mitchell johnson hearing demand regarding revocation of

TRANSCRIPT

Slttlo of Waehlngton ~ Office of lhe lrrlurance Commlsslonet ~ Ho~rlngs Uni

ilHW ollhbull PO Box 40755 IN5UllANCE Olympia WA 98504middot0255 ~~Mt~~JON~~ 5000 Capilol 13oulavmd

Tumwmer WA 08501 360) 725-7002 FAX (360) 664middot2782

bull

Demand for Hearing

FILEDHearingsUolcwe9ov

Please type or print in Ink Attach a copy of the Order or correspondence in dispL1te and all documents supportingl)i~r dJJWgt~P This Demand for Hearing can be mailed faxed hand-delivered or emailed to the Hearings Unit at the address above i 4 A fi 2 For OIC Demands please provide contact information for all other Interested parties and their representatives HE

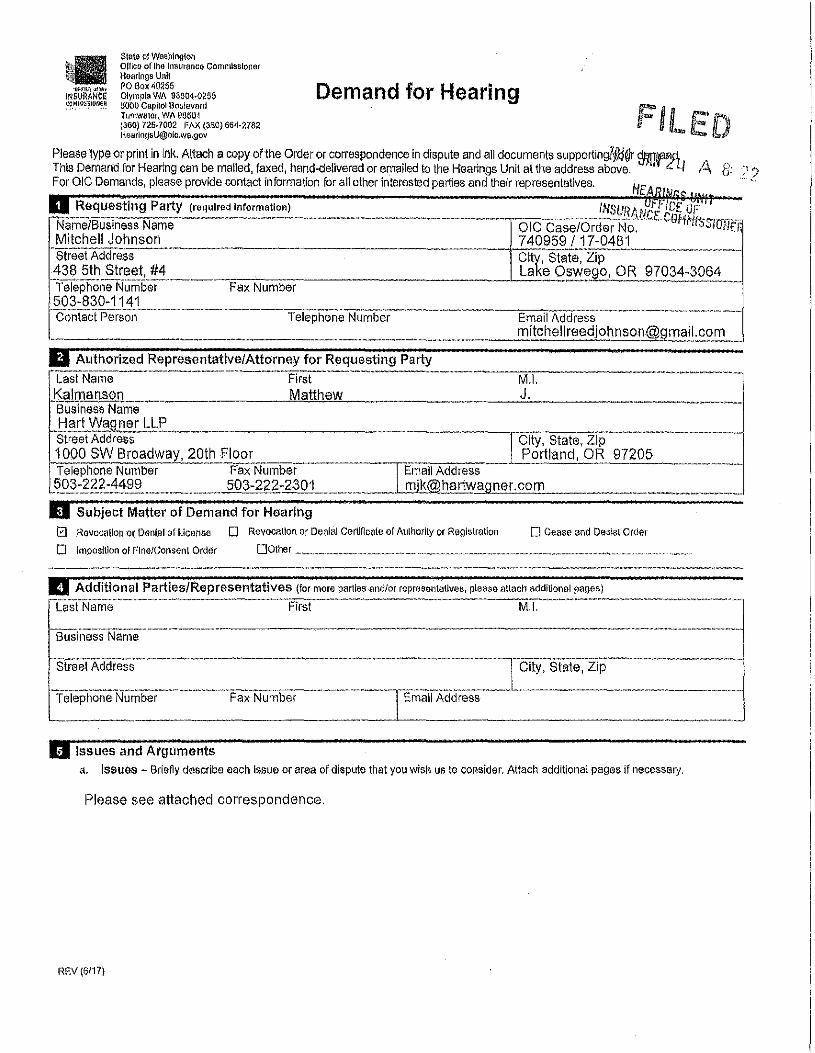

middotmiddotNae~~~~gN~Y lrbullqut~~deg~~~~~~~-- bull middotbullbullbullmiddot _____-----middot-- o1c caseOr~~f~~uc[o~s1011t1 Mitchell Johnson 7 40959 I 17-0481

middotmiddot~ffreit Addrassmiddot--- ____ c11y staiamiddot2rpmiddot~--- __ 438 5th Street 4 L~~C2~~lii~9R 972_34-3Q~-~ - shyfeTepiioneFmiddotfomiddotmber Fax Number middot-- shy503-830-1141-coniScfPerso1i ___ TelepiioneNumiler___________ Email Address middot--------- _ _____ _ mitchellreedjohnsongmailc_ltJ)2

II Authorized RepresentativeAttorney for Requesting Party LasfNamii__ ___Frrsi_ _ M1

Kalmanson Matthew JmiddotaUslnesSName---middot----- middot----=-----------______trade~tradetrade--_____~--

JrLYY~JlE LLP Street Address 1000 SW Broadway 20th Floocr~

Telephone Number Fax Number Email Address 5_D~11~~ 503-222-2301 ________ mk t1artwagnercom

II Subject Matter of Demand for Hearing 0 Revocation or Denial of Ucense D Revocation or DenisI Cerllflc~1te of Authority or Registration 0 Cease and Deslsl Order

D Imposition or FineConsent Order OOther -middotmiddotmiddotmiddotmiddotmiddot-middot------middot---------middotmiddotmiddot _ middot--~-~middot---middotmiddot ------------------middot-middotmiddotmiddot-middot--middot--middotmiddot--------middot----middot-----middot---shy

Additional PartiesRepresentatives for more parties andor representatives please attach additional pages)

sff8ei7ddress ---middot middotmiddot - -- -middot JciiYmiddotsiaie~-2~------

TeiePiiOrimiddote-NurnSer-middot middot-i=xmiddotNumber --middotmiddot-middot-middot-rrmiddotaffAciciress_ middotmiddotmiddotmiddotmiddot--------middot==~~~ II Issues and Arguments

a Issues - Briefly describe each Issue or area of dispute that you wish us to consider Attach additional pages if necessary

Please see attached correspondence

HGV (6111)

b Arguments - Explain why each Issue or area of dispute listed above should be decided in your favor Attach additional pages if necessary To the extent known cite applicable rules statutes or cases in support of your arguments Enclose copies of documents concerning your arguments including documents the Department previously requested from you that you have not yet provided

Please see attached correspondence

d Signature

Either the Requesting Party or the AttorneyRepresentative can sign this Demand for Hearing However If the Representative Is submitting the Demand contact Information for the Requesting Party lllYlll be provided under Section 1 above and the AttorneyRepresentatives contact Information must be provided In Section 2

Requesting Party

Signature Date

Name (please print or type) Title

~~---------- --~~JL Signature Matthew J Kalmanson Attorney---middot-------middotmiddot----- Name (please print or type) Title

REV (6117)

HART WAGNER

TRIAL ATTORNEYS

Matthew J Kalmanson Twentieth Floor

mjkhartwagnercom Admitted in Oregon New York and Washington

IOOO SW Broadway Portland Oregon 97205

Telephone (503) 222-4499 Fax (503) 222-230 I

January 24 2018

Via Email and US Mail

Mike Kreidler Insurance Commissioner State of Washington Office of the Insurance Commissioner Hearings Unit POBox40255 Olympia WA 98504-0255 HearingsUoicwagov

Re In the Matter aMitchell Johnson WAOIC No 740959 NPN7562935 Order No 17-0481 Our File No 28236

Dear Commissioner

Licensee Mitchell Johnson hereby exercises his right to demand a hearing on the Commissioners Order Because this request is being made before the effective date of the Order the penalty revoking his license must be stayed

Below are the answers to sections 5(a) and 5(b) of the attached Demand for Hearing form I also attach a copy of the underlying Order Revoking License

Answer to S(a)

Mr Johnson challenges the facts described in the Commissioners Order as well as the legal conclusions that the Commissioner draws from those facts Among other things Mr Johnson disputes that

bull he engaged in twisting he misrepresented the terms and benefits of the two annuities at issue or he sold the Consumers unsuitable annuities

bull he misrepresented to Consumers the terms of the ING annuity

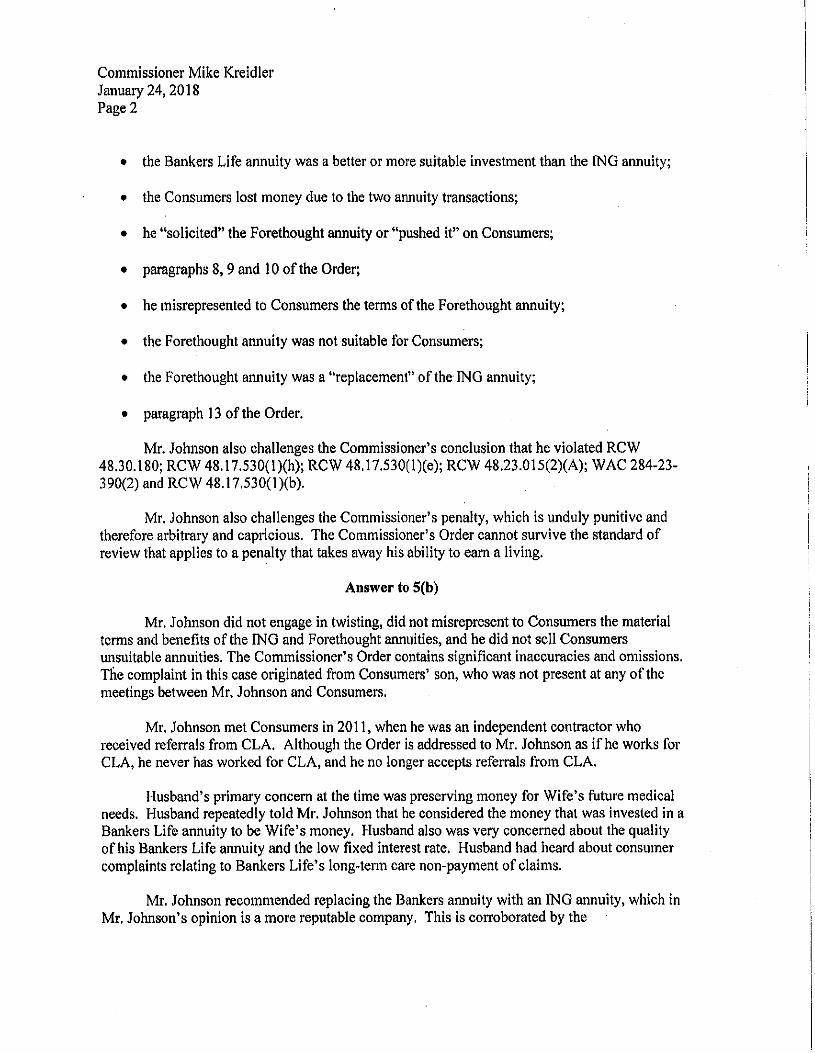

Commissioner Mike Kreidler January 24 2018 Page 2

bull the Bankers Life annuity was a better or more suitable investment than the ING annuity

