missouri agent january-february 2012

DESCRIPTION

Missouri Agent is a bimonthly magazine published by the Missouri Association of Insurance Agents. Its target audience is the independent insurance industry, particularly member agencies of the association. This issue focuses on the Small Agency Conference.TRANSCRIPT

Age

nt positivelychange your world with

one question?

missouri

spec

ial fo

cus:

small

agen

cy

confer

ence

jan

uar

y-fe

bru

ary

2012

Vo

l. 21

, No

. 1

For more details, contact your Business Development Manager or Customer Service at 1.800.442.0593 or [email protected]

The MEM DifferenceIn today’s market, the lowest price stands out. In the long-run, we believe value does. Missouri Employers Mutual has earned our 16-year reputation as the work comp market leader by offering competitive rates combined with exceptional service and a dedication to safe workplaces.

That’s a value unbeatable in any market or economic condition.

For a true work comp partner for you and your clients, contact MEM.

www.mem-ins.com

WHAT’S MISSOURI’S BEST VALUE FOR THE WORK COMP DOLLAR?

Introducing . . . www.worksafecenter.coman online tool to keep Missouri workplaces safe

january-february 2012 missouriagent 3

contentsSpecial Focus: Small Agency ConferenceThe Million Dollar Question 19Conference Highlights 20Conference Agenda and Speaker Bios 22

Tired and Retired 7Elite Earns Enthusiasm 232011 CSR Development Conference 26What is a Great Relationship? 27

AdvertisersACUITY 39Agents Marketing Corporation 28American Mining Insurance Co. 12BC&M 34Big “I” Flood 24Burns & Wilcox 8Electric Insurance Company 31FCCI Insurance Group 13Illinois Casualty Co. 17IPMG 27MAIA Education 6

DepartmentsFrom the President 5The Legal Side 9Missouri News 11Technology 12Technicalities 15From the DIFP 25

Errors & Omissions 29Regulatory Actions 33 Company Partner News 37Agency News 38Classifieds 38

missouriagent

3315 Emerald Lane, P.O. Box 1785, Jefferson City, MO 65102-1785 • 800-617-3658 in Mo. Phone 573-893-4301 • FAX 573-893-3708E-mail: [email protected]: www.missouriagent.org

Publisher Larry CaseEditor Amy J. HoffmanAdvertising Manager Amy J. Hoffman

Officers of the MAIAPresident Byron Robison, SpringfieldPresident-Elect Doug Clift, CIC, St. LouisVice President Brian Harrison, CIC, ColumbiaSec’y-Treasurer Louis Landwehr, CIC, CRM, Jeff City IIABA National Director Mitchell C. Mills, ClintonPIA National Director Richard Minor, CIC, Hannibal Past President Scott Brothers, CIC, Joplin

Board of DirectorsRegion 1 Ricky Baker, CIC, ChillicotheRegion 2 Steve Heying, CIC, St. PetersRegion 3 Chris Rupp, LUTCF, CIC, LibertyRegion 4 Shane Davolt, Kansas CityRegion 5 Rick Naught, CIC, CPCU, Jefferson CityRegion 6 Jim Baxendale, CPCU, St. LouisRegion 7 Jeff Mentel, J.D., St. LouisRegion 8 Jane Dobrinic, CIC, CPCU, St. LouisRegion 9 Randy Smart, MarionvilleRegion 10 Tom Montileone, BolivarRegion 11 Steve Rackley, CIC, CISR, GainesvilleRegion 12 Randy Baker, KennettAt-Large #1 Wil Turner, CIC, BeltonAt-Large #2 Ted Schroeder, UnionAt-Large #3 John Patterson, ChesterfieldCo. Rep. Diane Marshall, ColumbiaCo. Rep Dennis Putthoff, Murfreesboro, Tenn.

Staff of the MAIAExecutive Vice President Larry CaseVice President of Operations Sheryl Van LeerVice President of Marketing Lindsay Schmidt, AIPInsurance Services Manager Leona LoethenEvents Manager Jeanne Blomberg, AIPDatabase Administrator Laura BerendzenCustomer Service Representative Theresa Flippin, AIPCustomer Service Representative Monica Mize, AIPEditor Amy J. HoffmanMembership Services Representative Kelli Kloeppel, AIPEducation Director Emily KoenigsfeldAdministrative Assistant Dawn PattersonEducation Coordinator Julie Case

MISSOURI AGENT (USPS 709-210) is published bimonthly by the Missouri Association of Insurance Agents, 3315 Emerald Lane, Jefferson City, MO 65109, phone 573-893-4301. Periodical postage paid at Jefferson City, Mo.

MAIA does not necessarily endorse any of the companies advertising in this publication. Subscription rate for members is $25 per year, which is included in dues.

Address & Other Changes

Notify Missouri Agent if you change your address, change your agency name, or drop or change producers (who are voting members of the association). Write to Missouri Agent, P.O. Box 1785, Jefferson City, MO 65102-1785 or e-mail [email protected].

POSTMASTER: Send address changes to Missouri Agent, P.O. Box 1785, Jefferson City, MO 65102-1785.

© 2012 Missouri Association of Insurance Agents

On the Cover: Learn how asking the right question can make all the difference in the world. See page 19.

Volume 21, No. 1

MAIA Events 18MAIA Partners 40MEM Insurance 2Meramec Valley Mutual 16Missouri Rural Services 10M.J. Kelly Company 37Ringwalt & Liesche Co. 30RLI 14SECURA 32Surplus Lines Association of Mo. 36West Bend 4

Age

nt positivelychange your world with

one question?

missouri

spec

ial fo

cus:

small

agen

cy

confer

ence

jan

uar

y-fe

bru

ary

2012

Why choose West Bend

NSI is a division of West Bend Mutual Insurance Company. Rated A (Excellent) with a financial strength category of X by A.M. Best and Treasury listed at $54,201,000 (7/1/11).

Because we offer a standard market bond facility that doesn’t text-book underwrite. We look at each account based on its own merit. Having this flexibility and latitude translates into a common-sense approach to bond underwriting.

Because you’ll find on-line contract and commercial bond programs that offer you an IMMEDIATE response for...

• Rapid Bonds – our small contractor program for contract bonds up to $200,000;

• License & Permit Bonds;

• Miscellaneous Bonds;

• Court Bonds; and

• Public Official Bonds.

Because our contract surety programs also include:• Standard performance and payment bonds up to $5 million;

• SBA Contract Bond Guarantee Program; and

• Rapid PLUS Program for contract bonds of $200,000 to $400,000.

Because our surety associates offer:• Experience;

• Stability; and

• Flexibility ... with underwriters who WANT to talk to you and help you write business!

Because you’ll also get: • A stand-alone bond bonus program;

• Competitive commissions;

• Competitive four-tier rates;

• Direct or agency bill options; and

• A company that, more than anything, sincerely values the relationships we share with our agents and their customers.

Our business is writing your business. Trust our stability and experience when placing your bond accounts. We’ll provide you with the right solution.

With West Bend, you have the right market for bonds!

for your customers’ bond needs?

thesilverlining.com

january-february 2012 missouriagent 5

Happy new year and goodbye 2011

Byron Robisonpresident, MAIA

I hope 2011 wasn’t too bad for everyone, but it will go down as a year everyone will remember. I am not going to spend your time looking back but instead want to look forward for what the future may hold.

If you attended the compliance meetings this fall, you found out that there are several issues we are dealing with on the national level. We want to address the medical loss ratio calcula-tions. In other words, we want agent commis-sions removed from the formula. Another issue the industry is facing is the need to make it easi-er to get and hold out-of-state licenses through a single licensing portal rather than through each individual state. Last but not least, we want to work toward a long-term extension of the National Flood Insurance Program.

The state issues include workers’ compen-sation issues such as the second injury fund, employees being able to sue co-workers, and the instance where an employee collects work comp benefits and additionally has the oppor-tunity to make another claim under employer liability.

Larry Case mentioned the need to create a state health exchange. Earthquake coverage may get more attention with all the action in Oklahoma, and how did it make you feel when he pointed out there is no definition of actual cash value in your policy? With no definition, some companies are adjusting claims on fair market value. How many underwriters will ac-cept fair market value as a limit on a policy?

The last one I will mention is the valued policy law. This law tells the company to pay the limit of the policy when a structure is destroyed, but it applies only to the peril of fire. All other perils are fair game regarding the payout of a claim.

I think Larry’s part of the program scared me more than the errors and omissions class. One does not know how a court case may turn out,

but like we have seen, it will make changes on how coverage is determined for the future. When there is a new ruling from the court, companies can make changes in the policy, or we can make changes in the law.

At our meetings around the state, it was mentioned that not everyone is a friend to in-surance. We need to support our friends who will help us make changes in the law through InsurPac and MAPAC.

I don’t expect our contributions to buy votes, but they can get us in the door to receive sup-port and have a listening ear for our side. Our goal on a national level for the Big “I” is to raise over $1 million, but at press time, we remained short of that goal. We are not the largest asso-ciation in fundraising. Would you believe USAA contributes more than we do?

