midstream executory contracts in bankruptcy after...

TRANSCRIPT

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Presenting a live 90-minute webinar with interactive Q&A

Midstream Executory Contracts

in Bankruptcy After Sabine Navigating Court Treatment of Transportation, Gathering and

Processing Agreements; Negotiating Midstream Agreements

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, JUNE 1, 2016

Denis A. (Archie) Fallon, Partner, King & Spalding, Houston

Vince Slusher, Partner, DLA Piper, Dallas

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-755-4350 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Executory Contracts in Bankruptcy

Section 365(a) of the Bankruptcy Code allows a bankrupt

debtor, “subject to the court’s approval,” to “assume or reject

any executory contract”

This section allows a bankrupt debtor to evaluate its executory

contracts and seek to assume those that are most beneficial to

its business and to reject those agreements that are

burdensome

The test for approval of assumption or rejection of an

executory contract is whether the debtor’s decision to do so is

a “reasonable exercise” of its “business judgment”

6

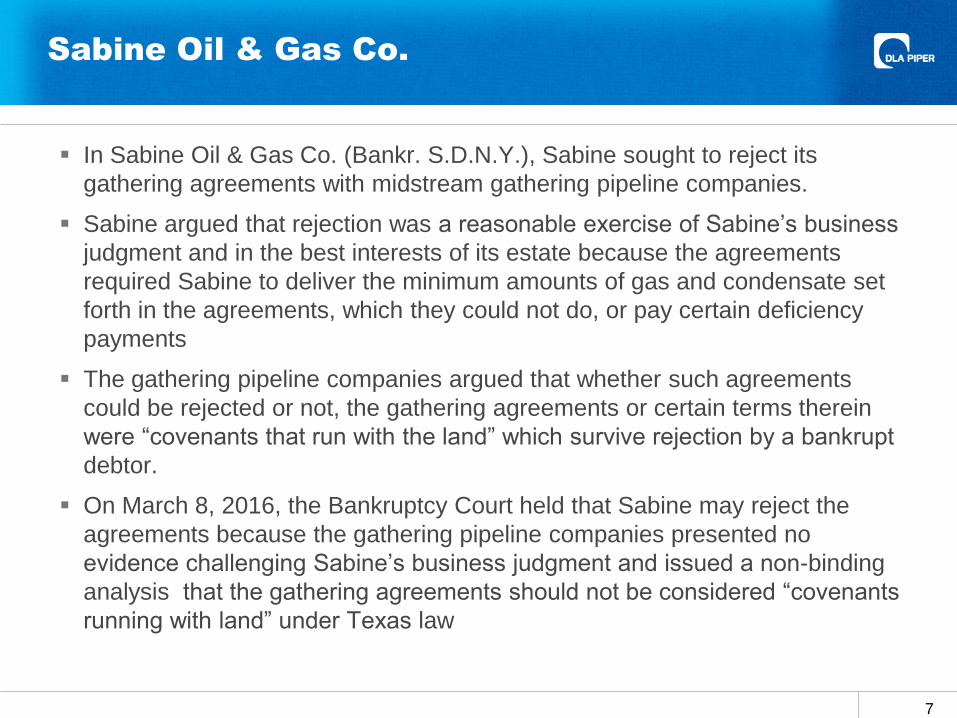

Sabine Oil & Gas Co.

In Sabine Oil & Gas Co. (Bankr. S.D.N.Y.), Sabine sought to reject its

gathering agreements with midstream gathering pipeline companies.

Sabine argued that rejection was a reasonable exercise of Sabine’s business

judgment and in the best interests of its estate because the agreements

required Sabine to deliver the minimum amounts of gas and condensate set

forth in the agreements, which they could not do, or pay certain deficiency

payments

The gathering pipeline companies argued that whether such agreements

could be rejected or not, the gathering agreements or certain terms therein

were “covenants that run with the land” which survive rejection by a bankrupt

debtor.

On March 8, 2016, the Bankruptcy Court held that Sabine may reject the

agreements because the gathering pipeline companies presented no

evidence challenging Sabine’s business judgment and issued a non-binding

analysis that the gathering agreements should not be considered “covenants

running with land” under Texas law

7

Sabine Oil & Gas Co. (cont.)

