military lending act

TRANSCRIPT

Military Lending Act

© 7/2021 American Bankers Association

Military Lending Act

ABA course content is not a substitute for professional legal advice.

Military Lending Act

© 7/2021 American Bankers Association

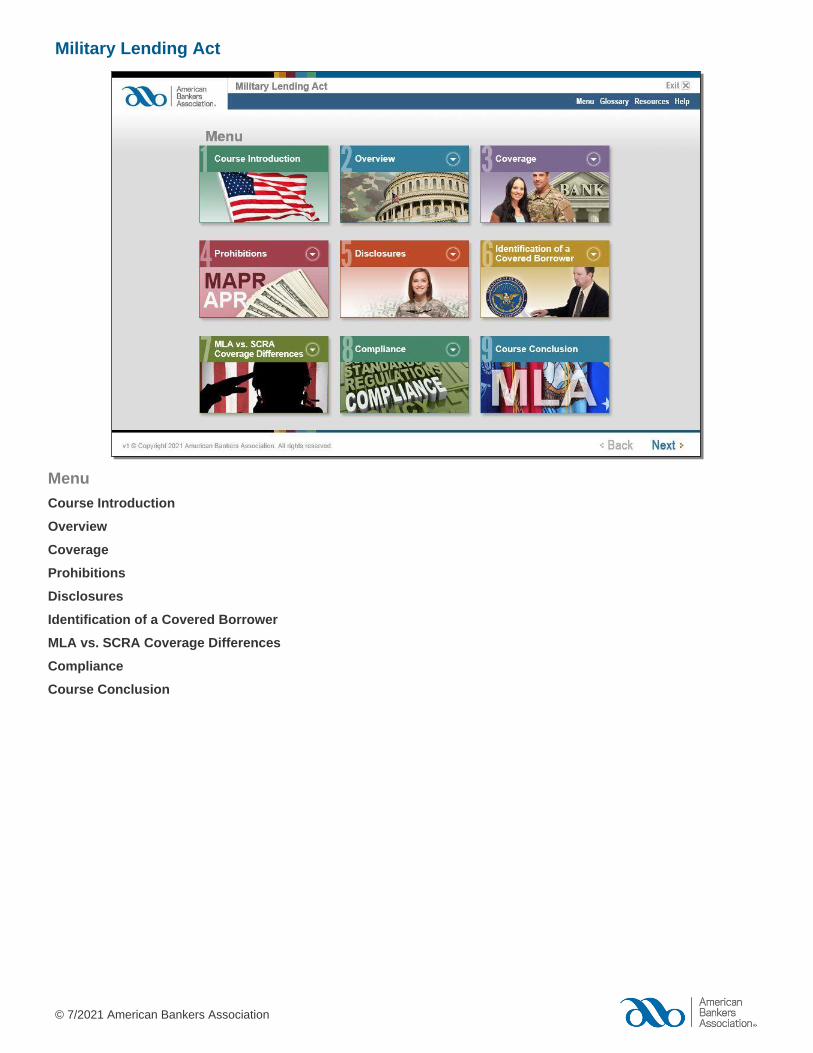

Menu

Course Introduction

Overview

Coverage

Prohibitions

Disclosures

Identification of a Covered Borrower

MLA vs. SCRA Coverage Differences

Compliance

Course Conclusion

Military Lending Act

© 7/2021 American Bankers Association

Introduction

Overview

The Department of Defense (DoD) on July 22, 2015, published amendments to its Military Lending Act (MLA) regulation, which restrict the terms on certain consumer loans made to military personnel and their spouses and dependents. The amendments expanded the regulation’s application to include all consumer credit except for residential mortgages and purchase money loans. Covered loans include personal loans, including car and boat refinances, small dollar loans, credit cards, student loans, and overdraft lines of credit.

On August 26, 2016, the DoD issued an interpretive rule (guidance) to clarify a number of aspects of the regulation. The DoD updated this interpretive rule in December 2017 and revised it again in February 2020.

Version: 1.0

Update: July 2021. No significant changes.

Objectives By the end of Military Lending Act, you will be able to

• Explain the MLA rule and regulation background and purpose

• Identify consumer credit the MLA regulation and the interpretive rule cover

• Explain prohibited terms in covered loans made to military personnel and their spouses and dependents

• Identify the disclosures covered borrowers must receive under the MLA regulation

• Identify a covered borrower

• Explain the major differences between SCRA and MLA

• Explain the penalties for non-compliance

ABA course content is not a substitute for professional legal advice.

Page 1

Military Lending Act

© 7/2021 American Bankers Association

Overview

Introduction

Congress enacted the initial Military Lending Act (MLA) in 2007.

Objectives By the end of this module, you will be able to

• Explain the MLA regulation background and purpose

• Describe the MLA amended regulation revisions

Page 2

Military Lending Act

© 7/2021 American Bankers Association

Overview

Background and Purpose

In 2007, the Department of Defense (DoD) requested, and Congress enacted, protections against predatory lending to safeguard active-duty servicemembers and their families.

At the time, the DoD was concerned about servicemembers who might be young people, away from home for the first time, earning their first paycheck. These individuals with limited money management experience could be enticed into using high-cost, repeat-use loans. The DoD was specifically concerned about servicemembers use of payday loans, auto title loans, tax refund anticipation loans, and rent-to-own plans. Predatory lenders often charged exorbitant rates, set up shop just outside military base gates, and targeted military personnel and their families.

In response, Congress adopted a law intended to address the following credit types:

• Payday loans

• Vehicle title loans

• Rent-to-own programs

• Refund anticipation loans

• Military installment loans

Page 3

Military Lending Act

© 7/2021 American Bankers Association

Overview

Background and Purpose

The Act’s express purpose was to prevent trapping military households in exorbitant short-term debt so onerous as to impose financial hardship on the family that thereby impaired military readiness.

The resulting MLA and its implementing regulation took effect October 1, 2007. This first iteration of the MLA set an “all-in” 36 percent annual rate cap for certain consumer loans made to covered servicemembers and their dependents. It imposed other restrictions, including prohibitions against mandatory arbitration, use of a check or other method of access to a bank account, and allotment of military pay.

Consistent with Congress’ and the DoD’s goal, the DoD adopted a regulation that limited application of the restrictions to the following loans:

• Payday loans under $2,000 with a term of 91 days or less

• Car title loans of short duration (181 days or less)

• Tax refund anticipation loans

Page 4

Military Lending Act

© 7/2021 American Bankers Association

Overview

Background and Purpose

Self Check Quiz

What two concerns was the MLA regulation trying to address when first implemented?

» Select the correct answers and click Submit.

A) Servicemembers might be young people with limited money management experience B) Servicemembers might be taken advantage of by predatory lenders who targeted military families C) Servicemembers might be injured or killed in the line of duty D) Servicemembers might be reassigned to another duty station

A and B are correct.

C and D are incorrect because, although they are DoD concerns, they are unrelated to the financial situations of military families.

