mis titles - مقاله erp , مقاله bpm , مقاله ...abedinionline.com/docs/concept...

TRANSCRIPT

mis titlesLook for these other popular course technology

Management Information

Systems, Sixth Edition

by Effy Oz

ISBN 13: 978-1-4239-0178-5 ISBN 10: 1-4239-0178-9

Information Technology Project

Management, Fifth Edition

by Kathy Schwalbe

ISBN 13: 978-1-4239-0145-7 ISBN 10: 1-4239-0145-2

View our entire collection of products online at www.course.com/mis.

Introduction to Project

Management, Second Edition

by Kathy Schwalbe

ISBN 13: 978-1-4239-0220-1 ISBN 10: 1-4239-0220-3

Information Technology in Theory

by Pelin Aksoy and Laura DeNardis

ISBN 13: 978-1-4239-0140-2 ISBN 10: 1-4239-0140-1

Problem-Solving Cases with

Microsoft Access and Excel,

Sixth Edition

by Joseph Brady and Ellen Monk

ISBN 13: 978-1-4239-0213-3 ISBN 10: 1-4239-0213-0

Database Systems: Design,

Implementation, and

Management, Eighth Edition

by Peter Rob and Carlos Coronel

ISBN 13: 978-1-4239-0201-0 ISBN 10: 1-4239-0201-7

C O N C E P T S I N E N T E R P R I S E

R E S O U R C E P L A N N I N G

Third Edition

This page intentionally left blank

C O N C E P T S I N E N T E R P R I S E

R E S O U R C E P L A N N I N G

Third Edition

Ellen F. MonkUniversity of Delaware

Bret J. WagnerWestern Michigan University

Australia • Brazil • Japan • Korea • Mexico • Singapore • Spain • United Kingdom • United States

Concepts in Enterprise Resource Planning,

Third Edition

by Ellen F. Monk and Bret J. Wagner

VP/Editorial Director: Jack W. Calhoun

Editor-in-Chief: Alex von Rosenberg

Senior Acquisitions Editor: CharlesMcCormick, Jr.

Product Manager: Tricia Coia, Kate Hennessy

Development Editor: Amanda Brodkin

Content Project Manager: Aimee Poirier

Manufacturing Coordinator: Justin Palmeiro

Marketing Manager: Bryant Chrzan

Editorial Assistant: Bryn Lathrop

Cover Designer: Laura Rickenbach

Cover Photo® 2007 JupiterimagesCorporation

Compositor: GEX Publishing Services

® 2009 Course Technology Cengage Learning

ALL RIGHTS RESERVED. No part of this work covered by the copyrighthereon may be reproduced, transmitted, stored, or used in any form or byany means graphic, electronic, or mechanical, including but not limited tophotocopying, recording, scanning, digitizing, taping, Web distribution,information networks, or information storage and retrieval systems, exceptas permitted under Section 107 or 108 of the 1976 United States CopyrightAct, without the prior written permission of the publisher.

For product information and technology assistance, contact us atCengage Learning Academic Resource Center, 1-800-423-0563

For permission to use material from this text or product,submit all requests online at www.cengage.com/permissions

Further permission questions can be emailed [email protected]

ISBN-13: 978-1-4239-0179-2ISBN-10: 1-4239-0179-7

Course Technology Cengage Learning

25 Thomson PlaceBoston, Massachusetts, 02210USA

Cengage Learning products are represented in Canada by NelsonEducation, Ltd.

For your lifelong learning solutions, visit course.cengage.com

Visit our corporate website at www.cengage.com

SAP is a registered trademark.

Printed in the United States of America

1 2 3 4 5 6 7 8 9 TW 12 11 10 09 08

In memory of our colleague Majdi Najm. His support and friendship are sorely missed.

This page intentionally left blank

BRIEF CONTENTS

zzzPreface xiii

Chapter 1

Business Functions and Business Processes 1

Chapter 2

The Development of Enterprise Resource Planning Systems 17

Chapter 3

Marketing Information Systems and the Sales Order Process 47

Chapter 4

Production and Supply Chain Management Information Systems 77

Chapter 5

Accounting in ERP Systems 117

Chapter 6

Human Resources Processes with ERP 157

Chapter 7

Process Modeling, Process Improvement, and ERP Implementation 179

Chapter 8

ERP and Electronic Commerce 211

Glossary 237

Index 245

This page intentionally left blank

TABLE OF CONTENTS

Preface xiii

Chapter 1 Business Functions and Business Processes 1Functional Areas and Business Processes 2

Functional Areas of Operation 2Business Processes 3

Functional Areas and Business Processes of a Very Small Business 6Marketing and Sales 6Supply Chain Management 7Accounting and Finance 7Human Resources 8

Functional Area Information Systems 8Marketing and Sales 8Supply Chain Management 9Accounting and Finance 11Human Resources 13

Chapter Summary 15Key Terms 15Exercises 15For Further Study and Research 16

Chapter 2 The Development of Enterprise Resource Planning Systems 17The Evolution of Information Systems 18

Computer Hardware and Software Development 19Early Attempts to Share Resources 20The Manufacturing Roots of ERP 20Management’s Impetus to Adopt ERP 21

ERP Software Emerges: SAP and R/3 23SAP Begins Developing Software Modules 24SAP R/3 24New Directions in ERP 25SAP ERP Software Implementation 29

ERP for Midsized Companies 32Responses of the Software to the Changing Market 32

Choosing Consultants and Vendors 33The Significance and Benefits of ERP Software and Systems 33Questions About ERP 34

How Much Does an ERP System Cost? 34Should Every Business Buy an ERP Package? 34Is ERP Software Inflexible? 35What Return Can a Company Expect from Its ERP Investment? 35How Long Does It Take to See a Return on an ERP Investment? 36Why Do Some Companies Have More Success with ERP Than Others? 37

The Continuing Evolution of ERP 39Additional Capabilities Within ERP 41The Internet 41

Chapter Summary 43Key Terms 43Exercises 44For Further Study and Research 44

Chapter 3 Marketing Information Systems and the Sales Order Process 47Overview of Fitter Snacker 48Problems with Fitter Snacker’s Sales Process 49

Sales Quotations and Orders 50Order Filling 51Accounting and Invoicing 53Payment and Returns 53

Sales and Distribution in ERP 54Pre-Sales Activities 54Sales Order Processing 54Inventory Sourcing 55Delivery 55Billing 55Payment 55

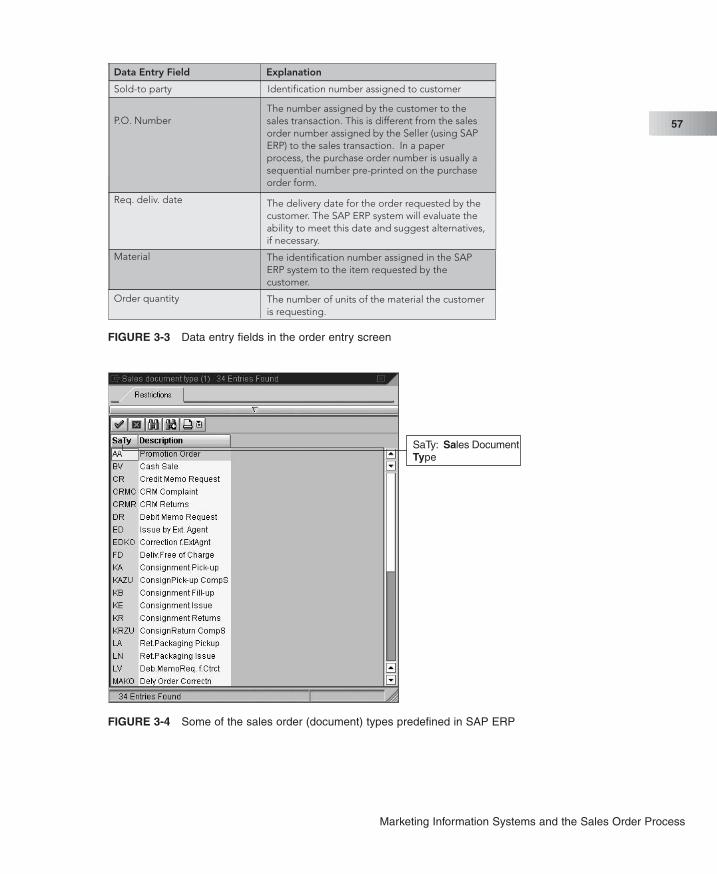

A Standard Order in SAP ERP 56Taking an Order in SAP ERP 56Discount Pricing in SAP ERP 62Integration of Sales and Accounting 64

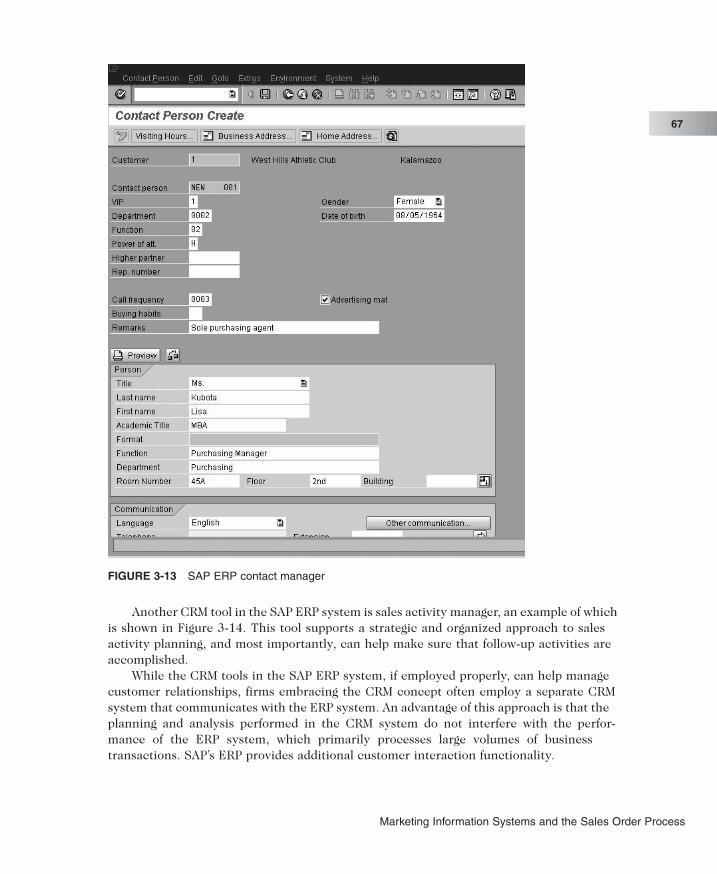

Customer Relationship Management 65Core CRM Activities 66SAP’s CRM Software 66The Benefits of CRM 71

