money-time relationships …and equivalence (or make money slowly)

TRANSCRIPT

Money-Time Relationships

…and equivalence

(or MAKE MONEY SLOWLY)

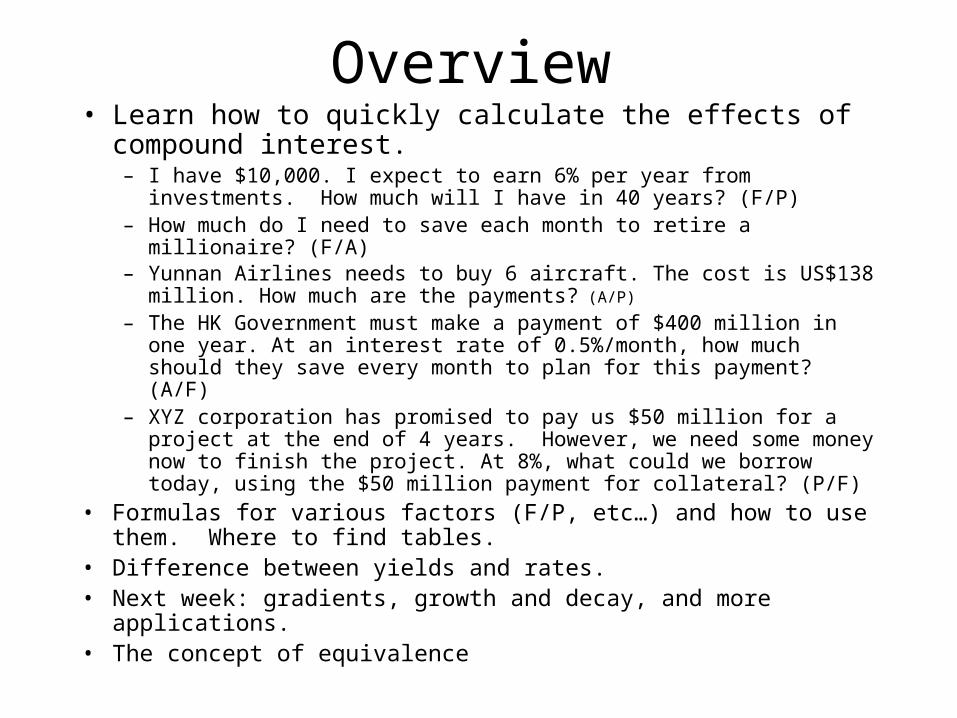

Overview• Learn how to quickly calculate the effects of compound

interest.– I have $10,000. I expect to earn 6% per year from investments. How

much will I have in 40 years? (F/P) – How much do I need to save each month to retire a millionaire? (F/A)– Yunnan Airlines needs to buy 6 aircraft. The cost is US$138 million. How

much are the payments? (A/P)

– The HK Government must make a payment of $400 million in one year. At an interest rate of 0.5%/month, how much should they save every month to plan for this payment? (A/F)

– XYZ corporation has promised to pay us $50 million for a project at the end of 4 years. However, we need some money now to finish the project. At 8%, what could we borrow today, using the $50 million payment for collateral? (P/F)

• Formulas for various factors (F/P, etc…) and how to use them. Where to find tables.

• Difference between yields and rates.• Next week: gradients, growth and decay, and more applications.• The concept of equivalence

Three Kinds of Money• Present money (year zero dollars)• Future money (year N dollars)• Flows of money over time

($/year, $/month)Later we will discuss the concept of equivalence.

We know that 1kg = 2.2 pounds. We also know that 2.54cm = 1 inch. If you buy something by the kilo or by the inch, you always know the equivalent amounts in pounds or cm.

The three kinds of money can be thought of in the same way. We will come back to this later.

MAKE MONEY FAST

‘Pyramid schemes’ - the person at the top makes all the money, and the people at the bottom lose.

• Chain letter is one example of a pyramid scheme. You can find a copy at this this web site and an analysis by the same person here.

• Ponzi scheme. EARN 100% in 6 months! What you don’t know is that investors are being cheated – there is no investment. “Profits” are actually being paid out of the amount borrowed from investors. At some point, the people borrowing the money disappear!

• You can avoid these scams by using the MAKE MONEY SLOWLY technique.

