monthly review and comment - credit suisse

TRANSCRIPT

Monthly Review and Comment

April 2011

Monthly Review and Comment

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

June 2016 Americas / United States

EQUITY RESEARCH Monthly Review and Comment

June 2016

Monthly Review and Comment 2

Table of Contents U.S. FOCUS LIST 3 COVERAGE AND OPINION CHANGES 4 ANALYST STOCK PICKS BY INDUSTRY 5 INVESTMENT STRATEGY AND ECONOMICS (excerpts from recently published macroeconomic reports) 7

Key Macro Forecasts 7 U.S. Economics 8 U.S. Equity Strategy 9 Global Equity Strategy 11 Global Energy Economics 12 Accounting & Tax 13

INDUSTRY REPORTS (excerpts from recently published industry and company research) 14 Consumer Discretionary 15

Media 15 Restaurants 16 Global Luxury Goods 17 Department Stores 18 Home Improvement 19 Specialty Softlines 21

Consumer Staples 23 Food and Drug Retailing 23

Energy 25 Canadian Energy 25 Offshore Services 26 Marine 27 Oilfield Services and Equipment 28

Financials 30 U.S. Large- and Mid-Cap Banks 30 April Real Estate Agents Survey 31 Canadian Banks 32 U.S. Brokers 33

Health Care 34 Hospital Volume Tracker 34 Global Pharmaceuticals 35 Health Care Technology and Distribution 36 Animal Tracks 37

Industrials 38 North American Railroads 38 Electrical Equipment and Multi-Industry 39

Materials 40 Agricultural Sciences Sector 40

INDUSTRY VALUATION TABLES 41 Consumer Discretionary 42

Apparel, Footwear & Specialty Softlines 42

Homebuilding 43 Media, Canada 44 Movie Exhibitors 44 Off Price Retail 45 Restaurants 45 Retail, Mall Anchors 46 Retail, Mass Merchants 46 Specialty Hardlines 47 Travel & Leisure 48 U.S. Media, Cable & Satellite 48

Consumer Staples 49 Agricultural Products & Agribusiness 49 Drug & Food Retail & General

Merchandise Stores 49 Drug & Food Retail, Canada 50 Packaged Foods 51

Energy 52 Alternative Energy 52 Independent Refiners 53 Integrated Oil & Gas 53 Master Limited Partnerships 54 Oil & Gas E&P, Canada/

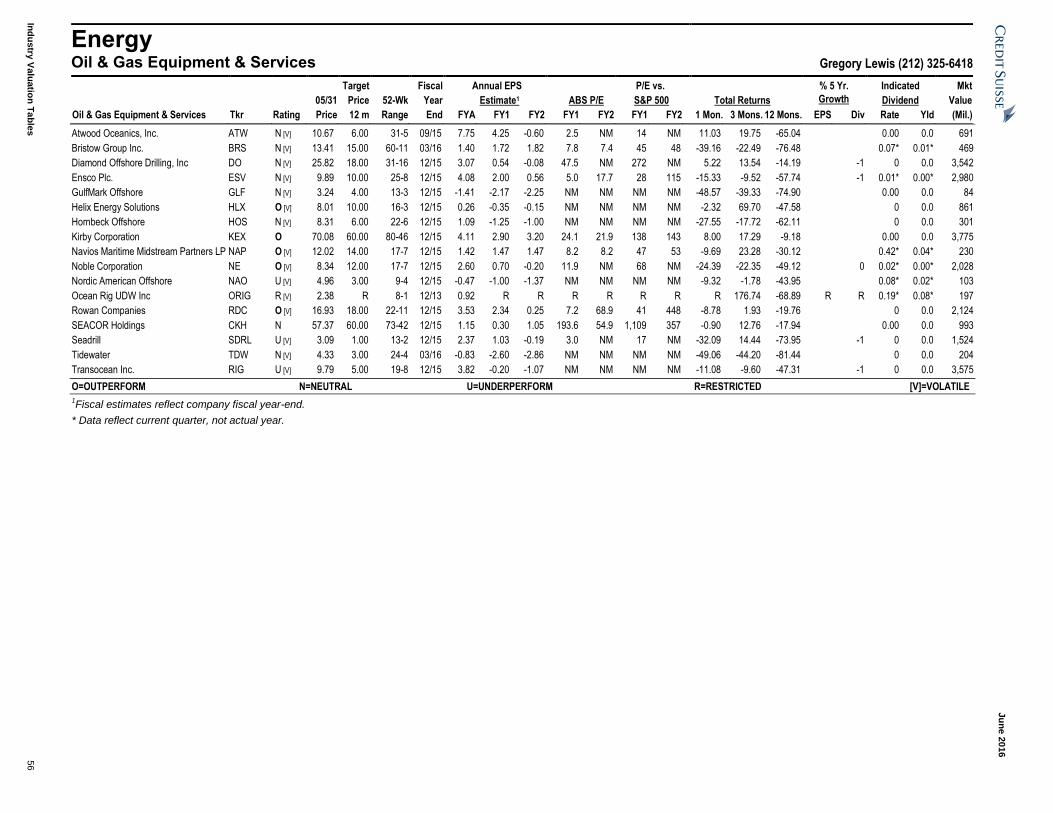

International 55 Oil & Gas Equipment & Services 56 Oil & Gas Exploration & Production 57

Oil & Gas, Canada 58 Oilfield Equipment & Services 59 Pipelines & Utilities 60

Financials 61 Asset Managers 61 Canadian Financials 62 Capital Markets 63 Diversified Financial Services 63 Large-Cap Banks 64 Mid-Cap Banks 64 Mortgage REITs, Servicers, Insurers,

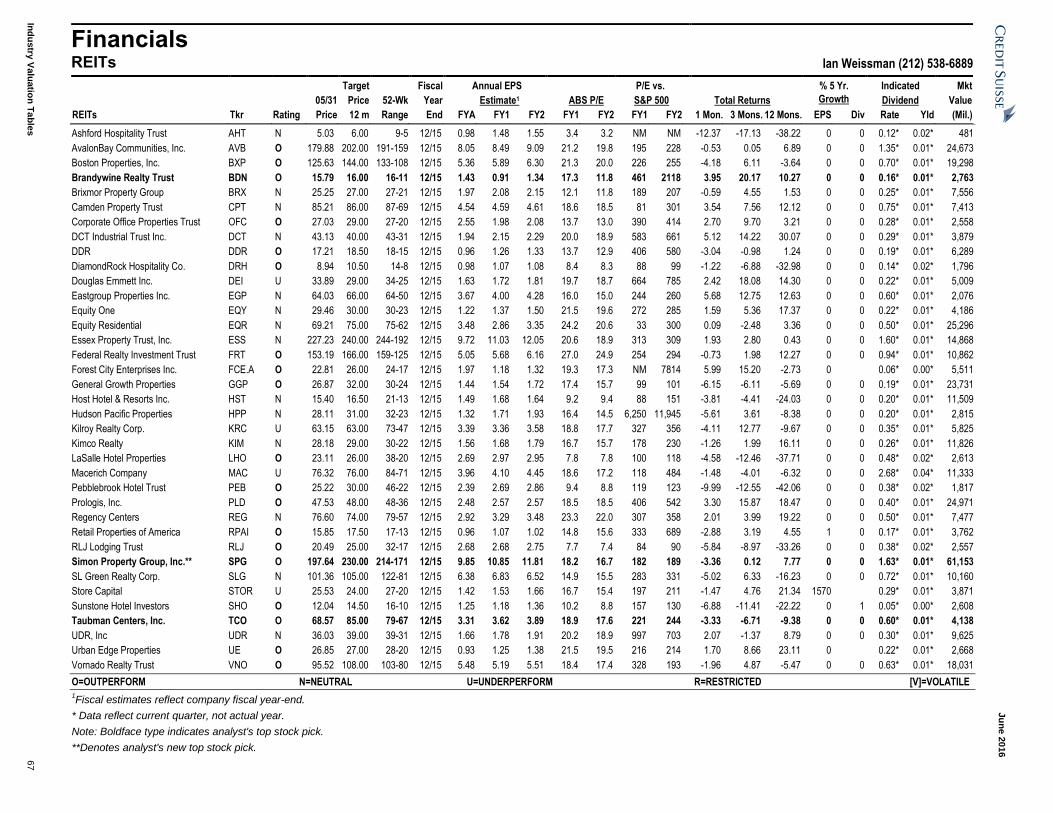

and BDCs 65 Property & Casualty Insurance 66 REITs 67 Specialty Finance 68

Global Services 69 Business & Professional Services 69 Knowledge Services 69 Payments & Financial Technology 70

Healthcare 71 Animal Health 71 Biotechnology 71 Healthcare Technology &

Distribution 72 Major Pharmaceuticals 73 Managed Care & Healthcare

Facilities 74 Medical Supplies & Devices 74

SMID-Cap Biotechnology 75 Industrials 76

Aerospace & Defense 76 Airfreight & Ground Transport 77 Airlines 78 Electrical Equipment &

Multi-Industry 79 Engineering & Construction 80 Environmental Services 80 Machinery 81 Ocean Shipping 81 SMID-Cap Aerospace & Defense 82 Trading Companies & Distributors 82

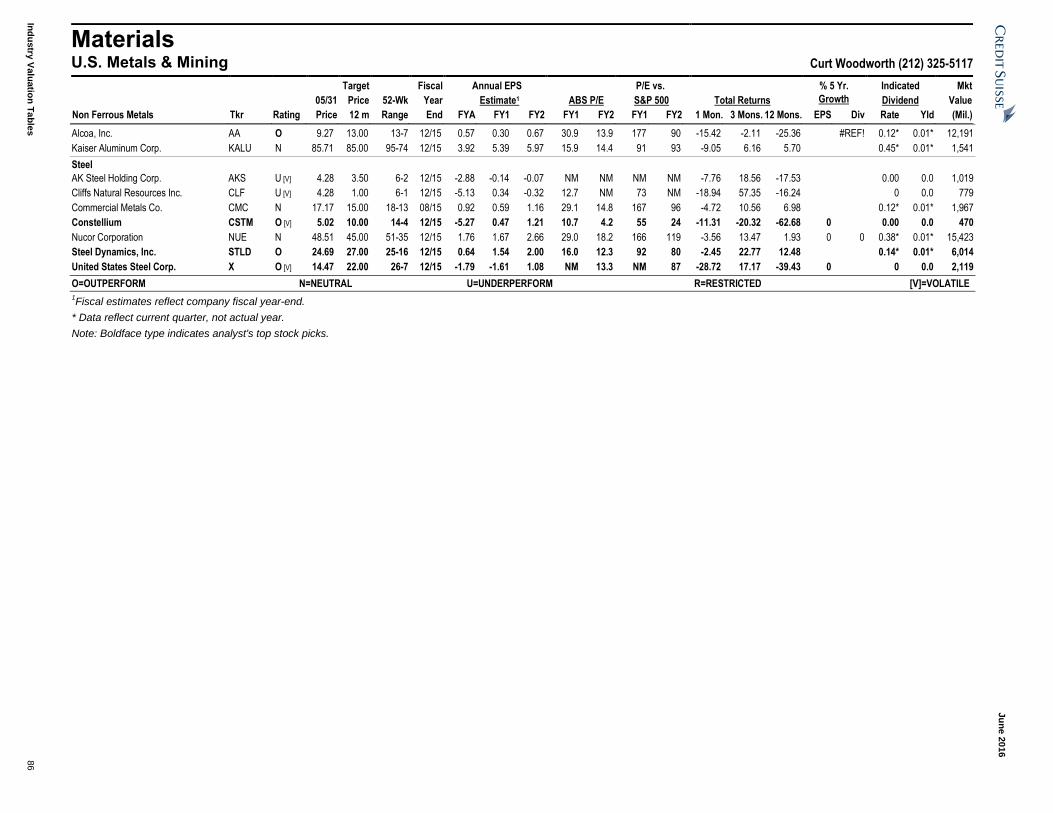

Materials 83 Metals & Materials, Canada 83 Paper & Packaging 83 Precious Metals 84 U.S. Chemicals & Agriculture 85 U.S. Metals & Mining 86