Chapter Summary 73Key Terms 73Exercises 74For Further Study and Research 75

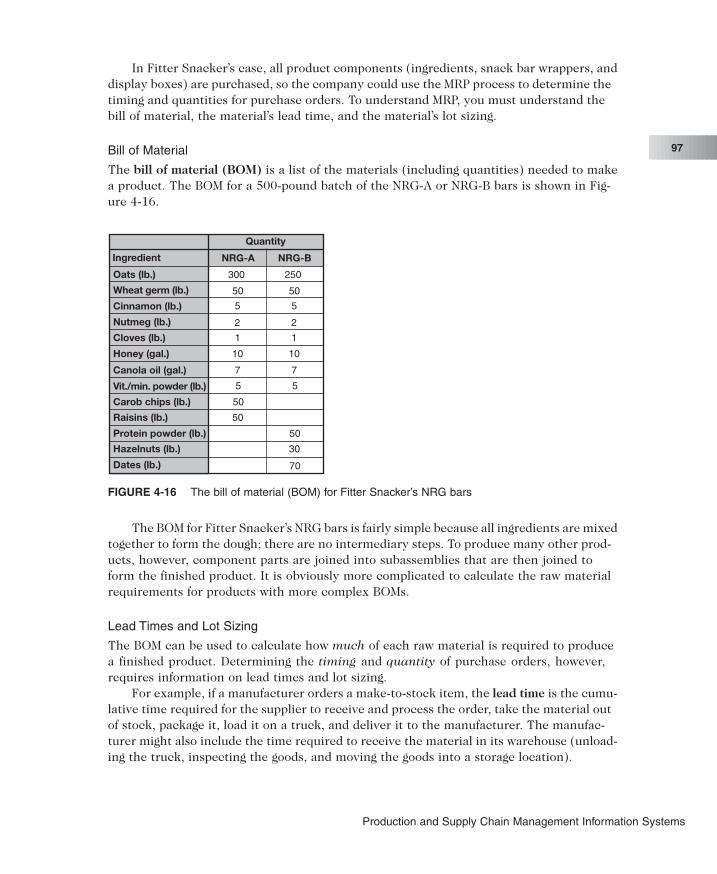

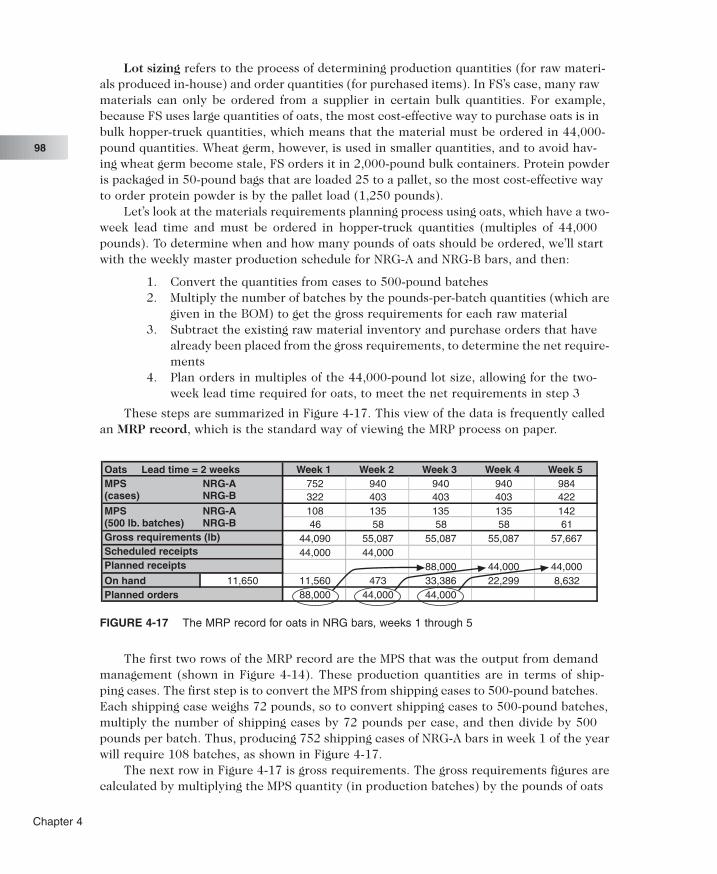

Chapter 4 Production and Supply Chain Management Information Systems 77Production Overview 78

Fitter Snacker’s Manufacturing Process 79Fitter Snacker’s Production Problems 80

The Production Planning Process 82The SAP ERP Approach to Production Planning 83Sales Forecasting 84Sales and Operations Planning 85Demand Management 95Materials Requirements Planning (MRP) 96Materials Requirements Planning in SAP ERP 100Detailed Scheduling 104Providing Production Data to Accounting 105

ERP and Suppliers 107The Traditional Supply Chain 108The Measures of Success 110

Chapter Summary 114Key Terms 114Exercises 114For Further Study and Research 115

x Concepts in Enterprise Resource Planning, Third Edition

Chapter 5 Accounting in ERP Systems 117Accounting Activities 118

Using ERP for Accounting Information 121Operational Decision-Making Problem: Credit Management 122

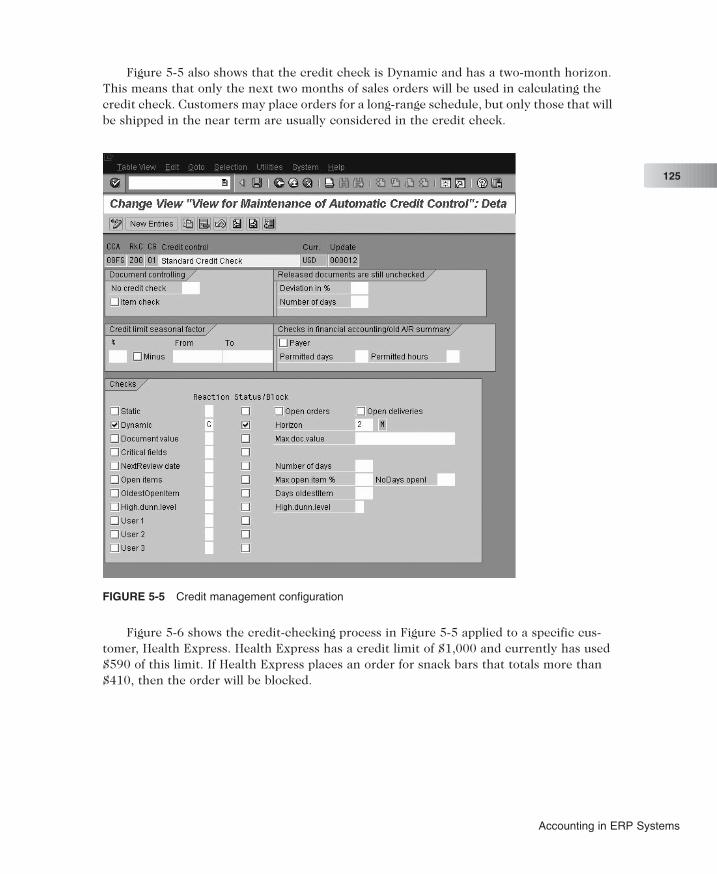

Industrial Credit Management 122Fitter Snacker’s Credit Management Procedures 124Credit Management in SAP ERP 124

Product Profitability Analysis 127Inconsistent Recordkeeping 127Inaccurate Inventory Costing Systems 128Companies with Subsidiaries 133

Management Reporting with ERP Systems 136Document Flow for Customer Service 136Built-In Management-Reporting and Analysis Tools 137

The Enron Collapse 138Outcome of the Enron Scandal 140Key Features of the Sarbanes-Oxley Act 140

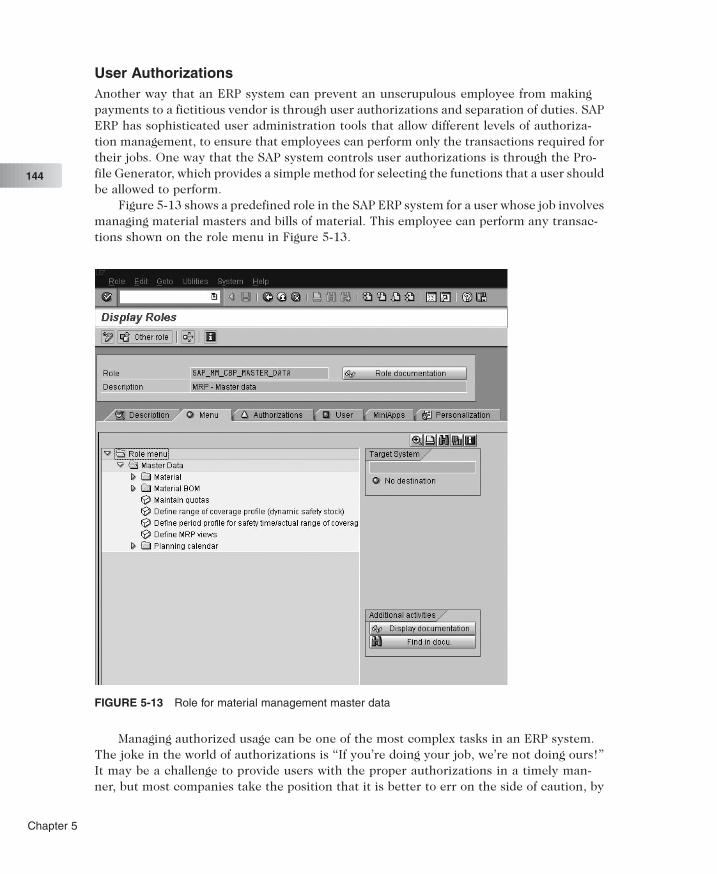

Implications of the Sarbanes-Oxley Act for ERP Systems 141Archiving 142User Authorizations 144Tolerance Groups 145Financial Transparency 146

Chapter Summary 149Key Terms 149Exercises 150For Further Study and Research 154

Chapter 6 Human Resources Processes with ERP 157Problems with Fitter Snacker’s Human Resources Processes 159

Recruiting Process 159The Interviewing and Hiring Process 160Human Resources Duties After Hiring 162

Human Resources with ERP Software 165Advanced SAP ERP Human Resources Features 170

Time Management 170Payroll 170Travel Management 171Training and Development 172

Additional Human Resources Features of SAP ERP 174Mobile Time Management 174Management of Family and Medical Leave 174Domestic Partner Handling 174Administration of Long-Term Incentives 175Personnel Cost Planning 175Management and Payroll for Global Employees 175Management by Objectives 175

Chapter Summary 176Key Terms 176Exercises 176For Further Study and Research 177

Table of Contents xi

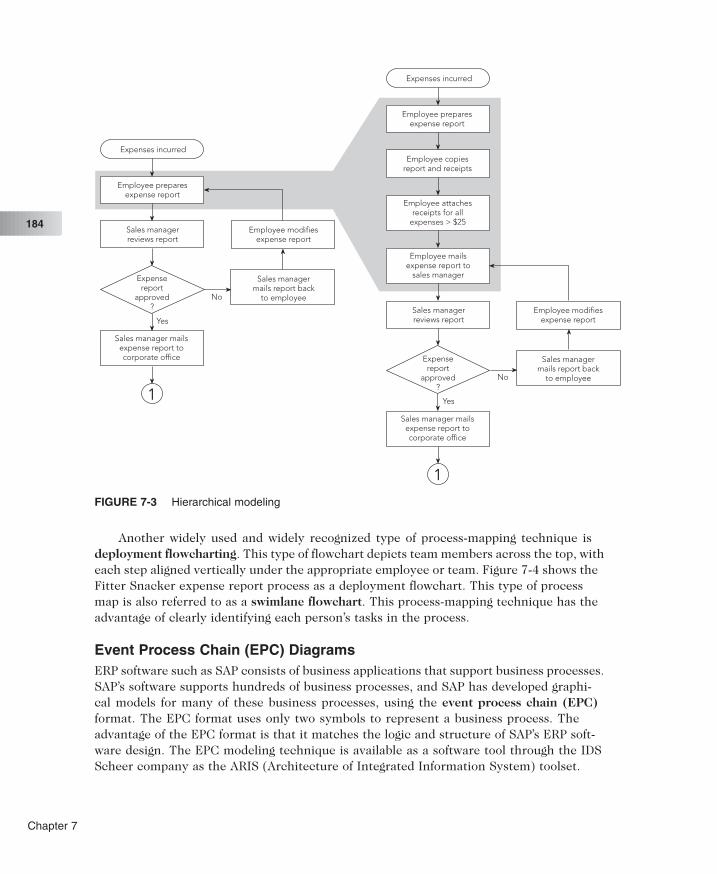

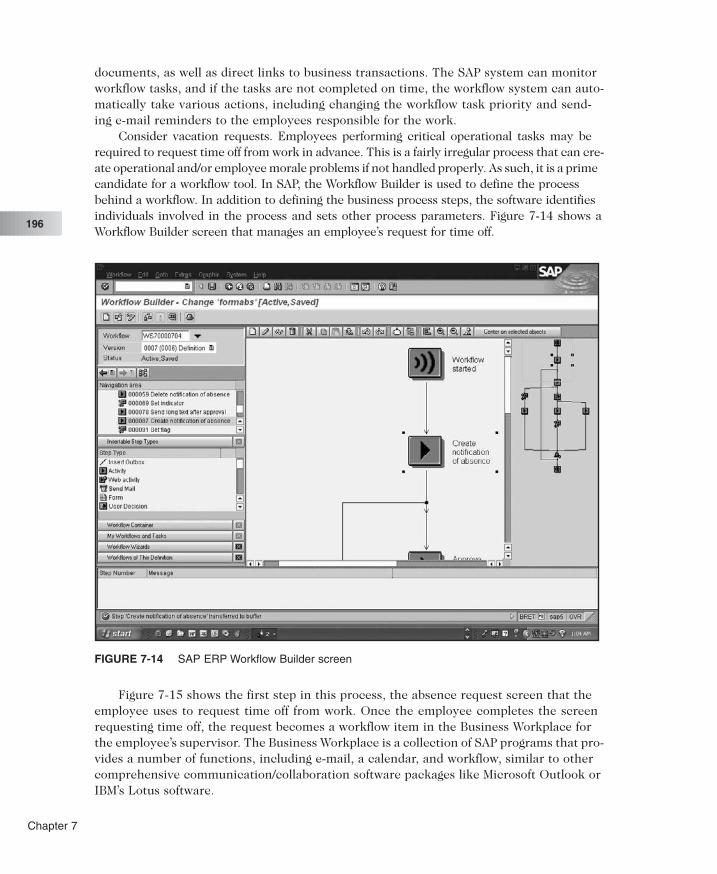

Chapter 7 Process Modeling, Process Improvement, and ERP Implementation 179Process Modeling 180

