money management for medical school students for the class of 2018 nicole knight, mba aamc fall 2014...

TRANSCRIPT

Money Management for Medical School Students

For the Class of 2018

Nicole Knight, MBAAAMCFall 2014

Disclaimer: All information and estimates are based on AAMC interpretation of federal regulations as of June 2014 and are subject to change. These are estimates only. Students should always contact their servicer(s) to discuss the terms and conditions of the loans.

©2014 Association of American Medical Colleges. All rights reserved.

“…Students must arrive at the door of the house of medicine with an

enhanced awareness of how they will navigate the rising tide of medical

education debt …”

Refer to page iv

©2014 Association of American Medical Colleges. All rights reserved.

“Can Medical Students Afford to Choose Primary Care? An Economic Analysis of Physician Education Debt

Repayment”

“Physician Education Debt and the Cost to Attend

Medical School”

www.aamc.org/FIRST

©2014 Association of American Medical Colleges. All rights reserved.

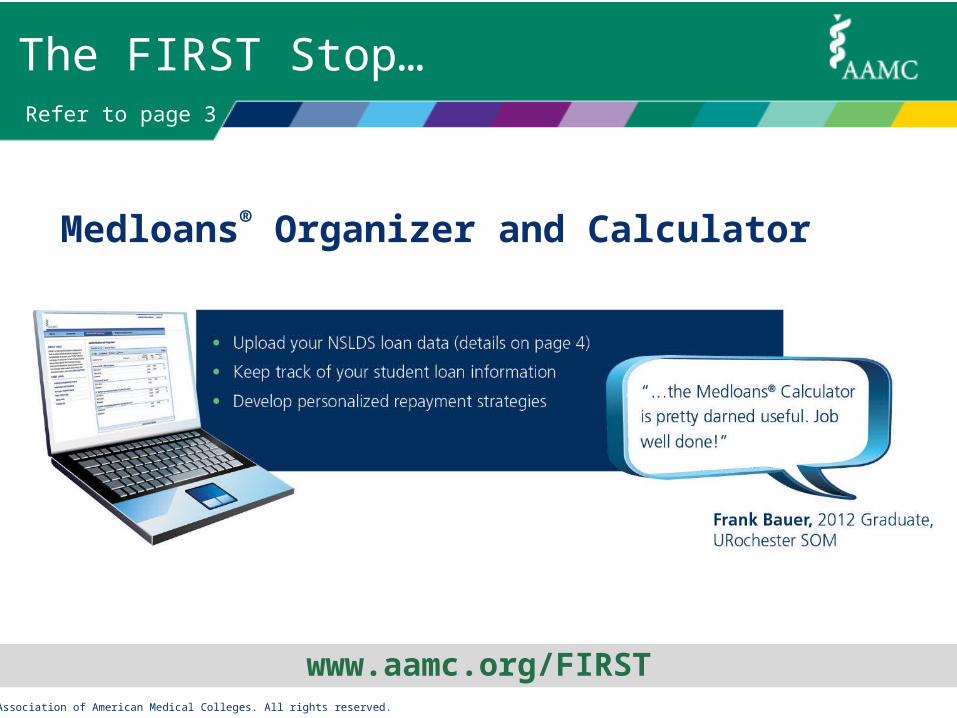

The FIRST Stop…

www.aamc.org/FIRST

Medloans® Organizer and Calculator

Refer to page 3

©2014 Association of American Medical Colleges. All rights reserved.

Class of 2013 Indebtedness

86% of class report having educational debt

Source: AAMC 2013 Graduate Questionnaire (GQ)

63% report debt of $150,000 or higher

$190,000

$168,000

PUBLIC PRIVATE

Median MD School Debt: $175,000

Refer to page 1

©2014 Association of American Medical Colleges. All rights reserved.

Source(s): 2013 Graduation Questionnaire and 2013 LCME I-B data

Education Debt

MUSC Median Education Debt

% with Education Debt

Education Debt $200,000 83%

Non-Education Debt (avg)

$13,423

Refer to page 1

©2014 Association of American Medical Colleges. All rights reserved.

The Details of Your Loans

©2014 Association of American Medical Colleges. All rights reserved.

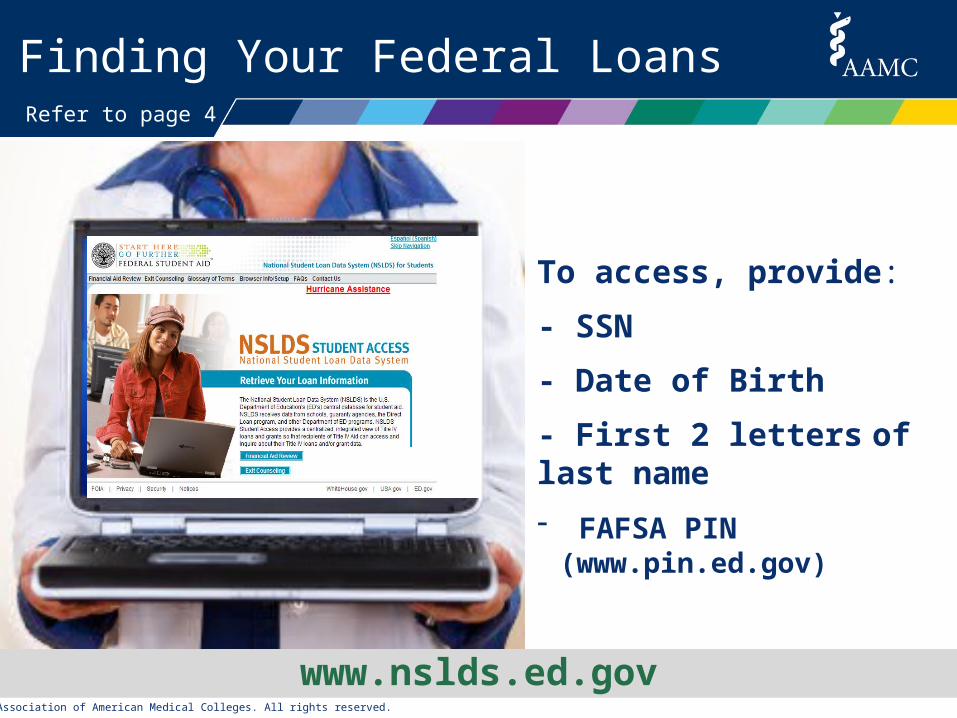

Finding Your Federal Loans

To access, provide:

- SSN

- Date of Birth

- First 2 letters of last name

- FAFSA PIN (www.pin.ed.gov)

www.nslds.ed.gov

Refer to page 4

©2014 Association of American Medical Colleges. All rights reserved.