Technology 87 Internet 87 IT Hardware, Networking & Telecom

Equipment 88 Semiconductor Equipment 89 Semiconductors 89 Small- & Mid-Cap Software 90 Software 91

Telecommunication Services 92 Wireline 92

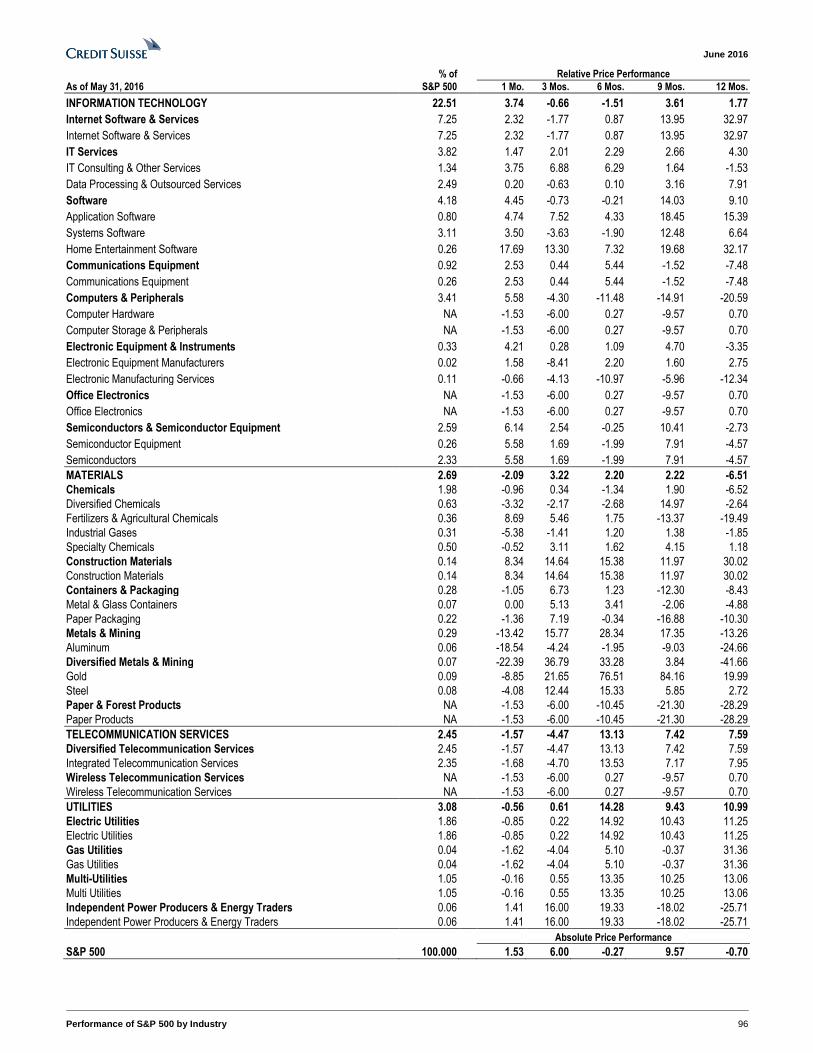

PERFORMANCE OF S&P 500 BY INDUSTRY 93 CONFERENCE CALENDAR 97 U.S. EQUITY RESEARCH ANALYSTS 98

June 2016

U.S. Focus List 3

U.S. FOCUS LIST

U.S. Focus List Performance Valuation

5/31 Total Return EPS Estimates1 P/E Ratios* Yield

Price YTD 3 Mos. 1 Mo. FY1 FY2 FY1 FY2 %

Equal Weighted Focus List 427.73 -0.15 13.14 -0.57 21.40 24.14 19.99 17.72 1.5

S&P 500 2096.96 2.59 6.00 1.53 122.65 130.58 17.10 16.06 2.2

DJIA 17787.20 2.08 5.47 0.08 1212.22 1299.47 14.43 13.69 2.7

Nasdaq Composite2 4948.05 -1.19 5.51 3.62 NA NA NA NA 1.3

Focus List Stocks3, 4

2016 Date Added or Return Potential

2015 Year-End 5/31 Relative Price EPS Estimates6

Ticker Date Price Price to S&P5 Price Return FY1 FY2 FY1 FY2 %

Consumer

21st Century Fox Inc. FOXA 5/23 28.19 28.88 0.01 40 38.5 1.74 2.25 16.57 12.84 1.0%

Hanesbrands Inc. HBI 12/31 29.43 27.07 -10.81 39 44.1 1.90 2.17 14.28 12.45 1.5%

Kellogg Company K 4/6 77.78 74.37 -5.53 86 15.6 3.73 4.10 19.94 18.13 1.6%

McDonald's Corp MCD 12/31 118.14 122.06 0.54 135 10.6 5.57 6.32 21.91 19.32 2.9%

Energy

Concho Resources, Inc. CXO 12/31 92.86 121.34 27.10 130 7.1 -0.63 -1.16 NM NM 0.0%

Financials

Affiliated Managers Group AMG 12/31 159.76 173.52 5.05 238 37.2 13.57 15.59 12.79 11.13 0.0%

JPMorgan Chase & Co. JPM 12/31 66.03 65.27 -3.30 75 14.9 5.56 6.47 11.75 10.09 2.7%

Taubman Centers, Inc. TCO 12/31 76.72 68.57 -13.44 85 24.0 3.62 3.89 38.50 37.54 3.4%

Healthcare

Eli Lilly & Co. LLY 12/31 84.26 75.03 -13.30 91 21.3 3.58 3.84 20.94 19.52 2.7%

Industrials

Allison Transmission ALSN 12/31 25.89 28.09 6.24 33 17.5 1.14 1.27 24.67 22.08 2.0%

Southwest Airlines Co. LUV 12/31 43.06 42.48 -4.74 60 41.2 4.29 5.33 9.90 7.96 0.8%

Materials

Sealed Air Corp. SEE 12/31 44.60 46.44 0.85 63 35.7 2.60 3.01 17.87 15.41 1.2%

Technology

Apple Inc AAPL 4/4 111.12 99.86 -11.44 150 50.2 8.18 9.64 12.20 10.36 0.0%

Autodesk Inc. ADSK 12/31 60.93 58.27 -7.93 100 71.6 -0.78 1.41 NM 41.20 0.0%

Facebook Inc. FB 12/31 104.66 118.81 9.95 145 22.0 3.49 4.94 34.07 24.04 0.0%

2011 2012 2013 2014 2015

Focus List Performance Statistics

Credit Suisse US Focus List Performance -5.5 16.5 35.9 15.1 -6.1

S&P 500 Return 2.1 16.0 32.4 11.4 0.0

Relative Performance -7.6 0.5 3.5 3.7 -6.1

Focus List Turnover Statistics

17 20 22 20 20

14 18 20 21 21

11 16 23 19 19

72% 86% 93% 89% 106%Turnover (% )

Average No. of Companies

Added

Deleted

Target

Year

P/E Ratios

1Actual earnings are reported; forecast earnings are First Call consensus operating EPS estimates for the S&P indices (top down) and DJIA (bottom up). 2Nasdaq Composite Index performance does not include dividends.

3 Removed from Focus List in 2016: Devon Energy Corp., 2/24, Marriott International, 2/29, Micron Technology Inc., 3/31, Mondelez, 4/6, and Canadian Pacific Railways, 4/8, Tesla Motors, Inc., 4/20, and Time Warner, Inc., 5/23. 4 Added to Focus List in 2016: Apple, 4/4, Kellogg Company, 4/6, and 21st Century Fox, Inc., 5/23.

5Return for period 12/31/15-5/31/16. The Start Price for stocks added to the Focus List prior to 2015 represents the closing price of the stock on 12/31/15. For stocks added subsequent to 12/31/15, the Start Price reflects the price of the stock on the date it was added to the Focus List. 6Fiscal estimates reflect company fiscal year-end. *P/E – Only profitable companies included. NA – Not available. NM – Not meaningful.

Copies of each analyst’s most recent report on the companies listed above are available on research-and-analytics.credit-suisse.com or by contacting Credit Suisse’s Equity Research Department.

The Credit Suisse U.S. Focus List is a bottom-up portfolio that seeks superior investment performance by identifying and analyzing our best research ideas, with a 12-month investment horizon. Stock selection resides with the U.S. Investment Policy Committee (IPC), which is not constrained by market cap, sector weightings, or market indices. The portfolio is screened against analysts’ “Top Picks” as published in the Monthly Review and Comment, Credit Suisse’s proprietary multifactor quantitative model, and against our HOLT valuation framework. The IPC meets regularly to review the portfolio and discuss analysts’ recommendations. The Focus List performance is calculated on a daily total-return basis and is published in the Monthly Review and Comment and Weekly Insights and is also available through Research & Analytics on the Credit Suisse website.