bull the Consumers lost money due to the two annuity transactions

bull he solicited the Forethought annuity or pushed it on Consumers

bull paragraphs 8 9 and I 0 of the Order

bull he misrepresented to Consumers the terms of the Forethought annuity

bull the Forethought annuity was not suitable for Consumers

bull the Forethought annuity was a replacement of the ING annuity

bull paragraph 13 of the Order

Mr Johnson also challenges the Commissioners conclusion that he violated RCW 4830180 RCW 48 l 7530(1)(h) RCW 48 I7530(1)(e) RCW 4823015(2)(A) WAC 284-23shy390(2) and RCW 4817530(l)(b)

Mr Johnson also challenges the Commissioners penalty which is unduly punitive and therefore arbitrary and capricious The Commissioners Order cannot survive the standard of review that applies to a penalty that takes away his ability to earn a living

Answer to 5(b)

Mr Johnson did not engage in twisting did not misrepresent to Consumers the material terms and benefits of the ING and Forethought annuities and he did not sell Consumers unsuitable annuities The Commissioners Order contains significant inaccuracies and omissions The complaint in this case originated from Consumers son who was not present at any of the meetings between Mr Johnson and Consumers

Mr Johnson met Consumers in 2011 when he was an independent contractor who received referrals from CLA Although the Order is addressed to Mr Johnson as if he works for CLA he never has worked for CLA and he no longer accepts referrals from CLA

Husbands primary concern at the time was preserving money for Wifes future medical needs Husband repeatedly told Mr Johnson that he considered the money that was invested in a Bankers Life annuity to be Wifes money Husband also was very concerned about the quality of his Bankers Life annuity and the low fixed interest rate Husband had heard about consumer complaints relating to Bankers Lifes long-term care non-payment of claims

Mr Johnson recommended replacing the Bankers annuity with an ING annuity which in Mr Johnsons opinion is a more reputable company This is corroborated by the

Commissioner Mike Kreidler January 24 2018 Page 3

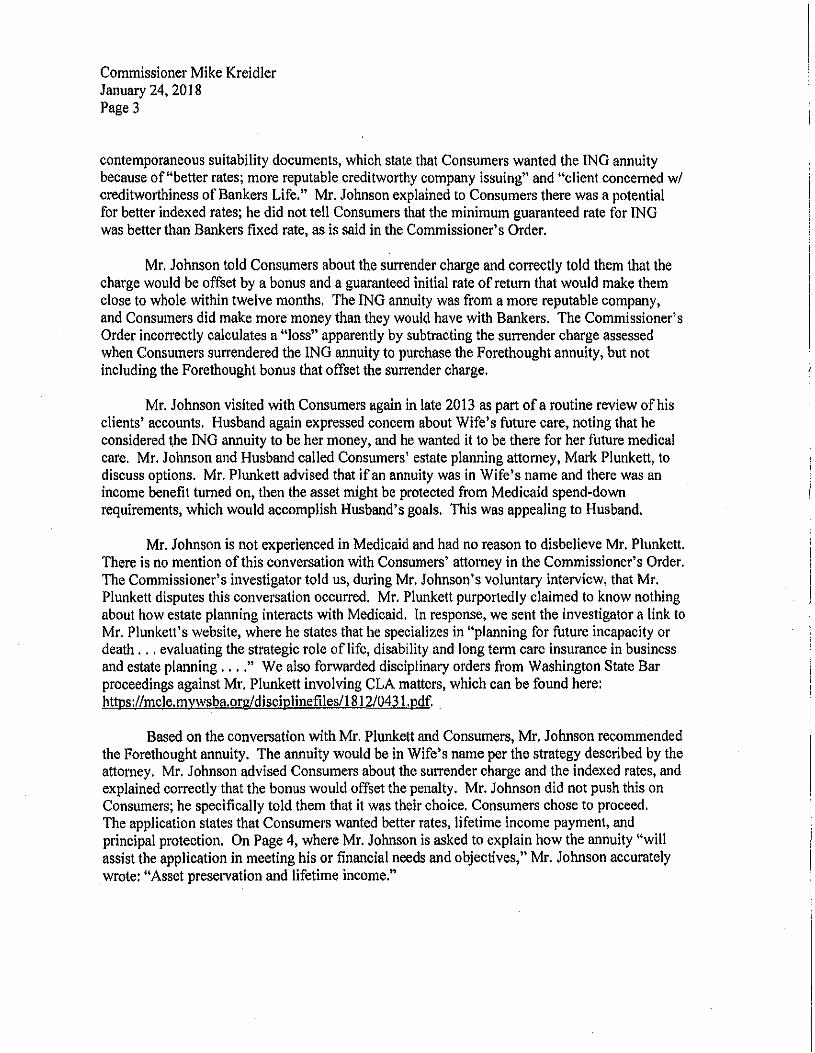

contemporaneous suitability documents which state that Consumers wanted the ING annuity because ofbetter rates more reputable creditworthy company issuing and client concerned w creditworthiness of Bankers Life Mr Johnson explained to Consumers there was a potential for better indexed rates he did not tell Consumers that the minimum guaranteed rate for ING was better than Bankers fixed rate as is said in the Commissioners Order

Mr Johnson told Consumers about the surrender charge and correctly told them that the charge would be offset by a bonus and a guaranteed initial rate of return that would make them close to whole within twelve months The ING annuity was from a more reputable company and Consumers did make more money than they would have with Bankers The Commissioners Order incorrectly calculates a loss apparently by subtracting the surrender charge assessed when Consumers surrendered the ING annuity to purchase the Forethought annuity but not including the Forethought bonus that offset the surrender charge

Mr Johnson visited with Consumers again in late 2013 as part of a routine review of his clients accounts Husband again expressed concern about Wifes future care noting that he considered he ING annuity to be her money and he wanted it to be there for her future medical care Mr Johnson and Husband called Consumers estate planning attorney Mark Plunkett to discuss options Mr Plunkett advised that ifan annuity was in Wifes name and there was an income benefit turned on then the asset might be protected from Medicaid spend-down requirements which would accomplish Husbands goals This was appealing to Husband

Mr Johnson is not experienced in Medicaid and had no reason to disbelieve Mr Plunkett There is no mention of this conversation with Consumers attorney in the Commissioners Order The Commissioners investigator told us during Mr Johnsons voluntary interview that Mr Plunkett disputes this conversation occurred Mr Plunkett purportedly claimed to know nothing about how estate planning interacts with Medicaid In response we sent the investigator a link to Mr Plunketts website where he states that he specializes in planning for future incapacity or death evaluating the strategic role of life disability and long term care insurance in business and estate planning We also forwarded disciplinary orders from Washington State Bar proceedings against Mr Plunkett involving CLA matters which can be found here httpslmclemywsbaorgdisciplinefiles18120431pdf

Based on the conversation with Mr Plunkett and Consumers Mr Johnson recommended the Forethought annuity The annuity would be in Wifes name per the strategy described by the attorney Mr Johnson advised Consumers about the surrender charge and the indexed rates and explained correctly that the bonus would offset the penalty Mr Johnson did not push this on Consumers he specifically told them that it was their choice Consumers chose to proceed The application states that Consumers wanted better rates lifetime income payment and principal protection On Page 4 where Mr Johnson is asked to explain how the annuity will assist the application in meeting his or financial needs and objectives Mr Johnson accurately wrote Asset preservation and lifetime income

Commissioner Mike Kreidler January 24 2018 Page 4

Because the annuity was going from Consumers to Wife individually Mr Johnson did not consider it a replacement Because Mr Johnson disclosed source of funds Forethought requested suitability replacement comparison information Mr Johnson provided the information The Order focuses on information in that form about minimum fixed rates but Consumers wanted the Forethought annuity based on the income rider and the index interestmiddot crediting methods

Mr Johnson reminded Consumers to turn on the income benefit rider several times but they did not do it He also tried to engage Consumers children in the planning process without success Mr Johnsons understanding ofwhHt happened next is that Wiles health took a turn for the worse and she entered assisted living For some reason Forethought denied the request for accelerated access to funds After that occurred and contrary to Mr Johnsons advice Consumers surrendered the Forethought annuity which led to the penalty

Mr Johnson does not believe these facts constitute twisting There may be some innocent misstateinents on the supplemental replacement form sent to Forethought about minimum fixed rates (we are continuing to investigate this issue) but this does not justify the draconian penalty Mr Johnson did not misrepresent the benefits of the mmuity to Consumers did not engage in twisting and the annuity was not unsuitable Nor did Mr Johnson believe tht1t the Forethought annuity was a replacement because the ING annuity was voluntarily surrendered by Husband and placed in an aanuity in Wifes name per the attorneys instructions Mr Johnson also earned somewhere between 23middot25 commission on these sales not the 38 stated in the Order