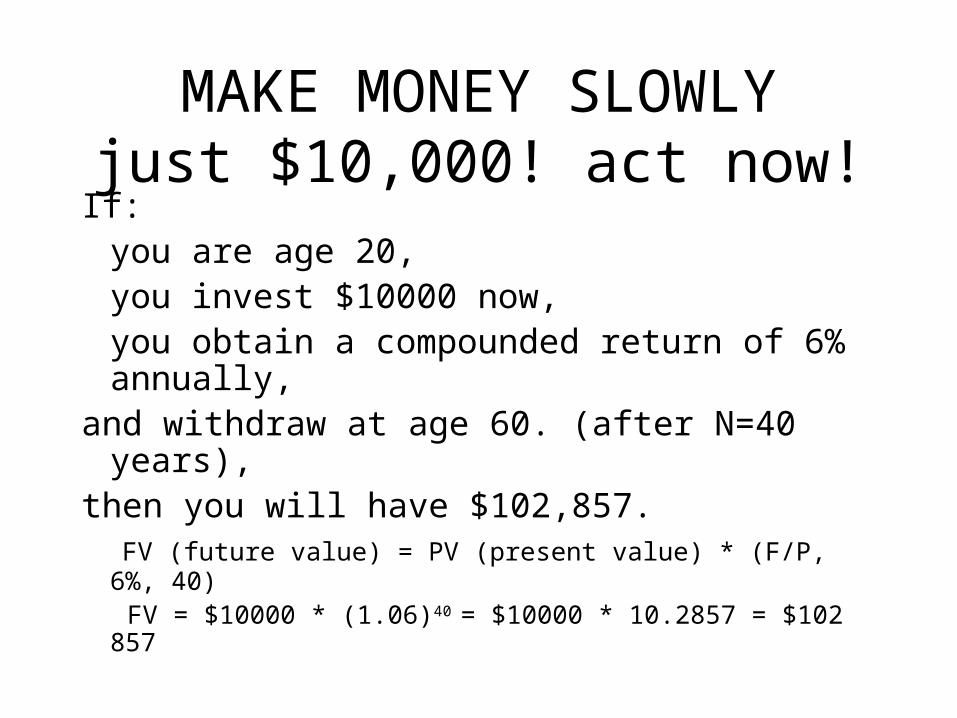

MAKE MONEY SLOWLYjust $10,000! act now!

If:you are age 20,you invest $10000 now,you obtain a compounded return of 6% annually,

and withdraw at age 60. (after N=40 years),then you will have $102,857. FV (future value) = PV (present value) * (F/P, 6%, 40)

FV = $10000 * (1.06)40 = $10000 * 10.2857 = $102 857

BECOME A MILLIONAIREwith our easy payment plan!

Invest hk$10000 every year for 40 yearsObtain a compounded return of 6% annuallyWithdraw at age 60.FV = AV * (F/A, 6%, 40) Future Value Annual or Annuity Value (=$10000)FV = $10000 * ([(1.06)40 – 1 ] / 0.06) = $10000 * 154.762

(formula for F/A) (or see p.630 for a table)

= $1 547 620GUARANTEED TO WORK EVERY TIME! ACT

TODAY!

DON’T DELAYLIMITED TIME OFFER

Johnny waited until age 40, look what will happen:

(He will save $10,000/year for 20 years @ 6%)

(Finding FV is an F/A problem, where A=$10,000)

FV = $10000 * (F/A, 6%, 20)

=$10000 * ([(1.06)20-1]/0.06)

= $10000 * 36.7856

= $367 856 -- not bad

But Johnny lost out on being a millionaire!

Beware of Credit CardsThey just drain your money

Fred bought a new computer for $9 000 on a credit card that charged interest of 2%/month!

He makes the minimum payment of $250, how long will it take to pay off? How much will he pay? (This is a new type of problem. A “P/A” question)

PV = $9000; A=$250; i=2%/month N=#monthsFind N where PV = A * (P/A, 2%, N months) $9000 = $250 * (P/A, 2%, N months)(P/A, 2%, N months) = $9000/$250 = 36.0

The algebra is ugly on this one

We need N so that (P/A, 2%, N)=36.

If we look up the formula for P/A, we find that

(P/A,2%,N) = ([1-(1.02)-N]/0.02)

From the tables on p.627, we can see that N should be between N=60 (P/A=34.76) and

N=72 (P/A=37.98).

