mineral resource availability and the...

TRANSCRIPT

MINERAL RESOURCE AVAILABILITY

and the

FUTURE OF INDUSTRIAL CIVILIZATION

John L. Berry John Berry Associates, Austin,TX

©John Berry Assoc.

Slide 1 of 45

MINERAL RESOURCE AVAILABILITY

OUTLINE

• Introduction

• Arguments

• History of Real Prices and Production

• Definitions

• Ore Grades, Resources and Life Expectancies

• Lognormal distribution of ore deposit sizes, grades, and locations

• Classical Economics views and problems with them

• External Costs and their Growth

• Competition for Land

• World-Wide Access to Minerals by Trade: Strategic Minerals

• “Ore is where you find it”

• Market concentration by country and company

• China and REE

• Role of Technology

• Role of capital requirements

• Examples: Iron, Copper, Titanium (Magnesium)

• Minerals and the Law of Supply and Demand

• Deposit Types, Prices and Volumes

• Implications of “Lumpy” Supply Curve

• Technological advances in Exploration, Mining, and substitution.

• Conclusions: Future of Minerals Availability

©John Berry Assoc.

Slide 2 of 45

MINERAL RESOURCE AVAILABILITY

INTRODUCTION

CIVILIZATION:

Tools: Stone>> Bronze>> Iron >>Machines (Alloys)>> Semi-conductors (Exotics)

ALL are based on mineral resources: Mining goes right back to the beginning

©John Berry Assoc.

Slide 3 of 45

Grime’s Graves ©Nic McPhee: 3000BC;433 shafts, 96 ac.

INDUSTRIAL CIVILIZATION:

Fossil Energy is the basic enabler:

Petroleum production has not increased since 2003.

Petroleum usage per person peaked in 1979 (R. Duncan, 2000) Pre-contact

Copper Mining, Kansanshi, Zambia

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 4 of 45

ARGUMENTS

Availability:

Inverse of Opportunity Cost, or what other goods must be given up to obtain a mineral commodity.

Real prices of a commodity Opportunity costs availability (Tilton, 2001).

In the Past:

Real prices of most mineral commodities have been flat or gone down almost continuously

since the beginning of the industrial revolution. This was due to three factors:

• Increased areas of land to explore

• Increased use of fossil energy to replace human labor

• Continually advancing technology.

In the future:

• No new frontiers left to explore

• Increasing energy prices

• Exponentially increasing production

• Asymptotically decreasing ore grades

• Increasing competition for land

• Exponentially increasing external costs

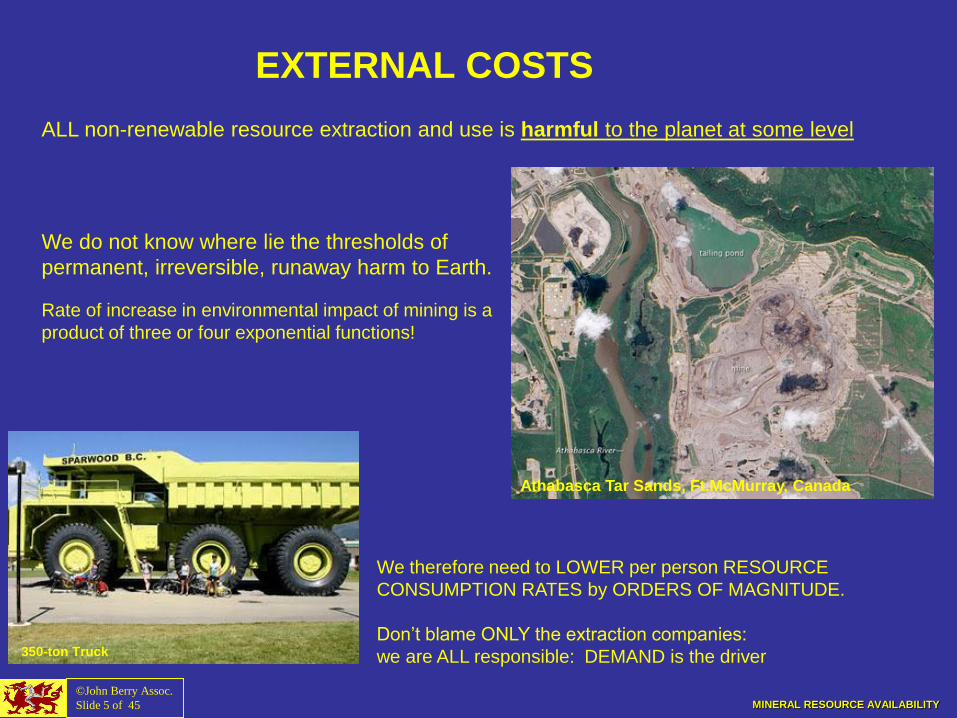

EXTERNAL COSTS

ALL non-renewable resource extraction and use is harmful to the planet at some level

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 5 of 45

350-ton Truck

Athabasca Tar Sands, Ft.McMurray, Canada

We do not know where lie the thresholds of

permanent, irreversible, runaway harm to Earth.

Rate of increase in environmental impact of mining is a

product of three or four exponential functions!

We therefore need to LOWER per person RESOURCE

CONSUMPTION RATES by ORDERS OF MAGNITUDE.

Don’t blame ONLY the extraction companies:

we are ALL responsible: DEMAND is the driver

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 6 of 45

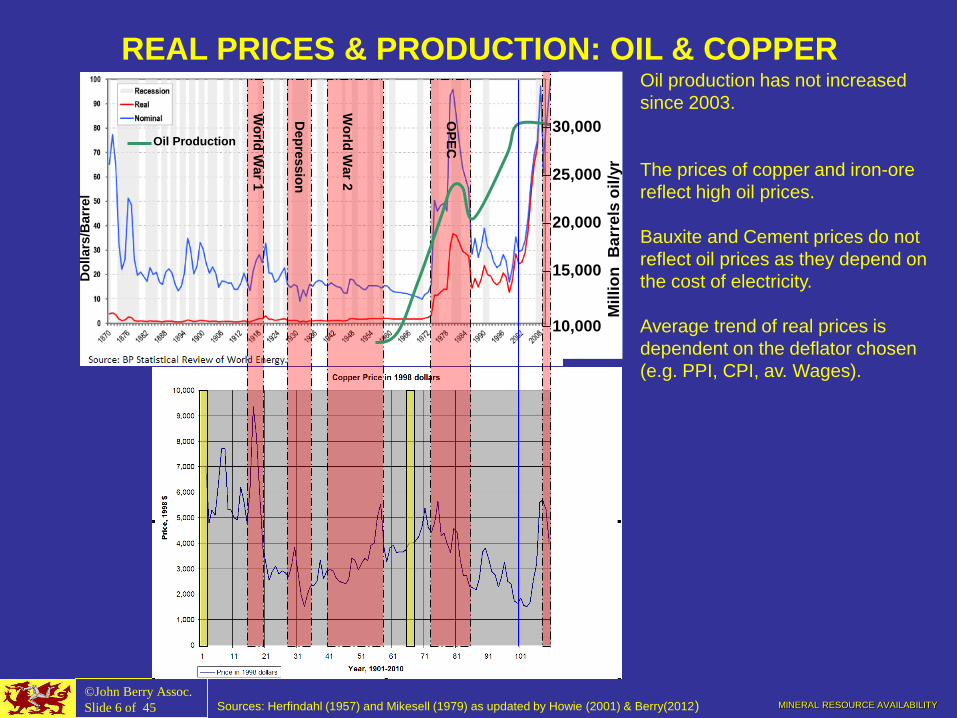

REAL PRICES & PRODUCTION: OIL & COPPER

Sources: Herfindahl (1957) and Mikesell (1979) as updated by Howie (2001) & Berry(2012)

Do

llars

/Barr

el

10,000

30,000

25,000

20,000

15,000

Mil

lio

n

Ba

rre

ls o

il/y

r

Oil Production

Wo

rld W

ar 1

Wo

rld W

ar 2

Dep

ressio

n

OP

EC

Oil production has not increased

since 2003.

The prices of copper and iron-ore

reflect high oil prices.

Bauxite and Cement prices do not

reflect oil prices as they depend on

the cost of electricity.

Average trend of real prices is

dependent on the deflator chosen

(e.g. PPI, CPI, av. Wages).

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 7 of 45

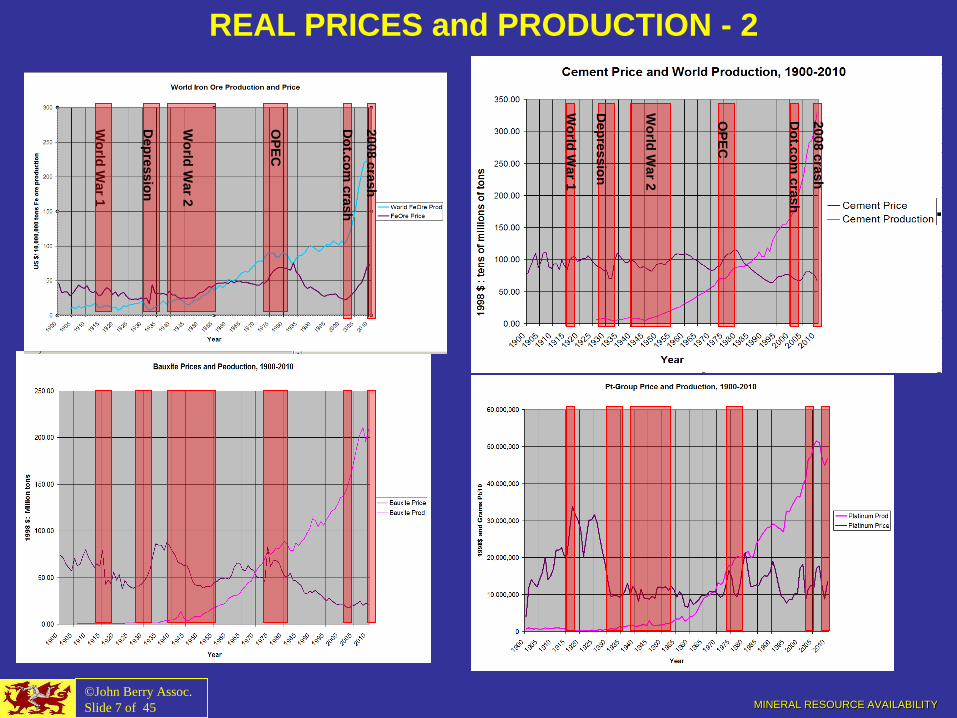

REAL PRICES and PRODUCTION - 2

Wo

rld W

ar 1

Dep

ressio

n

Dep

ressio

n

Wo

rld W

ar 1

Wo

rld W

ar 2

Wo

rld W

ar 2

OP

EC

OP

EC

Do

t.co

m c

rash

Do

t.co

m c

rash

2008 c

rash

2008 c

rash

MINERAL RESOURCE AVAILABILITY

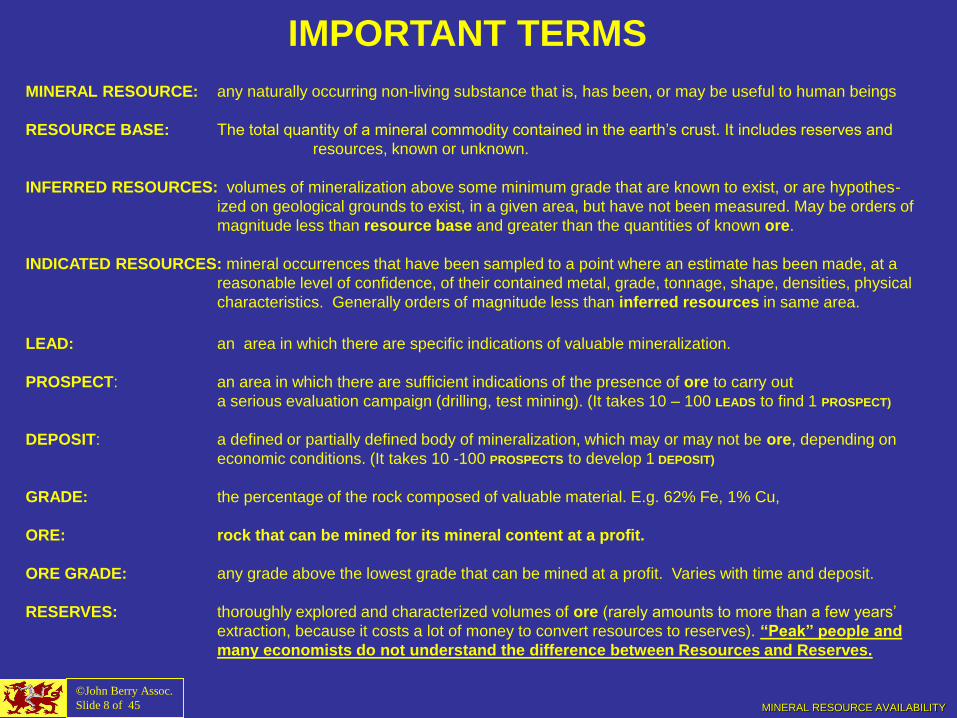

IMPORTANT TERMS MINERAL RESOURCE: any naturally occurring non-living substance that is, has been, or may be useful to human beings

RESOURCE BASE: The total quantity of a mineral commodity contained in the earth’s crust. It includes reserves and

resources, known or unknown.