June 2016

Coverage and Opinion Changes 4

COVERAGE AND OPINION CHANGES

Rating Company Ticker New Date Old Analyst

Initiations

Align Technology, Inc. ALGN OUTPERFORM 11-May-16

Robert Willoughby

Callon Petroleum Company CPE OUTPERFORM 24-May-16

Mark Lear

Intellia Therapeutics, Inc. NTLA OUTPERFORM 31-May-16

Alethia Young

SecureWorks Corp. SCWX NEUTRAL 17-May-16

Philip Winslow

Summit Midstream Partners, LP SMLP NEUTRAL 24-May-16

John Edwards

Tesaro, Inc. TSRO OUTPERFORM 12-May-16

Alethia Young

Teva Pharmaceutical Industries Ltd. TEVA NEUTRAL 04-May-16

Vamil Divan

Reinstating

Baker Hughes Inc. BHI OUTPERFORM 02-May-16 RESTRICTED James Wicklund

DHX Media Ltd DHX.TO OUTPERFORM 13-May-16 RESTRICTED Robert Peters

Halliburton HAL OUTPERFORM 02-May-16 RESTRICTED James Wicklund

Keyera Corp. KEY.TO NEUTRAL 25-May-16 RESTRICTED Andrew M. Kuske

Rating Changes Upgrades

Gibson Energy Inc. GEI.TO NEUTRAL 26-May-16 UNDERPERFORM Andrew M. Kuske

Golar LNG Ltd. GLNG OUTPERFORM 09-May-16 NEUTRAL Gregory Lewis

Johnson Controls Inc JCI OUTPERFORM 23-May-16 NEUTRAL Julian Mitchell

Midcoast Energy Partners, L.P. MEP NEUTRAL 03-May-16 UNDERPERFORM John Edwards

ONEOK Partners, LP OKS NEUTRAL 05-May-16 UNDERPERFORM John Edwards

Toronto Dominion Bank TD.TO OUTPERFORM 03-May-16 NEUTRAL Kevin R. Choquette

Downgrades

Acadian Timber Corp. ADN.TO NEUTRAL 10-May-16 OUTPERFORM Andrew M. Kuske

Alimentation Couche-Tard Inc. ATDB.TO UNDERPERFORM 02-May-16 NEUTRAL David Hartley

Anadarko Petroleum Corp. APC NEUTRAL 04-May-16 OUTPERFORM Edward Westlake

Atento S.A. ATTO NEUTRAL 11-May-16 OUTPERFORM Daniel Federle

Canadian Tire Corporation Limited CTCa.TO UNDERPERFORM 12-May-16 NEUTRAL David Hartley

Kinross Gold Corp. KGC NEUTRAL 03-May-16 OUTPERFORM Anita Soni

Marketo, Inc. MKTO NEUTRAL 31-May-16 OUTPERFORM Philip Winslow

National Bank of Canada NA.TO NEUTRAL 03-May-16 OUTPERFORM Kevin R. Choquette

Portola Pharmaceuticals PTLA NEUTRAL 30-May-16 OUTPERFORM Vamil Divan

SeaWorld Entertainment SEAS UNDERPERFORM 11-May-16 OUTPERFORM Benjamin Chaiken

St Jude Medical STJ NEUTRAL 02-May-16 OUTPERFORM Matthew Keeler

June 2016

Analyst Stock Picks by Industry 5

ANALYST STOCK PICKS BY INDUSTRY

Industry Stock Picks Tkr

Target Price

CONSUMER DISCRETIONARY Apparel, Footwear & Specialty Softlines Hanesbrands Inc. HBI 39.00 lululemon

athletica Inc. LULU 76.00

Nike Inc. NKE 68.00 Homebuilding CalAtlantic Inc. CAA 40.00 Caesarstone Ltd. CSTE 47.00 Taylor Morrison TMHC 18.00 Restaurants Darden

Restaurants, Inc DRI 72.00

McDonald's Corp MCD 135.00 Panera Bread

Company PNRA 225.00

Retail, Mass Merchants Costco Wholesale Corporation

COST 165.00

Specialty Hardlines Home Depot HD 147.00 Sportsman's

Warehouse Holdings, Inc.

SPWH 16.00

Travel & Leisure Vail Resorts MTN 145.00 Six Flags

Entertainment Corp.

SIX 67.00

Marriott Vacations Worldwide

VAC 73.00

U.S. Media, Cable & Satellite CBS Corporation CBS 75.00 21st Century Fox

Inc. FOXA 40.00

Time Warner Inc. TWX 90.00 CONSUMER STAPLES Drug & Food Retail & General Merchandise Stores

Dollar General DG 95.00

Sprouts Farmers Markets

SFM 28.00

Sysco Corporation SYY 55.00 Drug & Food Retail, Canada Loblaw

Companies Limited(C$)

L 77.00

Packaged Foods Kellogg Company K 86.00 Mondelez MDLZ 48.00 J.M. Smucker Co. SJM 142.00 ENERGY Alternative Energy Jinko Solar JKS 40.00 Sunrun RUN 18.00 SolarCity SCTY 38.00 Independent Refiners Marathon MPC 48.00 Integrated Oil & Gas Devon Energy

Corp DVN 42.00

Master Limited Partnerships EQT Midstream Partners, LP

EQM 109.00

Genesis Energy, LP

GEL 46.00

Tallgrass Energy Partners, L.P.

TEP 60.00

Oil & Gas E&P, Canada/International NuVista Energy(C$)

NVA 6.25

Parex Resources Inc.(C$)

PXT 13.00

Seven Generations Energy Ltd.(C$)

VII 26.00

Industry Stock Picks Tkr

Target Price

Oil & Gas Exploration Concho Resources, Inc. CXO 130.00 & Production Noble Energy NBL 42.00 PDC Energy PDCE 81.00 Oil & Gas, Canada Canadian Natural

Resources Limited(C$) CNQ 42.00

Suncor Energy(C$) SU 41.00 Oilfield Equipment & Services Baker Hughes Inc. BHI 56.00 Halliburton HAL 49.00 Schlumberger SLB 87.00 FINANCIALS Asset Managers Affiliated Managers

Group AMG 238.00

Capital Markets Goldman Sachs Group, Inc.

GS 180.00

IntercontinentalExchange, Inc.

ICE 280.00

Lazard Ltd. LAZ 44.00 Large-Cap Banks Bank of America Corp. BAC 18.00 JPMorgan Chase & Co. JPM 75.00 Mid-Cap Banks BB&T Corp. BBT 42.00 KeyCorp KEY 16.00 Zions Bancorporation ZION 30.00 Mortgage REITs, Servicers, Insurers, and BDCs

New Residential NRZ 17.00

Nationstar Mortgage Holdings Inc.

NSM 19.00

PennyMac Mortgage Investment Trust

PMT 16.00

Property & Casualty Insurance Arthur J. Gallagher & Co. AJG 47.00 Allstate Corporation ALL 74.00 CB Limited CB 131.00 REITs Brandywine Realty Trust BDN 16.00 Simon Property Group,

Inc. SPG 230.00

Taubman Centers, Inc. TCO 85.00 Specialty Finance Synchrony Financial SYF 38.00 Visa Inc. V 85.00 GLOBAL SERVICES Business & Professional Services Gartner Inc IT 106.00 Nielsen Holdings NLSN 58.00 ServiceMaster Global

Holdings Inc SERV 44.00

Knowledge Services Houghton Mifflin Harcourt Company

HMHC 23.00

Grand Canyon Education, Inc

LOPE 62.00

Nord Anglia Education Inc.

NORD 23.00

Payments & Financial Technology Global Payments Inc. GPN 68.00 PayPal Holdings, Inc. PYPL 39.00 HEALTHCARE Animal Health Zoetis ZTS 59.00 Biotechnology Biomarin

Pharmaceuticals, Incorporated

BMRN 114.00

Celgene Corporation CELG 140.00 Gilead Sciences,

Incorporated GILD 120.00

Healthcare Technology & Distribution

Cardinal Health CAH 97.00

Express Scripts ESRX 85.00 DENTSPLY-SIRONA XRAY 72.00

June 2016

Analyst Stock Picks by Industry 6

Industry Stock Picks Tkr

Target Price

Major Pharmaceuticals Bristol Myers Squibb Co. BMY 79.00 Eli Lilly & Co. LLY 91.00 Pfizer PFE 39.00 Managed Care & Healthcare Facilities

Centene Corporation CNC 78.00

HCA Holdings, Inc. HCA 90.00 UnitedHealth Group

Incorporated UNH 141.00

Medical Supplies & Devices Boston Scientific Corp BSX 22.00 SMID-Cap Biotechnology Five Prime

Therapeutics, Inc FPRX 55.00

UltraGenyx Pharmaceutical, Inc

RARE 101.00

INDUSTRIALS Aerospace & Defense BE Aerospace Inc. BEAV 58.00 CACI International, Inc. CACI 115.00 Spirit AeroSystems SPR 57.00 Airfreight & Ground Transport Canadian Pacific

Railways CP 163.00

JB Hunt Transport Services

JBHT 96.00

Union Pacific UNP 94.00 Airlines American Airlines Group

Inc. AAL 47.00

Delta Air Lines, Inc. DAL 58.00 Southwest Airlines Co. LUV 60.00 Electrical Equipment & Multi-Industry

Ingersoll-Rand Plc IR 72.00

Johnson Controls Inc JCI 50.00 3M MMM 178.00 Engineering & Construction AECOM ACM 35.00 Chicago Bridge & Iron CBI 51.00 Environmental Services Waste Management, Inc. WM 65.00 Machinery Allison Transmission ALSN 33.00 Cummins Inc. CMI 130.00 Parker Hannifin

Corporation PH 126.00

Industry Stock Picks Tkr

Target Price

Ocean Shipping Euronav NV EURN 20.00 Scorpio Tankers Inc. STNG 10.00 SMID-Cap Aerospace & Defense Allegheny Technologies,

Inc ATI 45.00

Trading Companies & Distributors W. W. Grainger, Inc. GWW 253.00 HD Supply HDS 35.00 MATERIALS Precious Metals Agnico Eagle Mines

Limited AEM 50.00

Paper & Packaging Sealed Air Corp. SEE 63.00 U.S. Chemicals & Agriculture Air Products & Chemicals APD 161.00 CF Industries Holding Inc. CF 38.00 U.S. Metals & Mining Constellium CSTM 10.00 Steel Dynamics, Inc. STLD 27.00 United States Steel Corp. X 22.00 TECHNOLOGY Internet Amazon com Inc. AMZN 880.00 Facebook Inc. FB 145.00 Alphabet GOOGL 920.00 IT Hardware, Networking & Telecom Equipment

Apple Inc AAPL 150.00

Arista Networks ANET 90.00 Nokia NOKIA 7.30 Semiconductor Equipment Lam Research Corp. LRCX 98.00 Semiconductors Broadcom Ltd AVGO 180.00 Intel Corp. INTC 40.00 NXP Semiconductors

N.V. NXPI 120.00

Small- & Mid-Cap Software 2U, Inc TWOU 32.00 The Ultimate Software

Group, Inc. ULTI 225.00

Software Autodesk Inc. ADSK 100.00 Box, Inc. BOX 24.00 Oracle Corporation ORCL 50.00

Note: Boldface names indicate analysts’ new top stock picks.

