monitoring of construction projects for third-party funders and investors

TRANSCRIPT

Monitoring of constructionprojects for third-party fundersand investorsStephen PorterReceived (in revised form): 6th August, 2002

AbstractThis paper examines the practical role of professional advisers tofunders and investors on real estate projects. It emphasises theadvantages of an early appointment and will differentiate betweenthe services and skills required during the due diligence andmonitoring phases. It also explains the different types of serviceneeded depending on the level of project and funding risk andconcludes by highlighting and explaining the use of riskassessment and management during the project evaluation andimplementation.

INTRODUCTIONIt was the best of times; it was the worst of times. A major realestate funding/investment deal has just been signed up but now theproblems are starting to come out of the woodwork:

. the project cost is escalating

. there are planning difficulties

. the programme is extending etc etc.

Real estate and construction deals are almost always a nightmare.This probably sounds familiar, but need it be the norm? The answeris emphatically ‘No’.This paper will explain how the early appointment of an

experienced specialist consultant can assist the funder/investor inchoosing the right project and significantly reduce his risk byallowing him to make informed decisions based on realisticindependent assessments.

THE CLIENTThe nature of the client and the type of proposed funding is key tothe whole process of designing and implementing the professionalservice. The client may be public or private; the funding may rangefrom an overdraft facility through a grant to purchase of thecompleted investment. Each has its own particular level of risk andrequires a tuned response.The public sector client may be handling funds from a diverse

range of sources including local ones, eg local authorities, regional

Stephen Porter

is a chartered surveyor with

worldwide project experience

as a client, consultant and

contractor. He was previously

head of projects at British

Airways and MD of Arnold

Project Services, a leading

City-based project

management firm. He has

acted for public and private

sector funders and investors on

projects costing over £1bn.

Keywords:

fund monitoring, project monitoring,

development funding, public sector

funding, risk management

Stephen PorterAppleyards Ltd72 Brighton RoadHorshamWest Sussex RH13 5BU, UKTel: +44 (0)8705 275 201Fax: +44 (0)8705 143 047E-mail: [email protected]

# HENRY S T EWART PUB L I C A T I ONS 14 7 3 – 1 8 9 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 2 NO . 3 P P 2 11 – 2 2 0 211

ones, eg regional development agencies, national ones, eggovernment offices, European ones, eg the European RegionalDevelopment Fund and international ones, eg the World Bank.Requirements may be commercial, social or even altruistic andresults may be measured in project delivery or required outcomes oroutputs. Typically these could include:

. delivery within capital budget

. producing required number of visitors — paid or free entry

. job creation

. increased communications between religious/ethnic communities

. set return on capital.

Inevitably, because of the need for public accountability, theadministrative requirements will be demanding and, because apackage of different funding sources will be used, diverse. It isunfortunate that many of the public funding bodies, while maybehaving different required outputs for the same project, have totallydifferent bid requirements, contracts and reporting processes. This isthe case with the four remaining National Lottery bodies in the UK,ie Sport, Arts, Heritage and New Opportunities, although it isunderstood that efforts are being made to harmonise the situation.The private sector client could be a bank, fund, developer/funder

or purchaser with an involvement ranging from an overdraft facility,guarantee through debt and equity finance to outright purchase.Increasingly there are also those projects where there is joint public

and private funding, typical of which are Lottery-funded projectswhere 50 per cent of the funding will be provided by the Lottery fundwith the other half having to be found from a combination of otherpublic funds, private donations, commercial funding, sponsorship etc.Irrespective of which sector a client is in, the complications willincrease as often their respective objectives will differ, if not clash,leading to more complicated documentation especially in areas such asinter-creditor agreements, deeds of dedication etc. A topical exampleof this is the question of naming rights.In all cases it is clear that the business needs are different and

consequently so should the professional service provided bedifferent. The ‘one fits all’ service ends up fitting no one. To designand provide a tailored service therefore the consultant needs first tounderstand his client’s business objectives particularly in respect of:

. availability of funds

. return requirements

. risk constraints

. legal and administrative constraints

. other business critical systems

and then the economic, financial and often political characteristics

Public sector clients

Private sector clients

Porter

# HENRY S T EWART PUB L I C A T I ONS 1473 ^189 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 2 NO . 3 P P 2 11 – 2 2 0212

of the proposed project. This will inevitably require an ability toread and understand a business plan.However, it must be stressed that this is not, in itself, an economic

or business review but a review of the real estate and capital projectaspects which form a critical element of the business plan. Neither isit necessary to have an in-depth knowledge of the above but ratheran appreciation of those elements that are critical to the project’ssuccess.Major projects frequently have several monitoring consultants

working at the same time, the so-called ‘fleas on the back of fleas’.The writer has observed five on one public/private project. This notonly increases the sponsor’s and the design team’s workload butleads to frustration with the role of the consultant itself. Whilerecognising that different funds have different requirements, there issurely a case to be made for a single joint appointment, which willnot only reduce costs but should lead to an improved standard ofservice.