By trial and error via calculator, we can find N=64, with $19.65 balance for the final, 65th month.

See I told you so!

The total paid for the $9000 computer was

64 * $250 + 19.65 =

$16000 + $19.65 = $16019.65($9000 principal plus $7019.65 accumulated interest)

Quite a bit of money considering that, after 5 years and 4 months, the computer is now junk and Fred wants another one!

Ok. I can see there are some ‘tricks’ here that might be useful

to know. What is happening?1. Factors called P/F and F/P allow for a quick

way to work compound interest problems with single amounts.

Present Value = (P/F,i%,N) * Future Value

Future Value = (F/P,i%,N) * Present Value

Ok. I can see there are some ‘tricks’ here that might be useful

to know. What is happening?2. Factors called P/A and F/A allow for a quick way

to work compound interest problems with cash flows. The flow per period is called the annuity amount A.

If someone has promised me $A for N periods, and the prevailing interest rate is i%/period, what is this worth now (Present Value)?

Present Value = (P/A, i%, N) * A If I save $A for N periods, and the prevailing interest rate is i%/period,

how much will this be worth at period N ?

Future Value = (F/A, i%, N) * A

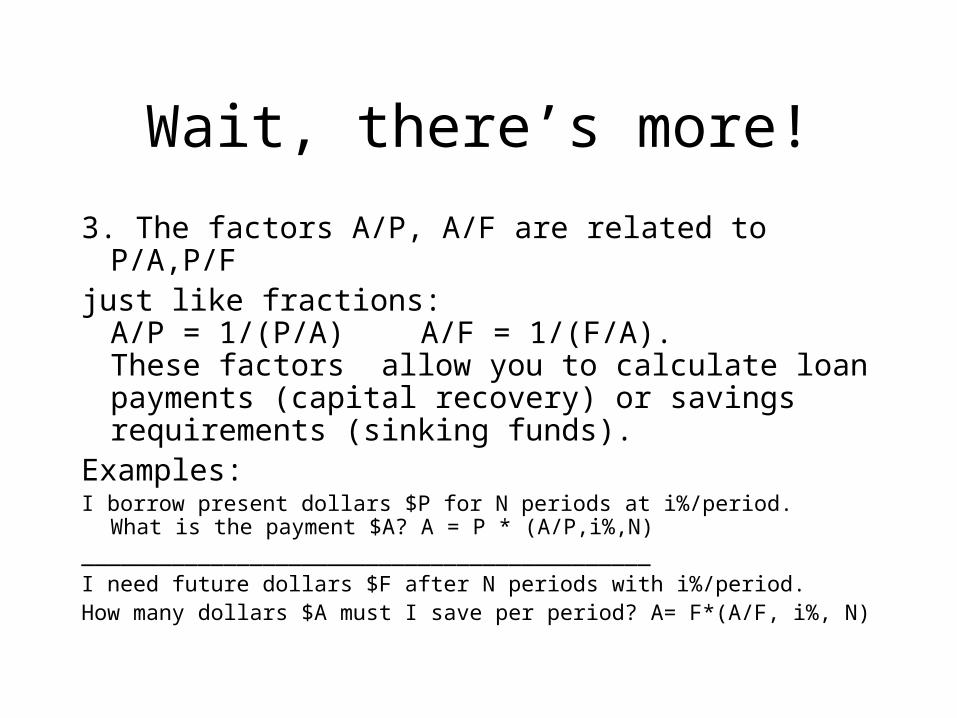

Wait, there’s more!

3. The factors A/P, A/F are related to P/A,P/F just like fractions:

A/P = 1/(P/A) A/F = 1/(F/A). These factors allow you to calculate loan payments (capital recovery) or savings requirements (sinking funds).

Examples:I borrow present dollars $P for N periods at i%/period.

What is the payment $A? A = P * (A/P,i%,N)____________________________________________I need future dollars $F after N periods with i%/period.How many dollars $A must I save per period? A= F*(A/F, i%, N)

Why waste words? Try pictures.

