mining in apec economies: opportunities and...

TRANSCRIPT

___________________________________________________________________________

2015/SOM3/MTF/025 Agenda Item: 6

Mining in APEC Economies: Opportunities and Challenges

Purpose: Information Submitted by: ABAC

9th Mining Task Force MeetingCebu, Philippines

26-27 August 2015

SANTIAGO | PITTSBURGH | LONDON | MUMBAI | HONG KONG | BEIJING | SYDNEY

Mining in APEC economies: opportunities and challenges

ABAC Mining Task Force Presentation, August 25th 2015

CRU CONSULTING

Disclaimer This presentation is supplied on a private and confidential basis to the customer. It must not be disclosed in whole or in part, directly or indirectly or in any other format to any other company, organisation or individual without the prior written permission of CRU International Limited.

Permission is given for the disclosure of this report to a company’s majority owned subsidiaries and its parent organisation. However, where the report is supplied to a client in his capacity as a manager of a joint venture or partnership, it may not be disclosed to the other participants without further permission.

CRU International Limited’s responsibility is solely to its direct client. Its liability is limited to the amount of the fees actually paid for the professional services involved in preparing this presentation. We accept no liability to third parties, howsoever arising.

Although reasonable care and diligence has been used in the preparation of this presentation, we do not guarantee the accuracy of any data, assumptions, forecasts or other forward-looking statements.

© CRU International Limited 2015. All rights reserved.

2

The importance of mining in APEC 2

Opportunities 3

Challenges 4

Background 1

5 Impact of government policy on mining investment

6 Recommendations

Structure

3

The importance of mining in APEC 2

Opportunities 3

Challenges 4

Background 1

5 Impact of government policy on mining investment

6 Best Practices

Structure

4

Introduction to CRU • We are independent and global experts in mining, metals and fertilizer industries.

• We were founded in the 1960s and support our clients with market analysis, management consultancy and events.

• From our London HQ to regional offices, we have 220+ experts across the world.

Pittsburgh New York

Santiago

Mumbai

London

Hong Kong

Sydney

Beijing Tokyo

CRU Offices Opening 2015

5

Source: CRU

Why the ABAC mining study?

6

• CRU was commissioned by ABAC in 2014 to conduct a study on the status of mining in the APEC region. Key objectives:

o Discuss the importance of the mining sector and how it can positively contribute to individual economies.

o Explain the positive steps governments can take to encourage investment in the mining sector.

o Describe the importance and benefits of mining companies maintaining best practices.

• The study included:

� Current and future potential of the Asia-Pacific (APAC) mining sector including CRU Mineral Potential Rating