THE CONSULTANTConsultants come under many names: fund monitor, technicaladvisor, third-party consultant etc and typically are provided byquantity surveying or real estate consultancies. Notwithstandingthis, it is perhaps more appropriate to look at the actual skills thatmay be needed.

Due diligence. an in-depth understanding of the project delivery process. a detailed knowledge of public and or private sector funding. an understanding of business plans. an understanding of clients in general. an in-depth understanding of project costs, programmes and

specifications. an understanding of the real estate market. an understanding of the relevant legal agreements. an understanding of good design. an understanding of costs in use and fund monitor costs. a detailed knowledge of the best project management practices. an in-depth understanding of risk management.

Monitoring. a detailed knowledge of detailed design and specification. a detailed knowledge of good construction management. an excellent understanding of building contracts. an excellent understanding of commercial management. an in-depth understanding of construction valuation and

certification.

It would be rare, on a complex deal, for these skills to beprovided by a single individual and, in particular, the

Skills required

Monitoring of construction projects for third-party funders and investors

# HENRY S T EWART PUB L I C A T I ONS 14 7 3 – 1 8 9 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 2 NO . 3 P P 2 11 – 2 2 0 213

differentiation between the skills required for due diligence andmonitoring will often, advisably, be provided separately albeitwithin the same organisation. In addition, depending on thecomplexity of the project itself, it will be sensible for theconsultant to sub-contract certain areas such as the review ofmechanical and electrical services.Given the time constraints under which the consultant will

normally operate it is imperative that he has the ability, with limitedinformation, to identify potential problems before they occur andwarn his client so that remedial actions can be taken. Unfortunatelyit is often the case that the consultant is expert at telling his clientwhat went wrong after it has gone wrong!This expertise rarely comes without the consultant individually

having extensive experience of both the project processes in generaland the third-party consultancy in particular.It is easy for the consultant to be seen as undertaking a negative

role in that he or she is normally identifying either what has notbeen done or what has not been done correctly. If this is true, as itoften is, then he or she is not acting in their client’s interest. Asstated above it is the success of the business that generates theoutputs that enable the client to meet business objectives. It shouldbe, therefore, the duty of the consultant to assist and not inhibitthose objectives. This can only be achieved if the project’s andclient’s businesses are properly understood.

THE PROJECTAlthough project types can vary considerably, it is not a detailedknowledge of the project type that is important but rather an in-depth understanding of the client, good practices and businessobjectives. Although it is a belief prevalent among most projectteams that the built project is an end in itself, this is rarely the case.Most buildings are an envelope in which the real business iscontained and it is this business that will generate the profits,outcomes and outputs on which the funders and investors will relyto satisfy their business requirements. An award-winning project,built on time and to budget but which does not meet its businessplan objectives, will probably fail, to everyone’s discomfort.Most clients are naturally unwilling to commit to paying fees too

early in their appraisal process, nevertheless an initial quick reviewby the consultant may highlight issues which can be changed moreeasily at this stage or result in his withdrawing and thereby avoidinghigher later abortive fees.

Due diligenceDue diligence is 85 per cent perspiration and 15 per centinspiration. Without undertaking the perspiration it is unlikelythat the inspiration can be revealed, however, just doing theperspiration does not mean that the inspiration will come and this

Early appointment

Porter

# HENRY S T EWART PUB L I C A T I ONS 1473 ^189 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 2 NO . 3 P P 2 11 – 2 2 0214

may be the difference between a successful and unsuccessfulinvestment.Modern agreements are frequently measured in metres rather than