T=Time

T=0

T=N

$F

$P

Know F, need P? P = F * (P/F, i%, N)Know P, need F? F = P * (F/P, i%, N)

Annuity can be valued in future dollars $F or present dollars $P

T=TimeT=0 T=N

$F$PCash flows of $A at T=1,2,3,…,N

Need F, Know A? F = A * (F/A, i%, N)Need P, Know A? P = A * (P/A, i%, N)Need A, Know P? A = P * (A/P,i%,N)Need A, Know F? A = F * (A/F,i%,N)

Formulas [p.89]

)//(1)/(

)/(*)/(1)1(

)%,,/(

)//(1)/(

)1(1)1(

1)1()%,,/(

)1()%,,/(

)1()%,,/(

AFFA

PFAPi

iNiAF

APPA

ii

iii

NiAP

iNiPF

iNiFP

N

N

N

N

N

N

Remember this sum?

ii

iiiAPiz

zzzzz

finallyor

zzz

zzzzzz

zzzz

z

k

k

k

k

k

k

k

k

k

k

k

k

k

k

k

k

/1)11/(1

])1(1/[)1()%,,/()1(

streamcash long infinitelyan of PV just the is sum that thenote i)1/(1z if

)1/()1/(

,

)1(

...

...

then

)!(important 1|z| if

11

11

1

1

1

32

1

32

1

1

Deriving the P/A formula

N

N

N

k

NN

k

kN

k

N

Nk

k

k

k

Nk

k

Nk

kN

k

k

N

k

kN

k

k

N

k

ii

i

ii

ii

iii

ii

iii

XXii

kiFPNiAP

)1(

1)1(

/])1(1[

)i%,(P/A, is sum thenoteor 1/i, is sum that thenote

)1(])1(1[

)1()1()1(

)1()1(

)1()1()1(

)1()1(

)%,,/()%,,/(

1

11

11

111

11

1

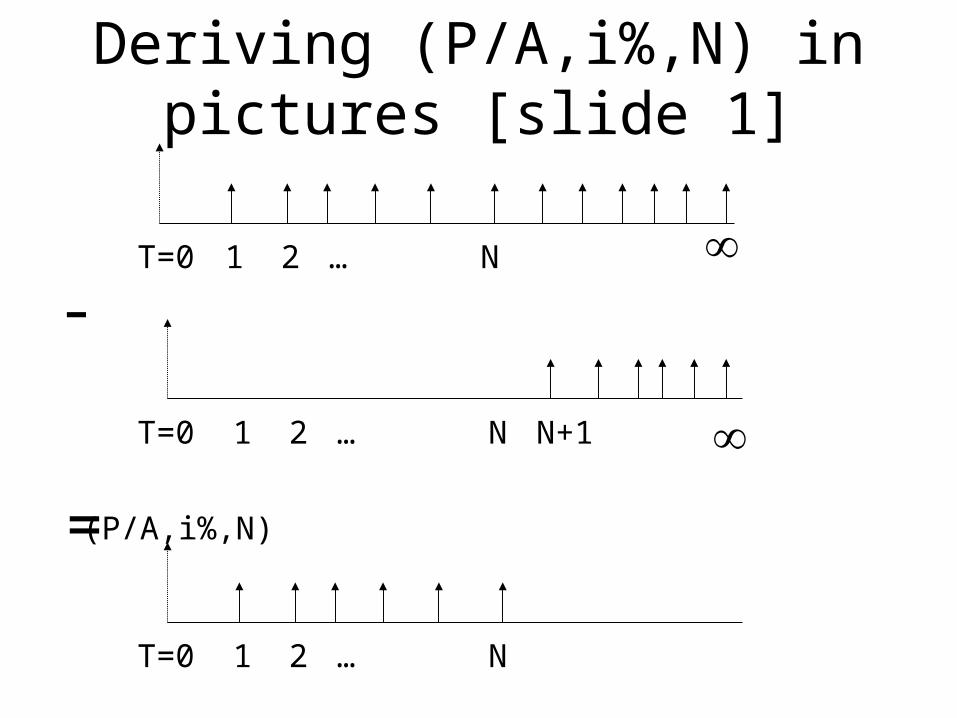

Deriving (P/A,i%,N) in pictures [slide 1]

T=0 1 2 … N

=

T=0 1 2 … N

T=0

-1 2 … N

N+1

(P/A,i%,N)

Deriving (P/A,i%,N) in pictures [slide 2]

T=0

(P/A,i%,N)=P1-P2=(1/i)(1-(1+i)-N)

1 2 … N

=

T=0

$P2=(P/F,i%,N)*(P/A,i%,)

=(1/i)(1+i)-N

1 2 … N

T=0

$P1=(P/A,i%,)=1/i

-1 2 … N

N+1

More examples – Yunnan Airlines

The SCMP reported that Bombardier aerospace, Canada, sold Yunnan Airlines 6 aircraft for a total of US$138 million.

