monday 26 february 2018 stock pickers’ paradise

TRANSCRIPT

Monday 26 February 2018

Stock pickers’ paradise

Have I got a treat for you today! You’re always asking me what to invest in for the long term, so notonly do I share what I do with my money in my story today, I’ve also asked the investment gurus fortheir best long-term pick.

Paul Rickard shares his opinion on what you should do with your Woodside rights, and James Dunnhas 3 small-cap surprises from earnings season. In Buy, Hold, Sell what the brokers say, we have abonanza of analyst actions – including upgrades for Medibank and Newcrest, and in Hot Stocks,Invocare gets a tick.

Sincerely,

Peter Switzer

Inside this Issue

3 small-cap surprisesfrom earnings seasonby James Dunn05

02 9 stocks to hold for 10 years – the guru selection!Experts nominate their favsby Peter Switzer

05 3 small-cap surprises from earnings seasonSmall packagesby James Dunn

08 Should you take up your Woodside rights?Great potentialby Paul Rickard

11 Buy, Hold, Sell – what the broker saysMedibank, Newcrest upgradedby Rudi Filapek-Vandyck

16 Hot Stocks – Invocare and CitigroupOut of favourby Staff Reporter

Switzer Super Report is published by Switzer Financial Group Pty Ltd AFSL No. 286 531Level 4, 10 Spring Street, Sydney, NSW, 2000T: 1300 794 893 F: (02) 9222 1456

Important information: This content has been prepared without taking accountof the objectives, financial situation or needs of any particular individual. It doesnot constitute formal advice. For this reason, any individual should, beforeacting, consider the appropriateness of the information, having regard to theindividual's objectives, financial situation and needs and, if necessary, seekappropriate professional advice.

9 stocks to hold for 10 years – the guruselection!by Peter Switzer

One of the most frequent questions I receive on radioand in real life is “what stocks/s can I buy for thelong-term?” Predictably I often refer novices to lookat the big four banks, CSL, and Macquarie wheneverthe market decides to fall out of love with thesegreat-performers.

Of course, individual stocks always have risks linkedto government, competition, technological change,etc. A crazy CEO can also be a risk and that’s why Isay to many newcomers that a core holding of sayiShares Core S&P/ASX 200 ETF (IOZ) or SPDR®S&P®/ASX 200 Fund (STW), maybe along with adividend-paying fund such as my own SwitzerDividend Growth Fund (SWTZ), is a pretty safe wayto dive into the stock market for the long-term. Youcould easily split your core holding in your portfolio ofstocks between, say IOZ and SWTZ and have a fairlystable foundation over a 10-year period.

The chart below shows why:

This shows that $10,000 invested in Australianshares in 1987 grows to $113,405 after 30 years andthat’s despite market crashes in 1987, 2000-01 and2007-09. Exchange traded funds, such as IOZ, withits dividends reinvested, should perform like this inthe future. My SWTZ is a little more defensive as it

searches for 30-40 dividend-payers but it also tracksthe index as well with a tad less capital gain, onaverage.

Best of breed

I have talked about this combo-holding, that I haveused in my SMSF, before but what about someindividual stocks that could be 10 or even 30 yearholds?

I asked John Murray of Perennial Value, CharlieAitken of Aitken Asset Management, AntonTagliaferro of Investors Mutual, Geoff Wilson fromWilson Asset Management, Mary Manning ofEllerston Capital, Nathan Bell of Naos AssetManagement, Rudi Filapek Vandyck of FM Arena andour own Paul Rickard, the founding CEO ofCommSec and a former Stockbroker of the Year togive us their best stock to hold for at least 10 years.

I believe this is a great way to get a collection of thebest of breed companies assessed by people, wholive and breathe stocks and the underlying businessthey represent. And some of the answers evensurprised me. I’ll start with a few overseascompanies that many of us should think about,especially if you have little or no exposure to foreignmarkets, and then look at some local surpriseselections.

Let’s start with our star stock picker, Charlie Aitken,whose fund can, and does, invest locally withcompanies such as Treasury Wine Estates, CSL andAristocrat, which he has always maintained are localworld-class companies. That said, his well-performingfund is top-heavy with overseas stocks, as he hasmaintained, for at least three years, that we shouldinvest here for income and overseas for growth.

02Monday 26 February 2018

So it’s not that surprising that he went abroad when Iasked him for his best stock to hold for 10 years.“Tencent (700HK),” he said. “I think it will be thebiggest market cap stock in the world in under 10years’ time!”

Sticking with the overseas theme, Nathan Bell ofNaos had an interesting stock that many of uswouldn’t have thought about.

This is what he told me to share with you:“While most Australian investors are heavily focusedon dividends, the best type of business to own overthe long term is one that can reinvest all its profits athigh rates of return. “Few companies can do this, butcable TV and internet provider Liberty LiLAC is one.Liberty LiLAC is the South American outpost of JohnMalone’s cable TV and internet empire.

“LiLAC occupies the number one or two marketposition in its markets, such as Chile, whereregulation encourages companies to invest in fasterinternet speeds for the long term.

“Internet usage in countries where LiLAC operates isoften at half the levels experienced by developednations, showing there’s a long runway for growth.LiLAC also expects to make acquisitions andincrease its market position over time.

“Although the company has a lot of debt, it shouldn’tbe a problem, given the currency exposures arehedged, maturities are increasing and the businessproduces plenty of cash. Owning it for 10 yearsmeans any volatility caused by short term fears aboutthe debt or regional issues, such as last year’shurricanes in Puerto Rico that impact 5% of thecompany’s revenues, will fade away as the newCEO’s acquisition-led strategy steadily increasesprofits.”