My goal is to educate you on how important it is for everyone to be involved in contributing to our political action committees. It is also im-portant to stress that every dollar counts. I ap-preciate all the support you have given. I know the New Year brings new opportunities, new hopes, new plans and new resolutions. It is my hope that one of your new resolutions will be to plan to take the opportunity to make a con-tribution to InsurPac and MAPAC.

I would like to end this article by thanking all of those who gave to InsurPac in 2011. I will have all the names listed in the next issue. We are now accepting contribu-tions for 2012. Remember, InsurPac donations have to be made by indi-viduals, not agencies. Happy new year!

fromthepresident

FOR INSURANCE PROFESSIONALSFOR INSURANCE PROFESSSIOONALSEDUC TION

Who Should Attend:CIC Institutes

CISR Courses AVAILABLE ONLINE

Programs That Give You “Response-Ability”

CIC & CISR

CIC Institutes

Personal Lines InstituteJan. 18-21, 2012, Independence

Commercial Property InstituteFeb. 29-March 3, 2012, Jefferson CityVNew location!

James K. Ruble Graduate Seminar**April 25-26, 2012, Independence

**You must be a designated CIC or CRM to at-tend this course.

CISR Courses

Personal Auto SeminarFeb. 9, 2012, Spring eldFeb. 15, 2012, IndependenceMarch 6, 2012, Chester eldMarch 15, 2012, Cape Girardeau

William T. Hold Seminar*March 28, 2012, Independence

*No designation required. All agency personnel welcome.

Register online at www.missouriagent.org.Questions? Call MAIA Education Director Emily Koenigsfeld at 800-617-3658.

See the entire

2012 CISR and CIC schedule on-line at missouri

agent.org.

january-february 2012 missouriagent 7

Larry Caseexecutive vice president, MAIA

FOR INSURANCE PROFESSIONALSFOR INSURANCE PROFESSSIOONALSEDUC TION

Who Should Attend:CIC Institutes

CISR Courses AVAILABLE ONLINE

Programs That Give You “Response-Ability”

CIC & CISR

CIC Institutes

Personal Lines InstituteJan. 18-21, 2012, Independence

Commercial Property InstituteFeb. 29-March 3, 2012, Jefferson CityVNew location!

James K. Ruble Graduate Seminar**April 25-26, 2012, Independence

**You must be a designated CIC or CRM to at-tend this course.

CISR Courses

Personal Auto SeminarFeb. 9, 2012, Spring eldFeb. 15, 2012, IndependenceMarch 6, 2012, Chester eldMarch 15, 2012, Cape Girardeau

William T. Hold Seminar*March 28, 2012, Independence

*No designation required. All agency personnel welcome.

Register online at www.missouriagent.org.Questions? Call MAIA Education Director Emily Koenigsfeld at 800-617-3658.

See the entire

2012 CISR and CIC schedule on-line at missouri

agent.org.

Tired and retiredLast summer, I received communications inform-ing me that I was eligible to draw retirement from my service with state government. Frankly, I have no idea what allows me to “retire” at age 57 when I haven’t worked for state government in over 25 years and my total service was limited to five years out of college and one additional year in a second stint. Nevertheless, that was the case, and I am now officially a retired state employee. My challenge is deciding how to spend the monthly $121.

While I could now be relaxing on the beach had I spent my entire career in state govern-ment, the work environment wasn’t for me. However, it did get me to thinking.

In spite of my career being in the private sector, I spend an inordinate amount of time working for or with the government. Rarely does a day go by that I am not addressing some problem or nonsensical bureaucratic require-ment that impacts your business or that of your clients. There is often little consideration of how the real world functions outside of the government, and all too often, common sense is ignored.

Ronald Reagan’s quote, “The nine most ter-rifying words in the English language are: ‘I’m from the government, and I’m here to help,’” continues to ring just as true today as when he uttered them.

For whatever reason, it seems that the Mis-souri Department of Revenue has more than its share of judgment lapses. Remember the inser-tion of automobile insurance advertising into auto license renewal notices? Remember the attempt to charge around $10 for every motor vehicle record? Well, they’re still at it.

One recent incident involved an auto license renewal. As everyone knows, one must pro-vide proof of insurance when renewing vehicle tags. Traditionally, you provide an insurance ID card. Well, last month, an individual actually presented his insurance policy to the licensing clerk, and the clerk indicated that it wasn’t ac-ceptable; the insurance card was needed. Think about it … The clerk actually wanted a card to certify that the policy the consumer was hold-ing actually existed.

Topping that was a much more problematic issue reported to us by several members. It dealt

with the renewal of boat dealer licenses. Like auto dealers, boat dealers must include a certifi-cate of insurance showing proper insurance cov-erage. This is nothing new. However, someone at Revenue apparently had some spare time and decided to re-interpret what coverage was acceptable.

Suddenly, certificates were being rejected because they did not specify that the coverage being provided was a garage policy. Of course, a garage policy is not designed for boat dealers and even has a watercraft exclusion. Boat deal-ers are commonly written on a general liability form designed to cover boat dealer exposures. Nevertheless, folks at Revenue determined that the certificate must specifically include the word garage.

Notwithstanding multiple agents providing factual explanations to Revenue officials, they would not relent. MAIA requested that officials from the Department of Insurance, Financial Institutions and Professional Registration inter-vene and explain the coverage issues. In spite of their detailed explanation and validation of what agents had indicated, officials at Revenue continued to insist that certificates include the word garage. Thus, the agent would either have to lie on a certificate (a violation jeopardiz-ing one’s license) or actually sell the customer a policy that provided no coverage but would satisfy the bureaucrats.

My only thought was that a more applicable quote than Reagan’s was uttered by Harry in the movie Dumb and Dumber: “Just when I thought you couldn’t possibly be any dumber, you go and do something like this … and totally redeem yourself.”

Continued frustrations led to a meeting in December, at which MAIA legal counsel Lew Melahn and I discussed with DIFP officials ways the issue might be finally resolved. We continue to work through the appropriate channels and hope there might be a long term resolution before long.

And, I continue to wonder how things might have been … Even as warped as my mind works now, what would a career in state govern-ment have done to me?

myturn

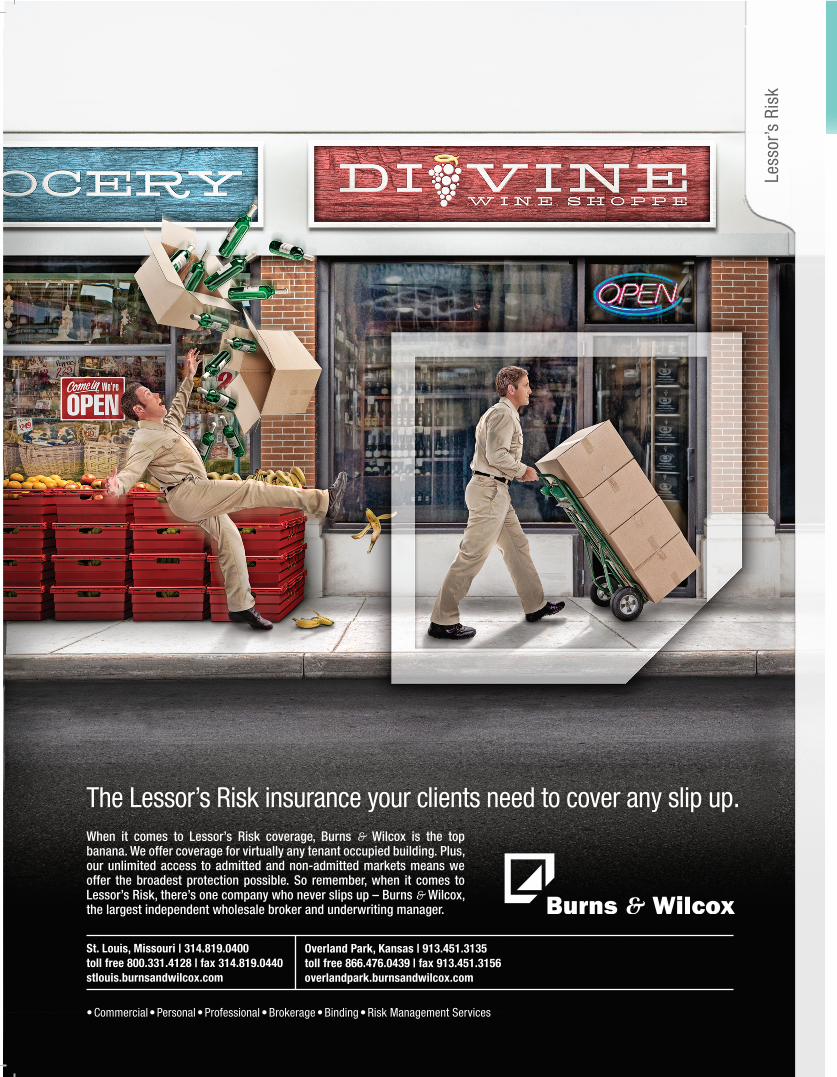

When it comes to Lessor’s Risk coverage, Burns & Wilcox is the top banana. We offer coverage for virtually any tenant occupied building. Plus, our unlimited access to admitted and non-admitted markets means we offer the broadest protection possible. So remember, when it comes to Lessor’s Risk, there’s one company who never slips up – Burns & Wilcox, the largest independent wholesale broker and underwriting manager.