Page 5

Military Lending Act

© 7/2021 American Bankers Association

Overview

MLA Regulation

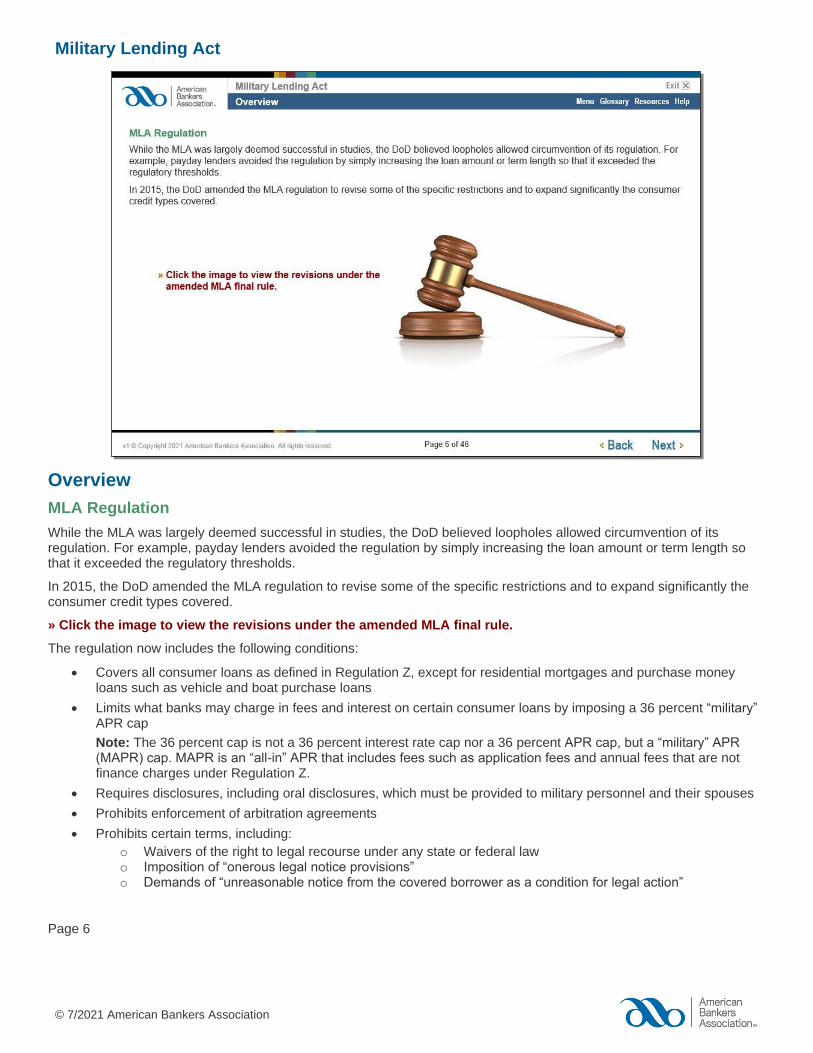

While the MLA was largely deemed successful in studies, the DoD believed loopholes allowed circumvention of its regulation. For example, payday lenders avoided the regulation by simply increasing the loan amount or term length so that it exceeded the regulatory thresholds.

In 2015, the DoD amended the MLA regulation to revise some of the specific restrictions and to expand significantly the consumer credit types covered.

» Click the image to view the revisions under the amended MLA final rule.

The regulation now includes the following conditions:

• Covers all consumer loans as defined in Regulation Z, except for residential mortgages and purchase money loans such as vehicle and boat purchase loans

• Limits what banks may charge in fees and interest on certain consumer loans by imposing a 36 percent “military” APR cap

Note: The 36 percent cap is not a 36 percent interest rate cap nor a 36 percent APR cap, but a “military” APR (MAPR) cap. MAPR is an “all-in” APR that includes fees such as application fees and annual fees that are not finance charges under Regulation Z.

• Requires disclosures, including oral disclosures, which must be provided to military personnel and their spouses

• Prohibits enforcement of arbitration agreements

• Prohibits certain terms, including:

o Waivers of the right to legal recourse under any state or federal law o Imposition of “onerous legal notice provisions” o Demands of “unreasonable notice from the covered borrower as a condition for legal action”

Page 6

Military Lending Act

© 7/2021 American Bankers Association

Overview

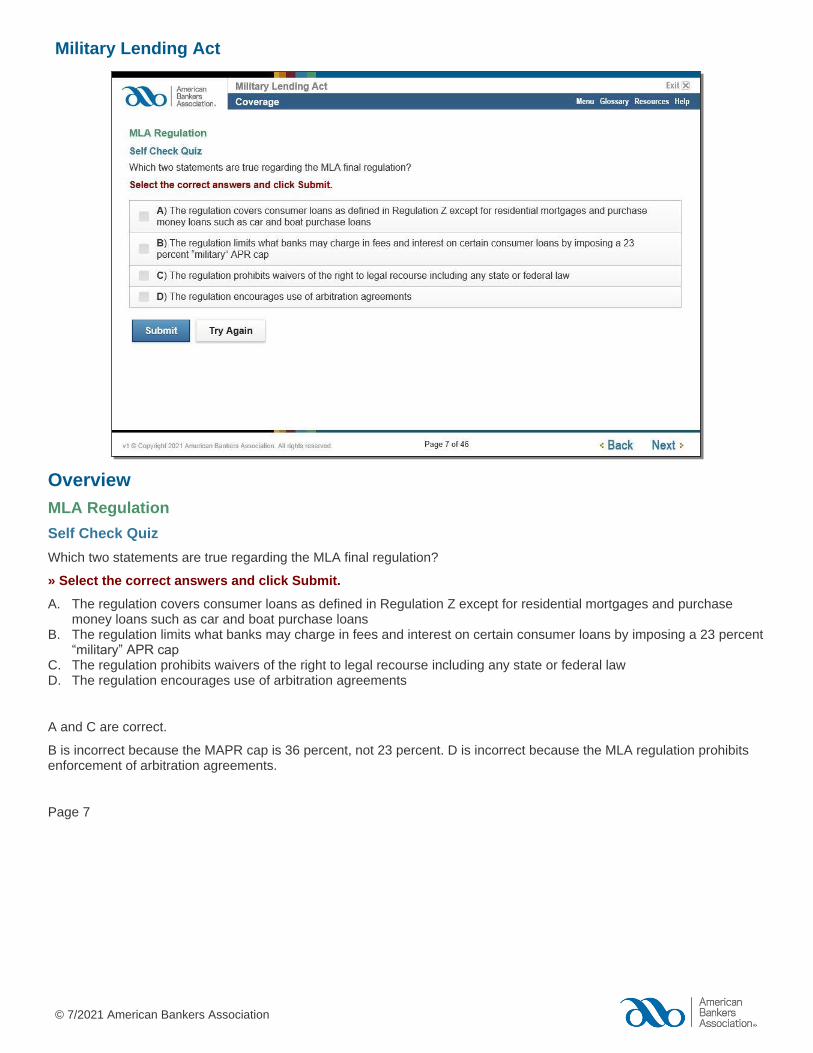

MLA Regulation

Self Check Quiz

Which two statements are true regarding the MLA final regulation?

» Select the correct answers and click Submit.

A. The regulation covers consumer loans as defined in Regulation Z except for residential mortgages and purchase money loans such as car and boat purchase loans

B. The regulation limits what banks may charge in fees and interest on certain consumer loans by imposing a 23 percent “military” APR cap

C. The regulation prohibits waivers of the right to legal recourse including any state or federal law D. The regulation encourages use of arbitration agreements

A and C are correct.

B is incorrect because the MAPR cap is 36 percent, not 23 percent. D is incorrect because the MLA regulation prohibits enforcement of arbitration agreements.

Page 7

Military Lending Act

© 7/2021 American Bankers Association

Overview

Wrap Up

In this module, you learned about the MLA background and purpose.

Page 8

Military Lending Act

© 7/2021 American Bankers Association

Coverage

Introduction

The MLA final regulation applies to “creditors” that extend “consumer credit” to “covered borrowers.” The regulation defines each term.

