monte titoli’s service for the iftt - lseg.com · monte titoli’s service for the iftt london...

TRANSCRIPT

Monte Titoli’s service for the iFTT

London Stock Exchange Group Page 1 8th October 2013

London Stock Exchange Group Page 2

Overview on iFTT

8th October 2013

Italian Financial Transaction Tax

Page 3

Shares and other instruments Derivatives

Transactions executed on or after Mar 1, 2013

Shares and participating financial instruments issued by Italian resident companies, with market cap above €500m; and

Other instruments representing the above (e.g. ADRs)

ETFs are not subject to the tax

Transactions executed on or after Sep 1, 2013

Derivatives, whether cash- or physically-settled, securitised or not, whose underlying is shares or value of Italian shares, including options, warrants, covered warrants, certificates. Physical transfer of taxable underlying is also taxed separately

Applicable to:

On what basis: On the net daily balance of transactions on the same security by the same person

Fixed amount depending on transaction

At what rate: 0.1% on transfers on-exchange (0.12% in 2013)

0.2% otherwise (0.22% in 2013)

Fee based on the notional value of the transaction

5 times higher for OTC transactions

HFT tax: Starting on Sep 1, 2013. Tax of 0.02% for trading activity generated by algos and exceeding the ratio of 60% between modified and cancelled orders vs. orders inserted and modified. The ratio included only orders modified or cancelled within 0.5 seconds. The ratio is separately calculated for each financial instrument

On whom: The ultimate transferee. Not on the intermediaries Both parties equally. Not on the intermediaries

For complete information and links to the official documents issued by the Italian Ministry of Economy and Finance, please consult Borsa Italiana website at: http://www.borsaitaliana.it/azioni/notiziedettaglio/iftt.en.htm

Main exceptions / exemptions:

Market making activities and hedging transactions, as per ESMA guidelines

New issues and transactions to ensure liquidity of newly issued shares

Pension funds and similar entities

London Stock Exchange Group 8th October 2013

Dealing on own account - Execution of orders for clients - Reception and transmission of orders

Page 4 London Stock Exchange Group 8th October 2013

Parties involved

The subject who are responsible for the payment of the financial transaction tax are:

Banks Investment firms

Any other intermediary not resident in the territory of the State, authorised in the State of origin to the professional offering activity to the public of services and investment

activities

Collective asset management service or portfolio management service providers are also liable for the tax, in case they do not carry out transactions by the means of another intermediary

Parties involved Liable parties

Responsible for payments

Overview: the collection model and the rationale

London Stock Exchange Group Page 5

The collection of a Financial Transactions Tax (FTT) could be organised in two ways: • direct payment and reporting from the liable parties to the tax agency; or • through entities that would act as intermediaries between the liable parties and the

tax agency To optimize the tax collection process and to provide a suitable solution for different entities, the Italian government did not impose one of the two model but allowed for the maximum flexibility leaving the choice to each party liable for the payment and reporting. Differently from the French approach, the use of the CSD is not mandatory: resident and not resident entities (tbc) may delegate Monte Titoli for the payment and reporting.

8th October 2013

London Stock Exchange Group Page 6

Considering the technicalities of the tax, Monte Titoli has not a full visibility on all taxable transactions and it does not have access to the transaction details.

The financial intermediaries are the only party able to identify the relevant information and assessing their liability, thus only the intermediary can be held liable for the correct accounting of the tax.

Consequently Monte Titoli:

• will operate the tax collection system on the basis of the so-called «declaration-based collection model» where the accountable parties send to Monte Titoli a self-declaration providing in summary the relevant information (instrumental duties and declaration) and the amount to be paid;

• will not be responsible for the correctness of the declaration.

Overview (2)

8th October 2013

London Stock Exchange Group Page 7

Overview (3)

The role of Monte Titoli in the collection of the FTT is defined in article 19 (5), of the Decree 21 February 2013. Accountable parties may delegate Monte Titoli to send the relevant documentation and to pay on their behalf.