Let’s get more locally-focused and start off with asurprising one from Roger Montgomery ofMontgomery Asset Management. Over the years,Roger and I have done a lot of interviews and I cantell you he has never been a big fan of Telstra andcompanies that pay too high dividends at the expenseof capital growth. He hates lazy companies that don’tretain profits to grow their operations, so I was a littlesurprised at his selection.

“I’d select CBA,” he said. “I would have said CSL,but it’s too expensive.”

WAM’s Geoff Wilson was just as brief but in histypical forthright manner opted for a telco in TPG andthat was bit of a surprise as well.

“It’s run by one of the best managing directors inAustralia,” he insisted. “Over the next decade, TPGwill do to mobiles what it did to the internet.”

In the ‘keep it brief and to the point’, my old mateAnton Tagliaferro of Investors Mutual emailed me hisselection, manufacturer of rigid plastic packaging :“Pact Group.”

John Murray, one of the country’s most respectedfund managers, who has a love affair with gooddividend-paying stocks says: “EVT — EventHospitality & Entertainment Limited — has a pristinebalance sheet, tourism and leisure theme, consistentprofit track record and steadily growing dividendsover time.”

FN Arena’s Rudi Filapek Vandyke is pouring overlocal companies pretty well 24/7, as his operationsurveys brokers and company analysts but he’sopted for the bluest of blue chips.

“My stock for the next 10 years is CSL,” he said.“This is a grossly underappreciated stock by many aninvestor in Australia.”

Another expert to opt for an overseas company wasMary Manning, who is a portfolio manager with anAsian focus at Ellerston. She is really enthusiasticabout China and India.

“A stock I would buy and keep for 10 years is MarutiSuzuki (MSIL IN), the largest car company in India,”she suggested confidently. “The stock was a 10bagger in the last 10 years, so hopefully the nextdecade will bring more of the same.”

“Maruti Suzuki has a world class management teamand excellent ESG (Environmental, Social andGovernance) credentials. Suzuki Motor Corp of Japanholds 56% of the Maruti Suzuki and there is crossfertilization of best practices from the Japanese automaker.”

03Monday 26 February 2018

“MSIL has pulled back 10% from its December high,so this level provides a good entry point.”

Price Chart of MSIL over the Last 10 Years: A 10Bagger

Finally, my colleague at the Switzer Report, PaulRickard, says: “A little reluctantly, I am going tonominate CSL,” he said. “Unquestionably it isAustralia’s best stock over the last decade andthough history says that companies rarely remain “atthe top” for such a long period, I think this will be anexception, even though it is super expensive!

“It has a global leading position in blood plasmaproducts and number two in influenza; a top notchmanagement team and the tailwinds of an ageingpopulation with its demand for health services.”

So there it is! I’ll recap the stocks given the 10-yearthumbs up:

1. Tencent2. Liberty LiLAC3. CBA4. TPG5. Pact Group6. CSL7. Event Hospitality & Entertainment8. Maruti Suzuki9. IOZ + SWTZ as a combo.

And I reckon this would prove to be a pretty goodportfolio to hold for 10 years. Let’s see in 10 years’time!

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regard to yourcircumstances.

04Monday 26 February 2018

3 small-cap surprises from earnings seasonby James Dunn

With the interim profit reporting season in its finaldays, the upshot is that it has been a good one:according to AMP Capital, 73% of companies havereported profits higher than a year ago, which is aproportion both well up on the “norm” of 65%, andmore impressively, the highest since the GFC hit adecade ago. About 46% of results have exceededexpectations – against a norm of 44% – and 66% ofcompanies have increased dividends from a yearago.

Consensus profit growth expectations for the 2017-18financial year across the market remain at about 7%,with resources stocks having been upgraded slightlyto 15% and the rest of the market downgraded to 5%from 6%, mostly on the back of diminishedexpectations for the banks. Profit expectations for the2018-19 financial year have been lifted from 4% to5%, on the back of higher expectations for resourcecompanies.

Here are three small-cap companies that surprisedthe market with good news during the reportingseason:

Afterpay Touch (APT)

Market capitalisation: $1.5 billionFY18 forecast yield: n/aAnalysts’ consensus target price: $9.20

Source: ASX

At $1.5 billion, fintech star Afterpay Touch is barely a“small-cap” these days, and it may not carry that tagmuch longer. Afterpay offers a buy-now, receive-now,pay-later service in the Australian and New Zealandretail markets: its frictionless payments technologyallows shoppers to buy goods and split the paymentover four equal fortnightly installments, with paymentslinked to the customers’ debit or credit accounts. Aretailer pays Afterpay a merchant’s fee for eachtransaction.

Afterpay did not so much surprise on the profit front: itreported a pre-tax profit of $700,000 for theDecember half-year, which turned into a net loss ofthe same amount. Nor did Afterpay upgrade itsguidance: it had done that in January, with respect tothe half-year. Its EBITDA (earnings before interest,tax, depreciation and amortisation) came in at $12.1million, slightly ahead of that guidance, which was forEBITDA in the range of $11 million–$12 million.

Where Afterpay surprised the market was in its keynumbers, which quite simply, defied the tough timesin retail. Underlying merchant sales for the Pay Laterbusiness increased to $918 million for the six months

05Monday 26 February 2018

to 31 December 2017, up from $145 million in thesame period in 2016. The number of merchantsintegrated into the Afterpay system swelled from2,044 in December 2016 to 11,500. Merchant feesgrew six-fold to $37 million in six months. The numberof customers using Afterpay jumped from 400,000 to1.5 million and 90% of transactions are repeatbusiness.

