monetary policy in india - cafral policy in india ... weighted average call rate as the explicit...

TRANSCRIPT

1

Monetary Policy in India

Deepak Mohanty Executive Director

Reserve Bank of India

September 16, 2013

2

An Outline

I. Objective(s)

II. Policy Framework

III. Operating Procedure

IV. Outcome

V. Conclusion

3

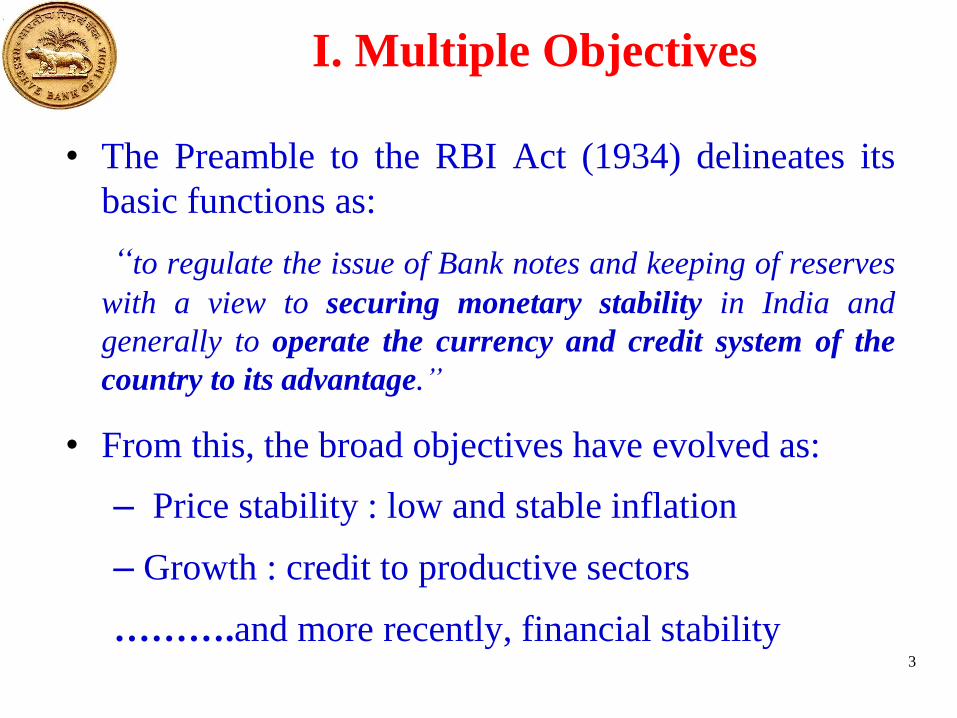

I. Multiple Objectives

• The Preamble to the RBI Act (1934) delineates its

basic functions as:

“to regulate the issue of Bank notes and keeping of reserves

with a view to securing monetary stability in India and

generally to operate the currency and credit system of the

country to its advantage.”

• From this, the broad objectives have evolved as:

– Price stability : low and stable inflation

– Growth : credit to productive sectors

……….and more recently, financial stability

4

II. Monetary Policy Framework

• Significant changes in monetary policy framework

Driven by:

- Financial market developments

- Institutional setting

- openness of the economy

- Shifts in monetary transmission mechanism

• No formal targets till mid-1980s

- Credit planning in mid-1960s

• Monetary Targeting : 1985-86 to 1997-98

• Multiple Indicators Approach : 1998-99 onwards

5

Monetary Targeting Framework (1986-1998)

• Key features

- Relatively closed economy

- Fiscal dominance

- Underdeveloped financial markets: interest rate regulation

• Broad money (M3) growth : the nominal anchor

• Reserve money : the operating target

• Bank Reserves: the operating instrument

• Stable relationship between money, output and prices

• Flexible approach allowing for feedback effects

6

Transition to the Multiple Indicators Approach (MIA)

Key features

- Relatively open economy

- Fiscal consolidation, eventually ‘fiscal rule’

- Financial market integration : through interest deregulation

- Problems in targeting money, rate channels gained importance

Use of multiple indicators

• High frequency data - interest rates/rates in financial markets

• Medium frequency data - currency, credit, banking data, inflation

• Low frequency data - fiscal, trade, capital flows and BoP, GDP

For drawing policy perspectives

7

Increasing Depth in the Financial Markets

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Per

cen

t o

f G

DP

G-sec (Central Govt) Foreign Exchange Market Money Market (including CP & CD Excl. T Bills )

