monetizing the future: business model...

TRANSCRIPT

Monetizing the Future: Business

Model Transformation in

Healthcare

Digital health technologies and value based

reimbursement spur new opportunities

December 2016

2

Advanced Woundcare Market Update

3 <0000-00>

Global Woundcare Market Value Based Care Transition, Opens the Door For New Services & Solutions

How big is the market and how fast

is it growing?

Revenue

($ Billion)

Growth

Rate (%)

2016 16.8

2017 17.3 3.2

2018 17.8 3.4

2019 18.4 3.4

Region: Global

Global Woundcare Market Revenue Share by Sector, 2016

Wound Cleansers and Debriding

Agents 7%

Dry Gauze 8%

Film Dressings 3%

Hydrocolloids 5%

Traditional Adhesive

18%

NPWT 11%

Wound Closure 21%

Alginates 2%

Hydrogels 1%

Skin Grafts & Substitutes

4%

Foam Dressings 6%

Non-Adherant 6%

Biomaterials 2%

Other 6%

Acelity 22%

Smith & Nephew

19%

Molnlycke 12%

Convatec 8%

Coloplast 4%

Medline 2%

3M 3%

Other 30%

Global Advanced Woundcare Market

Revenue Share by Competitor, 2016

*Red highlight denote

Advanced Woundcare

market segments

“What was once a payment is now a cost. What was

once a cost is now a potential savings.”- Hospital CEO

• Where is it Performed?

• Who Performs it?

• What is Tracked/Measured/ Documented?

• How is it Paid for?

Opportunities

For Business Model

Transformation

In

Woundcare

Source: Frost & Sullivan Research

4 <0000-00>

Market Snapshot U.S. Election and 21st Century Cures Act Alter Market Landscape

MACRA

In The

News

Industry

Shifts

• Chronic Care Management

Focus

• Codes for Mobility Related

Disability

• Screening

• Election/ New HHS and CMS heads

• Device Tax/ Cadillac Tax

• 21st Century Cures Act

• Consolidation

• Products to Services

• Patient Education

5 <0000-00>

Market Snapshot Europe New Rules Transform Regulation to be More like the FDA

Regulatory

In The

News

Industry

Shifts

• Stricter Requirements ( High

Risk)

• Increased Transparency &

Traceability

• BREXIT Impact?

• NHS Modernization Initiatives

• Precision Medicine Initiatives

(France, UK, Germany)

• Product Portfolio Strategies

• Managed Care Services

(Medtronic)

