minex consulting - image: shutterstock the...

TRANSCRIPT

MinEx Consulting Strategic advice on mineral economics & exploration

The current investment landscape for mining,

exploration & mineral sandsJohn Sykes

Strategist, MinEx Consultingalso

PhD Candidate, Centre for Exploration Targeting, The University of Western Australia (UWA)

Lecturer, Strategic Management of Resource Companies and Strategic Analysis & Consulting, Business School, UWA

Lecturer, Strategic Planning & Practice, Australian Institute of Management, WA

Managing Director, Greenfields Research

19th Australian Mineral Sands Conference 22nd March 2018, Perth, WA

Image: Shutterstock

MinEx Consulting Strategic advice on mineral economics & exploration

How do we make sense of this?

The White

House's Climate

Change Believers

Are Headed Out

the Door

- Time, 15 March 2018

U.S.-Backed Fighters Take Largest Syrian Oil Field From ISIS

- The New York Times, 22 October 2017

Sanjeev Gupta to beat Tesla's

Elon Musk with bigger

battery in South Australia

- Australian Financial Review, 16 March 2018

Brazil dam collapse: BHP to give $235 million more for clean-up of environmental disaster

- ABC, 22 December 2017

Rio Tinto unit

Turquoise Hill targeted

by Mongolian Anti-

Corruption Authority

- Australian Financial Review, 14 March 2018

MinEx Consulting Strategic advice on mineral economics & exploration

From the world to mining & exploration to mineral sands

The themes

1. Globalisation and sustainable development

2. The ‘tech boom’ and disruptive innovation

3. Climate change and the energy transition

The insight

How does each theme affect the mineral sands industry?

Contextual environment

(The rest of the world)

Transactional environment

(The mining industry)

The mineral sands

industry

Macroeconomics

Source: Ramirez & Wilkinson (2016)

MinEx Consulting Strategic advice on mineral economics & exploration

GLOBALISATION & SUSTAINABLE DEVELOPMENTThe current investment landscape for mining, exploration and mineral sands

Image: The Independent

MinEx Consulting Strategic advice on mineral economics & exploration

Nearly a decade of economic & financial growth…

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

World Annual Real GDP Growth (%)

-2

4998

9998

14998

19998

24998

29998

34998

Dow Jones Year-end Industrial Index

2017 estimate & 2018-20 forecasts made by the World Bank

2018-20 forecasts based on annual average growth rate 2008-2017

Data: World Bank, Statista

MinEx Consulting Strategic advice on mineral economics & exploration

…but concerns about inequality, China & the environment

2017 estimate & 2018-20 forecasts made by the World Bank

340

350

360

370

380

390

400

410

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

Atmospheric CO2 Levels (ppm)

‘Elephant’ curve of global inequality and growth, 1980-2016

Data: World Inequality Report 2018; NOAA

MinEx Consulting Strategic advice on mineral economics & exploration

…make for ‘interesting times’

Images: The Independent; Climate Depot; Quora; NewsBusters; National Review; The Australian; InDaily; Courier Mail; News.com.au; Shutterstock

MinEx Consulting Strategic advice on mineral economics & exploration

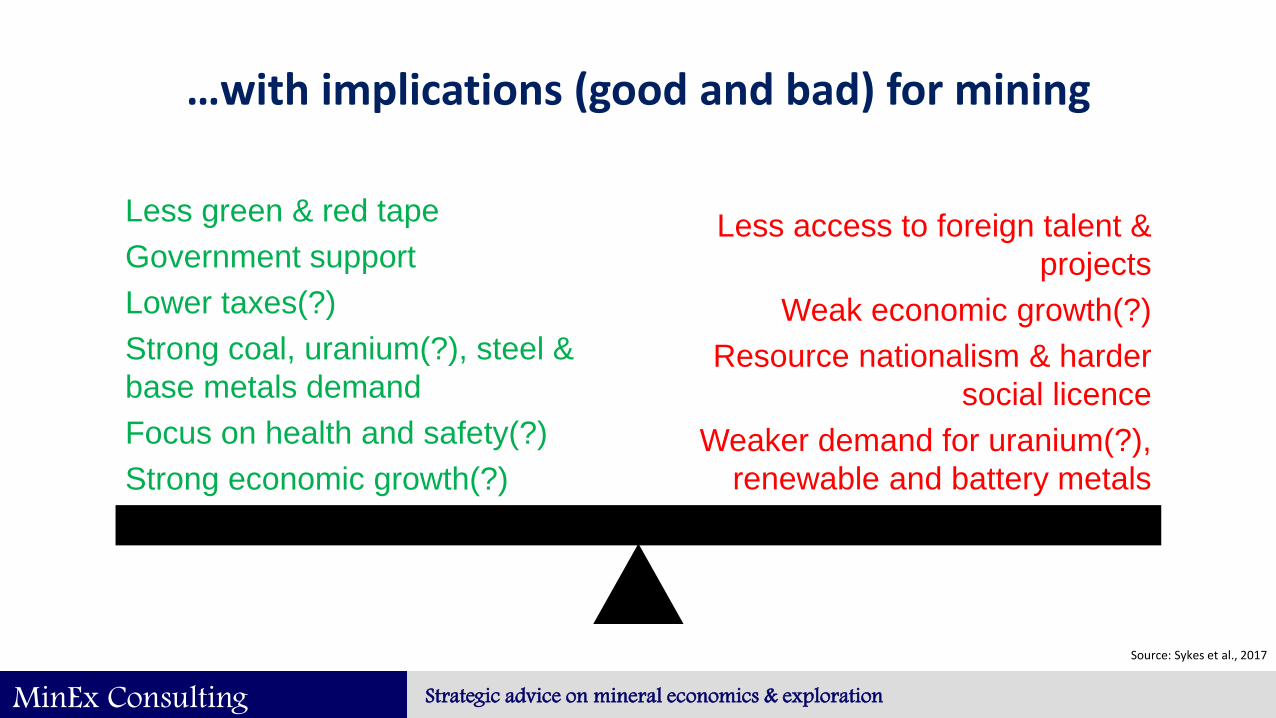

…with implications (good and bad) for mining

Less green & red tape

Government support

Lower taxes(?)

Strong coal, uranium(?), steel &

base metals demand

Focus on health and safety(?)

Strong economic growth(?)

Less access to foreign talent &

projects

Weak economic growth(?)