The Lessor’s Risk insurance your clients need to cover any slip up.Le

ssor

’s R

isk

• Commercial• Personal • Professional • Brokerage • Binding • Risk Management Services

St. Louis, Missouri | 314.819.0400toll free 800.331.4128 | fax 314.819.0440stlouis.burnsandwilcox.com

Overland Park, Kansas | 913.451.3135toll free 866.476.0439 | fax 913.451.3156overlandpark.burnsandwilcox.com

january-february 2012 missouriagent 9

Lewis E. Melahn is a practicing attorney in Jef-ferson City. He provides free legal consultation to MAIA members on a limit-ed basis. He served as the director for the Missouri Department of Insurance from 1989-1993. You can contact Lew Melahn at 573-636-5057.

Lewis E. Melahn, J.D.

When it comes to Lessor’s Risk coverage, Burns & Wilcox is the top banana. We offer coverage for virtually any tenant occupied building. Plus, our unlimited access to admitted and non-admitted markets means we offer the broadest protection possible. So remember, when it comes to Lessor’s Risk, there’s one company who never slips up – Burns & Wilcox, the largest independent wholesale broker and underwriting manager.

The Lessor’s Risk insurance your clients need to cover any slip up.

Less

or’s

Ris

k

• Commercial• Personal • Professional • Brokerage • Binding • Risk Management Services

St. Louis, Missouri | 314.819.0400toll free 800.331.4128 | fax 314.819.0440stlouis.burnsandwilcox.com

Overland Park, Kansas | 913.451.3135toll free 866.476.0439 | fax 913.451.3156overlandpark.burnsandwilcox.com

When agency records are subpoenaedI hear with increasing frequency of agencies receiving subpoenas for records of their custom-er policyholders, usually on very short notice. Those agencies are requesting some guidance for their response to the subpoena.

The agency must keep in mind that while the records it has are business records of the agency, they also contain the personal records of their policyholders and the business records of the companies which write the policies. Both of those parties may have an interest in what records are produced or not produced, and may wish to be included in determining the response to the subpoena.

In many cases, the agency may not know the issues of the lawsuit giving rise to the subpoena and thus will not know the impact the records may have on the matter. If either the policy-holder or the company is involved in the law-suit, they may have grounds to attempt to limit or quash the subpoena.

The agency should remember that gener-ally a subpoena is not a court-reviewed docu-ment. Any attorney in a lawsuit can request a subpoena from a court clerk. So, for example, if personal information of your policyholder which is protected by Gramm-Leach-Bliley or health information protected by HIPAA, is requested in the subpoena, there may not be sufficient protections specified within the sub-poena to meet the requirements of those laws.

How should an agency respond? If the sub-poena indicates your policyholder is a party to the lawsuit, it should name the attorney for the policyholder. The agency should contact that at-torney and ask if there are any objections to the subpoena. If so, that attorney can contest the subpoena without cost to the agency.

Second, the agency should advise the insur-ance carrier of the subpoena to determine if it

has any involvement or objections, especially if the lawsuit involves a claim. Some of the records the agency has may be privileged documents. If no party with information in the agency records indicates objections to their production, then the agency can proceed to produce the records.

The agency needs to be aware that most subpoenas will come as a subpoena for an ap-pearance at a deposition with a demand for the production of certain records at that appear-ance. However, Missouri statutes provide that if the party really is only requesting the custodian of records to bring the records, the custodian may prepare an affidavit certifying that all the records have been provided and thus poten-tially avoid the necessity of appearing at the deposition. The potential for using an affidavit should be discussed with the attorney who sent the subpoena to the agency.

While an agency could handle some of these contacts itself, if it appears there are any ques-tions about the agency’s conduct regarding the policy in question, the agency should strongly consider discussing all of these options with counsel before proceeding. When dealing with the personal records of the policyholder, there is some potential for liability for disclosing priv-ileged or protected information, and counsel may be able to assist in avoiding any adverse consequences.

thelegalside

january-february 2012 missouriagent 11

Mo. companies put into receivershipThe Barton Mutual GroupA Barton County judge has placed a group of three small insurance companies into receiver-ship, after claims from the Joplin tornado left the group insolvent. John M. Huff, director of the Missouri Department of Insurance, Financial Institutions and Professional Registration has been named receiver of the three companies that make up Barton Mutual Group: Barton Mu-tual Insurance Co., Gateway Mutual Insurance Co. and Cape Mutual Insurance Co.

A judge has approved a plan to rehabilitate the companies and remove them from receiver-ship. Under the plan:

• The three Barton Group companies will merge together into one company, with Gateway being the surviving company, effec-tive Jan. 1, 2012, and Missouri Farm Bureau Services will enter into an agreement to man-age the future operations;

• The Missouri Farm Bureau companies will invest approximately $14 million in surplus notes to restore the surplus to a positive level, with the notes being backed by the Missouri Property and Casualty Insurance Guaranty Association;

• The new company will then have the capacity to ensure all policyholder claims are paid and all policyholders’ coverage will continue, and the company will obtain an amount of rein-surance from Farm Bureau deemed adequate by the department to ensure that it can meet future claims obligations; and

• Once the plan is implemented, the depart-ment’s control will be lifted.

Long-term issues relating to Farm Bureau’s maintenance of independent agency relation-ship and whether Farm Bureau’s agencies will gain access to Gateway products remains un-stated in the plan of rehabilitation.

The three companies are licensed as extended Missouri mutuals, also known as county mutu-als for farm mutuals. In general, they are small companies serving rural policyholders. There are about 90 county mutuals in Missouri.

“As a group, these companies had their risk concentrated in a small geographic area, mainly

surrounding Joplin,” says Huff. “The once-in-a-lifetime event that was the Joplin tornado resulted in insured property losses that were simply too much for these companies to bear.”

The companies had about 41,000 policyhold-ers, primarily with homeowners and fire insur-ance, and premium sales of nearly $29 million in 2010. The companies’ 875 claims from the Joplin tornado totaled approximately $48 million.

Huff says there are significant outstanding claims that the companies would be unable to pay, but the rehabilitation plan will ensure that the claims are paid.

Huff says policyholders must continue making their premium payments to keep their insurance coverage intact. Payments should continue to be sent to the Barton Mutual Group’s offices.

Watkins Life and BenefitsA judge has placed a small, Dexter-based life in-surance company into rehabilitation and turned it over to the DIFP. Director John M. Huff was named receiver of Watkins Life and Benefits As-sociation, which allows the department to take over operations of the company. Because of its financial condition, the company’s board of di-rectors consented to the rehabilitation order.

With about 2,000 policyholders, Watkins is licensed to do business only in Missouri. With premium sales of just $45,000 in 2010, Watkins is one of the smallest of Missouri’s approximate-ly 400 licensed life insurance companies. With the company in rehabilitation, the department’s priority will be to process existing claims and uphold commitments to policyholders.

The department’s website, insurance.mo.gov, has more information about the receivership.

“This small company was formed 60 years ago mainly to provide insurance coverage for funeral contracts,” says Huff. “Unlike most life insurance companies, Watkins is an assessment plan formed by a mechanism that is no longer allowed under Missouri law.”

Huff says policyholders of the company should continue to pay their premiums, also referred to as assessments, to keep their cover-age intact. These payments should be mailed to: Receivership Supervisor, Room 530, P.O. Box 690, Jefferson City, MO 65101.

missourinewsEXTRA!

12 missouriagent january-february 2012

WWW.AMERICANMINING.COM

“insurance from people who know mining”

For more information, contact Bryant Brown, V.P. Marketing • 1.800.448.5621, x 249.

3490 Independence Drive • Birmingham, Alabama 35209

We Offer Workers’ Compensation and Liability Coverages For:

Copper, Silver & Coal mines: surface and underground

coal truckmen (workers’ Comp only)

c

c

c

c

c

c

quarries

sand and gravel digging

other types of mining

mining related risks

3 digital parallels to traditional marketing tacticsFor agencies that have spent years, decades, even generations building a local footprint with traditional marketing tools, it can be un-derstandably daunting to hear so many in the media assert that success in today’s market-

place now requires extensive e-marketing expertise and a dynamic online presence. The good news: Many of the tech-niques agents have long used to thrive in their communities are still relevant. They also have clear parallels in the digi-tal space, and in many cases, their online counterparts are easy to implement and mea-sure. Understand the connec-

tion, and you can use what you already know to master these new online tactics.

Matt Markomarketing manager, Progressive Insurance

Yellow Pages and local searchThe Yellow Pages Association reports that there are 900 million Yellow Page print references ev-ery month. The online equivalent? Local search. ComScore estimates that in March 2011, there were nearly 17 billion searches on all major search engines. With Google having released es-timates that local search represents 20 percent of their search volume and Bing reporting 53% of its mobile searches have local intent, the oppor-tunity for small businesses is immense.

When a consumer searches online for insur-ance, how your agency ranks in the local results makes all the difference. According to Chikita research, if you make the top three listings, your agency shares 63% of the traffic. Land in the bottom seven and that number drops to 32%. Only 5% of searchers continue to the second page of results. Yet only a fraction of indepen-

technology

january-february 2012 missouriagent 13

dent agents have taken the first step to benefit from this free service.