• R&D Strategy

6

Digital Transformation in Healthcare

Six Big Themes for Business Model Transformation Driving Factors For Change

7 Value Based

Reimbursement

Digital Transformation of

Care Delivery

New Market Entrants

Collaboration &

Partnerships

Healthcare

Consumerism

As-a-Service Centric

Business Models

8

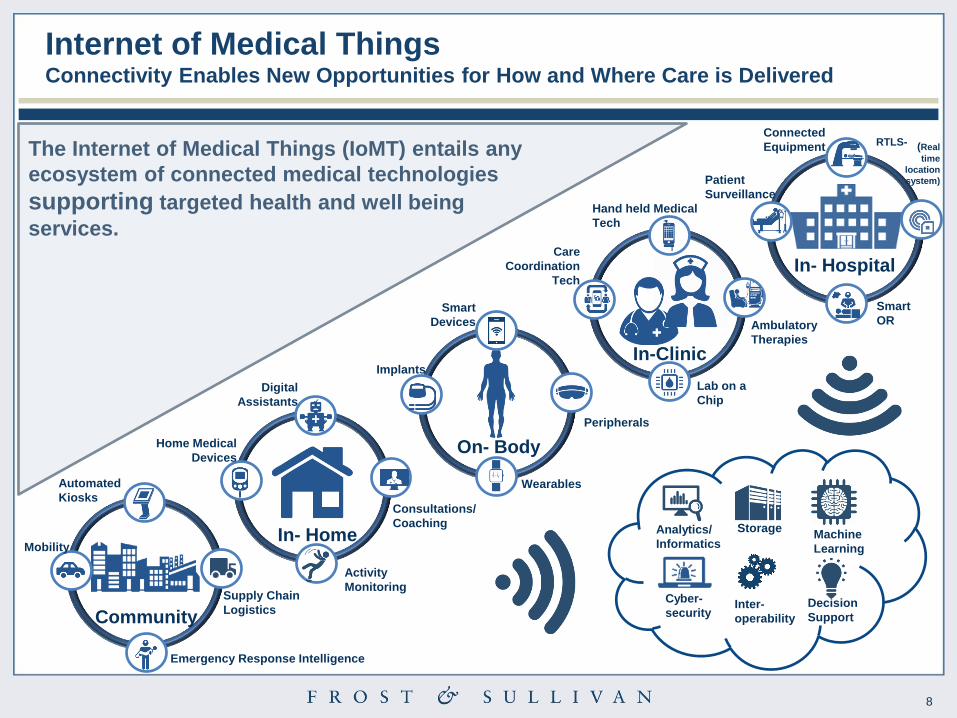

Community

Emergency Response Intelligence

Supply Chain

Logistics

Mobility

Automated

Kiosks

Internet of Medical Things Connectivity Enables New Opportunities for How and Where Care is Delivered

In- Home

In-Clinic

In- Hospital

Home Medical

Devices

Peripherals

Digital

Assistants

On- Body

Wearables

Implants

Smart

Devices

Activity

Monitoring

Consultations/

Coaching

Lab on a

Chip

Care

Coordination

Tech

Hand held Medical

Tech

Ambulatory

Therapies

Smart

OR

Patient

Surveillance

Connected

Equipment

Analytics/

Informatics

Storage Machine

Learning

Cyber-

security Inter-

operability

Decision

Support

The Internet of Medical Things (IoMT) entails any

ecosystem of connected medical technologies

supporting targeted health and well being

services.

(Real

time

location

system)

RTLS-

9 <0000-00>

Right Care, Right Place, at the Right Time Value Drivers in the New Healthcare Economy

Source: Frost & Sullivan

10 MA3C-18

Global Perspectives Digital Transformation Occurring in Varying Degrees within Each Region

Source: Frost & Sullivan Analysis

United States

• $200 M Precision Medicine Initiative

• 75% of large employers now offer

some form telehealth services as

part of plans (48% in 2015).

• Clarity on FDA guidelines regarding

regulation of digital health

technologies helping to accelerate

growth.

Western Europe

• Google DeepMind working with NHS in

UK on a number of health data initiatives.

• Notable start ups targeting care

coordination platforms.

• Companies like Philips, Siemens, Nokia

investing heavily in consumer digital

health.

India.

• Make in India movement, and

industry accelerator initiatives to lead

to the rise of a new breed of home

grown medical technology

developers.

• Tools are helping to bridge gaps in

care continuum.

China

• Regulatory barriers removed for

private insurance.

• Over $1.1 B in funding for digital

health start ups in 1H 2016 (Pin An

Good Doctor, Spring Rain, iCarbonX)