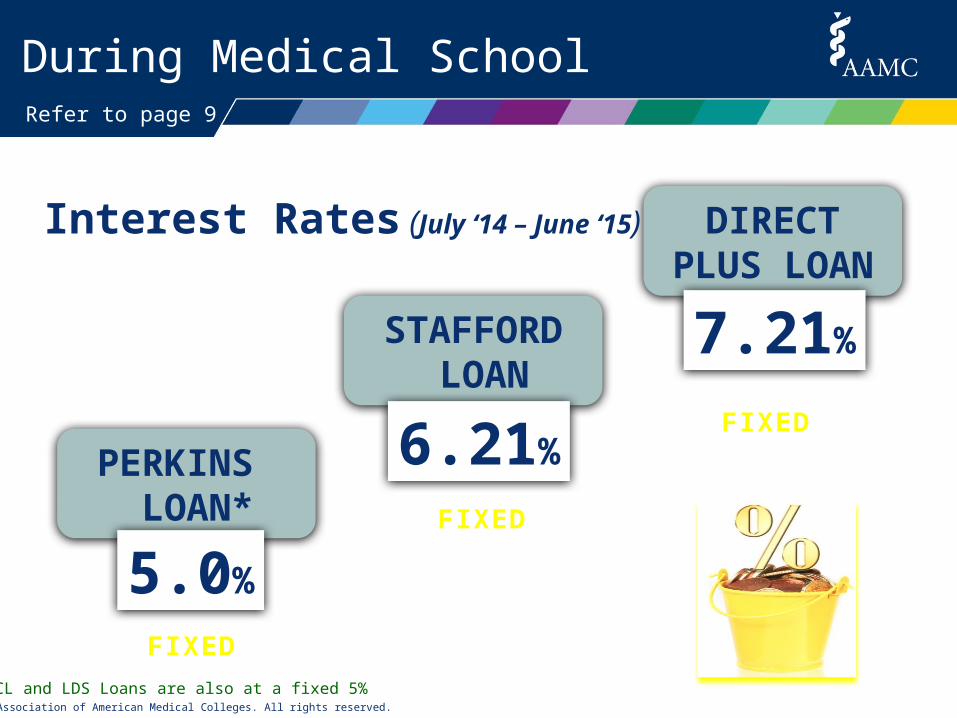

STAFFORD LOAN

During Medical School

PERKINS LOAN*

5.0%

DIRECT PLUS LOAN

7.21%

FIXED

FIXED

* PCL and LDS Loans are also at a fixed 5%

Interest Rates (July ‘14 – June ‘15)

6.21%

FIXED

Refer to page 9

©2014 Association of American Medical Colleges. All rights reserved.

STAFFORD LOAN

During Medical School

PERKINS LOAN*

5.0%

DIRECT PLUS LOAN

?%

FIXED

FIXED

* PCL and LDS Loans are also at a fixed 5%

Interest Rates (Loans after 06/30/15)

?%

FIXED

Refer to page 9

©2014 Association of American Medical Colleges. All rights reserved.

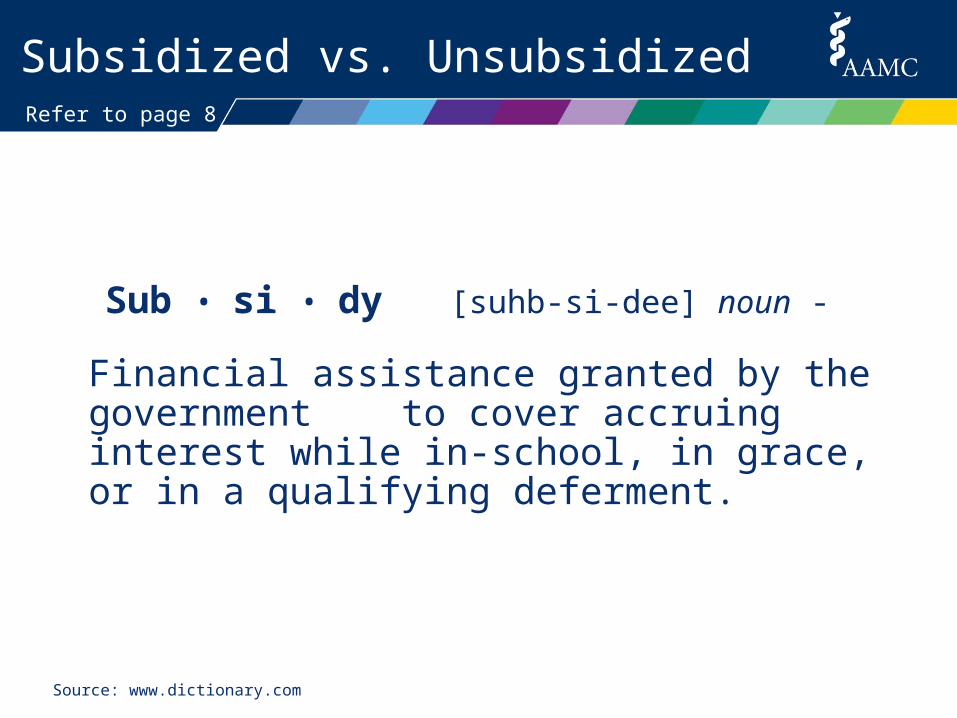

Subsidized vs. Unsubsidized

Sub • si • dy [suhb-si-dee] noun -

Financial assistance granted by the government to cover accruing interest while in-school, in grace, or in a qualifying deferment.

Source: www.dictionary.com

Refer to page 8

©2014 Association of American Medical Colleges. All rights reserved.