� Socio-economic effects of mining

� Best practices for responsible and sustainable mining

� Impact of the mining sector investment on national government policy

The importance of mining in APEC 2

Opportunities 3

Challenges 4

Background 1

5 Impact of government policy on mining investment

6 Recommendations

Structure

7

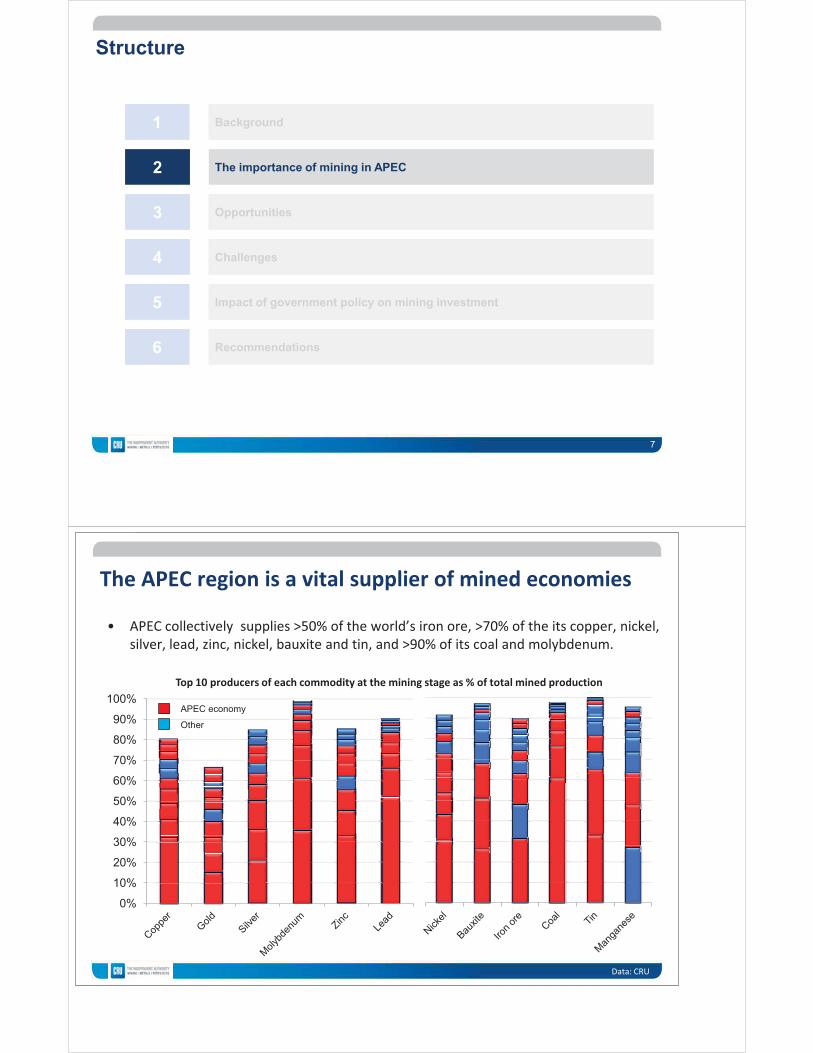

The APEC region is a vital supplier of mined economies

Data: CRU

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100% APEC economy

Other

Top 10 producers of each commodity at the mining stage as % of total mined production

• APEC collectively supplies >50% of the world’s iron ore, >70% of the its copper, nickel, silver, lead, zinc, nickel, bauxite and tin, and >90% of its coal and molybdenum.

In turn, mineral rents provide an important contribution to many APEC economies’ GDP in absolute and % terms

Data: World Bank, IMF

-

20

40

60

80

100

120

140

160

180

200

US

D b

illion

s

NB. Mineral rent as a % of GDP in 2013 applied to 2014 GDP figures.

5.42%

0.73%

14.61%

1.78%

0.99% 0.01% 0.38%

0.85% 0.45% 19.85%

7.09% 2.19%

1.19%

0.07%

0.13%

0.55%

Value of mineral rents in APEC member countries, 2014 (USD billions)

The MCI is a useful tool for assessing the relative importance of mining across different economies…

Data: ICMM, 2015

However some economies may still be involved in the mining industry through investment in projects abroad, e.g. Japanese companies investing in Chile, Aus.

Source: CRU

The CRU Mineral Potential Rating considers specific factors of individual economies in terms of mining potential

Resource-rich, mature and/or diversified economy means that mining isn’t a highly important part of the overall economy, e.g. USA, Canada.

Resource-rich, developed economies, where mining is a key part of the total economy, e.g. Australia, Chile.

Resource-rich developing or intermediate economies, where mining is by some margin the primary contributor to the economy, e.g. Papua New Guinea, Peru.

Resource-poor economies, where resources have either been depleted or simply don’t exist, and as such mining is not an important part of the overall economy, e.g. Japan, Singapore, Chinese Taipei, South Korea, Hong Kong SAR.

1

2

3

4

• Economies with a high CRU Mineral Potential Rating (Australia, Canada, US, Mexico, Indonesia, Chile, Philippines, Peru, PNG) fall into four main categories.