Other technical provisions are included within the Resolution of the Italian Tax Agency (Provvedimento Agenzia delle Entrate) n.2013/87896 of 18 July 2013.

8th October 2013

London Stock Exchange Group Page 8

How to fulfill the obligation of payment

8th October 2013

General Rules

Permanent establishment

Fiscal representative

Direct registration at the Italian Tax Agency

Alternatives for payment and reporting

London Stock Exchange Group Page 9

Resident

Tax Agency

Non Resident with stable

organisation in Italy

Tax Agency

Non Resident without stable organisation in

Italy

Tax Agency

Direct registration

Direct registration

Non Resident black list countries

Tax Agency

Through MT upon

voluntary registration

Monte Titoli

Monte Titoli

Monte Titoli

Tax representative

Monte Titoli

8th October 2013

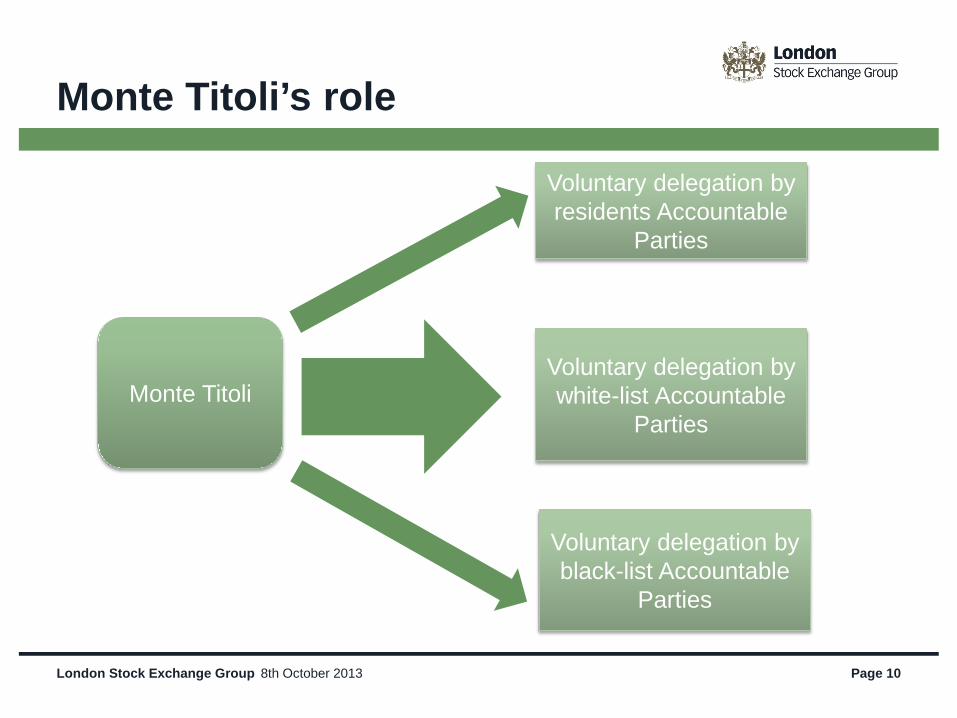

Monte Titoli’s role

London Stock Exchange Group Page 10

Monte Titoli

Voluntary delegation by residents Accountable

Parties

Voluntary delegation by white-list Accountable

Parties

Voluntary delegation by black-list Accountable

Parties

8th October 2013

London Stock Exchange Group Page 11

Monte Titoli’s Service Model

8th October 2013

Introduction

London Stock Exchange Group Page 12

According to the iFTT legislation, Monte Titoli can be delegated by an Accountable Party (domestic and non-domestic) to forward the tax declaration and to pay the Tax amount. The appointment of Monte Titoli should be intended for both the Tax declaration and the Tax payment; it can not be limited to only one of the two options Monte Titoli’s appointment is made on a voluntary basis by any entity involved in the declaration and in the payment, defined as “accountable party” Each participant in Monte Titoli’s iFTT service should have an Italian Tax Code (Codice Fiscale) Those entities whose legal offices are in a black-list country have to register to the Italian Tax Authority (Agenzia delle Entrate) in order to receive a Tax Code; to complete the registration they have to submit the Letter of Undertaking, available as an attachment of the Regulation, and the correspondent Monte Titoli acceptance