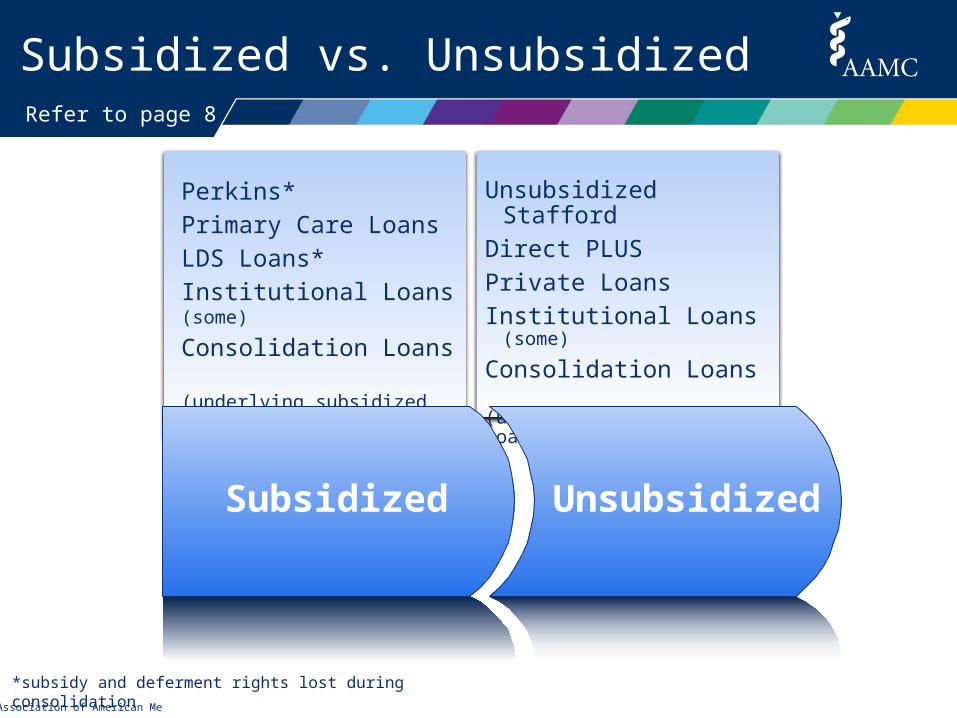

Subsidized vs. UnsubsidizedRefer to page 8

Perkins*

Primary Care Loans

LDS Loans*

Institutional Loans (some)

Consolidation Loans (underlying subsidized loans)

Unsubsidized Stafford

Direct PLUS

Private Loans

Institutional Loans (some)

Consolidation Loans (underlying unsubsidized loans)

Subsidized Unsubsidized

*subsidy and deferment rights lost during consolidation

©2014 Association of American Medical Colleges. All rights reserved.

Capitalization

Addition of unpaid interest to the principal

Principal + Interest =Larger

Principal

$200,000$233,200

$33,200

Refer to page 10

Debt Management Tip

Pay the interest on unsubsidized loans PRIOR to

capitalization

©2014 Association of American Medical Colleges. All rights reserved.

A Peek at Repayment

©2014 Association of American Medical Colleges. All rights reserved.

IN-SCHOOL

REPAYMENT

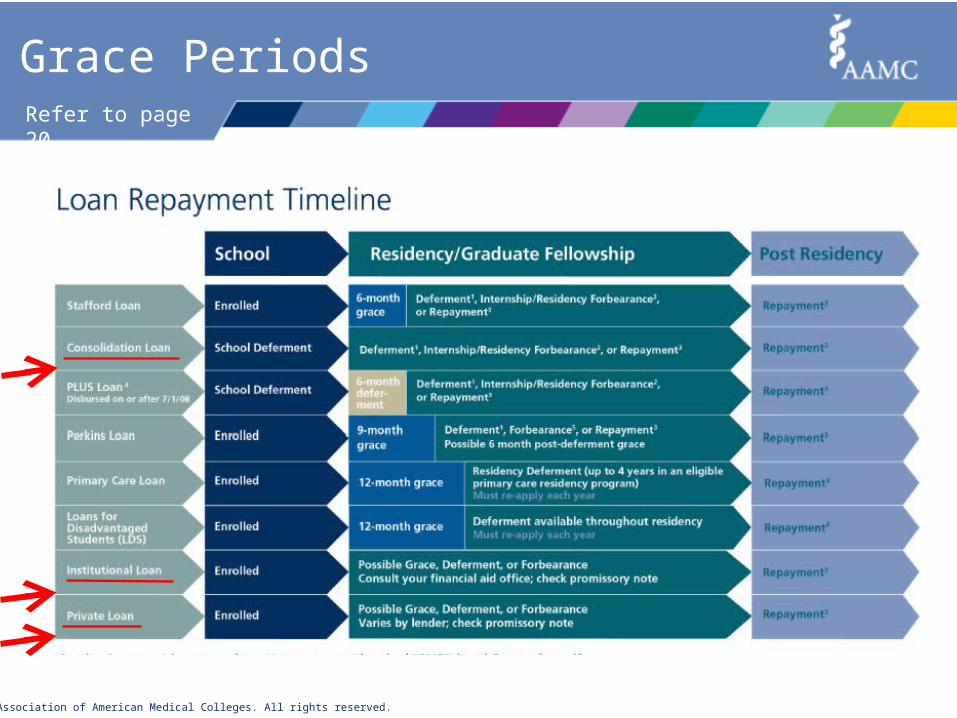

Grace PeriodsRefer to page 19

GRACE

The path for some loans

©2014 Association of American Medical Colleges. All rights reserved.

Grace PeriodsRefer to page 20

©2014 Association of American Medical Colleges. All rights reserved.

Options During Residency

During residency, there are two choices:

Postpone Payments

Make Payments

DefermentForbearance

Refer to page 22

©2014 Association of American Medical Colleges. All rights reserved.

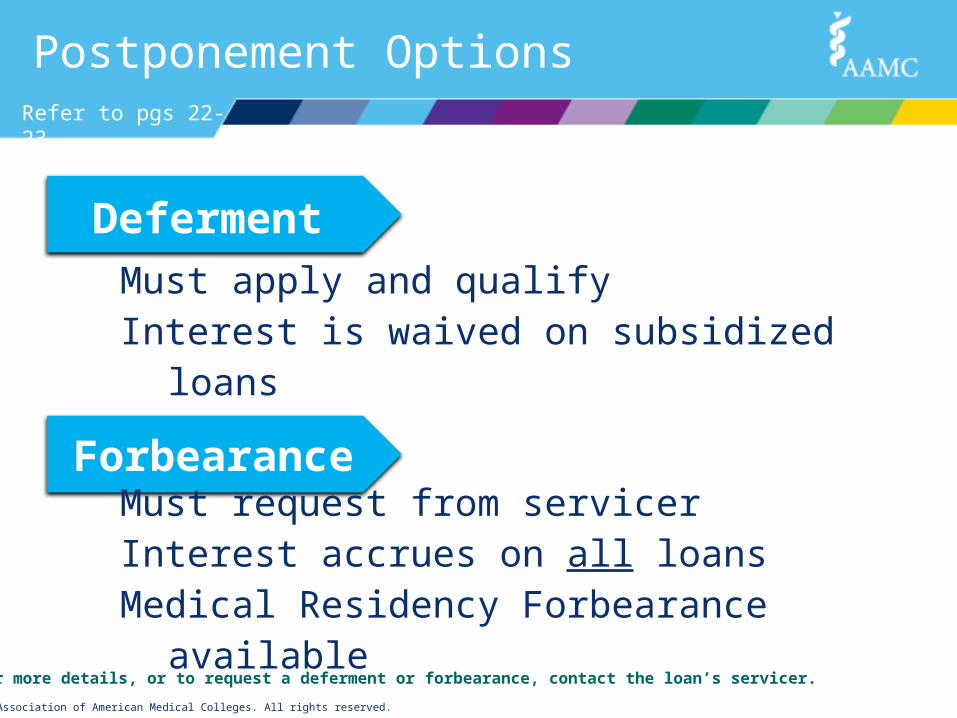

Postponement Options

NOTE: For more details, or to request a deferment or forbearance, contact the loan’s servicer.