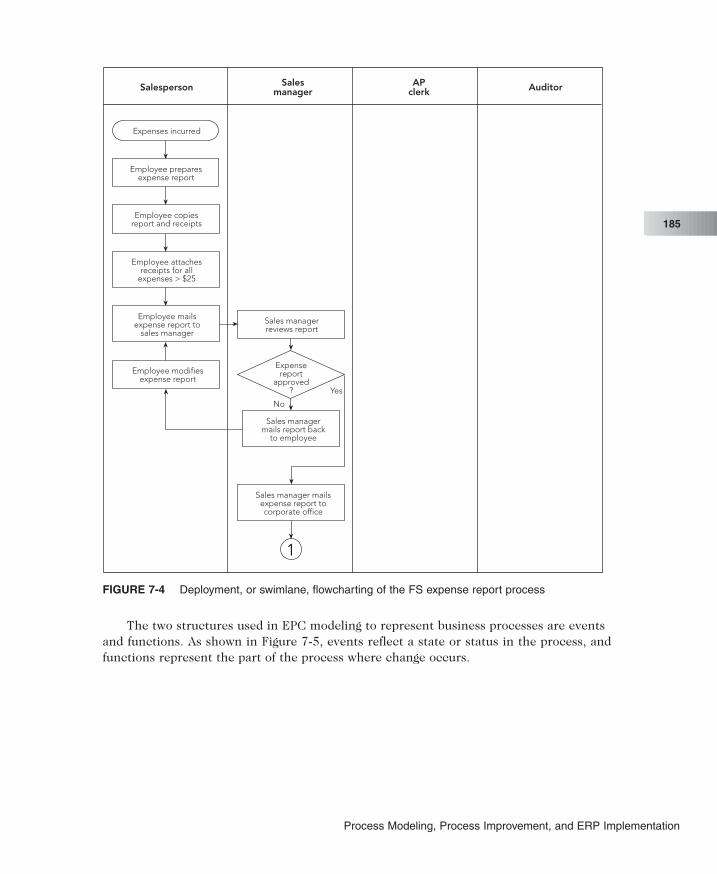

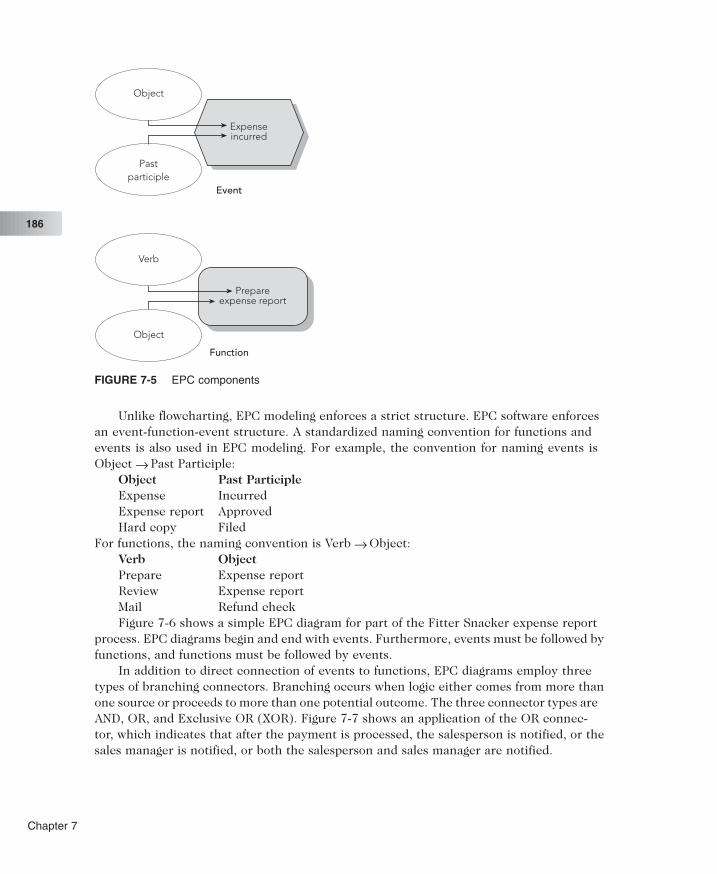

Flowcharting Process Models 180Fitter Snacker Expense Report Process 181Extensions of Process Mapping 183Event Process Chain (EPC) Diagrams 184

Process Improvement 192Evaluating Process Improvement 193

ERP Workflow Tools 195Implementing ERP Systems 198

ERP System Costs and Benefits 200Implementation and Change Management 201

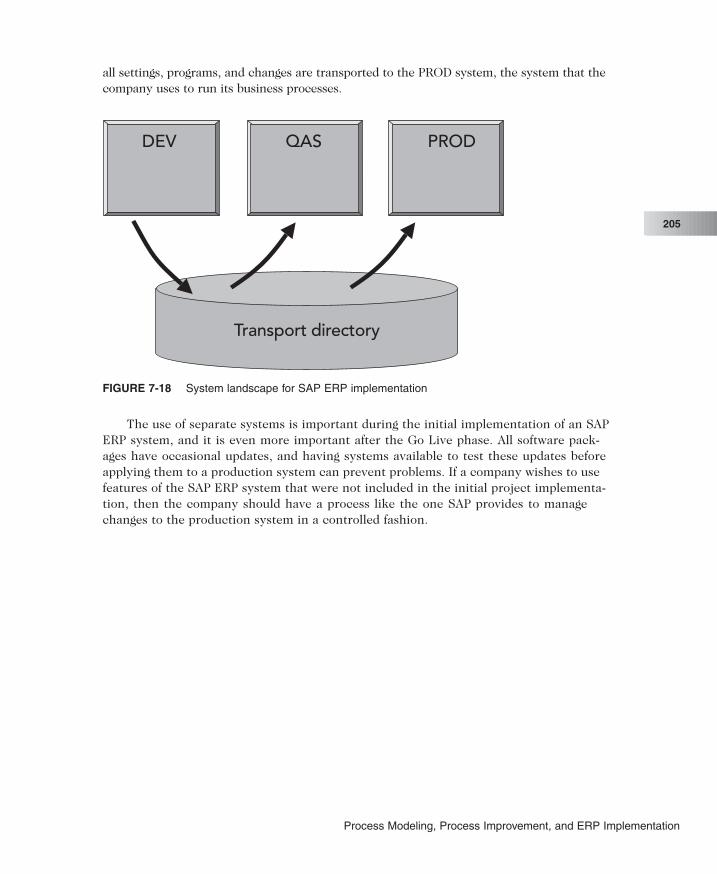

Implementation Tools 201System Landscape Concept 204

Chapter Summary 206Key Terms 206Exercises 206For Further Study and Research 210

Chapter 8 ERP and Electronic Commerce 211Electronic Commerce Background 212

Business-to-Business E-Commerce 212E-Commerce and ERP 215

Fitter Snacker and E-Commerce 216Using ERP Through an Application Service Provider 217

Application Service Providers 217NetWeaver 224

NetWeaver Tools and Capabilities 224NetWeaver at Work for Fitter Snacker 227

Duet 228Accessing ERP Systems Over the Internet 228XML 228Radio Frequency Identification Technology 230Chapter Summary 233Key Terms 233Exercises 234For Further Study and Research 234

Glossary 237

Index 245

xii Concepts in Enterprise Resource Planning, Third Edition

PREFACE

This is a book about Enterprise Resource Planning (ERP) systems; it’s also about how a businessworks and how information systems fit into business operations. More specifically, it’s about look-ing at the processes that make up a business enterprise and seeing how ERP software can improvethe performance of these business processes. ERP software is complicated and expensive. Unless acompany uses it to become more efficient and effective in delivering goods and services to its cus-tomers, the ERP system will only be a drain on company resources.

Prior to writing this book, our experience revealed that undergraduate business students don’talways understand how businesses operate, and advanced undergraduate students and even manyMBA students do not truly grasp the problems inherent in unintegrated systems. These studentsalso do not comprehend business processes and how different functional areas must worktogether to achieve company goals. As a result, students do not understand how an informationsystem should help business managers make decisions.

Consequently, we set out to write a book that does the following:

● Describes basic business functional areas and explains how they are related.

● Illustrates how unintegrated information systems fail to support business functionsand business processes that cut across functional area boundaries.

● Demonstrates how integrated information systems can help a company prosper byimproving business processes and by providing business managers with accurate,consistent, and current data.

We have found that our focus on business processes has been well received.

The Approach of This BookA key feature of our book is the use of the fictitious Fitter Snacker Company, a manufacturer ofnutritious snack bars, as an illustrative example throughout the book. We show how Fitter Snack-er’s somewhat primitive and unintegrated information systems cause operational problems. Weintentionally made the systems’ problems easy to understand, so the student could readily com-prehend them. Potential solutions for solving integration problems are illustrated using SAP’s ERPsoftware.

The third edition of Concepts in Enterprise Resource Management reflects the current stateof the ERP software market, while adding updated examples of how companies are using inte-grated systems to solve business problems and achieve greater success. The book has eightchapters:

● Chapter 1 explains the purposes for, and information systems requirements of, mainbusiness functional areas—Marketing and Sales, Supply Chain Management, Account-ing and Finance, and Human Resources. This chapter also describes how a businessprocess cuts across the activities within business functional areas and why managersneed to think about making business processes work.

● Chapter 2 provides a short history of business computing and thedevelopments that led to today’s ERP systems. Chapter 2 concludes with anoverview of ERP issues and an introduction to the SAP ERP software.

● Chapter 3 describes the Marketing and Sales functional area, and it highlightsthe problems that arise with unintegrated information systems. To make con-cepts easy to understand, the Fitter Snacker running example is introduced.After explaining FS’s problems with its unintegrated systems, we show howERP can avoid these problems. SAP ERP screens are used to illustrate theconcepts. Because using ERP can naturally lead a company into ever-broadening integration, a discussion of customer-relationship management(CRM) concludes the chapter.

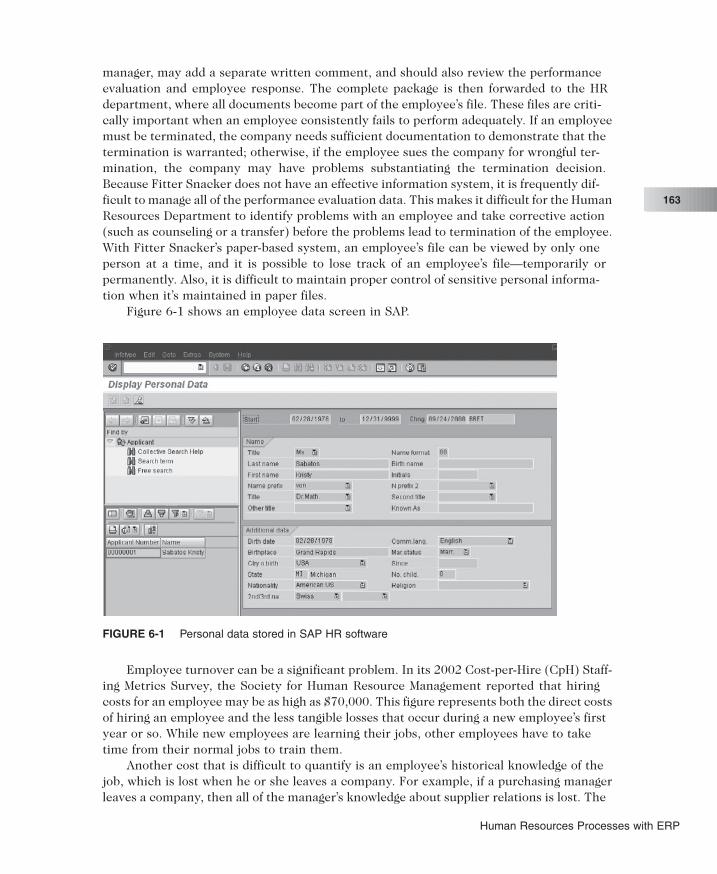

● Chapter 4 describes how ERP systems support Supply ChainManagement—the coordinated activities of all the organizations involved inconverting raw materials into consumer products on the retail shelf. As inChapter 3, the problems caused by Fitter Snacker’s unintegrated informationsystem are explored, followed by a discussion of how ERP software could helpsolve these problems.

● Chapter 5 describes Accounting and ERP systems. This chapter clearly distin-guishes between financial accounting (FI) and managerial accounting (CO)issues. Included is an overview of the Enron collapse and the resultingSarbanes-Oxley act along with the act’s impact on information systems, spe-cifically management controls and audit capabilities.