Objectives By the end of this module, you will be able to

• Identify consumer credit types the MLA regulation covers

• Describe who the MLA regulation covers

Glossary term:

Creditor The term “creditor” originally applied to a narrow category of creditors offering payday loans, vehicle title loans, and tax anticipation refund loans. Because banks generally did not offer those loans, they were not covered. The regulation as amended covers a wider range of consumer credit products, including those that banks offer. Therefore, the MLA regulation today covers banks, credit unions, and thrifts.

Page 9

Military Lending Act

© 7/2021 American Bankers Association

Coverage

What is Covered?

The MLA final regulation covers “consumer credit”, which is credit with the following characteristics:

• Offered or extended primarily for personal, family, or household purpose

• Subject to a finance charge or is payable by written agreement in more than four installments

• Is not exempt from Regulation Z (Truth in Lending Act)

The regulation’s consumer credit definition includes the following two important exemptions:

• Residential mortgages, and

• Non-residential mortgage loans expressly intended to finance property being used to secure the loan (purchase money loans), such as car purchase loans

» Click the image to see the types of consumer credit covered under the MLA.

The final regulation applies to the following consumer loan types:

• Overdraft lines of credit (but not overdraft protection services)

• Credit cards

• Private education loans

• Unsecured installment loans, including small dollar “accommodation” loans

• Unsecured open-end lines of credit

• Car and boat refinance loans

• Lot loans (real estate property loans on which there is no residence)

• Payday loans

• Refund anticipation loans

• Deposit advance loans

• Vehicle title loans

Note: Some loans may be exempt by Regulation Z because they exceed the regulation’s loan amount threshold ($58,300 through 2021.)

Military Lending Act

© 7/2021 American Bankers Association

Glossary term:

Residential mortgage Any credit transaction secured by an interest in a dwelling, including a transaction to finance the purchase or initial construction of the dwelling, any refinance transaction, home equity loan or line of credit, or reverse mortgage.

Page 10

Military Lending Act

© 7/2021 American Bankers Association

Coverage

What is Covered?

It is important to note that although a motor vehicle secured loan used to finance the purchase of a motor vehicle is exempt, a loan secured by a motor vehicle to refinance a car loan is not exempt. Indeed, the regulation applies to any loan secured by personal property if that loan is other than to purchase that property.

» Click the images to see examples.

Example 1 Private Ryan wants to purchase an inexpensive used car to use while temporarily stationed at Ft. Benning. The car is collateral for the loan.

This loan would not be subject to the regulation because it is to purchase a car.

Example 2 Captain Rose took out a five-year car loan when interest rates were 8 percent. A year after taking out the loan, interest rates had declined significantly. He wants to refinance the car loan to reduce his monthly payments.

This loan would be subject to the regulation because the loan is not to purchase the vehicle, but rather to refinance a loan secured by a vehicle.

Note: As noted earlier, certain types of loans that exceed the Regulation Z thresholds ($58,300 through 2021) are not covered. For example, a $100,000 loan to a servicemember to refinance a boat loan that otherwise would be covered would be not be covered due to the loan amount.

Page 11

Military Lending Act

© 7/2021 American Bankers Association

Coverage

What is Covered?

The DoD has, in its interpretive rule, a section to address “hybrid loans”—those loans that finance the purchase of personal property but also provide cash to the borrower. It is the DoD’s opinion that these loans are covered.

Page 12

Military Lending Act

© 7/2021 American Bankers Association

Coverage

What is Covered?

Scenario 1: Trade-in Scenario 2: Line of credit Scenario 3: Lot loan

The following scenarios describe a member of the military requesting bank financing. In each situation, consider if the loan is subject to the MLA rule.

» Click each tab to read a scenario and consider if the MLA applies.

Page 13

Military Lending Act

© 7/2021 American Bankers Association

Coverage

What is Covered?

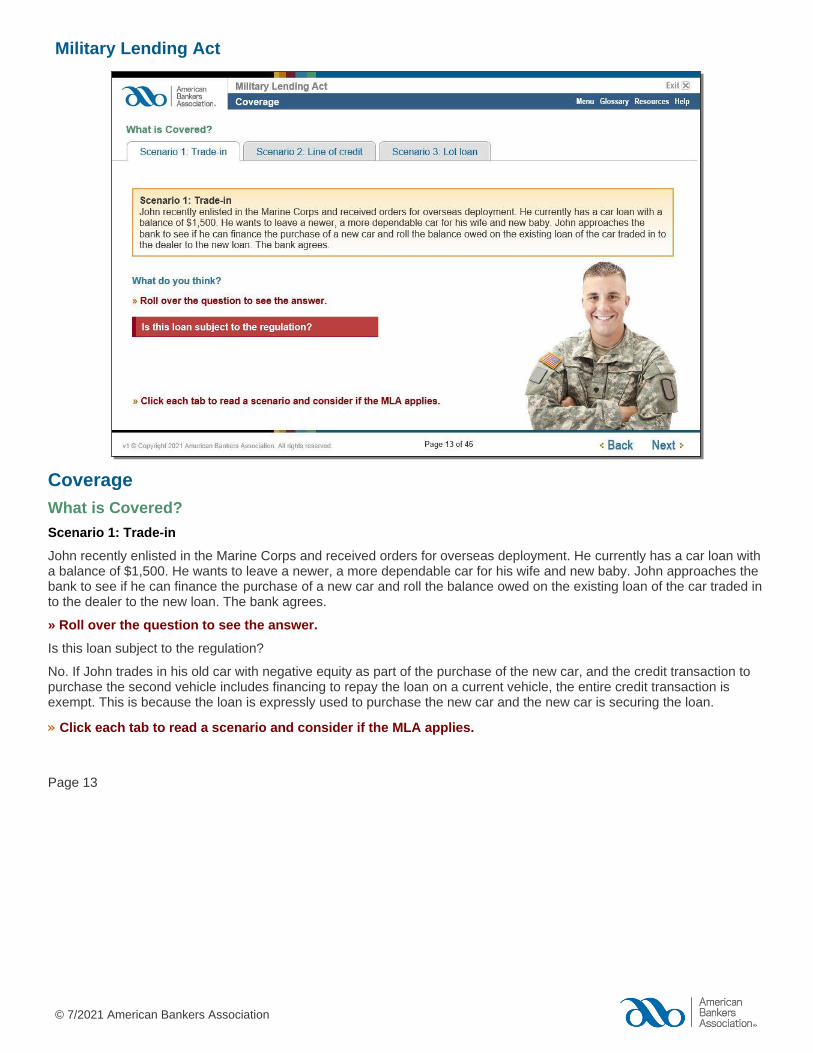

Scenario 1: Trade-in

John recently enlisted in the Marine Corps and received orders for overseas deployment. He currently has a car loan with a balance of $1,500. He wants to leave a newer, a more dependable car for his wife and new baby. John approaches the bank to see if he can finance the purchase of a new car and roll the balance owed on the existing loan of the car traded in to the dealer to the new loan. The bank agrees.

» Roll over the question to see the answer.

Is this loan subject to the regulation?

No. If John trades in his old car with negative equity as part of the purchase of the new car, and the credit transaction to purchase the second vehicle includes financing to repay the loan on a current vehicle, the entire credit transaction is exempt. This is because the loan is expressly used to purchase the new car and the new car is securing the loan.

» Click each tab to read a scenario and consider if the MLA applies.

Page 13

Military Lending Act

© 7/2021 American Bankers Association

Coverage

What is Covered?

Scenario 2: Line of credit

Shannon joined the Army and stationed at Ft. Benning, GA. She wants to apply for an overdraft line of credit just in case she encounters any unanticipated expenses when she visits her family in nearby Atlanta. Shannon applies for a $5,000 overdraft line at the bank.

» Roll over the question to see the answer.

Is this line of credit exempt from coverage under the regulation?