11

Business Model Transformation

12

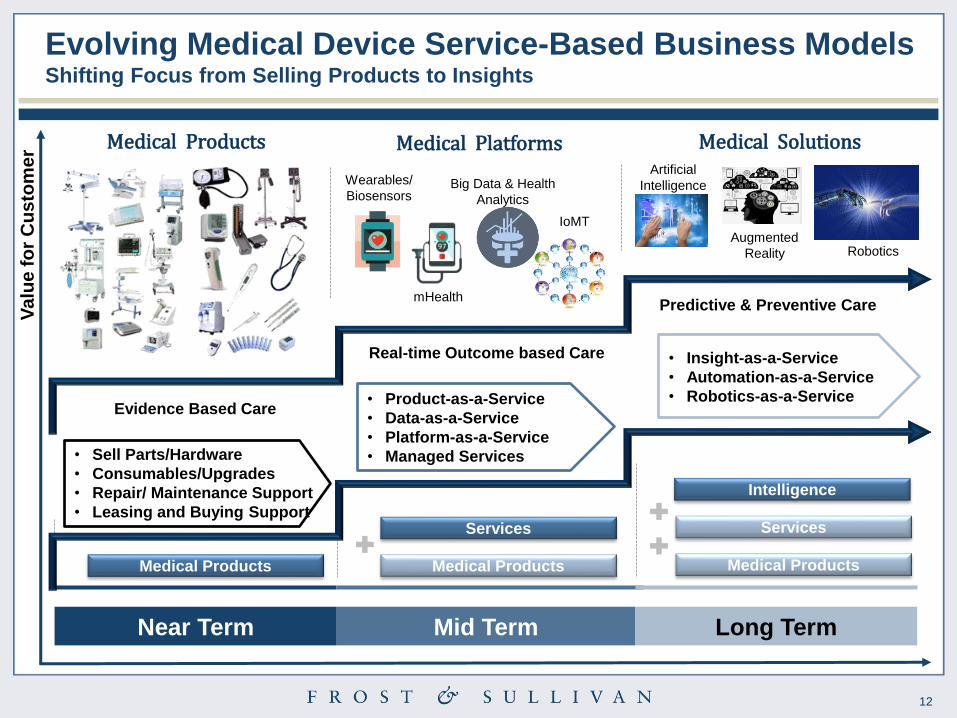

Evolving Medical Device Service-Based Business Models Shifting Focus from Selling Products to Insights

Va

lue

fo

r C

us

tom

er

Near Term Mid Term Long Term

Medical Products Medical Products

Services

Medical Products

Services

Intelligence

Medical Platforms Medical Solutions

• Product-as-a-Service

• Data-as-a-Service

• Platform-as-a-Service

• Managed Services

• Insight-as-a-Service

• Automation-as-a-Service

• Robotics-as-a-Service Evidence Based Care

Real-time Outcome based Care

Predictive & Preventive Care

Artificial

Intelligence

Augmented

Reality Robotics

Wearables/

Biosensors

mHealth

IoMT

Big Data & Health

Analytics

• Sell Parts/Hardware

• Consumables/Upgrades

• Repair/ Maintenance Support

• Leasing and Buying Support

Medical Products

13

Source: Frost & Sullivan

10

9

8

7

6

5

4

3

2

1 2 3 4 5 6 7 8 9 10

Emerging Business Models in Healthcare How do you find the right model for your solution?

Customer Value Enhancement

Mo

ne

tiza

tio

n O

pp

ort

un

ity

Healthcare

Marketplace

Product/

Process

Digitization

Mass

Customization

e-Commerce/

m-Commerce

Product-as-

a-Service

Software-as-

a-Service

Platform-as-

a-Service

Data-as-

a-Service

Managed

Services

Shared

Economy

Risk-sharing

Models Crowdsourcing

Open

Source

Single Firm

Independent

Model

New

Market

Creation

Single

Product

Strategy

Disaggregation

Social

Enterprise

On-demand

Health

Healthcare Industry: Comparative Analysis of B2B and B2C Models, Global, 2016

High

High

Low

Low

B2C

B2B

Note:

• The size of the bubble represents customer outreach. These business models are not exclusive to each other.

• Some of these models represent B2B2C relationships. The ratings for the business models are relative to each other.

Traditional

Business Models

Emerging

Business Models

14

0

10

20

30

40

50

60

70

2013 2014 2015 2016 2017 2018 2019 2020 2021

Dedicated HC SmartPhones

0.1 0.1 0.1 0.1 0.2 0.3 0.4 0.6 0.9

Mobile POC Tools 0.0 0.1 0.3 0.6 1.3 2.4 4.5 7.4 12.0

Wearables 2.0 3.9 5.1 6.6 8.5 11.1 14.5 18.9 23.0

Healthcare Apps 2.8 4.1 6.6 9.9 13.0 16.8 21.4 27.0 27.9

Re

ve

nu

e (

$ B

illio

n)

Novel Point of Care Technologies Transform mHealth Innovations in Product as-a-Service Business Models

Note: All Figures are rounded. The base year is 2015; Source: **mHealth App Developer Economics 2014, 2015, Frost & Sullivan

mHealth Enabled Care Market: Revenue Forecast,

Global, 2013–2021 Mobile Point of Care Tools

Silhouette Aranz Medical

EyeNETRA’s NetraG

MobiUS SP1 System

MedWand

CliniCloud Smart Devices

Philips Lumify Withings Blood Pressure

Scout Wound Vision

15

Clinical Grade Wearables Gain Commercial Traction Novel Data and Platform as-a-Service Business Models

Medical and Clinical-Grade Wearables

Source: Frost & Sullivan

Note: The consumer health wearables segment mainly includes unregulated

wellness, fitness, and sports wearables with defined health use case(s).