Afterpay estimates that it now handles more than25% of all Australian domestic apparel online salesand more than 8% of all online physical retail sales. Itsays more than 15% of all Australian “millennials”are Afterpay customers: its app has beendownloaded more than one million times. And beforethe result, in January, Afterpay announced plans tointroduce the Afterpay platform in the United States,in a strategic partnership with venture capital firmMatrix Partners, which took $19 million worth ofshares.

Afterpay looks to be a working example of the“network effect:” the more customers who use it, themore merchants want to join it – and the more itgrows. But the good news is that on analysts’consensus target price, Afterpay appears to havescope to rise. It is a growth story only at this stage,with no dividend foreseen.

Webjet (WEB)

Market capitalisation: $1.4 billionFY18 forecast yield: 1.7%, fully frankedAnalysts’ consensus target price: $13.33

Source: ASX

After disappointing the market in November 2017when it told its shareholders to expect totaltransaction volume (TTV) of $3 billion and EBITDA(earnings before interest, tax, depreciation andamortisation) of $80 million in FY18 – which was adisappointment because the market expected more –travel website operator Webjet came through with anoutstanding first-half result. The company upgradedits full-year guidance, but brokers appear to believethis could turn out to be conservative.

The first half result was replete with strong organicgrowth, which investors always want to see. TTV(total travel services sold) surged 55%, to $1.44billion, while EBITDA jumped 63% to $41 million. Thebusiness-to-consumer (B2C) flights booking businesslifted earnings by 26%, and continues to generatebookings growth ahead of the market.

Bookings for flights grew by 11%, while packagesbooking jumped by 86.4%. The business-to-business(B2B) segment reported bookings growth of 227%and TTV growth of 168%, which saw revenue surge170% and segment EBITDA increase 14 times.Webjet said bookings were up in January in allbusinesses and it expected trading in the second halfto be stronger than in the first half – TTV, bookings,and EBITDA are all expected to be higher. Analystsexpect about 47% growth in earnings per share(EPS) in FY18 and about 34% in FY19. And analystssee Webjet as undervalued, on consensus targetprice.

Integral Diagnostics (IDX)

Market capitalisation: $325 millionFY18 forecast yield: 3.6%, fully frankedAnalysts’ consensus target price: $2.33

06Monday 26 February 2018

Medical imaging business Integral Diagnostics, whichoperates 47 clinics across Western Australia,Queensland and Victoria, was one of the guidancestars of the half-year reporting season. At its 2017annual general meeting (AGM), Integral stated FY18guidance for “high single-digit” net profit growth, butnow expects to achieve full-year normalised net profitgrowth of about 20%, as a result of stronger revenuegrowth.

The upgraded guidance came after a first half thatsaw operating revenue rise 6% to $92.8 million andunderlying net profit climb 23% to $9.2 million. Thecompany expects strong revenue growth in thesecond half, as well as cost efficiency gains, lowercapital spending, driven by economies of scale,favourable lease negotiations and a reduction in itseffective tax rate from 30% to 28%, flowing fromcapital revaluations for tax depreciation purposes.

Integral Diagnostics is fighting off a takeover bid fromrival radiology business Capitol Health, which Capitollobbed in November. Integral has told itsshareholders to take no action, describing the offer as“opportunistic” questioning the underlying value ofCapitol’s shares, and saying it doubts that Capitolhas the ability to run a combined business.

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regard to yourcircumstances.

07Monday 26 February 2018

Should you take up your Woodside rights?by Paul Rickard

Woodside has the potential to be a truly greatAustralian company. It invests billions of dollars inincredibly complex, long lead time oil and gasprojects that involve huge feats of engineering,usually in partnership with one or more of the globalresource giants. And it’s doing it for Australia.

But unfortunately, it has struggled to live up to thispotential. Over its 40-plus years of being a listedcompany, it has disappointed shareholders moreoften than it has delivered. Maybe this is why Shellfinally quit Woodside last November, when it sold itsfinal tranche of shares at $31.10 per share. Aftertrying to buy 100% of Woodside in 2001 and beingfamously rejected by the then Treasurer PeterCostello on “national interest grounds”, it sold its firsttranche of 10% of Woodside in 2010 at $42.23 pershare. It sold another tranche of 9.5% in 2014 at$41.35 per share, before the final sale of 13.5%.

Four months’ after Shell’s exit, Woodside is tappingshareholders for $2.5 billion through a renounceableentitlement issue, the biggest capital raise by a listedcompany over the last two years.

Should you take up your entitlement, or as someshareholders might suggest, put more good money inafter bad?

Firstly, let’s look at why Woodside is raising thecapital.