No. The MLA covers overdraft lines of credit, therefore, the bank needs to follow all of the MLA requirements.

» Click each tab to read a scenario and consider if the MLA applies.

Page 13

Military Lending Act

© 7/2021 American Bankers Association

Coverage

What is Covered?

Scenario 3: Lot loan

A few months ago, the Air Force deployed Rochelle to a base in Ramstein, Germany. Her husband, Gerry, who still lives stateside, informed her that his college roommate is planning to sell a piece of land with a lake view in the nearby Sierra Mountains for $100,000, and it is a great deal. Rochelle and Gerry have applied at the bank to purchase this lot.

» Roll over the question to see the answer.

If the bank grants this loan, will it be subject to the regulation?

Yes. The regulation applies to “lot loans” (real estate property loans on which there is no residence) of any amount made to a consumer.

» Click each tab to read a scenario and consider if the MLA applies.

Page 13

Military Lending Act

© 7/2021 American Bankers Association

Coverage

What is Covered?

Self Check Quiz

Which two loans does the regulation cover?

» Select the correct answers and click Submit.

A) 15-year closed-end $150,000 loan to Marine Capt. Allen to buy a new boat, secured by the boat

B) 30-year mortgage loan to Navy Capt. Henry to buy a house in Norfolk, VA, secured by his home

C) Unsecured loan for $3,000 to Air Force Capt. Kirkpatrick to purchase food and camping supplies

D) Overdraft line of credit to Army Capt. Plant for protection from inadvertent overdrafts while he is traveling

C and D are correct.

A is incorrect because money purchase loans above the $58,300 Regulation Z threshold are excluded. B is incorrect because the regulation excludes loans secured by residential mortgages.

Page 14

Military Lending Act

© 7/2021 American Bankers Association

Coverage

Who is Covered?

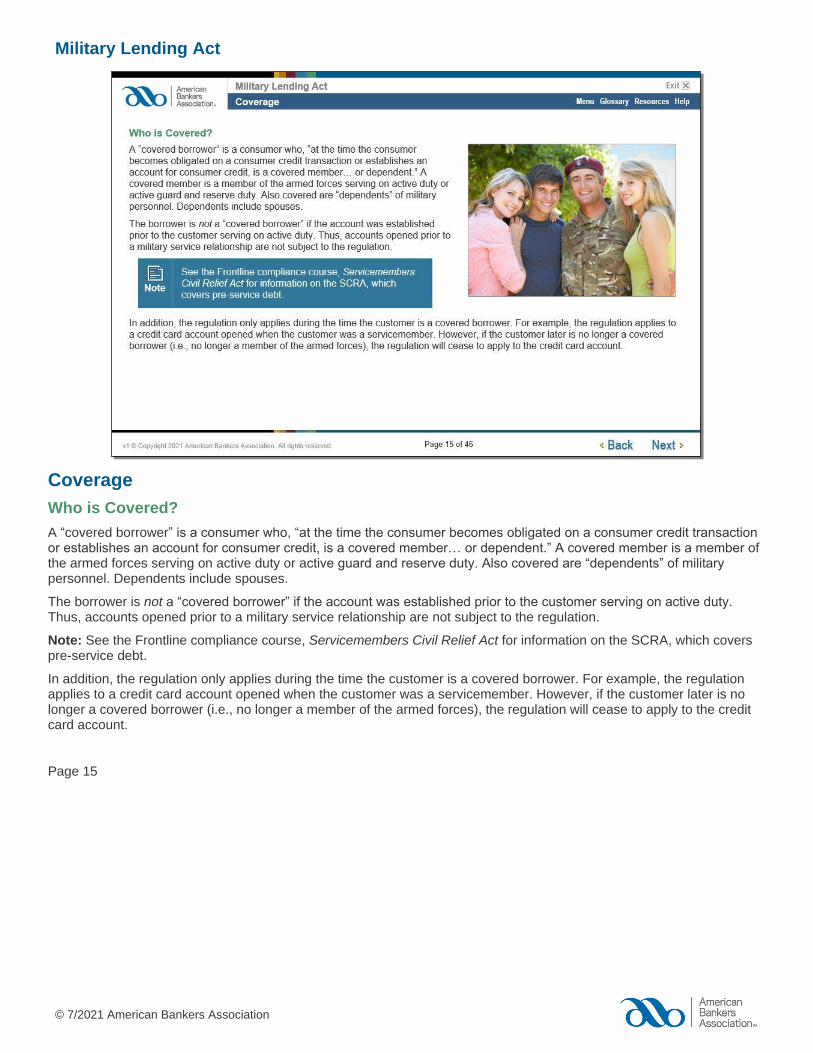

A “covered borrower” is a consumer who, “at the time the consumer becomes obligated on a consumer credit transaction or establishes an account for consumer credit, is a covered member… or dependent.” A covered member is a member of the armed forces serving on active duty or active guard and reserve duty. Also covered are “dependents” of military personnel. Dependents include spouses.

The borrower is not a “covered borrower” if the account was established prior to the customer serving on active duty. Thus, accounts opened prior to a military service relationship are not subject to the regulation.

Note: See the Frontline compliance course, Servicemembers Civil Relief Act for information on the SCRA, which covers pre-service debt.

In addition, the regulation only applies during the time the customer is a covered borrower. For example, the regulation applies to a credit card account opened when the customer was a servicemember. However, if the customer later is no longer a covered borrower (i.e., no longer a member of the armed forces), the regulation will cease to apply to the credit card account.

Page 15

Military Lending Act

© 7/2021 American Bankers Association

Coverage

Who is Covered?

True or False?

A “covered borrower” is a consumer who incurs the debt prior to induction into the military.

» Select the correct answer.

True

False

Answer: The statement is false because the regulation only applies to borrowers who qualify as a covered borrower at the time they become obligated on the loan. The loan is not subject to the regulation if opened prior to the customer serving on active duty, or the borrower is married to someone in the service. Note that the loan is also not subject to the regulation if the borrower is no longer serving in military service, even if they were when the loan was made.

Page 16

Military Lending Act

© 7/2021 American Bankers Association

Coverage

Wrap Up

In this module, you learned about the consumer credit types subject to the MLA regulation and who is a covered borrower.

Page 17

Military Lending Act

© 7/2021 American Bankers Association

Prohibitions

Introduction

The MLA regulation has significant, substantive limitations that apply to covered credit transactions.

Objectives By the end of this module, you will be able to

• Describe the differences between the MAPR and the APR

• Explain what terms are prohibited from being included in covered loans made to military personnel and their spouses and dependents

Page 18

Military Lending Act

© 7/2021 American Bankers Association

Prohibitions

Military Annual Percentage Rate (MAPR)

The most important substantive MLA rule prohibition is charging a covered borrower a “military” annual percentage rate (MAPR) that is greater than 36 percent. The MAPR is similar to the Truth in Lending Act (implemented by Regulation Z) APR definition, but with important differences. Unlike the APR, the MAPR includes fees, such as annual fees, that are not included in the APR.

The MAPR calculation includes the following fees:

• Finance charges as defined under Regulation Z

• “Participation” fees (e.g. annual fees)

• Application fees

• Fees and premiums for credit insurance, debt cancellation, and debt suspension

• Fees for a “credit-related” ancillary product sold in connection with the credit transaction

If a fee is not a “finance charge” and is not included in this list, it is not included in the MAPR calculation. For example, fees the law requires creditors to pay that the creditor passes on to the borrower are not included in the MAPR.