That first and most important step is proac-tively claiming and verifying your online list-ings. There are free, do-it-yourself options like getlisted.org, which audit how effectively your agency has claimed its local search listings and allow you to create listings with each of the pri-mary search engines from one website.

Just as a variety of factors (ad size, color, content) influence the success of your Yellow Pages print ad, several elements affect your lo-cal search ranking. Keep your listings consistent across search engines by using your official business name and avoiding abbreviations; generate as many consistent citations (online references to your business) as you can among search engines; eliminate duplicate listings; and be sure to include as much relevant content as possible, including your agency address, phone number, e-mail, website, photos and business details. Finally, create a strategy for getting your customers to review your business online.

Word-of-mouth and online reviewIt’s not a secret that a leading driver of new business is a happy customer. For agencies, which have nurtured word-of-mouth referrals from their customers (and for agencies which simply see the results walking through the door), encouraging your customers to share their feedback online is an easy way to amplify their voices.

Asking Facebook fans and LinkedIn connec-tions to recommend your agency to their social networks is the clearest bridge between tra-ditional and digital referral tactics, but online reviews on sites like Google Places, Citysearch, Yelp and Insider Pages have additional advan-tages: Not only can they boost your local search visibility, but they can sway strangers as well.

In fact, according to BrightLocal, 70% of con-sumers trust online reviews as much as personal recommendations. This is especially true in the insurance industry, where 57% of consumers said their insurance purchase was influenced by reviews more than websites, TV or radio advertising. Search engines like Google and Ya-hoo prominently display reviews in their query results, yet Progressive’s research into online referrals found that our independent agents have, on average, just 0.3 reviews on their on-line listings.

If you’re not currently soliciting online reviews from your customers, try adding requests to your customer communications. Develop e-mail templates that you can easily customize and send with links to review sites. Again, your carri-ers may be able to help you here by providing e-mail templates for you to use. You can also add links to your website and customer newsletters.

Don’t worry if a couple of negative reviews turn up with the positive. A 2011 Lightspeed Research study found that only 4% of shoppers change their mind about a service after reading one bad review, and only 25% of consumers

continued on page 36

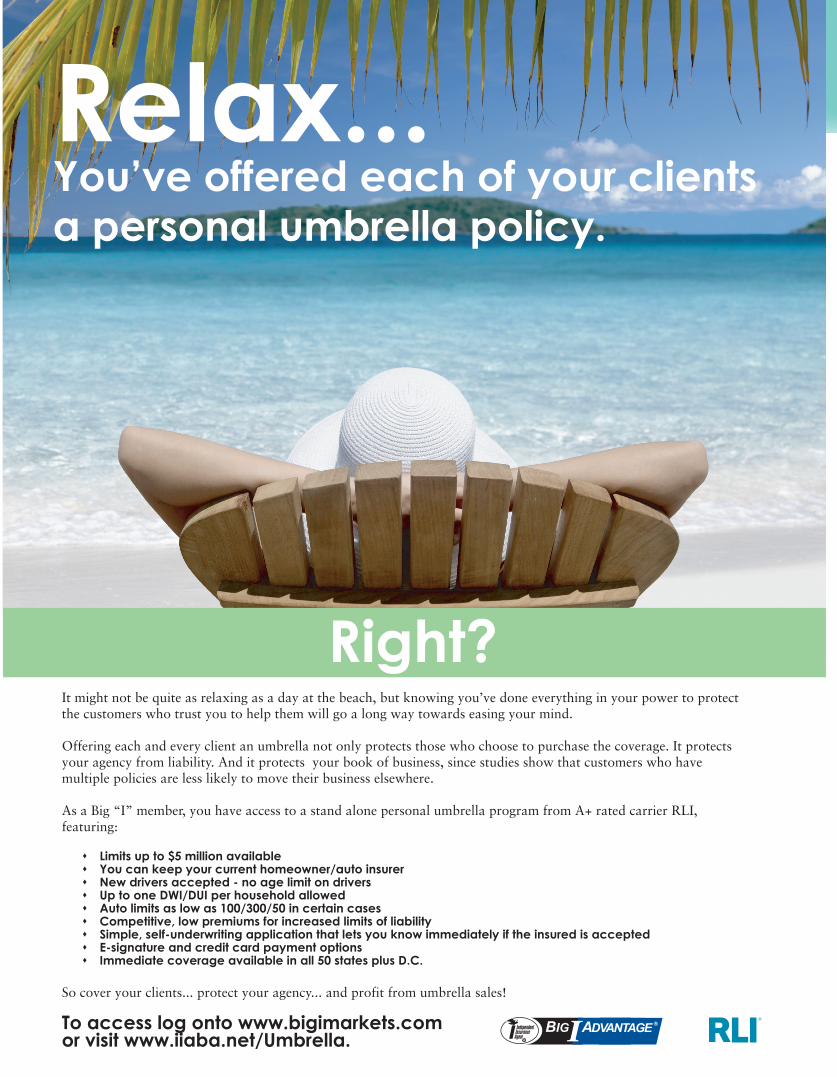

Relax... You’ve offered each of your clients a personal umbrella policy.

Right? It might not be quite as relaxing as a day at the beach, but knowing you’ve done everything in your power to protect the customers who trust you to help them will go a long way towards easing your mind.

Offering each and every client an umbrella not only protects those who choose to purchase the coverage. It protects your agency from liability. And it protects your book of business, since studies show that customers who have multiple policies are less likely to move their business elsewhere.

As a Big “I” member, you have access to a stand alone personal umbrella program from A+ rated carrier RLI, featuring:

� Limits up to $5 million available� You can keep your current homeowner/auto insurer� New drivers accepted - no age limit on drivers� Up to one DWI/DUI per household allowed� Auto limits as low as 100/300/50 in certain cases� Competitive, low premiums for increased limits of liability� Simple, self-underwriting application that lets you know immediately if the insured is accepted� E-signature and credit card payment options� Immediate coverage available in all 50 states plus D.C.

So cover your clients... protect your agency... and profit from umbrella sales!

To access log onto www.bigimarkets.com or visit www.iiaba.net/Umbrella.

®

january-february 2012 missouriagent 15

Relax... You’ve offered each of your clients a personal umbrella policy.

Right? It might not be quite as relaxing as a day at the beach, but knowing you’ve done everything in your power to protect the customers who trust you to help them will go a long way towards easing your mind.

Offering each and every client an umbrella not only protects those who choose to purchase the coverage. It protects your agency from liability. And it protects your book of business, since studies show that customers who have multiple policies are less likely to move their business elsewhere.

As a Big “I” member, you have access to a stand alone personal umbrella program from A+ rated carrier RLI, featuring:

� Limits up to $5 million available� You can keep your current homeowner/auto insurer� New drivers accepted - no age limit on drivers� Up to one DWI/DUI per household allowed� Auto limits as low as 100/300/50 in certain cases� Competitive, low premiums for increased limits of liability� Simple, self-underwriting application that lets you know immediately if the insured is accepted� E-signature and credit card payment options� Immediate coverage available in all 50 states plus D.C.

So cover your clients... protect your agency... and profit from umbrella sales!

To access log onto www.bigimarkets.com or visit www.iiaba.net/Umbrella.

®

Mid-America Insurance Conference makes a difference

Carol TeasleyWestrope General Agency

MAIA Technical Commitee

Nov. 7, 2011, a panel consisting of independent agents and representatives from the Insurance Services Office, ACORD, the National Coalition on Compensation Insurance and insurer guests came together to make a difference on policy forms and endorsements.

As a first time attendee, I was unsure what to expect. I was given a large packet of agenda items to review prior to the conference. What was I getting myself into? Forms, endorsements and people who actually read them? The entire process, as well as the reminder that there are agents in the world who care about their clients and put in so much extra work to make a differ-ence in policy wording, pleasantly surprised me.

The first day of the conference split the agent panel and the carrier and representative panel into two rooms. I was in the agent panel room. The first order of business was changes in the bylaws of the Mid-America Insurance Confer-ence Committee. It was announced that after 20-plus years, MAIA would be handing the reigns of the conference over to the Texas as-sociation. New bylaws to increase the board by one member, change the voting structure to add states, increase the treasurer’s term to four years, and add Florida and New York to the committee were all passed.

The forum transitioned to the meat of the conference: form change submissions, recom-mended coverage enhancements and updates from prior submissions. The panel reviewed all items, gave opinions, made changes, and then either assigned items to be presented to ISO, NCCI, ACORD and the companies or decided to drop the submissions.

I was impressed by the hard work and passion that the agents put into their submissions. Not only did they research the forms or problems they perceived and give solutions, but they also had examples ready from personal situations that their clients have faced.

After the meeting, there was a social gather-ing, and then attendees split off to have dinner.

It was time to get to know other attendees, dis-cuss agenda items further, and listen and learn. Everyone attending was extremely hospitable and welcoming. Any questions I had about why I was there and what I had gotten myself into disappeared.

On day two, the fun really began. The entire panel met to hash out the requests. Though there was witty banter at times, the day went smoothly, and in the end, ISO agreed to address eight of the 40 items that were on the agenda for discussion.

Agenda items that were addressed are sum-marized below.