Resource nationalism & harder

social licence

Weaker demand for uranium(?),

renewable and battery metals

Source: Sykes et al., 2017

MinEx Consulting Strategic advice on mineral economics & exploration

It was simple in the binary politics of the Cold War…S

ocia

list

Cap

italis

t

Australian Labor,

UK Labour,

US Democrats

Australian Liberals,

UK Conservatives,

US RepublicansFree Trading

Protectionist

‘Left wing’

‘Right wing’

Mid-20th Century ‘Western’ politics

Source: Sykes et al., 2017

MinEx Consulting Strategic advice on mineral economics & exploration

…then the ‘left’ was joined by a range of ‘progressives’P

rog

ressiv

eC

on

serv

ativ

e

Australian Labor,

UK Labour,

US Democrats

Australian Liberals,

UK Conservatives,

US RepublicansGlobalist

Localist

‘Left wing’

‘Right wing’

Late-20th Century ‘Western’ politics

$Source: Sykes et al., 2017

MinEx Consulting Strategic advice on mineral economics & exploration

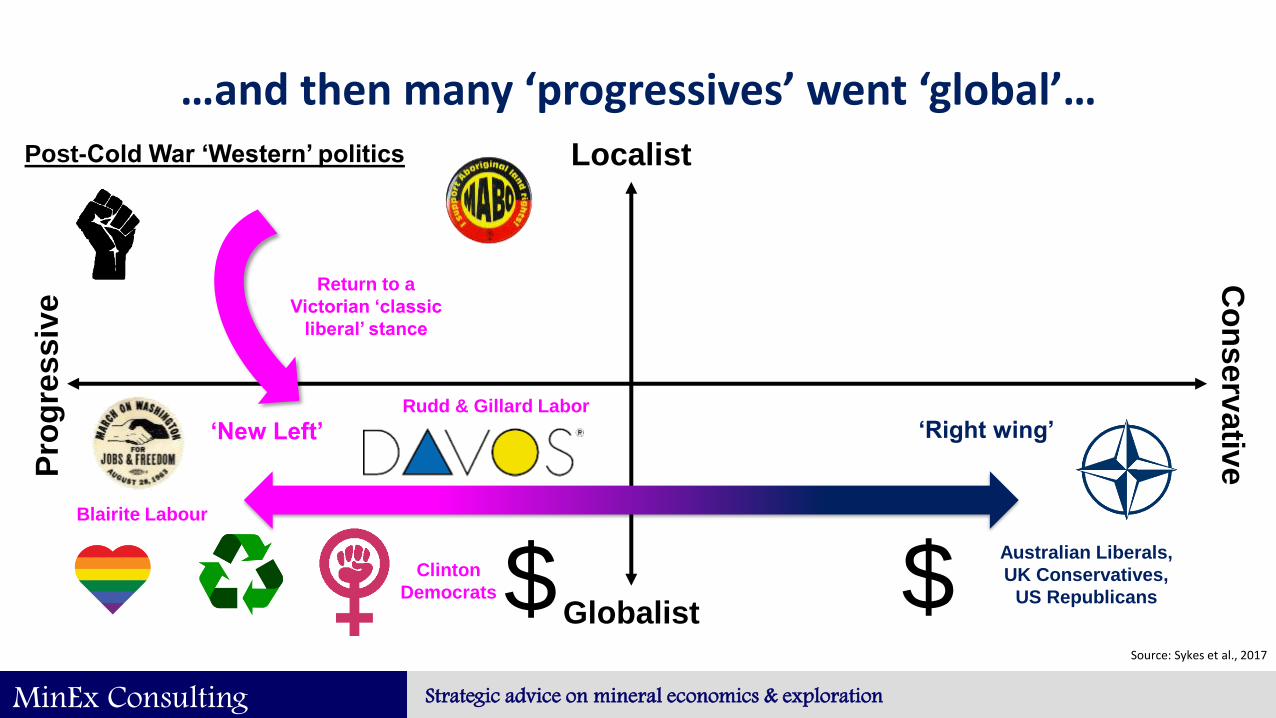

…and then many ‘progressives’ went ‘global’…P

rog

ressiv

eC

on

serv

ativ

e

Rudd & Gillard Labor

Australian Liberals,

UK Conservatives,

US RepublicansGlobalist

Localist

‘New Left’ ‘Right wing’

Post-Cold War ‘Western’ politics

$$Blairite Labour

Clinton

Democrats

Return to a

Victorian ‘classic

liberal’ stance

Source: Sykes et al., 2017

MinEx Consulting Strategic advice on mineral economics & exploration

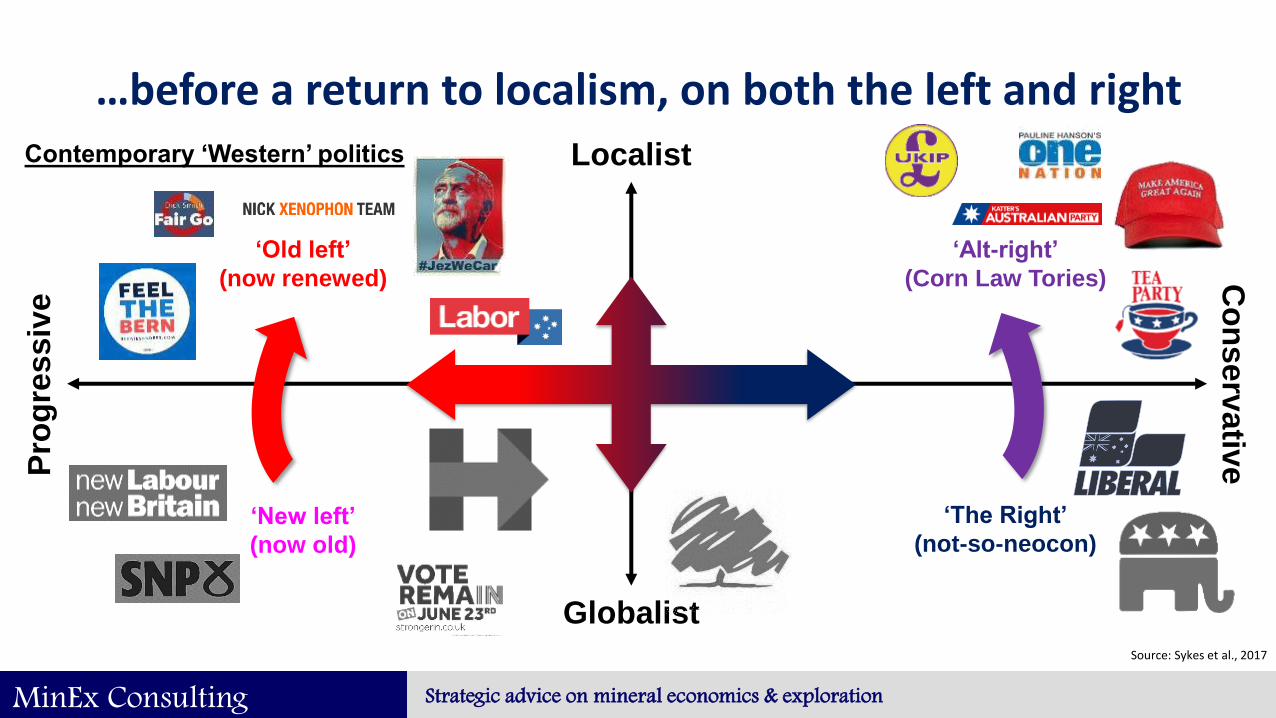

…before a return to localism, on both the left and rightP

rog

ressiv

eC

on

serv

ativ

e

Globalist

Localist

‘New left’

(now old)

‘The Right’

(not-so-neocon)

Contemporary ‘Western’ politics

‘Alt-right’

(Corn Law Tories)

‘Old left’

(now renewed)

Source: Sykes et al., 2017

MinEx Consulting Strategic advice on mineral economics & exploration

How do we interpret these many contradictory views?P

rog

ressiv

eC

on

serv

ativ

e

Globalist

LocalistContemporary ‘Western’ politics

‘Old left’

(now renewed)

‘New left’

(now old)

‘Alt-right’

(Corn Law Tories)

‘The Right’

(not-so-neocon)

Source: Sykes et al., 2017

MinEx Consulting Strategic advice on mineral economics & exploration

Politics is like a playground…

Swings

• The normal ‘back and forth’ of democratic politics;

• In a long-term industry to not to react to every ‘swing’ as can be wasteful and isolating;

• The mining industry generally over-reacts to the short-term.