Refer to pp. 55-56 in ABAC Mining Report

11

The importance of mining in APEC 2

Opportunities 3

Challenges 4

Background 1

5 Impact of government policy on mining investment

6 Recommendations

Structure

12

The APAC commodities sector is huge and growing

30%

40%

50%

60%

70%

80%

90%

3.9% 1.3% 4.7% 2.1% 3.0% 3.1% 1.9% 1.4% 5.4% 2.6% 1.2%

APAC demand as a proportion of global demand, 2014

2.2%

APAC Demand as % of Global Demand 14-19 CAGR Global Demand < APAC equivalent 14-19 CAGR Global Demand > APAC equivalent

Note: Asia includes China, India & S.Asia, SE.Asia and N.Asia 13

Fraser Institute survey rating of whether a jurisdiction’s geology ‘encourages exploration investment’ – essentially a subjective measure of mineral potential

The excellent geological prospectivity of various APAC economies presents a significant opportunity

0% 20% 40% 60% 80%

Ivory Coast Kenya

Burkina Faso Namibia

Bolivia Angola Russia

Norway China

Mongolia Myanmar

Turkey Sweden

Australia Ghana

Botswana Eritrea Liberia

Madagascar South Africa

Finland Ireland

Brazil USA

Zambia Colombia

Kazakhstan Canada Mexico

Greenland Indonesia

Peru DRC

Philippines Chile

Papua New Guinea

0% 20% 40% 60% 80%

Niger French Guiana

Suriname Saudi Arabia

Mozambique Thailand Portugal

France Bulgaria

Dominican Republic Nicaragua

Sierra Leone India

Malaysia Laos

Ethiopia Vietnam Guyana Poland

Honduras Fiji

Panama Greece

Romania Ecuador

Zimbabwe Kyrgyzstan

New Zealand Guinea

Mali Venezuela

Serbia Tanzania

Nigeria Spain

Guatemala

APEC APEC in APAC Non-APEC

Fraser Institute Global Mining Survey

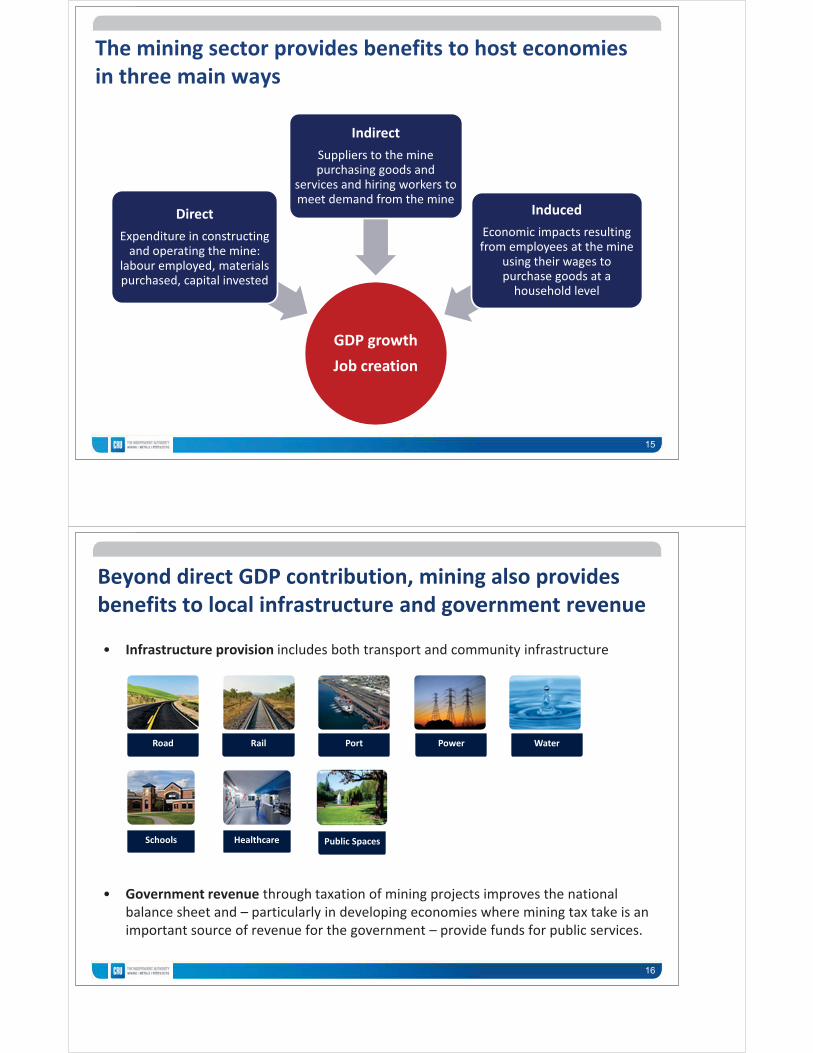

The mining sector provides benefits to host economies in three main ways

GDP growth Job creation

Direct Expenditure in constructing

and operating the mine: labour employed, materials purchased, capital invested

Indirect Suppliers to the mine purchasing goods and

services and hiring workers to meet demand from the mine

Induced Economic impacts resulting from employees at the mine

using their wages to purchase goods at a

household level

15

Beyond direct GDP contribution, mining also provides benefits to local infrastructure and government revenue