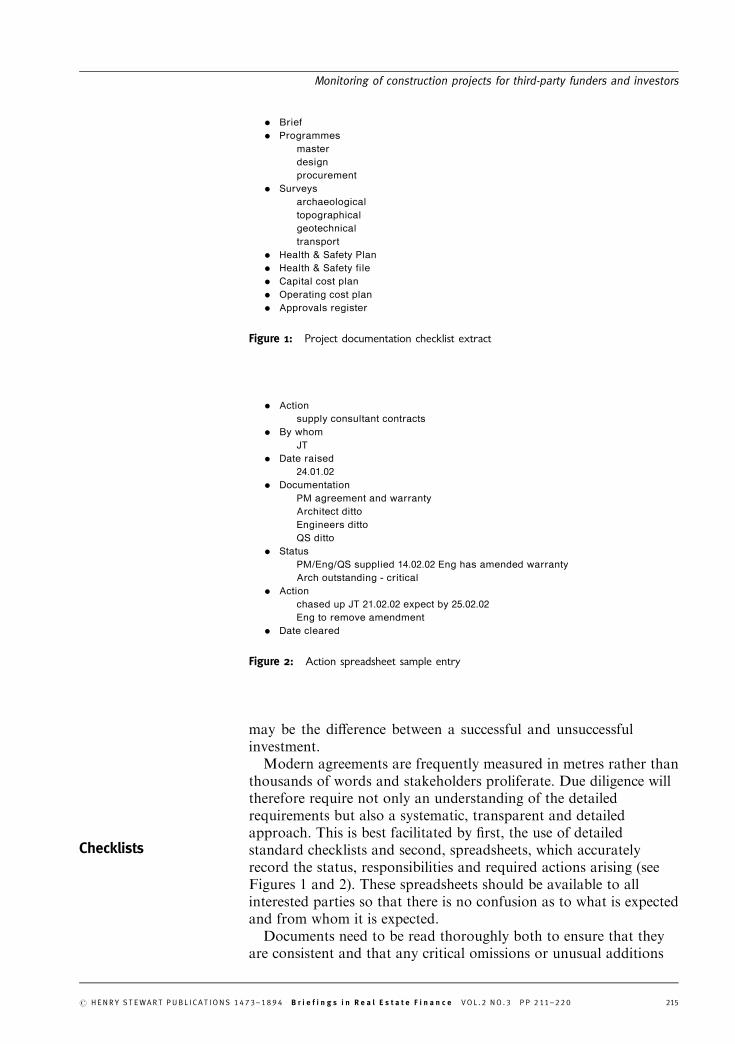

thousands of words and stakeholders proliferate. Due diligence willtherefore require not only an understanding of the detailedrequirements but also a systematic, transparent and detailedapproach. This is best facilitated by first, the use of detailedstandard checklists and second, spreadsheets, which accuratelyrecord the status, responsibilities and required actions arising (seeFigures 1 and 2). These spreadsheets should be available to allinterested parties so that there is no confusion as to what is expectedand from whom it is expected.Documents need to be read thoroughly both to ensure that they

are consistent and that any critical omissions or unusual additions

Checklists

. Brief

. Programmes

master

design

procurement

. Surveys

archaeological

topographical

geotechnical

transport

. Health & Safety Plan

. Health & Safety file

. Capital cost plan

. Operating cost plan

. Approvals register

Figure 1: Project documentation checklist extract

. Action

supply consultant contracts

. By whom

JT

. Date raised

24.01.02

. Documentation

PM agreement and warranty

Architect ditto

Engineers ditto

QS ditto

. Status

PM/Eng/QS supplied 14.02.02 Eng has amended warranty

Arch outstanding - critical

. Action

chased up JT 21.02.02 expect by 25.02.02

Eng to remove amendment

. Date cleared

Figure 2: Action spreadsheet sample entry

Monitoring of construction projects for third-party funders and investors

# HENRY S T EWART PUB L I C A T I ONS 14 7 3 – 1 8 9 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 2 NO . 3 P P 2 11 – 2 2 0 215

are noted. When reporting to the client it is important to rank thecomments so that the showstoppers are clearly identifiable from thenice-to-haves. This will require the consultant to utilise his in-depthexperience of the documentation but even then prudence needs to beexercised and apparently unimportant comments should not beomitted.It will be normal to comment on the projected estimate and

programme for the project, as these will be critical, to greater orlesser extents, to the success of the business. In the writer’sexperience there are often enormously detailed comments such as‘the rate for the formwork is low’ or ‘the duration for first fixelectrical installations is excessive’ while missing the fact that theoverall costs per sq.m and design programme are unachievable.The nature of the project type will be critical to the level of

comment required. With a standard building type, such as acommercial office or warehouse development, care will be needed toexamine the abnormals that might cause it to differ from theexpected range of costs and programmes. It will often be the casethat the key in these cases will be the ability of the team andstrategy to deliver.Projects are often, however, not standard types but one offs,

projects which are either unique in their design solutions or rarelybuilt at all. These inevitably require special and close attention notjust because of the difficulty in estimating their cost and theprogramme but also, and perhaps more significantly, their effect onthe businesses they contain. While it is undoubtedly true that hewho dares architecturally may win spectacularly, he may also fail —spectacularly.The key for these projects is:

. to ensure that the business and design briefs have beenthoroughly prepared

. the design has reached at least stage D and has been tested by theproject sponsor.

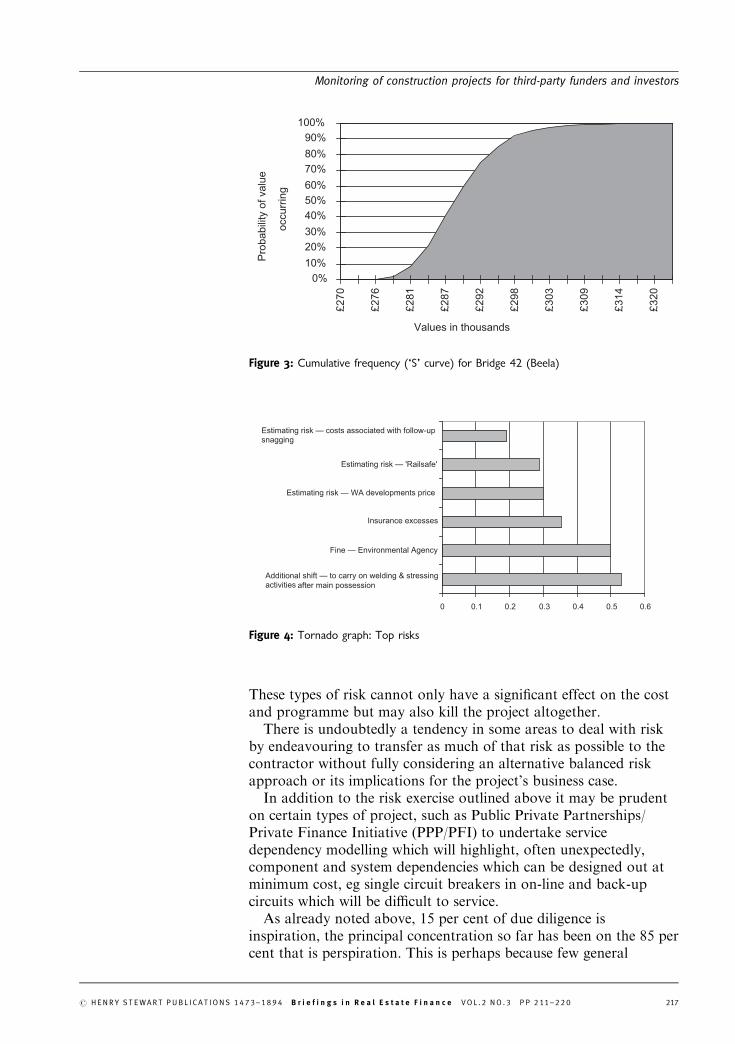

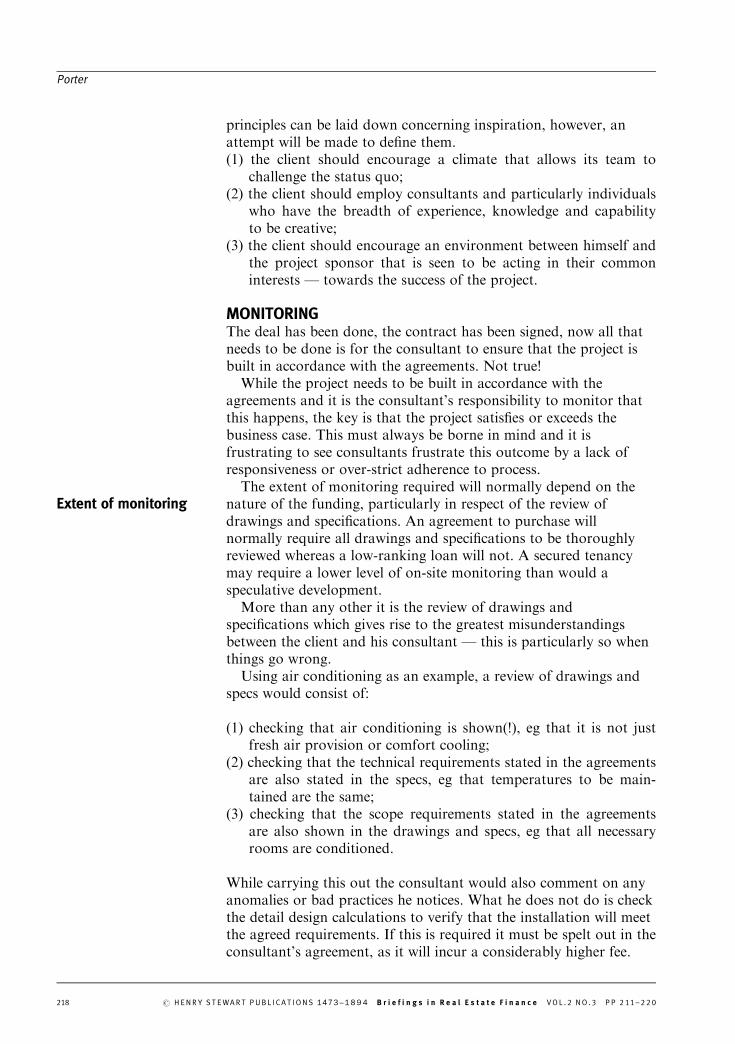

However, there is still one key outstanding exercise to be carried outby the consultant and this is not done often enough — a quantifiedrisk assessment (see Figures 3 and 4).While it is not unusual for risk assessments to be undertaken by

banks/funds, they rarely go into sufficient enough detail with respectto the real estate/building project either to identify the potentialcost/programme ranges or, more importantly, the risk ameliorationmeasures which may be open to them. As well as the usual cost andprogramme underestimating risks, it is the major project-specificrisks that need to be identified and quantified, eg

. ground conditions

. political risks

. client organisation

. co-funding.

One off projects

Risk assessments

Porter

# HENRY S T EWART PUB L I C A T I ONS 1473 ^189 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 2 NO . 3 P P 2 11 – 2 2 0216

These types of risk cannot only have a significant effect on the costand programme but may also kill the project altogether.There is undoubtedly a tendency in some areas to deal with risk

by endeavouring to transfer as much of that risk as possible to thecontractor without fully considering an alternative balanced riskapproach or its implications for the project’s business case.In addition to the risk exercise outlined above it may be prudent