Roundabouts

• Longer term structural shifts

that re-shape all sides of

politics;

• These are important to adapt to

as they will only reverse over

the long-term;

• The mining industry generally

misses these shifts.

Climbing frames

• Pre-determined elements of the

future that are yet to play out;

• You cannot avoid tackling these

issues, even if you want to;

• Often are recognised by the

industry, but nonetheless are

difficult to act upon.

Source: Sykes et al., 2017

MinEx Consulting Strategic advice on mineral economics & exploration

…but we’re on the roundabout and the climbing frame!

Is the shift against ‘sustainable development’ a swing,

roundabout, or climbing frame?

• A climbing frame: difficult to envision a developed society

paying less attention to environmental and social conditions

e.g. rise of environmentalism in Chinese middle class.

Is the shift against ‘globalisation’ a swing,

roundabout, or climbing frame?

• A roundabout (maybe): a key aspect of ‘globalisation’ is

‘glocalism’ i.e. the strengthening of local identity and rights as

everything is placed in global context – the franchise

‘McDonaldisation’ of the world.

Image: Local style McDonald’s fish burger in

Singapore

Image: Environmental protests in China

Images: South China Morning Post, Wikipedia; Sources: Steger, 2013; The Economist, 2016; Sykes et al., 2017

MinEx Consulting Strategic advice on mineral economics & exploration

…and mineral sands may be about to fall off!

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

0

5

10

15

20

25

30

35

40

45

50

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

A$

mill

ion

s

Mineral sands exploration expenditure in Australia

Exploration Expenditure (real) for Mineral Sands

Mineral Sands as a Share of All Exploration Expenditure (real)

0

1

2

3

4

5

6

7

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Global mineral sands discoveries by year

Giant Major Moderate Minor

Giant: >250Mt HMSMajor: > 50Mt HMSModerate: > 5Mt HMSSmall: <=5Mt HMS(ilmenite eq.)

Data: Australian Bureau of Statistics; MinEx Consulting © 21 March 2018

MinEx Consulting Strategic advice on mineral economics & exploration

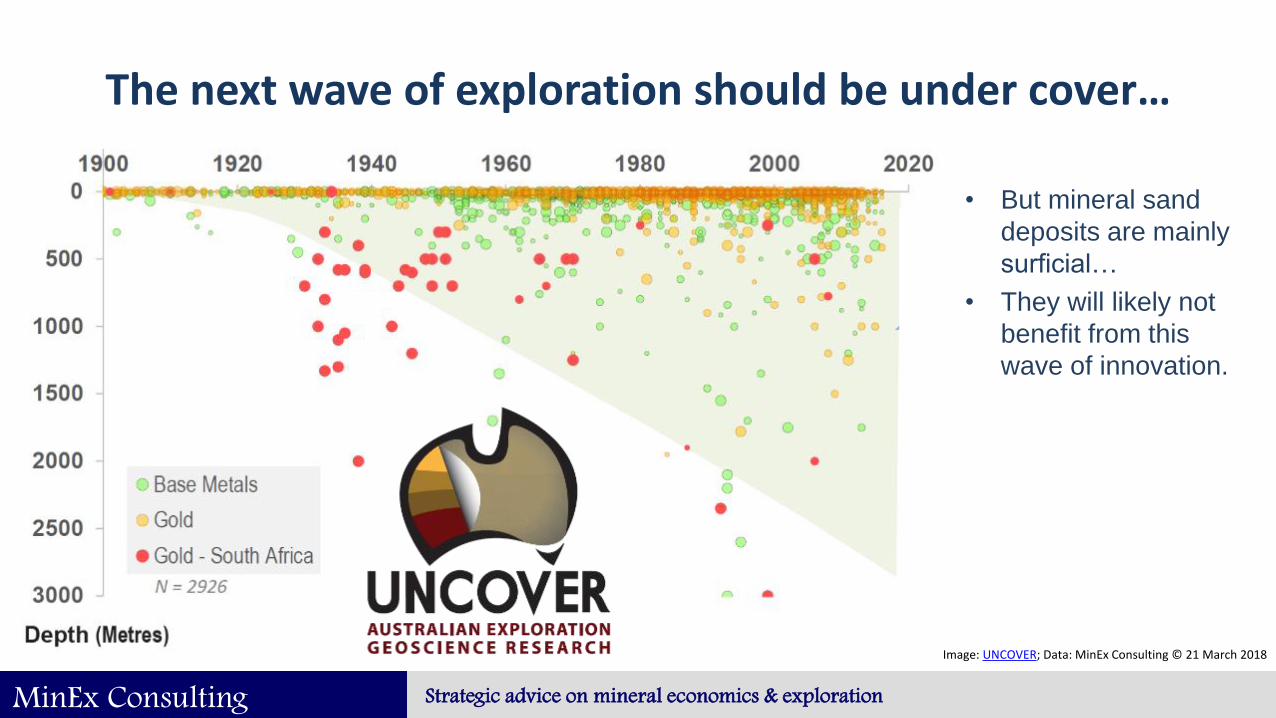

The next wave of exploration should be under cover…

Image: UNCOVER; Data: MinEx Consulting © 21 March 2018

• But mineral sand

deposits are mainly

surficial…

• They will likely not

benefit from this

wave of innovation.

MinEx Consulting Strategic advice on mineral economics & exploration

…but the mineral sands industry will have to go abroad

• It may be difficult to find

major new mineral

sands discoveries in

Australia;

• Mineral sand explorers

may be forced to abroad

to areas of increased

political risk;

• This may make ‘social

licence to operate’ even

more important than

elsewhere in the

minerals industry.