The penalty of revocation of his license is unduly punitive under the circumstances There is not clear and convincing evidence that Mr Johnson engaged in the conduct described in the Order Mr Johnson did what he believed was in the best interest of Consumers based on the information he received from them and their attorney Mr Johnson has worked in this industry for 35 years and strives to act in the best interests of his customers As far as he knows this is the first complaint he has received from a customer (he once received a complaint from a competitor which led to a consent order) He did his best to look out for Consumers best interests and comply with their wishes and the advice of their attorney He did not cause them to lose money as lJusbands son believed He feels terribly that things became difficult financially before Wifes death but it was not the result of Mr Johnsons conduct Revocation of his ability to earn a living is not warranted under these facts

Respectfully

Matthew J Kalmanson MJKfrh Enclosures

STATE OF WASHINGTON OFFICE OF THE INSURANCE COMMISSIONER

In The Matter of

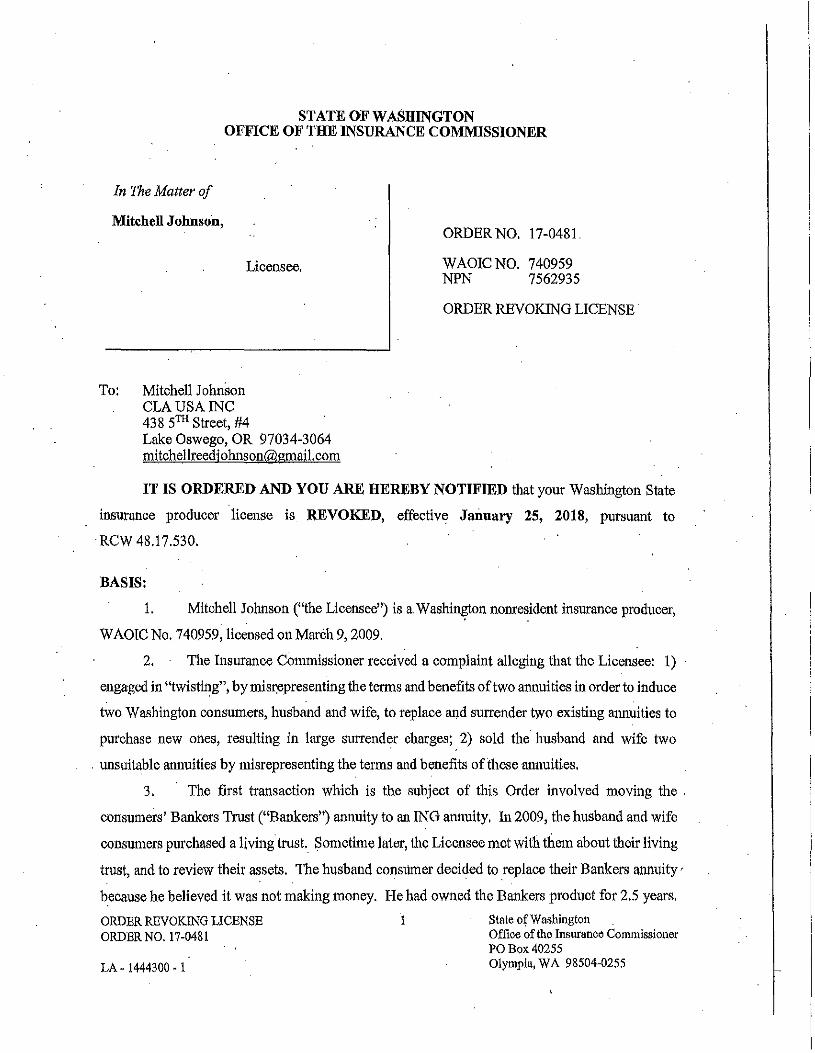

Mitchell Johnson ORDER NO 17-0481

Licensee WAOICNO NPN

740959 7562935

ORDER REVOKING LICENSE

To Mitchell Johnson CLA USA INC 438 5TH Street 4 Lake Oswego OR 97034-3064 mitchellreediohnsonrunailcom

IT IS ORDERED AND YOU ARE HEREBY NOTIFIED that your Washington State

insurance producer license is REVOKED effectivf January 25 2018 pursuant to

RCW 4817530

BASIS

1 Mitchell Johnson (the Licensee) is a Washington nonresident insurance producer

WAOIC No 740959 licensed on March 9 2009

2 The Insurance Commissioner received a complaint alleging that the Licensee 1)

engaged in twisting by misrepresenting the terms and benefits of two annuities in order to induce

two Washington consumers husband and wife to replace and surrender two existing annuities to

purchase new ones resulting in large surrender charges 2) sold the husband and wife two

unsuitable annuities by misrepresenting the terms and benefits of these annuities

3 The first transaction which is the subject of this Order involved moving the

consumers Bankers Trust (Bankers) annuity to an ING annuity In 2009 the husband and wife

consumers purchased a living trust Sometime later the Licensee met with them about their living

trust and to review their assets The husband consumer decided to replace their Bankers anm1ity bull

because he believed it was not making money He had owned the Bankers product for 25 years

ORDER REVOKING LICENSE 1 State of Washington ORDER NO 17-0481 Office of the Insurance Commissioner

P0Box40255 LA- 1444300 - 1 Olympia WA 98504-0255

The Licensee offered to move him to amiddotnew annuity with ING (aka VOYA) The Licensee told

him the ING annuity offered better rates than the Bankers annuity The Licensee told him about

a surrender penalty but assured himicroi the ING annuity would cover the loss The consumer incurred

a $526522 surrender fee and purchased the ING annuity on November 11 2011 funding it

entirely with the Bankers product

4 Factoring in the initial 3 interest bonus the ING policy earned a total of$623938

from inception until the consumer surrendered it on November 22 2013 an average interest gain

of66 over two (2) years When the ING annuity was cashed fee was

charged After factoring in the surrender penalty the consumer lost $60038 on this annuity

5 The ING annuity (an indexed annuity) offered a substantially lower guaranteed

minimum interest rate (contrary to the Licensees repres~ntations in the suitability paperwork) than

the Bankers product (a fixed annuity) The consumer surrendered the annuity after only thirty (30)

months incurring a substantial surrender charge In addition the ING annuitys initial interest

bonus was less than the Bankers surrender charge

6 The Licensee misrepresented to the consumer and ING the insurer that the fixed

interest rates on the ING product were better than the Bankers annuity thereby inducing the

consumer to replace the Bankers product with the ING annuity Moreover the Licensee denied in

an interview with Investigations that he had referred to fixed rates and middotclaimed he had been

referring to the potential for better indexed rates middotHowever in the suitability paperwork and in his

initial response to the Insurance Co1mnissioner the Licensee specifically mentioned fixed rates

out a $683976 surrender

7 The second transaction which is the subject of this Order involved moving the

consumers ING annuity to a Forethought Life Insurance Company (Forethought) annuity The

husband consumer had only had the ING annuity for about twenty-six (26) months when the

Licensee came to their house and solicited a Forethought annuity The consumer had never

approached the Licensee about it The Licensee said Ive got a better deal for you that would

make them more money Th~consumer explained that the Licens~e pushed it on me

8 However the Licensee realized the husband consumer was too old to purchase the

annuity and determined to put it in your wifes name The Licensee explained the plan was for

them to replace the ING annuity with the Forethought annuity

9 The husband consumer informed the Insurance Commissioner that the only reason

he proceeded with the Foreihought annuity was the Licensee told us the Forethought annuity ORDER REVOKING LICENSE 2 State ofWashington ORDER NO 17-0481 Office of the Insurance Commissioner

PO Box 40255 LA- 1444300 - I Olympia WA 98504-0255

would make more money because of the supposed better rate of return The Licensee told

Forethought however that the consumers surrendered the ING annuity because of poor

perfonnance The ING annuity 1Jamed $623988 in twenty-four (24) months and was not

suffering from poor perfonnance middotIt might have continued to perfonn well but the Licensee

recommended the consumer surrender it which made himincur a $683976 s~rrender fee an

amount larger than his interest gains

10 Forethought infonned the Insurance Commissioner that the Licensee did not

disclose the source of the lump sum $88157 payment in the initial application paperwork while

also declaring the purchase was not replacing another annuity

11 At Forethoughts request the Licensee submitted supplementary suitability

documents which compared the now-surrendered ING annuity with the proposed Forethought

annuity In these documents the Licensee incorrectly wrote the ING annuity had a 10

guaranteed minimum interest rate its actual minimum guaranteed rate for the fixed strategy was

15 In addition he also misrepresented that the guaranteed minimum interest rate on the

Forethought annuity was 25 This is incorrect it was 225 for the fixed strategy only for the

first year thereafter it would be 050 He also wrote there were no disadvantages for his client

to select the Forethought annuity The Licensee stated to the Insurance Commissioners

investigator that he did not know why he wrote the incorrect guaranteed minimum interest rates

on the annuity comparison in the Forethought suitability documents

12 On April 20 2015 the husband consumer surrendered his wifes Forethought

annuity to assist with m1foreseen nursing home costs The annuitys value was $8766175 at the

time of surrender meaning it lost $49525

13 The Licensee earned a total of $672245 in commissionsfrom the sale of the ING

and Forethought annuities

14 RCW 4830180 states twisting is prohibited No persop shall by

misrepresentations or by misleading comparisons induce or tend to induce any insured to lapse

tenninate forfeit surrender retain or convert any insurance policy

15 RCW 48 l 7530(l)(h) allows the Insurance Commissioner to place on probation

suspend revoke or refuse to issue or renew an insurance producers license for using fraudulent

coercive or dishonest practices or demonstrating incompetence untrustworthiness or financial

irresponsibility in this state or elsewhere ORDER REVOKING LICENSE 3 State of Washington