If the aircraft are financed at 8%/year for 15 years, with (quarterly) payments due every 3 months, what is the quarterly payment?

Identify: N=4*15=60; i=8%/4=0.02; P=us$138million; need annuity payment A

Yunnan Airlines – Loan payment

A = P * (A/P, i%, N)A= us$138million * (A/P, 2%, 60) = $138,000,000 * [0.02/(1-(1.02)-60)] = us$138million * 0.0288

(see p.626 for table) = us$3.974 millionThe quarterly payment is approximatelyus$3 974 000

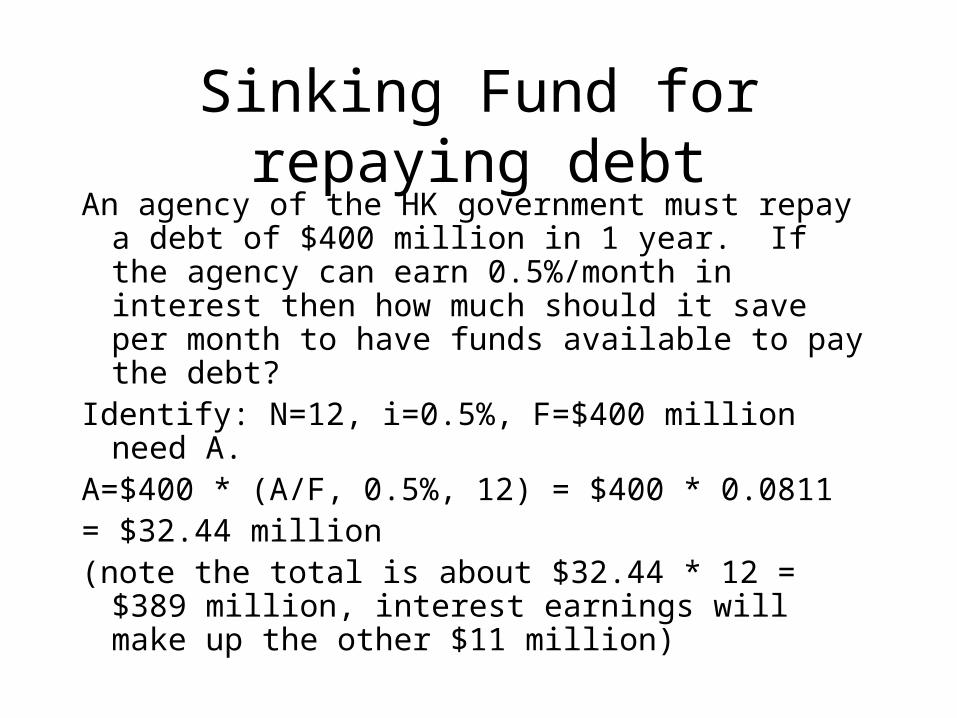

Sinking Fund for repaying debtAn agency of the HK government must repay a debt

of $400 million in 1 year. If the agency can earn 0.5%/month in interest then how much should it save per month to have funds available to pay the debt?

Identify: N=12, i=0.5%, F=$400 million need A.A=$400 * (A/F, 0.5%, 12) = $400 * 0.0811= $32.44 million(note the total is about $32.44 * 12 = $389 million,

interest earnings will make up the other $11 million)