2.4 3.1

3.9 5.0

6.5

8.3

10.6

1.5

2.0

2.6

3.4

4.6

6.2

8.3

0

2

4

6

8

10

12

14

16

18

20

2014 2015 2016(E) 2017(F) 2018(F) 2019(F) 2020(F)

Rev

en

ue (

$ B

illio

n)

Healthcare Wearables Segment: Revenue Forecast, Global, 2014–2020

Medical and Clinical-Grade Wearables

Consumer Health Wearables

Other Wearables

16

Artificial Intelligence Systems in Healthcare: Revenue

Forecast, Global, 2013–2021

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2013 2014 2015 2016 2017 2018 2019 2020 2021

Revenue 507.0 633.8 811.1 1,065 1,438 2,002 2,882 4,298 6,662

Re

ve

nu

e (

$ M

illi

on

)

Year

Note: All figures are rounded. The base year is 2015. Source: Frost & Sullivan

Artificial Intelligence Systems Automate Decision Suport Enabling Insights as-a-Service Business Models

Medical Imaging

Wellness Wearables

Ins

igh

ts

Clin

ica

l

Wo

rkfl

ow

Cognitive

Platforms

17

Business Model Innovation Case Studies

18

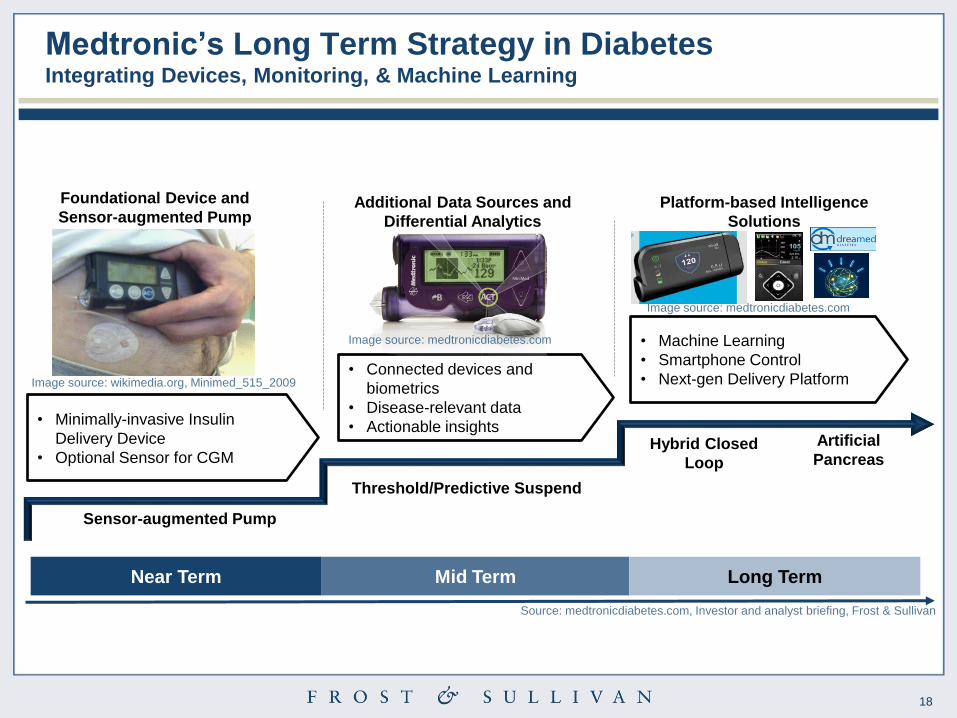

Medtronic’s Long Term Strategy in Diabetes Integrating Devices, Monitoring, & Machine Learning