Page 19

Military Lending Act

© 7/2021 American Bankers Association

Prohibitions

Military Annual Percentage Rate (MAPR)

For open-end credit—such as credit cards, personal lines of credit, and overdraft lines of credit—calculate the MAPR using the “effective” or “historic” APR. This means calculate the MAPR “retroactively” based on the actual daily balance, fees, and interest.

Although you may not be the person at the bank responsible for calculating the MAPR, it is important to understand that the “effective APR” aspect of the MAPR calculation could cause even small, modest fees to exceed the 36 percent MAPR significantly.

Page 20

Military Lending Act

© 7/2021 American Bankers Association

Prohibitions

Military Annual Percentage Rate (MAPR)

Self Check Quiz

Which two options describe differences between the MAPR and the Truth in Lending Act, (implemented by Regulation Z) APR definition?

» Select the correct answers and click Submit.

A) The MAPR is the same as an APR, only it applies to loans made to military personnel

B) The MAPR includes fees not considered “finance charges” under Regulation Z, such as annual fees

C) The MAPR calculation includes fees and premiums for credit insurance, debt cancellation, and debt suspension

D) The APR uses the “effective” APR for open-end credit, which even small transaction fees can inflate

B and C are correct.

A is incorrect because the MAPR is different from the Truth in Lending Act APR definition—the MAPR calculation includes certain fees that are not included in the APR. D is incorrect because the MAPR requires an effective APR calculation, which transaction fees can inflate.

Page 21

Military Lending Act

© 7/2021 American Bankers Association

Prohibitions

Fees Excluded From the MAPR

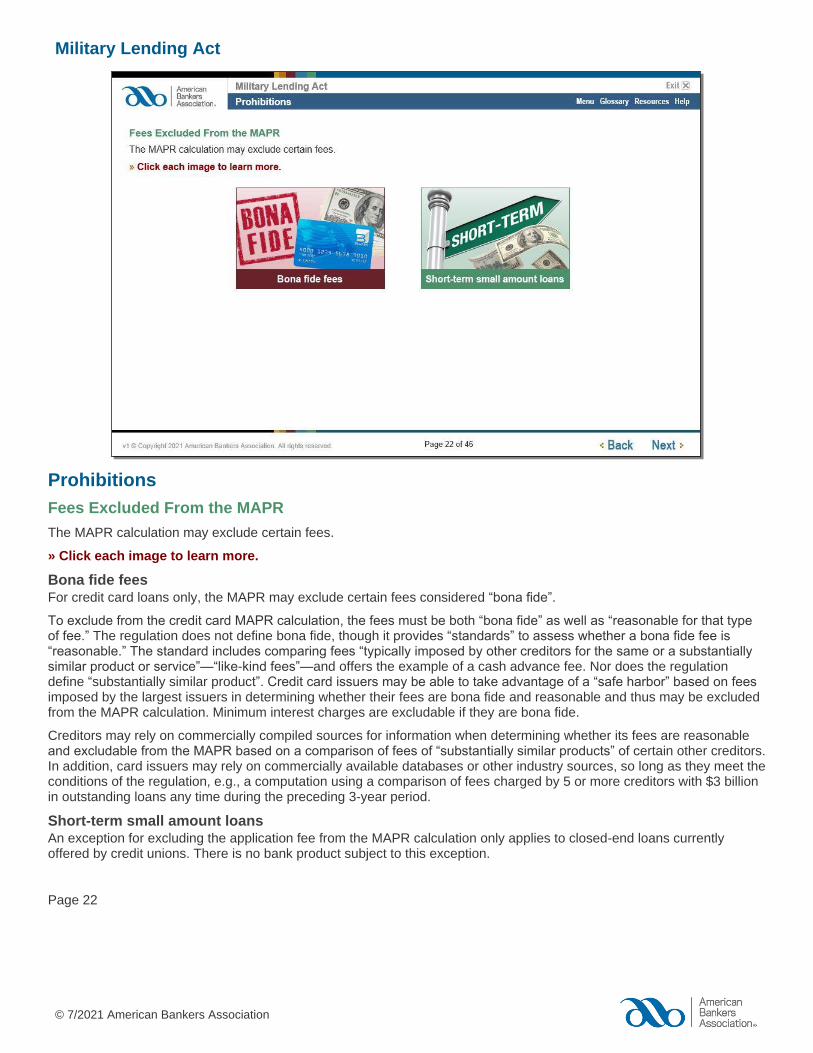

The MAPR calculation may exclude certain fees.

» Click each image to learn more.

Bona fide fees For credit card loans only, the MAPR may exclude certain fees considered “bona fide”.

To exclude from the credit card MAPR calculation, the fees must be both “bona fide” as well as “reasonable for that type of fee.” The regulation does not define bona fide, though it provides “standards” to assess whether a bona fide fee is “reasonable.” The standard includes comparing fees “typically imposed by other creditors for the same or a substantially similar product or service”—“like-kind fees”—and offers the example of a cash advance fee. Nor does the regulation define “substantially similar product”. Credit card issuers may be able to take advantage of a “safe harbor” based on fees imposed by the largest issuers in determining whether their fees are bona fide and reasonable and thus may be excluded from the MAPR calculation. Minimum interest charges are excludable if they are bona fide.

Creditors may rely on commercially compiled sources for information when determining whether its fees are reasonable and excludable from the MAPR based on a comparison of fees of “substantially similar products” of certain other creditors. In addition, card issuers may rely on commercially available databases or other industry sources, so long as they meet the conditions of the regulation, e.g., a computation using a comparison of fees charged by 5 or more creditors with $3 billion in outstanding loans any time during the preceding 3-year period.

Short-term small amount loans An exception for excluding the application fee from the MAPR calculation only applies to closed-end loans currently offered by credit unions. There is no bank product subject to this exception.

Page 22

Military Lending Act

© 7/2021 American Bankers Association

Prohibitions

Other Prohibited Credit Terms

The regulation also prohibits certain terms in covered loans made to servicemembers or their spouses or dependents, including the following prohibitions:

• Loan payment made using an allotment

• Prepayment penalties

• Requirements that borrowers submit to arbitration or “other onerous legal notice provisions in the case of dispute”

• Requirements that borrowers waive their right to legal recourse under state or federal law The regulation prohibits creditors from using checks or other methods of access to the account in connection with a covered loan. This means creditors may not create remotely created checks or use post-dated checks provided at the time credit is extended (as common in payday loans) in order to collect payments. However, it clarifies that covered borrowers may pay by check or other method, including electronic fund transfer. Creditors may make loans secured by a bank account to covered borrowers. The DoD’s interpretive rule clarifies that lenders may exercise a “right arising out of a security interest a borrower grants to a creditor to take a security interest in funds deposited within a covered borrower’s account at any time.” Provided the borrower agrees and it is otherwise permitted by law, this permits lenders to exercise a statutory right of set-off.

Glossary terms:

Allotment A designated amount of money distributed from the servicemember’s pay.

Right of set-off If a borrower defaults on a bank loan, the bank generally has the legal right to seize funds from any borrower held bank account at that bank.

Page 23

Military Lending Act

© 7/2021 American Bankers Association

Prohibitions

Other Prohibited Credit Terms

Self Check Quiz

Which three options are credit terms prohibited in covered loans made to servicemembers or their spouses or dependents?

» Select the correct answers and click Submit.

A) Statutory right of set-off

B) Prepayment penalties

C) Requirements that borrowers submit to arbitration or “other onerous legal notice provisions in the case of dispute”

D) Requirements that borrowers waive their right to legal recourse under state or federal law

B, C, and D are correct.

A is incorrect because creditors may exercise a “statutory right” to take a security interest in funds deposited into a covered borrower’s account, which means banks may apply a statutory right of set-off.