● Chapter 6 covers Human Resource Management. While the Human Resourcesoftware is the least integrated component of all ERP systems, it includesnumerous processes that are critical to a company’s success, including strate-gic issues like succession planning.

● Chapter 7 covers Process Modeling, Process Improvement, and ERPImplementation. The chapter first presents flowcharting basics using a mini-mum number of symbols, followed by the highly structured EPC processmodel. Implementation issues conclude the chapter. We believe that processimprovement, not large-scale implementation, should be the focus in an intro-ductory ERP course.

● Chapter 8 covers ERP and electronic commerce. Because this is a broad andrapidly changing area, we have chosen to provide this chapter as an introduc-tion, rather than an exhaustive treatment of the subjects. This chapter pro-vides an overview of topics such as electronic commerce and applicationservice providers, SAP NetWeaver, and the emerging technology of RFIDs.

xiv Concepts in Enterprise Resource Planning, Third Edition

How Can You Use This Book?This third edition continues our goal of keeping the text at an introductory level. The bookcan be used in a number of ways:

● The book, or selected chapters, could be used for a three-week ERP treatmentin undergraduate Management Information Systems, Accounting InformationSystems, or Operations Management courses.

● Similarly, the book or selected chapters could be used in MBA courses, such asfoundation Information Systems or Operations Management courses. Althoughthe concepts presented here are basic, the astute instructor can build on themwith more sophisticated material to challenge the advanced MBA student.Many of the exercises in the book require research for their solution, and theMBA student could do these in some depth.

● The book could serve as an introductory text in a course devoted wholly toERP. It would provide the student with a basis in how ERP systems help com-panies to integrate different business functions. The instructor might useChapter 8 as the starting point for teaching the higher-level strategic implica-tions of ERP and related topics. The instructor can pursue these and relatedtopics using his or her own resources, such as case studies and currentarticles.

● Because of the focus on fundamental business issues and business processes,the book can also be used in a sophomore-level Introduction to Businesscourse.

Except for a computer literacy course, we assume no particular educational or busi-ness background. Chapters 1 and 2 lay out most of the needed business and computinggroundwork, and the rest of the chapters build on that base.

Features of This TextTo bring ERP concepts to life (and down to earth!) this book uses sales, manufacturing,purchasing, human resources, and accounting examples for the Fitter Snacker company.Thus, the student can see problems, not just at an abstract level, but within the context ofa company’s operations. We believe that this approach makes business problems and therole ERP can play in solving them easier to understand.

The book’s exercises have the student analyze aspects of Fitter Snacker’s informationsystems in various ways. The exercises vary in their difficulty; some can be solved in astraightforward way, and others require some research. Not all exercises need to beassigned. This gives the instructor flexibility in choosing which concepts to emphasize andhow to assess students’ knowledge. Some exercises explore FS’s problems, and some askthe student to go beyond what is taught in the book and to research a subject. A solutionmight require the student to generate a spreadsheet, perform calculations, documenthigher-level reasoning, present the results of research in writing, or participate in a debate.

The book includes an additional element designed to bring ERP concepts to life:Another Look features, which are short, detailed case studies that focus on problems facedby real-world companies. Some of these cases include interviews with information systemsmanagers who share their experiences with ERP.

Preface xv

We have illustrated ERP concepts and applications by showing how SAP ERP wouldhandle the problems discussed in the book. Screen shots of key SAP ERP tools are shownthroughout to illustrate ERP concepts. Many of the book’s exercises ask the student tothink about how a problem would be addressed using ERP software.

Instructor MaterialsThe following supplemental materials are available when this book is used in a classroomsetting. All of the teaching tools available with this book are provided to the instructor on asingle CD-ROM. Most can also be found online at www.course.com. Instructor materials arepassword-protected.

● Electronic Instructor’s Manual—The Instructor’s Manual assists in class prepa-ration by providing suggestions and strategies for teaching the text, chapteroutlines, technical notes, quick quizzes, discussion topics, and key terms.

● Solutions—Answers to end-of-chapter questions and exercises are provided.

● Sample syllabi—The sample syllabi and course outlines are provided as a foun-dation to begin planning and organizing your course.

● ExamView Test Bank—ExamView allows instructors to create and administerprinted, computer (LAN-based), and Internet exams. The Test Bank includeshundreds of questions that correspond to the topics covered in this text,enabling students to generate detailed study guides that include page refer-ences for further review. The computer-based and Internet testing componentsallow students to take exams at their computers, and also save the instructortime by grading each exam automatically. The Test Bank is also available inBlackboard and WebCT versions posted online at www.course.com.

● PowerPoint Presentations—Microsoft PowerPoint slides for each chapter areincluded as a teaching aid for classroom presentation, to make available to stu-dents on the network for chapter review, or to be printed for classroomdistribution. Instructors can add their own slides for additional topics theyintroduce to the class.

● Distance learning—Course Technology is proud to present online test banks inWebCT and Blackboard to provide the most complete and dynamic learningexperience possible. Instructors are encouraged to make the most of thecourse, both online and offline. For more information on how to access theonline test bank, contact your local Course Technology sales representative.

● Figure Files—Figure and table files from each chapter are provided for youruse in the classroom.

● Hands-on SAP exercises—Exercises are available for member institutionsthrough the SAP University Alliance. These exercises use a database that wasbuilt for the fictitious Fitter Snacker company.

xvi Concepts in Enterprise Resource Planning, Third Edition

A C K N O W L E D G M E N T S

Our thanks go out to our development editor, Amanda Brodkin, who learned how to work withauthors who occasionally use too much jargon and have trouble meeting deadlines, and pro-vided the critical eye that we needed to make our writing into what we imagined it was. Weare grateful for the support and guidance of the entire MIS team at Course Technology, par-ticularly managing editor Tricia Coia and production editor Aimee Poirier. We would not havebeen able to continue on our journey to understand ERP systems without the continued sup-port of SAP America through its University Alliance program. We appreciate the efforts ofAmelia Maurizio, Heather Czech Matthews and Doug Peebles. We also thank our reviewersSam Gill; San Francisco State University and Cindy Joy Marselis, Temple University, forinsightful comments that pointed to needed improvements. In addition, we thank our inter-viewees, Maureen Sullivan, Linda Somers, Ellen Lepine, John Wheeler, and Pat Ryan with hiscolleagues from DuPont, as well as Phil Straniero and Don Scott, for their time and frankness.And finally, we thank our students, whose honesty and desire to learn have inspired us.

Preface xvii

This page intentionally left blank

C H A P T E R 1BUSINESS FUNCTIONSAND BUSINESSPROCESSES

L E A R N I N G O B J E C T I V E S

After completing this chapter, you will be able to:

● Name the main functional areas of operation used in business.

● Differentiate a business process from a business function.

● Identify the kinds of data that each main functional area produces.

● Identify the kinds of data that each main functional area needs.

● Define integrated information systems and explain why they areimportant.

I N T R O D U C T I O N

Enterprise Resource Planning (ERP) programs are core software used by companies to coordinate

information in every area of the business. ERP (pronounced “E-R-P”) programs help to manage company-

wide business processes, using a common database and shared management reporting tools. A

business process is a collection of activities that takes one or more kinds of input and creates an output,

such as a report or forecast, that is of value to the customer. ERP software supports the efficient operation

of business processes by integrating throughout a business tasks related to sales, marketing, manufac-

turing, logistics, accounting, and staffing. In later chapters, you will learn how successful businesspeople

use ERP programs to improve how work is done within a company. This chapter provides a background

for learning about ERP software.

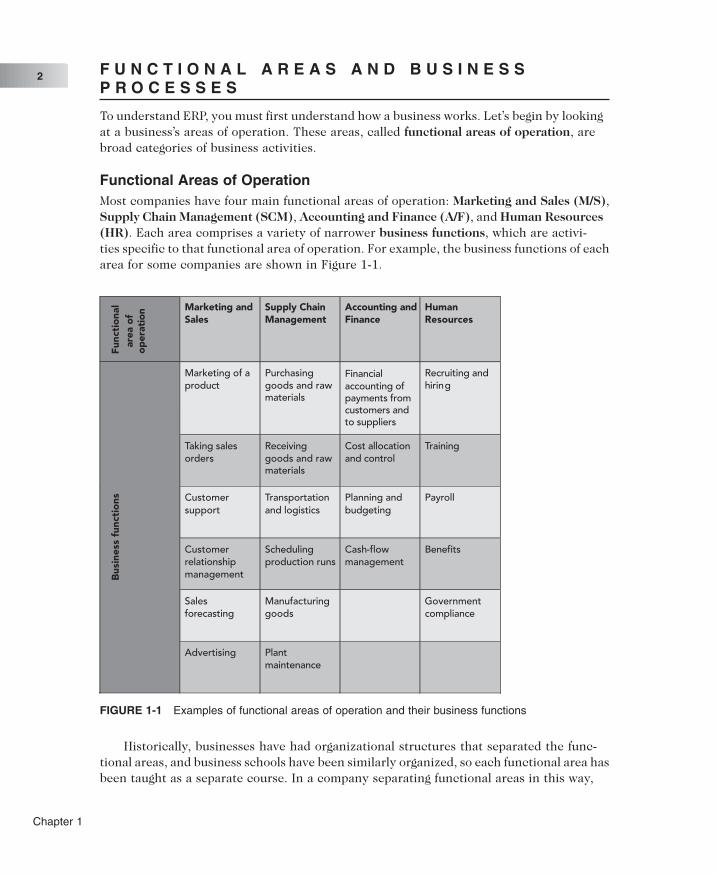

F U N C T I O N A L A R E A S A N D B U S I N E S SP R O C E S S E S

To understand ERP, you must first understand how a business works. Let’s begin by lookingat a business’s areas of operation. These areas, called functional areas of operation, arebroad categories of business activities.

Functional Areas of OperationMost companies have four main functional areas of operation: Marketing and Sales (M/S),Supply Chain Management (SCM), Accounting and Finance (A/F), and Human Resources(HR). Each area comprises a variety of narrower business functions, which are activi-ties specific to that functional area of operation. For example, the business functions of eacharea for some companies are shown in Figure 1-1.

Historically, businesses have had organizational structures that separated the func-tional areas, and business schools have been similarly organized, so each functional area hasbeen taught as a separate course. In a company separating functional areas in this way,

Func

tio

nal

area

of

op

erat

ion Marketing and

SalesSupply ChainManagement

Accounting andFinance

HumanResources

Marketing of aproduct

Purchasinggoods and rawmaterials

Financialaccounting ofpayments fromcustomers andto suppliers

Recruiting andhiring

Taking salesorders

Receivinggoods and rawmaterials

Cost allocationand control

Training

Customersupport

Transportationand logistics

Planning andbudgeting

Payroll

Customerrelationshipmanagement

Schedulingproduction runs

Cash-flowmanagement

Benefits

Salesforecasting

Manufacturinggoods

Governmentcompliance

Bus

ines

sfu

ncti

ons

Advertising Plantmaintenance

FIGURE 1-1 Examples of functional areas of operation and their business functions

Chapter 1

2

Marketing and Sales might be completely isolated from Supply Chain Management, even thoughM/S sells what SCM procures and produces. Thus, you might conclude that what happens inone functional area is not closely related to what happens in others. As you will learn in thischapter, however, functional areas are interdependent, each requiring data from the others.The better a company can integrate the activities of each functional area, the more success-ful it will be in today’s highly competitive environment. Integration also contributes toimprovements in communication and workflow. Each area’s information system depends ondata from those of other functional areas. An information system (IS) includes the comput-ers, people, procedures, and software that store, organize, and deliver information. This chap-ter illustrates the need for information sharing between functional areas and the effects on thebusiness if this information is not integrated. You will also see examples of typical businessprocesses and how these processes routinely cross functional areas.