June 2016

Investment Strategy and Economics 7

INVESTMENT STRATEGY AND ECONOMICS (excerpts from recently published macroeconomic reports)

Key Macro Forecasts Q-to-Q % Change at annual rate 2014A 2015A 2016A 2016E 2016E 2016E 2016E

Q1 Q2 Q3 Q4

Real GDP 2.5 2.0 0.8 2.6 2.3 2.6 2.1

CPI (Y/Y%) 0.4 0.4 1.1 1.0 1.0 1.4 1.4

Core CPI (Y/Y%) 2.0 2.0 2.3 2.2 2.2 2.2 2.2

Core PCE (Y/Y%) 1.4 1.4 1.7 1.6 1.7 1.8 1.8

Industrial Production -1.6 -1.6 -1.5 0.7 2.2 2.7 1.0

Unemployment Rate (qtr. Avg. %) 5.0 5.0 4.9 5.0 4.8 4.7 4.7

Fed Funds Rate (End of Period in %) 0-.25 .25-.50 .25-.50 .25-.50 .50-.75 .75-1.00 .75-1.00

Asset Allocation Benchmark

Recommended

Weight OW (+) UW (-)

Corporate Bonds 5.0 6.0#ERR: Could not find the time series 'GLS_CORPBONDS_T'

Global Equity Strategy Forecasts 2015E 2016E

S&P 500 Index 2,100 2,150

DJ Euro Stoxx 50 3,080 3,350

FTSE 100 6,600 6,600

Nikkei 225 20,500 18,000

MSCI EMF GEM 860 960

MSCI AC World 492 492

Regional Allocation Target Weight Benchmark Active Weight

US 52.7 56.9 -7.4

Europe ex UK 19.2 16.7 15.0

UK 7.5 7.5 0.0

Japan 10.2 8.5 20.0

GEM 10.3 10.3 0.0

Global Energy Forecasts 2015A 2016E 2017E 2018E 2019E Long Term

WTI ($/bbl) 48.8 36.9 52.9 65.0 65.0 67.5

Brent ($bbl) 53.6 37.8 54.3 67.5 67.5 70.0

US Natural Gas NYMEX ($/mcf) 2.7 2.3 3.3 3.5 3.5

Global Commodities Forecasts 2014A 2015A 2016E 2017E 2018E 2019E 2020E 2021E 2022E Long Term

Gold (US$/oz) 1265.5 1160.2 1270.3 1312.5 1250.0 1225.0 1200.0 1211.6 1230.1 1200.0

Silver (US$/oz) 19.0 15.7 16.2 16.5 17.0 17.0 17.5 17.7 18.1 18.0

Platinum (US$/oz) 1384.3 1198.2 1254.4 1550.0 1750.0 1839.0 1876.0 1878.3 1867.6 1700.0

Palladium (US$/oz) 803.0 691.2 757.3 912.5 955.0 973.5 993.0 994.4 988.8 900.0

Copper (US$/lb) 3.1 2.5 2.1 1.9 1.8 2.0 2.0 2.1 2.4 3.0

Nickel (US$/lb) 7.7 5.4 4.7 6.1 6.8 6.8 7.0 7.3 7.9 9.1

Alumina (Spot - US$/t) 330.3 300.9 236.5 250.0 260.0 270.0 280.0 285.4 294.0 300.0

lead (US$/lb) 1.0 0.8 0.8 0.9 0.9 0.9 0.9 0.9 0.9 0.9

Iron ore - fines, qtrly (US$/dMtu) 141.9 81.9 65.8 54.8 53.2 53.2 51.6 59.3 71.5 104.8

Global Foreign Exchange Forecasts 3M 12M

U.S. Dollar per Euro 1.17 1.10

Yen per U.S. Dollar 105.00 105.00

U.S. Dollar per British Pound 1.58 1.49

Swiss Franc per U.S. Dollar 0.97 1.05

U.S. Dollar per Australian Dollar 0.74 0.70

Canadian Dollar per U.S. Dollar 1.30 1.38

Interest Rates Forecasts 2016:Q1 2016:Q2 2016:Q3 2016:Q3

2-Yr Yield 0.70 0.75 0.80 0.90

5-Yr Yield 1.25 1.30 1.35 1.45

10-Yr-Yield 1.80 1.85 1.90 2.00

30-Yr-Yield 2.55 2.60 2.65 2.70

Source: Credit Suisse Group.

June 2016

U.S. Economics 8

From report dated 26 May 2016

Economics

U.S. Economics Research Analyst

James Sweeney 212 538 4648

ECONOMICS

Get Going

■ We still expect two Federal Reserve interest rate hikes of 25 basis points in

2016; however, we now believe that the first will be in July, not September.

Market pricing implies one hike in 2016, with near even chances of one

before August. Although the economic data are now consistent with a June

hike, careful risk management by the Fed suggests that it will delay until

July. The Federal Open Market Committee (FOMC) meets on June 15, and

the Brexit vote is on June 23. If the probability of Brexit really is roughly

25%1, then the Fed may hedge its risks by delaying slightly. A September

hike would occur close to the presidential election and amid potentially

stressful money market reforms. July appears to us as a window.

■ The Fed’s basic framework is consistent with multiple hikes in the coming 12

months. Several FOMC members, doves included, are publicly saying that

the United States is at or near full employment and that inflation is on track to

achieve the Fed’s target. Fed Chair Janet Yellen has said that the

time-varying real neutral rate is near zero, meaning she believes that the Fed

is currently supplying the market with roughly 150 basis points of

accommodation.

■ Our inflation outlook is similar to that of the FOMC. We see a gentle increase

in U.S. core personal consumption expenditure inflation toward 2%. We

recently laid out the details of our inflation view from bottom-up and a top-

down perspectives. In addition, we explored the global factors that are most

relevant to Fed decisions. Although global industrial production has been in a

slump for roughly six quarters, industrial production momentum has recently

improved, giving the Fed room to move. Our report, titled, Show Us Your

Decision Tree, published, February 6, 2015, showed that Fed decisions are

sensitive to global manufacturing indicators.

■ Moreover, we have also written recently about the Fed’s volatility phobia.

Significant dollar strength, equity market weakness, or renewed China

concerns could delay hikes as well as the omnipresent possibility of a broad

U.S. slowdown. However, although hikes may be taken as bad news by

some investors, we believe that the risks of rapid hikes grow the longer the

Fed waits. Hiking once or twice per year is a modest and bearable pace. On

the other hand, if the global growth slump finally ends while inflation is at

target and full employment has been surpassed, the Fed may feel forced to

play catch-up, and that would catch markets off guard in a way that could

harm the labor market.

1 Professor Phil Tetlock’s “Superforecasters” put the probability of a Brexit out vote as just shy of 25%, according to a Bloomberg report. Superforecasters target accurate probability estimates and there is empirical evidence supporting their approach.

June 2016

U.S. Equity Strategy 9

From report dated 09 May 2016

Strategy

■

U.S. Equity Strategy EQUITY STRATEGY

Carving Up the Consensus

■ Institutional investors, particularly contrarians, often ask us what does

everybody love and what does everybody hate. With this in mind, we have

outlined how views and positioning among long and short hedge funds, long-

only actively managed mutual funds, and sell-side analysts stack up by

industry group for U.S. large caps (stocks in the Russell 1000) and small

caps (stocks in the Russell 2000).

■ Our analysis utilizes a unique data set. Our hedge fund positioning data

were compiled by Credit Suisse Prime Services and capture net exposure

including single-stock and sector and industry exchange-traded fund

exposure. We compare April 2016 month-end positioning with averages

since 2010. Our sell-side ratings data capture net buys (industry group less

Russell 1000 or Russell 2000) as of April month-end versus post-2003

averages.

■ Our mutual fund positioning data capture the percent of funds overweight the

group through the first quarter of 2016 versus post-2003 averages. Although

our mutual fund data points are more than one month old, we still consider

them to be insightful, since changes in mutual fund overweights and

underweights tend to emerge gradually. For each of these indicators, we

consider a reading that is high relative to history to indicate that a group is

overly loved or owned and a reading that is low relative to history to indicate

that a group is deeply out of favor.

■ There is considerable variation in which indicator tracks performance most

closely. However, within large cap, sell-side net buys may be the single best

indicator to track, as they show a meaningful correlation with performance

trends for ten out of the 24 Russell 1000 industry groups examined.

■ Over the course of our study, within large cap, hedge fund positioning has

appeared to drive returns within most technology and consumer groups

along with energy. Since 2014, hedge fund net exposure has been a

noticeably strong driver of performance for energy; retailing; food and

staples retailing; autos and components; food, beverage, and tobacco; and

software and services within large cap as well as diversified financials,

retailing, software and services, and capital goods within small cap.

Continued on next page . . .

Research Analyst

Lori Calvasina 212 538 6396

June 2016

U.S. Equity Strategy 10

Top Take-aways

■ We observed more pockets of consensus thinking across the three investor bases

that we examined than we did in our previous update in mid-February 2016. Groups

that appear to be overly loved or owned on our analysis are large-cap banks, small-

cap semiconductors and semiconductor equipment, and small-cap software and

services. This is a risk factor for our overweight on banks and supports our mid-April

downgrades of semiconductors and semiconductor equipment and software and

services to market weight from overweight.

■ Groups that appear to be uniformly unloved and underowned on our analysis are

small-cap retailing, small-cap household and personal products, and large-cap

materials. We believe that this is supportive of our mid-April 2016 upgrades of retail

to market weight from underweight and of household and personal products to

overweight from market weight, and that it highlights the contrarian nature of these

calls. For materials, the results of our ownership analysis challenge our ongoing

underweight on the group (driven mostly by valuation concerns in the large-cap

segment that offset improvement on our earnings revisions indicator).

■ One group also emerged as a uniform neutral on our analysis: large-cap technology

hardware and equipment. We saw signs of a hedge fund retreat from food,

beverage, and tobacco and food and staples retail within large cap, indications of

deep bearishness on energy on the sell-side alongside reengagement by mutual

funds and a lack of capitulation by hedge funds, reasons to stay concerned about

crowding in health care, and evidence of waning enthusiasm for telecommunications.

June 2016

Global Equity Strategy 11

From report dated 31 May 2016

Investment Strategy

Global Equity Strategy Research Analysts

Andrew Garthwaite 44 20 7883 6477

Marina Pronina 44 20 7883 6476

Robert Griffiths 44 20 7883 8885

Nicolas Wylenzek 44 20 7883 6480

Alex Hymers 44 20 7888 9710

STRATEGY

Equities: The Dilemma We maintain our neutral stance on equities and stick to our year-end targets of 2,150 for the S&P 500 and 3,350 for the Euro Stoxx 50.

What has improved but is unlikely to improve further? (1) China: housing (prices rising in 65 out of 70 cities) and infrastructure (state/SoE investment up 23% year over year, a five-year high), but economic lead indicators look like they are rolling over, our policy indicators show tightening, and there has been no rebalancing. (2) Oil: almost all risk trades have been correlated to oil. We believe if oil moves above $50 per barrel, Saudi Arabia does not meet its apparent economic/political objectives, including preventing the U.S. from becoming self-sufficient in energy. Moreover, speculative positions are at all-time highs. (3) The Fed became more dovish as the market rallied, but this is now reversing. (Our economists expect two rate hikes this year; the market expects one.) (4) Bond yields have never decoupled to this extent from ISM new orders, cyclicals, or commodities. (5) Credit: in Europe there has been a 50% retracement in high-yield spreads from their trough in summer 2014. Spreads now look to be at fair value. (6) U.S. earnings revisions have turned positive for the first time since June 2014, but much of this is down to the dollar and commodities and hence this normally positive signal could be misleading. (7) U.S. lead indicators are now unusually ambiguous, and if anything, trending weaker.