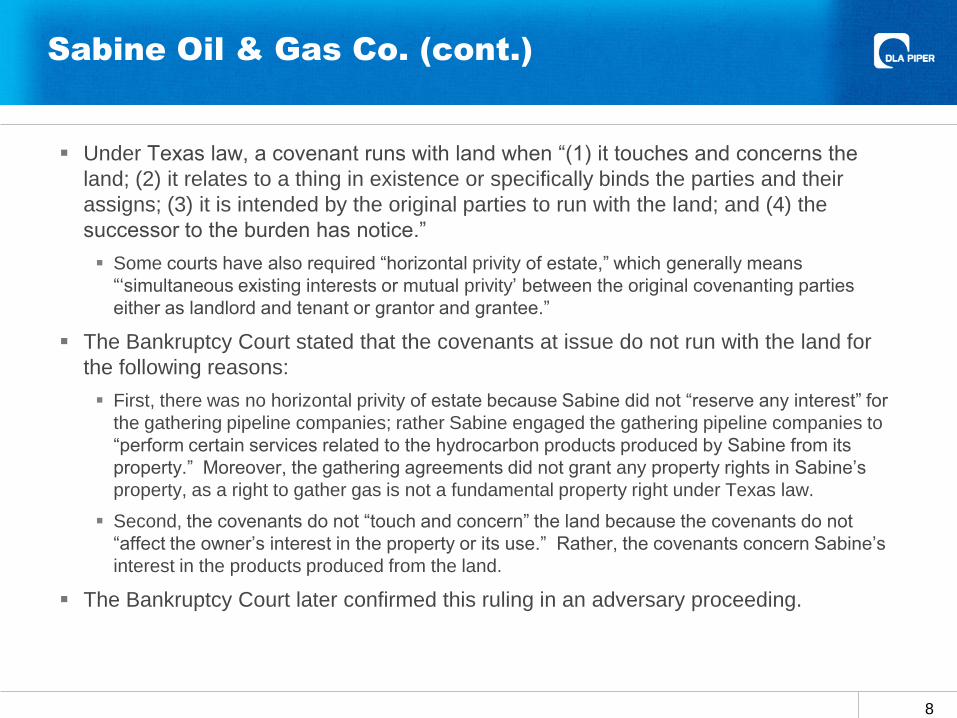

Under Texas law, a covenant runs with land when “(1) it touches and concerns the

land; (2) it relates to a thing in existence or specifically binds the parties and their

assigns; (3) it is intended by the original parties to run with the land; and (4) the

successor to the burden has notice.”

Some courts have also required “horizontal privity of estate,” which generally means

“‘simultaneous existing interests or mutual privity’ between the original covenanting parties

either as landlord and tenant or grantor and grantee.”

The Bankruptcy Court stated that the covenants at issue do not run with the land for

the following reasons:

First, there was no horizontal privity of estate because Sabine did not “reserve any interest” for

the gathering pipeline companies; rather Sabine engaged the gathering pipeline companies to

“perform certain services related to the hydrocarbon products produced by Sabine from its

property.” Moreover, the gathering agreements did not grant any property rights in Sabine’s

property, as a right to gather gas is not a fundamental property right under Texas law.

Second, the covenants do not “touch and concern” the land because the covenants do not

“affect the owner’s interest in the property or its use.” Rather, the covenants concern Sabine’s

interest in the products produced from the land.

The Bankruptcy Court later confirmed this ruling in an adversary proceeding.

8

Quicksilver Resources ;

Magnum Hunter

Quicksilver Resources (Bankr. D. Del.)

Buyer conditioned the acquisition of debtor Quicksilver’s assets on rejection of midstream

gathering agreements

Rejection of midstream gathering agreements, if successful, would have resulted in

substantial unsecured claim of midstream companies against the estate

The acquirer agreed to enter into a new contract with the debtor’s midstream pipeline

operator, averting the need for the Bankruptcy Court to rule on the motion to reject

Magnum Hunter Resources (Bankr. D. Del.)

On March 10, 2016, the debtors in the Magnum Hunter Resources reached an agreement

to terminate gas transportation and credit support agreements between one of the debtors

and its midstream pipeline partner

Pursuant to the agreement, the gas transportation and credit support agreements will

be rejected and the midstream gathering company will be allowed a $15 million claim

in the debtor’s chapter 11 case on account of the unfulfilled credit support agreement

to provide letters of credit totaling $65 million

On April 13, 2016, Magnum Hunter indicated that it reached an agreement to reject

agreements with another midstream pipeline partner. The terms of the resolution were not

disclosed. On April 14, the Bankruptcy Court authorized the rejection.