Must apply and qualifyInterest is waived on subsidized loans

Must request from servicerInterest accrues on all loans Medical Residency Forbearance available

Deferment

Forbearance

Refer to pgs 22-23

©2014 Association of American Medical Colleges. All rights reserved.

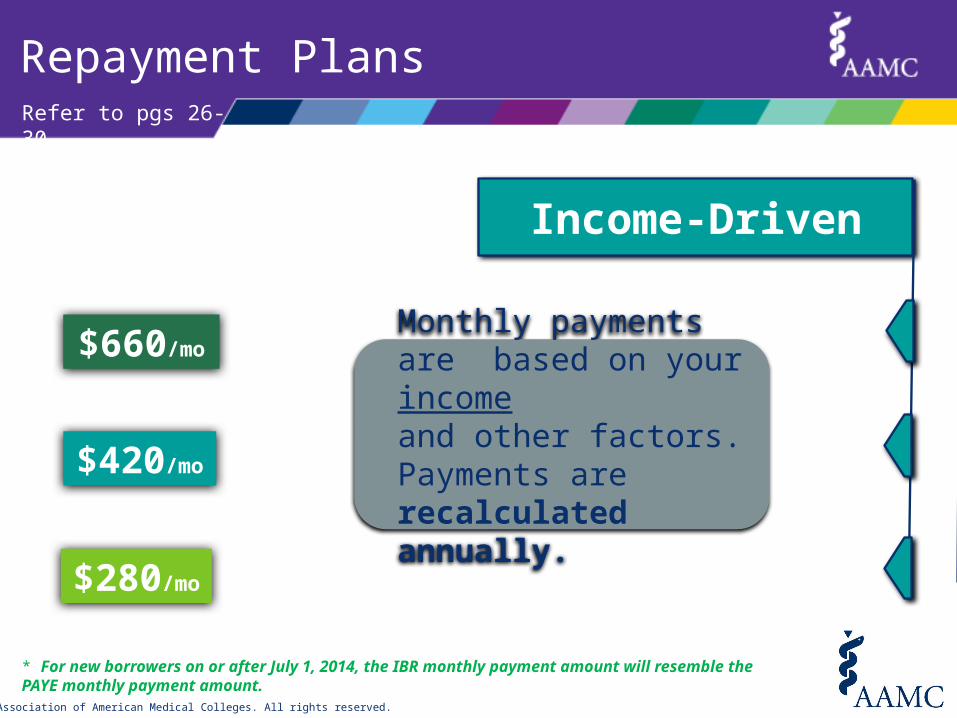

Options During Residency

During residency, there are two choices:

Postpone Payments

Make Payments

Select a Repayment Plan

Refer to pgs 25-30

©2014 Association of American Medical Colleges. All rights reserved.

Traditional

$2,600/mo

$1,500/mo

$1,200/mo

Repayment Plans

Monthly payments for the entire repayment term are calculated up-front and disclosed to you

Refer to pgs 26-30

©2014 Association of American Medical Colleges. All rights reserved.

Monthly payments are based on your incomeand other factors. Payments are recalculated annually.

Income-Driven

$660/mo

$420/mo

$280/mo

Repayment Plans

* For new borrowers on or after July 1, 2014, the IBR monthly payment amount will resemble the PAYE monthly payment amount.

Refer to pgs 26-30

©2014 Association of American Medical Colleges. All rights reserved.

Strategic Borrowing

©2014 Association of American Medical Colleges. All rights reserved.

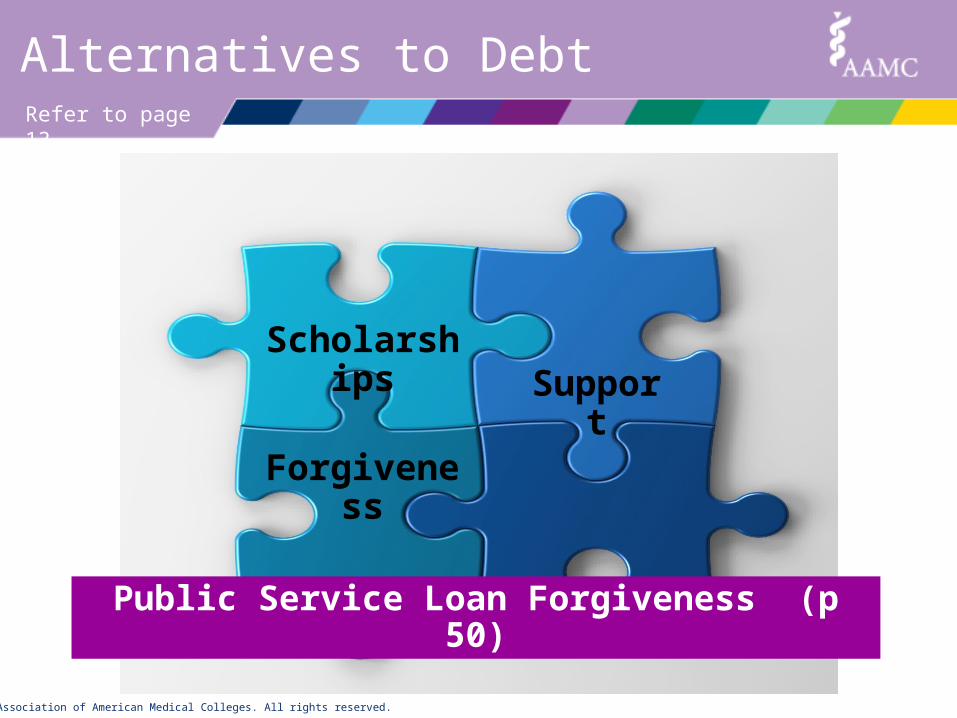

Alternatives to Debt

Scholarships

Refer to page 13

www.nhsc.hrsa.govwww.lrp.nih.gov

www.aamc.org/stloan

©2014 Association of American Medical Colleges. All rights reserved.