ORDER NO 170481 Office of the Insurance Collllllissioner PO Box40255

LA- 1444300 - I Olympia WA 98504-0255

16 RCW 48l 7530(1)(e) allows the Insurance Commissioner to place on probation

suspend revoke orrefuse to issue or renew an insurance producers license for intentionally

misrepresenting the terms of an actual or proposed insurance contract or application for insurance

17 RCW 4823015(2)(a) provides in recommending the purchase of an annuity or the

exchange of an annuity that results in another insurance transaction or series of insurance

transactions to a consumer the insurance producer must have reasonable grounds for believing

that the recommendation is suitable for the consumer on the basis of the facts disclosed by the

consumer about their investments and other insurance products and as to their financial situation

and needs

18 WAC 284-23-390(2) provides that in addition to the requirements in RCW

4823015 insurance middotproducers must havemiddot reasonable grounds to believe the following

requirements in recommending and executing a purchase or exchange of an annuity

(a) The consumer has beeri reasonably informed of various features of the annuity such as the potential surrender period and surrender charge potential tax penalty if the consumer sells exchanges surrenders or annuitizes the annuity mortality and expense fees investment advisory fees potential charges for and features of riders limitations on interest returns insurance and investment components and market risk

(b) The consumer would benefit from certain features of the annuity such as tax deferred growth annuitization or death or living benefit

(c) The particular annuity as a whole the underlying subaccounts to which funds are allocated at the time of purchase or exchange of the annuity and riders and similar product enhancements if any are suitable (and in the case of an exchange or replacement the transaction as a whole is suitable) for the particular consumer based on his or her suitability information and

(d) In the case of an exchange or replacement of an annuity the exchange or replacement is suitable including taking into consideration whether middot

(i) The consumer will incur a surrender charge be subject to the commencement of a new surrender period lose existing benefits (such as death living or other contractual benefits) or be subject to increased fees investment advisory fees or charges for riders and similar product enhancements

(ii) The consumer would benefit from product enhancements and improvements and (iii) The consumer has had another annuity exchange or replacement and in particular an

exchange or replacement within the preceding thirty-six months

middot19 RCW 4817530(1)(b) allows the Insurance Commissioner to place on probation

suspend revoke or refuse to issue or renew an insurance producers license for violating any

insurance laws or violating any rule subpoena or order of the Insurance Commissioner or of

another states insurance commissioner

ORDER REVOKING LICENSE 4 State of Washington ORDER NO 17-0481 Office of the lnsura~ce Commissioner

POBox40255

LA- 1444300 - I Olympia WA 98504-0255

20 RCW 4817 560 provides after hearing or upon stipulation by the licensee and in

addition to or in lieu of the suspension revocation or refusal to renew any such license the

Insurance Commissioner may levy a fine upon the licensee in an amount not more than one

thousand dollars

21 The Licensee engaged in twisting by misrepresenting the terms and benefits of

amrnities in order to induce two (2) consumers to replace and surrender existing ammities to

purchase new ones The Licensee also sold the consumers unsuitable annuities through

misrepresentation of the terms and benefits of the annuities These actions constitute violations of

RCW 4830180 RCW 4817530(l)(h) RCW 48l 7530(1)(e) RCW 4823015(2)(a) WAC 284shy

23-390(2) and RCW 4817530(1)(b) justifying the revocation ofhis license

ENTERED at Tumwater Washington this 2018

MIKE KREIDLER Insurance Commissioner

Insurance Enforcement Specialist Legal Affairs Division

ORDER REVOKING LICENSE 5 State of Washington

ORDER NO 17-0481 Office of the Insurance Connnissioner PO Box 40255

LA - 1444300 - 1 Olympia WA 98504-0255

NOTICE OF YOUR RIGHT TO A HEARING

If you are aggrieved by this Order Revoking License you may demand a hearing in

accordance with RCW 480401 O WAC 284-02-070 and WAC 10-08-110 Generally a hearing

demand must be in writing and received within ninety (90) days after the date of this Order

Revoking License which is the day it was mailed to you or you will waive your right to a

hearing

Ifthe Insurance Commissioner receives your demandfor a hearing before the effective

date listed on the order revoking your license the revocation will be automatically stayed

(postponed) and your license will remain in effect pending the hearing

You may fill out a demand for hearing fonn online at the following location httpswwwinsurancewagovhow-file-demand-hearing

Alternatively if you choose to file by mail your demand for hearing must briefly state

how you are harmed by this decision and why you disagree with it along with contact

infonnation (phone number mailing address e-mail address etc) for yourself and any

representative that appears on your behalf The demand may be sent to the following address

Hearings ()nit Office of the Insurance Commissioner P0Box40255 Olympia WA 98504-0255

You will be notified of the time and place of your hearing If you have questions about

filing a demand for hearing or the hearing process please telephone the Hearings Unit at (360)

725-7002 or send an email to HellringsUoicwagov

ORDER REVOKJNG LICENSE 6 State of Washington ORDER NO 17-0481 Office of the Insurance Commissioner

PO Box 40255

LA- 1444300 - 1 Olympia WA 98504-0255

CERTIFICATE OF MAILING

The tmdersigned certifies under the penalty of pe1jury under the laws of the state of

Washington that I am now and at all times herein mentioned a citizen of the United States a

resident of the state of Washington over the age of eighteen years not a party to or interested in

the above-entitled action and competent to be a witness herein

On the date given below I caused to be served the foregoing Order Revoking License on

the following individual by email and by depositing in the US mail via state Consolidated Mail

Service with proper postage affixed

Mitchell Johnson CLA USA INC 43 8 5TH Street 4 Lake Oswego OR 97034-3064 mitchcllreecjohnsongmailcom

Dated this__~__~--- day of 0w1~j- 2018 in Tumwater Washington

IP~ OS PACE

Legal Assistant Legal Affairs Division

ORDER REVOKING LICENSE 7 State of Washington

ORDER NO 17-0481 Office of the Insurance Co1n1nissioner PO Box40255

LA- 1444300 - I Olympia WA 98504-0255

b Arguments - Explain why each Issue or area of dispute listed above should be decided in your favor Attach additional pages if necessary To the extent known cite applicable rules statutes or cases in support of your arguments Enclose copies of documents concerning your arguments including documents the Department previously requested from you that you have not yet provided

Please see attached correspondence

d Signature

Either the Requesting Party or the AttorneyRepresentative can sign this Demand for Hearing However If the Representative Is submitting the Demand contact Information for the Requesting Party lllYlll be provided under Section 1 above and the AttorneyRepresentatives contact Information must be provided In Section 2

Requesting Party

Signature Date

Name (please print or type) Title

~~---------- --~~JL Signature Matthew J Kalmanson Attorney---middot-------middotmiddot----- Name (please print or type) Title

REV (6117)

HART WAGNER

TRIAL ATTORNEYS

Matthew J Kalmanson Twentieth Floor

mjkhartwagnercom Admitted in Oregon New York and Washington

IOOO SW Broadway Portland Oregon 97205

Telephone (503) 222-4499 Fax (503) 222-230 I

January 24 2018

Via Email and US Mail

Mike Kreidler Insurance Commissioner State of Washington Office of the Insurance Commissioner Hearings Unit POBox40255 Olympia WA 98504-0255 HearingsUoicwagov

Re In the Matter aMitchell Johnson WAOIC No 740959 NPN7562935 Order No 17-0481 Our File No 28236

Dear Commissioner

Licensee Mitchell Johnson hereby exercises his right to demand a hearing on the Commissioners Order Because this request is being made before the effective date of the Order the penalty revoking his license must be stayed

Below are the answers to sections 5(a) and 5(b) of the attached Demand for Hearing form I also attach a copy of the underlying Order Revoking License

Answer to S(a)

Mr Johnson challenges the facts described in the Commissioners Order as well as the legal conclusions that the Commissioner draws from those facts Among other things Mr Johnson disputes that

bull he engaged in twisting he misrepresented the terms and benefits of the two annuities at issue or he sold the Consumers unsuitable annuities

bull he misrepresented to Consumers the terms of the ING annuity

Commissioner Mike Kreidler January 24 2018 Page 2

bull the Bankers Life annuity was a better or more suitable investment than the ING annuity

bull the Consumers lost money due to the two annuity transactions

bull he solicited the Forethought annuity or pushed it on Consumers

bull paragraphs 8 9 and I 0 of the Order

bull he misrepresented to Consumers the terms of the Forethought annuity

bull the Forethought annuity was not suitable for Consumers

bull the Forethought annuity was a replacement of the ING annuity

bull paragraph 13 of the Order

Mr Johnson also challenges the Commissioners conclusion that he violated RCW 4830180 RCW 48 l 7530(1)(h) RCW 48 I7530(1)(e) RCW 4823015(2)(A) WAC 284-23shy390(2) and RCW 4817530(l)(b)

Mr Johnson also challenges the Commissioners penalty which is unduly punitive and therefore arbitrary and capricious The Commissioners Order cannot survive the standard of review that applies to a penalty that takes away his ability to earn a living

Answer to 5(b)

Mr Johnson did not engage in twisting did not misrepresent to Consumers the material terms and benefits of the ING and Forethought annuities and he did not sell Consumers unsuitable annuities The Commissioners Order contains significant inaccuracies and omissions The complaint in this case originated from Consumers son who was not present at any of the meetings between Mr Johnson and Consumers

Mr Johnson met Consumers in 2011 when he was an independent contractor who received referrals from CLA Although the Order is addressed to Mr Johnson as if he works for CLA he never has worked for CLA and he no longer accepts referrals from CLA