Near Term Mid Term Long Term

Sensor-augmented Pump

Threshold/Predictive Suspend

Hybrid Closed

Loop

Artificial

Pancreas

• Minimally-invasive Insulin

Delivery Device

• Optional Sensor for CGM

• Connected devices and

biometrics

• Disease-relevant data

• Actionable insights

• Machine Learning

• Smartphone Control

• Next-gen Delivery Platform Image source: wikimedia.org, Minimed_515_2009

Image source: medtronicdiabetes.com

Foundational Device and

Sensor-augmented Pump Additional Data Sources and

Differential Analytics

Platform-based Intelligence

Solutions

Image source: medtronicdiabetes.com

Source: medtronicdiabetes.com, Investor and analyst briefing, Frost & Sullivan

19

Medtronic Hospital Solutions— Managed Services Platform-based cath lab solution for hospitals in Europe

Devices

Smart Financing Model

Capital Equipment

Cath Lab & Hospital IT

Cath Lab Management & Staffing

Operational Excellence Consulting

Growth Acceleration Services

Capital Structure

Optimization

Operational

Efficiencies

Patient Access

Solutions

Till Q2 FY16, Medtronic’s Hospital Solutions business has completed 66 long-term CLMS and ORMS agreements

with hospital systems, representing over $1.5 Billion in revenue over an average span of 6 years.

Key Benefits Focus Areas

Source: Medtronic; Frost & Sullivan

20

Smith & Nephew Establishes Syncera eCommerce Enables Rep Free Sales Models

Key Components of the Rep Free Solution

Medical Device Procurement

(Smith & Nephew - Total Knee and

Hip Replacement Systems)

Hospital Staff Training

(Syncera Virtual Backtable -

Rapid Surgical Staff Learning)

Process Automation

(Syncera TrayTouch - Advanced

Tray Analytics for OR)

1 2 3

21

OPM—Mass Customization Leveraging 3D Printing to Personalize Medical Implants

Cranial

Facial Shoulder

Reconstruction

Spine Rib Replacement

Spacer for

Knee

Infection

Osteotomy Wedge Small Bones Foot

Small Bones

Hand

Acetabular

Cup

Ankle Reconstruction

Share patient’s imaging

(MRI or CT scan) for

custom solutions

Surgeon

Collaboratively design desired

implant using OsteoFab®

proprietary 3D-printing process

OPM’s OEM Services for Medical Device Implants

OPM’s Turnkey Contract Manufacturing Services

Range of OPM’s Custom-made 3D Implants

Shipped within 5 days of receipt of STL file

Imp

lan

t M

an

ufa

ctu

red

at

OP

M’s

Sit

e

Shipped within weeks to surgeon

OEM Client’s

Engineering Team

Selects approved design

files from OPM’s

OsteoFab® Platform

Determines manufacturability

and provides a price quotation

for your review

FDA Approved

Image source: Thinkstock, press kit. Source: OPM; Frost & Sullivan OPM (Oxford Performance Materials)