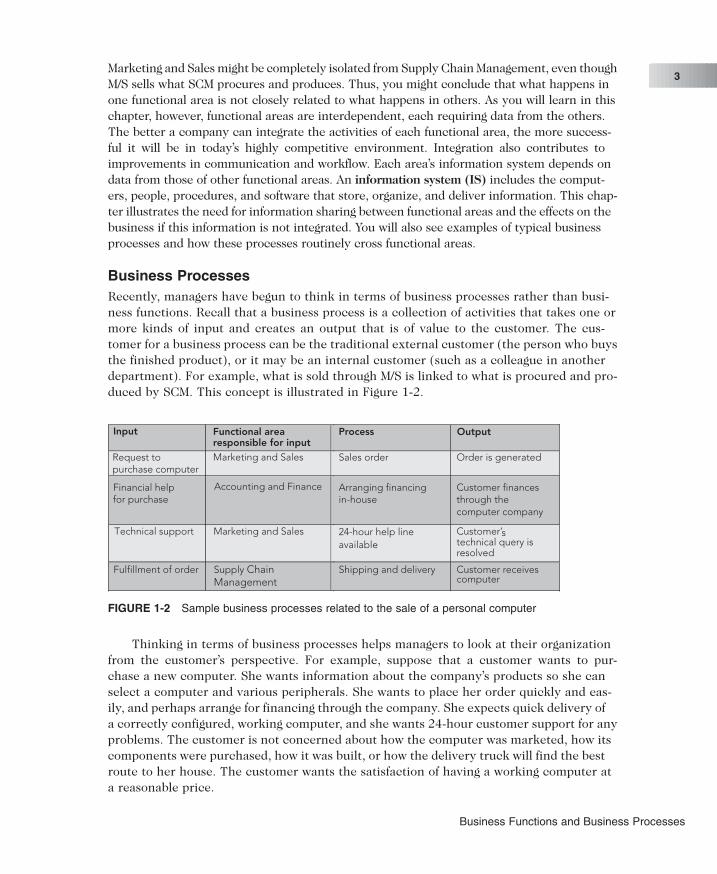

Business ProcessesRecently, managers have begun to think in terms of business processes rather than busi-ness functions. Recall that a business process is a collection of activities that takes one ormore kinds of input and creates an output that is of value to the customer. The cus-tomer for a business process can be the traditional external customer (the person who buysthe finished product), or it may be an internal customer (such as a colleague in anotherdepartment). For example, what is sold through M/S is linked to what is procured and pro-duced by SCM. This concept is illustrated in Figure 1-2.

Thinking in terms of business processes helps managers to look at their organizationfrom the customer’s perspective. For example, suppose that a customer wants to pur-chase a new computer. She wants information about the company’s products so she canselect a computer and various peripherals. She wants to place her order quickly and eas-ily, and perhaps arrange for financing through the company. She expects quick delivery ofa correctly configured, working computer, and she wants 24-hour customer support for anyproblems. The customer is not concerned about how the computer was marketed, how itscomponents were purchased, how it was built, or how the delivery truck will find the bestroute to her house. The customer wants the satisfaction of having a working computer ata reasonable price.

FIGURE 1-2 Sample business processes related to the sale of a personal computer

Business Functions and Business Processes

3

Businesses must always consider the customer’s viewpoint in any transaction. What is thedifference between a business function and a business process from the customer’s point ofview? Suppose the customer’s computer is damaged during shipment. Because only one func-tional area is involved in accepting the damaged item, receipt of the return is a business func-tion and is handled by the customer relationship management function of Marketing and Sales.Because several functional areas are involved in repair and return of the computer, the han-dling of the repair is a business process. Thus, the customer is dealing with many of the com-pany’s functional areas in her process of buying and obtaining a computer.

A successful customer interaction is one in which the customer (either internal orexternal) is not required to interact with each business function involved in the process.Successful business managers view their business operations from the perspective of asatisfied customer.

For the computer company to provide customer satisfaction, it must make sure thatits functional areas of operation are integrated. For example, computer technology changesrapidly, and the hardware the computer company sells changes frequently. In order to pro-vide customers with accurate information, people performing the sales function musthave up-to-date information about computer configurations; otherwise, a customer mightorder a computer that the company’s manufacturing plant no longer produces. People per-forming the manufacturing function need to get the details of a customer’s computer con-figuration quickly and accurately from the employees performing the sales function, so theright computer can be manufactured and shipped on time to the customer. If the cus-tomer is financing the computer through the computer company, then people perform-ing the sales order function must gather information about the customer and process itquickly, so financing can be approved in time to support shipping the computer.

Sharing data effectively and efficiently between and within functional areas leads tomore efficient business processes. Information systems can be designed so that functionalareas share data. These systems are called integrated information systems. Workingthrough this textbook will help you understand the benefits of integrated information sys-tems and the problems that can occur when information systems are not integrated. Fig-ure 1-3 illustrates the process view of business operations.

Customer Order Process

Sale

sFu

ncti

on

Acc

oun

ting

Func

tio

n

Pur

chas

ing

Func

tio

n

Pro

duc

tio

nFu

ncti

on

Log

isti

csFu

ncti

on

Material Order Process

FIGURE 1-3 A process view of business

Chapter 1

4

Businesses take inputs (resources) in the form of material, people, and equipment, andtransform these inputs into goods and services for customers. Managing these inputs andthe business processes effectively requires accurate and up-to-date information. Forexample, the sales function takes a customer’s order, and the production function sched-ules the manufacturing of the product. Logistics employees schedule and carry out the deliv-ery of the product. If raw materials are needed to make the product, production promptspurchasing to arrange for their purchase and delivery. In that case, logistics will receive thematerial, verify its condition to accounting so that the vendor can be paid, and deliver thegoods to production. Throughout, accounting keeps appropriate transaction records.

A N O T H E R L O O K

Integrated Information Systems

Integration of information is essential for company efficiency. Although people in organi-zations are often bombarded with too much information, it can still be challenging to getthe correct information to the department that needs it. The appliance giant WhirlpoolCorporation has faced just that challenge. Whirlpool is committed to Enterprise ResourcePlanning systems and in 2000 began a huge implementation of an SAP ERP system (youwill learn about SAP in Chapter 2).

Managing price increases is a particular challenge. With rising oil prices and increasedraw material costs, Whirlpool needs to be able to look at the business as a whole—in otherwords, globally. Its integrated SAP system helps it to do just that.

Whirlpool corporate vice president and chief information officer Esat Sezer explainsthat, regarding raw material price increases, “We had to have the capability to see prod-uct by product, category by category, country by country, day to day, the impact of mate-rial costs, logistics costs, and the impact into our (profit) margins.” With reference to thesupply chain, in particular, Whirlpool has updated and fixed an unintegrated system thatused to consist of spreadsheets and manual procedures. Now, with its integrated supplychain, demand from a trade partner or customer is integrated into production planning.“We can look into production plans and see if this item for this date in this quantity is forthis customer,” says Sezer.

Some of Whirlpool’s midsized trading partners could not connect directly toWhirlpool’s order entry system, and instead were ordering either by phone or fax, whichwas extremely inefficient. With the SAP integrated system, and a new online order sys-tem, these partners now can place orders over the Web. These improvements have trans-lated into a savings of 80 percent of the cost of taking the order.

continued

Business Functions and Business Processes

5

Many other large corporations have similar integration stories. The DuPontCorporation is committed to SAP for integrating business units. For example, DuPontFluorochemicals couldn’t do division-wide capacity planning, nor could its customers orderover the Web, until DuPont integrated its systems with one ERP system.

Other companies need to integrate information from acquisitions. For example, AirFrance is integrating its inventory and order systems after acquiring KLM.

When Colgate-Palmolive needed global reporting and global analysis along with moreaccurate and more timely cash positions, it looked to ERP systems to enable thosecapabilities.

Question:

1. Choose an industry in which you would enjoy working, and pick a company inthat industry. Assume this company is lacking an integrated information system.Write a memo to the CEO explaining the benefits of integrating the systems inthe company. Refer to the Functional Area Information Systems section of thechapter to help you compose this memo.

F U N C T I O N A L A R E A S A N D B U S I N E S SP R O C E S S E S O F A V E R Y S M A L L B U S I N E S S

As an introduction, we will look at the way business processes involve more than onefunctional area, using a very small business as an example—a fictitious lemonade stand thatyou own. We will examine the business processes of the lemonade stand and see why coor-dination of the functional areas helps achieve efficient and effective business processes.You will see the role that information plays in this coordination and how integration of theinformation system improves your business.

Even though one person can run a lemonade stand, the operation of the businessrequires a number of processes. Coordinating the activities within different functional areasrequires accurate and timely information.

Marketing and SalesThe functions of Marketing and Sales include developing products, determining pricing,promoting products to customers, and taking customers’ orders. M/S also helps to create asales forecast to ensure the successful operation of the lemonade stand.

For the most part, this is a cash business and does not require formal recordkeeping,but you still need to keep track of your customers so that you can send flyers or occa-sional thank you notes to repeat customers. Thus, your records must not only show theamount of sales, but also identify repeat customers.

Product development can be done informally in such a simple business; you gatherinformation about who buys which kind of lemonade and note what customers say abouteach product. You also analyze historical sales records to spot trends that are not obvious.Deciding whether to sell a product also depends on how much it costs to produce theproduct. For example, some customers might be asking for a sugar-free lemonade. To

Chapter 1

6

determine whether the new lemonade could be profitably produced and sold, you could ana-lyze data from SCM, including production information (such as mixing container size, timerequired to mix) and materials management data (cost of lemons and sweetener).

Even though you run a cash business, good repeat customers are allowed to chargepurchases—up to a point. Thus, your records must show how much each customer owes andhis or her available credit. It is very important that the data be available and accurate atthe time of a customer’s credit request. Since Accounting and Finance records must beaccessed as a part of the selling process, the accounting function has a critical role to playin the sales process.

Supply Chain ManagementThe functions within Supply Chain Management include making the lemonade(manufacturing/production) and buying raw materials (purchasing). Production is plannedso that, as much as possible, lemonade is available when needed, without excess produc-tion of lemonade that must be liquidated. This planning requires sales forecasts from theM/S functional area. Sales forecasts are analyses that attempt to predict the future sales ofa product. A forecast’s accuracy will be improved if it is based on historical sales figures (forexample, factors such as hot weather and nearby yard sales will impact the forecast). Thus,forecasts from M/S play an important role in the production planning process.

Production plans are also used to develop requirements for raw materials (bottledspring water, fresh lemons, artificial sweetener, and raw sugar) and packaging (cups, straws,and napkins). You must generate raw material and packaging orders from theserequirements. If the forecasts are accurate, you will not lose sales because of material short-ages, nor will you have excessive inventory that might spoil.

SCM and M/S must choose a recipe for each lemonade product sold. The standard recipeis a key input for deciding how much to order of each raw material, which is a purchas-ing function. Access to this recipe is also necessary for keeping good manufacturing records,allowing managers within the SCM functional area (working with those in A/F) to com-pare how much it actually costs to make a glass of lemonade, versus how much the recipeshould have cost.

Accounting and FinanceFunctions within Accounting and Finance include recording raw data about transactions(including sales), raw material purchases, payroll, and receipt of cash from customers. Rawdata are simply numbers collected from those operations, without any manipulation, cal-culation, or arrangement for presentation. Those data are then summarized in meaning-ful ways to determine the profitability of the lemonade stand and to support decisionmaking.

Note that data from Accounting and Finance are used by Marketing and Sales as wellas by Supply Chain Management. The sales records are an important component of thesales forecast, which is used in making staffing decisions and in production planning. Therecords from accounts receivable, which you use to determine whether to grant credit toa particular customer, are also used to monitor the overall credit-granting policy of the lem-onade stand. You want to be sure that you have enough cash on hand to purchase raw mate-rials, as well as to finance purchasing new equipment, such as a lemon juicer.

Business Functions and Business Processes

7

Human ResourcesEven a simple business needs employees to support the M/S and SCM functional areas,which means that the business must recruit, train, evaluate, and compensate employees.These are the functions of Human Resources.

At the lemonade stand, the number of employees and the timing of hiring depend onthe level of lemonade sales. HR uses sales forecasts developed by the individual depart-ments to plan personnel needs. A part-time helper might be needed at forecasted peak hoursor days. How much should a part-time helper be paid? That depends on prevailing job mar-ket conditions, and it is HR’s job to monitor those conditions.

Would increased sales justify hiring a part-time worker at the prevailing wage? Or, shouldyou think about acquiring more automated ways of making lemonade, so that a person work-ing alone could run the stand? Resolving these questions requires input from SCM and A/F.

The lemonade stand, while a simple business, has many of the processes needed inlarger organizations, and these processes involve activities in more than one functional area.In fact, it is impossible to discuss the processes in one functional area without discuss-ing the links to other functional areas—connections that invariably require the sharing ofdata. Systems that are integrated using ERP software provide the data sharing that is nec-essary between functional areas.

F U N C T I O N A L A R E A I N F O R M A T I O NS Y S T E M S

The lemonade stand provides simple examples of business processes and the functionalactivities required to support them. Next we will describe potential inputs and outputs foreach functional area (refer back to Figure 1-2 to review inputs and outputs related to thesale of a personal computer). Note the kinds of data needed by each area and how people usethe data. Also note that the information systems maintain relationships between all func-tional areas and processes.