8th October 2013

London Stock Exchange Group Page 13

Monte Titoli exclusively operates as a vehicle for declarations and payments, hence it does not assume any responsibility on the content of the declaration and the computation of the Tax amount The service does not include the provision of a fiscal advisory service (e.g., whether a specific transaction is eligible for taxation or not), but only technical and operational assistance The service does not foresee the functionality of transaction netting, which must be done directly by the client As stated in iFTT regulation, Monte Titoli should receive only the synthetic data (number of transactions, total tax amount); the detailed data is filed and stored by the client, in an order that would comply to any possible investigations disposed by the Tax Agency

Monte Titoli’s role

8th October 2013

London Stock Exchange Group Page 14

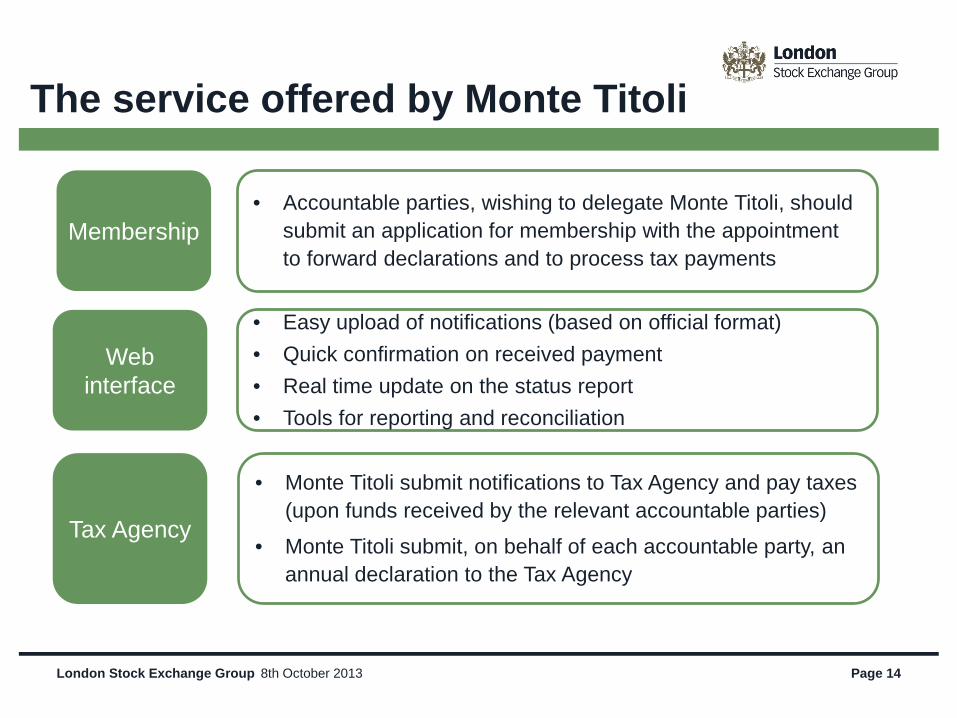

The service offered by Monte Titoli

Membership

Web interface

Tax Agency

• Accountable parties, wishing to delegate Monte Titoli, should submit an application for membership with the appointment to forward declarations and to process tax payments

• Easy upload of notifications (based on official format) • Quick confirmation on received payment • Real time update on the status report • Tools for reporting and reconciliation

• Monte Titoli submit notifications to Tax Agency and pay taxes (upon funds received by the relevant accountable parties)

• Monte Titoli submit, on behalf of each accountable party, an annual declaration to the Tax Agency