9

Impact of the Sabine Decision

Impact on Midstream Companies: adversely impacts midstream gathering

pipeline companies that have contracted with exploration companies facing

insolvency

The value of pipeline and gathering facilities construction would be jeopardized if

the agreements governing their use were rejected by the upstream exploration

companies in bankruptcy

Impact on E&P Companies: provides leverage to financially troubled

upstream exploration companies as they attempt to renegotiate agreements

with gathering pipeline companies, giving them the leverage of a bankruptcy

threat if their demands are not met

Note: The applicability of the Sabine decision is somewhat limited where

non-Texas state law governs the relevant contract and related property

rights.

10

The Impact of In re Sabine Oil & Gas Corp. and the Rejection of Agreements of

Midstream Companies in Bankruptcy

Presentation by Archie Fallon [email protected]

June 1, 2016

King & Spalding LLP 1100 Louisiana, Suite 4000

Houston, Texas 77002

In re Sabine Oil & Gas Corporation, et al. Case No. 15-11835 (Bankr. S.D.N.Y.) – Pertinent Facts

• Sabine entered into Gathering Agreements with Nordheim Eagle Ford Gathering,

LLC (“Nordheim”) in 2014

― Gathering Agreements state they are “covenant[s] running with the [land]” and

are enforceable by Nordheim against Sabine, its affiliates, and their successors

and assigns

― Privity Issue – Gathering Agreements with Sabine, but mineral rights located

in a specified geographical area in DeWitt County, Texas and owned by

Sabine South Texas LLC, who was not a party to the Gathering Agreements

Sabine did not convey any portion of its real property interests to

Nordheim through the Gathering Agreements

• The property subject to the Gathering Agreements was subject to preexisting liens

held by Sabine’s secured lenders

• Nordheim’s gathering fee was not secured

12

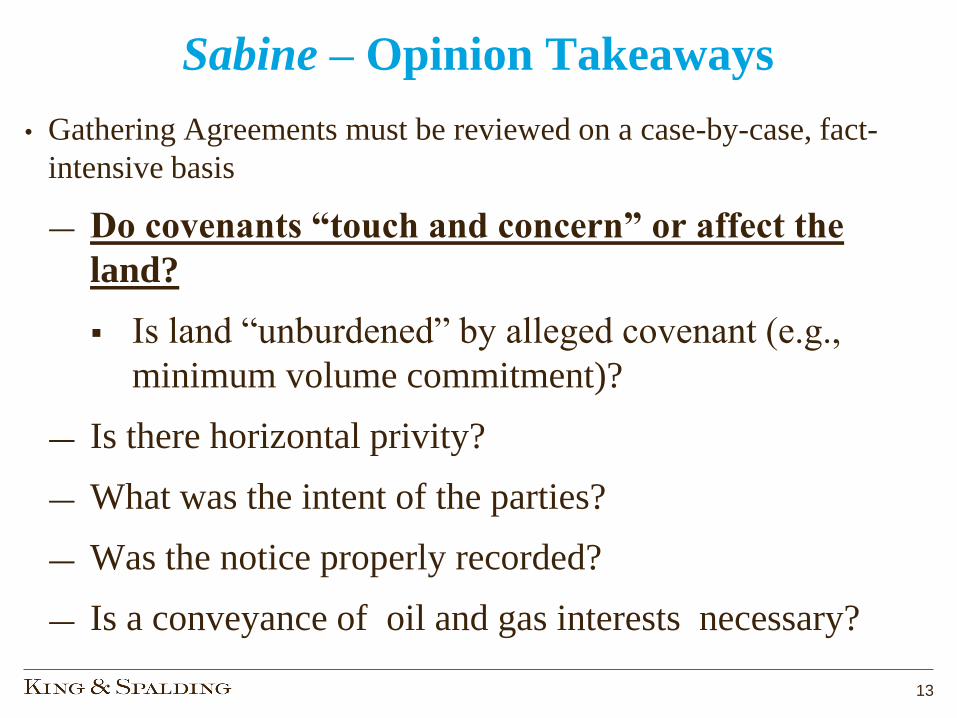

Sabine – Opinion Takeaways

• Gathering Agreements must be reviewed on a case-by-case, fact-

intensive basis

― Do covenants “touch and concern” or affect the

land?