Page 24

Military Lending Act

© 7/2021 American Bankers Association

Prohibitions

Wrap Up

In this module, you learned about the prohibited terms in covered loans made to military personnel and their spouses and dependents, including the 36 percent MAPR cap. You also learned about the differences in how the MAPR and APR are calculated.

Page 25

Military Lending Act

© 7/2021 American Bankers Association

Disclosures

Introduction

Among its other provisions, the regulation requires that covered borrowers receive certain disclosures at the time the account is established. All the disclosures must be in writing. Some of them must also be made or be available orally.

Objective By the end of this module, you will be able to

• Identify the regulation required disclosures provided to covered borrowers

Page 26

Military Lending Act

© 7/2021 American Bankers Association

Disclosures

Requirements

» Click each item to learn about the disclosures required under the Military Lending Act.

1. “Statement” of the MAPR

Banks must provide orally and in writing a description of the MAPR calculation. They are not required to disclose the numerical MAPR. The regulation provides a model MAPR statement.

Banks may use the following model statement or a substantially similar statement:

Federal law provides important protections to members of the Armed Forces and their dependents relating to extensions of consumer credit. In general, the cost of consumer credit to a member of the Armed Forces and his or her dependent may not exceed an annual percentage rate of 36 percent. This rate must include, as applicable to the credit transaction or account: the costs associated with credit insurance premiums; fees for ancillary products sold in connection with the credit transaction; any application fee charged (other than certain application fees for specified credit transactions or accounts); and any participation fee charged (other than certain participation fees for a credit card account).

2. Clear description of the covered borrower’s payment obligation

Banks must provide a clear description of the payment obligation both orally and in writing, though the oral and written descriptions need not be the same. For example, the oral disclosure might be a general statement applicable to all customers, and the written statement provides specific terms as explained in the Regulation Z disclosures.

3. Regulation Z disclosures

Disclosures that are already required under Regulation Z.

Note: Creditors must provide all the disclosures in writing at the time the account is established. However, they must also orally provide the MAPR statement and the payment obligation description. Creditors may provide the oral disclosures in person or through a toll-free number. They must provide the toll-free number on (1) the application form or (2) with the written disclosures. Oral disclosures provided through a toll-free number must be available from the time the creditor provides the toll-free telephone number, which may be at application, or with the MLA disclosures. Because the oral disclosures may be generic and general, creditors need not ensure that specific payment information is available through the 800 number before the consumer becomes obligated on the loan.

Page 27

Military Lending Act

© 7/2021 American Bankers Association

Disclosures

Requirements

Self Check Quiz

The regulation requires that covered borrowers receive certain disclosures at the time the account is established. Which two disclosures are required?

» Select the correct answers and click Submit.

A) The MAPR expressed to three decimal places

B) A clear description of the borrower's payment obligation

C) Regulation Z disclosures such as the Truth in Lending disclosure showing the payment obligations

D) The HUD SCRA delinquency notice for past due mortgage loans

B and C are correct.

A is incorrect because banks are not required to disclose the numerical MAPR. D is incorrect because MLA covered loans are not the same as SCRA covered loans.

Page 28

Military Lending Act

© 7/2021 American Bankers Association

Disclosures

Wrap Up

In this module, you learned about the regulation required disclosures—a statement of the MAPR, a clear description of the payment obligation, and the Regulation Z disclosures.

Page 29

Military Lending Act

© 7/2021 American Bankers Association

Identification of a Covered Borrower

Introduction

Depending on your bank’s products and account terms, the bank may have to determine all applicants’ military status at the time it makes the loan or at some time after the account is opened.

Objectives By the end of this module, you will be able to

• Explain the regulation requirements for safe harbor

• Identify the methods used to conduct a covered borrower check to confirm military status

Page 30

Military Lending Act

© 7/2021 American Bankers Association

Identification of a Covered Borrower

Safe Harbor

Previously, MLA allowed banks to rely on applicants’ statements about their military status. However, the DoD was concerned about “servicemembers or their dependents who make false statements” in order to obtain a loan such as a payday loan.

Accordingly, lenders may not rely on an applicant’s statement about his/her military status. Lenders must inquire with the DoD or through a nationwide credit bureau to determine an applicant’s or customer’s military status in order to enjoy a safe harbor that they have properly identified the applicant’s status.

To enjoy the safe harbor, banks must determine military status at a specific point in the loan process:

• Up until the time the loan is made or 30 days prior to that time, or

• Up until the time an applicant “initiates” a transaction or 30 days prior to that time

Glossary term:

Safe harbor A safe harbor is a provision of a statute or a regulation that specifies that certain conduct will be deemed not to violate a given regulatory requirement. It is a violation of the MLA regulation to make certain loans to covered borrowers. In determining whether applicants are covered, the lender may rely on information provided from the MLA database. If the MLA database indicates the applicant is not covered when in fact the applicant is covered, it will not be a violation to provide a loan that MLA otherwise prohibits.

Page 31

Military Lending Act

© 7/2021 American Bankers Association

Identification of a Covered Borrower

Safe Harbor

Creditors enjoy the safe harbor if they determine military status any time between 30 days prior to application, and the time the account is established.

Creditors may periodically screen credit accounts—such as credit card accounts—to detect changes to a covered borrower’s status.

They may discontinue MLA protections—such as the 36 percent MAPR cap—if the borrower is no longer a covered borrower.

Page 32

Military Lending Act

© 7/2021 American Bankers Association

Identification of a Covered Borrower

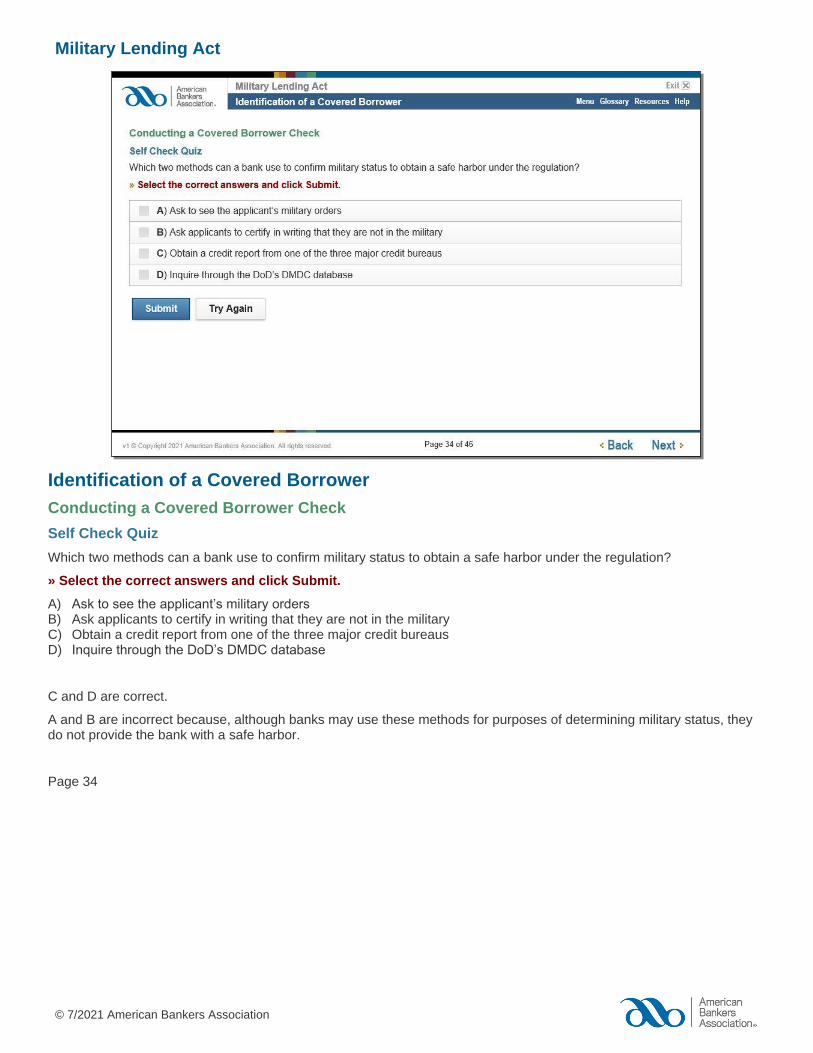

Conducting a Covered Borrower Check

To enjoy the safe harbor, banks must use one of three methods for conducting a covered borrower check.