8th October 2013

The Service Model - 1

London Stock Exchange Group Page 15

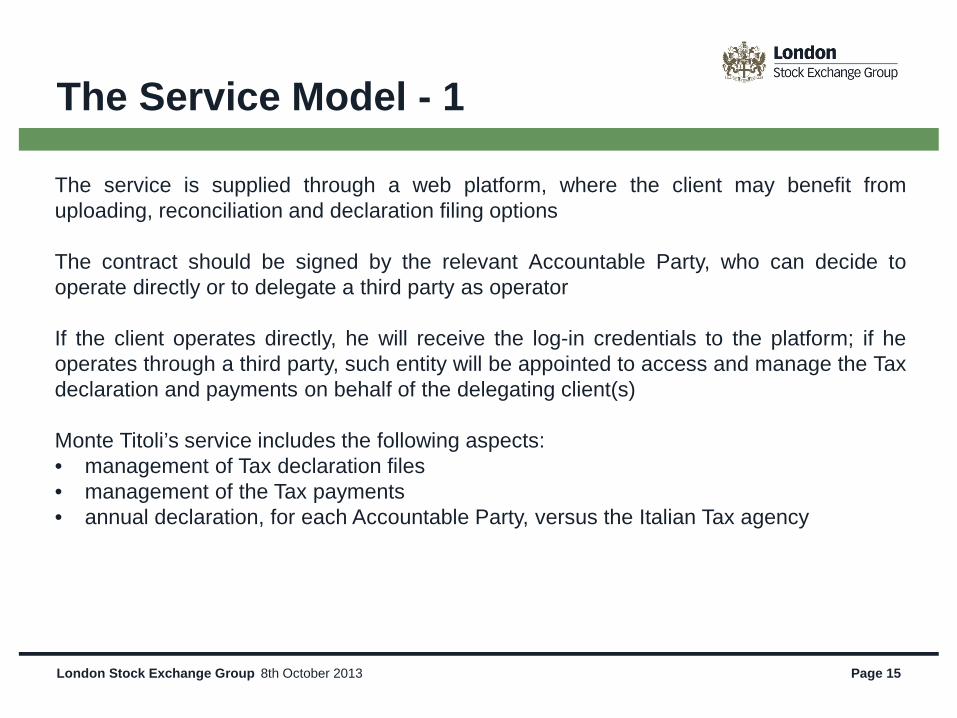

The service is supplied through a web platform, where the client may benefit from uploading, reconciliation and declaration filing options The contract should be signed by the relevant Accountable Party, who can decide to operate directly or to delegate a third party as operator If the client operates directly, he will receive the log-in credentials to the platform; if he operates through a third party, such entity will be appointed to access and manage the Tax declaration and payments on behalf of the delegating client(s) Monte Titoli’s service includes the following aspects: • management of Tax declaration files • management of the Tax payments • annual declaration, for each Accountable Party, versus the Italian Tax agency

8th October 2013

London Stock Exchange Group Page 16

The client may upload the declarations into the system by means the following means: • upload of the TXT file in the format requested by the Italian Tax agency • upload of a CSV file containing exclusively the «essential» data (attachment n.5 of the

Regulation) • manual upload through a mask of the web interface The client may decide whether to upload the declarations in one or more tranches, within the deadlines imposed by the Service model; late declarations will not be processed After the client has submitted the declaration of the month of reference, the system proceeds to forward the payment notification, detailing the Tax amount to be paid The client may settle the Tax by crediting a dedicated Monte Titoli account in T2, if the clients holds a T2 account, or by using a wire transfer to dedicate banking coordinates which will be communicated at a later stage; the payment should be done in an unique tranche and only in EUR according to the specific modality described in the Service Model Any payment beyond the deadline will not be accepted nor processed