Professional Liability endorsementsThe first submission addressed concerns about various aspects of ISO’s Professional Liability endorsements. Problems with care, custody or control for funeral homes and veterinarians, and expanded services provided by pharma-cists and hair salons were discussed. Gaps in coverage under ISO’s forms for these profes-sions were noted. Although technically it was dropped, ISO advised that it had already de-cided to change the professional liability form for pharmacists to provide coverage for giving vaccinations. Though this did not address every-thing noted in the submission, a change is being made and filed for a portion of the submission.

Additional Insured – Building Owner CP1219 06/07The agent who submitted this item was con-cerned over the form title. It reads, “Additional Insured,” yet the wording names the building owner as a named insured. The submission states, “It’s imperative to be clear when deal-ing with these descriptions, lest the public and plaintiff attorneys get even more confused by ISO’s own description, which could be used to open up the lid that merges the two.” ISO agreed and will change the form after review and filing with the states.

technicalities

continued on page 16

16 missouriagent january-february 2012

Rights of recovery under employee dishonestyIt was suggested that an employee dishonesty recovery exception be added to the Busines-sowners form BP0030 similar to the exception in the Commercial Crime forms CR0029 and CR0029. The BOP form allows for all rights of recovery to first go to the insurance company instead of the insured, while the crime forms do not. After review of all forms and discussion with panel members, ISO has decided to create such a form.

Water Damage Endorsement BP 01 59 08 08An update originally submitted from the 2009 conference was passed. This one was regarding the Water Exclusion endorsement. The intent of the form was questioned. Was the intent to negate coverage for the accidental bursting of a plumbing system that causes damage to an insured’s premises? Carriers were asked their opinion, and one said yes, while one said no.

After many panel advisories discussed this is-sue, ISO agreed a change should be made and expects the filing to have been made fourth quarter 2011.

Business Auto Policy “actual cost new” Also in 2009, an issue was brought to the panel’s attention regarding the Business Auto Physical Damage Coverage declarations page CA DS 15 10 01. Most carriers issue the BAP schedule of vehicles to include the “cost new” within the de-scription of the autos. However, the ISO declara-tion page defines the limit for commercial autos as actual cash value.

This causes confusion, as policyholders may perceive that they are paying premium on a cost new, or that they will be paid a cost new as a re-sult of the claim.

A change was requested to replace “actual cost new” with “actual cash value” on the decla-rations pages and related vehicle schedules. This would eliminate confusion and enable agents to

technicalities continued from page 15

january-february 2012 missouriagent 17

www.ilcasco.com

Restaurants Fine Dining

Fast Food Delivery Taverns

Wineries Nightclubs

Banquet Facilities Convenience Stores

Fraternal Organizations

Food and Beverage Insurance Specialists

spend less time explaining obscure policy defini-tion to the policyholder.

In 2009, ISO did not agree that the wording was an issue. After further discussion in 2010, ISO agreed to meet with an advisory commer-cial auto panel of insurers and determine its position. This year, ISO advised it will remove the cost new/used wording and to expect the change mid-2013.

Business Auto Policy “business income” The Business Auto Policy has another significant change that was approved. In 2009, it was sug-gested to add a Loss of Income or Down Time Coverage similar to the property coverage for Business Income and Extra Expense coverage. Where income is derived from the vehicle and the loss of the use of the vehicle would create a loss of income, there is currently no way to add coverage for this exposure.

An expected date was not given; however, ISO did advise that it agrees and is working with panels to write a form.

Debris removal broadening endorsement A concern about the debris removal limit and the fact that the 25 percent-of-loss limit is not an additional amount of insurance was first introduced in 2002. Although ISO was not willing to make an endorsement available to change the 25% limit to additional limits, it did announce that is has agreed that the debris removal limit will be increased to $25,000 in lieu of the current $10,000 limit. This request went through several committees and panels before being approved.

Total Pollution Exclusion CGL This was originally submitted in 2007. The CG 21 98 12 07 Pollution Exclusion form applies to all products and completed operations. Per the submission, a total pollution exclusion on prod-ucts and completed operations does not allow for the insurer or insured to exclude a specific

product or completed operations. For example, if there is only one operation that the under-writer wants to exclude and the other opera-tions are acceptable, there is no option or room for negotiation.

After four years of updates and discussions, ISO has finally agreed to create an endorse-ment, which will give the carrier and client op-tions to exclude specific pollution items.

The conference came to a close, and everyone headed home. As I drove home, I felt very hon-ored to have been amidst colleagues who saw issues and did not just pass them off as some-thing that could not be changed. They took their ideas and created a request for a change, and in the end, they made a difference in insur-ance policies for their clients.

If you would like to make a difference, please contact any member of the MAIA Technical Committee. They are here to help you and are glad to work with you to get your submissions on the floor of the next Mid-America Insurance Conference.

Carol Teasley, CSR, is a commercial lines produc-tion underwriter with Westrope General Agency, Overland Park, Kan. She joined the MAIA Technical Committee in 2011.

MAIA WInter events

regIster onlIne At WWW.MIssourIAgent.org.

Small Agency ConferenceMarch 22-23, 2012, Holiday Inn, Columbia

Featuring

Dr. Jason Selk, LPC, NCC, uses his in-

depth knowledge and experience

of working with the world’s finest

business leaders, organizations and

athletes to help you develop the

mental toughness needed for high-

level success.

Benefits

• Unparalleled Networking

• Education For Small Agencies

• Experienced Instructors

• Giant Trade Show

• Optional E&O Seminar (6 Hrs CE)

• Up to 6 CE Credits, Pending

About the Conference

If your agency is small to mid-sized

and is looking for edcuation and

networking opportunities, this is

the conference for you. The Small

Agency Conference is designed to

be useful to all agency employees,

from CSRs to principals.

Day at the CapitolMarch 7, 2012, Capitol Plaza Hotel, Jefferson City

What Is It?

MAIA members and friends come to-

gether to discuss topics in the state

legislature that affect our industry.

After getting briefed on the issues,

agents have time to visit their Sena-

tors and Representatives at the

state Capitol.

Why Does It Matter?

Each year, the Missouri General Assem-

bly passes new laws that change the

way producers do business. Day at the

Capitol is a chance to educate yourself

and your leaders on the effects those

laws have on the Missouri insurance in-

dustry and its consumers.

Who Can Come?

Day at the Capitol is free to all

MAIA members. We ask only that

you register in advance. Your repre-

senatives want to hear from their

constituants at home. This is your

chance to be their insurance indus-

try experts.

1ce

credit pending

6 ce

credits pending

Risk Specialist Series: Insuring Public EntititesJanuary 25-26, 2012, MAIA Headquarters, Jefferson City

The Course

This course outlines the foundation

of essential risk practices for gov-

ernmental and other public entites.

It gives producers a solid grasp of

the insurance issues involving the

public, public employees and public

entity property.

The Instructor

Michael G. Fann, ARM-P, MBA, is the di-

rector of loss control at TML Risk Man-

agement Pool and owner of Gannon

Risk Solutions, founded in 2009. In his

role at TML, Fann provides loss control

assistance to more than 35,000 goven-

mental employees.

Topics to be Covered

• Areas of Exposure

• Public Entity Risk Control Basics

• Claim Management Issues

• The Basis for Liability

• Workers’ Compensation

• Special Concerns

12p-c ce

credits

january-february 2012 missouriagent 19

The million dollarMAIA WInter events

regIster onlIne At WWW.MIssourIAgent.org.

Small Agency ConferenceMarch 22-23, 2012, Holiday Inn, Columbia

Featuring

Dr. Jason Selk, LPC, NCC, uses his in-

depth knowledge and experience

of working with the world’s finest

business leaders, organizations and

athletes to help you develop the

mental toughness needed for high-

level success.

Benefits

• Unparalleled Networking

• Education For Small Agencies

• Experienced Instructors

• Giant Trade Show

• Optional E&O Seminar (6 Hrs CE)

• Up to 6 CE Credits, Pending

About the Conference

If your agency is small to mid-sized

and is looking for edcuation and

networking opportunities, this is

the conference for you. The Small

Agency Conference is designed to

be useful to all agency employees,

from CSRs to principals.

Day at the CapitolMarch 7, 2012, Capitol Plaza Hotel, Jefferson City

What Is It?

MAIA members and friends come to-

gether to discuss topics in the state

legislature that affect our industry.

After getting briefed on the issues,

agents have time to visit their Sena-

tors and Representatives at the

state Capitol.

Why Does It Matter?

Each year, the Missouri General Assem-

bly passes new laws that change the

way producers do business. Day at the

Capitol is a chance to educate yourself

and your leaders on the effects those

laws have on the Missouri insurance in-

dustry and its consumers.

Who Can Come?

Day at the Capitol is free to all

MAIA members. We ask only that

you register in advance. Your repre-

senatives want to hear from their

constituants at home. This is your

chance to be their insurance indus-

try experts.

1ce

credit pending

6 ce

credits pending

Risk Specialist Series: Insuring Public EntititesJanuary 25-26, 2012, MAIA Headquarters, Jefferson City

The Course

This course outlines the foundation

of essential risk practices for gov-

ernmental and other public entites.

It gives producers a solid grasp of

the insurance issues involving the

public, public employees and public

entity property.