8

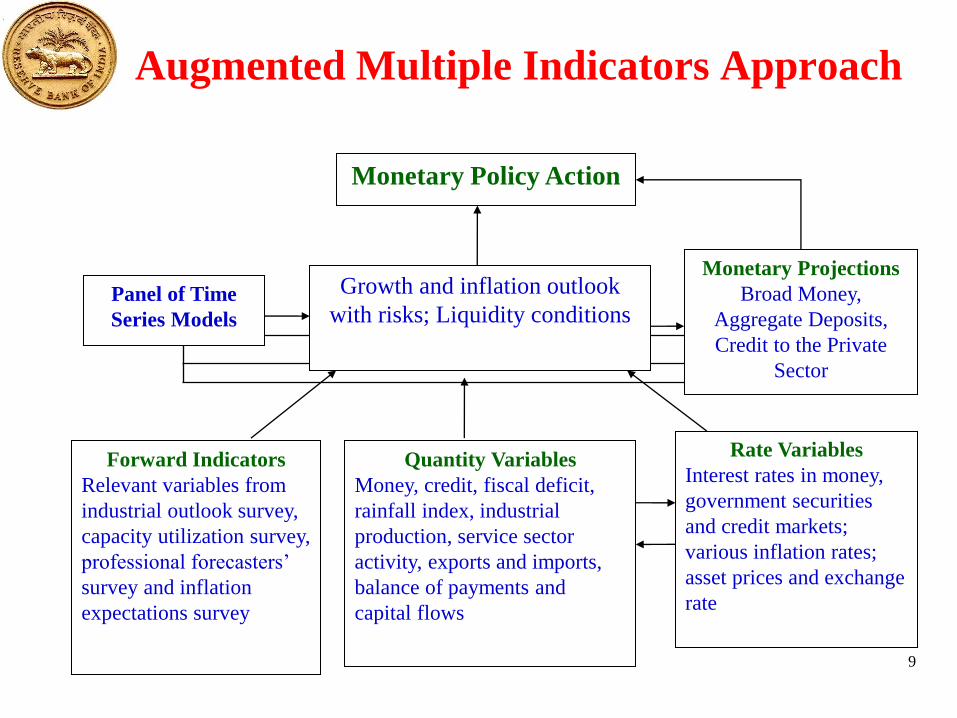

Evolution of Multiple Indicators Approach

• Multiple indicators approach

- Use of both quantity and rate variables

- Broad money continues to be an information variable

• Augmented multiple indicators approach

- Forward looking indicators (mid-2000s)

- Panel of models

9

Augmented Multiple Indicators Approach

Augmented Multiple Indicators Approach

Monetary Policy Action

Growth and inflation outlook

with risks; Liquidity conditions

Quantity Variables

Money, credit, fiscal deficit,

rainfall index, industrial

production, service sector

activity, exports and imports,

balance of payments and

capital flows

Rate Variables

Interest rates in money,

government securities

and credit markets;

various inflation rates;

asset prices and exchange

rate

Forward Indicators

Relevant variables from

industrial outlook survey,

capacity utilization survey,

professional forecasters’

survey and inflation

expectations survey

Monetary Projections

Broad Money,

Aggregate Deposits,

Credit to the Private

Sector

Panel of Time

Series Models

10

III. Operating Procedure

• Shift to indirect instruments of monetary control

• Money market the focal point for liquidity management

Liquidity Adjustment Facility (LAF)

- Repo and Reverse repo rate defines the corridor

- Primary instruments of interest rate signaling

- Primary instrument of managing day-to-day liquidity

Open Market Operations (OMO)

- Outright purchases/sales of G-Sec

Market Stabilisation Scheme (MSS)

- to absorb liquidity of more enduring capital flows

Flexible use of multiple instruments – LAF, OMO, CRR, SLR

11

Moving to a New Operating Procedure

Limitations of Extant LAF

Lack of single policy rate

lack of a firm corridor

Therefore, new operating procedure in May 2011.

Key Features of New LAF:

Weighted average call rate as the explicit operating target

Repo rate: only independently varying policy rate

New Marginal Standing Facility (MSF): linked to repo rate

The revised corridor with a fixed width of 200 basis points

12

New operating procedure

Rate of

interest

X+100 bps

X

X-100 bps

Bank Rate / Marginal Standing

Facility Rate (Ceiling)

Policy Rate (Repo Rate)

Overnight Call Rate (Target

Rate)

Reverse Repo Rate (Floor)

Liquidity

[This standing facility is available unlimited against collateral of

government securities from excess SLR and up to 2 per cent of

banks’ NDTL from required SLR].