Alternatives to Debt

Scholarships Suppo

rt

Refer to page 13

©2014 Association of American Medical Colleges. All rights reserved.

Alternatives to Debt

Scholarships

Forgiveness

Support

Refer to page 13

Public Service Loan Forgiveness (p 50)

©2014 Association of American Medical Colleges. All rights reserved.

Alternatives to Debt

Scholarships

Forgiveness

Support

Budgeting

Refer to page 13

©2014 Association of American Medical Colleges. All rights reserved.

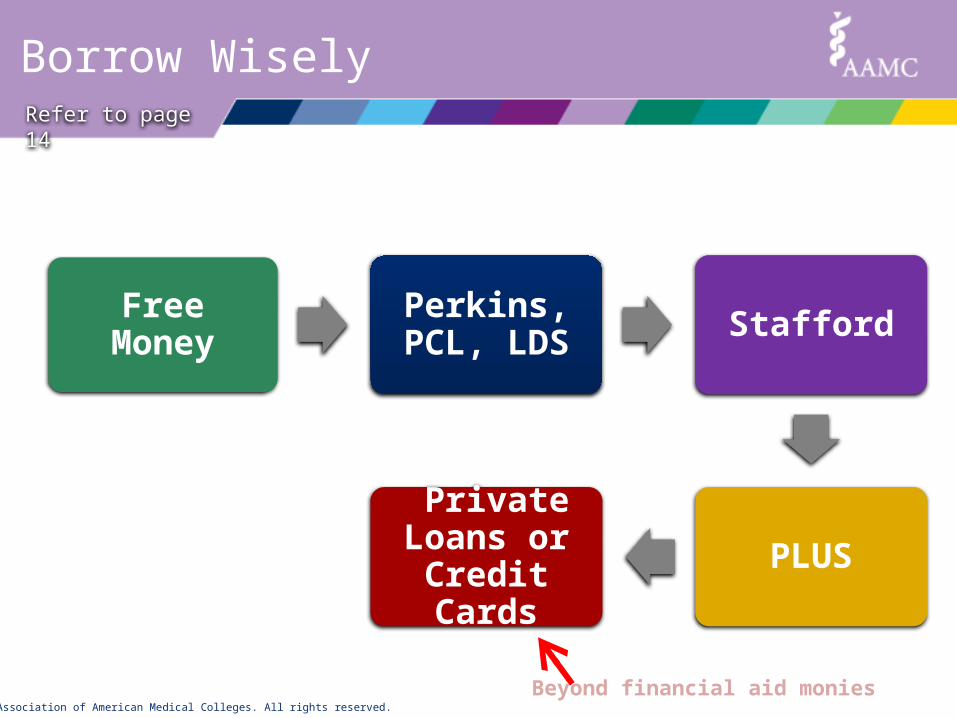

Free Money Perkins, PCL, LDS Stafford

PLUS Private

Loans or Credit Cards

Borrow WiselyRefer to page 14

Beyond financial aid monies

©2014 Association of American Medical Colleges. All rights reserved.

How Will You Borrow?Refer to page 15

©2014 Association of American Medical Colleges. All rights reserved.

How Will You Borrow?

Do NOT borrow just because you are eligible

Borrow what you need, not what you want

Decline loans that exceed your need

Accepting loans may affect eligibility for other aid

Avoid forfeiting low rate loans for higher rate debt

Refer to page 15

Financial Aid FactIf a shortfall occurs, previously

declined monies may be obtained – see financial aid for assistance

©2014 Association of American Medical Colleges. All rights reserved.

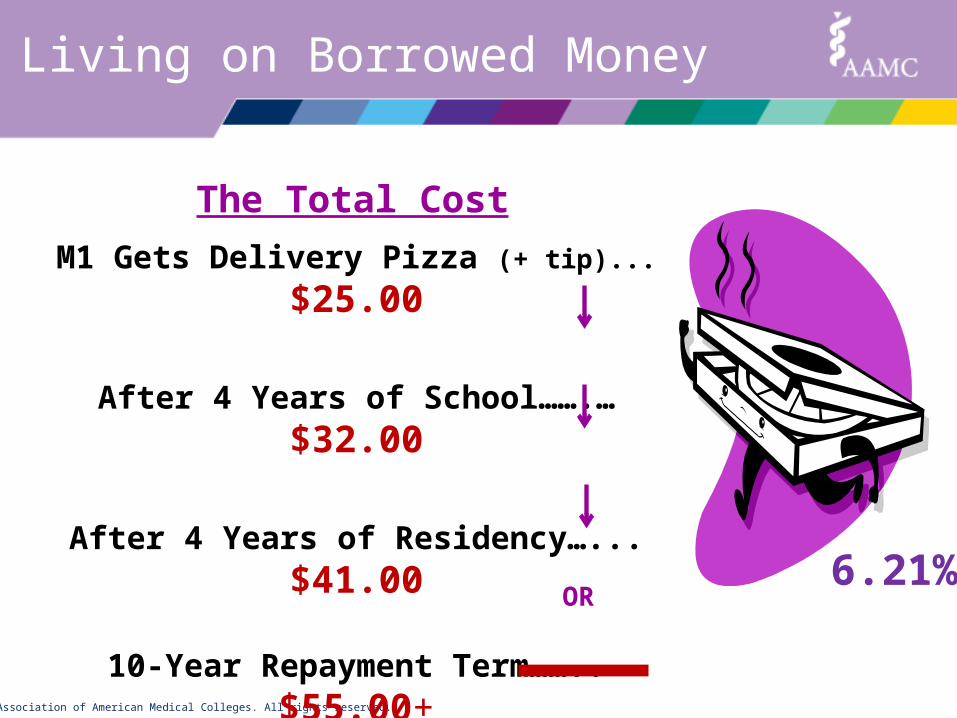

Living on Borrowed Money

M1 Gets Delivery Pizza (+ tip)... $25.00

After 4 Years of School…….… $32.00

After 4 Years of Residency…... $41.00

10-Year Repayment Term…….. $55.00+

25-Year Repayment Term…….. $84.00+OR

The Total Cost

6.21%

©2014 Association of American Medical Colleges. All rights reserved.

Have a Spending Plan

©2014 Association of American Medical Colleges. All rights reserved.

Have a Spending Plan

A Spending Plan in 1-2-3

1) Put it in writing

2) Review periodically to identify leaks

3) Make necessary adjustments

“Live like a student while you are a student…”

Refer to page 41

©2014 Association of American Medical Colleges. All rights reserved.

Have a Spending Plan

www.aamc.org/FIRST

Refer to page 44

©2014 Association of American Medical Colleges. All rights reserved.