Husbands primary concern at the time was preserving money for Wifes future medical needs Husband repeatedly told Mr Johnson that he considered the money that was invested in a Bankers Life annuity to be Wifes money Husband also was very concerned about the quality of his Bankers Life annuity and the low fixed interest rate Husband had heard about consumer complaints relating to Bankers Lifes long-term care non-payment of claims

Mr Johnson recommended replacing the Bankers annuity with an ING annuity which in Mr Johnsons opinion is a more reputable company This is corroborated by the

Commissioner Mike Kreidler January 24 2018 Page 3

contemporaneous suitability documents which state that Consumers wanted the ING annuity because ofbetter rates more reputable creditworthy company issuing and client concerned w creditworthiness of Bankers Life Mr Johnson explained to Consumers there was a potential for better indexed rates he did not tell Consumers that the minimum guaranteed rate for ING was better than Bankers fixed rate as is said in the Commissioners Order

Mr Johnson told Consumers about the surrender charge and correctly told them that the charge would be offset by a bonus and a guaranteed initial rate of return that would make them close to whole within twelve months The ING annuity was from a more reputable company and Consumers did make more money than they would have with Bankers The Commissioners Order incorrectly calculates a loss apparently by subtracting the surrender charge assessed when Consumers surrendered the ING annuity to purchase the Forethought annuity but not including the Forethought bonus that offset the surrender charge

Mr Johnson visited with Consumers again in late 2013 as part of a routine review of his clients accounts Husband again expressed concern about Wifes future care noting that he considered he ING annuity to be her money and he wanted it to be there for her future medical care Mr Johnson and Husband called Consumers estate planning attorney Mark Plunkett to discuss options Mr Plunkett advised that ifan annuity was in Wifes name and there was an income benefit turned on then the asset might be protected from Medicaid spend-down requirements which would accomplish Husbands goals This was appealing to Husband

Mr Johnson is not experienced in Medicaid and had no reason to disbelieve Mr Plunkett There is no mention of this conversation with Consumers attorney in the Commissioners Order The Commissioners investigator told us during Mr Johnsons voluntary interview that Mr Plunkett disputes this conversation occurred Mr Plunkett purportedly claimed to know nothing about how estate planning interacts with Medicaid In response we sent the investigator a link to Mr Plunketts website where he states that he specializes in planning for future incapacity or death evaluating the strategic role of life disability and long term care insurance in business and estate planning We also forwarded disciplinary orders from Washington State Bar proceedings against Mr Plunkett involving CLA matters which can be found here httpslmclemywsbaorgdisciplinefiles18120431pdf

Based on the conversation with Mr Plunkett and Consumers Mr Johnson recommended the Forethought annuity The annuity would be in Wifes name per the strategy described by the attorney Mr Johnson advised Consumers about the surrender charge and the indexed rates and explained correctly that the bonus would offset the penalty Mr Johnson did not push this on Consumers he specifically told them that it was their choice Consumers chose to proceed The application states that Consumers wanted better rates lifetime income payment and principal protection On Page 4 where Mr Johnson is asked to explain how the annuity will assist the application in meeting his or financial needs and objectives Mr Johnson accurately wrote Asset preservation and lifetime income

Commissioner Mike Kreidler January 24 2018 Page 4

Because the annuity was going from Consumers to Wife individually Mr Johnson did not consider it a replacement Because Mr Johnson disclosed source of funds Forethought requested suitability replacement comparison information Mr Johnson provided the information The Order focuses on information in that form about minimum fixed rates but Consumers wanted the Forethought annuity based on the income rider and the index interestmiddot crediting methods

Mr Johnson reminded Consumers to turn on the income benefit rider several times but they did not do it He also tried to engage Consumers children in the planning process without success Mr Johnsons understanding ofwhHt happened next is that Wiles health took a turn for the worse and she entered assisted living For some reason Forethought denied the request for accelerated access to funds After that occurred and contrary to Mr Johnsons advice Consumers surrendered the Forethought annuity which led to the penalty

Mr Johnson does not believe these facts constitute twisting There may be some innocent misstateinents on the supplemental replacement form sent to Forethought about minimum fixed rates (we are continuing to investigate this issue) but this does not justify the draconian penalty Mr Johnson did not misrepresent the benefits of the mmuity to Consumers did not engage in twisting and the annuity was not unsuitable Nor did Mr Johnson believe tht1t the Forethought annuity was a replacement because the ING annuity was voluntarily surrendered by Husband and placed in an aanuity in Wifes name per the attorneys instructions Mr Johnson also earned somewhere between 23middot25 commission on these sales not the 38 stated in the Order

The penalty of revocation of his license is unduly punitive under the circumstances There is not clear and convincing evidence that Mr Johnson engaged in the conduct described in the Order Mr Johnson did what he believed was in the best interest of Consumers based on the information he received from them and their attorney Mr Johnson has worked in this industry for 35 years and strives to act in the best interests of his customers As far as he knows this is the first complaint he has received from a customer (he once received a complaint from a competitor which led to a consent order) He did his best to look out for Consumers best interests and comply with their wishes and the advice of their attorney He did not cause them to lose money as lJusbands son believed He feels terribly that things became difficult financially before Wifes death but it was not the result of Mr Johnsons conduct Revocation of his ability to earn a living is not warranted under these facts

Respectfully

Matthew J Kalmanson MJKfrh Enclosures

STATE OF WASHINGTON OFFICE OF THE INSURANCE COMMISSIONER

In The Matter of

Mitchell Johnson ORDER NO 17-0481

Licensee WAOICNO NPN

740959 7562935

ORDER REVOKING LICENSE

To Mitchell Johnson CLA USA INC 438 5TH Street 4 Lake Oswego OR 97034-3064 mitchellreediohnsonrunailcom

IT IS ORDERED AND YOU ARE HEREBY NOTIFIED that your Washington State

insurance producer license is REVOKED effectivf January 25 2018 pursuant to

RCW 4817530

BASIS

1 Mitchell Johnson (the Licensee) is a Washington nonresident insurance producer

WAOIC No 740959 licensed on March 9 2009

2 The Insurance Commissioner received a complaint alleging that the Licensee 1)

engaged in twisting by misrepresenting the terms and benefits of two annuities in order to induce

two Washington consumers husband and wife to replace and surrender two existing annuities to

purchase new ones resulting in large surrender charges 2) sold the husband and wife two

unsuitable annuities by misrepresenting the terms and benefits of these annuities

3 The first transaction which is the subject of this Order involved moving the

consumers Bankers Trust (Bankers) annuity to an ING annuity In 2009 the husband and wife

consumers purchased a living trust Sometime later the Licensee met with them about their living

trust and to review their assets The husband consumer decided to replace their Bankers anm1ity bull

because he believed it was not making money He had owned the Bankers product for 25 years

ORDER REVOKING LICENSE 1 State of Washington ORDER NO 17-0481 Office of the Insurance Commissioner

P0Box40255 LA- 1444300 - 1 Olympia WA 98504-0255

The Licensee offered to move him to amiddotnew annuity with ING (aka VOYA) The Licensee told

him the ING annuity offered better rates than the Bankers annuity The Licensee told him about

a surrender penalty but assured himicroi the ING annuity would cover the loss The consumer incurred

a $526522 surrender fee and purchased the ING annuity on November 11 2011 funding it

entirely with the Bankers product

4 Factoring in the initial 3 interest bonus the ING policy earned a total of$623938

from inception until the consumer surrendered it on November 22 2013 an average interest gain

of66 over two (2) years When the ING annuity was cashed fee was

charged After factoring in the surrender penalty the consumer lost $60038 on this annuity

5 The ING annuity (an indexed annuity) offered a substantially lower guaranteed

minimum interest rate (contrary to the Licensees repres~ntations in the suitability paperwork) than

the Bankers product (a fixed annuity) The consumer surrendered the annuity after only thirty (30)

months incurring a substantial surrender charge In addition the ING annuitys initial interest

bonus was less than the Bankers surrender charge

6 The Licensee misrepresented to the consumer and ING the insurer that the fixed

interest rates on the ING product were better than the Bankers annuity thereby inducing the

consumer to replace the Bankers product with the ING annuity Moreover the Licensee denied in

an interview with Investigations that he had referred to fixed rates and middotclaimed he had been

referring to the potential for better indexed rates middotHowever in the suitability paperwork and in his

initial response to the Insurance Co1mnissioner the Licensee specifically mentioned fixed rates

out a $683976 surrender

7 The second transaction which is the subject of this Order involved moving the

consumers ING annuity to a Forethought Life Insurance Company (Forethought) annuity The

husband consumer had only had the ING annuity for about twenty-six (26) months when the

Licensee came to their house and solicited a Forethought annuity The consumer had never

approached the Licensee about it The Licensee said Ive got a better deal for you that would

make them more money Th~consumer explained that the Licens~e pushed it on me

8 However the Licensee realized the husband consumer was too old to purchase the

annuity and determined to put it in your wifes name The Licensee explained the plan was for

them to replace the ING annuity with the Forethought annuity

9 The husband consumer informed the Insurance Commissioner that the only reason

he proceeded with the Foreihought annuity was the Licensee told us the Forethought annuity ORDER REVOKING LICENSE 2 State ofWashington ORDER NO 17-0481 Office of the Insurance Commissioner

PO Box 40255 LA- 1444300 - I Olympia WA 98504-0255

would make more money because of the supposed better rate of return The Licensee told

Forethought however that the consumers surrendered the ING annuity because of poor

perfonnance The ING annuity 1Jamed $623988 in twenty-four (24) months and was not

suffering from poor perfonnance middotIt might have continued to perfonn well but the Licensee

recommended the consumer surrender it which made himincur a $683976 s~rrender fee an

amount larger than his interest gains

10 Forethought infonned the Insurance Commissioner that the Licensee did not

disclose the source of the lump sum $88157 payment in the initial application paperwork while

also declaring the purchase was not replacing another annuity

11 At Forethoughts request the Licensee submitted supplementary suitability

documents which compared the now-surrendered ING annuity with the proposed Forethought

annuity In these documents the Licensee incorrectly wrote the ING annuity had a 10

guaranteed minimum interest rate its actual minimum guaranteed rate for the fixed strategy was