What has not improved: (1) Global PMI or global nominal GDP growth (which is the weakest it has been outside of 2008-09). (2) U.S. labor is getting some modest pricing power (which is bad for profit margins) and hence the gap between nominal GDP and wage growth has fallen to its lowest in this cycle. (3) There is above-average political risk (relating to immigration, the Italian referendum, and the U.S. presidential election).

The other worries for equities: (1) Both our fair value models are close to fair value. (U.S. ERP is 5.7% against a warranted of 5.6%.) (2) We have never seen so much disruption to business models from new technology, regulation, and China in an environment where governments are helping labor relative to capital (via taxation and minimum-wage legislation). (3) We marginally raise our 2016 U.S. EPS growth forecast to 1% from zero. The problems for corporates are (1) labor is getting pricing power, (2) operating earnings appear abnormally overstated compared to reported, and (3) one-off factors, which accounted for roughly 60% of margin improvement, are diminished. (4) Buybacks as a style is underperforming. (5) Seasonals are unsupportive: since 1988; May to September has seen flat markets. (6) A fall in the 50-week MA below the 100-week MA sees down markets 56% of the time over the next six months.

We remain benchmark of equities: (1) Fair value for equities could be considered reasonable when bonds/real estate appear so expensive. The cost of equity in the U.S. is 9.1%, still in its normal range (though at the lower end). (2) Risk appetite is pricing in an ISM below 50. (3) Excess liquidity is extremely high, and retail, institutional, and prime positioning is also supportive. (4) Market breadth has improved.

The critical issues to watch are Chinese lead indicators, U.S. wage growth, and U.S. lead indicators.

June 2016

Global Energy Economics 12

From report dated 31 May 2016

Oil & Gas

Global Energy Economics Research Analyst

Jan Stuart 212 325 1013

GLOBAL ENERGY ECONOMICS

OPEC Could Simply Leave Well Enough Alone ■ As OPEC ministers have begun to gather in Vienna, Austria, for their regular

meeting on Thursday, oil market fundamentals appear very close to slipping

into a supply deficit. Large inventory reductions lie in store for the second half

of 2016. We also believe that one of the few remaining outright bearish risks

to prices at this stage is that of an intensifying market share tussle

developing among key sovereign exporters Saudi Arabia, Iran, Iraq, and

Russia.

■ Therefore, we believe that the best possible outcome of tomorrow's meeting

is also the most widely anticipated and likely outcome, which is that nothing

happens. In this scenario, delegates talk mostly about the next secretary

general and other organizational issues and do not quibble about price or

quotas.

■ Tail risks (i.e., those with a probability of less than 2.5%) involve a public fight

resulting in promises of rapid supply increases or, at the other extreme, a

surprise deal to take oil off the market. Sell in May and go away is probably

not the right idea this year, as we believe that the price risk skews up through

the third quarter, not down.

■ More interesting than the OPEC meeting is the oil market context. The most

important background feature is that of falling supply and rising demand

trends. There is a fascinating but largely peripheral debate about the modest

degree in which the ongoing rebalance of supply and demand is accelerated

by outages of supply in Nigeria and Canada, which are partly offset by lower

refiner demand due to labor issues in France.

■ Risks remain, but with all producers excluding Saudi Arabia now pumping at

or near capacity, the short-term bearish risk resides nearly exclusively in

Riyadh. In addition, oil markets, prices, futures time-spreads, and curves

suggest that the worst is over, and our own base-case price forecast for 2016

seems too cautious. In our full report, we highlight in charts and tables the

background details of oil markets and fundamentals.

June 2016

Accounting & Tax 13

From report dated 18 May 2016

Accounting & Tax

Accounting & Tax ACCOUNTING

SEC Squeezing Non-GAAP: Staff Releases

New/Updated Guidance

Exhibit 1: Highlights of the New/Updated Guidance

Source: Credit Suisse Accounting & Tax Research .

■ Non-GAAP is a hot topic (again). You might have noticed a bit more

attention being paid to non-GAAP results recently. (It tends to happen every

ten years or so.) The widening gap between GAAP and non-GAAP earnings

and some noise from the SEC have resulted in a number of articles in the

financial press along with increased investor interest.

■ New/Updated guidance from the SEC may just be the start. The SEC

staff released new interpretations and updated some existing guidance for

the use of non-GAAP financial measures. Some of the key issues clarified

by the SEC include: companies shouldn't come up with their own accounting

rules for individual line items (like accelerating revenue that is recognized

over time); cash flow per share is not allowed regardless of what companies

call it; cash taxes can be used in cash flow measures but not in non-GAAP

earnings, etc. We expect to hear more from the SEC on non-GAAP,

including comment letters to companies that appear to be pushing the

envelope, and we wouldn't be surprised to see the SEC make an example

out of a few companies by investigating them for providing "misleading" non-

GAAP info. If that doesn’t do the trick, the SEC might write some new rules.

■ Be wary of non-GAAP results (not just because of heightened

regulatory risk). Don't be afraid to challenge the consensus. Does the non-

GAAP number better reflect the underlying economics or is management

just trying to paint a prettier picture? Keep an eye out for recurring non-

recurring charges, "non-cash" costs that involve cash, inconsistent

adjustments over time and versus peers, wide GAAP/non-GAAP spreads,

lots of adjustments, non-GAAP diverging from cash flows, etc.

Research Analysts

David Zion, CFA, CPA 212 538 4837

Ravi Gomatam, CFA 212 325 8137

June 2016

Industry Reports 14

INDUSTRY REPORTS (excerpts from recently published industry and company research)

June 2016

Consumer Discretionary 15

CONSUMER DISCRETIONARY

From report dated 22 May 2016

Media

Media Research Analyst

Omar Sheikh 212 325 6818

COMMENT

Viacom and CBS—Redstone Shakes Up

National Amusements Board and Trust

■ On Friday, May 20, 2016, Sumner Redstone removed Philippe Dauman and George Abrams from the boards of National Amusements and Redstone's Trust. Unless this decision is reversed, it has important implications for Viacom (VIAB) and, potentially, for CBS Corporation (CBS). We highlight the following thoughts.

■ A statement from Sumner Redstone's lawyer highlighted that "Mr. Redstone acted after he expressed his concerns regarding Viacom’s performance to Messrs. Abrams and Dauman, both Viacom directors, and received no response from them." If it is true that the controlling shareholder is unhappy with VIAB's performance, this suggests that Redstone could at some point seek to use his roughly 80% voting interest to remove Dauman from the CEO role, as he has done with former CEOs in the past. Public statements from the VIAB board show that it fully supports Dauman; however, it is hard to see how it could prevent his removal if that is Redstone's wish.

■ We note than one press report that suggests "Mr. Redstone was frustrated that he wasn't being heard by the board and management of Viacom on a variety of concerns, including his disapproval of Mr. Dauman’s plan to sell off a minority stake of Paramount Pictures." If true, again, we assume that Mr. Redstone could seek to use his voting interest to halt the sale of a partial stake in Paramount, which VIAB's management team under Dauman was

planning to conclude by the end of June.

■ A spokesman for Dauman responded to his removal from both boards by highlighting that "as court proceedings and other facts have demonstrated, Sumner Redstone now lacks the capacity to have taken these steps." If the CEO of VIAB believes this to be true, we believe that this puts pressure on the boards of VIAB and CBS to take steps to protect the interests of minority shareholders in both companies by independently verifying Redstone's mental competency. If the controlling shareholder does lack the mental capacity to make decisions regarding the strategy of both companies, this could trigger the transfer of control over his approximate 80% voting interest to the five remaining trustees of the Sumner M. Redstone National Amusements, Inc. Trust.

■ We note that a spokesman for Dauman called Redstone's action to remove him and George Abrams "invalid and illegal." This suggests to us that a legal challenge to their removal is possible. We would argue that the outcome of such a challenge would likely need to be seen before the boards of VIAB or

CBS could decide on the appropriate course of action for both companies.

June 2016

Consumer Discretionary 16

From report dated 19 May 2016

Restaurants

Restaurants Research Analyst

Jason West, CFA 617-556-5745

COMMENT

Labor Costs: Thoughts on New Overtime Rules

■ On May 18, 2016, the U.S. Department of Labor released its final rules updating overtime regulations. The overtime salary threshold will be raised to $47,476 per year from $23,660 starting on December 1, 2016. This means that any salaried employee making less than $47,476 will soon be eligible for overtime compensation. As we discussed in our recent report on wage inflation, titled, How Bad Could It Get?, published, May 12, 2016, our contacts often cited a potential change in the overtime rules as even more concerning than minimum wage increases. We believe that the final rules came in slightly favorable to expectations, as most operators with which we spoke had anticipated a higher threshold, no allowance for incentive compensation, and implementation as early as July 2016. We expect most restaurants to find ways to mitigate much of this impact. However, in an industry known for relatively low salaries and long hours, these new rules represent a material change to the operating model.

■ Estimating the financial impact from the new overtime rules is difficult, given the wide variance in operating models and limited disclosures around salaried versus hourly workers. However, we believe that the new rules could potentially add 0-50 basis points to restaurants' labor costs as a percentage of sales. The extent to which a restaurant is affected by the new rules will depend on the proportion of salaried workers making less than $47,476 and working more than 40 hours per week. We believe that casual dining companies will be most affected, given a higher number of salaried employees per store, limited pricing power, and typically a higher mix of company-operated restaurants versus other segments. However, we also expect a large percentage of store managers within quick-service restaurants and fast-casual concepts to be affected. Upscale operators should see a relatively muted impact.

■ We expect restaurants to bump up salaries for managers near the threshold. Operators could then choose to absorb the incremental salary expense or reduce incentive compensation to keep all-in compensation unchanged. The latter option results in no discrete incremental cost, but shrinking the discretionary portion of a manager's total compensation could compromise the incentive structure and raise the overall proportion of fixed versus variable costs in the profit and loss (P&L). We also expect restaurants to convert salaried managers earning well below the threshold to an hourly wage and cap their hours to limit overtime pay. In this case, operators would likely have to hire employees to make up those hours, which could have other knock-off implications for training costs, turnover, morale, and store-level execution. We could see store-level labor costs rising anywhere from a few thousand dollars to perhaps over $10,000 per year, which would affect the typical store-level P&L by 0-50 basis points. Corporate headquarters employees could also be affected by the new rules, which would show up in general and administration expense. We watch for more guidance from companies on this topic in the coming quarters.