Is land “unburdened” by alleged covenant (e.g.,

minimum volume commitment)?

― Is there horizontal privity?

― What was the intent of the parties?

― Was the notice properly recorded?

― Is a conveyance of oil and gas interests necessary?

13

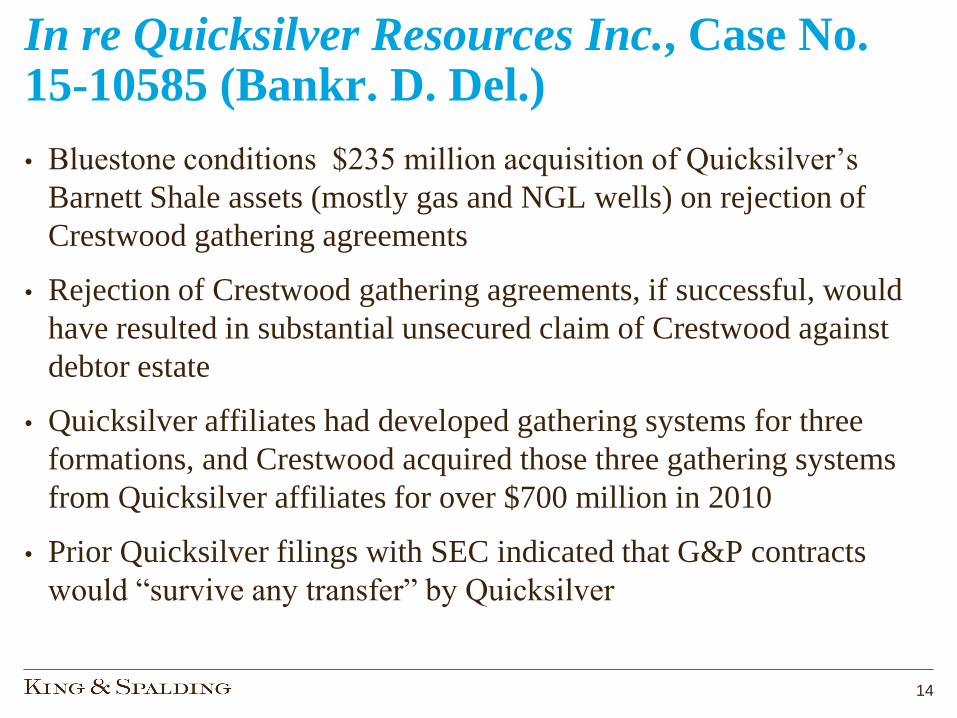

In re Quicksilver Resources Inc., Case No. 15-10585 (Bankr. D. Del.)