15 In addition he also misrepresented that the guaranteed minimum interest rate on the

Forethought annuity was 25 This is incorrect it was 225 for the fixed strategy only for the

first year thereafter it would be 050 He also wrote there were no disadvantages for his client

to select the Forethought annuity The Licensee stated to the Insurance Commissioners

investigator that he did not know why he wrote the incorrect guaranteed minimum interest rates

on the annuity comparison in the Forethought suitability documents

12 On April 20 2015 the husband consumer surrendered his wifes Forethought

annuity to assist with m1foreseen nursing home costs The annuitys value was $8766175 at the

time of surrender meaning it lost $49525

13 The Licensee earned a total of $672245 in commissionsfrom the sale of the ING

and Forethought annuities

14 RCW 4830180 states twisting is prohibited No persop shall by

misrepresentations or by misleading comparisons induce or tend to induce any insured to lapse

tenninate forfeit surrender retain or convert any insurance policy

15 RCW 48 l 7530(l)(h) allows the Insurance Commissioner to place on probation

suspend revoke or refuse to issue or renew an insurance producers license for using fraudulent

coercive or dishonest practices or demonstrating incompetence untrustworthiness or financial

irresponsibility in this state or elsewhere ORDER REVOKING LICENSE 3 State of Washington

ORDER NO 170481 Office of the Insurance Collllllissioner PO Box40255

LA- 1444300 - I Olympia WA 98504-0255

16 RCW 48l 7530(1)(e) allows the Insurance Commissioner to place on probation

suspend revoke orrefuse to issue or renew an insurance producers license for intentionally

misrepresenting the terms of an actual or proposed insurance contract or application for insurance

17 RCW 4823015(2)(a) provides in recommending the purchase of an annuity or the

exchange of an annuity that results in another insurance transaction or series of insurance

transactions to a consumer the insurance producer must have reasonable grounds for believing

that the recommendation is suitable for the consumer on the basis of the facts disclosed by the

consumer about their investments and other insurance products and as to their financial situation

and needs

18 WAC 284-23-390(2) provides that in addition to the requirements in RCW

4823015 insurance middotproducers must havemiddot reasonable grounds to believe the following

requirements in recommending and executing a purchase or exchange of an annuity

(a) The consumer has beeri reasonably informed of various features of the annuity such as the potential surrender period and surrender charge potential tax penalty if the consumer sells exchanges surrenders or annuitizes the annuity mortality and expense fees investment advisory fees potential charges for and features of riders limitations on interest returns insurance and investment components and market risk

(b) The consumer would benefit from certain features of the annuity such as tax deferred growth annuitization or death or living benefit

(c) The particular annuity as a whole the underlying subaccounts to which funds are allocated at the time of purchase or exchange of the annuity and riders and similar product enhancements if any are suitable (and in the case of an exchange or replacement the transaction as a whole is suitable) for the particular consumer based on his or her suitability information and

(d) In the case of an exchange or replacement of an annuity the exchange or replacement is suitable including taking into consideration whether middot

(i) The consumer will incur a surrender charge be subject to the commencement of a new surrender period lose existing benefits (such as death living or other contractual benefits) or be subject to increased fees investment advisory fees or charges for riders and similar product enhancements

(ii) The consumer would benefit from product enhancements and improvements and (iii) The consumer has had another annuity exchange or replacement and in particular an

exchange or replacement within the preceding thirty-six months

middot19 RCW 4817530(1)(b) allows the Insurance Commissioner to place on probation

suspend revoke or refuse to issue or renew an insurance producers license for violating any

insurance laws or violating any rule subpoena or order of the Insurance Commissioner or of

another states insurance commissioner

ORDER REVOKING LICENSE 4 State of Washington ORDER NO 17-0481 Office of the lnsura~ce Commissioner

POBox40255

LA- 1444300 - I Olympia WA 98504-0255

20 RCW 4817 560 provides after hearing or upon stipulation by the licensee and in

addition to or in lieu of the suspension revocation or refusal to renew any such license the

Insurance Commissioner may levy a fine upon the licensee in an amount not more than one

thousand dollars

21 The Licensee engaged in twisting by misrepresenting the terms and benefits of

amrnities in order to induce two (2) consumers to replace and surrender existing ammities to

purchase new ones The Licensee also sold the consumers unsuitable annuities through

misrepresentation of the terms and benefits of the annuities These actions constitute violations of

RCW 4830180 RCW 4817530(l)(h) RCW 48l 7530(1)(e) RCW 4823015(2)(a) WAC 284shy

23-390(2) and RCW 4817530(1)(b) justifying the revocation ofhis license

ENTERED at Tumwater Washington this 2018

MIKE KREIDLER Insurance Commissioner

Insurance Enforcement Specialist Legal Affairs Division

ORDER REVOKING LICENSE 5 State of Washington

ORDER NO 17-0481 Office of the Insurance Connnissioner PO Box 40255

LA - 1444300 - 1 Olympia WA 98504-0255

NOTICE OF YOUR RIGHT TO A HEARING

If you are aggrieved by this Order Revoking License you may demand a hearing in

accordance with RCW 480401 O WAC 284-02-070 and WAC 10-08-110 Generally a hearing

demand must be in writing and received within ninety (90) days after the date of this Order

Revoking License which is the day it was mailed to you or you will waive your right to a

hearing

Ifthe Insurance Commissioner receives your demandfor a hearing before the effective

date listed on the order revoking your license the revocation will be automatically stayed

(postponed) and your license will remain in effect pending the hearing

You may fill out a demand for hearing fonn online at the following location httpswwwinsurancewagovhow-file-demand-hearing

Alternatively if you choose to file by mail your demand for hearing must briefly state

how you are harmed by this decision and why you disagree with it along with contact

infonnation (phone number mailing address e-mail address etc) for yourself and any

representative that appears on your behalf The demand may be sent to the following address

Hearings ()nit Office of the Insurance Commissioner P0Box40255 Olympia WA 98504-0255

You will be notified of the time and place of your hearing If you have questions about

filing a demand for hearing or the hearing process please telephone the Hearings Unit at (360)

725-7002 or send an email to HellringsUoicwagov

ORDER REVOKJNG LICENSE 6 State of Washington ORDER NO 17-0481 Office of the Insurance Commissioner

PO Box 40255

LA- 1444300 - 1 Olympia WA 98504-0255

CERTIFICATE OF MAILING

The tmdersigned certifies under the penalty of pe1jury under the laws of the state of

Washington that I am now and at all times herein mentioned a citizen of the United States a

resident of the state of Washington over the age of eighteen years not a party to or interested in

the above-entitled action and competent to be a witness herein

On the date given below I caused to be served the foregoing Order Revoking License on

the following individual by email and by depositing in the US mail via state Consolidated Mail

Service with proper postage affixed

Mitchell Johnson CLA USA INC 43 8 5TH Street 4 Lake Oswego OR 97034-3064 mitchcllreecjohnsongmailcom

Dated this__~__~--- day of 0w1~j- 2018 in Tumwater Washington

IP~ OS PACE

Legal Assistant Legal Affairs Division

ORDER REVOKING LICENSE 7 State of Washington

ORDER NO 17-0481 Office of the Insurance Co1n1nissioner PO Box40255

LA- 1444300 - I Olympia WA 98504-0255

HART WAGNER

TRIAL ATTORNEYS

Matthew J Kalmanson Twentieth Floor

mjkhartwagnercom Admitted in Oregon New York and Washington

IOOO SW Broadway Portland Oregon 97205

Telephone (503) 222-4499 Fax (503) 222-230 I

January 24 2018

Via Email and US Mail

Mike Kreidler Insurance Commissioner State of Washington Office of the Insurance Commissioner Hearings Unit POBox40255 Olympia WA 98504-0255 HearingsUoicwagov

Re In the Matter aMitchell Johnson WAOIC No 740959 NPN7562935 Order No 17-0481 Our File No 28236

Dear Commissioner

Licensee Mitchell Johnson hereby exercises his right to demand a hearing on the Commissioners Order Because this request is being made before the effective date of the Order the penalty revoking his license must be stayed

Below are the answers to sections 5(a) and 5(b) of the attached Demand for Hearing form I also attach a copy of the underlying Order Revoking License

Answer to S(a)

Mr Johnson challenges the facts described in the Commissioners Order as well as the legal conclusions that the Commissioner draws from those facts Among other things Mr Johnson disputes that

bull he engaged in twisting he misrepresented the terms and benefits of the two annuities at issue or he sold the Consumers unsuitable annuities

bull he misrepresented to Consumers the terms of the ING annuity

Commissioner Mike Kreidler January 24 2018 Page 2

bull the Bankers Life annuity was a better or more suitable investment than the ING annuity

bull the Consumers lost money due to the two annuity transactions

bull he solicited the Forethought annuity or pushed it on Consumers

bull paragraphs 8 9 and I 0 of the Order

bull he misrepresented to Consumers the terms of the Forethought annuity

bull the Forethought annuity was not suitable for Consumers

bull the Forethought annuity was a replacement of the ING annuity

bull paragraph 13 of the Order

Mr Johnson also challenges the Commissioners conclusion that he violated RCW 4830180 RCW 48 l 7530(1)(h) RCW 48 I7530(1)(e) RCW 4823015(2)(A) WAC 284-23shy390(2) and RCW 4817530(l)(b)

Mr Johnson also challenges the Commissioners penalty which is unduly punitive and therefore arbitrary and capricious The Commissioners Order cannot survive the standard of review that applies to a penalty that takes away his ability to earn a living