Boosting reserves and production to meet aglobal LNG supply gap

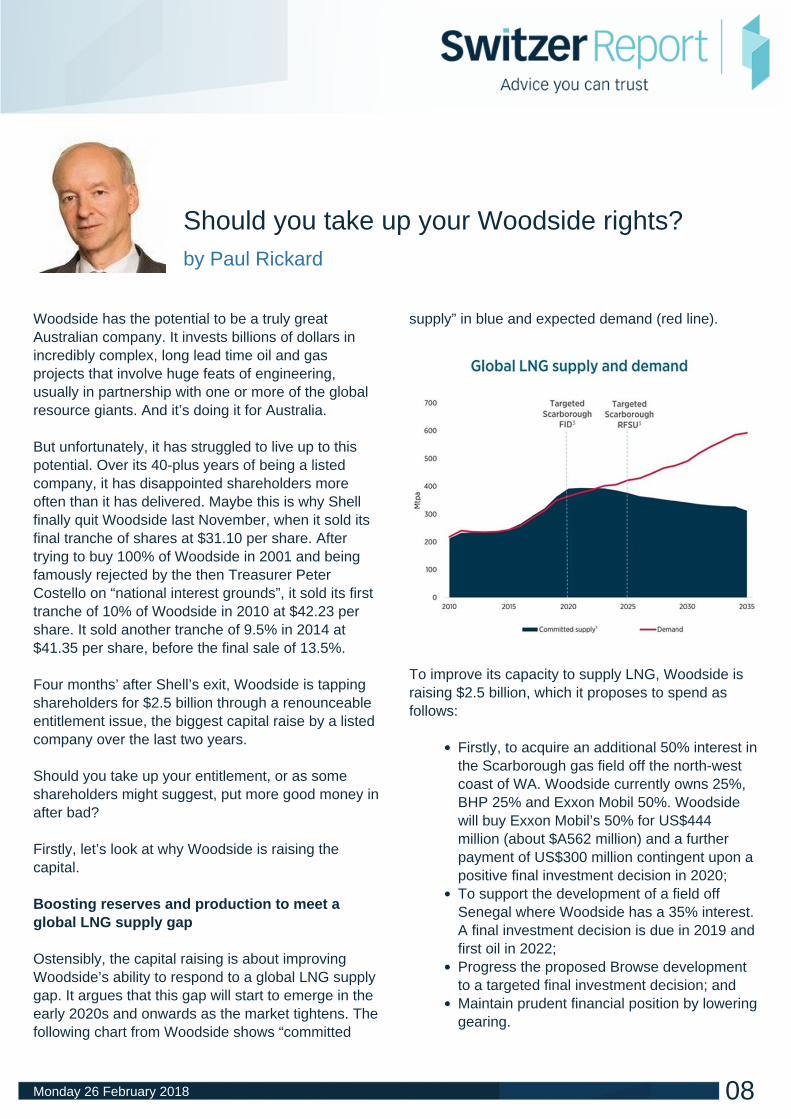

Ostensibly, the capital raising is about improvingWoodside’s ability to respond to a global LNG supplygap. It argues that this gap will start to emerge in theearly 2020s and onwards as the market tightens. Thefollowing chart from Woodside shows “committed

supply” in blue and expected demand (red line).

To improve its capacity to supply LNG, Woodside israising $2.5 billion, which it proposes to spend asfollows:

Firstly, to acquire an additional 50% interest inthe Scarborough gas field off the north-westcoast of WA. Woodside currently owns 25%,BHP 25% and Exxon Mobil 50%. Woodsidewill buy Exxon Mobil’s 50% for US$444million (about $A562 million) and a furtherpayment of US$300 million contingent upon apositive final investment decision in 2020;To support the development of a field offSenegal where Woodside has a 35% interest.A final investment decision is due in 2019 andfirst oil in 2022;Progress the proposed Browse developmentto a targeted final investment decision; andMaintain prudent financial position by loweringgearing.

08Monday 26 February 2018

The rational for acquiring a 75% majority interest inScarborough and sharing ownership of that resourcewith just one joint venture partner is that it givesgreater alignment, certainty and control of the project.Woodside believes that Scarborough can leverage a“brownfield expansion” of its existing onshore PlutoLNG liquefaction facility near Karratha.

Shareholder options

Woodside is raising $2.5 billion through a 1 for 9renounceable entitlement issue to acquire newWoodside shares at $27.00 per share. Fractions arerounded up, so if for example you have 1,000Woodside shares, you will receive an entitlement tobuy 112 new shares.

The first part of the issue, the offer to institutions, wascomplete last week. It raised $1.57 billion. The retailoffer, which is fully underwritten, is set to raise $0.96billion.

Shareholders have three choices. Firstly, you canaccept the offer (for all or part) and purchase newshares at $27.00. Payment must be made by 5.00pmon Wednesday 7 March.

Secondly, you can sell your entitlement on the ASX.Trading, under stock code WPLR, ceases thisWednesday (28 February).

The third option is to “do nothing”. In this scenario,your entitlement will be sold through a retail shortfallbookbuild to be held on 12 March. If the bookbuildclearing price is greater than $27.00, then you willreceive the amount more than $27.00 (or thepremium) via a refund, which is expected to be paidon 21 March.