» Click each image to learn about the methods for conducting a covered borrower check.

DoD’s MLA website Individual or batched inquiry through DoD’s MLA website. There is no charge. This website is different from the SCRA website.

DoD’s DMDC database Inquiry through a direct connection to the DoD’s Defense Manpower Data Center (DMDC) database. There is no charge. However, access is limited to a handful of companies, including the three nationwide credit bureaus.

To screen individuals through the DoD servicemember database, banks need the person’s name, date of birth, and Social Security number. In 2020, the DoD issued updated guidance that indicates that a dependent of a servicemember who does not have a Social Security number can be screened in the DoD servicemember database using an individual taxpayer identification number.

Credit bureaus Inquiry through a nationwide credit reporting bureau. The credit reporting bureaus make military status information available on credit reports and as stand-alone products.

Note: Lenders are only entitled to the safe harbor if they timely create and thereafter maintain a record of the information obtained. A record could include, for example, a screen shot from the DoD database or a copy of the credit report.

Page 33

Military Lending Act

© 7/2021 American Bankers Association

Identification of a Covered Borrower

Conducting a Covered Borrower Check

Self Check Quiz

Which two methods can a bank use to confirm military status to obtain a safe harbor under the regulation?

» Select the correct answers and click Submit.

A) Ask to see the applicant’s military orders B) Ask applicants to certify in writing that they are not in the military C) Obtain a credit report from one of the three major credit bureaus D) Inquire through the DoD’s DMDC database

C and D are correct.

A and B are incorrect because, although banks may use these methods for purposes of determining military status, they do not provide the bank with a safe harbor.

Page 34

Military Lending Act

© 7/2021 American Bankers Association

Identification of a Covered Borrower

Wrap Up

In this module, you learned about the MLA requirements to determine whether a borrower is covered in order to obtain a safe harbor. You also learned about the methods used to conduct a covered borrower check to confirm military status.

Page 35

Military Lending Act

© 7/2021 American Bankers Association

MLA vs. SCRA Coverage Differences

Introduction

You may be familiar with the Servicemembers Civil Relief Act (SCRA) and the bank has probably spent a great deal of time putting policies and procedures in place to comply with that Act. Although the SCRA and the MLA both apply to servicemembers, they are very different and cover different servicemember populations.

Note: To learn more about the SCRA, see the Frontline compliance course, Servicemembers Civil Relief Act.

Warning: Do not confuse the MLA with the SCRA—there are significant differences.

Objectives By the end of this module, you will be able to

• Explain the difference between coverage under the MLA and the Servicemembers Civil Relief Act (SCRA)

Page 36

Military Lending Act

© 7/2021 American Bankers Association

MLA vs. SCRA Coverage Differences

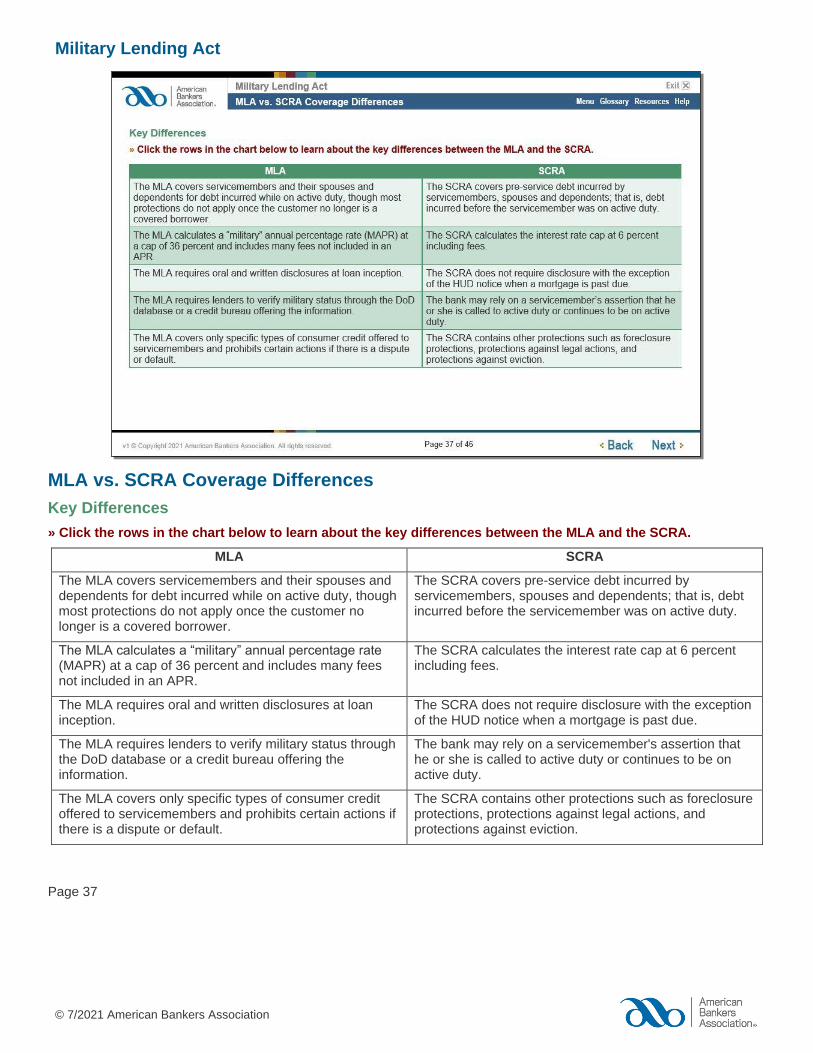

Key Differences

» Click the rows in the chart below to learn about the key differences between the MLA and the SCRA.

MLA SCRA

The MLA covers servicemembers and their spouses and dependents for debt incurred while on active duty, though most protections do not apply once the customer no longer is a covered borrower.

The SCRA covers pre-service debt incurred by servicemembers, spouses and dependents; that is, debt incurred before the servicemember was on active duty.

The MLA calculates a “military” annual percentage rate (MAPR) at a cap of 36 percent and includes many fees not included in an APR.

The SCRA calculates the interest rate cap at 6 percent including fees.

The MLA requires oral and written disclosures at loan inception.

The SCRA does not require disclosure with the exception of the HUD notice when a mortgage is past due.

The MLA requires lenders to verify military status through the DoD database or a credit bureau offering the information.

The bank may rely on a servicemember's assertion that he or she is called to active duty or continues to be on active duty.

The MLA covers only specific types of consumer credit offered to servicemembers and prohibits certain actions if there is a dispute or default.

The SCRA contains other protections such as foreclosure protections, protections against legal actions, and protections against eviction.

Page 37

Military Lending Act

© 7/2021 American Bankers Association

MLA vs. SCRA Coverage Differences

Key Differences

Self Check Quiz

Although the SCRA and the MLA both apply to servicemembers, they are very different and cover different populations. Which three options describe significant differences between the SCRA and the MLA?