Have a Spending Plan

www.mint.com

Refer to page 44

©2014 Association of American Medical Colleges. All rights reserved.

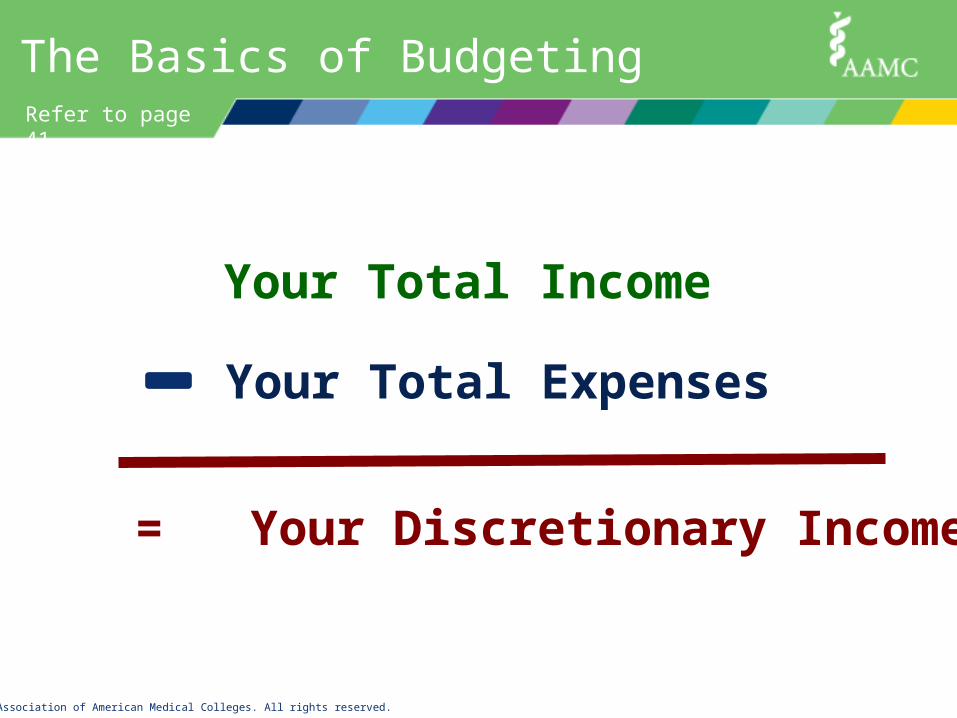

The Basics of BudgetingRefer to page 41

Your Total Income

Your Total Expenses

= Your Discretionary Income

©2014 Association of American Medical Colleges. All rights reserved.

The Basics of Budgeting

UNLOCKS DEEPER INSIGHT

INTO YOUR BUDGET

©2014 Association of American Medical Colleges. All rights reserved.

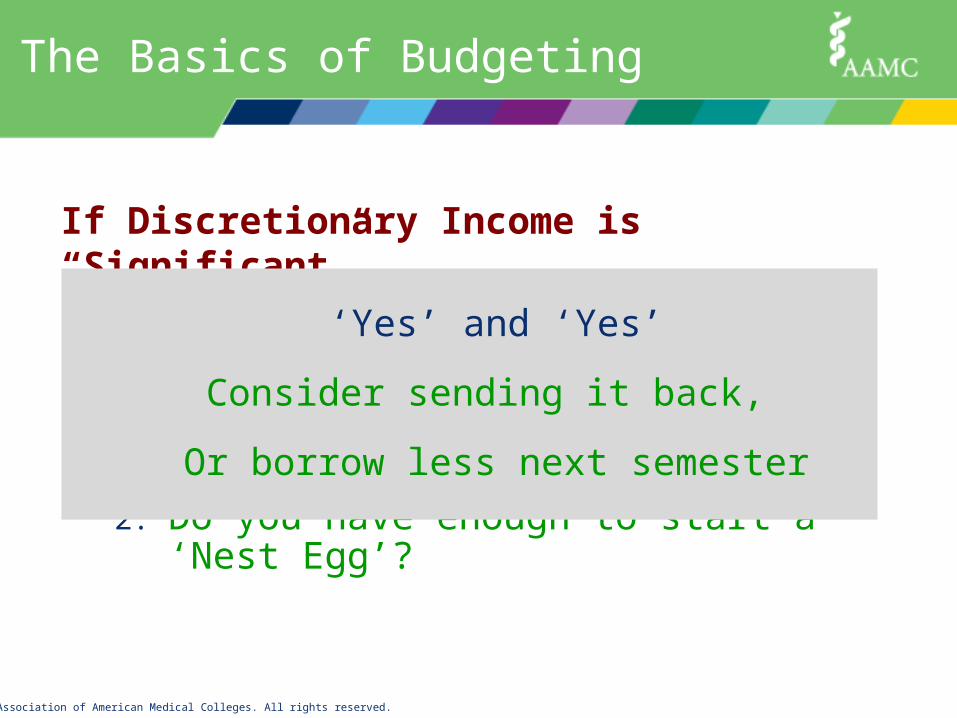

If Discretionary Income is “Significant”

Ask Yourself 2 Questions

1. Were you honest about your expenses?

2. Do you have enough to start a ‘Nest Egg’?

‘Yes’ and ‘Yes’

Consider sending it back,

Or borrow less next semester

The Basics of Budgeting

©2014 Association of American Medical Colleges. All rights reserved.