Data: MinEx Consulting © 21 March 2018

Global mineral sands discoveries, 1997-2017

MinEx Consulting Strategic advice on mineral economics & exploration

THE ‘TECH BOOM’ & DISRUPTIVE INNOVATIONThe current investment landscape for mining, exploration and mineral sands

Image: Shutterstock

MinEx Consulting Strategic advice on mineral economics & exploration

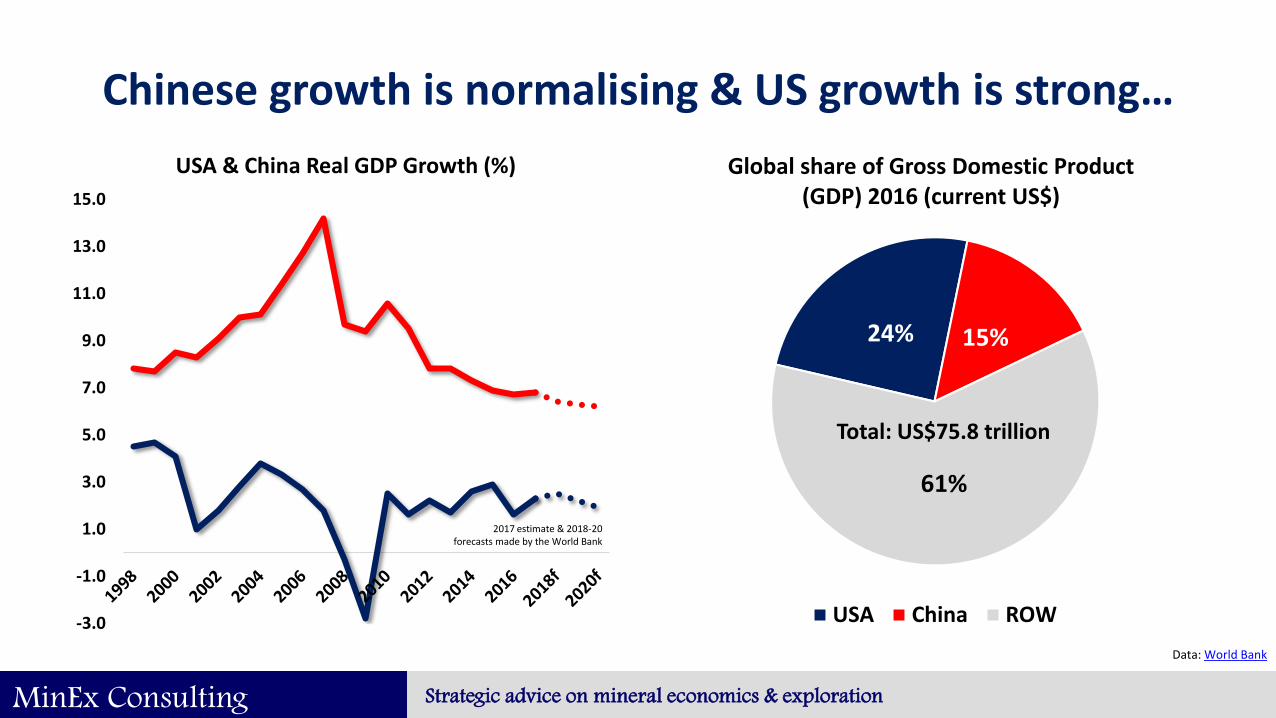

Chinese growth is normalising & US growth is strong…

-3.0

-1.0

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

USA & China Real GDP Growth (%)

24% 15%

61%

Global share of Gross Domestic Product (GDP) 2016 (current US$)

USA China ROW

Data: World Bank

2017 estimate & 2018-20 forecasts made by the World Bank

Total: US$75.8 trillion

MinEx Consulting Strategic advice on mineral economics & exploration

But, titanium dioxide’s China story may not be over…*

0

50

100

150

200

250

300

350

400

450

500

North America China

kg p

er

cap

ita

Steel Use Intensity

0

1

2

3

4

5

6

7

8

9

North America China

kg p

er

cap

ita

Copper Use Intensity

0

0.5

1

1.5

2

2.5

3

North America China

kg p

er

cap

ita

Titanium Use Intensity

Data: World Steel Association; International Copper Study Group; World Bank; Iluka

Ratio~ 1.0 : 1.8

Ratio~ 1.0 : 1.8

Ratio~ 2.5 : 1.0

*Ask an expert – this is one of the things I’ll be asking them at this conference!

MinEx Consulting Strategic advice on mineral economics & exploration

But this is the return of post-industrial ‘weightless’ economy

0

500

1,000

1,500

2,000

2,500

3,000

3,500

NASDAQ Composite (1998) ASX 200 (1998)

Data: Yahoo Finance; Images: Shutterstock

MinEx Consulting Strategic advice on mineral economics & exploration

The mining industry is currently experiencing FOMO

Real estate

+8.9%

Healthcare

+21.9%

Finance

+5.8%

Mining

& Metals

-1.4%

Telecoms

-2.9%

Energy

-3.5%

I.T.

+10.8%

Utilities

0.8%

Consumer

Staples

2.3%

+12.9%

Consumer

Discretionary Industrials

+12.6%

Materials

2.3%

Data: ASX; NB: Indices are for ASX200, apart from ‘Mining & Metals’ which is based on ASX300. Materials, based on ASX200, includes Mining & Metals constituents of ASX200. Real estate based on REITS. Finance excludes A-REITs

ASX sector 5-year performance

MinEx Consulting Strategic advice on mineral economics & exploration

…our margins will now come from better operation

100

150

200

250

300

350

400

450

500

550

600

100

110

120

130

140

150

160

170

180

190

200

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Index of US Open Pit Mine Costs vs Nominal Copper Prices

US OP Mine Index (1999) Copper Price Index (1999)

Source: Trench & Sykes, 2014; Data: Costmine

In theory… In actuality…

MinEx Consulting Strategic advice on mineral economics & exploration

Will the ‘tech boom’ make us more innovative?

Traditionally miners appear to be “sustainers”…

Bigger,Bigger,Bigger…

…and now automated! …whilst the oil industry seems a bit more disruptive?

Based on: Christensen, 1997; Images: miniature-construction-world.co.uk; The Telegraph; Shutterstock; mining-technology.com; stanford.edu; lancs.ac.uk

MinEx Consulting Strategic advice on mineral economics & exploration

e.g. the future of the past is still the future!

…by 2135… there will hardly be any miners underground. Minerals will be won either by robotized machinery or by in situ extraction of

the valuable ingredients. …biotechnology will be increasingly employed in situ to convert metals into a readily soluble form.

Mineral processing would then become largely a matter of handling solutions, thus obviating the need for crushing and grinding.”

- Arvi Parbo, former BHP Chairman, in 1986

The radically different view of the future of mining has been the same for a long time. Why?