• Bluestone conditions $235 million acquisition of Quicksilver’s

Barnett Shale assets (mostly gas and NGL wells) on rejection of

Crestwood gathering agreements

• Rejection of Crestwood gathering agreements, if successful, would

have resulted in substantial unsecured claim of Crestwood against

debtor estate

• Quicksilver affiliates had developed gathering systems for three

formations, and Crestwood acquired those three gathering systems

from Quicksilver affiliates for over $700 million in 2010

• Prior Quicksilver filings with SEC indicated that G&P contracts

would “survive any transfer” by Quicksilver

14

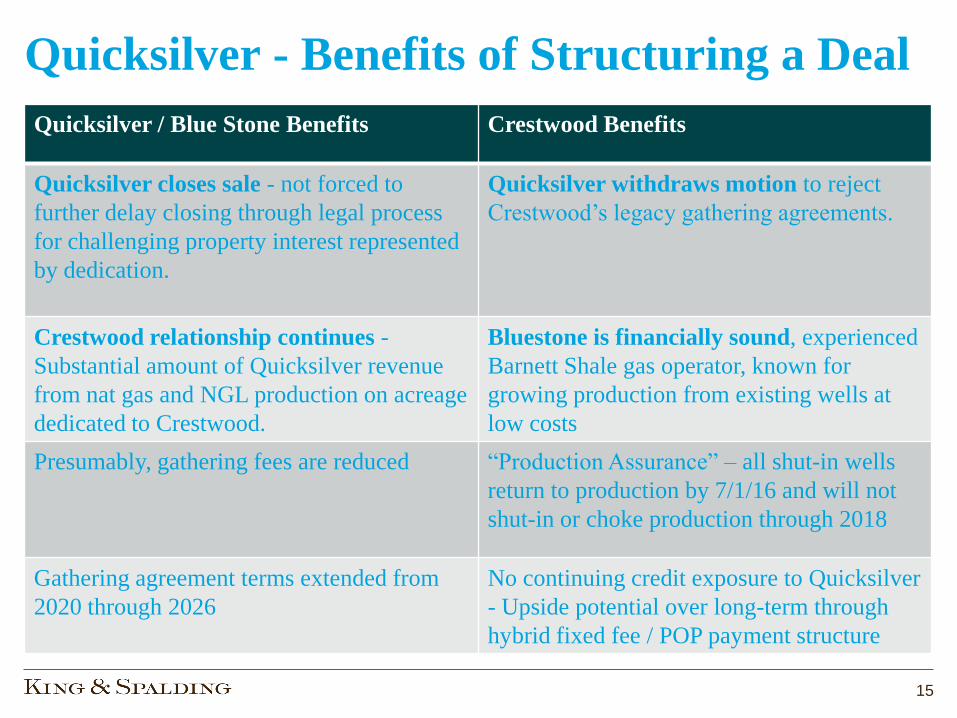

Quicksilver - Benefits of Structuring a Deal

Quicksilver / Blue Stone Benefits Crestwood Benefits

Quicksilver closes sale - not forced to

further delay closing through legal process

for challenging property interest represented

by dedication.

Quicksilver withdraws motion to reject

Crestwood’s legacy gathering agreements.

Crestwood relationship continues -

Substantial amount of Quicksilver revenue

from nat gas and NGL production on acreage

dedicated to Crestwood.

Bluestone is financially sound, experienced

Barnett Shale gas operator, known for

growing production from existing wells at

low costs

Presumably, gathering fees are reduced “Production Assurance” – all shut-in wells

return to production by 7/1/16 and will not

shut-in or choke production through 2018

Gathering agreement terms extended from

2020 through 2026

No continuing credit exposure to Quicksilver

- Upside potential over long-term through

hybrid fixed fee / POP payment structure

15

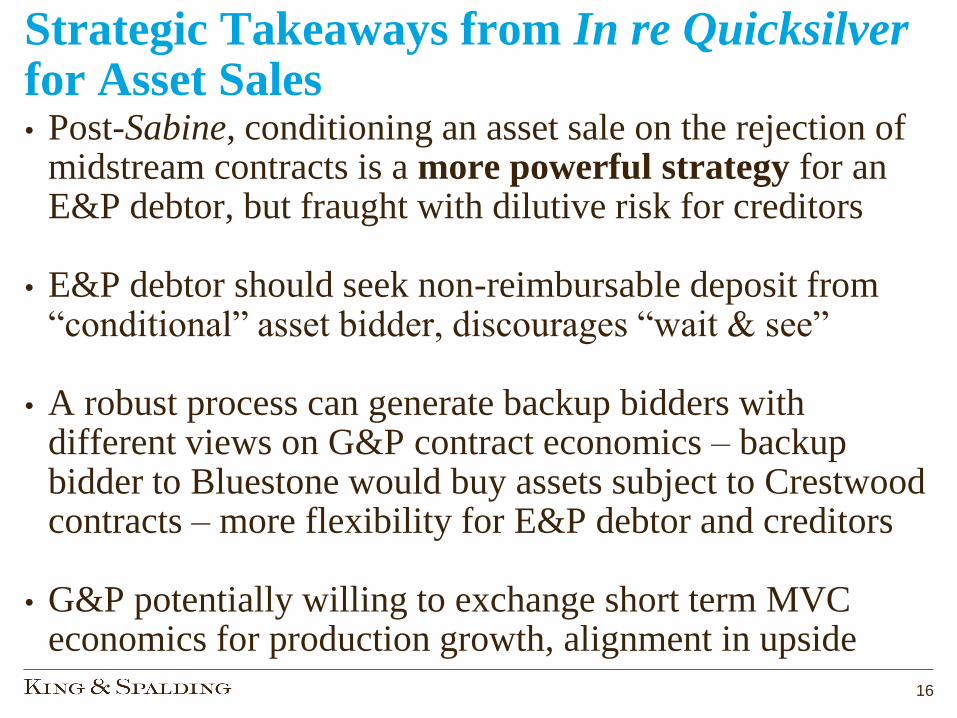

Strategic Takeaways from In re Quicksilver for Asset Sales • Post-Sabine, conditioning an asset sale on the rejection of