June 2016

Consumer Discretionary 17

From report dated 13 May 2016

Luxury Goods

Global Luxury Goods Research Analysts

Guillaume Gauvillé, CFA 44 207 888 0321

Christian Buss 212 325 9667

Isis Wong 852 2101 7109

Catherine Tillson 44 20 7888 6052

Sara Shuler 212 325 7643

Ivy Ji 852 2101 7951

SECTOR REVIEW

Mind the Regional Price Gap

■ Managing regional price gaps increasingly matters. Tourism spending

on luxury goods in Europe and the United States is declining. Chinese

consumers are now buying in China and the development of ecommerce

has enabled easy comparison of prices across markets. Therefore, the

concept of fair pricing for the luxury industry in China has become more

relevant than ever.

■ We analyzed over 1,000 handbag SKUs across six markets. Our

proprietary analysis shows a wide disparity across brands regarding price

gaps. The more affordable U.S. brands like Michael Kors (KORS.N, $44.01,

Neutral, target $47) and Coach (COH.N, $38.18, Neutral, target $42) apply

the largest premiums between China and the U.S. at over 80%. Among

European brands, Tod's (TOD.MI, €61.00, Underperform, target €55) shows

the highest price gap at roughly 50% between China and Europe while Louis

Vuitton (LVMH.PA, €146.45, Outperform, target €168), Bottega Veneta

(owned by Kering [PRTP.PA, €144.35, Underperform, target €140]), SL, and

Prada (1913.HK, HK$27.15, Underperform, target HK$17.50) seem to be

more reasonably priced.

■ Price cuts in China may be necessary. Historically, brands have raised

prices in their home markets to narrow the gap. However, they can no longer

do this or they will face the risk of putting more pressure on an already-weak

domestic consumption. Moreover by persistently keeping high price gaps,

we think luxury brands simply forgo sales opportunities in China. Therefore

the possible adjustment is to cut prices in China to the roughly 30% premium

we deem necessary to cover duties and taxes. The potential price cuts in

China certainly have negative margin implications.

■ LVMH seems to be better placed. We believe companies with a greater

exposure to affordable luxury will see more resilient organic growth in the

current environment. Our proprietary analysis indicates that LV's ASP sits

below its direct peers, Gucci (also owned by Kering) and Prada. We estimate

that some 50% of sales stem from canvas bags, which drive volumes.

Regarding price gaps, the China versus Europe premium does not exceed

30% and, therefore, we see limited risk of LV having to cut prices in China.

Figure 1: Price Differentials Between China and Home Markets (=100)

183 181

149140 139

132 128 126 121 119

Coach MichaelKors

Tod's Gucci Ferragamo Burberry LouisVuitton

Prada SL BottegaVeneta

Source: Company data, Credit Suisse research.

June 2016

Consumer Discretionary 18

From report dated 10 May 2016

Department Stores

Department Stores

Research Analyst

Michael Exstein 212 325 4147

COMMENT

Quality over Quantity, Part II—Identifying the 184 LVP Malls and Retailers' Exposure to Them

■ We recently identified 95 of the most valuable property (MVP) malls in which the mall anchors in our coverage (and Sears [SHLD) have a presence. (See our report, titled, Quality over Quantity: Identifying the "MVP" Malls That Emerging Brands Want to Be In, published, March 17, 2016.) In this follow-up note, we identify 184 of the least valuable property (LVP) malls with these same tenants, at least for now. We identified almost twice as many LVP malls as MVP malls; however, we estimate that the LVP malls generate only 30-40% of the aggregate sales volume generated by the MVP malls owing to their low productivity levels.

■ For the basis of this exercise, we defined LVP malls as those with mortgages in four distressed categories, which tend to occur when a mall has lost (or is about to lose) a major tenant. The prime reason for this happening is the location having very low sales productivity, making it difficult for the tenant to generate a four-walls profit. Nordstrom (JWN) appears to have the highest-quality store base, with only 3% of its locations in LVP malls and 62% in MVP malls. Dillard's (DDS) and SHLD appear worst positioned, with 18% and 16% of locations in LVP malls and only 6% and 5% in MVP malls, respectively.

■ As the industry evolves, the list of LVP malls could grow as more malls struggle to drive traffic as they lose tenants. These malls are likely prime candidates for further future store closures as retailers attempt to adjust their fixed cost base for permanently lower levels of brick-and-mortar sales as sales mix shifts to e-commerce. At the same time, there is likely to be an increased focus on MVP malls and improving the quality and productivity of the existing store base. While the optimum number of stores for traditional retailers remains unclear, we believe that having a strong brick-and-mortar presence will remain a necessity, especially since having a physical store near a customer may affect their decision to purchase online.

Figure 1: Mall Anchors—Percentage of Locations in LVP vs. MVP Malls

18%

16%

12%

11%

10%

3%

6%

5%

3%

11%

62%

50%

0% 20% 40% 60% 80% 100%

Dillard's

Sears

Bon-Ton

JCPenney

Macy's

Nordstrom

Bloomingdale's

% in "LVP" Malls % in Other Malls % in "MVP" Malls

Source: Company data, Credit Suisse estimates.

June 2016

Consumer Discretionary 19

From report dated 09 May 2016

Specialty Hardline

Home Improvement INDUSTRY OUTLOOK

Proprietary Store Analysis Assessing HD versus

LOW Housing Drivers and Near-Term Outlook

■ In our full report, we track the local drivers of demand for Home Depot (HD) and Lowe's (LOW) using data from the Census Bureau, the American Community Survey, and Zillow. Our analysis includes home price appreciation, housing turnover, and inventory availability at the zip code level for all of HD and LOW's stores in the United States. In our report, titled, Store Analysis Shows a More Even Housing Playing Field: It's All About Execution Now, published, October 15, 2015, we helped explain the relative outperformance of HD over the past few years. In this update, we go deeper, cutting the data by market size and market median value, among other characteristics, to help explain and project the differences in sales trends for HD and LOW and assess the sales and margin upside potential (or recoverability in LOW’s case). While the data still favor HD, we believe that the incremental opportunity lies with LOW, as there are signs that the differences in housing trends are starting to neutralize. Therefore, we expect that relative performance comes down to execution, success with the Pro, capitalizing on other market share opportunities (e.g., Sears [SHLD]), omnichannel, other efforts within the store to drive productivity, and keeping

expenses under control.

■ In the short term, the analysis supports an acceleration in first quarter 2016 comps for HD and LOW based on strong housing trends in their respective markets. Data for February and March signal an acceleration from the fourth quarter 2015 9% U.S. comps for HD and LOW of 9% and 5.5%. However, we expect some giveback in April based on a reversal in weather trends after a favorable start to the season, which is consistent with our leading macroeconomic indicator and supplier index. While we are wary of high expectations into the print (as seen with O'Reilly Automotive [ORLY]), HD and LOW should be able to deliver on the relatively high market

expectations.

■ On a relative basis, HD’s average home price appreciation still outperformed in the first quarter 2016; therefore, we are not assuming a significant change in the comps gap. HD may have also benefited more from weather as it relates to big ticket, Pro-oriented projects, which have been outcomping the company average. However, our data signal that the housing gap could be plateauing: HD’s concentration in larger markets, where home price appreciation has been greatest, has contributed to its sales outperformance versus LOW. However, our work suggests that this benefit has started to moderate, as LOW markets pick up or ultra high-end markets moderate. LOW's comps gap with HD should have peaked in late 2015 or early 2016

and should narrow throughout 2016.

Continued on next page . . .

Research Analyst

Seth Sigman 212 538 8043

June 2016

Consumer Discretionary 20

Digging Back into the Gap

■ We tracked the 2006-09 class of stores (around 400 stores, or 22%) that were

opened late in the game after HD had stopped growing. During the downturn, these

stores saw a larger decrease; however, they are currently outperforming the chain.

Data suggest that home price appreciation is still outpacing the LOW store base.

We estimate that this group of stores could add 20-30 basis points incrementally to

comps as they recover and outperform.

■ While the average home price appreciation across HD and LOW’s store bases was

relatively similar to the fourth quarter of 2015, there were noticeably fewer stores for

which the growth accelerated. In the first quarter of 2015, 37% of HD stores and

36% of LOW stores were in markets where median home price growth accelerated

sequentially or was the same as the fourth quarter of 2015. That percent had

previously been tracking over 60%. We assume less appreciation as 2016 goes on,

and HD’s guidance assumes 3.5% growth (200 basis points below that of 2015).

This could point to some moderation in remodel demand through 2016. The key will

be offsets for HD, particularly Interline Brands.

June 2016

Consumer Discretionary 21

9 May 2016

Specialty Softlines

Specialty Softlines Research Analysts

Christian Buss 212 325 9667

Sara Shuler 212 325 7643 [email protected]

Pallavi Bakshi 212 538 8434

INDUSTRY PRIMER

Credit Suisse Private Internet Company

Summit Softlines Take-aways

In early May, we attended Credit Suisse’s Private Internet Company Summit, which brought together executives and investors from across the country. With an eye towards the softlines space, we focused on the structural changes that companies are trying to facilitate in changing consumers’ shopping behavior and their efforts to build efficiencies in customer acquisition, fulfilment, and marketing. Our view remains that 40% of industry sales are likely to migrate online, with radical consequences for traditional brick-and-mortar sales, sourcing and marketing competencies. See our recent report Revolution In The Softlines Brand Landscape: Digital Is The New Wholesale for more detail.

Key takeaways are as follows:

■ eCommerce Has Become Mobile Commerce And The Rules Have Changed. Discussions with eCommerce players highlight the dramatic changes that are occurring as consumers shift their engagement from the desktop into the mobile space. Given limited screen real estate and the challenges navigating large pieces of information on a mobile platform, retailers are struggling to maintain conversion rates and transactional velocity. One solution to this problem appears to be the move away from search-oriented purchasing to discovery-oriented purchasing, where the app or site serves to guide the consumer to a more bounded set of options, using prior purchases, self-identified preferences, and engagement analysis to offer a more limited selection to the consumer. Effectively, this turns the act of shopping into a social and entertainment experience, just as specialty retailers in the 1980’s brought a guided and curated shopping experience to the mall as an improvement of the legacy “everything in one place” model of the department store. Retailers are in essence building recommendation engines with low purchasing hurdles to address the limitations of the form factor.

■ Data Intensity Is Increasing, Metrics Are Changing. As purchasing behavior is increasingly trackable, and consumers are sharing their preferences more explicitly with retailers and brands, we are seeing companies build tools to monitor what consumers choose to buy, but also how they select, what they like, how they share, and when their consumption patterns change. This allows companies to think very differently about how they evaluate their customers, bringing to bear the metrics of the media industry into the eCommerce industry. Questions of customer engagement, time on site, and average pages visited serve to augment the traditional metrics of order velocity, average transaction value, and average unit retail to come up with a more comprehensive view of the lifetime value of the customer. Building robust, comprehensive consumer profiles and mining data to identify different tranches of customers becomes a baseline skill set in order to succeed online, with the goal to increase conversion and improve efficiency of customer acquisition cost.

