeter

Bookings in Consulting, Technology and Local Professional Services

10

Morgan Stanley TMT Conference – Nov 06

Outsourcing margin recovery plan

11

Morgan Stanley TMT Conference – Nov 06

The Margin Acceleration Plan was a key challenge for the year: we are on track

Creation of IM remote management center in Poland with 264 seats900 additional positions created in India since beginning ‘06

Mainframe and hardware rationalization in multiple regionsSoftware renegotiation within France and UKContractor price reductions in various countries and large accounts

Successful renegotiation of four service contractsEnding or already exited five service contractsBusiness extension or expansion within to improve overall account margin19/20 of 2005 bottom quartile accounts improved; nine fully profitable

Migration of internal F&A in UK to Rightshore™ location

People restructuring in select countriesClosure of sites in UK and Benelux regions

Objective: 8% Divisional MarginObjective: 8% Divisional Margin

Support FunctionSupport Function 1 – 1.5%1 – 1.5%

Rightshore™Rightshore™ 1.5 – 2%1.5 – 2%

IndustrializationIndustrialization 1 – 1.5%1 – 1.5%

ProcurementProcurement 1 – 1.5%1 – 1.5%

RenegotiationRenegotiation 0.5%0.5%

Business MixBusiness Mix TBDTBD

On TrackOn

Track

Achieved2006

Achieved2006

Achieved2006

Achieved2006

Visibility2007

Visibility2007

Visibility2007

Visibility2007

Acquisition of majority stake in Indigo, Unilever’s F&A platform in IndiaNIS outsourced to BTSold French Break/Fix business

LeversLeversMid-termDivisional

Margin Impact

Mid-termDivisional

Margin Impact

12

Morgan Stanley TMT Conference – Nov 06

Even though the Schneider contract was even more difficult thanexpected earlier in the year, we will meet our objectives

-0.2%

0.6%

H1 05

2.7%

5.6%

H2 05

3.3%

6.0%

H1 06

≃ 4.0%Including Schneider

≤ 7.0%Excluding Schneider

FY 06

Strong margin improvement excluding Schneider

Schneider still a significant drag on profitability

(at divisional margin level)

13

Morgan Stanley TMT Conference – Nov 06

Outsourcing will continue to be a key driver for our margin expansion

Objectives> 7.5% full year Divisional Margin (approximately 5.5% Operating Margin) excluding Schneider5 - 5.5% full year Divisional Margin including Schneider

Restructuring

€ 35 m

90%-95% Cash

20 month payback

14

Morgan Stanley TMT Conference – Nov 06

Investing for the future (I3)