22

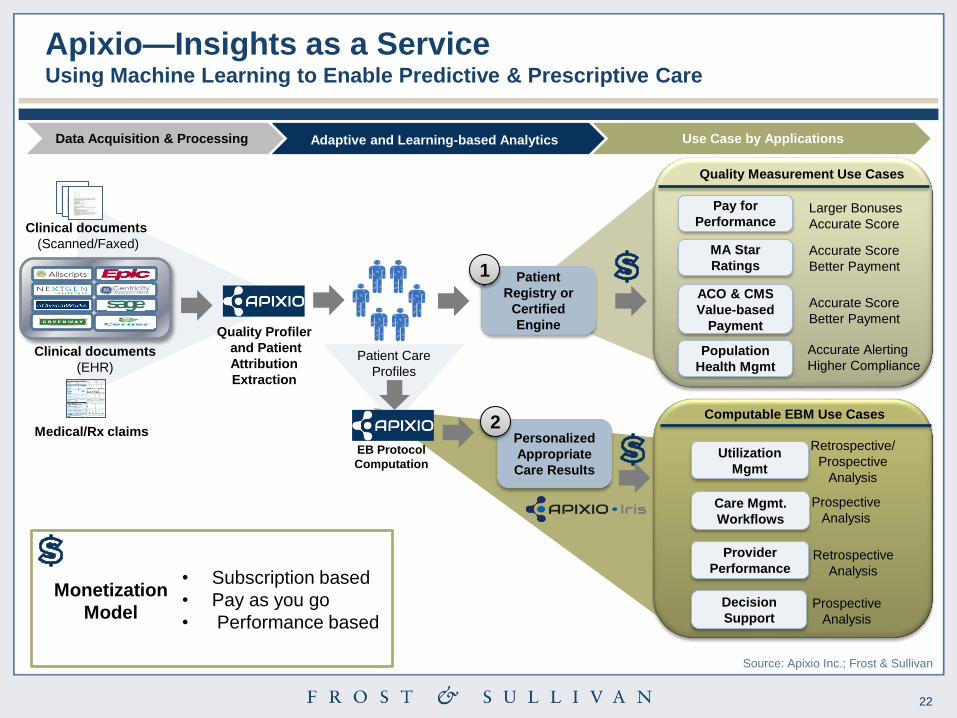

Apixio—Insights as a Service Using Machine Learning to Enable Predictive & Prescriptive Care

Medical/Rx claims

Clinical documents

(EHR)

Clinical documents

(Scanned/Faxed)

Patient Care

Profiles

Quality Profiler

and Patient

Attribution

Extraction

Personalized

Appropriate

Care Results

Patient

Registry or

Certified

Engine

ACO & CMS

Value-based

Payment

MA Star

Ratings

Pay for

Performance

Population

Health Mgmt

Larger Bonuses

Accurate Score

Accurate Score

Better Payment

Accurate Alerting

Higher Compliance

Accurate Score

Better Payment

Quality Measurement Use Cases

EB Protocol

Computation Utilization

Mgmt

Decision

Support

Provider

Performance

Care Mgmt.

Workflows

Retrospective

Analysis

Prospective

Analysis

Prospective

Analysis

Retrospective/

Prospective

Analysis

Computable EBM Use Cases

Data Acquisition & Processing Adaptive and Learning-based Analytics Use Case by Applications

1

2

Monetization

Model

• Subscription based

• Pay as you go

• Performance based

Source: Apixio Inc.; Frost & Sullivan

23

Healint – Innovation Happening Across the Globe Global Platform for Patient Monitoring, Research and Clinical Data (Singapore)

Source: Healint; Frost & Sullivan

Operating Model

Chronic Disease Management Research and

Development

Institutes

Dashboards

Monitoring Devices

Inputs - Vitals signs

B2B

Inputs - Data

Academic

Healthcare

Provider

B2C

Healint app

available on

Apple Store

Actionable Insights

Inputs - Data

Active input by

physician

1

2

3

4

Population

study

24

Digital Woundcare Opportunities

25

Source: Frost & Sullivan

Current Wound Treatment

Paradigm

Integrated Wound Management

• Outcomes Tracking

• Best Practices

Data Driven Healthcare

• Efficient Communication

• Patient Transition

Care Co-ordination/Monitoring

• Wound Bed Preparation

• Healing

Treatment

• Right treatment

• Right Patient, Right Time

Diagnosis/Detection

• Patient Engagement

• Prevent Recurrence

Prevention Inefficent:

• Standardized Protocols

• Clinical Coordination

• Understanding of True

Patient Impact

Integrating Wound Management Coordinated Care Facilitation the Key to Service Based Solutions

26

Innovation Opportunities Technology Enabled Solutions to Optimize the Clinical Workflow

Innovation

Opportunities

Deep Tissue Injury

Detection

Point of Care

Diagnostics

Healing Technologies

Biosensors

Next Generation

Mechanical/ Energy

Devices

Clinical

Algorithms

Outcomes

Tracking

Risk Stratification

Tools

Source: Frost & Sullivan; Image Source: http://imageresource.gilcommunity.com/

Data-driven Best

Practices

Ca

re

Co

-ord

ina

tion

27

Digital Health in Wound Diagnostics Innovative Point of Care Tools Help Track Wound Healing