INFERRED RESOURCES: volumes of mineralization above some minimum grade that are known to exist, or are hypothes-

ized on geological grounds to exist, in a given area, but have not been measured. May be orders of

magnitude less than resource base and greater than the quantities of known ore.

INDICATED RESOURCES: mineral occurrences that have been sampled to a point where an estimate has been made, at a

reasonable level of confidence, of their contained metal, grade, tonnage, shape, densities, physical

characteristics. Generally orders of magnitude less than inferred resources in same area.

LEAD: an area in which there are specific indications of valuable mineralization.

PROSPECT: an area in which there are sufficient indications of the presence of ore to carry out

a serious evaluation campaign (drilling, test mining). (It takes 10 – 100 LEADS to find 1 PROSPECT)

DEPOSIT: a defined or partially defined body of mineralization, which may or may not be ore, depending on

economic conditions. (It takes 10 -100 PROSPECTS to develop 1 DEPOSIT)

GRADE: the percentage of the rock composed of valuable material. E.g. 62% Fe, 1% Cu,

ORE: rock that can be mined for its mineral content at a profit.

ORE GRADE: any grade above the lowest grade that can be mined at a profit. Varies with time and deposit.

RESERVES: thoroughly explored and characterized volumes of ore (rarely amounts to more than a few years’

extraction, because it costs a lot of money to convert resources to reserves). “Peak” people and

many economists do not understand the difference between Resources and Reserves.

©John Berry Assoc.

Slide 8 of 45

MINERAL RESOURCE AVAILABILITY

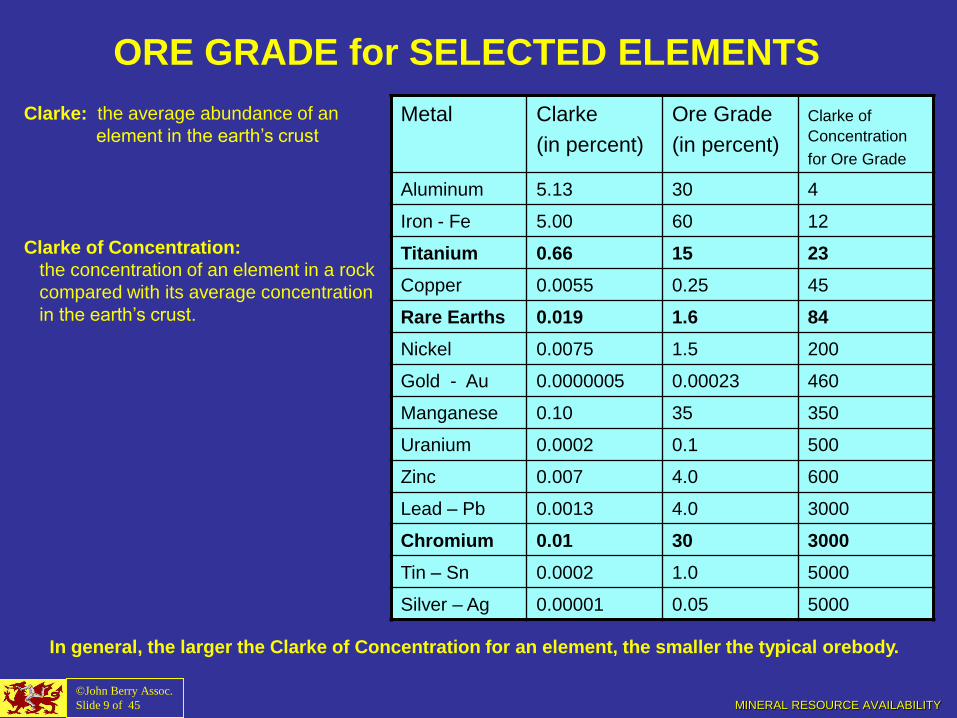

ORE GRADE for SELECTED ELEMENTS

Metal Clarke

(in percent)

Ore Grade

(in percent)

Clarke of Concentration

for Ore Grade

Aluminum 5.13 30 4

Iron - Fe 5.00 60 12

Titanium 0.66 15 23

Copper 0.0055 0.25 45

Rare Earths 0.019 1.6 84

Nickel 0.0075 1.5 200

Gold - Au 0.0000005 0.00023 460

Manganese 0.10 35 350

Uranium 0.0002 0.1 500

Zinc 0.007 4.0 600

Lead – Pb 0.0013 4.0 3000

Chromium 0.01 30 3000

Tin – Sn 0.0002 1.0 5000

Silver – Ag 0.00001 0.05 5000

Clarke: the average abundance of an

element in the earth’s crust

Clarke of Concentration:

the concentration of an element in a rock

compared with its average concentration

in the earth’s crust.

©John Berry Assoc.

Slide 9 of 45

In general, the larger the Clarke of Concentration for an element, the smaller the typical orebody.

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 10 of 45

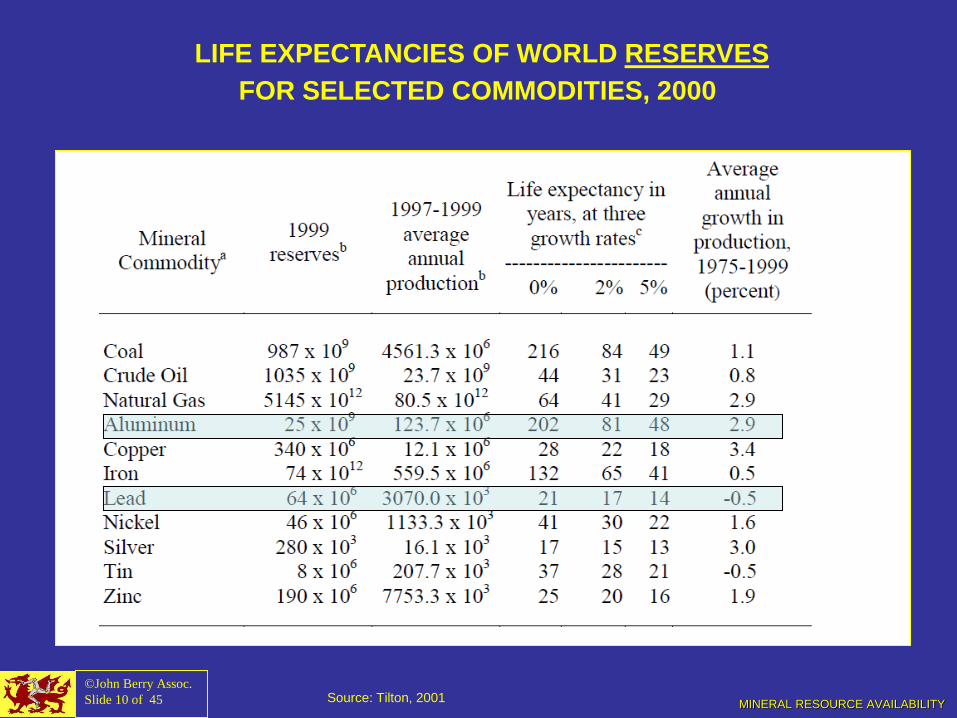

LIFE EXPECTANCIES OF WORLD RESERVES

FOR SELECTED COMMODITIES, 2000

Source: Tilton, 2001

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 11 of 45

SOURCE: Tilton, 2001, who used Brobst & Pratt, 1973; Lee & Yao, 1970 for the Clarke)

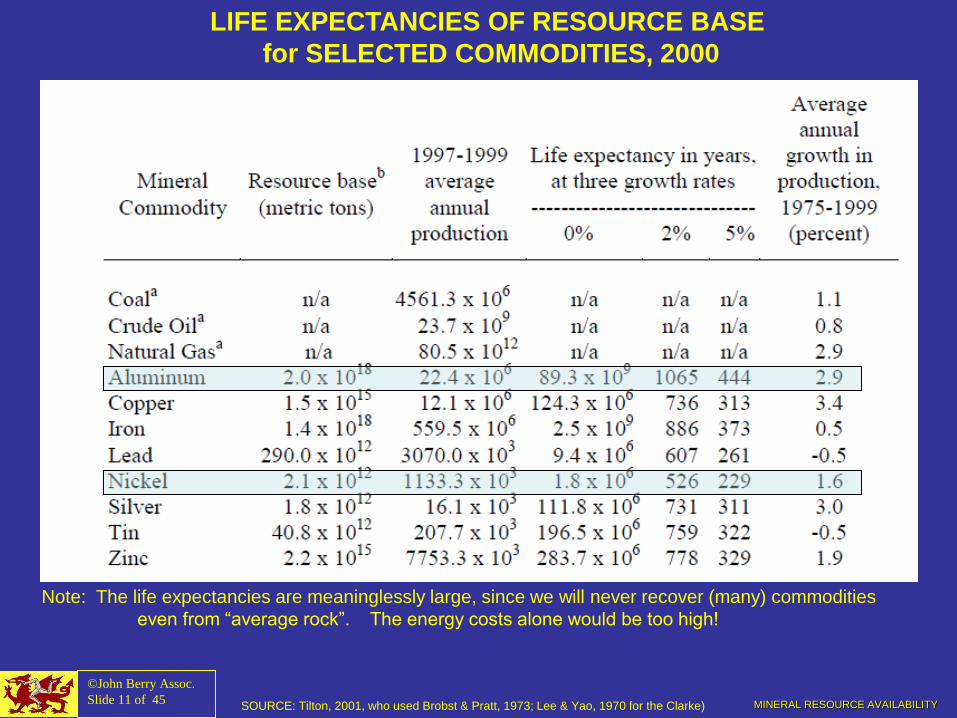

LIFE EXPECTANCIES OF RESOURCE BASE

for SELECTED COMMODITIES, 2000

Note: The life expectancies are meaninglessly large, since we will never recover (many) commodities

even from “average rock”. The energy costs alone would be too high!

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 38 of 45

THE LOG-NORMAL DISTRIBUTION

“A continuous probability distribution of a random variable whose logarithm is normally distributed”

VIRTUALLY ALL GEOLOGICAL PHENOMENA ARE LOG-NORMALLY DISTRIBUTED, including SIZES AND GRADES OF

MINERAL DEPOSITS. Thus MOST OF THE SUPPLY IS IN A FEW VERY LARGE or VERY HIGH-GRADE OREBODIES.

Most of the World’s Mineral Supply is in A FEW BIG MINES:

For the distribution above, the threshold for the top 2.3% of the deposits is

4 times the Median. This is “equivalent” to a normal distribution with

¯x=100, σ=150

A log-normal distribution with original scale (a) and with logarithmic scale (b).

Shaded areas = 1 and 2 σ (from http://stat.ethz.ch/~stahel/lognormal/bioscience.pdf)

Clarke

Massive

sulfides Veins

Grade

To

nn

age

Multimodal distribution of

elements in Earth’s crust

MINERAL RESOURCE AVAILABILITY

Laws of Deposit Size and Grade:

• Ore grade and tonnage statistical

distributions are lognormal, both

within deposits and across deposits:

• Most ore is thus in a few very large

deposits.

• For Copper - Mines

#1: Escondida, Chile: 8% 1.3 Mt 2008

#2: Chuquicamata, Chile: 6% 0.9 Mt 2006

#3: Grasberg, Indon: 4% 0.6 Mt 2006

Bingham Canyon, UT: 265,600 t 2006

Highland Valley, BC: 119,300 t 2008

The top 3 mines produce around 18% of the

world’s copper

• For Copper – Production by country, 2009 Chile: 5,941,000 Mt 34% 34%

Peru: 1,407,000 Mt 8%

USA: 1,302,000 Mt 7%

China: 1,171,000 Mt 7%

Indonesia: 1,098,000 Mt 6% 62%

Australia: 941,000 Mt 5%

Russia: 745,000 Mt 4%

Zambia: 614,000 Mt 4%

Canada: 540,000 Mt 3%

Poland: 484,000 Mt 3%______ 81%

Example: Porphyry Copper Deposits. Lognormal

Distribution of Ore Deposit Tonnage. These are

the largest class of copper deposits, and also

contain Au, Ag, and Mo. The vertical lines indicate

the 10th, 50th and 90th percentile of deposits.

©John Berry Assoc.

Slide 39 of 45 http://www.copper.org/resources/market_data/pdfs/annual_data.pdf

P90/median = 6.3

MINERAL RESOURCE AVAILABILITY

Source: Singer ©John Berry Assoc.

Slide 41 of 45

DEPOSIT TYPES, GRADES AND TONNAGE: GOLD

1850-1920

Viable at $24/oz

1890-1990

Viable at $35/oz

1980-Present

Viable at $300/oz

Gold is a by-product

Price barely matters

NOTES:

Not shown: Since 1980 there has been a modern gold rush for SH/HS Gold in Nevada, but it

takes ~500 of these deposits to replace the output from 1 Witwatersrand deposit,

Their average grade is 1/7 that of the Witwatersrand, which is a “Paleoplacer”.