[Liquidity against excess SLR securities and export credit refinance

facility for banks and liquidity facility for PDs]

[Liquidity absorption by the Reserve Bank of India against government securities]

• MSF rate recalibrated at 300 basis points above the policy repo rate on July 16, 2013 as part of measures to address exchange rate volatility.

13

Transmission Generally Stronger

Under Liquidity Deficit

-2.5

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

0

2

4

6

8

10

12

14

16

Oct

/09

Dec

/09

Feb

/10

Ap

r/10

Jun

/10

Au

g/1

0O

ct/1

0D

ec/1

0

Feb

/11

Ap

r/11

Jun

/11

Au

g/1

1O

ct/1

1D

ec/1

1

Feb

/12

Ap

r/12

Jun

/12

Au

g/1

2O

ct/1

2D

ec/1

2

Feb

/13

Ap

r/13

Jun

/13

Au

g/1

3

Liq

uid

ity (

Rs.

Tri

llio

n)

Rat

e (P

erce

nt)

Repo Rate Weighted Call Rate Liquidity (RHS)

-2.5

-2

-1.5

-1

-0.5

0

0

2

4

6

8

10

12

14

16

May

/13

May

/13

May

/13

Jun

/13

Jun

/13

Jul/

13

Jul/

13

Aug

/13

Aug

/13

Sep

/13

14

Call Rate More Stable

Under the New Procedure

Recent volatilities largely due to pressure in foreign exchange market.

4

6

8

10

12

14

02/J

ul/

10

02/S

ep/1

0

02/N

ov

/10

02/J

an/1

1

02/M

ar/1

1

02/M

ay/1

1

02/J

ul/

11

02/S

ep/1

1

02/N

ov

/11

02/J

an/1

2

02/M

ar/1

2

02/M

ay/1

2

02/J

ul/

12

02/S

ep/1

2

02/N

ov

/12

02/J

an/1

3

02/M

ar/1

3

02/M

ay/1

3

02/J

ul/

13

02/S

ep/1

3

Rat

e (P

erce

nt)

Call rate(ON) Average call rate

Average (AV) = 6.32

Standard Deviation (SD) = 0.74

Coefficient of variation (CV) =

11.72

Average (AV) = 8.07

Standard Deviation (SD) = 0.74

Coefficient of variation (CV) = 9.15

4

6

8

10

12

14

02/M

ay/1

3

16/M

ay/1

3

30/M

ay/1

3

13/J

un/1

3

27/J

un/1

3

11/J

ul/

13

25/J

ul/

13

08/A

ug

/13

22/A

ug

/13

05/S

ep/1

3

15

Call Rates Highly Correlated with

Other Money Market Rates

• Weighted call rate explicitly recognised as the operating target

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2-A

pr-

09

2-J

un

-09

2-A

ug-0

9

2-O

ct-0

9

2-D

ec-0

9

2-F

eb-1

0

2-A

pr-

10

2-J

un

-10

2-A

ug-1

0

2-O

ct-1

0

2-D

ec-1

0

2-F

eb-1

1

2-A

pr-

11

2-J

un

-11

2-A

ug-1

1

2-O

ct-1

1

2-D

ec-1

1

2-F

eb-1

2

2-A

pr-

12

2-J

un

-12

2-A

ug-1

2

2-O

ct-1

2

2-D

ec-1

2

2-F

eb-1

3

2-A

pr-

13

2-J

un

-13

2-A

ug-1

3

Ra

te (

Per

cen

t)

Weighted Money Market Rate (Call+CBLO+MR)

Weighted Call Rate

91 Day T-Bill (secondary market)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2-M

ay-1

3

16

-May

-13

30

-May

-13

13

-Jun

-13

27

-Jun

-13

11

-Jul-

13

25

-Jul-

13

8-A

ug-1

3

22

-Aug

-13

5-S

ep-1

3

16

IV: Outcome Improved Macroeconomic Performance

Under MIA albeit Some Recent Deterioration

Indicator

GDP

Growth (%)

Inflation (%) Call Rate

(%) WPI CPI-IW

1 2 3 4 5

Monetary Targeting

1985-86 to1997-98 5.5 8.1 9.1 11.7

(2.2) (3.0) (2.1) (4.0)

Multiple Indicators Approach

Pre-crisis

1998-99 to 2008-09 6.9 5.4 5.7 6.7

(1.9) (1.6) (3.0) (1.5)