The Instructor

Michael G. Fann, ARM-P, MBA, is the di-

rector of loss control at TML Risk Man-

agement Pool and owner of Gannon

Risk Solutions, founded in 2009. In his

role at TML, Fann provides loss control

assistance to more than 35,000 goven-

mental employees.

Topics to be Covered

• Areas of Exposure

• Public Entity Risk Control Basics

• Claim Management Issues

• The Basis for Liability

• Workers’ Compensation

• Special Concerns

12p-c ce

credits

One question. One simple little question that if answered consistently could be worth millions, not to mention improved happiness and health. Before I give you this powerful question, let me explain why this question will literally change your life. In 2006, after just helping the St Louis Cardi-nals win their first world championship in 20 years, I was asked to identify the psychological characteristics that would help the team select future draftees with the greatest poten-tial for high-level success. While searching for the magical combination of mental make-up, I stumbled across the importance of optimism. Many researchers consider optimism, the ability to focus on solutions especially in the face of adversity, as the key to improved health, happi-ness and success.

For years we have heard the importance of “be positive,” but prior to this one little ques-tion, very few knew exactly how to be optimis-tic and positive. Granted, being positive is ab-normal; the truth is our minds are built in a way that it is easier to focus on problems than it is to emphasize solutions.

When I present this topic to large groups, I illustrate the point by showing a photograph of a beautiful desert landscape with majestic snow-cap mountains in the background, with an oil pipeline running through the middle of the photo. I take the photo down and ask at-tendees to write down what they remember most, at which point 90 percent list the pipeline as the most remembered item.

We see and focus on that which is wrong instead of seeing all the positive and good. The tendency to emphasize problems is something I call PCT, “problem centric thought.” PCT is the biological reason why being positive is so difficult.

The great news is that we have the capacity to train ourselves to overcome PCT and become optimistic. The key to optimism lies in the simple question: What is one thing I can do differently that could make this better?

Jack Welch, GE’s former boisterous boss, cre-ated an equation of human characteristics to

Dr. Jason Selk

Join us at the 2012 Small Agency Conference for more great motivational tips from Dr. Jason Selk. See the next page for more details.

continued on page 31

identify potential leaders, which was used as hiring methodology at GE. For years, Welch used the 4E+P equation (Energy + Energizer + Edge + Execution + Passion) in determining who had the metal edge to succeed on the GE execu-

tive team. Considering that

the average CEO earns $10,408,054 annually, whereas the annual income for a non-executive is $50,233, a leader-ship position seems rather enticing.

With Welch’s leadership equation in mind, there is, of course, a method of learning how to develop the 4E+P characteristics. Accord-ing to researchers like Daniel Goleman (author of Emotional Intelligence), the most effective method of developing Welch’s traits and leader-ship capabilities is to hone in on becoming more optimistic. Optimism appears to be the key trait for increasing success, happiness and health.

Additional research suggests that modeling a positive attitude reduces injury and sickness by 30% and can even extend a person’s life by 14 years. In his groundbreaking book Learned Optimism, Dr. Martin Seligman outlines how optimism undoubtedly impacts an indi-vidual’s ability to improve many of the very characteristics that Jack Welch and other employers look for in job applicants.

The good news: We all have the capacity for change. We are able to overcome our human tendency to focus continuously on problems and actually become solu-tion focused and optimistic simply by answering the question, “What is one thing I can do differently that could make this better?” every time we catch ourselves thinking negatively.

Be sure to follow a few guide-lines when using the million dollar question:

• The + 1 concept: Focus on improving, not per-fecting. You do not need complete resolution of the problem. You only need improvement. Consistent improvement over time leads to

question

specialfocus smallagencyconference

20 missouriagent january-february 2012

thursday

specialfocus smallagencyconference

2012

Keynote sessionRelentless Solution Focus: The Ultimate Measure of Mental ToughnessSpeaker: Dr. Jason SelkThursday, March 22, 8:30 a.m.

Learn to use the tool that allows individuals to overcome all obstacles of achieve-ment. Relentless solution focus is a concrete and proven method of increasing individual health, happiness and success, and by extension, it pro-duces organizations that are healthier, happier and more successful. Your organization will once and for all develop the collective positive mindset needed to outperform the competition.

Dr. Jason SelkEnhanced Performance Inc., St. Louis

Dr. Jason Selk, LPC, NCC, is the director of mental training for the St. Louis Cardinals and best-selling author of 10-Minute Toughness and Executive Toughness. Selk is a regular contributor to ABC, CBS, ESPN, and NBC radio and television, and has been featured in USA Today, Fitness, Men’s Health, Muscle and Fitness, and Shape magazines.

Selk utilizes his in-depth knowledge and experience of working with the world’s finest business leaders, athletes and coaches to help individuals and organizations develop the mental toughness needed for high-level success. His first book, 10-Minute Toughness, is on pace to be one of the best-selling sport psychology books of all time, and his second book, Executive Tough-ness: The Mental Training Program for Increasing Leadership Performance, was released in book stores across the country in November 2011.

Dr. Selk has experience providing services for the following clients: Anheuser-Busch, Edward Jones, Charles Schwab, Enterprise Holdings, Northwestern Mutual, Wells Fargo, the NCAA, the St. Louis Cardinals, USA Gymnastics, the St. Louis Rams and numerous other professional ath-letes and organizations.

Thursday morning sessionLegislative Update DIFP Director John M. HuffThursday, March 22, 10:15 a.m.

Join John M. Huff, director of the Missouri De-partment of Insurance, Financial Institutions and Professional Registration, as he discusses issues

Mitch Holthus chats with Mark Baker and Dawn Oney after the 2011 keynote session.

MAIA’s Small Agency Conference is designed for small to mid-sized agencies and is a benefit to everyone in the

agency, including the agency managers, producers and CSRs. It offers smaller agencies a compact and meaty

schedule with an array of education topics and unparalleled networking opportunities. A huge trade show, and the

optional errors and omissions seminar and Crawfish Feast round out the experience.

Small AgencyConference

Multi-conference discountAny MAIA member agency that registers an employee for the Small Agency Conference will receive a 15 percent discount off one full registration for the this summer’s 2012 Leader-ship Conference.

Note: The discount is for agents only, is transferrable within the agency and is limited to one per agency.

Network at our company reception and trade showWith more than 95 exhibitors expected, the trade show at the Small Agency Conference will provide more information, knowledge and business opportunities for small agencies than you’ll find anywhere else. This is an outstand-ing opportunity to network with other agents, to establish or strengthen company relation-

ships, and to find out what the excess and surplus lines market has to offer. Watch our website, www.mis-souriagent.org, for an up-to-date list of exhibitors.

january-february 2012 missouriagent 21

friday

thursday

specialfocus smallagencyconference

that impact you and your agency. Director Huff will provide insight into legislative actions, de-partment initiatives and regulatory activities, as well as his perspective on current industry issues and how they affect our insurance market.

CE credits filed and pending

Thursday afternoon concurrent sessionsCommercial Lines: Are Those Losses Covered?Jerry Milton, CICThursday, March 22, 12:45 and 2:45 p.m.

Each loss that will be reviewed is an actual loss for which the insurer denied coverage. We will review the loss and discuss the reasons for denial by the insurer. We will then determine if that loss should be covered by the insured’s cur-rent or past policies. If the loss was not covered, we will identify how the loss could have been covered. Finally, we will review the eventual outcome of each case: settlement by the insurer, coverage granted or denied by the courts, or errors and omissions claim against the agent.

Approved for 2 property-casualty CE credits in Mo. and filed in Kan.

Electronic Communication Without ElectrocutionLisa Burnside, CIC, CPCU, MOUSThursday, March 22, 12:45 and 2:45 p.m.

This class will discuss the different types of electronic communication used in the insurance industry. Proper e-mailing, instant and text messaging, anti-spam regulations, and social networking will be covered to help you under-stand how to use electronic communication effectively, as well as how to reduce errors and omissions exposure.

Personal Lines Insurance: The Art of CommunicationsCharles Hembree, CIC, CPIAThursday, March 22, 12:45 and 2:45 p.m.

Many consumers view personal lines as a commodity. Are you helping further this view-point in the way that you communicate with and provide service for your clients? Join us as we look at how we can dispel this position by being the trusted advisors that independent insurance agents need to be. We’ll also look at some coverage issues that will help our insureds see the difference between an insurance seller

of a commodity and an in-surance professional selling quality personal protection.

Approved for 2 property-casualty CE credits in Mo. and filed in Kan.

Friday morning sessionContracts and Leases: What’s Insurable and What’s NotJerry Milton, CICFriday, March 23, 8:30 a.m.

A contract is an agreement between two or more parties, which creates certain obligations. The contract not only obligates a person to do or not do something, but it also transfers the obligation to pay for the financial consequences of certain losses from one party (the indemni-tee) to another (the indemnitor). The indem-nitee will require the indemnitor to purchase certain policies of insurance and provide proof of the required insurance. We will review these

Randy Baker discusses technology with Roy Overacre in the Idea Lab.

continued on page 22

Optional Wednesday eventsE&O Loss Control Seminar 2012

Crawfish Feast

22 missouriagent january-february 2012

specialfocus smallagencyconference

requirements and discuss the obligations that can be covered by the indemnitor’s insurance, as well as those that cannot be covered.