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 12 of 45

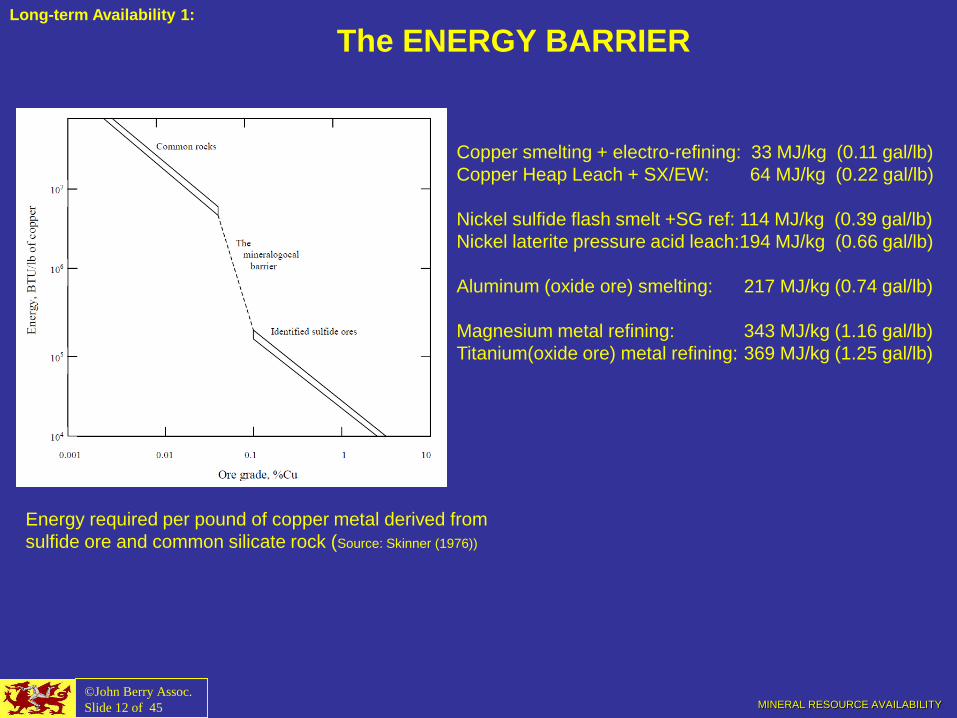

The ENERGY BARRIER

Energy required per pound of copper metal derived from

sulfide ore and common silicate rock (Source: Skinner (1976))

Long-term Availability 1:

Copper smelting + electro-refining: 33 MJ/kg (0.11 gal/lb)

Copper Heap Leach + SX/EW: 64 MJ/kg (0.22 gal/lb)

Nickel sulfide flash smelt +SG ref: 114 MJ/kg (0.39 gal/lb)

Nickel laterite pressure acid leach:194 MJ/kg (0.66 gal/lb)

Aluminum (oxide ore) smelting: 217 MJ/kg (0.74 gal/lb)

Magnesium metal refining: 343 MJ/kg (1.16 gal/lb)

Titanium(oxide ore) metal refining: 369 MJ/kg (1.25 gal/lb)

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 13 of 45

TWO CLASSICAL ECONOMICS VIEWS

Two approaches to analyzing exhaustion and depletion

Physical: Mineral resources occur as deposits in the earth that were formed in geologic time

and cannot be duplicated in human time. Removal of ore directly depletes the

resource.

The Pure Theory of Exhaustion (the Gray-Hotelling Theory), has been developed to

fit this physical view. (p.457)

Economic Approach:

“Minerals … have not limited society’s welfare in the past. Nor do they have the potential

for limiting the welfare of mankind in the future, so long as certain conditions are

maintained.

• Internalization of external environmental damages,

• Access to the earth’s crust for exploration,

• Worldwide trade access to raw materials and,

• Prevention of market control by either sellers or buyers.

“If these rules … are followed, markets will provide supplies and ration use so that minerals and

materials will be available to meet society’s needs without significantly increasing costs for a very long

time, probably for ever. (p.457)” VOGELY, William A., Nonfuel Minerals and the World Economy.

Chapter 15 in REPETTO, Robert, ed., 1985: The Global Possible.

Resources, Development, and the New Century. Yale UP, New Haven.

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 14 of 45

PROBLEMS WITH THE PHYSICAL AND ECONOMIC VIEWS

• The Gray-Hotelling Theory ignores new discovery, technology, and substitution

• The “Economic Approach” has severe limitations, stemming from:

1. Internalization of external environmental damages:

Taxation vs regulation vs markets in “credits”

2. Access to the earth’s crust for exploration (Competition for land)

Cities, farms, Wilderness Areas & Parks & Ice “sterilize” much of it.

3. Worldwide trade access to raw materials

Deposit distribution is “lumpy” – haves and have nots.

Some people don’t play by our rules

4. Prevention of market control by either sellers or buyers.

Mineral deposits are log-normally distributed

many more low-grade deposits than high grade

many more small deposits than large ones

Log-normal distribution and capital intensive operations give opportunities

for market control by companies (DeBeers) & countries (China)

soil

overburden

MINERAL RESOURCE AVAILABILITY

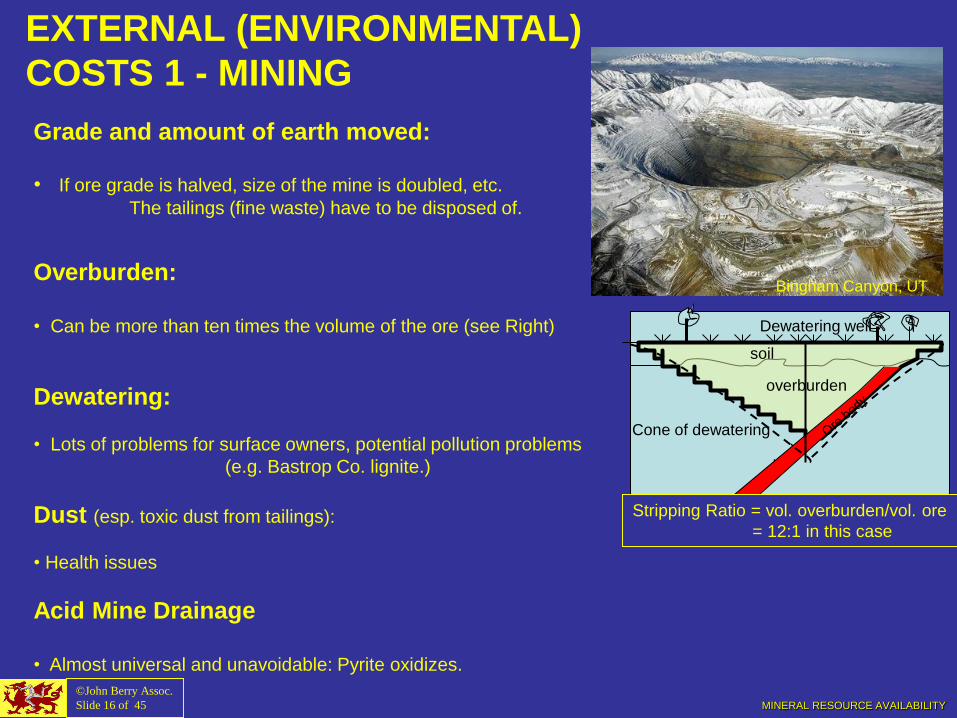

EXTERNAL (ENVIRONMENTAL)

COSTS 1 - MINING

Grade and amount of earth moved:

• If ore grade is halved, size of the mine is doubled, etc.

The tailings (fine waste) have to be disposed of.

Overburden:

• Can be more than ten times the volume of the ore (see Right)

Dewatering:

• Lots of problems for surface owners, potential pollution problems

(e.g. Bastrop Co. lignite.)

Dust (esp. toxic dust from tailings):

• Health issues

Acid Mine Drainage

• Almost universal and unavoidable: Pyrite oxidizes.

Stripping Ratio = vol. overburden/vol. ore

= 12:1 in this case

Dewatering well

Cone of dewatering

Bingham Canyon, UT

©John Berry Assoc.

Slide 16 of 45

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 17 of 45

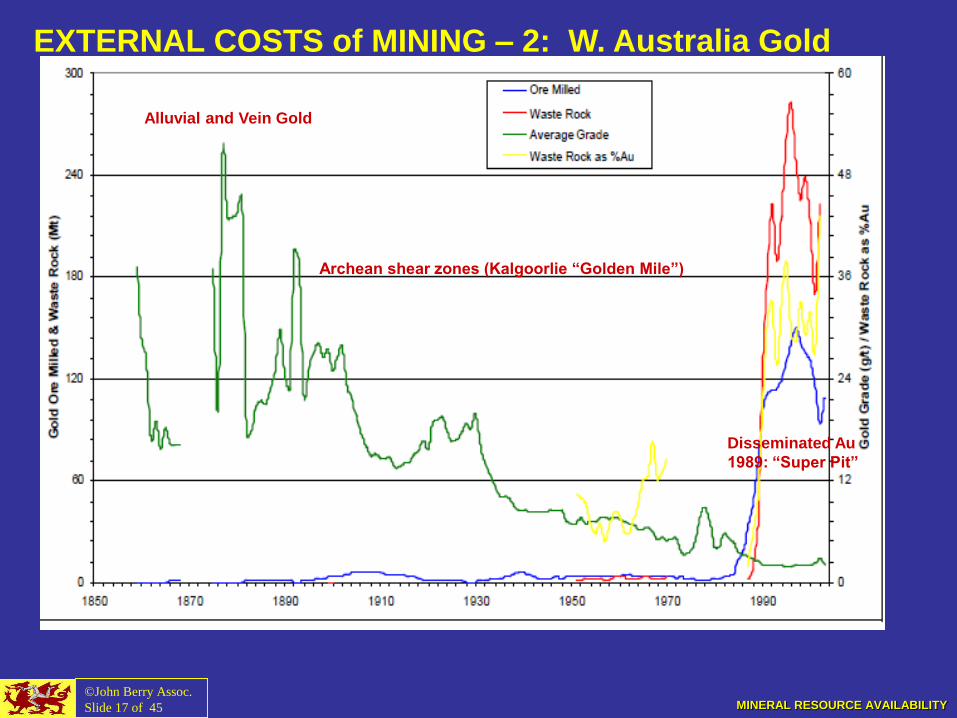

EXTERNAL COSTS of MINING – 2: W. Australia Gold

Alluvial and Vein Gold

Archean shear zones (Kalgoorlie “Golden Mile”)

Disseminated Au

1989: “Super Pit”

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 18 of 45

EXTERNAL COSTS 3: SMELTING AND REFINING

Water Pollution:

Cadmium: Imperial Zinc, Bristol Channel, UK

Mercury: Minami Bay, Japan

Soil Pollution:

Coweeta Forest Research Station, NC: 1% SO4 80 mi downwind of Ducktown, TN

Ducktown, TN: Completely deforested by Cu in soil.

Nkana, Zambia: 0.5% Cu in surface soil after 25 years.

Air Pollution:

Nkana, Zambia: 550 tons CuSO4/mo

Rockdale, TX: Fluorosis from Al smelter?

Solutions:

Taxation (Europe), Regulation (USA),

Cap-and-Trade schemes(USA/EU)

Not very specific; subject to corruption & politics;

no $ value for damage

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 19 of 45

MODEL FOR GROWTH OF TOTAL EXTERNAL COSTS

Rate of Growth of External Costs = Rate of Increase of Population x rate of increase in GDP per person x

rate of increase in intensity of use x rate of increase in stripping ratio

divided by the rate of decrease in average ore grade

dWP * dGDPind * dI * dS

dE dt dt dt dt

---- = ----------------------------------- integrated over all countries & commodities

dt dG

dt

Where E = environmental and other external costs

WP = World Population

GDPind= income per person

I = Intensity of use of each commodity

S = Average stripping ratio

G = average ore grade for each commodity.

This can be simplified to :

dP * dS

dE dt dt

---- = --------------- integrated over all commodities and types of impact.

dt dG

dt

where P = total world production of a commodity

A very rough estimate of this would be = 1.10 * 1.05 * 1/0.985 = 1.17 or 17% per year; doubling time of 3.3 years

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 20 of 45

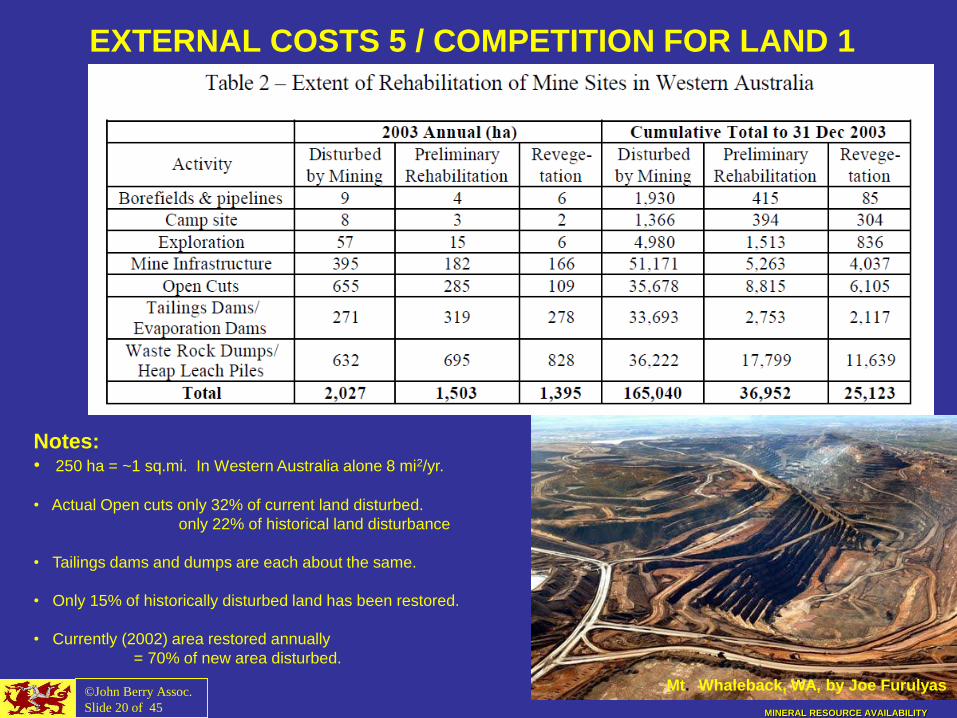

EXTERNAL COSTS 5 / COMPETITION FOR LAND 1

Mt. Whaleback, WA, by Joe Furulyas

Notes: • 250 ha = ~1 sq.mi. In Western Australia alone 8 mi2/yr.