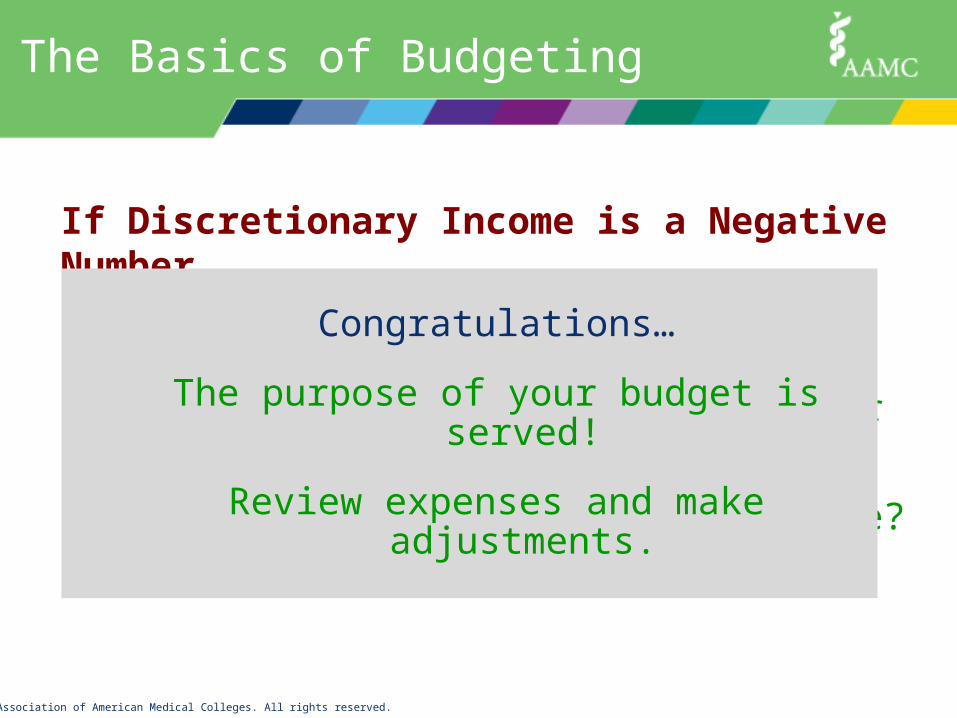

If Discretionary Income is a Negative Number

Ask Yourself 2 Questions

1. Are you budgeting for ‘Needs’ or ‘Wants’?

2. What alternatives might there be?

Congratulations…

The purpose of your budget is served!

Review expenses and make adjustments.

The Basics of Budgeting

©2014 Association of American Medical Colleges. All rights reserved.

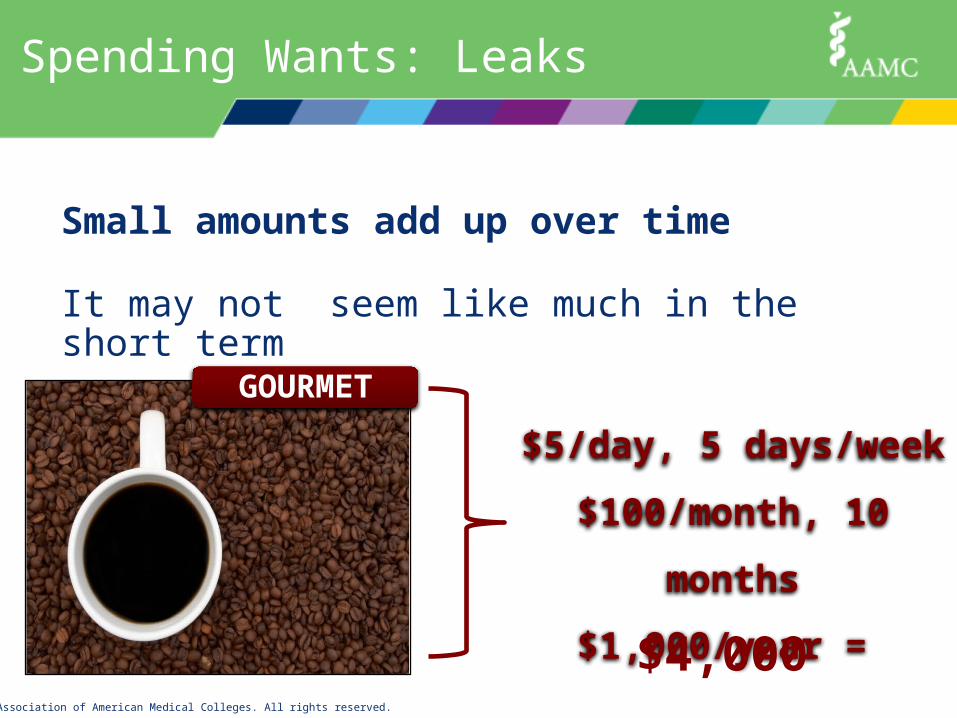

Spending Wants: Leaks

Small amounts add up over time

It may not seem like much in the short term

GOURMET

$5/day, 5 days/week

$100/month, 10 months

$1,000/year =

$4,000

©2014 Association of American Medical Colleges. All rights reserved.

Spending Wants: Leaks

$4,000 spent during medical school =

GOURMETAfter graduation, grace and 4-yr residency w forbearance

@ 5.41% = ~$7,000, then paid• 10 yr Term = ~$9K• 25 yr Term = ~$13K

Rounded Estimates

©2014 Association of American Medical Colleges. All rights reserved.

Spending Wants: Leaks

Consider the alternatives

Savings can also add up quickly

AT HOME

$10/month

10 months/year

$100/year

$400

©2014 Association of American Medical Colleges. All rights reserved.

$400 spent during medical school =

AT HOMEAfter graduation, grace and 4-yr residency w forbearance

@ 5.41% = ~$550, then paid• 10-yr Term = ~$700• 25-yr Term = ~$1,000

Spending Wants: Leaks

Rounded Estimates

Are Credit Cards Bad?

©2014 Association of American Medical Colleges. All rights reserved.

Credit Cards

Reasons to have a Credit Card

Builds Credit

Emergencies

Consumer Protection

Convenience

Refer to page 38

©2014 Association of American Medical Colleges. All rights reserved.

Credit Cards

The DON’Ts of Credit Cards

Don’t use them for cash advances

Don’t charge more than you can pay in a month

Don’t use one card to pay off another

Refer to page 39

TIP: If you can eat, drink or wear an item, it’s usually not a good use of credit.

©2014 Association of American Medical Colleges. All rights reserved.