Source: Strauss, 1986

MinEx Consulting Strategic advice on mineral economics & exploration

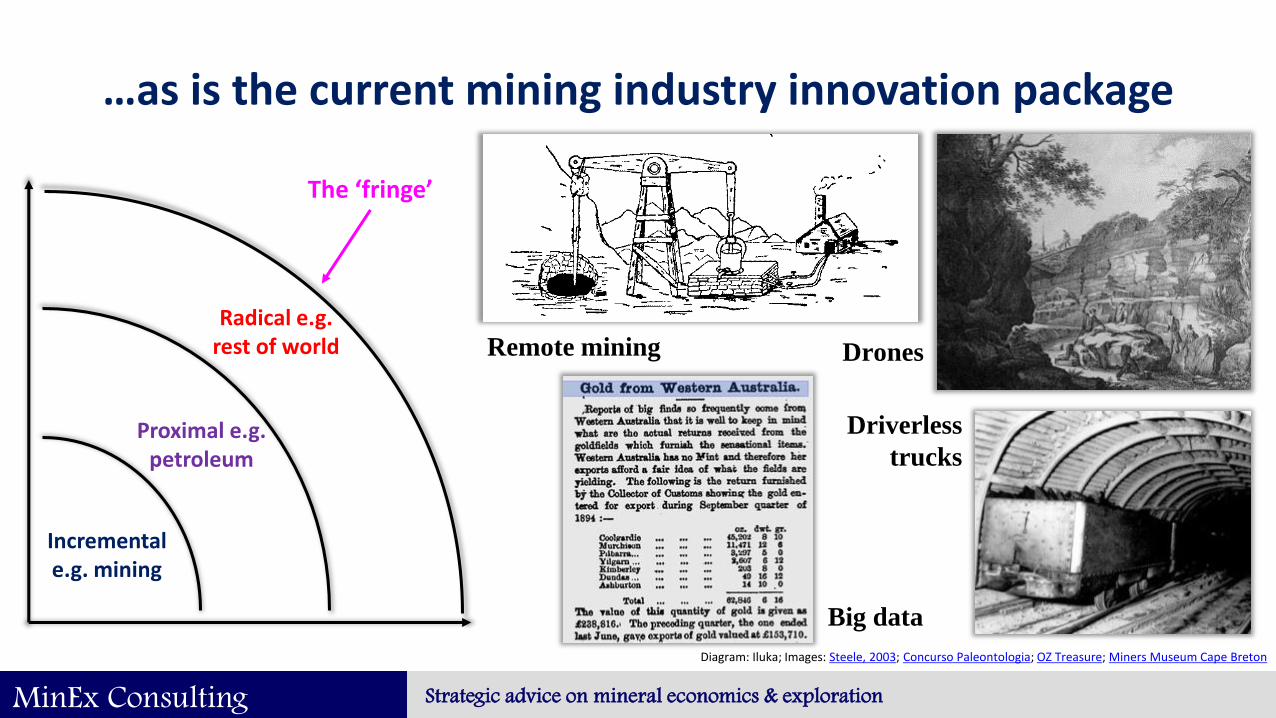

…as is the current mining industry innovation package

Incremental e.g. mining

Proximal e.g. petroleum

Radical e.g. rest of world

The ‘fringe’

DronesRemote mining

Big data

Driverless

trucks

Diagram: Iluka; Images: Steele, 2003; Concurso Paleontologia; OZ Treasure; Miners Museum Cape Breton

MinEx Consulting Strategic advice on mineral economics & exploration

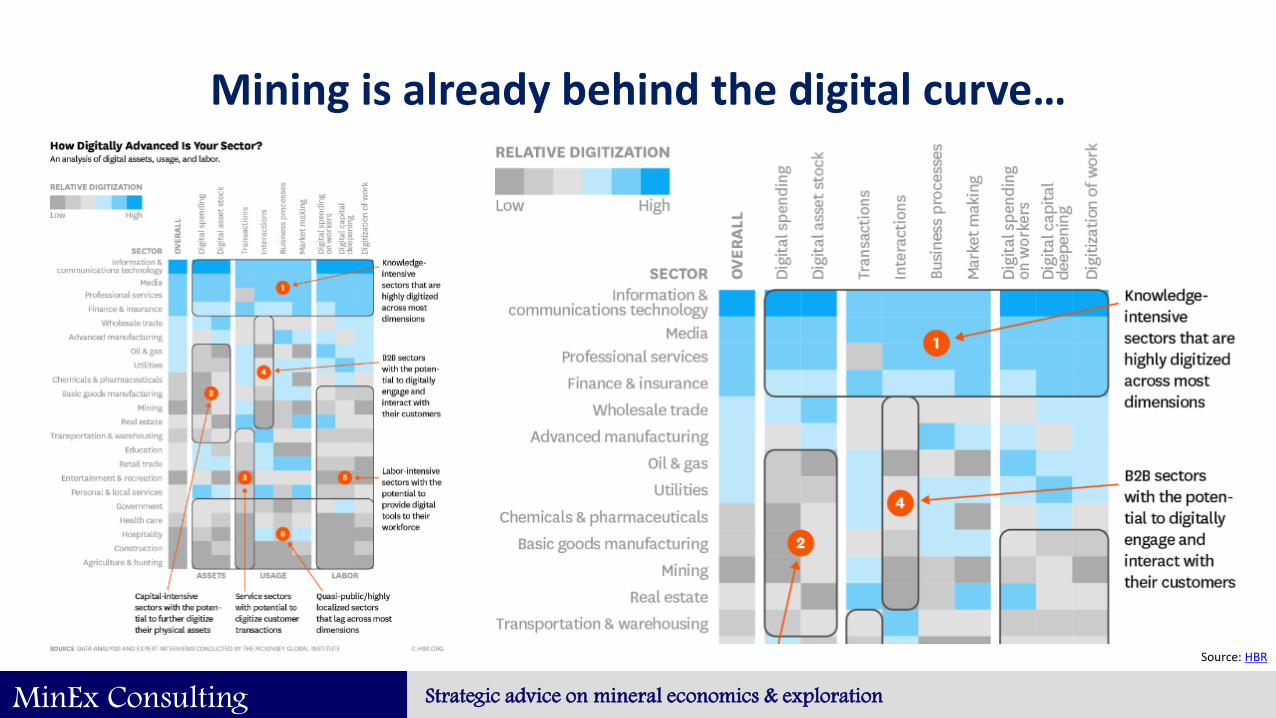

Mining is already behind the digital curve…

Source: HBR

MinEx Consulting Strategic advice on mineral economics & exploration

…the fringe is where radical innovation is occurring…

• Four key areas of science, technology and innovation:

Biotechnology & genetics

Computer science & IT*

Nanotechnology

Neurology & psychology

Sources: Turney, 2010; Imperial Tech Foresight*Computer science, IT, data science, machine learning, AI etc., are proximal industries to mining so we are already aware of their potential – what about the others?