• Actual Open cuts only 32% of current land disturbed.

only 22% of historical land disturbance

• Tailings dams and dumps are each about the same.

• Only 15% of historically disturbed land has been restored.

• Currently (2002) area restored annually

= 70% of new area disturbed.

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 21 of 45

Commodities Ranked by Worldwide Area of Land Disturbed per Year

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000

Peat

Zirconium

Feldspar

Nickel

Lead

Molybdenum

Industrial sand

Manganese

Vanadium*

Kaolin

Fluorspar

Zinc

Gypsum

Lime

Gold

Clays

Petroleum

Bauxite

Boron

Lignite

Iron Ore

Chromites

Crushed rock

Copper

Cement

Phosphates

Diamonds

Coal

Sand/grav

Co

mm

od

ity

Square Kilometers

800 1600 2400 3200 4000 4800 5600 6400 sq.mi.

COMPETITION FOR LAND 2

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 22 of 45

“ORE IS WHERE YOU FIND IT” or “If it isn’t there you won’t find it”

• Ore deposits are rare

• If you make a mineral deposit inaccessible (e.g.ANWR), you can’t replace it.

• There has to be favorable geology

You can’t move a deposit from where you don’t want it to somewhere else.

Some countries have it all, some have none (Strategic Minerals)

• Exploration requires access to lots of land

Rule of thumb: 100 leads > 10 prospects >1 mine

(This also implies a need for large companies)

It usually takes 5 exploration campaigns

to delineate a mineable deposit.

DiaVik Diamond Mines, NWT, Canada

COMPETITION FOR LAND 3

Kansanshi, Zambia: old head frame

Copper Flower

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 23 of 45

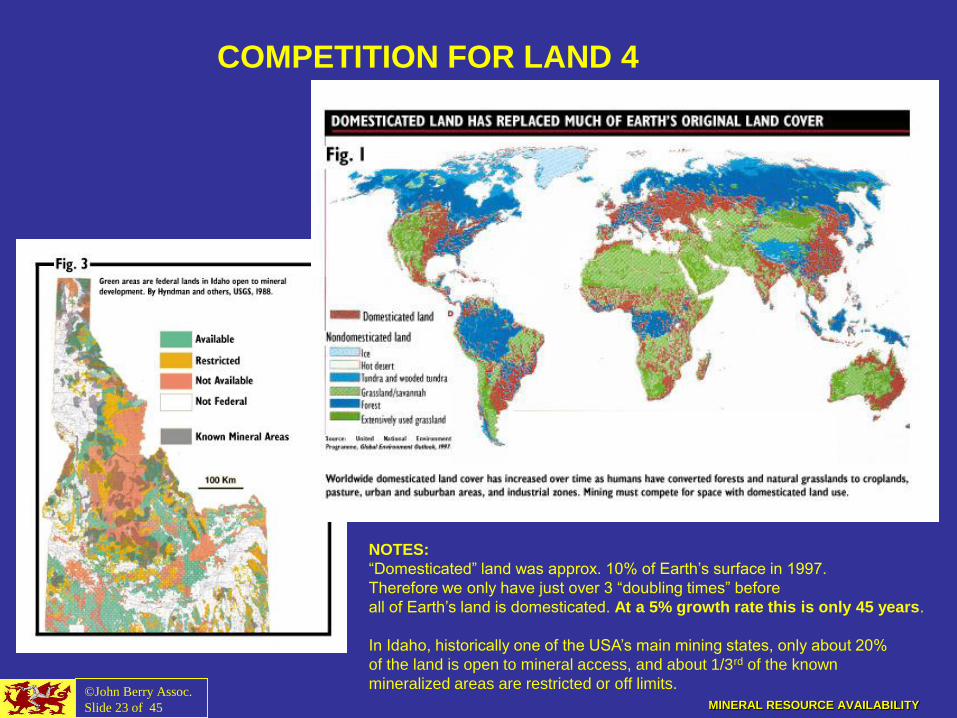

COMPETITION FOR LAND 4

NOTES:

“Domesticated” land was approx. 10% of Earth’s surface in 1997.

Therefore we only have just over 3 “doubling times” before

all of Earth’s land is domesticated. At a 5% growth rate this is only 45 years.

In Idaho, historically one of the USA’s main mining states, only about 20%

of the land is open to mineral access, and about 1/3rd of the known

mineralized areas are restricted or off limits.

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 24 of 45

WORLD-WIDE FREE ACCESS 1:

STRATEGIC MINERALS

Data: USGS, Mineral Commodity Summaries, 2011.

Definition: Minerals essential to the national

defense for which during war we are

wholly or partly dependent upon

sources outside the continental

limits of the United States

Most critical: Platinum Group Metals (PGM),

NAS (2007) Rare Earths (REE) (La>Nd>Dy>Tb)

Indium,

Manganese

Niobium (Columbium) (ColTan)

Beryllium

Uranium

Chromium

Cobalt

Tungsten

Petroleum

Source: http://www.helium.com/items/

1949042-what-are-strategic-minerals

MINERAL RESOURCE AVAILABILITY

STRATEGIC MINERALS - 2

• Thus, different mineral commodities are Strategic for different countries

(e.g. China: copper, chromium, platinum

Europe: almost everything)

• Strategic Mineral Endowment and War:

1925: geologist C.K.Leith predicted WWII and the line-up because:

• USA, the USSR, The British and French Empires were virtually self-sufficient in

mineral resources,

• Germany, Italy, and Japan were lacking in all but a few.

(C.K.Leith. Political Control of mineral resources, Foreign Affairs, July 1925.)

©John Berry Assoc.

Slide 25 of 45

Free Access to Minerals 2:

MINERAL RESOURCE AVAILABILITY

CHINA

"China has made the assured access to strategic mineral imports a critical component

of its geopolitical strategy and is moving aggressively to purchase control of mineral

concessions and mining companies.

“China’s resulting role in the mineral trade has increased Western security community

concern over strategic minerals to its highest point since the end of the Cold War.”

Recap: Leonid Brezhnev, 1973: “Our aim is to gain control of the two great treasure

houses on which the West depends, the energy treasure house of the Persian Gulf

and the mineral treasure house of Central and Southern Africa”” (Nixon 1980).

(JLB comment) It was this kind of fear, that the US would cut off Japan’s oil supply, that

led directly to Pearl Harbor.

Source: Butts K H, B Bankus & A Norris, 2011. Strategic Minerals:

Is China’s Consumption a threat to United States Security? US

Army War College, CSL Issue Paper, v. 7-11.

©John Berry Assoc.

Slide 26 of 45

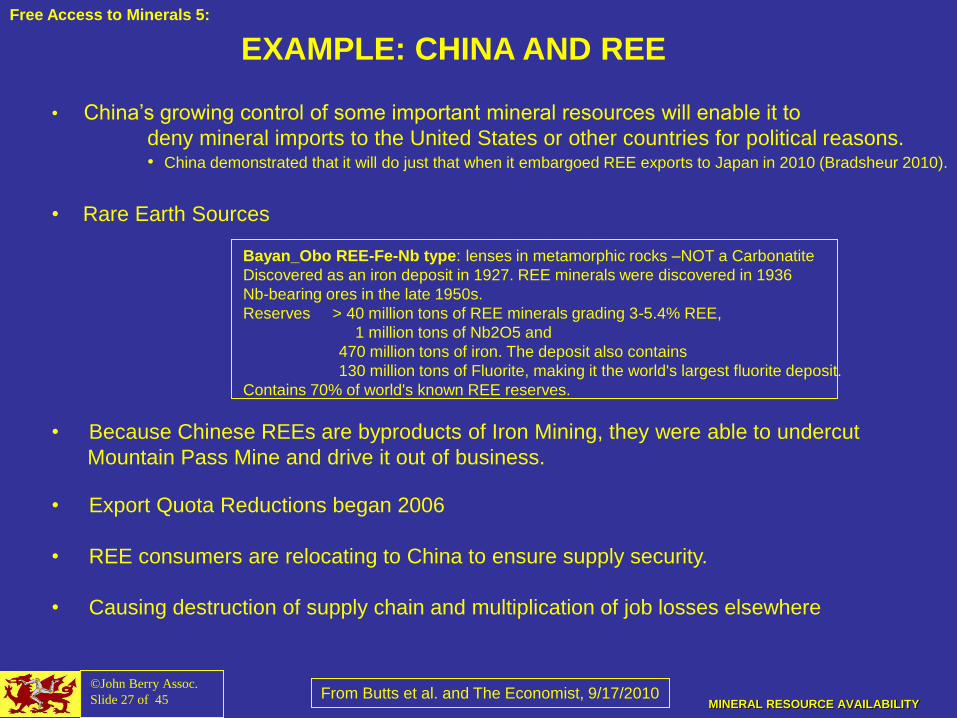

Free Access to Minerals 3:

• China’s growing control of some important mineral resources will enable it to

deny mineral imports to the United States or other countries for political reasons. • China demonstrated that it will do just that when it embargoed REE exports to Japan in 2010 (Bradsheur 2010).

• Rare Earth Sources

Bayan_Obo REE-Fe-Nb type: lenses in metamorphic rocks –NOT a Carbonatite

Discovered as an iron deposit in 1927. REE minerals were discovered in 1936

Nb-bearing ores in the late 1950s.

Reserves > 40 million tons of REE minerals grading 3-5.4% REE,

1 million tons of Nb2O5 and

470 million tons of iron. The deposit also contains

130 million tons of Fluorite, making it the world's largest fluorite deposit.

Contains 70% of world's known REE reserves.

• Because Chinese REEs are byproducts of Iron Mining, they were able to undercut

Mountain Pass Mine and drive it out of business.

• Export Quota Reductions began 2006

• REE consumers are relocating to China to ensure supply security.

• Causing destruction of supply chain and multiplication of job losses elsewhere

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 27 of 45

EXAMPLE: CHINA AND REE

From Butts et al. and The Economist, 9/17/2010

Free Access to Minerals 5:

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 28 of 45

Problems for New REE Mining Ventures:

Rare Earths occur with radioactive thorium or uranium.

Extraction, separation and refining are difficult. (Ion-exchange, fractional Xtallisation and liquid-liquid X)

Requires lots of water, acid and electricity

Handling the radioactive and chemical waste produced in the process adds significantly to the cost.

(The Economist, 9/17/2010)

A “Rare Earth Rush” is developing in the west, with major exploration projects in the USA, Alaska,

Canada, Australia, Greenland, Vietnam, and Estonia.

This will lead to a Rare Earth mining “bubble”, which will depress prices for many years.

Mining more rare earths in the West is just the beginning.

Rebuilding the downstream supply chain for them is equally important (Steve Jobs, 2010):

purification, alloying, fabrication, end usage (batteries, screens, etc).

Otherwise processing and fabrication will be in China!

CHINA AND REE ELEMENTS (Cont)

From Butts et al.

Free Access to Minerals 6:

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 30 of 45

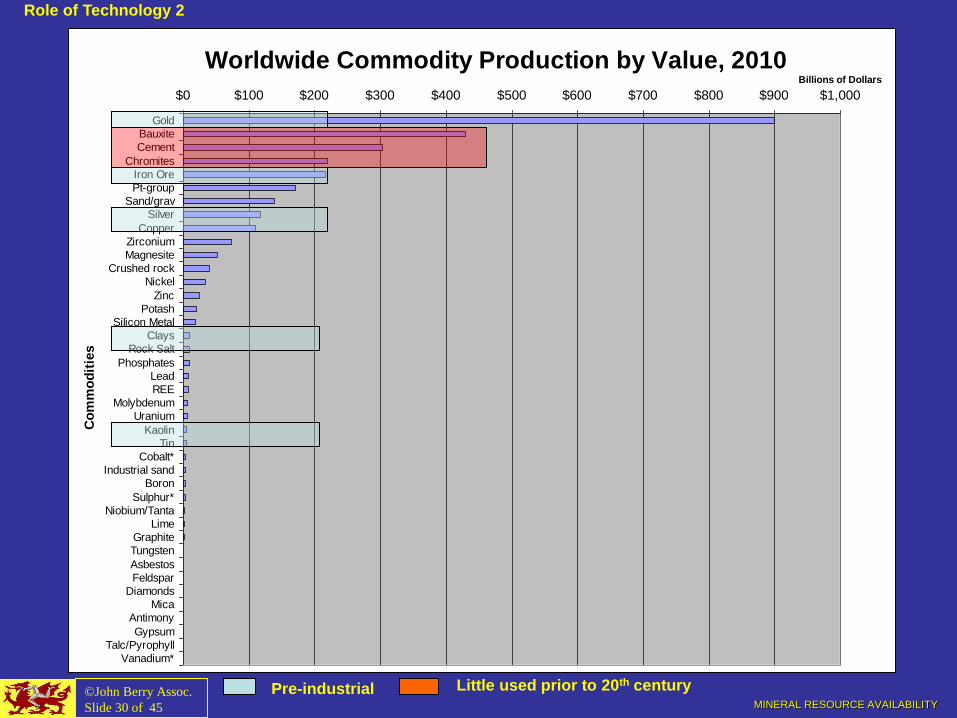

Worldwide Commodity Production by Value, 2010

$0 $100 $200 $300 $400 $500 $600 $700 $800 $900 $1,000

Gold

Bauxite

Cement

Chromites

Iron Ore

Pt-group

Sand/grav

Silver

Copper

Zirconium

Magnesite

Crushed rock

Nickel

Zinc

Potash

Silicon Metal

Clays

Rock Salt

Phosphates

Lead

REE

Molybdenum

Uranium

Kaolin

Tin

Cobalt*

Industrial sand

Boron

Sulphur*

Niobium/Tanta

Lime

Graphite

Tungsten

Asbestos

Feldspar

Diamonds

Mica

Antimony

Gypsum

Talc/Pyrophyll

Vanadium*

Co

mm

od

itie

sBillions of Dollars

Role of Technology 2

Pre-industrial Little used prior to 20th century

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 31 of 45

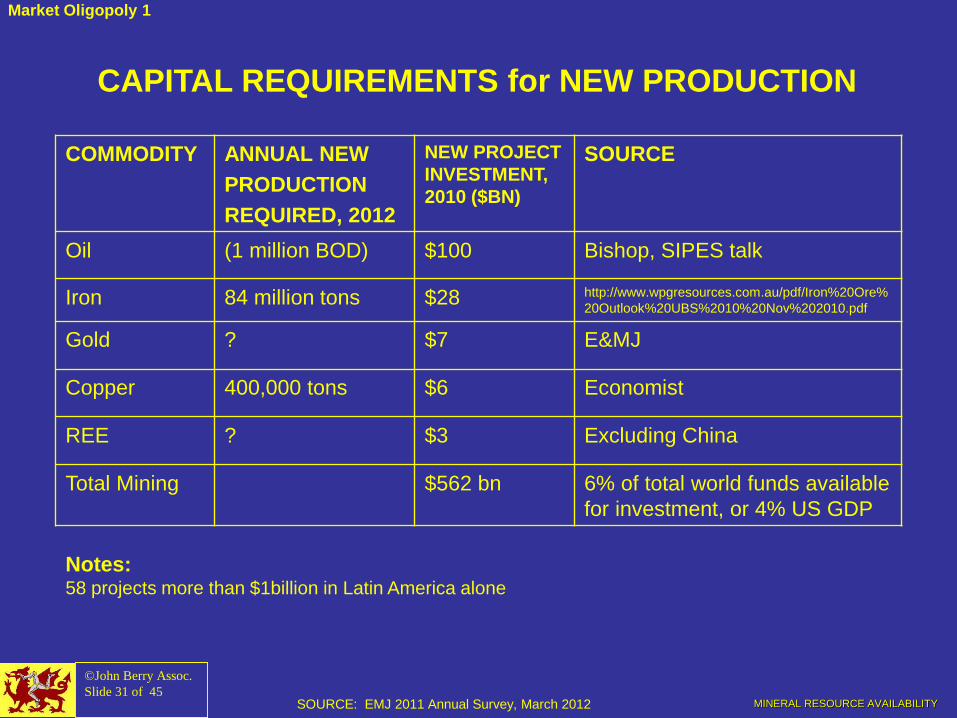

CAPITAL REQUIREMENTS for NEW PRODUCTION

SOURCE: EMJ 2011 Annual Survey, March 2012

COMMODITY ANNUAL NEW

PRODUCTION

REQUIRED, 2012

NEW PROJECT

INVESTMENT,

2010 ($BN)

SOURCE

Oil (1 million BOD) $100 Bishop, SIPES talk

Iron 84 million tons $28 http://www.wpgresources.com.au/pdf/Iron%20Ore%

20Outlook%20UBS%2010%20Nov%202010.pdf

Gold ? $7 E&MJ

Copper 400,000 tons $6 Economist

REE ? $3 Excluding China

Total Mining $562 bn 6% of total world funds available

for investment, or 4% US GDP

Notes: 58 projects more than $1billion in Latin America alone

Market Oligopoly 1

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 32 of 45

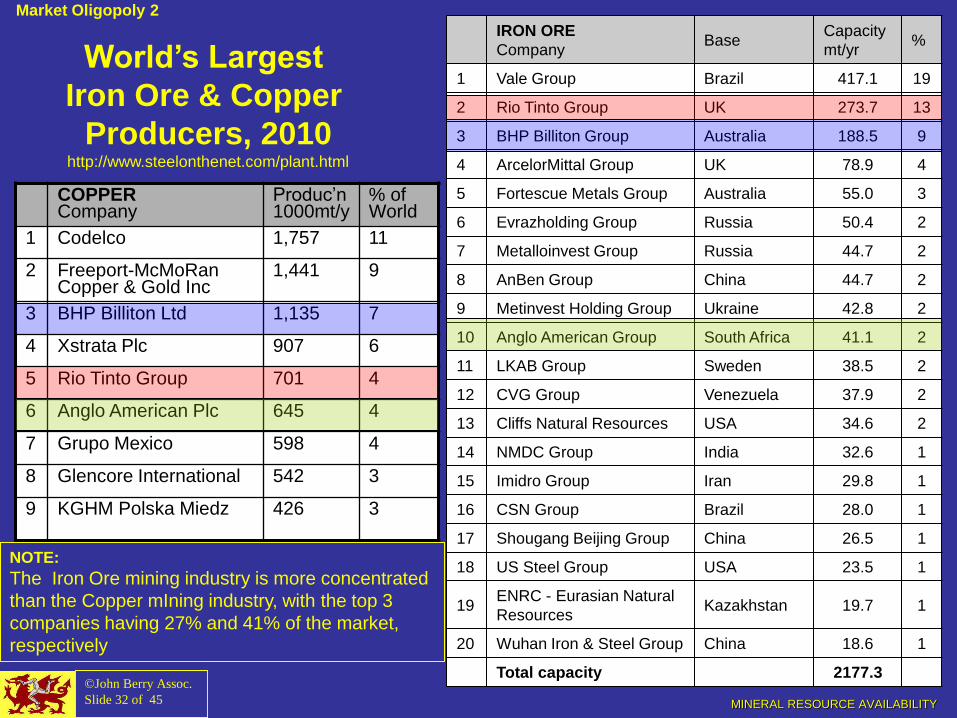

IRON ORE

Company Base

Capacity

mt/yr %

1 Vale Group Brazil 417.1 19

2 Rio Tinto Group UK 273.7 13

3 BHP Billiton Group Australia 188.5 9

4 ArcelorMittal Group UK 78.9 4

5 Fortescue Metals Group Australia 55.0 3

6 Evrazholding Group Russia 50.4 2

7 Metalloinvest Group Russia 44.7 2

8 AnBen Group China 44.7 2

9 Metinvest Holding Group Ukraine 42.8 2

10 Anglo American Group South Africa 41.1 2

11 LKAB Group Sweden 38.5 2

12 CVG Group Venezuela 37.9 2

13 Cliffs Natural Resources USA 34.6 2

14 NMDC Group India 32.6 1

15 Imidro Group Iran 29.8 1

16 CSN Group Brazil 28.0 1

17 Shougang Beijing Group China 26.5 1

18 US Steel Group USA 23.5 1

19 ENRC - Eurasian Natural

Resources Kazakhstan 19.7 1

20 Wuhan Iron & Steel Group China 18.6 1

Total capacity 2177.3

World’s Largest

Iron Ore & Copper

Producers, 2010 http://www.steelonthenet.com/plant.html

COPPER Company

Produc’n 1000mt/y

% of World

1 Codelco 1,757 11

2 Freeport-McMoRan Copper & Gold Inc

1,441 9

3 BHP Billiton Ltd 1,135 7

4 Xstrata Plc 907 6

5 Rio Tinto Group 701 4

6 Anglo American Plc 645 4

7 Grupo Mexico 598 4

8 Glencore International 542 3

9 KGHM Polska Miedz 426

3

NOTE:

The Iron Ore mining industry is more concentrated

than the Copper mIning industry, with the top 3

companies having 27% and 41% of the market,

respectively

Market Oligopoly 2

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 32a of 45

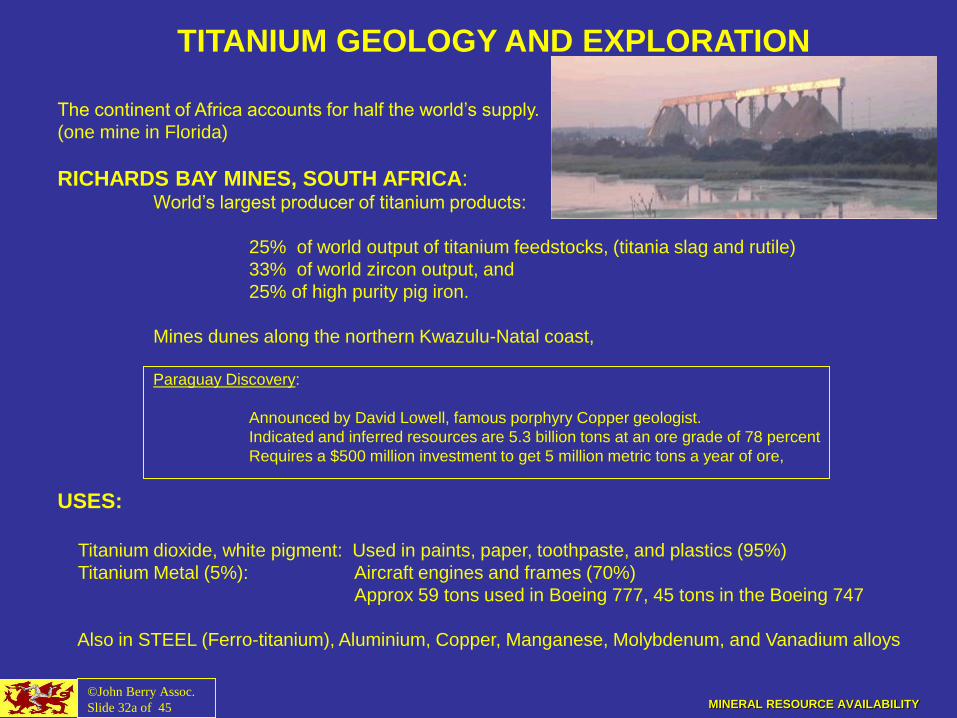

TITANIUM GEOLOGY AND EXPLORATION

The continent of Africa accounts for half the world’s supply.

(one mine in Florida)

RICHARDS BAY MINES, SOUTH AFRICA: World’s largest producer of titanium products:

25% of world output of titanium feedstocks, (titania slag and rutile)

33% of world zircon output, and

25% of high purity pig iron.

Mines dunes along the northern Kwazulu-Natal coast,

Paraguay Discovery:

Announced by David Lowell, famous porphyry Copper geologist.

Indicated and inferred resources are 5.3 billion tons at an ore grade of 78 percent

Requires a $500 million investment to get 5 million metric tons a year of ore,

USES:

Titanium dioxide, white pigment: Used in paints, paper, toothpaste, and plastics (95%)

Titanium Metal (5%): Aircraft engines and frames (70%)

Approx 59 tons used in Boeing 777, 45 tons in the Boeing 747

Also in STEEL (Ferro-titanium), Aluminium, Copper, Manganese, Molybdenum, and Vanadium alloys

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 32b of 45

TITANIUM & the MAGNESIUM SUPPLY

Titanium metal production consumes Magnesium on a 1:1 basis.

The United States was traditionally the major supplier of Magnesium,

To 1995: 45% of world production

Today; 7% of world production

1 domestic producer left, US Magnesium, in Utah.

Uses electrolysis of fused magnesium chloride from brines.

China is now the dominant supplier , pegged at 60%

1995: 4% of world production.

2005: 60% of world production .

China uses the silicothermic Pidgeon process:the reduction of the

oxide at high temperatures with silicon. http://en.wikipedia.org/wiki/Magnesium

Note: Both the manufacture of Magnesium and the subsequent manufacture of

Titanium require large quantities of energy (electrolysis at high temperatures).

Mineral

Supply

Curve

D3 Sm

MINERAL RESOURCE AVAILABILITY

SUPPLY INELASTICITY: “BREAKDOWNS” OF THE

STANDARD MODEL OF THE LAW OF SUPPLY AND DEMAND

“If demand increases and supply remains unchanged, then it leads

to higher equilibrium price and quantity, etc.“

• The Price vs Quantity curve for minerals tends to be stepped, or

“lumpy” (my term).

• The volume of mineral supply is price inelastic over the short term

(up to several years) once current production capacity is reached

(blue curve – vertical section):

• it may require a huge investment of time and money (up to

$20billion and 25 years, see sidebar) to bring in a new deposit.

• The reverse is true: if overcapacity develops, production can

not easily be shut-in. Therefore there are long periods (up to

20 years) when mineral prices are unsustainably low (oil from

1986-2002; copper 1975-2004 (PoCu “bubble”, next slide)).

Example, from The Economist, 1/24/2112:

Oyu Tolgoi Cu/Au Mine, Mongolia

Discovery: 2001

Explo Drilling: 2003

Cost to 1st production (2013): $6bn

Expenditure to 2020: $10bn

Full Prod.Rate (2018): 450,000t Cu/yr

(3% of global total)

Mine represents 30% Mongolian GDP

©John Berry Assoc.