Post-crisis

2009-10 to 2012-13

Projection (latest)

2013-14

7.3

5.5

7.4

5.0

10.4

6.3

Post-crisis: Inflation has remained high

17

Inflation Pressures Emerge, though the level is lower

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0A

pri

l

May

Ju

ne

Ju

ly

Au

gu

st

Sep

tem

ber

Oct

ob

er

No

vem

ber

Dec

emb

er

Ja

nu

ary

Feb

ruary

Marc

h

Y-o

-Y P

er

Ce

nt

WPI Inflation (Y-o-Y)

2011-12 2012-13 2013-14

18

Inflation Pressures from Food and Fuel Persist

* Three month moving average

0

5

10

15

20

25

Ap

r-1

0

Jun-1

0

Au

g-1

0

Oct

-10

Dec

-10

Feb

-11

Ap

r-1

1

Jun-1

1

Au

g-1

1

Oct

-11

Dec

-11

Feb

-12

Ap

r-1

2

Jun-1

2

Au

g-1

2

Oct

-12

Dec

-12

Feb

-13

Ap

r-1

3

Jun-1

3

Y-o

-y *

per

cen

t

All Commodities Food Articles Fuel & Power Non food manufacturing

19

Second-round Impact on CPI is visible

4

5

6

7

8

9

10

11

12

per

cen

t

WPI, CPI New (Combined) YoY Trends

WPI- All Commodities

New CPI (Combined)

New CPI (Combined)- ex. Food, Fuel and housing (Weight 33.2)

20

Demand Pressures from Fiscal Deficit are Significant

2

3

4

5

6

7

8

9

10

11

200

0-0

1

200

1-0

2

200

2-0

3

200

3-0

4

200

4-0

5

200

5-0

6

200

6-0

7

200

7-0

8

200

8-0

9

200

9-1

0

201

0-1

1

201

1-1

2

201

2-1

3

201

3-1

4

Per

cen

t o

f G

DP

Gross Fiscal Deficit- Budget Estimate vs Outcome

GFD - Centre BE GFD - Centre Outcome

GFD - Combined BE GFD - Combined Outcome

21

CAD Risks Remain

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

19

70

-71

19

72

-73

19

74

-75

19

76

-77

19

78

-79

19

80

-81

19

82

-83

19

84

-85

19

86

-87

19

88

-89

19

90

-91

19

92

-93

19

94

-95

19

96

-97

19

98

-99

20

00

-01

20

02

-03

20

04

-05

20

06

-07

20

08

-09

20

10

-11

20

12

-13

Perc

ent

of

GD

P

Both Oil and Non-oil current account balance deteriorated Significantly since 2008-09

Non-oil CAB CAB

22

Monetary Policy: Changes in Key Policy Rate

Overall NFMP Fuel Food

I. Oct-09 to Mar-10 25 75 7.1 1.6 4.6 18.1

II. Apr to Jul-10 75 25 10.4 5.6 13.8 15.4

III. Aug to Nov-10 50 - 8.8 5.4 11.2 10

IV. Dec-10 to Dec-11 225 - 9.5 7.6 13.1 8.1

V. Jan-12 to Aug-13 (-)125 (-)200 6.9 4.5 10.7 8.4

Inflation rates in last row are till July 2013

MSF rate increased by 200 bps from 8.25% to 10.25% w.e.f July 15, 2013

Inflation Phases and Changes in Key Policy Rates

PeriodRepo

(bps)

CRR

(bps)

WPI

23

Monetary Policy Witnessing Calibrated Easing After a Tightening Cycle

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

Ap

r-07

Jul-

07

Oct

-07

Jan

-08

Ap

r-08

Jul-

08

Oct

-08

Jan

-09

Ap

r-09

Jul-

09

Oct

-09

Jan

-10

Ap

r-10

Jul-

10

Oct

-10

Jan

-11

Ap

r-11

Jul-

11

Oct

-11

Jan

-12

Ap

r-12

Jul-

12

Oct

-12

Jan

-13

Ap

r-13

Jul-

13

Repo Rate CRR WPI Inflation 3m-MA

24

V. Conclusion

• Monetary policy in India : more eclectic

• Multiple Objectives: price stability, growth and financial stability

• Multiple instruments : provides flexibility

• Role of other factors: Fiscal consolidation & Globalisation

• Post-crisis:

- Some worsening in growth and inflation

• More-recent:

- Currency market pressure

- Stability? Pass-through?

25

Thank You