• Infrastructure provision includes both transport and community infrastructure

• Government revenue through taxation of mining projects improves the national balance sheet and – particularly in developing economies where mining tax take is an important source of revenue for the government – provide funds for public services.

Schools Healthcare

Road Rail Port Power Water

Public Spaces

16

The importance of mining in APEC 2

Opportunities 3

Challenges 4

Background 1

5 Impact of government policy on mining investment

6 Recommendations

Structure

17

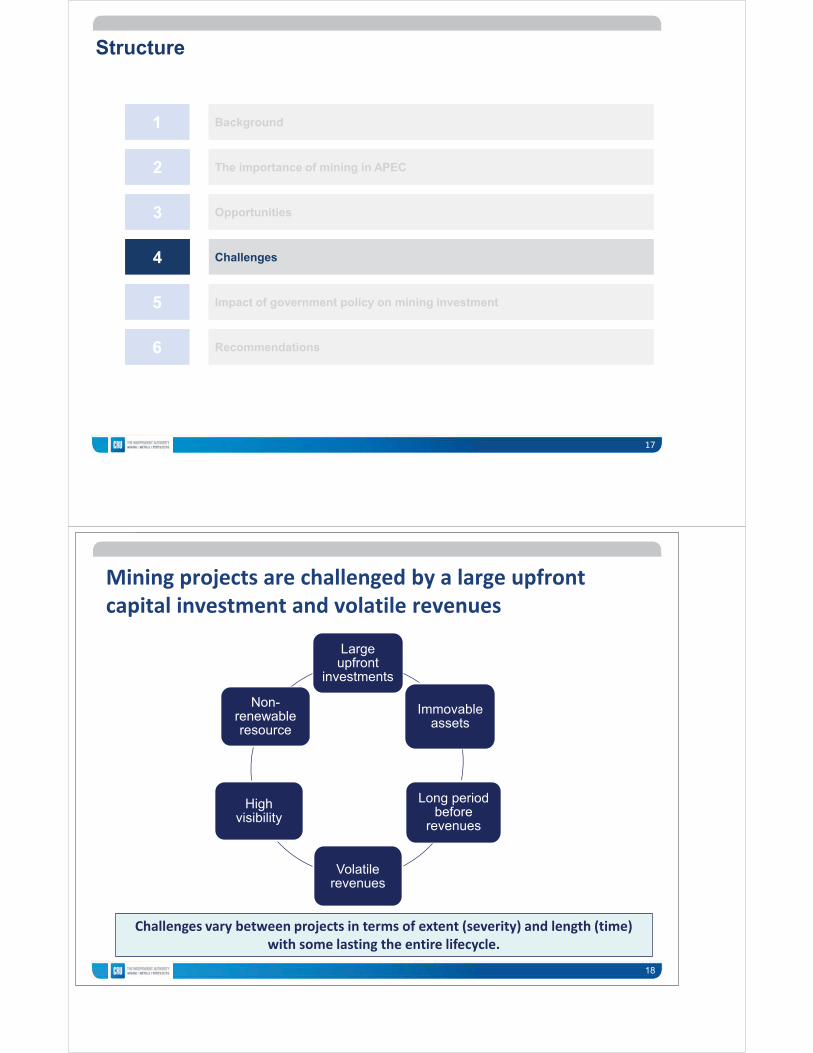

Mining projects are challenged by a large upfront capital investment and volatile revenues

18

Large upfront

investments

Immovable assets

Long period before

revenues

Volatile revenues

High visibility

Non-renewable resource

Challenges vary between projects in terms of extent (severity) and length (time) with some lasting the entire lifecycle.