Slide 33 of 45

D5 D4

Time

Transition to

Open-Cast Mining

Ore-Grade

$8

5%

4%

3%

1%

2%

0%

0.5%

Ore

-Gra

de

Veins

Skarns

Sedimentary Copper

$3

$4

$5

$6

$7

$0

$1

$2

Pri

ce

in

19

98 $

Lan

d A

rea

Dis

turb

ed

/yr

(km

2)

1000

0

400

800

Production (106tons/yr)

Price (1998$)

Land

Disturbance

(km2/yr

COPPER SUPPLY 1900-2030: PRICES, VOLUMES & LAND DISTURBANCE

INVERSE SUPPLY_DEMAND CURVE

MANY PORPHYRY COPPERS DISCOVERED

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 37 of 45

2050

Massive Sulfides

Porphyries

2000

PRICE SHOCK: SED CU

DEPOSITS IN FULL PRO-

DUCTION, NO NEW

DISCOVERIES FEW NEW PoCu

DISCOVERIES

INCREASING

ENVIRONMENTAL

ISSUES

Supply Inelasticity 5

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 43 of 45

TECHNOLOGY - NEW ORE DEPOSIT TYPES

Iron-Oxide-Copper-Gold (IOCG) Deposits.

Contain Uranium and some REEs. Grades similar to PoCu.

World-class Olympic Dam deposit in S.Australia

Seabed Mn Nodules: Grades similar to Porphyry copper.

Much more inaccessible. Environmentally impermissible?

SOURCES: http://www.technologyreview.com/energy/38458/ http://www.outotec.com/pages/Page.aspx?id=38091&epslanguage=EN

NEW MINING TECHNOLOGY Solvent Extraction/Electrowinning: VERY energy intensive. Very harmful chemicals.

“Virtual Mining”: Machines controlled from surface. Capital intensive

Solution Mining: Groundwater effects hard to control. Can be very

energy intensive.

SUBSTITUTION

Carbon Composites – dependent on petroleum?

Nanotubes - volume production

Organo-Metals

Outukumpu Zinc solvent extraction plant

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 45 of 45

CONCLUSIONS

1. No immediate threat of exhaustion of any important commodity: trouble starts around 2050.

2. A major flaw of most economists’ analyses: they ignore “colonial” expansion of 1900s.

3. The Supply Curve for Mineral Commodities is “Lumpy” because

• Mineral Deposit Distribution is Log-Normal – a few large deposits control supply

• Capital Requirements are huge (billions to tens of billions)

• Time required to bring in new capacity is measured in decades

• Exploration and development are subject to “Bubbles” (PoCu, Epithermal Gold, REE)

4. Population and economic growth is causing the exploitation of larger deposits of lower grade, causing

• Increased “lumpiness” of supply (capital, time, societal constraints)

• Increased political risk (“Lumpy” distribution of deposits; single country controlling > 50%)

• Increased market concentration (top 3 companies up to 50% of market).

• Exponentially increasing environmental damage (on the order of 20% per year)

5. Technology is leading to the use of more and more exotic minerals, which causes:

Increased refining cost (refining is generally more complex and energy intensive)

Increased environmental costs (low grades, noxious effluents)

6. In the long-term, prices are dependant on a race between technology and resource depletion.

Since 1800 technology has been winning the race, but as the frontier has closed

and resource grades approach the Clarke, this becomes more difficult.

7. The major constraints on mineral production are going to be external costs and land availability.

8. Thus the Opportunity Cost for many essential minerals will increase, particularly after 2050.

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 46 of 45

THE END

Thankyou!

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 1 of 54

MINERAL RESOURCE AVAILABILITY

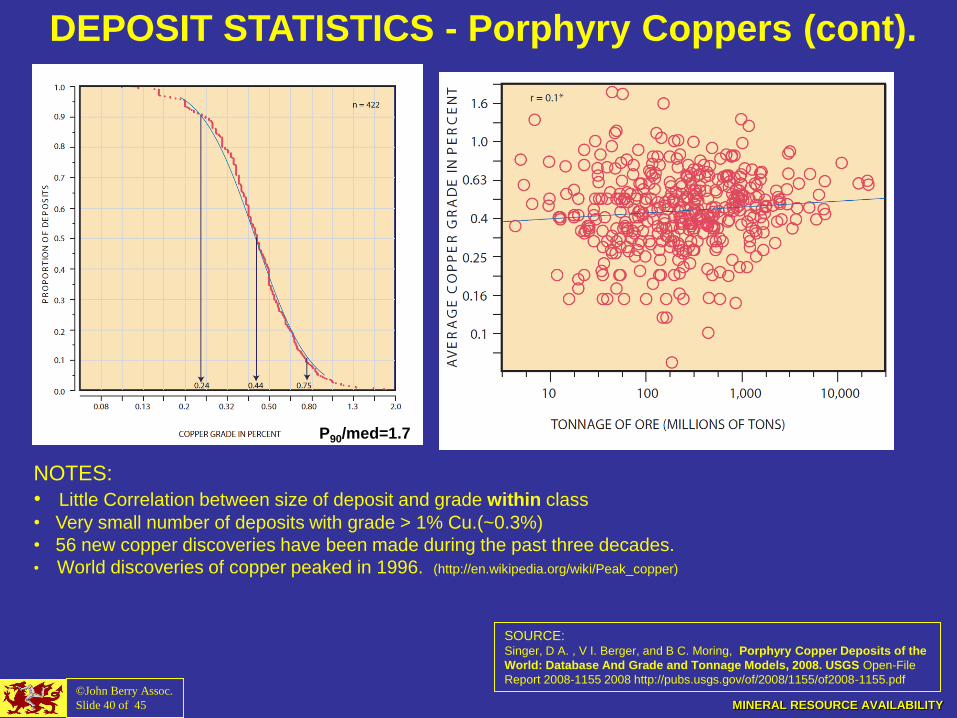

SOURCE: Singer, D A. , V I. Berger, and B C. Moring, Porphyry Copper Deposits of the

World: Database And Grade and Tonnage Models, 2008. USGS Open-File

Report 2008-1155 2008 http://pubs.usgs.gov/of/2008/1155/of2008-1155.pdf

NOTES:

• Little Correlation between size of deposit and grade within class

• Very small number of deposits with grade > 1% Cu.(~0.3%)

• 56 new copper discoveries have been made during the past three decades.

• World discoveries of copper peaked in 1996. (http://en.wikipedia.org/wiki/Peak_copper)

DEPOSIT STATISTICS - Porphyry Coppers (cont).

©John Berry Assoc.

Slide 40 of 45

P90/med=1.7

MINERAL RESOURCE AVAILABILITY

Source: Singer, Donald A, Grade and Tonnage Models for the ANALYSIS OF Nevada’s Mineral Resources. Chapter 11 in ???)

©John Berry Assoc.

Slide 42 of 45

WORLD AND NEVADA GOLD DEPOSIT STATISTICS

Grades: P90/median =2 Tonnage: P90/median = 7

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 15 of 45

MORE PROBLEMS WITH THE “ECONOMIC VIEW”

5. Log-normal distribution curve and high capital requirements also mean that the

supply curve gets increasingly “lumpy” with time, causing major price troughs and

spikes.

6. Technology sometimes creates more problems than it solves

• Many more elements used for very specific properties

• Huge capital investments required for low-grade

deposits.

• Exploration “bubbles”.

7 . Substitution is not always possible (e.g. Copper vs Silver)

8. The short horizon of economic thinking:

Consumption over the past century more than over all earlier centuries put

together.

Pace continues to accelerate (Source: Tilton, 2001, p.1-1)

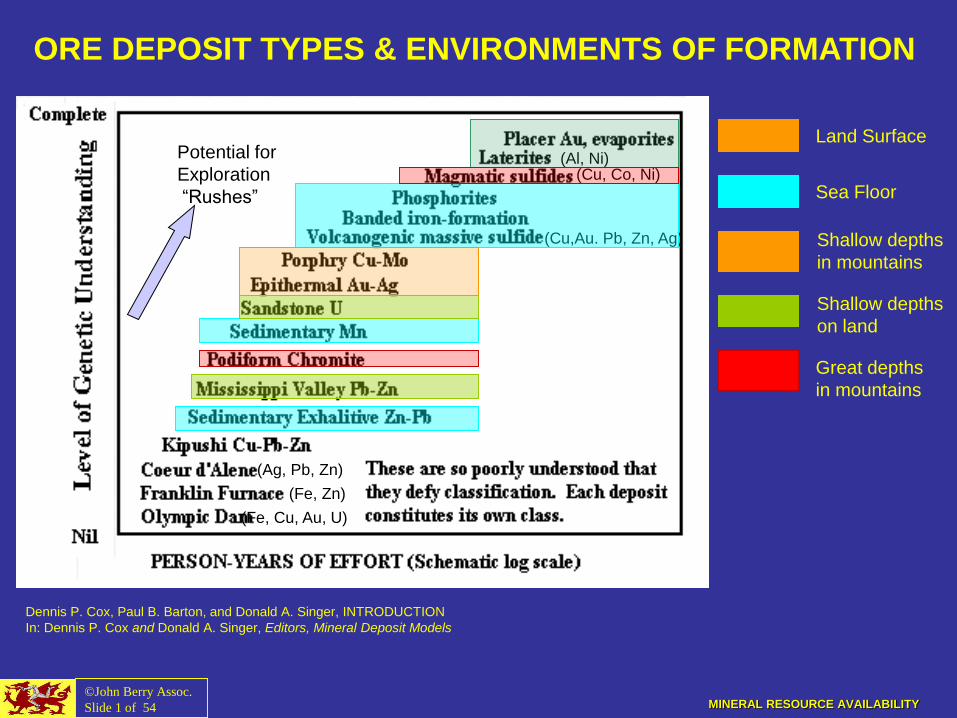

(Fe, Cu, Au, U)

(Ag, Pb, Zn)

(Fe, Zn)

(Al, Ni) (Cu, Co, Ni)

(Cu,Au. Pb, Zn, Ag)

Land Surface

Sea Floor

Shallow depths

in mountains

Shallow depths

on land

Great depths

in mountains

Potential for

Exploration

“Rushes”

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 1 of 54

Dennis P. Cox, Paul B. Barton, and Donald A. Singer, INTRODUCTION

In: Dennis P. Cox and Donald A. Singer, Editors, Mineral Deposit Models

ORE DEPOSIT TYPES & ENVIRONMENTS OF FORMATION

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 1 of 54

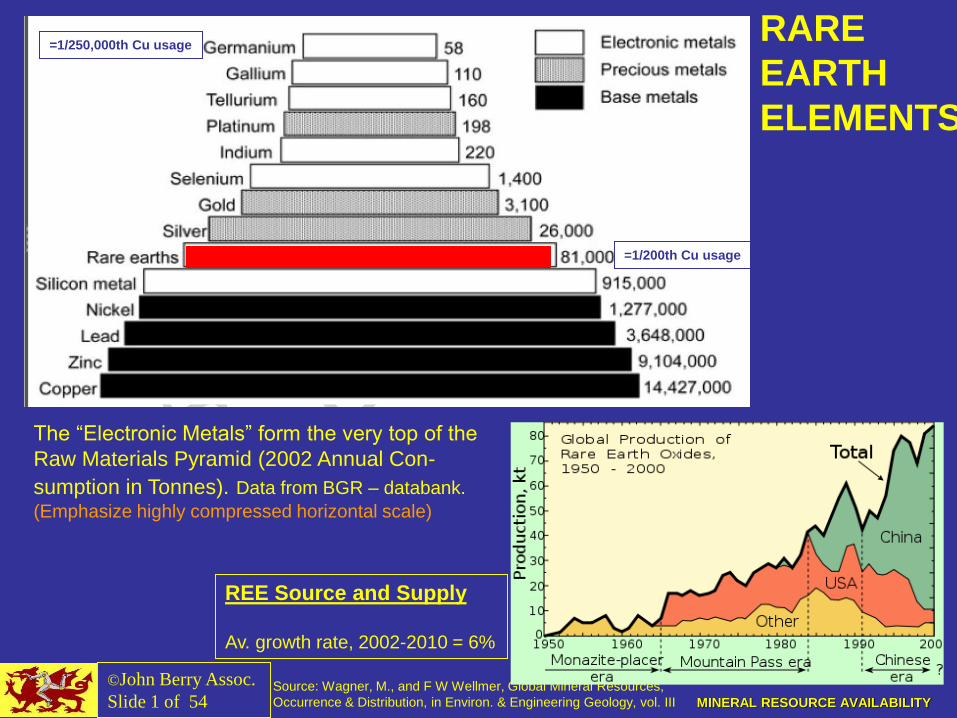

Source: Wagner, M., and F W Wellmer, Global Mineral Resources,

Occurrence & Distribution, in Environ. & Engineering Geology, vol. III

The “Electronic Metals” form the very top of the

Raw Materials Pyramid (2002 Annual Con-

sumption in Tonnes). Data from BGR – databank.

(Emphasize highly compressed horizontal scale)

2010: 130,000t

REE Source and Supply

Av. growth rate, 2002-2010 = 6%

RARE

EARTH

ELEMENTS

=1/250,000th Cu usage

=1/200th Cu usage

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 1 of 54

CHINA - 3

• High growth rates essential for Communists to retain legitimacy

• The Chinese people are seeking affluence on par with the industrial West.

• Chinese consumption patterns are driving world commodity markets.