June 2016

Consumer Discretionary 22

■ Solving a Style Velocity Problem. One of the key problems identified by

companies looking at apparel sales is the increasing velocity of style change within

the industry. The rise of fast fashion has met with the growing presence consumers

have on social media, which is increasing the need to show new looks and new

styles. Effectively, when you wear it once, and post it online, it’s as if you’ve already

worn it for everyone. As a result, companies like Le Tote and Rent The Runway are

trying a model that allows consumers to rent clothing with a low price hurdle for

purchasing and a simple all-you can eat purchase and delivery model, while Wish is

focusing on low price-point impulse purchase product. Underlying many of the

apparel brands and retailers is a further acknowledgement that the ability to keep up

with the pace of change of preference and style is challenging, leaving many brands

and retailers focused on curating product for a targeted audience. In essence, the

brand and retailer become trusted partners in helping a consumer choose a new

look, with low barriers to try, buy and sometimes return.

■ Solving a Convenience Problem. Increasingly, eCommerce providers are looking

to solve convenience problems for consumers. Companies like Adore Me are trying

to ease the hurdle for trying and buying women’s intimates. Bonobos is trying to

lower the fashion hurdle for male consumers. Boxed is trying to build out the

warehouse club bulk-purchase model online with no membership fees and no need

to visit a store. Casper is focused on easing the selection process for mattresses.

ClassPass is building a fitness class marketplace for athletes. Dollar Shave Club is

building a replenishment model for shaving supplies directly with customers. M.

Gemi is trying to bring handcrafted shoes to a broader audience. Stance is bringing

fashion and athletic industry disciplines to bear in the sock category. While none of

these businesses are creating product that doesn’t have an analog in the brick-and-

mortar landscape, they are really changing the means of selection, purchasing, and

fulfillment for industries that have been reliant on mall and catalog distribution for

decades.

June 2016

Consumer Staples 23

CONSUMER STAPLES

From report dated 25 May 2016

Food & Drug Retailing

Food and Drug Retailing Research Analyst

Edward J. Kelly, CFA, CPA 212 325 3241

COMMENT

Small-Box Retailers in the Crosshairs of New

Overtime Rules; Dollar Stores Most at Risk

■ New overtime rules are slated to go into effect on December 1, 2016. The U.S. Department of Labor regulation that was finalized in the previous week will increase the annual salary threshold for most nonwhite-collar workers who qualify for overtime pay to $47,476 from $23,660. The government estimates that approximately 4.2 million Americans will now be eligible for overtime pay who previously were not. This legislation will likely have the most impact on retail store managers that have salaries below the threshold and are asked to work meaningful overtime. Mitigation strategies are possible (raising salaries above the threshold, adjusting hourly wages, capping overtime, and using more part-time workers) but still carry a cost and could take time to implement.

■ To estimate the impact to the stocks in our coverage universe, we used company commentary and Glassdoor.com to focus on salaried store labor currently earning annual pay below the newly announced threshold but above the prior one, as these employees will be eligible for overtime pay in December 2016. Determining the overtime hours worked is more difficult; therefore, we provided a sensitivity analysis based on feedback from industry contacts.

■ The sheer number of dollar stores and their unique low-cost labor model place them straight in the crosshairs of the new overtime rules. With often only two to three employees in a store at any given time, store managers constitute a significant percentage of store labor and are often asked to work 55-60 hours per week. At the same time, store managers at Dollar General (DG) and Dollar Tree (DLTR) on average earn annual salaries that will qualify them for overtime under the new regulation. We estimate that DG and DLTR could face a gross incremental EPS headwind of 5-7% once the rules take effect. We believe that the companies would likely be able to mitigate at least one-half of this via increased use of part-time labor or adjusting hourly wages. At DLTR, raising salaries to the threshold level and averting overtime pay altogether is a likely step that the company could take. Big Lots (BIG) may have some exposure, as Glassdoor data indicate that only assistant managers earn salaries that will qualify them for overtime in December; however, these employees typically work less overtime. Five Below (FIVE) should see less impact given its smaller store base.

■ Drugstores have less exposure to new overtime rules, as store managers typically earn above the new threshold. Risk could lie in the assistant manager population; however, this employee typically works less overtime and accounts for a smaller percentage of total store labor given high pharmacy-related costs. We estimate the EPS impact of the new rules to be $0.01-0.03 at most.

Continued on next page . . .

June 2016

Consumer Staples 24

Food Retailers

■ Within our coverage universe, it appears that food retailers could see the least

impact from the change in overtime rules. Grocery store managers appear to

already earn annual salaries above the new $47,476 threshold, and a significant

portion of store labor tends to be part-time. Many assistant managers could be

newly eligible for overtime pay come December; however, these employees likely

work fewer hours per week than do store managers. Five hours of overtime per

week registered by each assistant manager would have de minimis impact on

Kroger (KR) or SUPERVALU (SVU). Store managers and assistant managers

appear to already earn salaries above the new threshold at Whole Foods Market

(WFM).

■ We are not changing forward estimates for our covered companies at this time as

we await further color from management teams in the upcoming earnings season.

While the gross impact from the finalized rules appears sizable for dollar stores in

particular, the net impact could be mitigated as aforementioned. We will watch for

incremental clarity on this timely issue with earnings prints from DG, DLTR and BIG

later this week.

June 2016

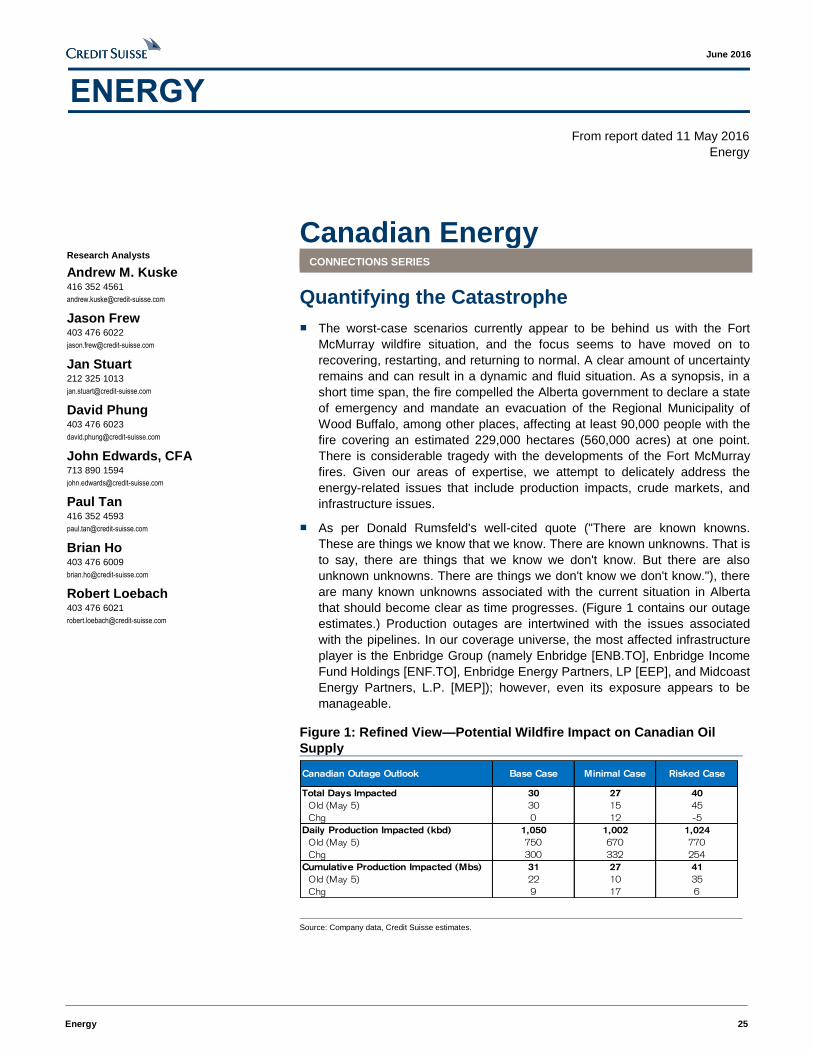

Energy 25

ENERGY

From report dated 11 May 2016

Energy

Canadian Energy Research Analysts

Andrew M. Kuske 416 352 4561

Jason Frew 403 476 6022

Jan Stuart 212 325 1013

David Phung 403 476 6023

John Edwards, CFA 713 890 1594

Paul Tan 416 352 4593

Brian Ho 403 476 6009

Robert Loebach 403 476 6021

CONNECTIONS SERIES

Quantifying the Catastrophe

■ The worst-case scenarios currently appear to be behind us with the Fort

McMurray wildfire situation, and the focus seems to have moved on to

recovering, restarting, and returning to normal. A clear amount of uncertainty

remains and can result in a dynamic and fluid situation. As a synopsis, in a

short time span, the fire compelled the Alberta government to declare a state

of emergency and mandate an evacuation of the Regional Municipality of

Wood Buffalo, among other places, affecting at least 90,000 people with the

fire covering an estimated 229,000 hectares (560,000 acres) at one point.

There is considerable tragedy with the developments of the Fort McMurray

fires. Given our areas of expertise, we attempt to delicately address the

energy-related issues that include production impacts, crude markets, and

infrastructure issues.

■ As per Donald Rumsfeld's well-cited quote ("There are known knowns.

These are things we know that we know. There are known unknowns. That is

to say, there are things that we know we don't know. But there are also

unknown unknowns. There are things we don't know we don't know."), there

are many known unknowns associated with the current situation in Alberta

that should become clear as time progresses. (Figure 1 contains our outage

estimates.) Production outages are intertwined with the issues associated

with the pipelines. In our coverage universe, the most affected infrastructure

player is the Enbridge Group (namely Enbridge [ENB.TO], Enbridge Income

Fund Holdings [ENF.TO], Enbridge Energy Partners, LP [EEP], and Midcoast

Energy Partners, L.P. [MEP]); however, even its exposure appears to be

manageable.

Figure 1: Refined View—Potential Wildfire Impact on Canadian Oil

Supply

Canadian Outage Outlook Base Case Minimal Case Risked Case

Total Days Impacted 30 27 40

Old (May 5) 30 15 45

Chg 0 12 -5

Daily Production Impacted (kbd) 1,050 1,002 1,024

Old (May 5) 750 670 770

Chg 300 332 254

Cumulative Production Impacted (Mbs) 31 27 41

Old (May 5) 22 10 35

Chg 9 17 6

Source: Company data, Credit Suisse estimates.

June 2016

Energy 26

From report dated 20 May 2016

Oil & Gas Equipment & Services

■

Offshore Services SECTOR REVIEW

Seasonal Pickup Should Help

Exhibit 1: Oil Price Versus Decommissioning Activity

$0

$30

$60

$90

$120

0

40

80

120

160

2000 2002 2004 2006 2008 2010 2012 2014 2016

Platforms Decomissioned Oil Price

Source: Bloomberg, BOEM, Credit Suisse estimates.