28

Digital Health Support in Wound Care Workflow Digital Tools Help Connect a Fragmented Clinical Environment

29

Conclusion

30

Business Model Flaws

Over Engineered – Unnecessary Device

Complexity

Lack of Interoperability

Security Vulnerabilities

Unreliable/ Inaccurate Data

Targeting the Wrong Customers

6 Common Points of Failure in Digital Health Solution

Key Areas of Market Failure

Source: Frost & Sullivan Analysis

31

For Additional Information

Venkat Rajan Global Research Director: Visionary Healthcare

(210) 247-2427

Diana Bragg Strategic Account Manager: Transformational

Health

(210)-247-3825

32

Appendix-

Supplementary Analysis & Case Studies

33

Making the Transition from Reactionary to Predictive &

Proactive Care Intervention

Analysis

Data Collection

Comprehension

34

Precision Medicine Involves More than Just Genomics

Clinical

Factors

Real-Time

Monitoring

Factors

Exogenous

Factors

Omics/Dx

Factors

• Reduce adverse

drug reaction

(ADRs)

• Reduce Ineffective

prescriptions and

treatments

• More accurate and

rapid determination

of response to

therapy

• Patient-

empowerment

• Enhanced data for

future scientific

discoveries

• More effective and

safer therapeutics

• More precise

predictions of

diseases

• Earlier disease

detection

• Shift to more

patient-centric care

• Increased value-

based care

• New monetization

opportunities

Functions Benefits Precision Medicine

Patient

Source: Frost & Sullivan

35

Validic API— Interoperability Bridging the interoperability gap between healthcare companies and digital health technologies

On-body/

In-home/

RPM Home

Medical

Devices

Peripherals

Wearables

Implants

Health

Apps

Activity

Monitoring Other

mHealth

Solutions

Pu

sh

es S

ca

tte

red

an

d

Unsta

nd

ard

ize

d D

ata

Pu

lls A

ggre

ga

ted

an

d S

tan

dard

ize

d

Rele

va

nt H

ea

lth

Data

Health Systems

& Providers

Wellness

Companies

Payers

Pharmaceuticals

Cloud-based Technology

Platform:

Standardizes and normalizes the

data in an easily digestible format

1 2

Clinical, Fitness, and Wellness

Data from Non-hospital Settings

Source: Validic; Frost & Sullivan

36

Medtronic Hospital Solutions— Managed Services Platform-based cath lab solution for hospitals in Europe

Devices

Smart Financing Model

Capital Equipment

Cath Lab & Hospital IT

Cath Lab Management & Staffing

Operational Excellence Consulting

Growth Acceleration Services

Capital Structure

Optimization

Operational

Efficiencies

Patient Access

Solutions

Till Q2 FY16, Medtronic’s Hospital Solutions business has completed 66 long-term CLMS and ORMS agreements

with hospital systems, representing over $1.5 Billion in revenue over an average span of 6 years.

Key Benefits Focus Areas

Source: Medtronic; Frost & Sullivan

37

physiQ - Personalized Predictive Analytics Solution

Transform patient’s

multivariate data set into

personalized health and

wellness index.

Cloud-based Personalized

Predictive Analytics Platform

Physician remotely access personalized

health index and provide personalized

consultation/medication

Wellness professional leverages fitness

index to personalize activity and diet

Healthcare Providers and

Payers

Partnership with OEMs/Software Providers

B2

B2

C

B2

B

Feedback

1 2 3

Consumer wearables OEMs Clinical Wearables OEMs

B2B

Consum

er

Devic

e +

phys

iQ

Pre

dic

tive A

naly

tics P

latf

orm

Solu

tion

Clinical Device + physiQ

Predictive Analytics

Platform Solution

Marketing Channels

Direct

Indirect

FDA 510k-cleared

Source: physiQ; Frost & Sullivan

DaaS Business Model - Transform and personalize multivariate data set from wearables/sensors