Investment intensity also varies throughout the lifecycle

19

0

10

20

30

40

50

60

70

80

90

100

0 5 10 15 20 25 30 35 40 45

Inve

stm

ent i

nten

sity

($m

per

yea

r)

Lifespan in years

Exploration Drilling Licensing Rent

Design Scoping studies (Pre-)feasibility Social & economic impact

Construction Pre-stripping Site preparation Infrastructure

Operation Sustaining capital expenditures

Closure Decommissioning Reclamation

Revenues commence

There is also a significant risk that the market landscape changes during lead times

Investment required per year over lifespan for a theoretical mid-sized mining operation

Some APEC economies have a large gap between investment attractiveness under ideal vs. actual conditions

Fraser Institute Global Mining Survey

0% 10% 20% 30% 40%

Ireland Ecuador

Chile Portugal Ethiopia

Peru Canada Norway

Venezuela Panama

Papua New Guinea Mexico

Namibia New Zealand

USA Nicaragua

Tanzania Sweden Greece

Australia Botswana

Guyana Russia

Burkina Faso Thailand

French Guiana Finland

Kazakhstan Greenland

Saudi Arabia India

Mongolia Romania

Myanmar France Bolivia

APEC

non-APEC

0% 10% 20% 30% 40%

Kenya Malaysia

Eritrea Bulgaria

Poland Indonesia

Philippines Zambia

Suriname Honduras Colombia

Niger Mali DRC

Kyrgyzstan Dominican Republic

Spain China Brazil

Fiji Ghana

Mozambique Serbia

Angola Zimbabwe

Nigeria Turkey Guinea

South Africa Vietnam

Ivory Coast Liberia

Guatemala Madagascar

Laos Sierra Leone

Fraser Institute implied ‘room for improvement’ index

This discrepancy is preventing some APEC economies from achieving the full potential benefits available from their mineral wealth

Apart from Australia, as GDP increases, the relative importance of mining decreases…

Data: CRU, IMF, World Bank

-

2

4

6

8

10

12

14

1 10 100 1,000 10,000

No.

of c

omm

oditi

es in

rese

rves

GDP 2014 (bn $USD)

USA

China Australia

Canada

Russia

Mexico

Peru

Indonesia

Chile

Papua New Guinea

Vietnam

New Zealand Philippines

Malaysia

*Mineral rent as a % of GDP in 2013 applied to 2014 GDP.

Thailand

Size of the bubble represents mineral rents as a % of GDP for the year 2014*. > 5% 1-3% <1%

The importance of mining in APEC 2

Opportunities 3

Challenges 4

Background 1

5 Impact of government policy on mining investment

6 Recommendations

Structure

22

What makes an economy attractive for mining investors?

• Four factors generally dictate the attractiveness of an economy to investment in mining.

The last three are all subject to

Government policy

Geological prospectivity

Country risk

Mining sector policy

Infrastructure

1

2

3

4

23

Mineral potential is worthless if the region is not mining friendly

0

10

20

30

40

50

60

70

80

90

• The Fraser Institute's Mineral Policy Potential - advertised as a “scorecard” to governments.

• Data presented below by jurisdiction – some provinces are better.

APEC economy

Worst scores Best scores

Fraser Institute Global Mining Survey

Policy stability is extremely important to mining companies given the high upfront investment required

Geological prospectivity Country risk Mining sector policy Infrastructure

25

General policy • Rule of law • Property rights • Sanctity of contracts • Efficiency of administration & courts

Macroeconomic policy • Monetary policy- inflation • Exchange rate policy • Policy towards FDI • Convertibility and repatriation

Mining sector policy • Exploration and mining licensing • Taxation • Regulations

Export policy • Tariffs, taxes, quotas and bans • Port & logistics access/ownership • Regulations & red tape • Policy equitability across

economies/WTO

Decentralisation • Delineation of powers at central,

provincial and local levels

Summary measures • Fraser institute • Cost of capital • Corruption indices

Governments can also play a key role in facilitating best practice operation of mining projects • At a minimum, this involves the creation of legislation outlining appropriate standards in the mining

industry throughout the lifecycle – e.g. the requirement for:

• Environmental and social impact studies

• An appropriate regulatory environment for mining exploration

• Construction and operation in terms of its impact on local communities, limits on emissions, etc.