MinEx Consulting Strategic advice on mineral economics & exploration

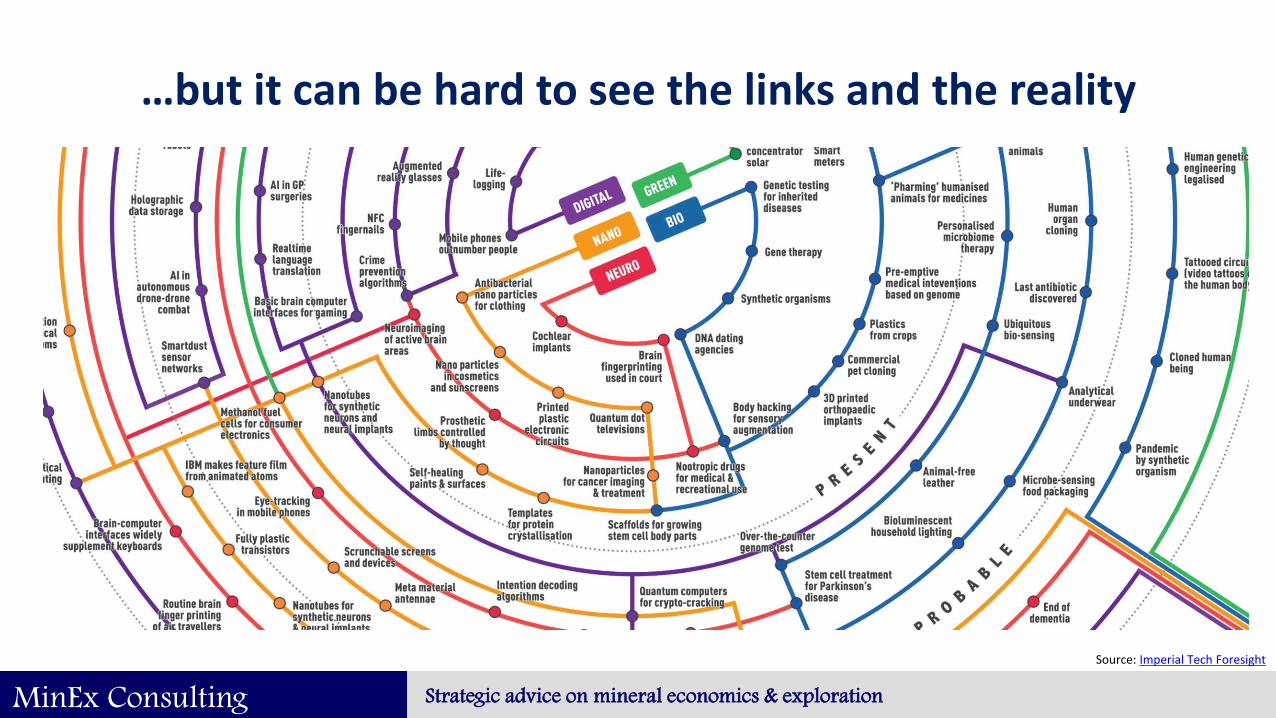

…but it can be hard to see the links and the reality

Source: Imperial Tech Foresight

MinEx Consulting Strategic advice on mineral economics & exploration

…and we have abandoned our own innovation engine

0

500

1000

1500

2000

2500

3000

3500

4000

4500

A$

Mill

ion

s

Total Exploration Expenditure (Australia)

Nominal Real

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

A$

Mill

ion

s

Total Exploration Expenditure (Australia)

Greenfields Brownfields

0

50

100

150

200

250

300

350

400

450

A$

per

met

re d

rille

d

Unit Exploration Cost (Australia)

Nominal Real

Source: Australian Bureau of Statistics

MinEx Consulting Strategic advice on mineral economics & exploration

But before we get carried away, society has a view too…

Remember:

• Drones are militarily

technology used for spying

on & killing people!

• Big data is military

technology used to spy on

people…

• A.I. is the stuff of Hollywood

dystopia…

• Remote ‘lairs’ are what the

villains have!

Remote explorationYes No

Lo

cal

en

gag

em

en

t

Yes

No

Attack of

the Drones

The Lone

Ranger

Local

Hero

Robinson

Crusoe

Scenarios for the adoption of remote exploration technologies

MinEx Consulting Strategic advice on mineral economics & exploration

…so we have to be careful not to create problems

• Which seems the most

plausible skill set to recruit in

the future?

• Compare it to the previous

slide…

Remote explorationYes No

Lo

cal

en

gag

em

en

t

Yes

No

Data

scienceField

geology

Social science

& field geology

Social

science &

data science

Capabilities required for each of the remote exploration technology scenarios

Image: Star Wars

MinEx Consulting Strategic advice on mineral economics & exploration

We are already seeing a technology backlash (‘techlash’)

The techlash against

Amazon, Facebook

and Google—and

what they can do- The Economist, 20 Jan 2018

Facebook says it can't guarantee social media is good for democracy- Reuters, 22 Jan 2018

James Damore,

Google engineer

fired for writing

manifesto on

women’s

‘neuroticism,’

sues company

- NBC, 8 Jan 2018

Facebook braces for

new E.U. privacy law

- The Washington Post, 29 Jan 2018

EU gives Facebook and Google three months to tackle extremist content- The Guardian, 1 Mar 2018

MinEx Consulting Strategic advice on mineral economics & exploration

Beware disruptive innovation in a concentrated industry!

Rutile (2017e)

Australia Sierra LeoneUkraine KenyaSouth Africa Other

Zircon (2017e)

Australia South AfricaChina IndonesiaMozambique Other

• Mining may be about to

undergo a rapid period of

technological innovation,

especially digital;

• However, in general highly

consolidated industries can

be slow adopters leaving

them open to disruption;

• Especially if there are

diversified players in the

sector which may be

exposed to more

competitive parts of the

mining industry…Top 5 Market Share: 94%Herfindahl Index (2015): 0.31

(High concentration)

Top 5 Market Share: 36%Herfindahl Index (2015): 0.22

(Moderate concentration)Data: USGS; Source: Christensen (1997)

MinEx Consulting Strategic advice on mineral economics & exploration

CLIMATE CHANGE & THE ENERGY TRANSITIONThe current investment landscape for mining, exploration and mineral sands

Image: Shutterstock

MinEx Consulting Strategic advice on mineral economics & exploration

What about the fifth technological driver?

Source: Imperial Tech Foresight

MinEx Consulting Strategic advice on mineral economics & exploration

The world is entering the ‘energy transition’…

BATTERIES

• Power storage / averaging• Portable energy• Rechargeable (reduced

waste & energy efficient)

RENEWABLES

• Theoretically infinite• Non-carbon emission

generating (at source)• Distributed sources

Increased energy

demand

Increased environmental

focus

Increased transport &

mobility

Image: Shutterstock

MinEx Consulting Strategic advice on mineral economics & exploration

…creating new opportunities for some metals, but not all…

RENEWABLES METALS

Uranium

Rare earths (neodymium,praseodymium &

dysprosium) – in the generator magnet

Silicon & germanium;Gallium-arsenide;Copper-indium-gallium-selenide (CIGS);Cadmium-telluride

Lead-acid Alkaline (zinc-manganese)

Lithium-ion (graphite,manganese & cobalt)

Nickel-cadmium/ zinc

Nickel metal (lanthanum-rare

earth) hydride

Vanadiumredox

BATTERY METALS

Images: Shutterstock; Wikipedia; solarchoice

Note absence of titanium & zirconium!

MinEx Consulting Strategic advice on mineral economics & exploration

However, the energy transition will also affect supply…

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Surface Mine UG Mine Mill

Other

Steel

Equipment,Tyres & Parts

Explosives &Reagents

Fuel &Electricity

Labour

Solar power at Sandfire

Resources Degrussa mine, WA

All electric underground mine

planned by Goldcorp at Borden,

Canada

Wind power for copper mines in

Chile owned by Barrick

‘Flexicycle’ using biodiesel power at

Pueblo Viejo, Dominican Republic

(Barrick)

Data: CostMine

MinEx Consulting Strategic advice on mineral economics & exploration

…maybe helping drive mining underground

• …but not

mineral sands

• Surface mining

of mineral

sands means

may miss out

on the

underground

transition

• May leave it

vulnerable to

environmental

and socio-

political issues

Movement towards all

electric underground

mines

Focus on greenhouse

gas reduction

Health concerns surrounding diesel

emissions in confined spaces

Improved battery

technology

Volkswagen NOX & SOX emission

scandal

Movement towards

underground mines

Focus on social & environmental

footprint of surface mining

Fewer surface mineral deposits

awaiting discovery

MOVEMENT TOWARDS ALL RENEWABLE ELECTRIC

UNDERGROUND MINING?