The Service Model - 2

8th October 2013

London Stock Exchange Group Page 17

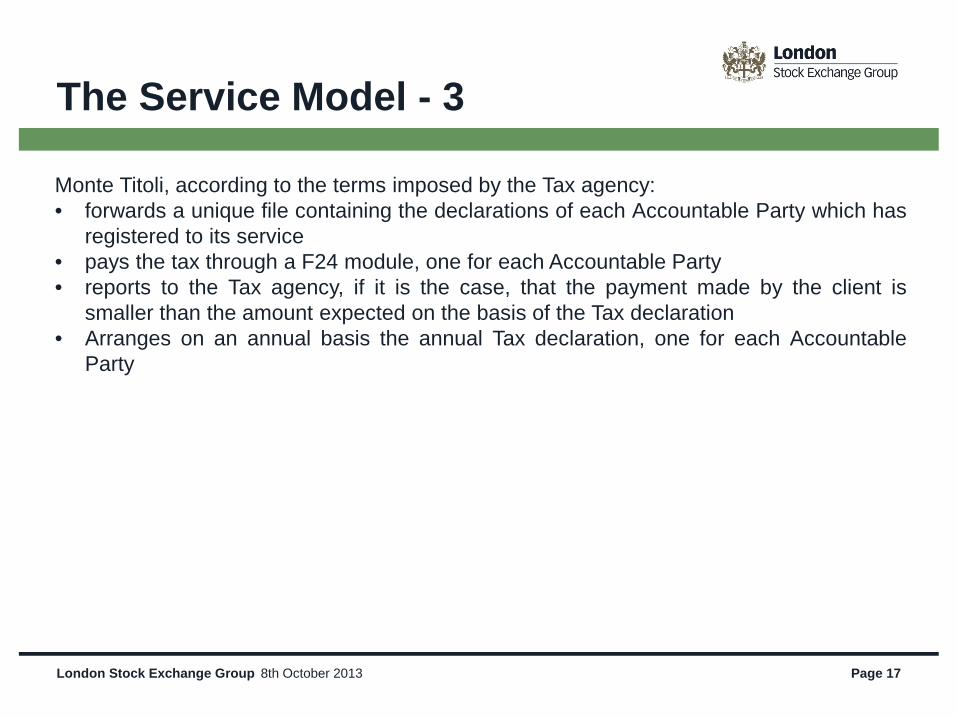

Monte Titoli, according to the terms imposed by the Tax agency: • forwards a unique file containing the declarations of each Accountable Party which has

registered to its service • pays the tax through a F24 module, one for each Accountable Party • reports to the Tax agency, if it is the case, that the payment made by the client is

smaller than the amount expected on the basis of the Tax declaration • Arranges on an annual basis the annual Tax declaration, one for each Accountable

Party

The Service Model - 3

8th October 2013

London Stock Exchange Group Page 18

Web interface

8th October 2013

Web interface- Login

London Stock Exchange Group Page 19 8th October 2013

Web interface– Accountable Parties

London Stock Exchange Group Page 20 8th October 2013

Web interface - Upload

London Stock Exchange Group Page 21 8th October 2013

Web interface– Data inquiry

London Stock Exchange Group Page 22 8th October 2013

Payment and declaration

London Stock Exchange Group Page 23

The first payment was originally due on the 16 October, also for those who operate through Monte Titoli

We decided to guarantee an extension of the deadline for declaration and payment until 31 October, as the payment to be done by Monte Titoli is due on 16 November (as according to the law Monte Titoli pays one month after the relevant tax amount has been received)

Such extension is given only for the first deadline, to offer more flexibility and allow all clients to take the necessary actions to meet the deadline

8th October 2013

Documentation and pricing

London Stock Exchange Group Page 24

The contract and the Service Model in the English version are already available on Monte Titoli’s website.