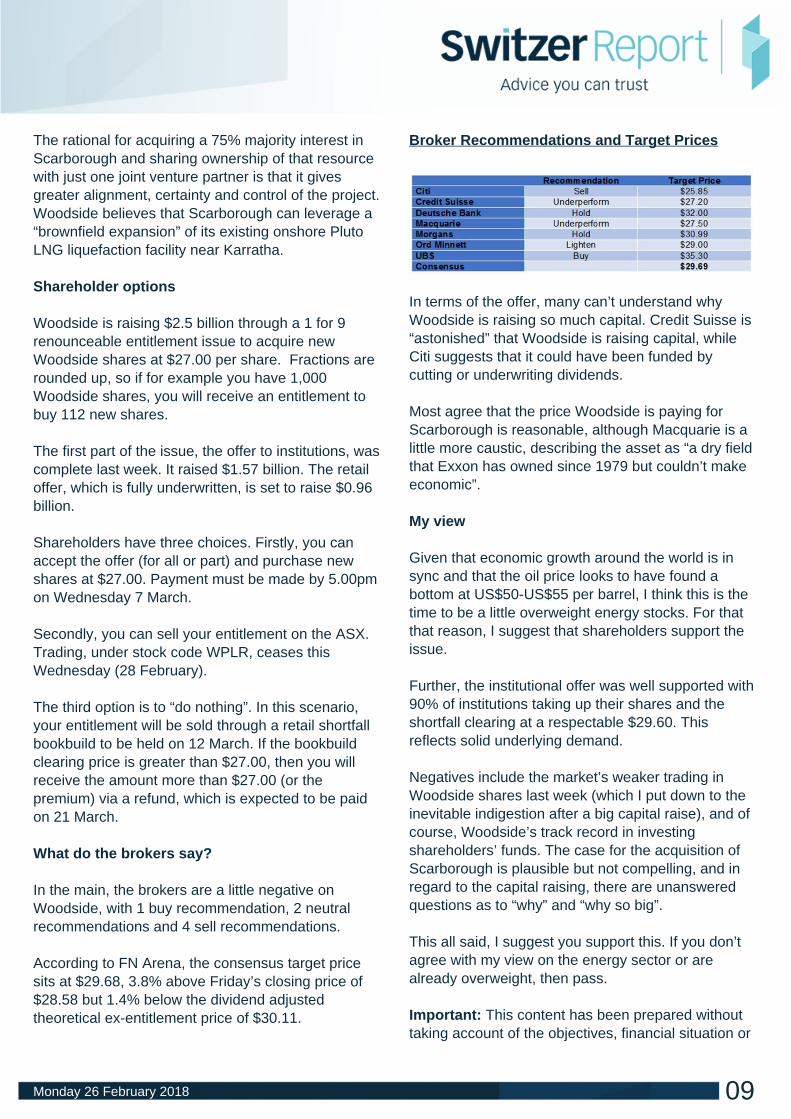

What do the brokers say?

In the main, the brokers are a little negative onWoodside, with 1 buy recommendation, 2 neutralrecommendations and 4 sell recommendations.

According to FN Arena, the consensus target pricesits at $29.68, 3.8% above Friday’s closing price of$28.58 but 1.4% below the dividend adjustedtheoretical ex-entitlement price of $30.11.

Broker Recommendations and Target Prices

In terms of the offer, many can’t understand whyWoodside is raising so much capital. Credit Suisse is“astonished” that Woodside is raising capital, whileCiti suggests that it could have been funded bycutting or underwriting dividends.

Most agree that the price Woodside is paying forScarborough is reasonable, although Macquarie is alittle more caustic, describing the asset as “a dry fieldthat Exxon has owned since 1979 but couldn’t makeeconomic”.

My view

Given that economic growth around the world is insync and that the oil price looks to have found abottom at US$50-US$55 per barrel, I think this is thetime to be a little overweight energy stocks. For thatthat reason, I suggest that shareholders support theissue.

Further, the institutional offer was well supported with90% of institutions taking up their shares and theshortfall clearing at a respectable $29.60. Thisreflects solid underlying demand.

Negatives include the market’s weaker trading inWoodside shares last week (which I put down to theinevitable indigestion after a big capital raise), and ofcourse, Woodside’s track record in investingshareholders’ funds. The case for the acquisition ofScarborough is plausible but not compelling, and inregard to the capital raising, there are unansweredquestions as to “why” and “why so big”.

This all said, I suggest you support this. If you don’tagree with my view on the energy sector or arealready overweight, then pass.

Important: This content has been prepared withouttaking account of the objectives, financial situation or

09Monday 26 February 2018

needs of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regard to yourcircumstances.

10Monday 26 February 2018

Buy, Hold, Sell – what the broker saysby Rudi Filapek-Vandyck

“Busy” no longer covers it. In the third week of thelocal February reporting season, ending on Friday,23rd February 2018, FNArena registered no less than45 upgrades for individual ASX-listed entitiesaccompanied by 23 downgrades. The comboJPMorgan/Ord Minnett has now joined the three Ms(Macquarie, Morgans and Morgan Stanley) incarrying more Buy ratings for stocks under coveragethan either Neutral or Sell ratings.

In the good books

THE A2 MILK COMPANY LIMITED (A2M) wasupgraded to Outperform from Neutral by CreditSuisse and to Buy from Hold by Deutsche Bank.B/H/S: 4/1/0. First half results beat expectationsacross the board. With significant financial capacityand a commitment to further investment in marketing,Credit Suisse expects the company to double itsrevenue stream in 10 years. Target is raised toNZ$12.75 from NZ$8.50. Deutsche Bank wasexpecting a strong result, but what A2 Milk releasedwas still a “strong beat”. Announcing a strategicagreement with Fonterra further lifted overallsentiment. Price target rises to NZ$14 (up 52%).

APN OUTDOOR GROUP LIMITED (APO) wasupgraded to Outperform from Neutral by CreditSuisse. B/H/S: 3/3/0 FY17 results were “not great”in the broker’s opinion. Of most interest was thesecond half sales growth of 2% in Roadside againstan 11% forecast, a big miss for the company’sbiggest division. Credit Suisse lowers EPS forecastsby 7-8%. With turnaround measures either completeor in train the broker expects a better performance in2018. The broker upgrades to Outperform from

11Monday 26 February 2018

Neutral and raises the target price to $5.05 from$4.70.See also APO downgrade.