In 2009, 35 % (37.7Mt) of world’s primary Aluminum production (#1 in world).(Halpern 2010).

• China’s supplies of minerals such as Cr, Pt and Co and Cu are inadequate (i.e. strategic for China),

Between 2002 and 2010 the price of copper rose from $0.70/lb to over $4.00/lb (Blas, 2010).

• China has high quality reserves of, and exports, tungsten, REEs, tin, antimony and zinc

47% of the 19 minerals on which the USA is 100% import dependent come from China

In 2002 mineral imports and exports accounted for nearly 20% of China’s total trade (CIMG 2003).

• China views the world financial and trade systems as creations of the West and does not trust

them to supply its needs.

• China’s “Go Out Strategy” to reduce its geopolitical vulnerability to mineral and energy import cut off: Pursuing equity ownership of fuel and mineral producing companies & deposits worldwide

Approx. $3 trillion in foreign exchange reserves to support this strategy.

In 2008 China offered $18.5 bn for UNOCAL (which owned the Mountain Pass, CA, REE mine)

$19.5 bn for a stake in the 2nd largest minerals company, Rio Tinto.

In 2009 China’s National Oil Companies established approximately $50 billion in energy agreements with

Brazil, Russia, Venezuela and Kazakhstan (Jiang 2009).

Free Access to Minerals 4:

Source: Butts K H, B Bankus & A Norris, 2011. Strategic

Minerals: Is China’s Consumption a threat to United States

Security? US Army War College, CSL Issue Paper, v. 7-11.

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 1 of 54

RARE EARTH ELEMENTS

aka “LANTHANIDES”, plus Scandium & Yttrium

GEOLOGY:

REE are found in mineable concentrations mainly in fascinating rocks called Carbonatites. • These are intrusive or, rarely, extrusive igneous rocks consisting of >50 percent carbonate (e.g. calcite)

• Carbonatites usually occur as small plugs within zoned alkalic intrusive complexes, or as breccias.

• They occur in continental rift-related tectonic settings.

• Only one carbonatite volcano is known to have erupted in historical time, Ol Doinyo Lengai volcano in

Tanzania. It erupts with the lowest temperature lava in the world, at 500-600 °C.

• Nb; Nb–rutile and Nb–ilmenite occur in some deposits.

• Monazite (Ce,La,Di)PO4, Bastnaesite (CeF)CO3, and synchysite are the most important source of REE elements.

• Much of China’s production is a by-product of iron mining in Inner Mongolia (The Economist, 9/17/2010)

WHAT THEY ARE:

Elements in Group 3

of the Atomic Table,

in the 7th Period

Lanthanum

Cerium

Prasodymium

Neodymium

Promethium

Samarium

Europium

Gadolinium

Terbium

Dysprosium

Holmium

Erbium

Thulium

Ytterbium

Lutetium

MINERALOGY

Bastnäsite: US, China

Monazite: Rest of world

Phosphorites: Florida

REE can also be found in clays and in placer deposits derived from carbonatites

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 1 of 54

DISTRIBUTION:

• Ancient Shields – therefore

Africa, Australia, Brazil,

Canada, Baltic Shield

• Very few in USA, Russia, India

Euro zone.

• Several in China, Mongolia.

US IMPORTS 2009: $ 113 M.

2010: $ 161 M

RARE EARTH ELEMENTS

Unstable Places: •Congo

•Gabon

•Angola

•Mozambique

•Mauretania

•Tanzania

•Namibia

•South Africa

Stable Places

USES (2009) - total 1,400 mt.

Chemical catalysts 22%; Cerium,

Metallurgical alloys, Jet engines 21%; Yttrium

Petroleum refining catalysts 14%; Cerium, Lanthanum

Automotive catalytic converters 13%; Cerium

Glass polishing and ceramics 9%; Cerium

REE phosphors for displays, lasers 8%; Yttrium, Europium

Permanent magnets 7%; Gd, Pr, Neodymium

Electronics 3%; Tm, Gd, Pm

Batteries: 25 lbs La, Nd, Dy, Tb per Prius

Other (Fiber Optics (Er), Radar systems) 3%.

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 1 of 54

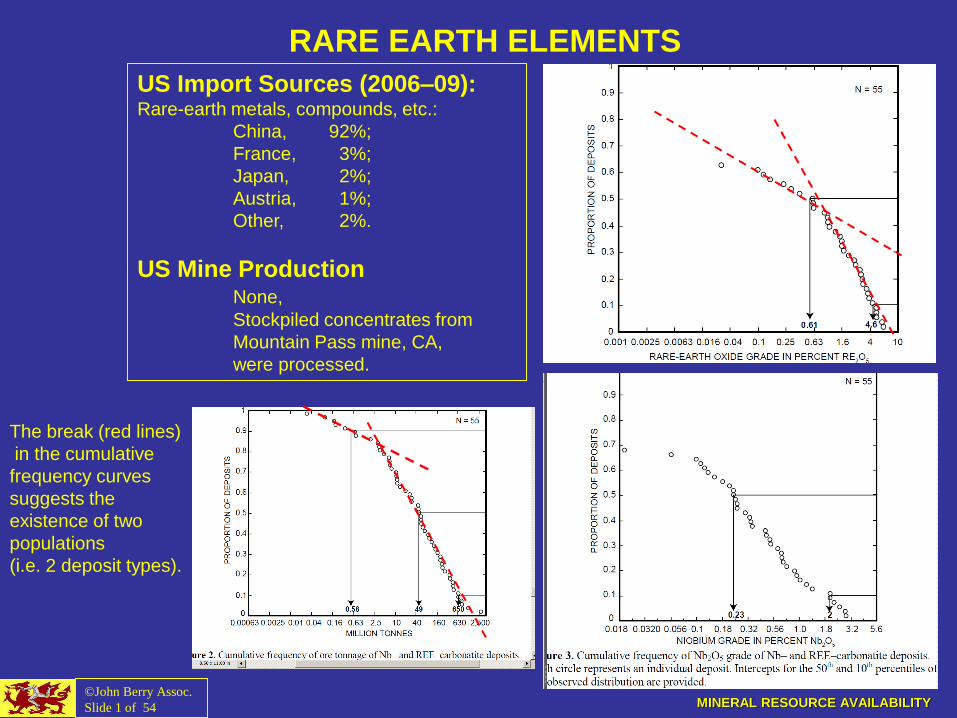

RARE EARTH ELEMENTS

US Import Sources (2006–09): Rare-earth metals, compounds, etc.:

China, 92%;

France, 3%;

Japan, 2%;

Austria, 1%;

Other, 2%.

US Mine Production None,

Stockpiled concentrates from

Mountain Pass mine, CA,

were processed.

The break (red lines)

in the cumulative

frequency curves

suggests the

existence of two

populations

(i.e. 2 deposit types).

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 1 of 54

REE EXPLORATION & DEVELOPMENT “RUSH”

Mining Companies are trying to reopen old mines and develop new supplies:

Hoidas Lake, Canada: could supply about 10% of the $1 billion market for REE in N. America.

Mountain Pass Mine: Molycorp has raised $500 million. Projected to reopen in 2011.

SE Nebraska: Quantum Rare Earth Devel., of Canada, conducting test drilling.

Alaska: Ucore Rare Metals, of Canada, has started drilling for REE.

Kvanefjeld, Greenland: large, recent discovery. Drilling at this site has confirmed significant

quantities of black lujavrite, which contains ~1% rare earth oxides (REO).

Vietnam: agreed in 2010 to supply Japan with rare earths from Lai Châu Province.

Mt. Weld, Australia: Ore to be refined at Kuantan, Malaya. Designed to supply 1/3 of world’s

demand, exclusive of China. $730 million already spent on it. The

Lanthanide concentrate from Mount Weld is “slightly radioactive”: this has

caused permitting and political problems.

(At Bukit Merah in Perak, a rare-earth mine operated by Mitsubishi,

closed in 1992 and left continuing environmental and health concerns).

Estonia (Alum Shale): Tailings from 50 years of uranium, shale and loparite mining at

Sillamäe are now ore, and yield 3000 mt, or 2% of world REE production.

Nuclear reprocessing: Nuclear fission produces a full range of elements. Due to the radioactivity

hazard, it is unlikely that refining can be done safely and economically.

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 34 of 45

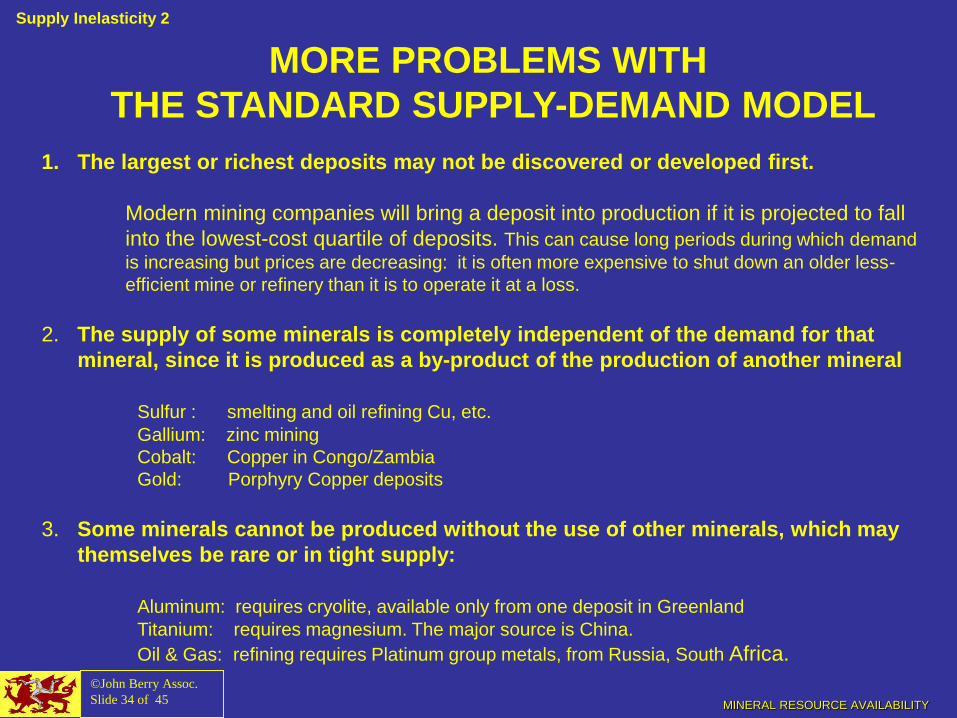

MORE PROBLEMS WITH

THE STANDARD SUPPLY-DEMAND MODEL

1. The largest or richest deposits may not be discovered or developed first.

Modern mining companies will bring a deposit into production if it is projected to fall

into the lowest-cost quartile of deposits. This can cause long periods during which demand

is increasing but prices are decreasing: it is often more expensive to shut down an older less-

efficient mine or refinery than it is to operate it at a loss.

2. The supply of some minerals is completely independent of the demand for that

mineral, since it is produced as a by-product of the production of another mineral

Sulfur : smelting and oil refining Cu, etc.

Gallium: zinc mining

Cobalt: Copper in Congo/Zambia

Gold: Porphyry Copper deposits

3. Some minerals cannot be produced without the use of other minerals, which may

themselves be rare or in tight supply:

Aluminum: requires cryolite, available only from one deposit in Greenland

Titanium: requires magnesium. The major source is China.

Oil & Gas: refining requires Platinum group metals, from Russia, South Africa.

Supply Inelasticity 2

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 1 of 54

TITANIUM

PROCESSING:

The Kroll process used to extract titanium from its various ores is laborious and costly:

it sacrifices another expensive metal, Magnesium.

Chlorine gas is passed over red-hot rutile or ilmenite in the presence of carbon to make Titanium

tetrachloride TiCl4. This is condensed and purified by fractional distillation and then reduced with

800 °C molten magnesium in an argon atmosphere.

USES:

• Titanium dioxide, white pigment used in paints, paper, toothpaste, and plastics (95%)

• Titanium Metal (5%)

Aircraft engines and frames (70%)

The SR-71 “Blackbird”.

Approx 59 tons used in Boeing 777, 45 tons in the Boeing 747

• As a strengthening agent in graphite composite fishing rods and golf clubs and bicycles.

• Also in STEEL (Ferro-titanium), Aluminium, Copper, Manganese, Molybdenum, and Vanadium alloys

• Powdered titanium is used in pyrotechnics as a source of bright-burning particles.

MINERAL RESOURCE AVAILABILITY

The “LUMPY” SUPPLY CURVE

Deposit Types, Prices and Volumes

• Almost all mineral commodities are found in a variety of different types of deposit

• Each type of deposit is characterized by its own average size and grade, etc.

• Large, low grade deposits require lots of capital,

energy, other resources, and land, but

have low labor costs and low cost in $/ton.

• Low grade deposits are much more environmentally

unfriendly than high-grade deposits (amount

of land disturbance, permanence of damage,

damage to waterways, carbon footprint).

©John Berry Assoc.