Answer to 5(b)

Mr Johnson did not engage in twisting did not misrepresent to Consumers the material terms and benefits of the ING and Forethought annuities and he did not sell Consumers unsuitable annuities The Commissioners Order contains significant inaccuracies and omissions The complaint in this case originated from Consumers son who was not present at any of the meetings between Mr Johnson and Consumers

Mr Johnson met Consumers in 2011 when he was an independent contractor who received referrals from CLA Although the Order is addressed to Mr Johnson as if he works for CLA he never has worked for CLA and he no longer accepts referrals from CLA

Husbands primary concern at the time was preserving money for Wifes future medical needs Husband repeatedly told Mr Johnson that he considered the money that was invested in a Bankers Life annuity to be Wifes money Husband also was very concerned about the quality of his Bankers Life annuity and the low fixed interest rate Husband had heard about consumer complaints relating to Bankers Lifes long-term care non-payment of claims

Mr Johnson recommended replacing the Bankers annuity with an ING annuity which in Mr Johnsons opinion is a more reputable company This is corroborated by the

Commissioner Mike Kreidler January 24 2018 Page 3

contemporaneous suitability documents which state that Consumers wanted the ING annuity because ofbetter rates more reputable creditworthy company issuing and client concerned w creditworthiness of Bankers Life Mr Johnson explained to Consumers there was a potential for better indexed rates he did not tell Consumers that the minimum guaranteed rate for ING was better than Bankers fixed rate as is said in the Commissioners Order

Mr Johnson told Consumers about the surrender charge and correctly told them that the charge would be offset by a bonus and a guaranteed initial rate of return that would make them close to whole within twelve months The ING annuity was from a more reputable company and Consumers did make more money than they would have with Bankers The Commissioners Order incorrectly calculates a loss apparently by subtracting the surrender charge assessed when Consumers surrendered the ING annuity to purchase the Forethought annuity but not including the Forethought bonus that offset the surrender charge

Mr Johnson visited with Consumers again in late 2013 as part of a routine review of his clients accounts Husband again expressed concern about Wifes future care noting that he considered he ING annuity to be her money and he wanted it to be there for her future medical care Mr Johnson and Husband called Consumers estate planning attorney Mark Plunkett to discuss options Mr Plunkett advised that ifan annuity was in Wifes name and there was an income benefit turned on then the asset might be protected from Medicaid spend-down requirements which would accomplish Husbands goals This was appealing to Husband

Mr Johnson is not experienced in Medicaid and had no reason to disbelieve Mr Plunkett There is no mention of this conversation with Consumers attorney in the Commissioners Order The Commissioners investigator told us during Mr Johnsons voluntary interview that Mr Plunkett disputes this conversation occurred Mr Plunkett purportedly claimed to know nothing about how estate planning interacts with Medicaid In response we sent the investigator a link to Mr Plunketts website where he states that he specializes in planning for future incapacity or death evaluating the strategic role of life disability and long term care insurance in business and estate planning We also forwarded disciplinary orders from Washington State Bar proceedings against Mr Plunkett involving CLA matters which can be found here httpslmclemywsbaorgdisciplinefiles18120431pdf

Based on the conversation with Mr Plunkett and Consumers Mr Johnson recommended the Forethought annuity The annuity would be in Wifes name per the strategy described by the attorney Mr Johnson advised Consumers about the surrender charge and the indexed rates and explained correctly that the bonus would offset the penalty Mr Johnson did not push this on Consumers he specifically told them that it was their choice Consumers chose to proceed The application states that Consumers wanted better rates lifetime income payment and principal protection On Page 4 where Mr Johnson is asked to explain how the annuity will assist the application in meeting his or financial needs and objectives Mr Johnson accurately wrote Asset preservation and lifetime income

Commissioner Mike Kreidler January 24 2018 Page 4

Because the annuity was going from Consumers to Wife individually Mr Johnson did not consider it a replacement Because Mr Johnson disclosed source of funds Forethought requested suitability replacement comparison information Mr Johnson provided the information The Order focuses on information in that form about minimum fixed rates but Consumers wanted the Forethought annuity based on the income rider and the index interestmiddot crediting methods

Mr Johnson reminded Consumers to turn on the income benefit rider several times but they did not do it He also tried to engage Consumers children in the planning process without success Mr Johnsons understanding ofwhHt happened next is that Wiles health took a turn for the worse and she entered assisted living For some reason Forethought denied the request for accelerated access to funds After that occurred and contrary to Mr Johnsons advice Consumers surrendered the Forethought annuity which led to the penalty

Mr Johnson does not believe these facts constitute twisting There may be some innocent misstateinents on the supplemental replacement form sent to Forethought about minimum fixed rates (we are continuing to investigate this issue) but this does not justify the draconian penalty Mr Johnson did not misrepresent the benefits of the mmuity to Consumers did not engage in twisting and the annuity was not unsuitable Nor did Mr Johnson believe tht1t the Forethought annuity was a replacement because the ING annuity was voluntarily surrendered by Husband and placed in an aanuity in Wifes name per the attorneys instructions Mr Johnson also earned somewhere between 23middot25 commission on these sales not the 38 stated in the Order

The penalty of revocation of his license is unduly punitive under the circumstances There is not clear and convincing evidence that Mr Johnson engaged in the conduct described in the Order Mr Johnson did what he believed was in the best interest of Consumers based on the information he received from them and their attorney Mr Johnson has worked in this industry for 35 years and strives to act in the best interests of his customers As far as he knows this is the first complaint he has received from a customer (he once received a complaint from a competitor which led to a consent order) He did his best to look out for Consumers best interests and comply with their wishes and the advice of their attorney He did not cause them to lose money as lJusbands son believed He feels terribly that things became difficult financially before Wifes death but it was not the result of Mr Johnsons conduct Revocation of his ability to earn a living is not warranted under these facts

Respectfully

Matthew J Kalmanson MJKfrh Enclosures

STATE OF WASHINGTON OFFICE OF THE INSURANCE COMMISSIONER

In The Matter of

Mitchell Johnson ORDER NO 17-0481

Licensee WAOICNO NPN

740959 7562935

ORDER REVOKING LICENSE

To Mitchell Johnson CLA USA INC 438 5TH Street 4 Lake Oswego OR 97034-3064 mitchellreediohnsonrunailcom

IT IS ORDERED AND YOU ARE HEREBY NOTIFIED that your Washington State

insurance producer license is REVOKED effectivf January 25 2018 pursuant to

RCW 4817530

BASIS

1 Mitchell Johnson (the Licensee) is a Washington nonresident insurance producer

WAOIC No 740959 licensed on March 9 2009

2 The Insurance Commissioner received a complaint alleging that the Licensee 1)

engaged in twisting by misrepresenting the terms and benefits of two annuities in order to induce

two Washington consumers husband and wife to replace and surrender two existing annuities to

purchase new ones resulting in large surrender charges 2) sold the husband and wife two

unsuitable annuities by misrepresenting the terms and benefits of these annuities

3 The first transaction which is the subject of this Order involved moving the

consumers Bankers Trust (Bankers) annuity to an ING annuity In 2009 the husband and wife

consumers purchased a living trust Sometime later the Licensee met with them about their living

trust and to review their assets The husband consumer decided to replace their Bankers anm1ity bull

because he believed it was not making money He had owned the Bankers product for 25 years

ORDER REVOKING LICENSE 1 State of Washington ORDER NO 17-0481 Office of the Insurance Commissioner

P0Box40255 LA- 1444300 - 1 Olympia WA 98504-0255

The Licensee offered to move him to amiddotnew annuity with ING (aka VOYA) The Licensee told

him the ING annuity offered better rates than the Bankers annuity The Licensee told him about

a surrender penalty but assured himicroi the ING annuity would cover the loss The consumer incurred

a $526522 surrender fee and purchased the ING annuity on November 11 2011 funding it

entirely with the Bankers product

4 Factoring in the initial 3 interest bonus the ING policy earned a total of$623938

from inception until the consumer surrendered it on November 22 2013 an average interest gain

of66 over two (2) years When the ING annuity was cashed fee was

charged After factoring in the surrender penalty the consumer lost $60038 on this annuity

5 The ING annuity (an indexed annuity) offered a substantially lower guaranteed

minimum interest rate (contrary to the Licensees repres~ntations in the suitability paperwork) than

the Bankers product (a fixed annuity) The consumer surrendered the annuity after only thirty (30)

months incurring a substantial surrender charge In addition the ING annuitys initial interest

bonus was less than the Bankers surrender charge

6 The Licensee misrepresented to the consumer and ING the insurer that the fixed

interest rates on the ING product were better than the Bankers annuity thereby inducing the

consumer to replace the Bankers product with the ING annuity Moreover the Licensee denied in

an interview with Investigations that he had referred to fixed rates and middotclaimed he had been

referring to the potential for better indexed rates middotHowever in the suitability paperwork and in his

initial response to the Insurance Co1mnissioner the Licensee specifically mentioned fixed rates

out a $683976 surrender

7 The second transaction which is the subject of this Order involved moving the

consumers ING annuity to a Forethought Life Insurance Company (Forethought) annuity The

husband consumer had only had the ING annuity for about twenty-six (26) months when the

Licensee came to their house and solicited a Forethought annuity The consumer had never

approached the Licensee about it The Licensee said Ive got a better deal for you that would

make them more money Th~consumer explained that the Licens~e pushed it on me

8 However the Licensee realized the husband consumer was too old to purchase the

annuity and determined to put it in your wifes name The Licensee explained the plan was for

them to replace the ING annuity with the Forethought annuity

9 The husband consumer informed the Insurance Commissioner that the only reason

he proceeded with the Foreihought annuity was the Licensee told us the Forethought annuity ORDER REVOKING LICENSE 2 State ofWashington ORDER NO 17-0481 Office of the Insurance Commissioner