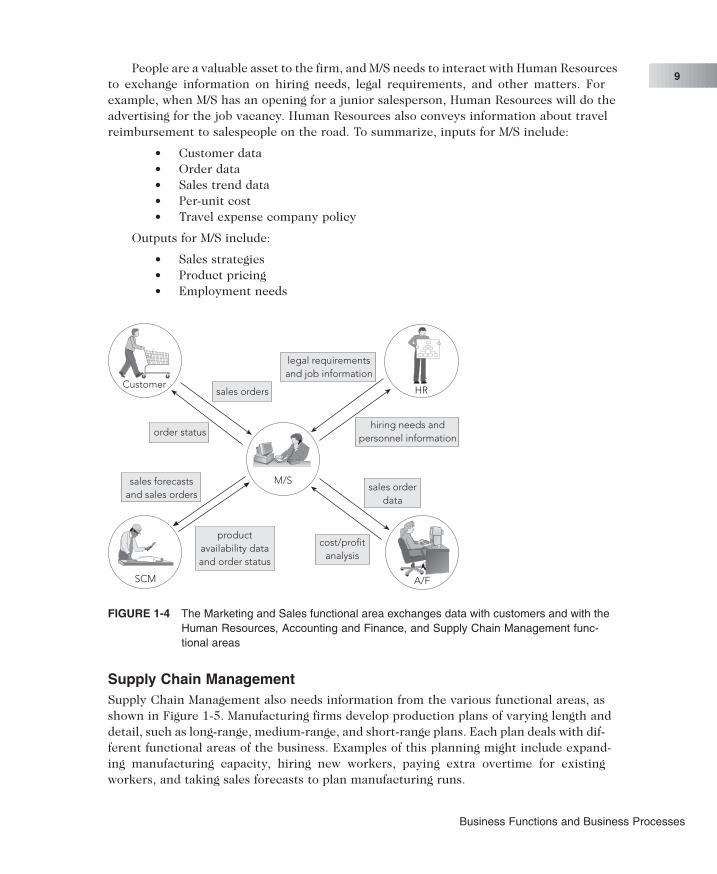

Marketing and SalesThe Marketing and Sales area needs information from all other functional areas to do its job.See Figure 1-4. Customers communicate their orders to M/S in person or by telephone,e-mail, fax, the Web, and so on. In the case of Web-based systems, customer and order datashould be stored automatically in the information system; otherwise, data must be storedmanually, by a person typing data into a keyboard or point-of-sale system, or using a bar codereader or other device. Sales orders must be passed to SCM for planning purposes and to A/Ffor billing. Sales order data are also valuable for analyzing sales trends for business deci-sion making. For example, M/S management might use a report showing the trend of a prod-uct’s sales to evaluate marketing efforts and to determine strategies for the sales force.

M/S also has a role in determining product prices, which requires an understanding ofthe market competition and the costs of manufacturing the product. Pricing might bedetermined based on a product’s unit cost, plus some percentage markup. For example, ifa product costs $5 per unit to make, and management wants a 40 percent markup, the sell-ing price must be $7 per unit. Where does the per-unit cost come from? Determining thecost of manufacturing a product requires information from Accounting and Finance,which, in turn, relies on Supply Chain Management data.

Chapter 1

8

People are a valuable asset to the firm, and M/S needs to interact with Human Resourcesto exchange information on hiring needs, legal requirements, and other matters. Forexample, when M/S has an opening for a junior salesperson, Human Resources will do theadvertising for the job vacancy. Human Resources also conveys information about travelreimbursement to salespeople on the road. To summarize, inputs for M/S include:

● Customer data● Order data● Sales trend data● Per-unit cost● Travel expense company policy

Outputs for M/S include:

● Sales strategies● Product pricing● Employment needs

Supply Chain ManagementSupply Chain Management also needs information from the various functional areas, asshown in Figure 1-5. Manufacturing firms develop production plans of varying length anddetail, such as long-range, medium-range, and short-range plans. Each plan deals with dif-ferent functional areas of the business. Examples of this planning might include expand-ing manufacturing capacity, hiring new workers, paying extra overtime for existingworkers, and taking sales forecasts to plan manufacturing runs.

Customersales orders

M/S

A/FSCM

HR

order status

sales forecastsand sales orders

productavailability dataand order status

cost/profitanalysis

sales orderdata

hiring needs andpersonnel information

legal requirementsand job information

FIGURE 1-4 The Marketing and Sales functional area exchanges data with customers and with theHuman Resources, Accounting and Finance, and Supply Chain Management func-tional areas

Business Functions and Business Processes

9

Production plans are based on information about product sales (actual and projected)that comes from Marketing and Sales. The purchasing function bases its orders of rawmaterials on production plans, expected shipments, delivery lead times, and existing inven-tory levels. With accurate data about required production levels, raw material and pack-aging can be ordered as needed, and inventory levels can be kept low, saving money. On theother hand, if data are inaccurate or not current, manufacturing may run out of raw mate-rial or packaging; such a shortfall is called a stockout. Shortages of this type can shutdown production and cause the company to miss delivery dates. To avoid stockouts, man-agement might carry extra raw material and packaging, known as safety stock, which canresult in an overinvestment in inventory. If certain time-sensitive goods are held too long,they can spoil and will need to be destroyed, rather than sold for profit. The accuracy ofthe forecast determines the amount of safety stock that is required to reduce the risk of astockout to an acceptable level. The less accurate the forecast, the more safety stock isrequired. Accurate forecasting and production planning can reduce the need for extrainventory and manufacturing capacity.

Supply Chain Management records can provide the data needed by Accounting andFinance to determine how much of each resource (materials, labor, supplies, and over-head) was used to make completed products in inventory.

S

M/SA/F

SCM

HR

orders for rawmaterials and

packaging

productionplans, materials,

and inventory

sales data andmanufacturingcost analysis

hiring needs andpersonnel information

raw materialsavailability and

delivery

sales forecastsand sales

orders

productavailabilitydata and

order status

legal requirementsand job information

FIGURE 1-5 The Supply Chain Management functional area exchanges data with suppliers andwith the Human Resources, Marketing and Sales, and Accounting and Finance func-tional areas

Chapter 1

10

Supply Chain Management data can support the M/S function by providing informa-tion about what has been produced and shipped. For example, some computer manufactur-ers, such as Gateway, have automated systems that call customers to notify them that theircomputer order has been shipped. Shipping companies, such as UPS and FedEx, pro-vide shipment-tracking information on the Internet. By entering a tracking number, the cus-tomer can see each step of the shipping process by noting where the package’s bar code wasscanned. Thus, accurate and timely production information can support the sales pro-cess and increase customer satisfaction.

For long-range planning, management might want to see monthly reports showing salesand production figures. The data for such reports must come from the production andinventory data.

Supply Chain Management also interacts in some ways with Human Resources. SCMpasses hiring information to HR, and HR informs SCM of the company’s layoff and recallpolicy, which might pertain to workers in the plant.

To summarize, inputs for SCM include:

● Product sales data● Production plans● Inventory levels● Layoff and recall company policy

Outputs for SCM include:

● Raw material orders● Packaging orders● Resource expenditure data● Production and inventory reports● Hiring information

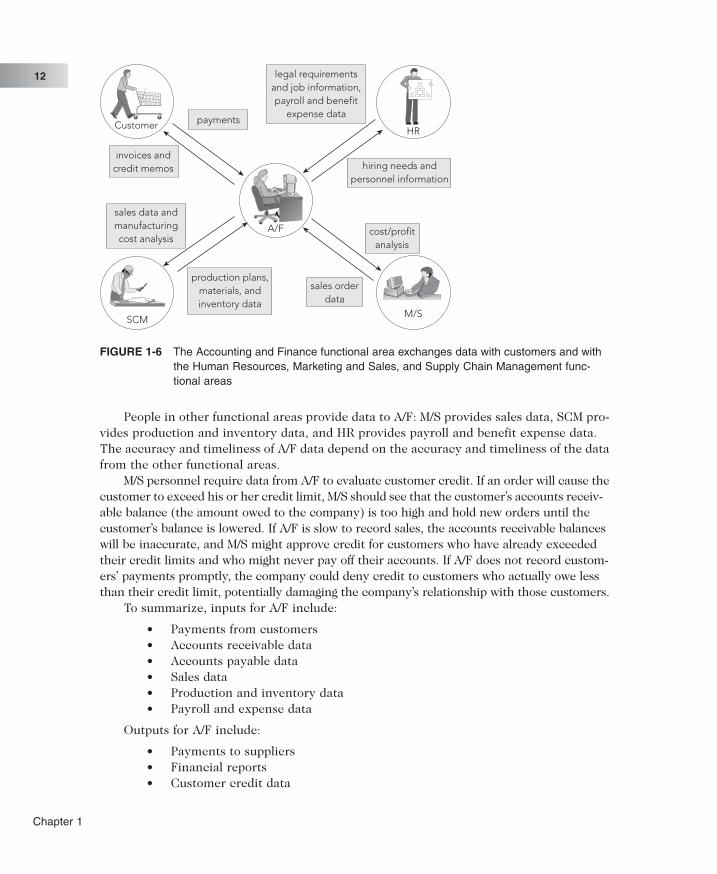

Accounting and FinanceAccounting and Finance needs information from all the other functional areas to completeits jobs accurately, as depicted in Figure 1-6. A/F personnel record the company’s trans-actions in the books of account. For example, they record accounts receivable when salesare made and cash receipts when customers send in payments. In addition, they recordaccounts payable when raw materials are purchased and cash outflows when they pay formaterials. Finally, A/F personnel summarize the transaction data to prepare reports aboutthe company’s financial position and profitability.

Business Functions and Business Processes

11

People in other functional areas provide data to A/F: M/S provides sales data, SCM pro-vides production and inventory data, and HR provides payroll and benefit expense data.The accuracy and timeliness of A/F data depend on the accuracy and timeliness of the datafrom the other functional areas.

M/S personnel require data from A/F to evaluate customer credit. If an order will cause thecustomer to exceed his or her credit limit, M/S should see that the customer’s accounts receiv-able balance (the amount owed to the company) is too high and hold new orders until thecustomer’s balance is lowered. If A/F is slow to record sales, the accounts receivable balanceswill be inaccurate, and M/S might approve credit for customers who have already exceededtheir credit limits and who might never pay off their accounts. If A/F does not record custom-ers’ payments promptly, the company could deny credit to customers who actually owe lessthan their credit limit, potentially damaging the company’s relationship with those customers.

To summarize, inputs for A/F include:

● Payments from customers● Accounts receivable data● Accounts payable data● Sales data● Production and inventory data● Payroll and expense data

Outputs for A/F include:

● Payments to suppliers● Financial reports● Customer credit data

Customer payments

M/S

A/F

SCM

HR

invoices andcredit memos

sales data andmanufacturingcost analysis

production plans,materials, andinventory data

cost/profitanalysis

sales orderdata

hiring needs andpersonnel information

legal requirementsand job information,payroll and benefit

expense data

FIGURE 1-6 The Accounting and Finance functional area exchanges data with customers and withthe Human Resources, Marketing and Sales, and Supply Chain Management func-tional areas

Chapter 1

12

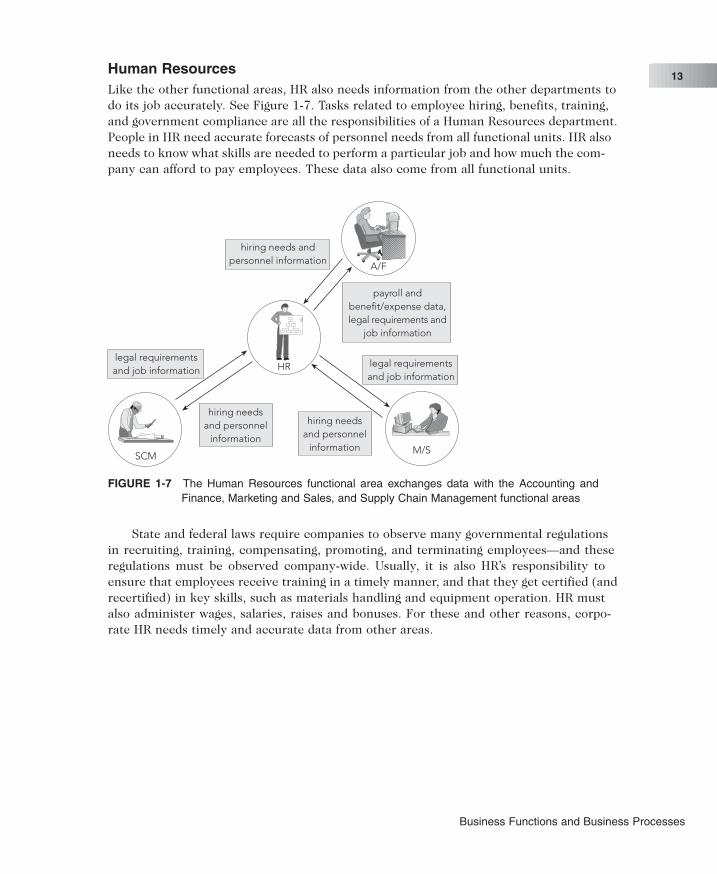

Human ResourcesLike the other functional areas, HR also needs information from the other departments todo its job accurately. See Figure 1-7. Tasks related to employee hiring, benefits, training,and government compliance are all the responsibilities of a Human Resources department.People in HR need accurate forecasts of personnel needs from all functional units. HR alsoneeds to know what skills are needed to perform a particular job and how much the com-pany can afford to pay employees. These data also come from all functional units.