» Select the correct answers and click Submit.

A) The SCRA allows the creditor to rely on the servicemember’s assertion of military status but the MLA does not

B) The SCRA covers pre-service debt while the MLA covers debt incurred during military service

C) The MLA contains other protections such as foreclosure protections, protections against legal actions, and protections against eviction but the SCRA does not

D) The MLA caps interest on new loans at 36 percent MAPR while the SCRA caps interest on pre-existing credit at 6 percent during a servicemember’s military service.

A, B, and D are correct.

C is incorrect because the SCRA, not the MLA, contains foreclosure protections, protections against legal actions, and protections against eviction.

Page 38

Military Lending Act

© 7/2021 American Bankers Association

MLA vs. SCRA Coverage Differences

Wrap Up

In this module, you learned about the coverage differences between the MLA and the SCRA.

Page 39

Military Lending Act

© 7/2021 American Bankers Association

Compliance

Introduction

Banks have several options to comply with the MLA regulation requirements. Compliance is critical, as the penalties for violations are harsher than for other consumer protection regulations.

Objectives By the end of this module, you will be able to

• Describe the options for compliance with the MLA regulation

• Explain the penalties for non-compliance with the MLA regulation

Page 40

Military Lending Act

© 7/2021 American Bankers Association

Compliance

Compliance Options

Most banks offer loans subject to the MLA regulation. The question is, “What are banks’ options?” Banks may deny loans to covered borrowers, conform all loans to the regulation, offer covered borrowers different terms or products, or eliminate products that do not comply. The bank’s choices about these options will determine whether, when, and how often it must inquire with the DoD database or obtain military status from the credit bureaus.

» Roll over each option to learn more.

Denying the loan The regulation requires banks to deny loan applications when the loans do not conform to the regulation or the bank cannot comply with other provisions such as the disclosure provisions. There is no requirement that banks conform their loan products to the regulation’s requirements.

Conforming the loan Banks may ensure that the particular loan type complies with the regulation.

Offering separate loans for military personnel The bank might have separate loans for military personnel where the terms of such loan comply with the regulation.

Eliminating products Banks may discontinue loans for all consumers, for example, if the cost of compliance or risk of violation is too great.

Page 41

Military Lending Act

© 7/2021 American Bankers Association

Compliance

Compliance Options

Question: Community National Bank is concerned that it does not have enough staff to comply with all the MLA regulation requirements. What are some actions the bank could take to limit its risk?

Answer: Community National Bank could consider checking applicants’ military status and denying noncompliant loans to covered borrowers. It could also discontinue offering the loan rather than try to comply with the regulation.

Page 42

Military Lending Act

© 7/2021 American Bankers Association

Compliance

Penalties for Non-Compliance

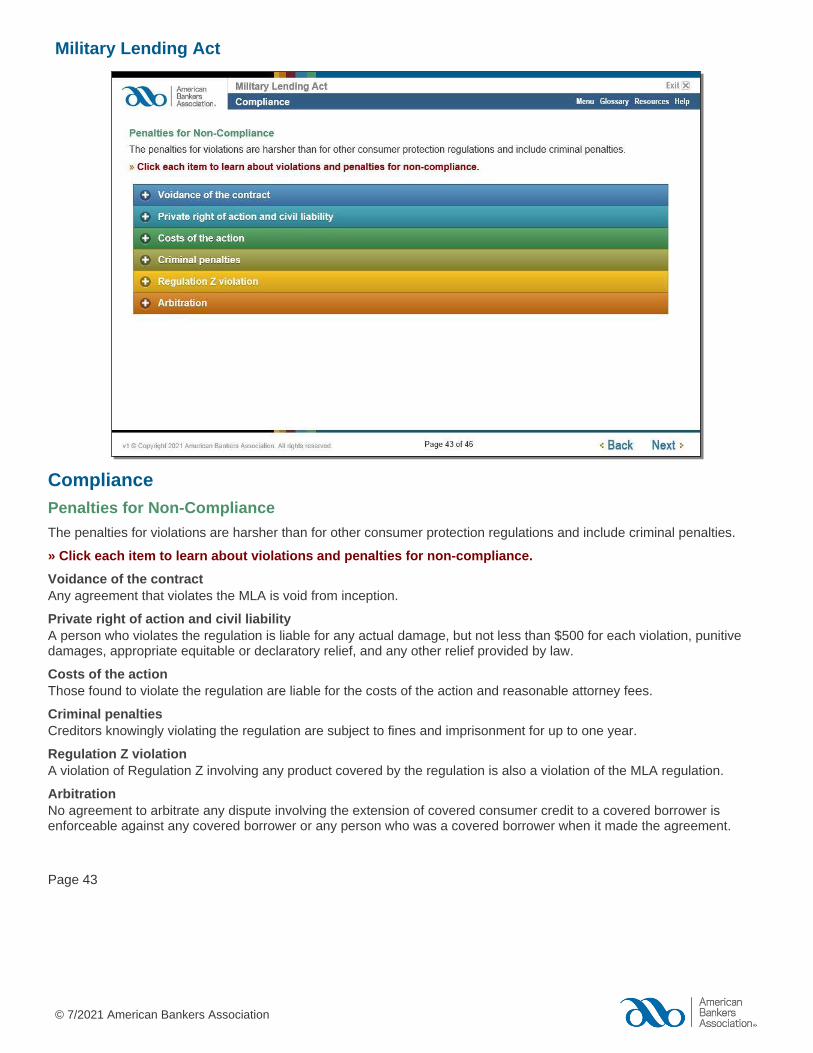

The penalties for violations are harsher than for other consumer protection regulations and include criminal penalties.

» Click each item to learn about violations and penalties for non-compliance.

Voidance of the contract

Any agreement that violates the MLA is void from inception.

Private right of action and civil liability

A person who violates the regulation is liable for any actual damage, but not less than $500 for each violation, punitive damages, appropriate equitable or declaratory relief, and any other relief provided by law.

Costs of the action

Those found to violate the regulation are liable for the costs of the action and reasonable attorney fees.

Criminal penalties

Creditors knowingly violating the regulation are subject to fines and imprisonment for up to one year.

Regulation Z violation

A violation of Regulation Z involving any product covered by the regulation is also a violation of the MLA regulation.

Arbitration

No agreement to arbitrate any dispute involving the extension of covered consumer credit to a covered borrower is enforceable against any covered borrower or any person who was a covered borrower when it made the agreement.

Page 43

Military Lending Act

© 7/2021 American Bankers Association

Compliance

Penalties for Non-Compliance

True or False?

The penalties for violations of the MLA regulation are less harsh than for other consumer protection regulations.

» Select the correct answer.

True

False

Answer: The statement is false because the penalties for violations are harsher than for other consumer protection regulations and include voidance of the loan, fines, and criminal penalties.

Page 44

Military Lending Act

© 7/2021 American Bankers Association

Compliance

Wrap Up

In this module, you learned about the options for compliance with the MLA regulation and the penalties for non-compliance.

Page 45

Military Lending Act

© 7/2021 American Bankers Association

Course Conclusion

Wrap Up

By completing Military Lending Act, you now can explain the background and purpose of the MLA regulation and can identify what terms are not permitted for certain loans made to military personnel and their spouses and dependents.

You are also familiar with the regulation required disclosures and you can explain who is covered, and what loans are covered.

You know that banks relying on information about military status from the DoD database, or from credit reporting agencies, do not violate the regulation if the information provided is incorrect and the bank makes a noncompliant loan. In addition, you can describe the penalties for non-compliance as well as some of the potential options for compliance.

Click Exit to close the course

Page 46