• A robust legislative environment that protects the rights of the local communities is also important:

• Communities are likely to be more positive about a project if they feel that the host government has their interests protected e.g. health and safety

26

Legislation which allows for mining returns to be distributed to the affected communities are also important.

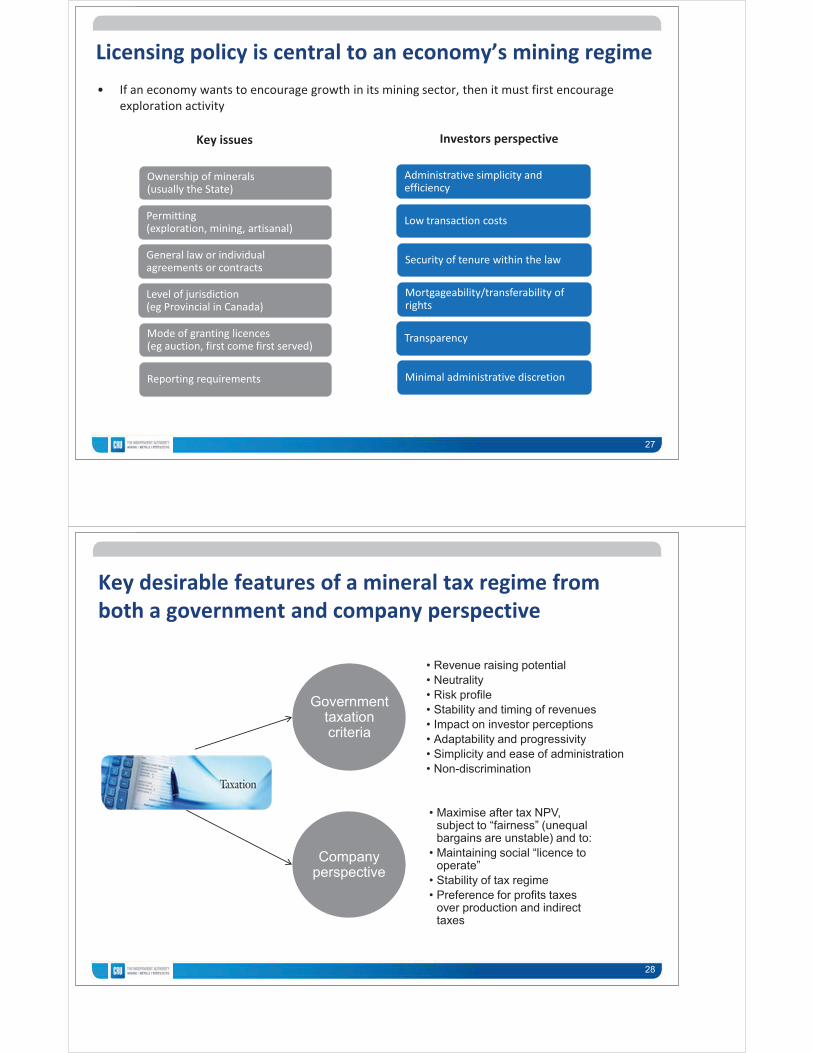

Key issues Investors perspective

Licensing policy is central to an economy’s mining regime • If an economy wants to encourage growth in its mining sector, then it must first encourage

exploration activity

27

Ownership of minerals (usually the State)

Permitting (exploration, mining, artisanal)

General law or individual agreements or contracts

Level of jurisdiction (eg Provincial in Canada)

Mode of granting licences (eg auction, first come first served)

Reporting requirements

Administrative simplicity and efficiency

Low transaction costs

Security of tenure within the law

Mortgageability/transferability of rights

Transparency

Minimal administrative discretion

Key desirable features of a mineral tax regime from both a government and company perspective

28

Government taxation criteria

• Revenue raising potential • Neutrality • Risk profile • Stability and timing of revenues • Impact on investor perceptions • Adaptability and progressivity • Simplicity and ease of administration • Non-discrimination