State and federal laws require companies to observe many governmental regulationsin recruiting, training, compensating, promoting, and terminating employees—and theseregulations must be observed company-wide. Usually, it is also HR’s responsibility toensure that employees receive training in a timely manner, and that they get certified (andrecertified) in key skills, such as materials handling and equipment operation. HR mustalso administer wages, salaries, raises and bonuses. For these and other reasons, corpo-rate HR needs timely and accurate data from other areas.

M/S

A/F

SCM

HR

hiring needs andpersonnel information

legal requirementsand job information

hiring needsand personnel

information

hiring needsand personnel

information

legal requirementsand job information

payroll andbenefit/expense data,legal requirements and

job information

FIGURE 1-7 The Human Resources functional area exchanges data with the Accounting andFinance, Marketing and Sales, and Supply Chain Management functional areas

Business Functions and Business Processes

13

HR must create accurate and timely data for management use. For example, HR shouldmaintain a database of skills required to do particular jobs and the prevailing pay rates.When the company evaluates employees’ performance and compensation, analysis of thesedata can help to prevent the loss of valued employees because of low pay.

To summarize, inputs for HR include:

● Personnel forecasts● Skills data

Outputs for HR include:

● Regulation compliance● Employee training and certification● Skills database● Employee evaluation and compensation

As shown in Figures 1-4 through 1-7, a significant amount of data is maintained by andshared among the functional areas. The timeliness and accuracy of these data are criti-cal to each area’s success and to the company’s ability to make a profit and generate futuregrowth. ERP software allows all the functional areas to share a common database so thataccurate, real-time information is available. In the next chapter, we will trace the evolu-tion of data management systems that led to ERP.

Chapter 1

14

Chapter Summary

● Companies that make and sell products have business processes that involve thesebasic functional areas: Marketing and Sales, Supply Chain Management, Accounting andFinance, and Human Resources. They perform these functions:

● Marketing and Sales sets product prices, promotes products through advertising andmarketing, takes customer orders, supports customers, and creates sales forecasts.

● Supply Chain Management develops production plans, orders raw materials fromsuppliers, receives the raw material into the facility, manufactures products, main-tains facilities, and ships products to customers.

● Accounting and Finance performs financial accounting to provide summaries ofoperational data in managerial reports, and also is responsible for tasks such as con-trolling accounts, planning and budgeting, and cash-flow management.

● Human Resources recruits, hires, trains, and compensates employees, ensures com-pliance with government regulations, and oversees the evaluation of employees.

● A functional area is served by an information system. Information systems capture, pro-cess, and store data to provide information needed for decision making.

● Employees working in one functional area need data from employees in other func-tional areas. Ideally, functional area information systems should be integrated, so shareddata are accurate and timely.

● Today, business managers try to think in terms of business processes that integrate thefunctional areas, thus promoting efficiency and competitiveness. An important aspect ofthis integration is the need to share information between functions and functional areas.ERP software provides this capability by means of a single common database.

Key Terms

Accounting and Finance (A/F)

Business function

Business process

Enterprise Resource Planning (ERP)

Functional areas of operation

Human Resources (HR)

Information system (IS)

Integrated information system

Marketing and Sales (M/S)

Raw data

Safety stock

Sales forecast

Stockout

Supply Chain Management (SCM)

Exercises

1. Distinguish between a business function and a business process. Describe how a busi-ness process cuts across functional lines in an organization. Why do managers organizetheir teams in terms of business processes instead of functional departments? What ben-efits do you see from this new method of organization?

2. Reproduce Figure 1-1 for the lemonade stand business example. Add a one-sentencedescription for each function as it relates to the lemonade stand.

Business Functions and Business Processes

15

3. Assume you run an Internet business with a couple of friends from college. Your companysells tickets to concerts and sporting events. Describe all the flows of information betweenMarketing and Sales and Accounting and Finance.

4. Using the Internet, research your state’s regulations for waiters and waitresses, such as mini-mum age of employment.Why is it important that Human Resources communicate this infor-mation to the hiring department?

5. Think of the last time you bought a pair of shoes. How does the process of buying thoseshoes cut across the store’s various functional lines? What information from your receiptwould need to be available to the business functions? Which business functions would needthat information?

For Further Study and Research

Albright, Evan. “Whirlpool: Actionable Analytics.” SAP NetWeaver magazine 02, no. 03(Summer 2006).

Anthes, Gary H. “Case Study: Supply Chain Whirl.” Computerworld, September 6, 2005.http://www.computerworld.com.au/index.php/id;1550407298;fp;2;fpid;1239068928.

IBM Corporation. Case Study, Whirlpool: “Whirlpool’s B2B trading portal cuts per-order costssignificantly.” 2000. http://www-07.ibm.com/hk/e-business/case_studies/manufacturing/whirlpool.html.

Pang, Albert. IDC case study: “Air France Soars to New Heights with Upgraded my SAP ERPSystem: Meeting Its Commitment to Excellence.” July 2006. http://www.sap.com/solutions/business-suite/erp/pdf/CCS_Air_France.pdf.

SAP Business Community Webcast. 2005. http://www.sap.com/community/pub/events/2005_12_01_cp/index.epx.

Sullivan, Laurie. “ERPzilla,” Information Week, July 11, 2005.

Chapter 1

16

C H A P T E R 2THE DEVELOPMENT OFENTERPRISE RESOURCEPLANNING SYSTEMS

L E A R N I N G O B J E C T I V E S

After completing this chapter, you will be able to:

● Identify the factors that led to the development of Enterprise ResourcePlanning (ERP) systems.

● Describe the distinguishing modular characteristics of ERP software.

● Discuss the pros and cons of implementing an ERP system.

● Summarize ongoing developments in ERP.

I N T R O D U C T I O N

In today’s competitive business environment, companies try to provide customers with goods and

services faster and less expensively than their competition. How do they do that? Often, the key is to have

efficient, integrated information systems. Increasing the efficiency of information systems results in more

efficient management of business processes. When companies have efficient business processes, they

can be more competitive in the marketplace.

An Enterprise Resource Planning (ERP) system can help integrate a company’s operations by acting

as a company-wide computing environment that includes a database that is shared by all functional areas.

Such software can deliver consistent data across all business functions in real time. Real time refers to

data and processes that are always current.

This chapter will help you to understand how and why ERP systems came into being and what the

future might hold for business information systems. The chapter follows this sequence:

● Review of the evolution of information systems and related causes for the recent development

of ERP systems

● Discussion of the few ERP software vendors that dominate the market. The current industry

leader, German software maker SAP AG, and its industry-leading software product, SAP ERP,

are discussed as an example of an ERP system.

● Review of factors influencing a company’s decision on whether to purchase an ERP system

● Description of ERP’s benefits

● Overview of frequently asked questions related to ERP systems

● Discussion of the future of ERP software and its impact on the Internet and Web services

T H E E V O L U T I O N O F I N F O R M A T I O NS Y S T E M S

Until recently, most companies had unintegrated information systems that supported onlythe activities of individual business functional areas. Thus, a company would have a Mar-keting information system, a Production information system, and so on, each with its ownhardware, software, and methods of processing data and information. This configurationof information systems is known as silos because each department has its own stack, or silo,of information that is unconnected to the next silo. Silos are also known as stovepipes.

Such unintegrated systems might work well within individual functional areas, but toachieve its goals, a company must share data among all the functional areas. When a com-pany’s information systems are not integrated, costly inefficiencies can result. For example,suppose two functional areas have separate, unintegrated information systems. To sharedata, a clerk in one functional area needs to print out data from another functional area andthen type the information into her area’s information system. Not only does this data inputtake twice the time, it also significantly increases the chance for data entry errors. Alter-natively, the process might be automated by having one information system write data toa file to be read by another information system. This would reduce the probability oferrors, but it could only be done periodically (usually overnight or on a weekend), to mini-mize the disruption to normal business transactions. Because of the time lag in updatingthe system, the transferred data would rarely be up to date. In addition, data can be defineddifferently in different data systems, such as calling products by different part numbers in

Chapter 2

18

different systems. This variance can create further problems in timely and accurate infor-mation sharing between functional areas.

It seems obvious today that a business should have integrated software to manage allfunctional areas. An integrated ERP system, however, is an incredibly complex hard-ware and software system that was not feasible until the 1990s. Current ERP systemsevolved as a result of three things (1) the advancement of hardware and software tech-nology (computing power, memory, and communications) needed to support the system,(2) the development of a vision of integrated information systems, and (3) the reengineer-ing of companies to shift from a functional focus to a business process focus.

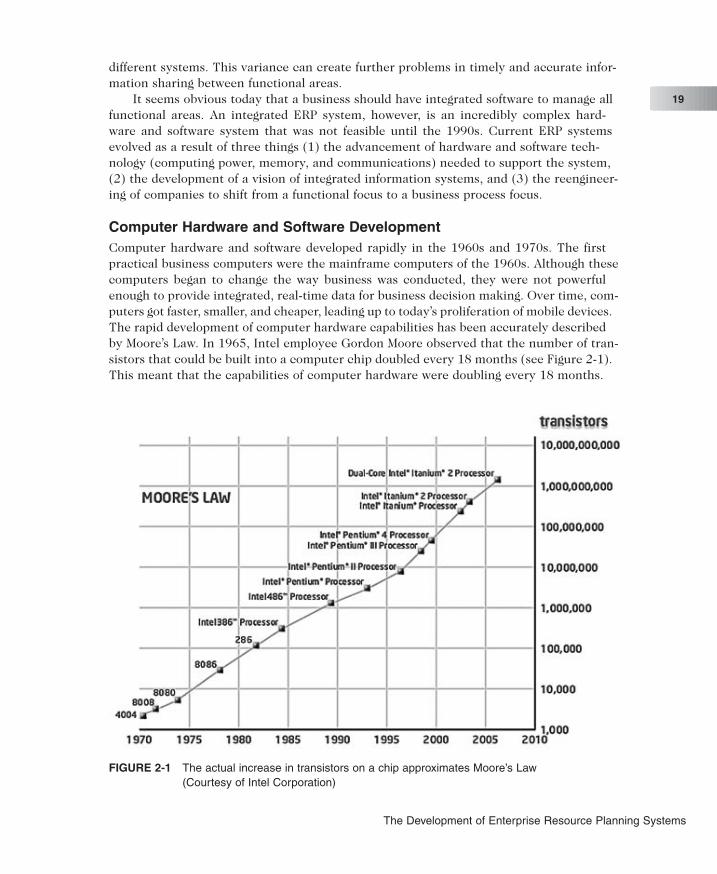

Computer Hardware and Software DevelopmentComputer hardware and software developed rapidly in the 1960s and 1970s. The firstpractical business computers were the mainframe computers of the 1960s. Although thesecomputers began to change the way business was conducted, they were not powerfulenough to provide integrated, real-time data for business decision making. Over time, com-puters got faster, smaller, and cheaper, leading up to today’s proliferation of mobile devices.The rapid development of computer hardware capabilities has been accurately describedby Moore’s Law. In 1965, Intel employee Gordon Moore observed that the number of tran-sistors that could be built into a computer chip doubled every 18 months (see Figure 2-1).This meant that the capabilities of computer hardware were doubling every 18 months.

FIGURE 2-1 The actual increase in transistors on a chip approximates Moore’s Law(Courtesy of Intel Corporation)

The Development of Enterprise Resource Planning Systems

19

During this time, computer software was also advancing to take advantage of theincreasing capabilities of computer hardware. In the 1970s, relational database software wasdeveloped, providing businesses with the ability to store, retrieve, and analyze large vol-umes of data. Spreadsheet software, a fundamental business tool today, became popular inthe 1980s. With spreadsheets, managers could perform complex business analyses with-out having to rely on a computer programmer to develop custom programs.

The computer hardware and software developments of the 1960s and 1970s paved theway for the development of ERP systems.