Approved for 3 property-casualty CE credits in Mo. and filed in Kan.

Speaker biosLisa Burnside, CIC, CPCU, MOUSBurnside Dynamics, Forest Lake, Minn.

Lisa Burnside is president of Burnside Dynamics and a partner in 4 Dynamic Women, both provid-ing dynamic presentations to various organiza-tions. She got her start in the industry in 1981, working with her father at Valley View Insurance Agency, Edina, Minn. Two years later, the family opened its own agency, Administrative Safety Services. In 2008, Burnside founded Burnside Dy-namics. She currently speaks across the country on insurance and technology topics.

John M. HuffDIFP, Jefferson City

John M. Huff was appointed as director of the Department of Insurance, Financial Institutions and Professional Registration in 2009 by Gov. Nix-on. Huff’s initial start in the industry was practic-ing insurance law in the ‘90s in Kansas City. Fol-lowing that, he served as a global claims leader for GE Insurance Solutions and later joined the management team at Swiss Re. Huff understands the workings of the industry and believes in an open and common sense approach to governing.

Jerry Milton, CICOrange Beach, Ala.

Jerry Milton makes his living in the insurance industry by teaching and consulting. He is also recognized by the legal profession as an expert on insurance coverages. His insurance experi-ence includes company, agency and association employment. Milton has addressed insurance groups in all 50 states, Puerto Rico and the Virgin Islands. In addition to teaching, consulting and working with the legal profession, Milton works with the CISR, CIC and other programs.

Charles Hembree Jr., CIC, CPIAClark-Lami-Hembree, St. LouisCharles Hembree Jr. is president and CEO of Clark-Lami-Hembree Insurance. He joined the firm in 1982, become president in 1995 and CEO in 2000. He now divides his time between sales, agency management and insurance technical instruction in the Midwest. Hembree is a national faculty member for the Certified Insurance Ser-vices Representative program. He is also a past president of MAIA.

Conference AgendaWednesday, March 21 (Optional Events) 10 am – 5 pm (Optional) E&O Loss Control Seminar Holiday Inn, Columbia Speaker: Lisa Burnside Approved for 6 ethics CE credits in Mo.

5 – 7:30 pm (Optional) Crawfish Feast (Knights of Columbus, 2525 N. Stadium,

Columbia) Sponsored by the MAIA Young Agents

Committee

Thursday, March 22 7:30 am Registration Opens Continental Breakfast

7:30 am – 5 pm Idea Lab Open For appointment, contact Sheryl at

8:30 – 10 am Opening Session: The Ultimate Measure of Mental Toughness

Speaker: Dr. Jason Selk

10:15 – 11:15 am Legislative Update Speaker: John M. Huff CE credit filed and pending

11:30 am – 12:45 pm Lunch and Conferment Ceremony

12:45 – 2:30 pm CONCURRENT SESSIONS Commercial Lines: Are These Losses

Covered? Speaker: Jerry Milton Approved for 2 p-c CE credits in Mo. -OR- Personal Lines Insurance: The Art of

Communications Speaker: Chuck Hembree Approved for 2 p-c CE credits in Mo. -OR- Electronic Communication Without

Electrocution Speaker: Lisa Burnside

2:45 – 4:30 pm Repeat Concurrent Sessions

4:30 – 8 pm Company Reception and Trade Show (Booths open 4:30-8 p.m. Prizes announced

at 7:30 p.m. You must be present to win.)

Friday, March 23 8 – 8:30 am Continental Breakfast 8:30 – 11:15 am Contracts and Leases: What’s Insurable and

What’s Not Speaker: Jerry Milton Approved for 3 p-c CE credits in Mo.

2012Small AgencyConference continued

january-february 2012 missouriagent 23

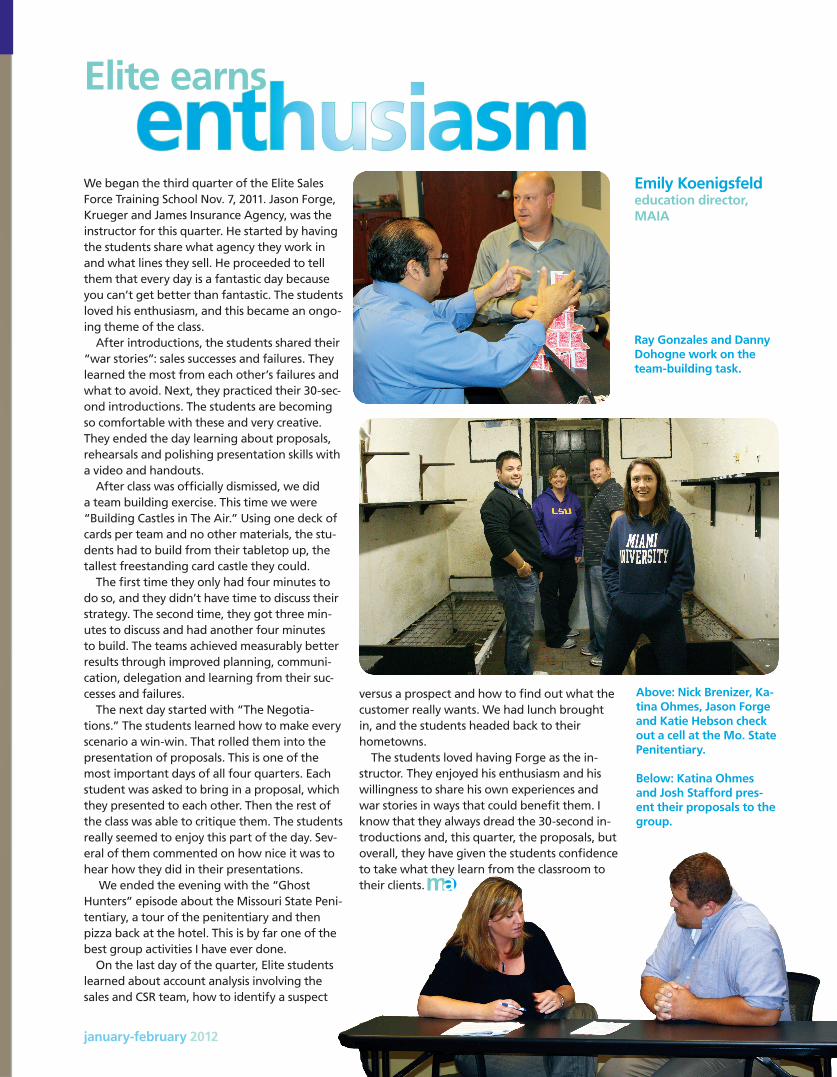

Elite earns

We began the third quarter of the Elite Sales Force Training School Nov. 7, 2011. Jason Forge, Krueger and James Insurance Agency, was the instructor for this quarter. He started by having the students share what agency they work in and what lines they sell. He proceeded to tell them that every day is a fantastic day because you can’t get better than fantastic. The students loved his enthusiasm, and this became an ongo-ing theme of the class.

After introductions, the students shared their “war stories”: sales successes and failures. They learned the most from each other’s failures and what to avoid. Next, they practiced their 30-sec-ond introductions. The students are becoming so comfortable with these and very creative. They ended the day learning about proposals, rehearsals and polishing presentation skills with a video and handouts.

After class was officially dismissed, we did a team building exercise. This time we were “Building Castles in The Air.” Using one deck of cards per team and no other materials, the stu-dents had to build from their tabletop up, the tallest freestanding card castle they could.

The first time they only had four minutes to do so, and they didn’t have time to discuss their strategy. The second time, they got three min-utes to discuss and had another four minutes to build. The teams achieved measurably better results through improved planning, communi-cation, delegation and learning from their suc-cesses and failures.

The next day started with “The Negotia-tions.” The students learned how to make every scenario a win-win. That rolled them into the presentation of proposals. This is one of the most important days of all four quarters. Each student was asked to bring in a proposal, which they presented to each other. Then the rest of the class was able to critique them. The students really seemed to enjoy this part of the day. Sev-eral of them commented on how nice it was to hear how they did in their presentations.

We ended the evening with the “Ghost Hunters” episode about the Missouri State Peni-tentiary, a tour of the penitentiary and then pizza back at the hotel. This is by far one of the best group activities I have ever done.

On the last day of the quarter, Elite students learned about account analysis involving the sales and CSR team, how to identify a suspect

versus a prospect and how to find out what the customer really wants. We had lunch brought in, and the students headed back to their hometowns.

The students loved having Forge as the in-structor. They enjoyed his enthusiasm and his willingness to share his own experiences and war stories in ways that could benefit them. I know that they always dread the 30-second in-troductions and, this quarter, the proposals, but overall, they have given the students confidence to take what they learn from the classroom to their clients.

Emily Koenigsfeldeducation director, MAIA

Ray Gonzales and Danny Dohogne work on the team-building task.

Above: Nick Brenizer, Ka-tina Ohmes, Jason Forge and Katie Hebson check out a cell at the Mo. State Penitentiary.

Below: Katina Ohmes and Josh Stafford pres-ent their proposals to the group.

enthusiasm

24 missouriagent january-february 2012

www.iiaba.net/Flood

Just a guppy

when it comes to selling flood?