ARB CORPORATION LIMITED (ARB) Upgrade toOutperform from Neutral by Macquarie. B/H/S:1/2/0. Domestic conditions remain robust and theoutlook is positive. Export markets are strengtheningand the company’s initiatives have improved revenuegrowth, which should lead to margin expansion.Greater market confidence in the improving growthoutlook should prompt a re-rating, the brokerbelieves. Target rises to $21.00 from $17.70. Seealso ARB downgrade.

CORPORATE TRAVEL MANAGEMENT LIMITED(CTD) was upgraded to Buy from Accumulate byOrd Minnett and to Buy from Neutral by UBS. B/H/S: 4/1/0.The interim report was carried by a largeincrease in EBITDA margins, and Ord Minnett seesyet more evidence of the strength on top of thesimplicity of Corporate Travel’s business model.Estimates were lifted. Price target moves to $24.36from $21.98. Rating upgraded to Buy fromAccumulate with the analysts lauding “the strength ofthe business model”. First half results were just shyof UBS estimates. ANZ and Europe were thestand-outs while N America and Asia facedchallenging conditions. UBS raises the target to$25.85 from $23.25.

CLEANAWAY WASTE MANAGEMENT LIMITED(CWY) was upgraded to Add from Hold byMorgans. B/H/S: 3/2/0. First half results were aheadof forecasts. Morgans lifts operating earningsforecasts for FY18-21 by 1-2%. The companyenvisages recent changes to the Chinese importationof municipal recycled waste as an opportunity, byassisting local governments to mitigate the issue.Target is raised to $1.68 from $1.61.

ESTIA HEALTH LIMITED (EHE) was upgraded toBuy from Neutral by UBS. B/H/S: 1/2/0. The solidfirst half result was in line with UBS estimates. The100% dividend pay-out ratio was a surprise to theupside. FY18 EBITDA guidance was reiterated atmid-single digit percentage growth, with the updatedUBS forecast now sitting at $92.1 million. Target israised to $4.00 from $3.75.

FLIGHT CENTRE LIMITED (FLT) was upgraded to

Neutral from Sell by Citi and to Equal-weight fromUnderweight by Morgan Stanley. B/H/S: 2/4/2. Firsthalf results were above the top end of guidanceranges despite the disruption to the core Australianbusiness. Citi notes the results were driven by theUS, EMEA and Asia, which have been challengedfrom a profitability perspective for many years. Targetis raised to $54 from $45. First half results werebetter than Morgan Stanley expected, driven byacquisitions and cost savings. The broker expectstotal transaction value growth to accelerate in thesecond half. Target rises to $54 from $38 to reflectlower capex and expanding corporatebusiness. Industry view is Cautious.

FLEXIGROUP LIMITED (FXL) was upgraded toBuy from Neutral by Citi. B/H/S: 3/3/0. Citi analystshave been biding their time, waiting for that triggerthat would allow for the gap between share price andvaluation to close. It appears they now think therecent interim report release might be that trigger.Upgrade to Buy from Neutral. Target price rises by14% to $2.14.

IRESS MARKET TECHNOLOGY LIMITED (IRE)was upgraded to Hold from Lighten by OrdMinnett. B/H/S: 0/4/0. 2017 results were at the topend of the prior guidance range and ahead of OrdMinnett’s forecasts. Given the substantial number ofacquisitions over the last couple of years the brokerawaits signs of a sustained recovery in profitabilitybefore becoming more constructive. Nevertheless,the drop in the share price since January leads to araising of the recommendation to Hold from Lighten.Target is $11.

MEDIBANK PRIVATE LIMITED (MPL) wasupgraded to Buy from Hold by Deutsche Bank. B/H/S: 1/4/2. Medibank Private’s results impressedthe broker. Deutsche Bank noted a $34 million claimsprovision release boosted the result, but itdemonstrates positive momentum on claimsmanagement. The broker notes strong marginmomentum resulting from cost control and lowerhospital utilisation. Target rises to $3.35 from $3.20.

NEWCREST MINING LIMITED (NCM) wasupgraded to Accumulate from Hold by OrdMinnett. B/H/S: 2/3/3. Ord Minnett observes thestock has underperformed the US dollar and

12Monday 26 February 2018

Australian dollar gold price as well as mid-cap peers.Yet, despite major production disruptions and ashrinking portfolio, the company is considered inbetter shape than it has been for many years. Thebalance sheet has been repaired, gearing is 16% andfree cash flow is improving while there are accretivegrowth options. Target is raised to $25.00 from$22.50.

NINE ENTERTAINMENT CO. HOLDINGS LIMITED(NEC) was upgrade to Neutral from Sell by UBS. B/H/S: 3/2/1. UBS was impressed by the first halfresults, which showed revenue share at 13-yearhighs. UBS believes FY18 guidance of $231-261million looks slightly conservative and is factoringFY18 EBITDA of $262 million. The broker raises thetarget price to $1.90 from $1.35.

NIB HOLDINGS LIMITED (NHF) Upgrade to Neutralfrom Sell by Citi. B/H/S: 0/5/2. Management hasupgraded guidance, but Citi maintains the risk is tothe upside. Their own forecast remains well aboveincreased guidance for this year. Estimates havebeen increased by 6-8%. Target price lifts by 50c to$6.50.