Early Attempts to Share ResourcesAs PCs gained popularity in business in the 1980s, managers became aware that importantbusiness information was being stored on individual PCs, but that there was no easy wayto share the information electronically. Users needed a way to share costly peripheral equip-ment (such as printers and hard disks, which in the early 1980s were fairly expensive) and,more importantly, data.

By the mid-1980s, telecommunications developments allowed users to share data andperipherals on local networks. Usually, these networks were groups of computers con-nected to one another within a single physical location. This meant that workers coulddownload data from a central computer to their desktop PCs and work with the data attheir desks.

This central computer–local computer arrangement is now called a client-serverarchitecture. Servers (central computers) became more powerful and less expensive andprovided scalability. Scalability means that when a piece of equipment’s capacity isexhausted, its capacity can be increased by adding new hardware. In the case of a client-server network, the ability to add servers makes the network scalable—thus extending thelife of the hardware investment.

By the end of the 1980s, much of the hardware needed to support the development ofERP systems was in place: fast computers, networked access, and advanced databasetechnology. Recall from Chapter 1 that ERP programs help to manage company-wide busi-ness processes using a common database. This common database holds a very largeamount of data. The technology to hold that data in an organized fashion, and to retrievedata easily, is the database management system, known as a DBMS. By the mid-1980s, theDBMS required to manage the development of complex ERP software existed. The final ele-ment required for the development of ERP software was understanding and acceptancefrom the business community. Businesspeople did not yet recognize the benefits of inte-grated information systems, nor were they willing to commit the resources to developERP software.

The Manufacturing Roots of ERPThe concept of an integrated information system took shape on the factory floor. Manu-facturing software developed during the 1960s and 1970s, evolving from simple inventory-tracking systems to material requirements planning (MRP) software. MRP softwareallowed a plant manager to plan production and raw materials requirements by workingbackward from the sales forecast, the prediction of future sales. Thus, the manager firstlooked at Marketing and Sales’ forecast of demand (what the customer wants), then looked

Chapter 2

20

at the production schedule needed to meet that demand, calculated the raw materialsneeded to meet production, and finally, projected raw materials purchase orders tosuppliers. For a company with many products, raw materials, and shared productionresources, this kind of projection was impossible without a computer to keep track of vari-ous inputs.

The basic functions of MRP could be handled by mainframe computers. Electronic datainterchange (EDI), the direct computer-to-computer exchange of standard business docu-ments, allowed companies to handle the purchasing process electronically, avoiding thecost and delays resulting from paper purchase order and invoice systems. The functionalarea now known as Supply Chain Management (SCM) began with the sharing of long-range production schedules between manufacturers and their suppliers.

Management’s Impetus to Adopt ERPThe hard economic times of the late 1980s and early 1990s caused many companies todownsize and reorganize. These company overhauls were a stimulus to ERP development.Companies needed to find some way to avoid the following kind of situation, which theyhad tolerated for a long time.

Imagine you are the CEO of Styling, a clothing manufacturing company. Styling isprofitable and is keeping pace with the competition, but your IS is unintegrated andinefficient (as are the systems of your competitors). You’ve learned to live with this kindof inefficiency: Your Marketing and Sales department creates a time-consuming papertrail for negotiating and making a sale. To schedule factory production, however,your Manufacturing manager needs accurate, timely information about actual andprojected sales orders from the M/S manager. Without such information, theManufacturing manager must guess which products to produce—and how many ofthem to produce. To keep goods moving through the production line, the manager oftendoes guess. Sometimes the guess overestimates demand for some garments, andsometimes it underestimates demand.

Overproduction of a certain garment might mean your company is stuck withgarments for which there is no market, or you might face a diminishing market due tostyle changes or seasonal demand. When you store the garments, waiting for a buyer, youincur warehouse expense. On the other hand, underproduction of a certain garmentmight result in garments not being ready for delivery when a salesperson promised,leading to unhappy customers and canceled orders. If you try to catch up on orders, you’llhave to pay factory workers overtime, or resort to the extra expense of rapid-deliveryshipments.

The Development of Enterprise Resource Planning Systems

21

The management of large companies decided they could no longer afford the type ofinefficiencies illustrated by the Styling example—inefficiencies caused by the functionalmodel of business organization. This model, illustrated in Figure 2-2, had deep roots inU.S. business, starting with the General Motors organizational model developed by AlfredP. Sloan in the 1930s. The functional business model illustrates the concept of silos ofinformation, which limit the exchange of information between the lower operating levels.Instead, the exchange of information between operating groups is handled by top man-agement, which might not be knowledgeable about the functional area.

The functional model was very useful for decades, and was successful in the UnitedStates, where there was limited competition and where flexibility and rapid decision mak-ing were not requirements for success. In the quickly changing markets of the 1990s, how-ever, the functional model led to top-heavy and overstaffed organizations incapable ofreacting quickly to change. The time was right to view a business as a set of cross-functional processes, as illustrated in Figure 2-3. In this organizational model, the func-tional business model, with its separate silos of information, is gone. Now informationflows between the operating levels without top management’s involvement.

Top management

Mar

ketin

g

Sale

s

Man

ufac

turin

g

Log

istic

s

Fina

nce

& A

cco

untin

g

Info

rmat

ion

flow

Info

rmat

ion

flow

Info

rmat

ion

flow

Info

rmat

ion

flow

Info

rmat

ion

flow

Material & product flow

FIGURE 2-2 Information and material flows in a functional business model

Chapter 2

22

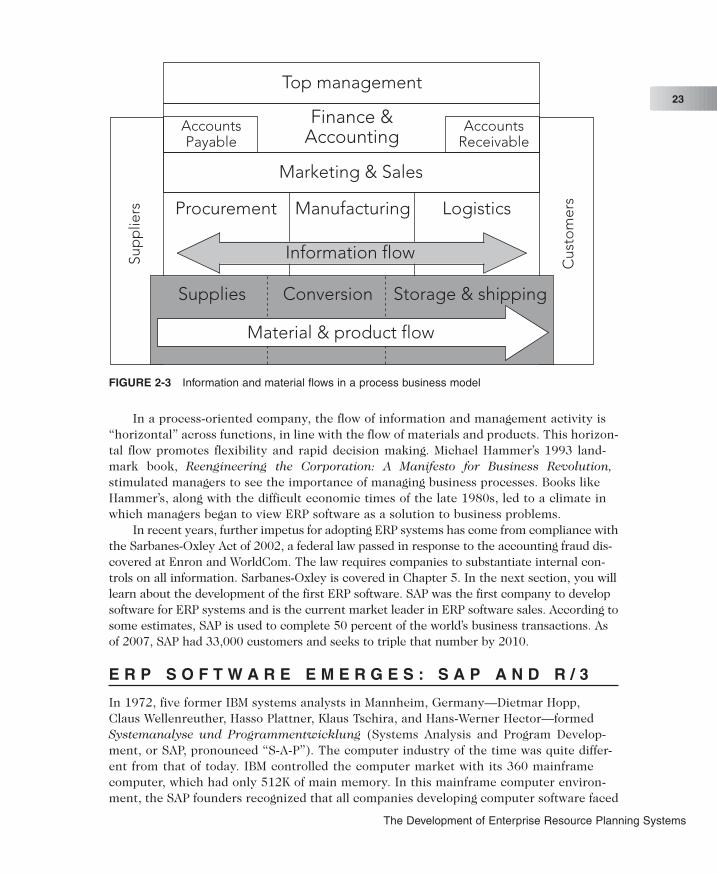

In a process-oriented company, the flow of information and management activity is“horizontal” across functions, in line with the flow of materials and products. This horizon-tal flow promotes flexibility and rapid decision making. Michael Hammer’s 1993 land-mark book, Reengineering the Corporation: A Manifesto for Business Revolution,stimulated managers to see the importance of managing business processes. Books likeHammer’s, along with the difficult economic times of the late 1980s, led to a climate inwhich managers began to view ERP software as a solution to business problems.

In recent years, further impetus for adopting ERP systems has come from compliance withthe Sarbanes-Oxley Act of 2002, a federal law passed in response to the accounting fraud dis-covered at Enron and WorldCom. The law requires companies to substantiate internal con-trols on all information. Sarbanes-Oxley is covered in Chapter 5. In the next section, you willlearn about the development of the first ERP software. SAP was the first company to developsoftware for ERP systems and is the current market leader in ERP software sales. According tosome estimates, SAP is used to complete 50 percent of the world’s business transactions. Asof 2007, SAP had 33,000 customers and seeks to triple that number by 2010.

E R P S O F T W A R E E M E R G E S : S A P A N D R / 3

In 1972, five former IBM systems analysts in Mannheim, Germany—Dietmar Hopp,Claus Wellenreuther, Hasso Plattner, Klaus Tschira, and Hans-Werner Hector—formedSystemanalyse und Programmentwicklung (Systems Analysis and Program Develop-ment, or SAP, pronounced “S-A-P”). The computer industry of the time was quite differ-ent from that of today. IBM controlled the computer market with its 360 mainframecomputer, which had only 512K of main memory. In this mainframe computer environ-ment, the SAP founders recognized that all companies developing computer software faced

Top management

Finance &Accounting

AccountsReceivable

Marketing & Sales

Procurement Manufacturing Logistics

Sup

plie

rs

Cus

tom

ers

Information flow

Supplies Conversion Storage & shipping

AccountsPayable

Material & product flow

FIGURE 2-3 Information and material flows in a process business model

The Development of Enterprise Resource Planning Systems

23

the same basic business problems, and each developed unique, but similar, solutions fortheir needs in payroll processing, accounting, materials management, and other func-tional areas of business. SAP’s goal was to develop a standard software product that couldbe configured to meet the needs of each company. SAP’s concept from the beginning was toset standards in information technology, according to founder Dietmar Hopp. In addi-tion, the founders wanted data available in real time, and they wanted users to work on acomputer screen, not with voluminous printed output. These goals were lofty and forward-looking for 1972, and it took almost 20 years to achieve them.

SAP Begins Developing Software ModulesBefore leaving IBM, Plattner and Hopp had worked on an order-processing system for theGerman chemical company ICI. The order-processing system was so successful that ICImanagers also wanted a materials and logistics management system—a system for han-dling the purchase, receiving, and storage of materials—that could be integrated into thenew order-processing system. In the course of their work for ICI, Plattner and Hopp hadalready developed the idea of modular software development. Software modules are indi-vidual programs that can be purchased, installed, and run separately, but that all extractdata from the common database. Instead of giving Plattner and Hopp the new ICI project,IBM made them traveling software experts, removing them from hands-on developmentduties. Plattner and Hopp approached Claus Wellenreuther, an expert in financialaccounting who had just left IBM, about forming their own company.

When Plattner, Hopp, and Wellenreuther established SAP on April 1, 1972, they couldnot afford to purchase their own computer. Their first contract, with ICI, to develop thefollow-on materials and logistics management system, included access to ICI’s mainframecomputer at night—a practice they repeated with other clients until they acquired theirfirst computer in 1980. At ICI, the SAP founders developed their first software package, vari-ously called System R, System RF (for real-time financial accounting), and R/1.

To keep up with the ongoing development of mainframe computer technology, in 1978SAP began developing a more integrated version of its software products, called the R/2system. In 1982, after four years of development, SAP released its R/2 mainframe ERP soft-ware package.

Sales grew rapidly in the 1980s, and SAP extended its software’s capabilities and expandedinto international markets. This was no small task, because the software had to be able toaccommodate different languages, currencies, accounting practices, and tax laws.

By 1988, SAP had established subsidiaries in numerous foreign countries, establisheda joint venture with consulting company Arthur Andersen, and sold its 1,000th system.SAP also became SAP AG, a publicly traded company.

SAP R/3In 1988, SAP realized the potential of client-server hardware architecture and begandevelopment of its R/3 system to take advantage of client-server technology. The first ver-sion of SAP R/3 was released in 1992. Each subsequent release of the SAP R/3 software con-tained new features and capabilities. The client-server architecture used by SAP allowed R/3to run on a variety of computer platforms, including UNIX and Windows NT. The SAP R/3system was also designed using an open architecture approach. In open architecture,

Chapter 2

24

third-party software companies are encouraged to develop add-on software products thatcan be integrated with existing software. The open architecture also makes it easy for com-panies to integrate their hardware products, such as bar code scanners, personal digitalassistants (PDAs), cell phones, and global information systems with the SAP system.

New Directions in ERPIn the late 1990s, the Year 2000, or Y2K, problem motivated many companies to move toERP systems. As it became clear that the date turnover from December 31, 1999 to Janu-ary 1, 2000 would wreak havoc on some information systems, companies searched for waysto consolidate data, and ERP systems provided one solution.