Don’t be shy - Big “I” Flood is here to help.

FLOODIn, Above, and Outside the NFIP!

There’s a lot to understand when it comes to flood insurance. We admit it! From

changing flood zones to determining the best level of protection for our client,

there is a lot to navigate. So even though you’re a big fish when it comes to selling

other coverages, flood can make you feel like a guppy! But don’t let this prevent

you from offering flood coverage to your clients. We’re here to help you

understand and sell flood.

Big “I” Flood provides:

ACCESS - In, Above & Outside of the NFIP!

EDUCATION - Classroom CE or the new Flood Learning Center on VU

ADVOCACY - Representation on Capitol Hill & NFIP advisory committees

Learn more at www.iiaba.net/Flood, or contact Big “I” Flood Program Manager

Linda Mackey at [email protected] or (800) 221-7917. Let us explain how we

operate in, above, and outside the NFIP!

january-february 2012 missouriagent 25

www.iiaba.net/Flood

Just a guppy

when it comes to selling flood?

Don’t be shy - Big “I” Flood is here to help.

FLOODIn, Above, and Outside the NFIP!

There’s a lot to understand when it comes to flood insurance. We admit it! From

changing flood zones to determining the best level of protection for our client,

there is a lot to navigate. So even though you’re a big fish when it comes to selling

other coverages, flood can make you feel like a guppy! But don’t let this prevent

you from offering flood coverage to your clients. We’re here to help you

understand and sell flood.

Big “I” Flood provides:

ACCESS - In, Above & Outside of the NFIP!

EDUCATION - Classroom CE or the new Flood Learning Center on VU

ADVOCACY - Representation on Capitol Hill & NFIP advisory committees

Learn more at www.iiaba.net/Flood, or contact Big “I” Flood Program Manager

Linda Mackey at [email protected] or (800) 221-7917. Let us explain how we

operate in, above, and outside the NFIP!

News and reflectionsNew service offers help finding lost life insurance policiesThroughout the years, our department has frequently received inquiries from consumers about how to locate missing life insurance poli-cies or annuity contracts. For example, a man’s elderly mother passes away. He knows she had life insurance but has no policy in hand and doesn’t even know the name of the carrier. Until now, there was very little the department could do to help.

In November, we announced the Life Policy Locator, a service that gives consumers a way to contact licensed life insurance companies about lost policies or annuity contracts purchased in Missouri. After a consumer submits a request form and some other information, we will send it electronically each month to licensed life in-surance companies in Missouri.

Once a positive identification has been made, the insurance company that issued the life insur-ance policy or annuity contract will contact the beneficiary or beneficiaries about benefits they are entitled to receive.

So far, insurers representing about 90 percent of state premium volume have signed on to this voluntary program. We are aware of two other states offering a similar program: Ohio and Louisiana. Ohio is reporting a better-than 50 percent success rate on locating policies.

This type of service would not be possible without technology, as hard-copy mailings to each licensed life insurance company would be inefficient and costly for the department.

Time to socialize?With the New Year upon us, it’s a good time to remind agents that another crop of young adults will soon be ready to venture out into the world to make their own mark. A number of those young adults will be looking at pur-chasing insurance for the first time. And it’s no secret that they’ll be looking for ways to save their money.

A member of our communications team re-cently attended a State Farm marketing and sales competition at the University of Central Missouri. Marketing students from universities across the country offered plans to sell insur-

ance products to their age group. Their obser-vations were eye opening for us here at the department, and I want to share some of them with you.

Social media, like Facebook and Twitter, were at the forefront in these young adults’ minds. These outlets are the first places they turn for information on just about everything, includ-ing what products to buy. They were clear in saying they wouldn’t want to be “friends” with an insurance agent on Facebook, but at the same time, they want an online connection so they can reach out to agents when needed. An agency’s fan page could accomplish this, as would allowing people to “follow” you on your Twitter account.

These social media sites are generally a free avenue for agents to get some name recogni-tion, especially in their local communities. When you are able to interact with people on the same platform they use in everyday life, it can make a difference when they begin shopping for insurance.

We also observed that people in this age group like, at least on the surface, the idea of using direct writers offering toll-free and online quotes, and often times haven’t considered going through a local agent. So agencies have some selling to do in this regard. We at the de-partment will continue to encourage consumers to consult a qualified, local agent to help them make informed choices.

Other popular insurance trends among these young adults were pay-as-you-drive auto insur-ance and programs that monitor driving habits and reward safe drivers with discounts. Those savings are beneficial to college students who may not drive very much throughout the year and need the extra money for other college expenses. We are seeing more insurers offer-ing these customer-driven programs across the country, as I’m sure you are too.

I wish you the best of success for a prosperous year and thank you for your service to Missouri consumers.

John. M. Huffdirector, Mo. Department of Insurance, Financial Institutions and Professional Registration

This article expresses the official views and opin-ion of the Missouri De-partment of Insurance, Financial Institutions and Professional Registration, which may not necessar-ily be those reflected by the Missouri Association of Insurance Agents.

fromtheDIFP

26 missouriagent january-february 2012

2011 CSR

The first annual CSR Development Conference drew nearly 60 participants to Jefferson City in November 2011. Attendees were treated to an array of courses designed especially for customer service employees, including personality train-ing, cross-selling and time management. Instructors Angie Heavener and Cleva Moore made sure the participants took home plenty of tools to make their jobs easier and more satisfying.

Development Conference

I thought the conference was great! I loved the personality profiling and classes that went along with it. It has been very helpful in dealing with my clients and co-workers. I had the staff in my office take the tests, and we discussed the results. It was very eye-opening.CSR Development Conference attendee

Above: Trivia Night winners, Team

Butterfly

Above: CSRs tune in to the optional

ethics session.

Right: Members of Team Baseball enjoy

Trivia Night.

Directly Above: Team Racecar discusses their answers.

Left and Top: Friday breakout sessions.

january-february 2012 missouriagent 27

What is a

Remember that your brand is a relationship: the relationship between your firm and your cus-tomers and prospects. When well understood, it’s your path to new sales, growth and success. Ultimately, it’s the single-most important driver of agency value.

“We have a great relationship with our cus-tomers,” independent agents and brokers often say proudly.

Fine. But as an agency owner, do you truly understand what that great relationship re-ally means from the customer’s point of view? How it then relates to your sales and retention performance? How it translates to building and burnishing your agency value?

There is a more objective way to answer these questions. Author and sales coach Todd Young-blood, with Atlanta-based YPS Group, says we must first agree on a precise definition of the term relationship. And second, he notes, we need to measure the quality of our own busi-ness relationships. “Only then can we have an intelligent discussion about it,” he says.

Agents say clients are like their friends. But Youngblood argues that isn’t enough. “Like it or not, friendship is not particularly relevant except at the very beginning of a business rela-tionship,” Youngblood says. “In today’s highly competitive environment, relationships are grounded in how reliably you can deliver value. As value delivered increases, so does the friend-ship and vice versa.”

Youngblood offers five levels of customer relationship that provide a more objective, mea-surable way to look at your agency value with commercial accounts:

• Level 0, Hope: You have no relationship. And in your prospect or customer’s mind, you’re just another agency name rather than a strong brand.

• Level 1, Price: Your customer buys from you because of your low price. This is not a place most independent agents and brokers want to be, although it can be a foot in the door to growing accounts beyond a low-cost auto or BOP product.

• Level 2, Features and Benefits: Your customer justifies buying from you based on how the features and functions you provide fulfill his or her expectations.

• Level 3, Value Added: Justification is ground-ed in improvements to the customer’s busi-ness processes, and one of the following also is true: The customer is willing to pay a pre-

mium because of extra services you provide, or the customer always calls you first for help and gives you the last chance to bid.

• Level 4, Total Cost of Ownership: Justification for your products and services is based on a hard-dollar analysis of the impact you have on the customer’s financial statements.

Note how these levels replace the term great service, which is subjective, with a more measur-able and objective approach.

Take a sampling of your commercial accounts, and assign scores. Be brutally honest, especially with regard to a level 3 rating. If you have any doubt, drop it down to a level 2.

Review your scores every quarter. Keep driv-ing them upward.

Remember, what gets measured, gets done. Over time, you’ll see how this scoring compels you and your staff to get better. You’ll think of new ways to provide value-added services. For instance, dropping off a policy to a busy com-mercial account might seem impossible now, but when you’re trying to move from an aver-age score of 2 up to a 3 (and hopefully to a 4), it could be an obvious activity for your staff.

Go beyond great service to be a truly great brand. You can do it; you already have momen-tum. Great brands can lock clients up for life. And the best part of it is, your clients gladly will ask for handcuffs.

from TrustedChoice.com

Check out www.TrustedChoice.com/agents for more branding tips.

great relationship?

s! E&O HappenWhen that inevitable claim arises, we are your Trusted Choice® for professional liability protection.

AMC offers you a choice of the two most prestigious Errors and Omissions carriers in the country:

Agents Marketing Corporation is a subsidiary of Missouri Association of Insurance Agents

For a quote or for more information contact Theresa Flippin at [email protected] or 800/617-3658

In fact, with the two best choices in the business...

why would you trust anyone else?

Agents Marketing Corporation Your Trusted Choice®

Westport