Slide 35 of 45

Grade

Output

Deposit Size

Energy

Inputs

Cost/Ton

Ore

Gra

de %

Co

st

in D

olla

rs

Supply Inelasticity 3

Nkana Mine, Zambia, 1971

Nchanga Mine, Zambia, 1971

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 1 of 54

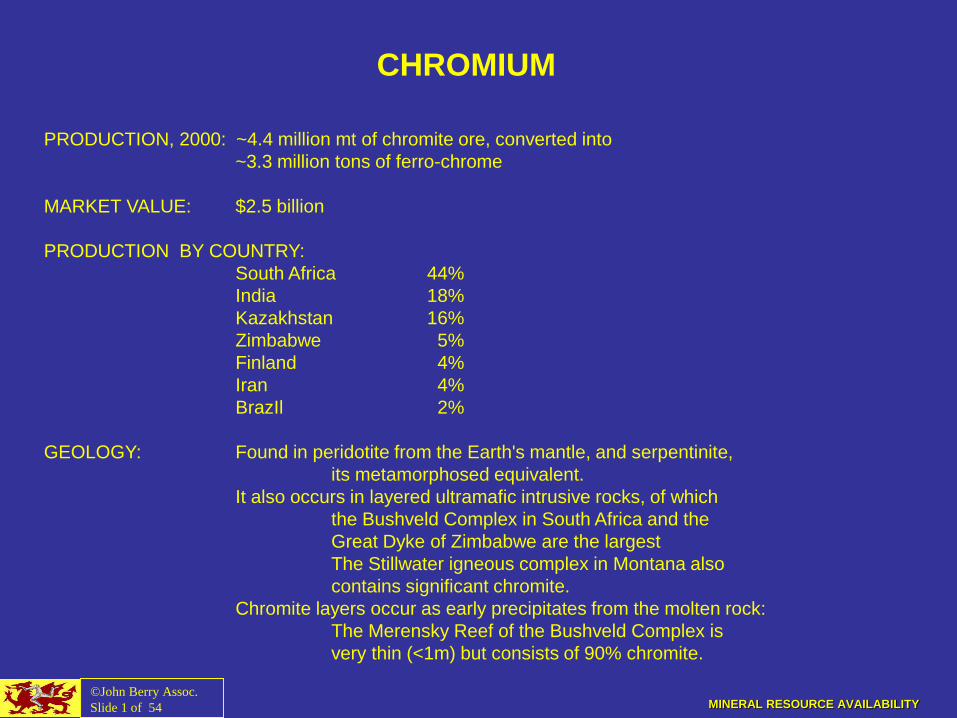

CHROMIUM

PRODUCTION, 2000: ~4.4 million mt of chromite ore, converted into

~3.3 million tons of ferro-chrome

MARKET VALUE: $2.5 billion

PRODUCTION BY COUNTRY:

South Africa 44%

India 18%

Kazakhstan 16%

Zimbabwe 5%

Finland 4%

Iran 4%

BrazIl 2%

GEOLOGY: Found in peridotite from the Earth's mantle, and serpentinite,

its metamorphosed equivalent.

It also occurs in layered ultramafic intrusive rocks, of which

the Bushveld Complex in South Africa and the

Great Dyke of Zimbabwe are the largest

The Stillwater igneous complex in Montana also

contains significant chromite.

Chromite layers occur as early precipitates from the molten rock:

The Merensky Reef of the Bushveld Complex is

very thin (<1m) but consists of 90% chromite.

MINERAL RESOURCE AVAILABILITY

©John Berry Assoc.

Slide 1 of 54

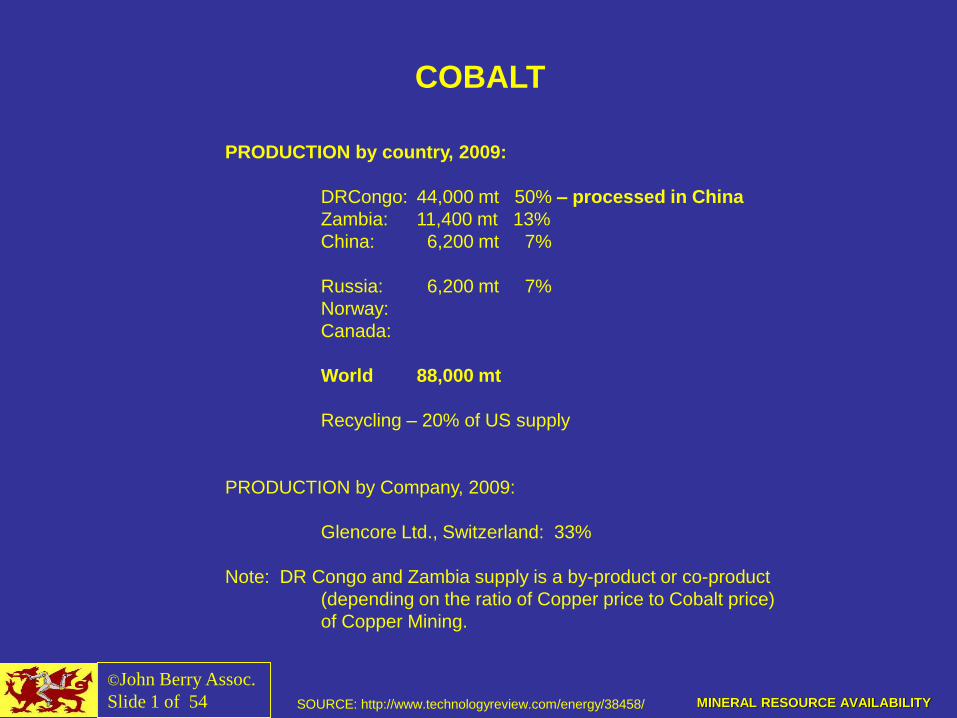

COBALT

SOURCE: http://www.technologyreview.com/energy/38458/

PRODUCTION by country, 2009:

DRCongo: 44,000 mt 50% – processed in China

Zambia: 11,400 mt 13%

China: 6,200 mt 7%

Russia: 6,200 mt 7%

Norway:

Canada:

World 88,000 mt

Recycling – 20% of US supply

PRODUCTION by Company, 2009:

Glencore Ltd., Switzerland: 33%

Note: DR Congo and Zambia supply is a by-product or co-product

(depending on the ratio of Copper price to Cobalt price)

of Copper Mining.

= Standard Model of supply and

demand breaks down temporarily

MINERAL RESOURCE AVAILABILITY

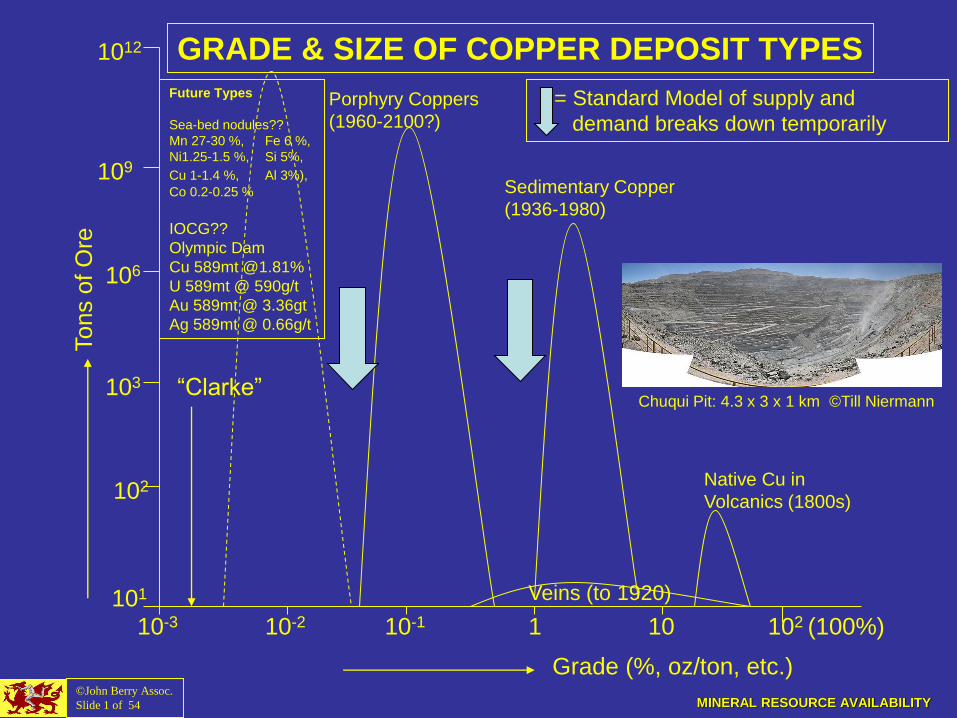

Grade (%, oz/ton, etc.)

Tons o

f O

re

“Clarke”

101

103

102

106

1012

109

10-2 10-3 102 (100%) 10 1 10-1

Native Cu in

Volcanics (1800s)

Veins (to 1920)

Porphyry Coppers

(1960-2100?)

Sedimentary Copper

(1936-1980)

GRADE & SIZE OF COPPER DEPOSIT TYPES

Future Types

Sea-bed nodules??

Mn 27-30 %, Fe 6 %,

Ni1.25-1.5 %, Si 5%,

Cu 1-1.4 %, Al 3%), Co 0.2-0.25 %

IOCG??

Olympic Dam

Cu 589mt @1.81%

U 589mt @ 590g/t

Au 589mt @ 3.36gt

Ag 589mt @ 0.66g/t

©John Berry Assoc.

Slide 1 of 54

Chuqui Pit: 4.3 x 3 x 1 km ©Till Niermann

MINERAL RESOURCE AVAILABILITY

• Deposit type becomes ex-

hausted: HUGE & possibly

PERMANENT JUMP in price

• The price may then decline

slightly over time as more de-

posits of the same type are

found and efficiencies increase.

• “Exploration Rush”: prices may

decline steeply and for a long

time.

• Supply from a few very large deposits: one deposit goes off-line - large but temporary (decade)

jump in price until new supplies are developed.

“LUMPY” SUPPLY CURVE (cont.)

Source: Singer

Metals Economics Group (December 15, 2011) ”Copper will almost certainly go into

surplus for the first time in many years but the lack of significant discoveries and the

challenges faced by today’s developers mean that a brief period (3 yrs) of over-supply

will be followed by another prolonged period of deficit.” ©John Berry Assoc.

Slide 36 of 45

GRADES AND SIZES OF COPPER DEPOSIT TYPES

Supply Inelasticity 4

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 44 of 45

MODIFIED ECONOMIC VIEW - TILTON

The Opportunity Cost Paradigm

A consensus is emerging among the members of both “fixed stock” and “infinite

resources” schools that the fixed stock paradigm should be retired in favor of an

alternative that focuses on the opportunity costs of finding and extracting mineral

resources.

• Over time the depletion of the lowest-cost deposits forces society to turn to lower-

grade, more-remote, and more difficult-to-process deposits.

• This tends to push production costs and mineral commodity prices

up, reflecting their growing scarcity.

• If prices rise sufficiently, demand will fall to zero and production will cease even

though uneconomic mineral resources remain in the ground.

• However, advances in technology continually work to make mining and extraction

cheaper, and to provide substitutes for commodities in short supply. A “race

against depletion”.

• MUST internalize external costs or true opportunity cost is not known.

MINERAL RESOURCE AVAILABILITY

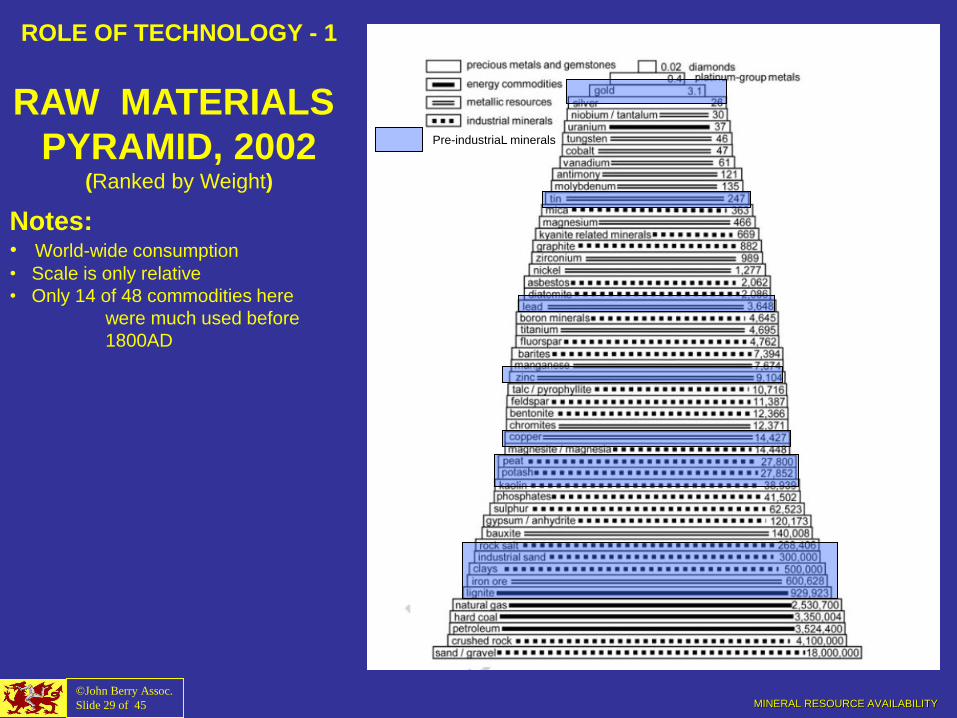

ROLE OF TECHNOLOGY - 1

RAW MATERIALS

PYRAMID, 2002 (Ranked by Weight)

Notes: • World-wide consumption

• Scale is only relative

• Only 14 of 48 commodities here

were much used before

1800AD

©John Berry Assoc.

Slide 29 of 45

Pre-industriaL minerals

MINERAL RESOURCE AVAILABILITY ©John Berry Assoc.

Slide 1 of 54