PO Box 40255 LA- 1444300 - I Olympia WA 98504-0255

would make more money because of the supposed better rate of return The Licensee told

Forethought however that the consumers surrendered the ING annuity because of poor

perfonnance The ING annuity 1Jamed $623988 in twenty-four (24) months and was not

suffering from poor perfonnance middotIt might have continued to perfonn well but the Licensee

recommended the consumer surrender it which made himincur a $683976 s~rrender fee an

amount larger than his interest gains

10 Forethought infonned the Insurance Commissioner that the Licensee did not

disclose the source of the lump sum $88157 payment in the initial application paperwork while

also declaring the purchase was not replacing another annuity

11 At Forethoughts request the Licensee submitted supplementary suitability

documents which compared the now-surrendered ING annuity with the proposed Forethought

annuity In these documents the Licensee incorrectly wrote the ING annuity had a 10

guaranteed minimum interest rate its actual minimum guaranteed rate for the fixed strategy was

15 In addition he also misrepresented that the guaranteed minimum interest rate on the

Forethought annuity was 25 This is incorrect it was 225 for the fixed strategy only for the

first year thereafter it would be 050 He also wrote there were no disadvantages for his client

to select the Forethought annuity The Licensee stated to the Insurance Commissioners

investigator that he did not know why he wrote the incorrect guaranteed minimum interest rates

on the annuity comparison in the Forethought suitability documents

12 On April 20 2015 the husband consumer surrendered his wifes Forethought

annuity to assist with m1foreseen nursing home costs The annuitys value was $8766175 at the

time of surrender meaning it lost $49525

13 The Licensee earned a total of $672245 in commissionsfrom the sale of the ING

and Forethought annuities

14 RCW 4830180 states twisting is prohibited No persop shall by

misrepresentations or by misleading comparisons induce or tend to induce any insured to lapse

tenninate forfeit surrender retain or convert any insurance policy

15 RCW 48 l 7530(l)(h) allows the Insurance Commissioner to place on probation

suspend revoke or refuse to issue or renew an insurance producers license for using fraudulent

coercive or dishonest practices or demonstrating incompetence untrustworthiness or financial

irresponsibility in this state or elsewhere ORDER REVOKING LICENSE 3 State of Washington

ORDER NO 170481 Office of the Insurance Collllllissioner PO Box40255

LA- 1444300 - I Olympia WA 98504-0255

16 RCW 48l 7530(1)(e) allows the Insurance Commissioner to place on probation

suspend revoke orrefuse to issue or renew an insurance producers license for intentionally

misrepresenting the terms of an actual or proposed insurance contract or application for insurance

17 RCW 4823015(2)(a) provides in recommending the purchase of an annuity or the

exchange of an annuity that results in another insurance transaction or series of insurance

transactions to a consumer the insurance producer must have reasonable grounds for believing

that the recommendation is suitable for the consumer on the basis of the facts disclosed by the

consumer about their investments and other insurance products and as to their financial situation

and needs

18 WAC 284-23-390(2) provides that in addition to the requirements in RCW

4823015 insurance middotproducers must havemiddot reasonable grounds to believe the following

requirements in recommending and executing a purchase or exchange of an annuity

(a) The consumer has beeri reasonably informed of various features of the annuity such as the potential surrender period and surrender charge potential tax penalty if the consumer sells exchanges surrenders or annuitizes the annuity mortality and expense fees investment advisory fees potential charges for and features of riders limitations on interest returns insurance and investment components and market risk

(b) The consumer would benefit from certain features of the annuity such as tax deferred growth annuitization or death or living benefit

(c) The particular annuity as a whole the underlying subaccounts to which funds are allocated at the time of purchase or exchange of the annuity and riders and similar product enhancements if any are suitable (and in the case of an exchange or replacement the transaction as a whole is suitable) for the particular consumer based on his or her suitability information and

(d) In the case of an exchange or replacement of an annuity the exchange or replacement is suitable including taking into consideration whether middot

(i) The consumer will incur a surrender charge be subject to the commencement of a new surrender period lose existing benefits (such as death living or other contractual benefits) or be subject to increased fees investment advisory fees or charges for riders and similar product enhancements

(ii) The consumer would benefit from product enhancements and improvements and (iii) The consumer has had another annuity exchange or replacement and in particular an

exchange or replacement within the preceding thirty-six months

middot19 RCW 4817530(1)(b) allows the Insurance Commissioner to place on probation

suspend revoke or refuse to issue or renew an insurance producers license for violating any

insurance laws or violating any rule subpoena or order of the Insurance Commissioner or of

another states insurance commissioner

ORDER REVOKING LICENSE 4 State of Washington ORDER NO 17-0481 Office of the lnsura~ce Commissioner

POBox40255

LA- 1444300 - I Olympia WA 98504-0255

20 RCW 4817 560 provides after hearing or upon stipulation by the licensee and in

addition to or in lieu of the suspension revocation or refusal to renew any such license the

Insurance Commissioner may levy a fine upon the licensee in an amount not more than one

thousand dollars

21 The Licensee engaged in twisting by misrepresenting the terms and benefits of

amrnities in order to induce two (2) consumers to replace and surrender existing ammities to

purchase new ones The Licensee also sold the consumers unsuitable annuities through

misrepresentation of the terms and benefits of the annuities These actions constitute violations of

RCW 4830180 RCW 4817530(l)(h) RCW 48l 7530(1)(e) RCW 4823015(2)(a) WAC 284shy

23-390(2) and RCW 4817530(1)(b) justifying the revocation ofhis license

ENTERED at Tumwater Washington this 2018

MIKE KREIDLER Insurance Commissioner

Insurance Enforcement Specialist Legal Affairs Division

ORDER REVOKING LICENSE 5 State of Washington

ORDER NO 17-0481 Office of the Insurance Connnissioner PO Box 40255

LA - 1444300 - 1 Olympia WA 98504-0255

NOTICE OF YOUR RIGHT TO A HEARING

If you are aggrieved by this Order Revoking License you may demand a hearing in

accordance with RCW 480401 O WAC 284-02-070 and WAC 10-08-110 Generally a hearing

demand must be in writing and received within ninety (90) days after the date of this Order

Revoking License which is the day it was mailed to you or you will waive your right to a

hearing

Ifthe Insurance Commissioner receives your demandfor a hearing before the effective

date listed on the order revoking your license the revocation will be automatically stayed

(postponed) and your license will remain in effect pending the hearing

You may fill out a demand for hearing fonn online at the following location httpswwwinsurancewagovhow-file-demand-hearing

Alternatively if you choose to file by mail your demand for hearing must briefly state

how you are harmed by this decision and why you disagree with it along with contact

infonnation (phone number mailing address e-mail address etc) for yourself and any

representative that appears on your behalf The demand may be sent to the following address

Hearings ()nit Office of the Insurance Commissioner P0Box40255 Olympia WA 98504-0255

You will be notified of the time and place of your hearing If you have questions about

filing a demand for hearing or the hearing process please telephone the Hearings Unit at (360)

725-7002 or send an email to HellringsUoicwagov

ORDER REVOKJNG LICENSE 6 State of Washington ORDER NO 17-0481 Office of the Insurance Commissioner

PO Box 40255

LA- 1444300 - 1 Olympia WA 98504-0255

CERTIFICATE OF MAILING

The tmdersigned certifies under the penalty of pe1jury under the laws of the state of

Washington that I am now and at all times herein mentioned a citizen of the United States a

resident of the state of Washington over the age of eighteen years not a party to or interested in

the above-entitled action and competent to be a witness herein

On the date given below I caused to be served the foregoing Order Revoking License on

the following individual by email and by depositing in the US mail via state Consolidated Mail

Service with proper postage affixed

Mitchell Johnson CLA USA INC 43 8 5TH Street 4 Lake Oswego OR 97034-3064 mitchcllreecjohnsongmailcom

Dated this__~__~--- day of 0w1~j- 2018 in Tumwater Washington

IP~ OS PACE

Legal Assistant Legal Affairs Division

ORDER REVOKING LICENSE 7 State of Washington

ORDER NO 17-0481 Office of the Insurance Co1n1nissioner PO Box40255

LA- 1444300 - I Olympia WA 98504-0255

Commissioner Mike Kreidler January 24 2018 Page 2

bull the Bankers Life annuity was a better or more suitable investment than the ING annuity

bull the Consumers lost money due to the two annuity transactions

bull he solicited the Forethought annuity or pushed it on Consumers

bull paragraphs 8 9 and I 0 of the Order

bull he misrepresented to Consumers the terms of the Forethought annuity

bull the Forethought annuity was not suitable for Consumers

bull the Forethought annuity was a replacement of the ING annuity

bull paragraph 13 of the Order

Mr Johnson also challenges the Commissioners conclusion that he violated RCW 4830180 RCW 48 l 7530(1)(h) RCW 48 I7530(1)(e) RCW 4823015(2)(A) WAC 284-23shy390(2) and RCW 4817530(l)(b)

Mr Johnson also challenges the Commissioners penalty which is unduly punitive and therefore arbitrary and capricious The Commissioners Order cannot survive the standard of review that applies to a penalty that takes away his ability to earn a living

Answer to 5(b)

Mr Johnson did not engage in twisting did not misrepresent to Consumers the material terms and benefits of the ING and Forethought annuities and he did not sell Consumers unsuitable annuities The Commissioners Order contains significant inaccuracies and omissions The complaint in this case originated from Consumers son who was not present at any of the meetings between Mr Johnson and Consumers

Mr Johnson met Consumers in 2011 when he was an independent contractor who received referrals from CLA Although the Order is addressed to Mr Johnson as if he works for CLA he never has worked for CLA and he no longer accepts referrals from CLA