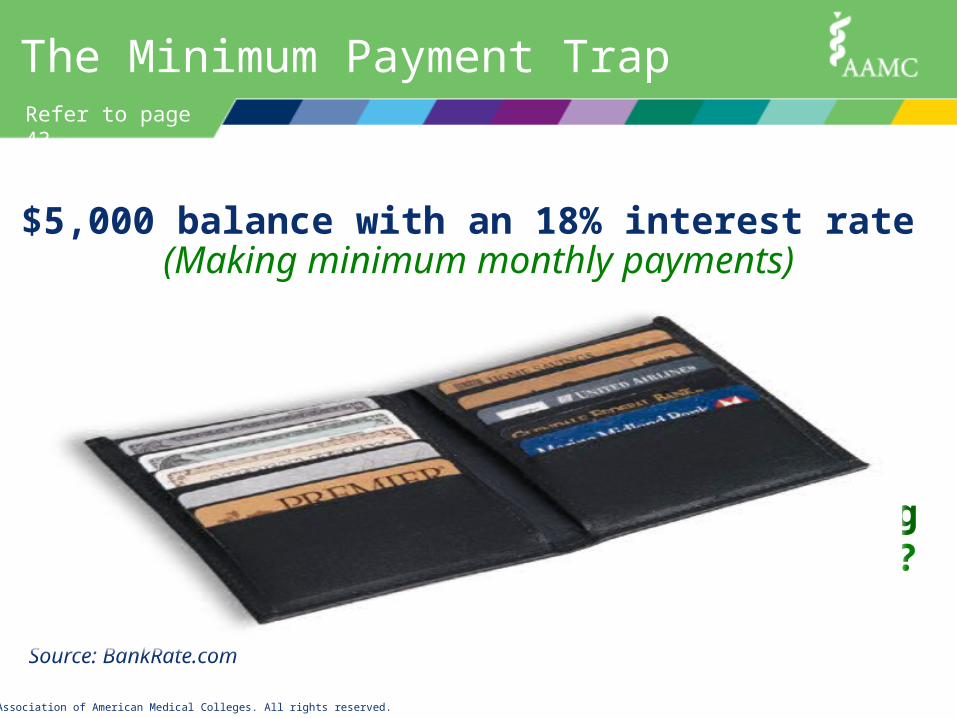

22.75 years to repay in full

$12,000 in total repayment cost

What could possibly be worth paying more than twice its original value?

The Minimum Payment Trap

Source: BankRate.com

$5,000 balance with an 18% interest rate (Making minimum monthly payments)

Refer to page 43

©2014 Association of American Medical Colleges. All rights reserved.

Credit: Understand & Protect

©2014 Association of American Medical Colleges. All rights reserved.

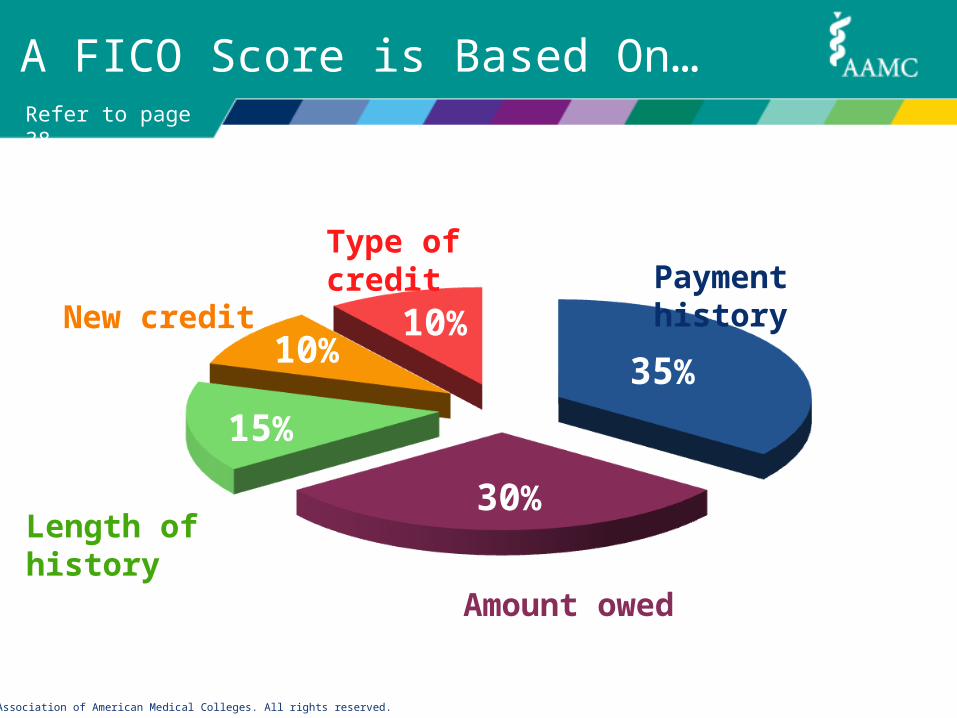

35%

30%

15%

10%10%

Payment history

Amount owed

Length of history

New credit

Type of credit

A FICO Score is Based On…Refer to page 38

©2014 Association of American Medical Colleges. All rights reserved.

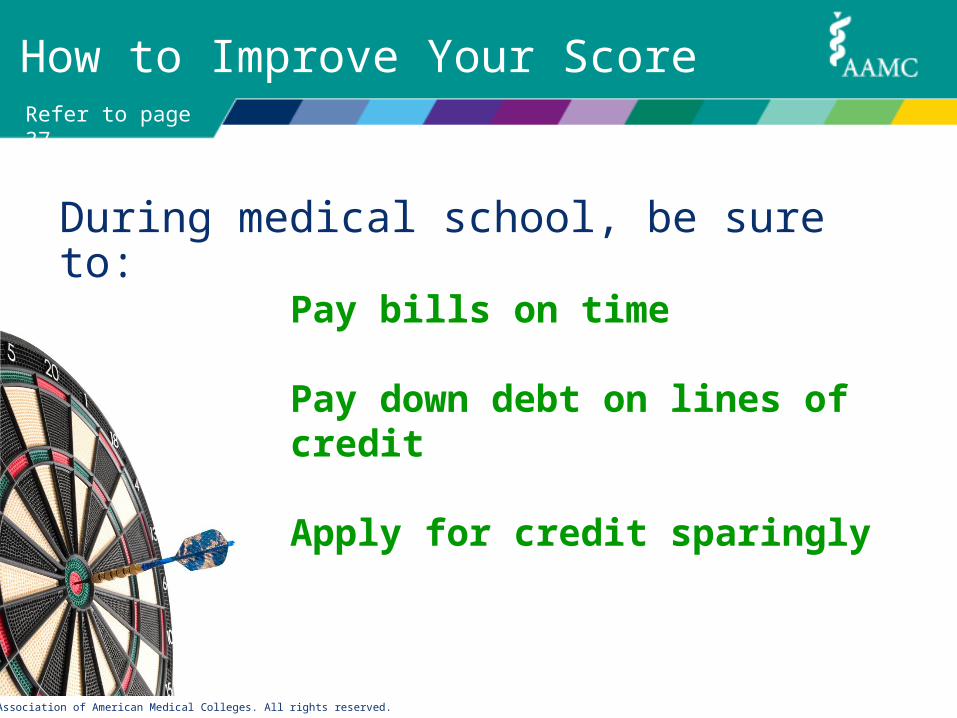

How to Improve Your Score

During medical school, be sure to:

Pay bills on time

Pay down debt on lines of credit

Apply for credit sparingly

Refer to page 37

©2014 Association of American Medical Colleges. All rights reserved.

Refer to page 39

Check your Credit Report

www.annualcreditreport.com

“An investment in knowledge always pays

the best interest”

- Benjamin Franklin

- Benjamin Franklin

Questions? [email protected]

Follow us on Twitter: @AAMCFIRST Like us on Facebook: Facebook.com/AAMCFIRST