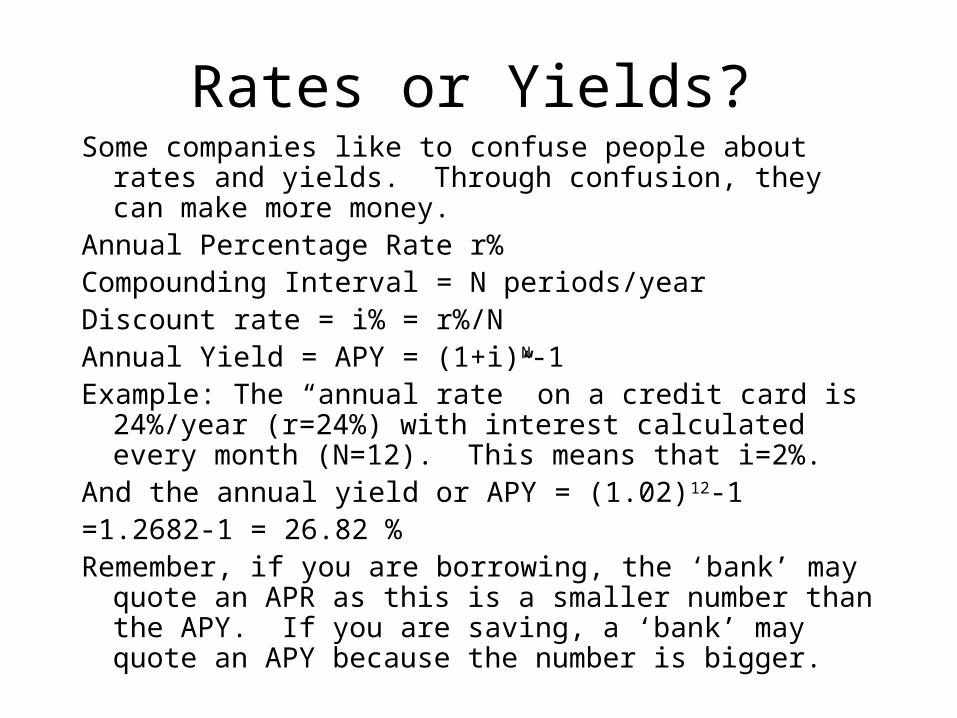

Rates or Yields?Some companies like to confuse people about rates and

yields. Through confusion, they can make more money.Annual Percentage Rate r%Compounding Interval = N periods/yearDiscount rate = i% = r%/NAnnual Yield = APY = (1+i)N-1Example: The “annual rate” on a credit card is 24%/year

(r=24%) with interest calculated every month (N=12). This means that i=2%.

And the annual yield or APY = (1.02)12-1=1.2682-1 = 26.82 %Remember, if you are borrowing, the ‘bank’ may quote an

APR as this is a smaller number than the APY. If you are saving, a ‘bank’ may quote an APY because the number is bigger.

Back to equivalence

In the introduction we gave an example that we haven’t solved yet:– XYZ corporation has promised to pay us $50 million for a project

at the end of 4 years. However, we need some money now to finish the project. At 8%, what could we borrow today, using the $50 million payment for collateral? (P/F)

The solution is easy.

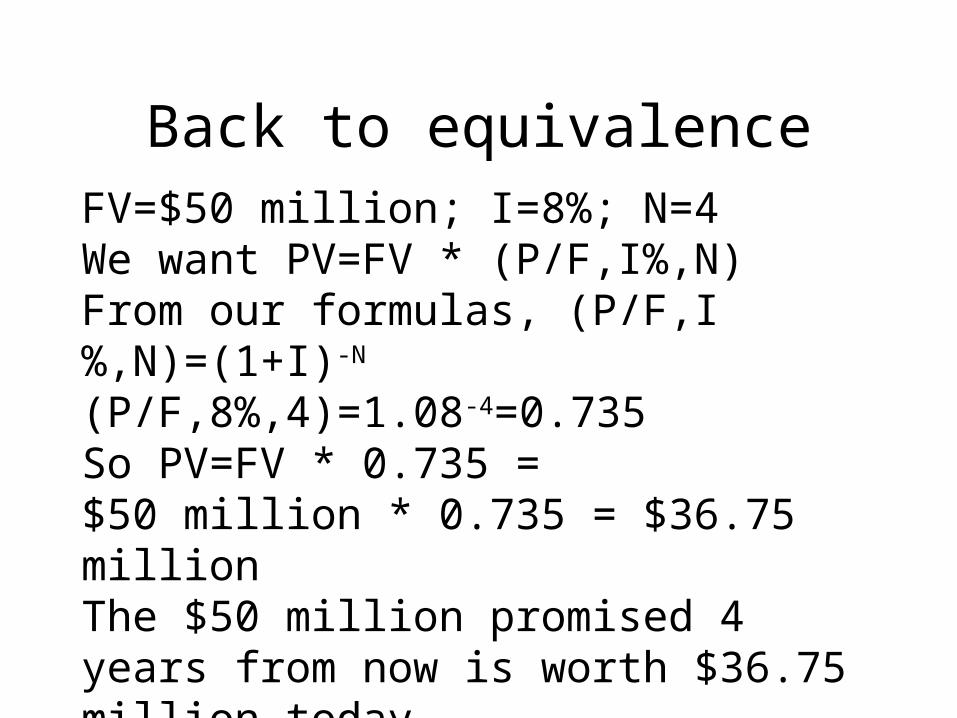

We have FV=$50 million; I=8%; N=4, and we want PV=FV * (P/F,I%,N)