15

Morgan Stanley TMT Conference – Nov 06

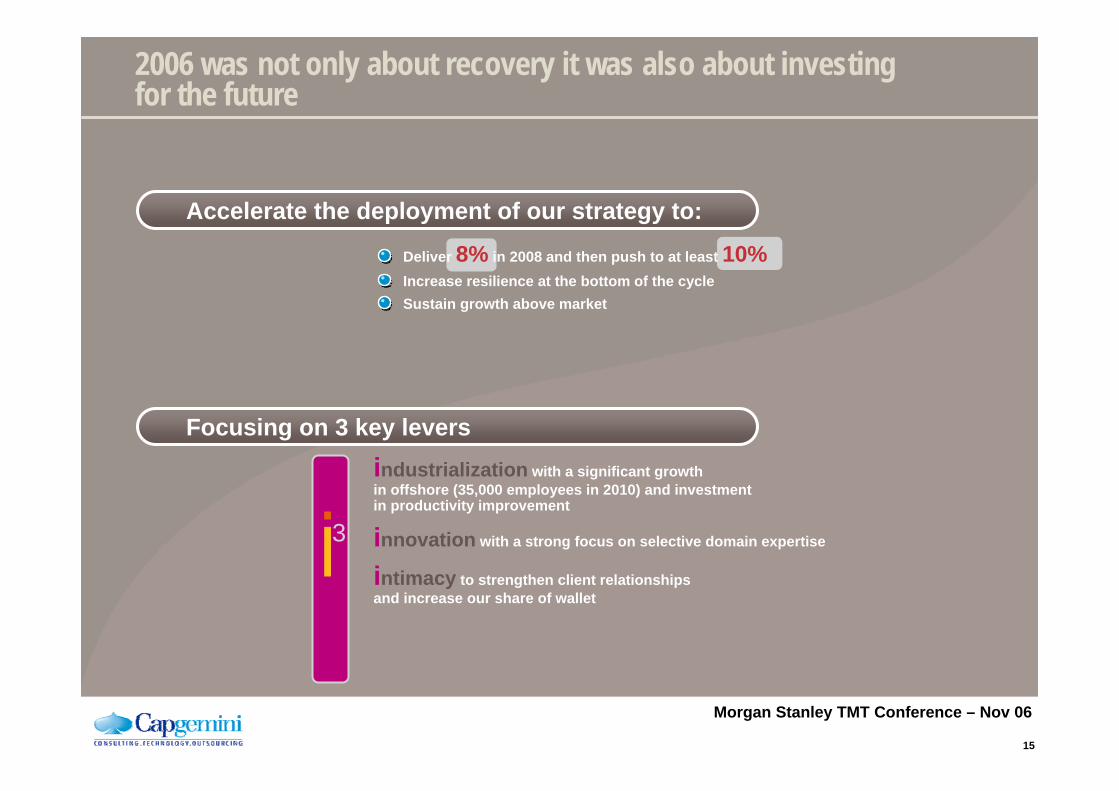

2006 was not only about recovery it was also about investingfor the future

3

Deliver 8% in 2008 and then push to at least 10%Increase resilience at the bottom of the cycleSustain growth above market

industrialization with a significant growth in offshore (35,000 employees in 2010) and investmentin productivity improvement

innovation with a strong focus on selective domain expertise

intimacy to strengthen client relationships and increase our share of wallet

Accelerate the deployment of our strategy to:

Focusing on 3 key levers

16

Morgan Stanley TMT Conference – Nov 06

Kanbay acquisition

17

Morgan Stanley TMT Conference – Nov 06

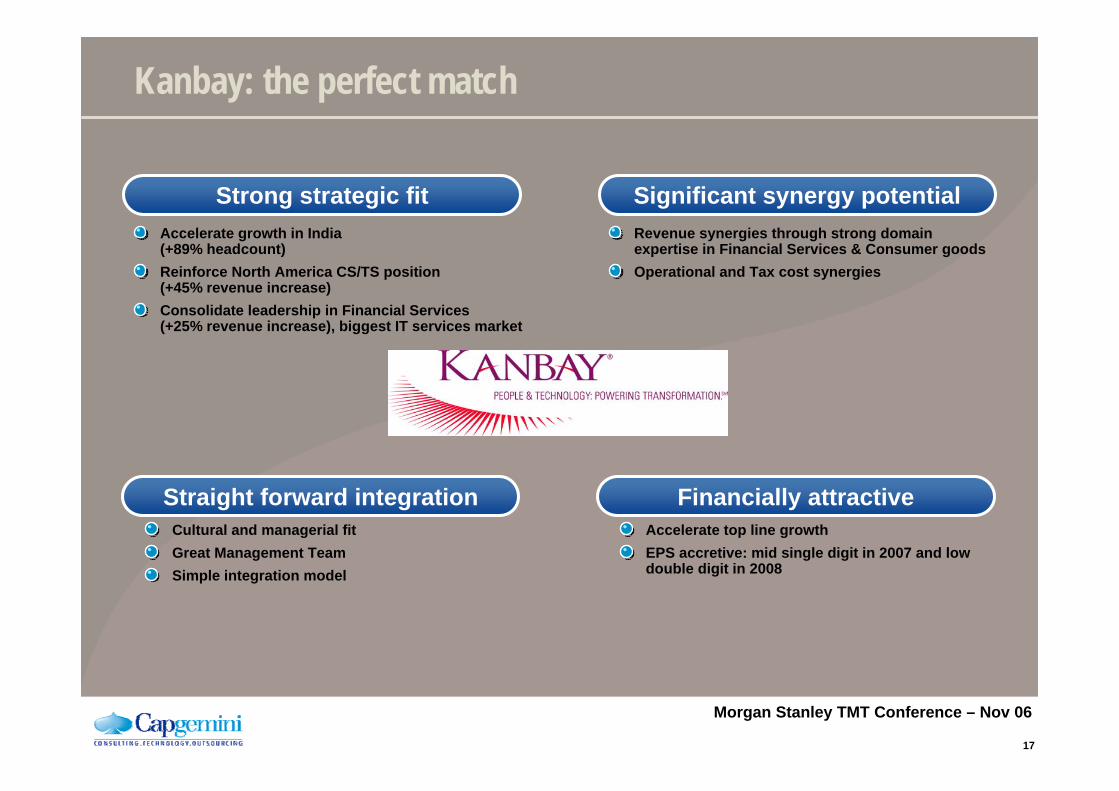

Kanbay: the perfect match

Revenue synergies through strong domain expertise in Financial Services & Consumer goodsOperational and Tax cost synergies

Cultural and managerial fitGreat Management TeamSimple integration model

Accelerate top line growthEPS accretive: mid single digit in 2007 and low double digit in 2008

Accelerate growth in India (+89% headcount)Reinforce North America CS/TS position(+45% revenue increase)Consolidate leadership in Financial Services (+25% revenue increase), biggest IT services market

Strong strategic fit Significant synergy potential

Straight forward integration Financially attractive

18

Morgan Stanley TMT Conference – Nov 06

Kanbay is not only about growing staff in India, it is also another way to use offshore

Strategic alignment with client businessIntegration of industry and technology expertise for innovativebusiness focused solutionsValue-based delivery modelSelf-enriching knowledge base

Value-BasedGlobal Delivery Model

Integrated Global Delivery Model

Basic Global Delivery ModelEasy to establish, low upfront planning needed

Requires high involvement from customer management “Over-the-wall” delivery process – “blame games” followHard concerns like rate, technology, skills are the primary drivers

Core project teams retained across projectsIntegrated usage of Kanbay near-shore, onsite, offshore and clientteams to maximize leverage – over 1:4Multi-layered relationship alignment between Kanbayand customers including goal-sharing

Next-Gen value based global delivery model

Engagement-based delivery leveraginghuman assets

Transactional project based onsite-offshoredelivery model

19

Morgan Stanley TMT Conference – Nov 06

As in any integration there are risks but everything is made to limit them

Preserve and leverage Kanbay deep domain expertise and growth momentum

Speed up integration by creating a Financial Services BU covering NA + UK + FS IndiaLed by Raymond Spencer reporting directly to Capgemini CEOFinancial Services India Platform to be leveraged by Capgemini European clients

Integrate Consumer Products business in Capgemini NACreate a Consumer Products BU led by Rodney Rogers reporting to Salil Parekh (CEO NA CS/TS)Kanbay to leverage Capgemini’s strong Indian platform

Financial services (5,500 FTE): Integrated with new Financial Services BUNon Financial Services (primarily current Capgemini India, 6,500 FTE)

Financial Services

North America Non Financial Services

Capgemini India*

*Estimated end 2006 headcount

20

Morgan Stanley TMT Conference – Nov 06

We are exiting 2006 with a strong business momentum

Outsourcing well on track to normality

The launch of marks the end of our turnaround story

Kanbay is a key investment for our future

Summary

3

Morgan Stanley TMT Conference Barcelona, November 17, 2006

Paul Hermelin, CEO