on certain types of project, such as Public Private Partnerships/Private Finance Initiative (PPP/PFI) to undertake servicedependency modelling which will highlight, often unexpectedly,component and system dependencies which can be designed out atminimum cost, eg single circuit breakers in on-line and back-upcircuits which will be difficult to service.As already noted above, 15 per cent of due diligence is

inspiration, the principal concentration so far has been on the 85 percent that is perspiration. This is perhaps because few general

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

£2

70

£2

76

£2

81

£2

87

£2

92

£2

98

£3

03

£3

09

£3

14

£3

20

Values in thousands

Pro

babili

ty o

f valu

e

occu

rrin

g

Figure 3: Cumulative frequency (‘S’ curve) for Bridge 42 (Beela)

0 0.1 0.2 0.3 0.4 0.5 0.6

Additional shift — to carry on welding & stressing activities after main possession

Fine — Environmental Agency

Insurance excesses

Estimating risk — WA developments price

Estimating risk — 'Railsafe'

Estimating risk — costs associated with follow-up snagging

Figure 4: Tornado graph: Top risks

Monitoring of construction projects for third-party funders and investors

# HENRY S T EWART PUB L I C A T I ONS 14 7 3 – 1 8 9 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 2 NO . 3 P P 2 11 – 2 2 0 217

principles can be laid down concerning inspiration, however, anattempt will be made to define them.(1) the client should encourage a climate that allows its team to

challenge the status quo;(2) the client should employ consultants and particularly individuals

who have the breadth of experience, knowledge and capabilityto be creative;

(3) the client should encourage an environment between himself andthe project sponsor that is seen to be acting in their commoninterests — towards the success of the project.