Improved automation and

remote technology

Safer underground

mines

MinEx Consulting Strategic advice on mineral economics & exploration

Titanium metal demand is not what it should be…

86%

7%7%

Titanium minerals demand (2012)

Pigment (TiO2) Metal Other

55%29%

8%8%

Titanium metal demand (2012)

Industrial Aerospace

Military Other

• Titanium metal is not widely used,

despite it being light and useful

because it is expensive;

• Aerospace is the main end-use for

metal, but it is CO2 intensive;

• In theory, aerospace biofuel

developments may stimulate the

air industry and titanium metal

demand;

• But cheaper, greener titanium

would be even better, as it could

then be used across multiple

sectors where ‘lightness’ is an

asset, e.g. transport, infrastructure,

energy…Data: Iluka

MinEx Consulting Strategic advice on mineral economics & exploration

…and we have seen metal markets transform before…

0

100

200

300

400

500

600

700

800

900

19

00

19

09

19

18

19

27

19

36

19

45

19

54

19

63

19

72

19

81

19

90

19

99

20

08

Growth in market size indices of copper and aluminium 1900-2014

(1900 = 1)

Cu Index Al Index

0

50

100

150

200

250

300

19

00

19

09

19

18

19

27

19

36

19

45

19

54

19

63

19

72

19

81

19

90

19

99

20

08

Growth in market size indices of copper and nickel 1900-2013

(1900 = 1)

Cu Index Ni Index

0

5

10

15

20

25

30

19

50

19

55

19

60

19

65

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

Growth in market size indices of copper and uranium 1950-2013

(1950 = 1)