ST BARBARA LIMITED (SBM) was upgraded toNeutral from Underperform by Credit Suisse andto Accumulate from Hold by Ord Minnett. B/H/S:2/2/1. First half earnings were in line withexpectations. The extra guidance for Gwalia, with amaterially improved production and cost profile, addsto Credit Suisse’s valuation on base caseassumptions. Target is raised to $3.85 from $3.00.Ord Minnett estimates the new mining strategy couldadd $400 million in value, or $0.80 a share, over theprevious mine plan. Target is raised to $4.30 from$3.80.

SANTOS LIMITED (STO) was upgraded to Neutralfrom Sell by UBS. B/H/S: 3/4/1. The positivetake-away is that, after cutting costs, Santos looks tobe on track to shrink net debt to below $2 billion bythe end of 2019. Not only is this well ahead ofschedule, it also allows for the return of shareholderdividends in 2019, points out UBS. The brokerupgrades to Neutral from Sell on a weak share price,noting that the above should also allow for anincrease in growth investment. Target remains $5.25.

VILLAGE ROADSHOW LIMITED (VRL) wasupgraded to Hold from Lighten by Ord Minnett, toNeutral from Underperform by Macquarie and toBuy from Neutral by Citi. B/H/S: 1/3/0. Thecompany stated that theme parks have shown asignificant recovery in January, with ticket yield up30% and admission revenue up 24%. Ord Minnettwelcomes the positive developments but would preferto wait for an extended recovery, given recentdisappointments. The broker upgrades to Hold fromLighten. Target is $3.25. Macquarie sees animproving outlook for Village Roadshow post resultrelease. Improvement at Gold Coast theme parkssuggests upside risk to earnings and capital structureis more sustainable. Risk/reward potential isnevertheless better reflected in the current price,hence Macquarie upgrades to Neutral fromUnderperform. Target rises to $3.50 from $3.30. Aworried Citi has remained on the sideline for a longwhile, but now the analysts believe the time is rightfor an upgrade to Buy from Neutral. Improved themepark momentum seems to be the trigger point. Pricetarget has lifted to $3.90 from $3.45 with higherforecasts further out supported by the company’scost out ambition.

WEBJET LIMITED (WEB) was upgraded toOutperform from Neutral by Credit Suisse. B/H/S:4/0/1. First half results were materially better thanforecast. Credit Suisse observes the company hassuccessfully de-risked the core flights businessthrough ancillary products. Despite a history of weakfirst half cash flow, worst fears did not materialize.Credit Suisse believes the short-term overhang onthe stock will continue to unwind and upgrades toOutperform from Neutral. Target rises to $13.65 from$11.80.

WESFARMERS LIMITED (WES) was upgraded toHold from Sell by Deutsche Bank and to Neutralfrom Sell by Citi. B/H/S: 1/6/1. First half earningswere slightly ahead of estimates. Deutsche Bank stillenvisages risks around the UK operations amidcontinued large operating losses or the potential forsubstantial exit costs. Meanwhile, BunningsAustralasia and Kmart are well-positioned. The brokerbelieves the risk/reward is now balanced andupgrades to Hold from Sell. Target rises to $40 from$37. Citi has now upgraded to Neutral from Sell, whilebumping up the price target to $41 from $39.30. The

13Monday 26 February 2018

good news, as Citi sees it, is the supermarketoperators are seemingly behaving rationally for now.

In the not-so-good books

APN OUTDOOR GROUP LIMITED (APO) wasdowngraded to Hold from Add by Morgans. B/H/S:3/3/0. The new CEO, James Warburton, has outlineda plan to rebuild the company, involving a step up ininvestment in personnel and technology. Morganssuggests this may provide long-term benefits but willmake earnings growth almost impossible in 2018.The broker slashes profit forecasts to reflect highercosts and higher ongoing capital expenditure. Targetis reduced to $4.44 from $5.48.See also APOupgrade.

ARB CORPORATION LIMITED (ARB) wasdowngraded to Neutral from Buy by Citi. B/H/S:1/2/0. Citi believes it is time to take some profits inlight of the strong start to FY18 in the first half. Ratingis downgraded to Neutral from Buy. The brokerincreases FY19-20 forecasts by 6-7%. Citi expectsthe PE will moderate over the short term. Target israised to $22.43 from $17.85 as the model is rolledforward amid index multiple expansion. See also ARBupgrade.

BLACKMORES LIMITED (BKL) was downgradedto Neutral from Outperform by Credit Suisse.B/H/S: 1/2/0. Credit Suisse has downgraded toNeutral from Outperform with a reduced target to$130 from $150, suggesting the share price might

remain under pressure short term, but alsoemphasising it remains “optimistic” on thecompany’s growth prospects. Following the interimreport, the analysts now suggest Blackmores will stillgrow, but it won’t be at a spectacular rate. They alsoobserve competitor Swisse seems to be performingbetter.

HT&E LIMITED (HT1) Downgrade to Neutral fromBuy by UBS. B/H/S: 4/2/0. 2017 results were largelyin line with estimates. UBS notes Adsheloutperformed the broader market in both Australiaand New Zealand while Hong Kong outdoor alsoimproved. Despite meeting expectations, UBSdowngrades to Neutral from Buy, now incorporating apotential liability from the ATO tax dispute. Target isreduced $1.80 from $2.25.

INVOCARE LIMITED (IVC) was downgraded toNeutral from Outperform by Macquarie. B/H/S:1/2/3. InvoCare posted a solid result ahead ofMacquarie’s forecast. FY guidance neverthelesssurprised to the downside, suggesting flat earningsgrowth due to capital spending on the company’sprotect & grow strategy. Target falls to $14.34 from$15.31.