MONITORINGThe deal has been done, the contract has been signed, now all thatneeds to be done is for the consultant to ensure that the project isbuilt in accordance with the agreements. Not true!While the project needs to be built in accordance with the

agreements and it is the consultant’s responsibility to monitor thatthis happens, the key is that the project satisfies or exceeds thebusiness case. This must always be borne in mind and it isfrustrating to see consultants frustrate this outcome by a lack ofresponsiveness or over-strict adherence to process.The extent of monitoring required will normally depend on the

nature of the funding, particularly in respect of the review ofdrawings and specifications. An agreement to purchase willnormally require all drawings and specifications to be thoroughlyreviewed whereas a low-ranking loan will not. A secured tenancymay require a lower level of on-site monitoring than would aspeculative development.More than any other it is the review of drawings and

specifications which gives rise to the greatest misunderstandingsbetween the client and his consultant — this is particularly so whenthings go wrong.Using air conditioning as an example, a review of drawings and

specs would consist of:

(1) checking that air conditioning is shown(!), eg that it is not justfresh air provision or comfort cooling;

(2) checking that the technical requirements stated in the agreementsare also stated in the specs, eg that temperatures to be main-tained are the same;

(3) checking that the scope requirements stated in the agreementsare also shown in the drawings and specs, eg that all necessaryrooms are conditioned.

While carrying this out the consultant would also comment on anyanomalies or bad practices he notices. What he does not do is checkthe detail design calculations to verify that the installation will meetthe agreed requirements. If this is required it must be spelt out in theconsultant’s agreement, as it will incur a considerably higher fee.

Extent of monitoring

Porter

# HENRY S T EWART PUB L I C A T I ONS 1473 ^189 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 2 NO . 3 P P 2 11 – 2 2 0218

As well as monitoring the design and construction process, theconsultant needs to communicate his findings to his client and makehis recommendations for payment. The format and timing for thisshould be agreed on a project by project basis with his client, butshould contain the following principles:

. be brief and to the point

. have an executive summary with comments

. report on time, cost, management and quality

. forecast outturn cost and programme

. highlight key risks and actions being taken

. highlight key outstanding decisions to be taken

and not just repeat, parrot fashion, information supplied to theconsultant by the design team.

CLOSE OUTIt is all too common to witness projects that have been built welland then handed over poorly, resulting in disgruntled clients and de-motivated teams. In so far as it is possible, the consultant shouldensure that adequate time is allowed for completion, includingtesting and commissioning, final inspections and completion of handover documentation. This is best dealt with by the inclusion ofappropriate clauses in the funding/purchase agreements.Approval/certification of completion will also vary in accordance

with the agreements, but to varying degrees will comprise:

. visual inspection of completed works

. witnessing of system checks

. receipt of approved documentation

. review of agreements to check compliance

. review of correspondence etc to check compliance.

It is also recommended that completion under the agreements shouldbe distinct and separate from practical completion under the buildingcontract, it being a condition precedent to the former.On projects such as PPP/PFI which have medium and long-term

project commitments, completion will also need to include verifyingthat certain outputs are met, which can only be done after theproject is in operation. Similarly, this may be required for periodslong after completion depending on both the duration of thefunding agreement and the project contract.No project should be considered as complete until a post-

completion review is undertaken. This should include reviews of:

. adequacy of agreements

. processes and procedures

. performance of team

. performance of project

Communications

Post completionreview

Monitoring of construction projects for third-party funders and investors

# HENRY S T EWART PUB L I C A T I ONS 14 7 3 – 1 8 9 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 2 NO . 3 P P 2 11 – 2 2 0 219

highlighting both successes and failures and makingrecommendations for the future. In particular, performance againstcontract criteria should also be measured and reasons stated forunder/over performance, eg

. net/gross areas

. maintenance costs

. functional availability.

CONCLUSIONSThe employment of consultants to undertake the monitoring ofconstruction projects for third-party investors/funders is often givenlittle thought both by clients and the consultants themselves. Thisfails to recognise the value they can add both to the project itselfand to their client’s success.Their early employment can result in unsuitable deals being

abandoned or improvements to the project’s risk profile beingobtained. The use of appropriately qualified and experienced staffwill further reduce the risk of project cost and time overruns andenhance the project’s out-turn business viability.

‘If you pays your money you must make the right choices’.

Porter

# HENRY S T EWART PUB L I C A T I ONS 1473 ^189 4 B r i e f i n g s i n R e a l E s t a t e F i n a n c e VO L . 2 NO . 3 P P 2 11 – 2 2 0220