Cu Index U Index

Source: Sykes et al., 2016; Data: USGS

MinEx Consulting Strategic advice on mineral economics & exploration

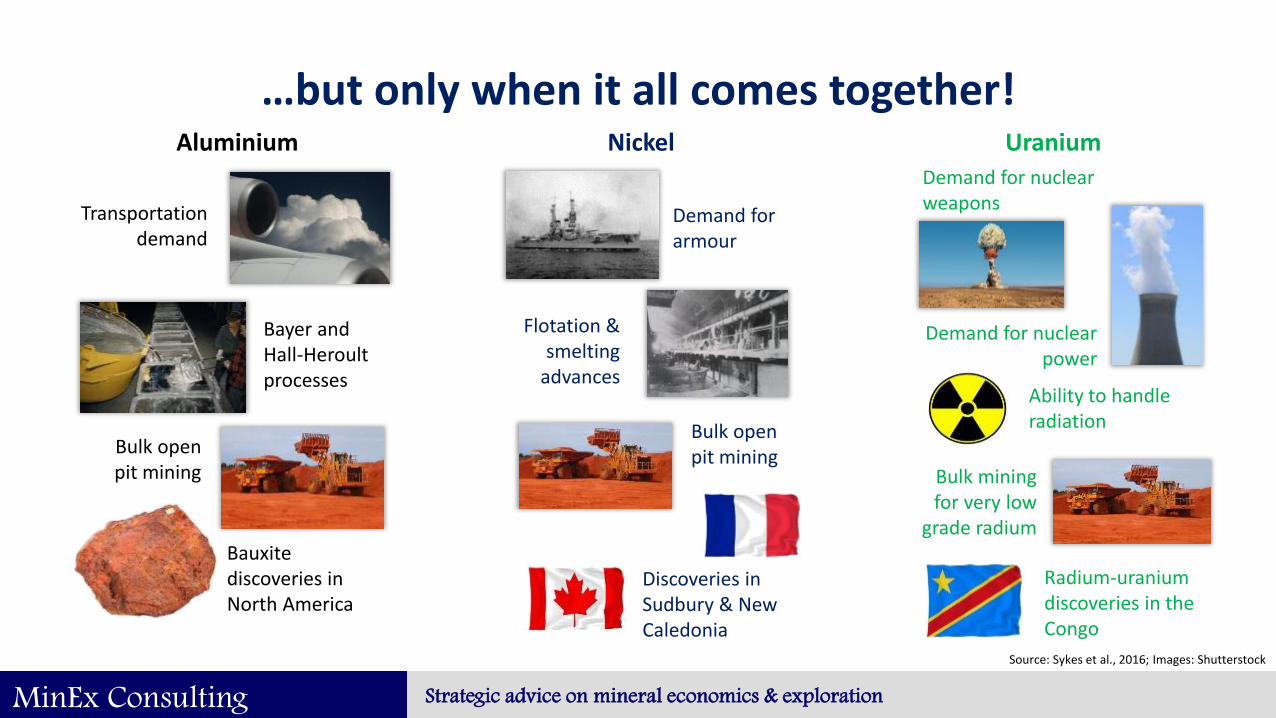

…but only when it all comes together!Nickel

Discoveries in Sudbury & New Caledonia

Bulk open pit mining

Flotation & smelting

advances

Demand for armour

Ability to handle radiation

Uranium

Demand for nuclear weapons

Demand for nuclear power

Bulk mining for very low

grade radium

Radium-uranium discoveries in the Congo

Aluminium

Bauxite discoveries in North America

Bayer and Hall-Heroultprocesses

Transportation demand

Bulk open pit mining

Source: Sykes et al., 2016; Images: Shutterstock

MinEx Consulting Strategic advice on mineral economics & exploration

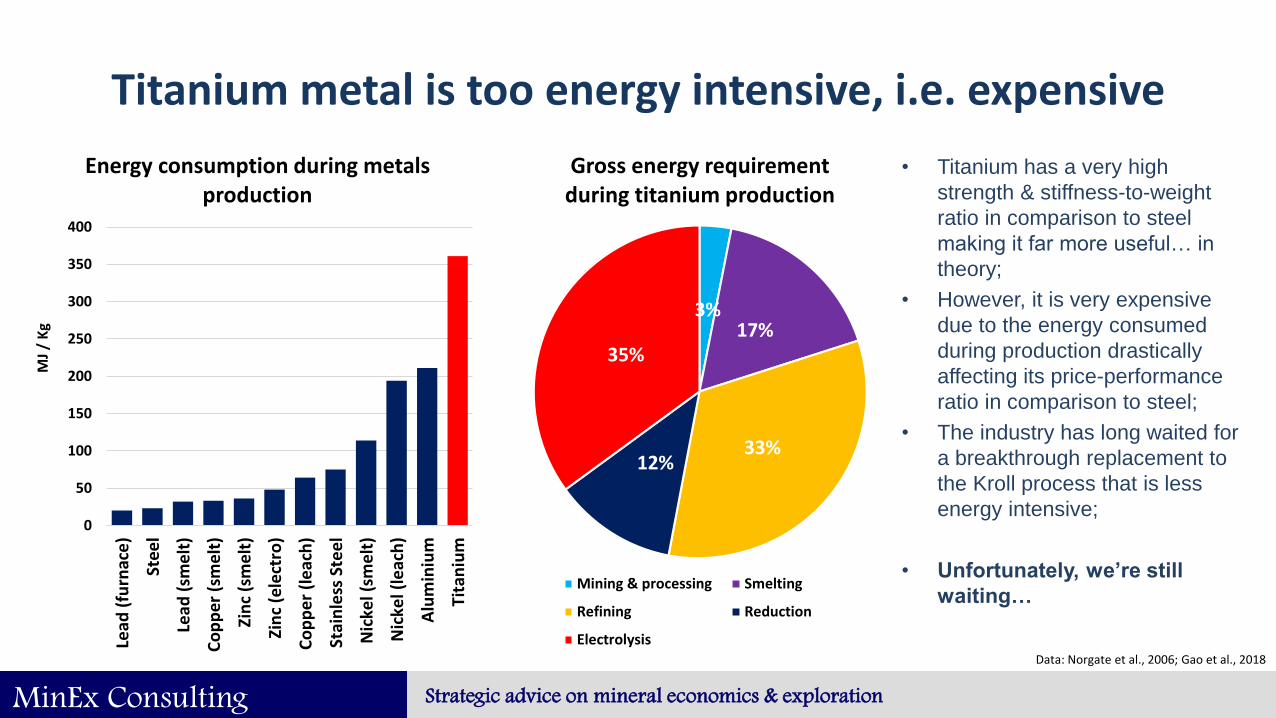

Titanium metal is too energy intensive, i.e. expensive

0

50

100

150

200

250

300

350

400

Lead

(fu

rnac

e)

Stee

l

Lead

(sm

elt

)

Co

pp

er (

sme

lt)

Zin

c (s

me

lt)

Zin

c (e

lect

ro)

Co

pp

er (

leac

h)

Stai

nle

ss S

teel

Nic

kel (

sme

lt)

Nic

kel (

leac

h)

Alu

min

ium

Tita

niu

m

MJ

/ K

g

Energy consumption during metals production

• Titanium has a very high

strength & stiffness-to-weight

ratio in comparison to steel

making it far more useful… in

theory;

• However, it is very expensive

due to the energy consumed

during production drastically

affecting its price-performance

ratio in comparison to steel;

• The industry has long waited for

a breakthrough replacement to

the Kroll process that is less

energy intensive;

• Unfortunately, we’re still

waiting…

3%17%

33%12%

35%

Gross energy requirement during titanium production

Mining & processing Smelting

Refining Reduction

ElectrolysisData: Norgate et al., 2006; Gao et al., 2018

MinEx Consulting Strategic advice on mineral economics & exploration

…and too polluting! But is a solution appearing?

0

5

10

15

20

25

30

35

40

Lead

(b

last

fu

rnac

e)

Stee

l

Lead

(sm

elt

ing)

Co

pp

er (

sme

ltin

g)

Zin

c (I

mp

eri

al)

Zin

c (e

lect

roly

tic)

Co

pp

er (

leac

hin

g)

Stai

nle

ss S

teel

Nic

kel (

sme

ltin

g)

Nic

kel (

leac

hin

g)

Alu

min

ium

Tita

niu

m

Kg

CO

2 e

q. /

Kg

CO2 emissions during metals production

• Renewable energy would resolve CO2

intensity issues;

• Would this alone stimulate titanium metal demand?

• However, ‘super’ cheap renewable energy (e.g. near-free solar) would resolve both cost and environmental issues and could be the market growth trigger…

• …thus an alternative to the Kroll process may not be required.

4%17%

9%

18%

52%

Electricity consumption during titanium production

Mining & processing Smelting

Refining Reduction

ElectrolysisData: Norgate et al., 2006; Gao et al., 2018

MinEx Consulting Strategic advice on mineral economics & exploration

Thank You!

Contact details

John Sykes

Strategist

MinEx Consulting

Perth, Australia

Email: [email protected]

Website: www.MinExConsulting.com

Copies of this and other similar presentations can be downloaded

from our website

MinEx Consulting Strategic advice on mineral economics & exploration

Acknowledgements

• I’d like to acknowledge the efforts of the Centre for Exploration Targeting scenario planning teams

whose work contributed to this presentation including Jon Bell, Leila Ben Mcharek, Rob Bills, Aida

Carneiro, Ivy Chen, Aaron Colleran, Tim Craske, Liz Dallimore, Deon deBruin, Edoaldo Di Dio, Joe

Dwyer, Mayara Fraeda, Nick Franey, Simon Gatehouse, Jeremie Giraud, Marcelo Godefroy Rodriguez,

Chris Gonzalez, Isabel Granado, Matt Greentree, David Groves, Mike Haederle, Mike Hannington, Nick

Hayward, Amanda Hellberg, Paul Hodkiewicz, Amy Imbergamo, Constanza Jara, Caroline Johnson,

Heta Lampinen, Helen Langley, John Libby, Martin Lynch, Stuart Masters, Michael Mead, Adele Millard,

Joanne Moo, Suzanne Murray, Sandra Occhipinti, Ahmad Saleem, Ian Satchwell, Robert Sills, John

Southalan, David Stevenson, Narendran Subramaniam, Siobhan Sullivan, Daniel Sully, Janet

Sutherland, Marcus Tomkinson, Marnie Tonkin, Jan Tunjic, Will Turner, Stanislav Ulrich, Jessica Volich,

Wenchao Wan, Peter Williams, Marcus Willson and Afira Zulkifli Tahmali, as well as my PhD

supervision team: Allan Trench, Campbell McCuaig, Mark Jessell and Nico Thebaud, and finally

Richard Schodde at MinEx Consulting.

MinEx Consulting Strategic advice on mineral economics & exploration

References

• Christensen, C., 1997, The Innovator's Dilemma: When New Technologies Cause Great Firms to Fail, Harvard Business Review Press: Brighton (MA), 225p.

• Gao, F., Nie, Z., Yang, D., Sun, B., Liu, Y., Gong, X., & Wang, Z., 2018, Environmental impacts analysis of titanium sponge production using Kroll process in China, Journal of Cleaner Production, 174, pp 771-779.

• Norgate, T.E., Jahanshahi, S., & Rankin, W.J., 2007, Assessing the environmental impact of metal production processes, Journal of Cleaner Production, 15, pp 838-848.

• Ramirez, R., & Wilkinson, A., 2016, Strategic Reframing: The Oxford Scenario Planning Approach, Oxford University Press: Oxford, 242p.

• Steger, M., 2013, Globalization: A Very Short Introduction, Oxford University Press: Oxford, 176p.

• Strauss, S.D., 1986, Trouble in the Third Kingdom: Minerals Industry in Transition, Mining Journal Books: London, 227p.

• Sykes, J.P., Trench, A., McCuaig, T.C., & Jessell, M., 2017, Charles Dickens on the (potentially) changing role of globalisation and sustainability in the long-term future of mining and exploration, Tenth International Mining Geology Conference, Hobart (TAS), 20-22 September, pp 239-256.

• Sykes, J.P., Wright, J.P., & Trench, A., 2016, Discovery, supply and demand: From Metals of Antiquity to critical metals, Applied Earth Science, 125:1, pp 3-20.

• Trench, A., & Sykes, J.P., 2014, Perspectives on Mineral Commodity Price Cycles and their Relevance to Underground Mining, 12th AusIMM Underground Operators’ Conference, Adelaide (SA), 24-26 March, pp 19-31.

• Turney, J., 2010, The Rough Guide to The Future, Rough Guides: London, 376p.