OOH!MEDIA LIMITED (OML) was downgraded toNeutral from Outperform by Credit Suisse. B/H/S:4/1/0. 2017 gross profit was ahead of expectations.Credit Suisse believes the risk/reward profile warrantsa more circumspect view. Most of the business isperforming well but there are areas that requirecaution. The company continues to press on with anelevated capital expenditure program despite industrygrowth declining to mid-low single digits, the brokernotes. Target is raised to $4.95 from $4.75.

THE STAR ENTERTAINMENT GROUP LIMITED(SGR) was downgraded to Neutral fromOutperform by Credit Suisse. B/H/S: 7/1/0. Firsthalf earnings were mixed. Net debt was higher thanCredit Suisse modelled while Gold Coast earningssurpassed the broker’s forecasts. While the first halfwas costly, the broker believes good growth remainsintact. Costs are the main reason the brokerdowngrades forecasts for earnings per share by6%.Target is reduced to $5.90 from $6.25.

SIRTEX MEDICAL LIMITED (SRX) was

14Monday 26 February 2018

downgraded to Neutral from Buy by UBS. B/H/S:0/3/0. First half results were in line with UBSestimates. A soft top line was more than offset bysales force and R&D cost out. As previouslyannounced, Sirtex has entered into a bindingagreement with Varian Medical Systems for thecompany to acquire all of Sirtex’s shares for $28cash. UBS downgrades the stock to Neutral from Buyand moves the price target into line with the offerprice of $28.00.

WESTPAC BANKING CORPORATION (WBC) wasdowngraded to Equal-weight from Overweight byMorgan Stanley. B/H/S: 4/4/0. Morgan Stanley haslowered its target to $30.00 from $32.10. The brokerhas a negative stance on the major banks butprovides six reasons for its Westpac downgrade. Themargin sweet spot has ended, the capital intensity ofretail banking is increasing, there is growing scrutinyof conduct and competition, little scope for a costsurprise, no institutional tailwind this year and thestock is fully valued. The broker prefers ANZ Bank(ANZ), also Equal-weight, and has Underweightratings on the other two. Industry view: In Line

Earnings forecast

Listed below are the companies that have had theirforecast current year earnings raised or lowered bythe brokers last week. The qualification is that thestock must be covered by at least two brokers. Thetable shows the previous forecast on an earnings pershare basis, the new forecast, and the percentagechange.

The FNArena database tabulates the views of eightmajor Australian and international stock brokers: Citi,Credit Suisse, Deutsche Bank, Macquarie, MorganStanley, Morgans, Ord Minnett and UBS.

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regard to yourcircumstances.

15Monday 26 February 2018

Hot Stocks – Invocare and Citigroupby Staff Reporter

Likes

Michael McCarthy, chief market strategist at CMCmarkets has picked Invocare (IVC) for his like thisweek.

He says that despite a 37% lift in full year profit thestock is under pressure.

“Investors have reacted badly to management’s planto re-invest in the business. In the short term earningswill likely fall as facilities are taken off line forrefurbishment, but in my view this will further cementIVC’s leading position in its key markets.”

He says he is a ‘backfoot buyer’ between $13 and$14 for long-term value.

Our chartist Gary Stone from Share Wealth Systemslikes ComputerShare (CPU),

He says the 15-year chart (below) shows that there isa high probability that CPU is well entrenched in along-term uptrend that started a year ago when itbroke above $13 – a 7-year resistance zone – andout of a wide-ranging 10-year sideways consolidationmove that followed an eight-fold rise in price.

And looking overseas, Peter Wilmshurst, portfoliomanager at Templeton Global Growth Fund Ltd likesCitigroup (NYSE:C). He says it is now returning tohealth following a rough patch during the globalfinancial crisis.

“The bank went through a multi-year restructuringwhich included closing branches as well as exitingvarious businesses and countries. The stock has nowappreciated and is trading at a slight premium to bookvalue of $62/share,” he says.

“The management has a long-term goal of a returnon tangible equity of 16% from their pared down setof businesses. Should they deliver, the shares wouldbe on a single digit P/E ratio.”

Dislikes

Michael is not a fan of Woolworths. He says thatalthough the half year result strongly indicates aturnaround due to CEO Banducci’s plan, thevaluation looks stretched above $27.

“At around 20 times earnings he would need a magicwand to transform this stable earner to a growthstock. Additionally, the stock initially broke throughprevious resistance at $27.75, only to fall back

16Monday 26 February 2018

through after the announcement, a stronger technicalsell signal.”

Gary doesn’t like Ramsay Health Care (RHC).

“Ramsay’s share price is currently battling to breakthrough a resistance zone between $67.50 and $69,”he says.

“At this stage there is a higher probability of aretracement around the $60 mark than an advanceabove this resistance zone.”

And as for Peter Wilmshurst’s least favourite stockthis week, it’s another big international name –Colgate-Palmolive.

He says that although consumer staples have been amarket favourite, should interest rates rise, which hasbeen the trend so far in 2018, staples are likely tounderperform the market.

“Colgate-Palmolive is trading at 22 times 2018earnings but offering a yield of only 2.3%. Therevenue has shrunk 10% over the last five years withincreasing competition beating down the prices (morethan 2% in Americas and Europe). In summary, it’s astock with an expensive valuation and decliningbusiness,” he explains.

Important: This content has been prepared withouttaking account of the objectives, financial situation orneeds of any particular individual. It does notconstitute formal advice. Consider theappropriateness of the information in regard to yourcircumstances.

Powered by TCPDF (www.tcpdf.org)

17Monday 26 February 2018