■ We expect to see a pickup in demand for plug and abandon (P&A) work in

the near term in the Gulf of Mexico. We believe that the following factors

should drive the pickup in work: (1) the Bureau of Ocean Energy

Management's (BOEM) continued push to clean up neglected platforms

(decommissioning platforms); (2) ample idle capacity (e.g., intervention

assets, rigs, and boats); and (3) seasonal pickup in construction activity.

■ Platforms and wells need to be decommissioned, and while maintenance

and decommissioning can be deferred, we expect some urgency on the

BOEM's part following concerns that some operators may not be around

forever. (Two oil and gas companies recently declared bankruptcy.) We

expect the BOEM to highlight the Idle Iron policy (2010) that requires

operators to decommission platforms that typically run $3-10 million.

■ Estimates put the number at 400 fixed platforms that are eligible for

decommissioning in the Gulf of Mexico. This work is done primarily with well

intervention boats, offshore supply vessels, liftboats, and rigs. Well

intervention vessels are about 25-30% more efficient than rigs; however, the

type of P&A matters. Offshore supply vessels can be a cheaper alternative

depending on scope of work. We note that P&A is not a game changer for

the industry; however, every little bit helps in the current market.

■ We view Helix Energy Solutions (HLX) and Tetra Technologies (TTI) as the

largest beneficiaries from a pickup in P&A work; however, names such as

Hornbeck Offshore (HOS), SEACOR Holdings (CKH, liftboats), and TTI

should also benefit from the pickup in activity.

Research Analyst

Gregory Lewis 212 325 6418

June 2016

Energy 27

From report dated 09 May 2016

Marine

Marine SECTOR FORECAST

Offshore Midstream Liquefied Natural Gas

Outlook; Upgraded Golar LNG to Outperform

■ Liquefied natural gas (LNG) spot rates are hovering around $30,000 per day,

or down 60% year over year. Gone are the days of 2013 when spot rates

averaged $100,000 per day. The reasons are plenty: (1) fewer cargoes

moving east and west, (2) limited cargo demand, and (3) too many ships.

The year 2016 is shaping up to be the trough in the conventional LNG

shipping market, which is usually a pretty good time to buy. We may be a

bit early in our call; however, we believe that the road to the recovery is

being built.

■ We expect approximately 45 million tons per annum (mtpa) of LNG capacity

start-ups over the coming two years (roughly 140 mtpa over the coming ten

years), which should reduce tonnage in the spot market. Current charter

rates that are generating negative 15% internal rates of return are

unsustainable. This has put a dead stop on new orders and has even

resulted in some retirements. We see the market as healing slowly.

■ With Petronas’s floating liquefied natural gas (FLNG) 1 delivering in 2016,

we expect the kickoff of a multidecade FLNG trend in resource development.

In our view, Golar LNG (GLNG) is positioned to benefit in the near and

medium term with its FLNG solution. We upgraded GLNG to Outperform

from Neutral and increased our target price to $30 from $20. In our view,

GLNG is a story stock with many of chapters to be written. We expect FLNG

to capture 3-4% of the LNG market by 2025 and see much potential.

■ Given LNG master limited partnerships are yielding 10%-plus, we stressed

the models against current spot rates. Holding distributions fixed, GasLog

Partners LP (GLOP), Teekay LNG Partners (TGP), and Golar LNG Partners

(GMLP) appear covered through 2018, while Dynagas LNG Partners LP

(DLNG) likely needs some help (think dropdowns). More importantly, current

coverage ratios imply charter rates of $50,000-60,000 per day, which is

in-line with the long-term average.

Research Analyst

Gregory Lewis, CFA 212 325 6418

June 2016

Energy 28

From report dated 3 May 2016

Oil & Gas Equipment & Services

Oilfield Services and Equipment Research Analyst

James Wicklund 214 979 4111

COMMENT

Offshore Technology Conference Take-aways

■ We are back in Houston, Texas for the Offshore Technology Conference

(OTC), the granddaddy of tradeshows for the oil and gas industry, for the

Credit Suisse 24th annual OTC tour. The key take-away in 2015 was that

deepwater was not dead. Flash forward to today, and while the industry does

not expect a pickup in activity anytime soon, we are at least one year closer

to the recovery. On day one, we had the opportunity to meet with the Reach

Group, Technip (TECF.PA), Frank's International (FI), Rowan Companies

(RDC), Oceaneering (OII), and Deep Gulf Energy.

■ Probably the most optimistic on the timing of the recovery was TECF.PA

(and it was not bullish), which makes sense given its focus on engineering

and construction and its Forsys joint venture with FMC Technologies (FTI).

The whole point of front-end engineering design studies is to get in on the

ground floor of a project; therefore, TECF.PA should see a pickup in activity

before others. The least optimistic was OII mostly owing to the uncertainty

around the timing of a deepwater rig activity recovery. While OII is best in

class, we understand its angst, given our expectation of another approximate

25% decline in the working floater count (currently 150).

■ Two years into the downcycle, companies are generally accepting that

low-hanging cost reductions are in the rearview mirror. While costs remain a

focus, global footprints need to be maintained to capture the eventual

upcycle. In addition, the Reach Group noted an increased focus on

maintaining safety and balancing efficiency by operators and service

providers. There is still work to be done, and the industry will likely appear

different when the market recovers.

■ A common question asked to nearly every presenter on day one was a

variation of what is the breakeven oil price for an offshore field. The answer

consistently was that it depends. Deepwater projects, specifically subsea

tiebacks, can be economic in the current environment; the problem is that

these types of projects do not require significant capital investment. Oil

prices need to continue upward for significant investment to occur, which we

do not see as a surprise.

Continued on next page . . .

June 2016

Energy 29

Day Two Take-aways

■ Day two at OTC was eventful, as we met with Schlumberger (SLB), National Oilwell

Varco (NOV), Helix Energy Solutions (HLX), Fieldwood Energy, SCF Partners,

Canyon Oak Energy, and many others. While this is an offshore industry event,

much of the focus at investor meetings has been centered on onshore and short-

cycle work that will come back first when the cycle finally turns. Given nearly

everyone in the industry agrees that onshore will be the first place to see an activity

pickup, it is no surprise that attendance at the 2016 conference is down. Times are

tough.

■ For months, investors and companies have discussed onshore North America as

the first market to see a recovery. SLB made the case that conventional onshore

and shelf activity could come back at the same time, if not before, North American

onshore activity. The notion that any type of offshore work could come back sooner

rather than later is a sign of life for many companies that need something to hang

their hat on.

■ To no one's surprise, NOV made the point that a new offshore rig order may not be

seen for years. The interest by SLB and private equity in the land drilling space may

have surprised some. New rigs of the future are destined to further crowd the land

rig market in short order, internationally (SLB) and domestically (private equity).

■ The state of the offshore industry is well understood by companies and investors;

therefore, companies are positioning themselves and telling their stories in ways

that focus on short-cycle work. On the offshore side, HLX drove home its exposure

to well intervention activity, while NOV discussed its ability to take advantage of the

shorter useful life of Tier 1 land rigs.

■ There was a general consensus among the companies that the relatively strong

decremental margins seen in the first quarter of 2016 will be harder to replicate in

the second quarter for the following reasons: (1) companies are beginning to

position (i.e., holding costs) for increased activity in short-cycle businesses, and (2)

low-hanging fruit cost cuts are largely complete. We note that incremental margins

after the second quarter should be better than many are currently modeling owing to

the deep and structural nature of many of the cuts that have been made this

downcycle.

June 2016

Financials 30

FINANCIALS

From report dated 31 May 2016

Banks

U.S. Large- and Mid-Cap Banks SECTOR FORECAST

2016 Comprehensive Capital Analysis and

Review Expectations

■ As soon as Thursday, June 2, 2016, at 4:30 PM EST, the Federal Reserve

will release the results of the 2016 Dodd-Frank Act Stress Test (DFAST).

Disclosure will include minimum capital ratios and revenue and loss

estimates under the severely adverse scenario. DFAST assumes no change

to dividend payments and no common stock buybacks (to provide

comparability across banks). Results reveal the Fed’s determination of

capital adequacy (absolute and relative to the banks’ forecasts) relative to

minimum thresholds.

■ One week after that, as early as Wednesday, June 8, 2016, at 4:30 PM EST,

the Fed will release the results of the Comprehensive Capital Analysis and

Review (CCAR). CCAR results detail quantitatively-derived poststress

capital ratios under adverse and severely adverse scenarios inclusive of

requested capital actions over the course of the nine-quarter horizon. The

Fed will also provide its qualitative assessment through nonobjection,

objection, or conditional nonobjection to a given bank’s capital plans

■ We expect all of the large and mid-cap banks under Credit Suisse coverage

to pass the quantitative element of CCAR (above 4.5% Common Equity Tier

1 and other stressed minimums). We also expect the total net capital return

ask (dividends and buybacks) increases to 76% with 2016 CCAR from

68% in 2015 CCAR inclusive of a dividend payout of 31% in 2016 versus

26% in 2015.

■ We believe that the best positioned are American Express (AXP), Morgan

Stanley (MS), The Bank of New York Mellon (BK), State Street (STT), and

Regions Financial (RF) and expect them to return the greatest percentage of

capital (around 85-100% of earnings). In our view, Zions Bancorporation

(ZION), Bank of America (BAC), Citigroup (C) and M&T Bank (MTB) will

exhibit the most incremental capital return with greatest year-over-year

improvement, with Synchrony Financial (SYF), and Ally Financial (ALLY)

returning common for the first time.

■ We believe that ZION, Huntington Bancshares (HBAN), SYF, and BAC will be

at the lower end of payout range and expect them to seek the least amount of

capital return in CCAR 2016 (around 50-60% of earnings). Success is less

clear on the qualitative aspect of the CCAR process. We expect more

conditional nonobjections to capital plans as well as potentially select

objections. In our view, those submitting for the first time are more at risk.

Research Analyst

Susan Roth Katzke 212 325 1237

June 2016

Financials 31

From report dated 09 May 2016

Homebuilding

April Real Estate Agents Survey PROPIETARY SURVEY

Growing Spring Traffic Faced with Still Limited

Inventories

■ Our buyer traffic index rose to 53 in April 2016 from 49 in March, suggesting

that traffic remained in-line with agents’ expectations. Our weighted traffic

index was up 2 points month over month. Agents highlighted strengthening

spring demand met with persistently tight inventory, making competitive

multiple-offer situations commonplace in many markets and contributing to

widespread price appreciation. Sellers remain elusive, likely given the lack of

available product to which to trade up, although in a few places, agents

observed a marginal loosening in supply. Markets with typically high

international demand continued to see depressed foreign buyer activity. In

terms of price points, agents cited consistently slower demand for high-end

property in several markets. By region, Florida experienced a strong

sequential increase (still below expectations) and the Pacific Northwest was