Indicative pricing will be € 50 for each month and each Accountable Party (subject to an initial period of volumes monitoring)

8th October 2013

London Stock Exchange Group Page 25

Contract framework

8th October 2013

Contract framework

London Stock Exchange Group Page 26

Monte Titoli has defined a contractual model for each entity responsible for the payment of the Tax and those who operate through Monte Titoli’s iFTT service; such entities should identify themselves as:

Responsible for the Tax payment

Stable Organization («Stabile organizzazione») of non-resident Subjects responsible for the Tax payment

Tax Agent of Subjects Responsible for the Tax Payment

The contract includes a Service Documentation, which defines in detail the participation rules

8th October 2013

Contract– main client’s duties

London Stock Exchange Group Page 27

The contract defines the client’s obligation regarding the fulfillment of the Tax and declaration duties according to Law 228/2011, the Minister of Finance Decree and relative implementation provisions

In particular, the client is obliged to:

a) send to Monte Titoli the information used to compute the Tax amount, which are necessary to conciliate the payment and fulfill the declaration duties imposed by the Law and the Decree, according to the modality and terms included in the Service Documentation

b) to pay the Tax amount to Monte Titoli, on the base of the terms and conditions specified in the Service Documentation and selected by the Client the contract

8th October 2013

London Stock Exchange Group Page 28

By signing the contract, the client delegates Monte Titoli (in quality of Central Depository as in article 80 of D.Lgs 58/98) to provide for the payment of the Tax on financial transactions and to fulfill the relevant declarative duties according to article 19.5 of the Decree.

The contracts allows to delegate the Service management to a third party

In this sense, the third party must be identified by filling in the specific part of the contract

It is important to highlight that the delegation does not imply any modification in the responsibility of the client, who will in any case be liable for the correct accomplishment of the Tax duty and for the relative instrumental obligations, according to the Law and to the Decree

Contract– mandate to a third party

8th October 2013

London Stock Exchange Group Page 29

Monte Titoli has created a dedicated section of www.montetitoli.com, accessible form the main page as: Monte Titoli's service for the Italian FTT: quick link

It contains: Regulatory framework, Contracts, Operating Model, Test Plan, CSV files templates, Contact Details, Q&A

Next steps:

- Clients can already send us the signed contract to: [email protected]

- External testing commences on 9 October

- Tentative go live date 22 October, to be confirmed ASAP

Web-information

8th October 2013

London Stock Exchange Group Page 30

Contacts Luca Silano Head of Customer Support

[email protected] T +39 02 33635359

Alessandro Zignani Head of Post Trade Sales

[email protected] T +39 02 33635 212; M +39 366 6120430

Cristina Belloni Senior Sales

[email protected] T +39 02 72426504; M +39 335 1041561

Fabrizio Plateroti Head of Regulation

[email protected] T +39 02 72426383

8th October 2013

The publication of this document does not represent solicitation, by Borsa Italiana S.p.A., of public saving and is not to be considered as a recommendation by Borsa Italiana as to the suitability of the investment, if any, herein described.This document has not to be considered complete and it is meant for information and discussion purposes only. Borsa Italiana accepts no liability, arising, without limitation to the generality of the foregoing, from inaccuracies and/or mistakes, for decisions and/or actions taken by any party based on this documents. Trademarks Cassa di Compensazione e Garanzia and CC&G are owned by Cassa di Compensazione e Garanzia S.p.A. Trademarks Monte Titoli, X-TRM and MT-X are owned by Monte Titoli S.p.A. London Stock Exchange, the coat of arms device and AIM are a registered trade mark of London Stock Exchange plc. The above trademarks and any other trademark owned by the London Stock Exchange Group cannot be used without express written consent by the Company having the ownership of the same. Borsa Italiana S.p.A. and its subsidiaries are subject to direction and coordination of London Stock Exchange Group Holdings (Italy) Ltd – Italian branch. The Group promotes and offers the post-trading services of Cassa di Compensazione e Garanzia S.p.A. and Monte Titoli S.p.A. in an equitable, transparent and non-discriminatory manner and on the basis of criteria and procedure aimed at assuring interoperability, security and equal treatment among market infrastructures, to all subjects who so request and are qualified in accordance with national and community legislation, applicable rules and decisions of the competent Authorities.

London Stock Exchange Group Page 31 8th October 2013