Company perspective

• Maximise after tax NPV, subject to “fairness” (unequal bargains are unstable) and to:

• Maintaining social “licence to operate”

• Stability of tax regime • Preference for profits taxes

over production and indirect taxes

28

The importance of mining in APEC 2

Opportunities 3

Challenges 4

Background 1

5 Impact of government policy on mining investment

6 Recommendations

Structure

29

Source: CRU

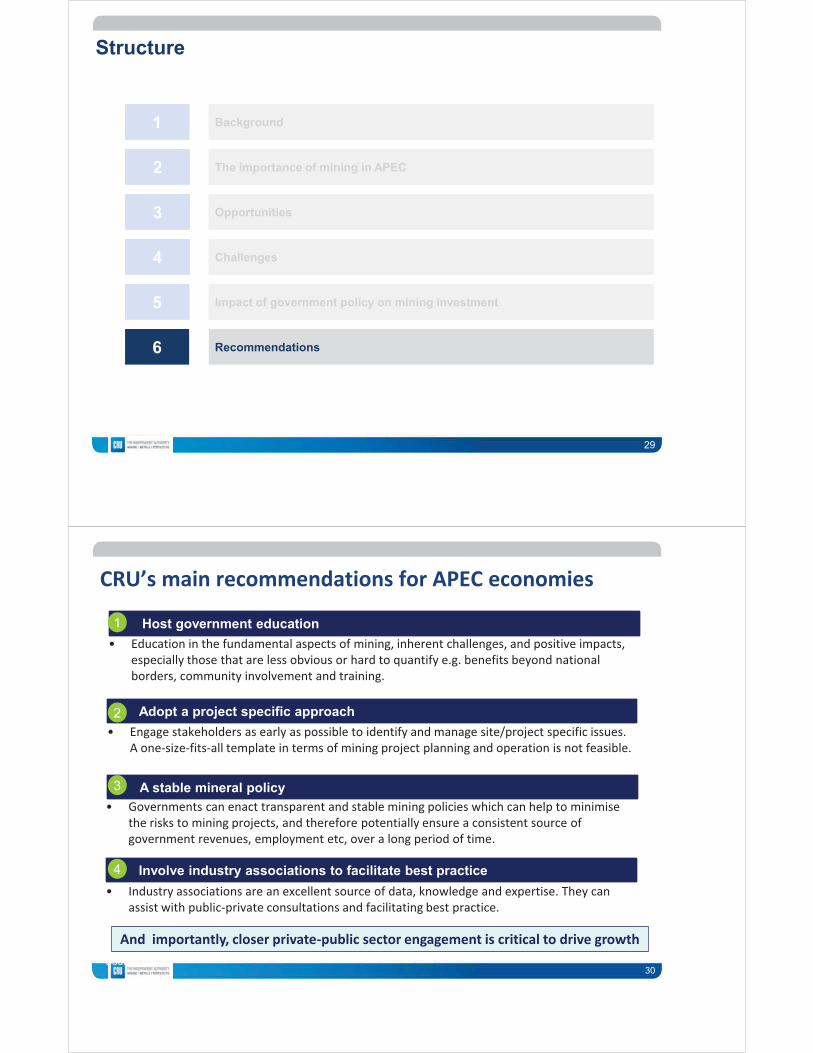

CRU’s main recommendations for APEC economies

Host government education

Adopt a project specific approach

A stable mineral policy

Involve industry associations to facilitate best practice

• Education in the fundamental aspects of mining, inherent challenges, and positive impacts, especially those that are less obvious or hard to quantify e.g. benefits beyond national borders, community involvement and training.

1

2

3

4

• Engage stakeholders as early as possible to identify and manage site/project specific issues. A one-size-fits-all template in terms of mining project planning and operation is not feasible.

• Governments can enact transparent and stable mining policies which can help to minimise the risks to mining projects, and therefore potentially ensure a consistent source of government revenues, employment etc, over a long period of time.

• Industry associations are an excellent source of data, knowledge and expertise. They can assist with public-private consultations and facilitating best practice.

30

And importantly, closer private-public sector engagement is critical to drive growth