Back to equivalenceFV=$50 million; I=8%; N=4We want PV=FV * (P/F,I%,N)From our formulas, (P/F,I%,N)=(1+I)-N

(P/F,8%,4)=1.08-4=0.735So PV=FV * 0.735 = $50 million * 0.735 = $36.75 millionThe $50 million promised 4 years from now is worth $36.75 million today.We can think of this as establishing an equivalence between money today and money tomorrow.

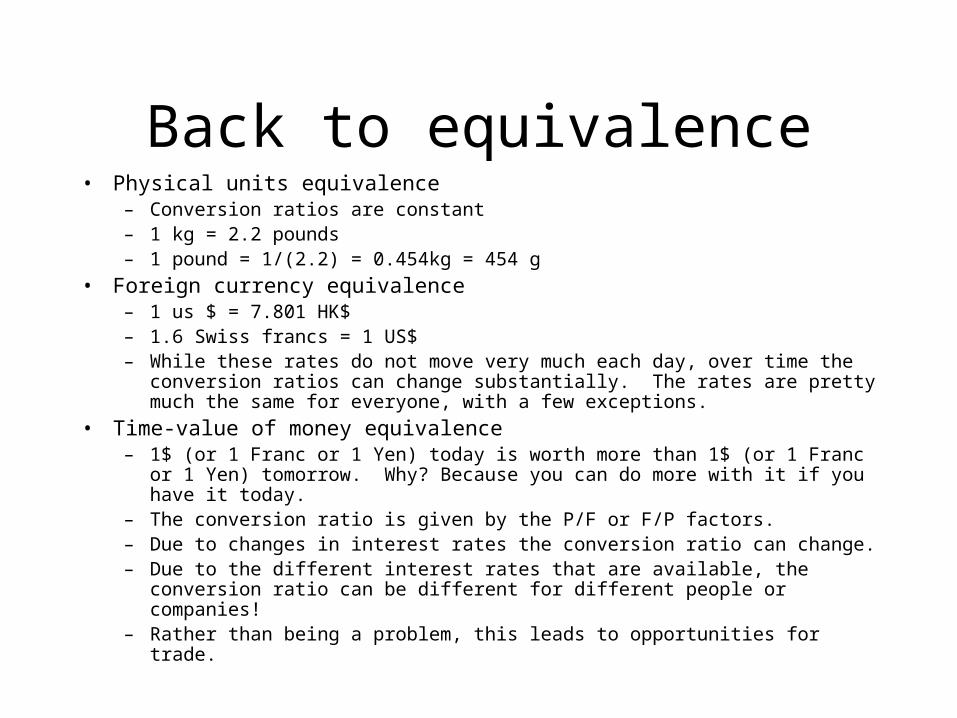

Back to equivalence• Physical units equivalence

– Conversion ratios are constant– 1 kg = 2.2 pounds– 1 pound = 1/(2.2) = 0.454kg = 454 g

• Foreign currency equivalence– 1 us $ = 7.801 HK$– 1.6 Swiss francs = 1 US$– While these rates do not move very much each day, over time the conversion ratios

can change substantially. The rates are pretty much the same for everyone, with a few exceptions.

• Time-value of money equivalence– 1$ (or 1 Franc or 1 Yen) today is worth more than 1$ (or 1 Franc or 1 Yen)

tomorrow. Why? Because you can do more with it if you have it today. – The conversion ratio is given by the P/F or F/P factors.– Due to changes in interest rates the conversion ratio can change.– Due to the different interest rates that are available, the conversion ratio can be

different for different people or companies!– Rather than being a problem, this leads to opportunities for trade.

Next week

Shortcuts for:Linear gradients

Exponential growth/decay

Additional applications

You should be reading chapter 3!