midstream contracts is a more powerful strategy for an E&P debtor, but fraught with dilutive risk for creditors

• E&P debtor should seek non-reimbursable deposit from

“conditional” asset bidder, discourages “wait & see” • A robust process can generate backup bidders with

different views on G&P contract economics – backup bidder to Bluestone would buy assets subject to Crestwood contracts – more flexibility for E&P debtor and creditors

• G&P potentially willing to exchange short term MVC

economics for production growth, alignment in upside

16

In re Energytec, Inc., 739 F.3d 215 (5th Cir. 2013)

• Factually distinguishable from Sabine

• Pipeline system owner assigned its property rights to one party but reserved “by covenant” for another party (an affiliate) the right to receive a fee for product transported through the pipeline and a right to consent to any assignment of that property

• Original seller sought to ensure the transfer of its property interests did not eliminate an interest in the property of a third party

17

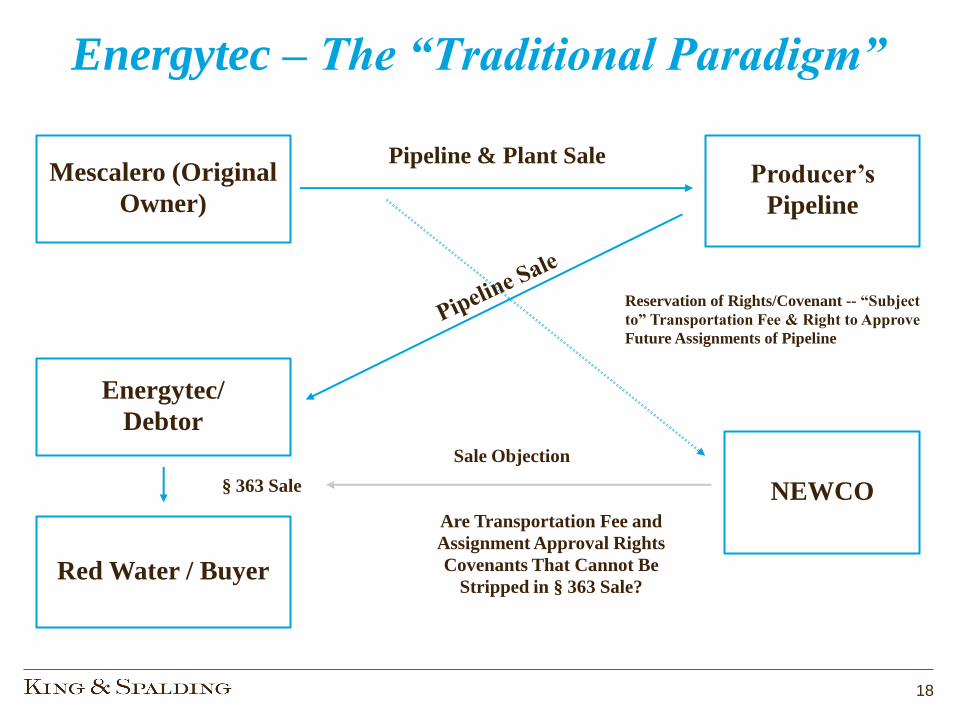

Energytec – The “Traditional Paradigm”

Mescalero (Original

Owner)

Reservation of Rights/Covenant -- “Subject

to” Transportation Fee & Right to Approve

Future Assignments of Pipeline

Producer’s

Pipeline

Energytec/

Debtor

NEWCO

Pipeline & Plant Sale

Red Water / Buyer

§ 363 Sale

Are Transportation Fee and

Assignment Approval Rights

Covenants That Cannot Be

Stripped in § 363 Sale?

Sale Objection

18

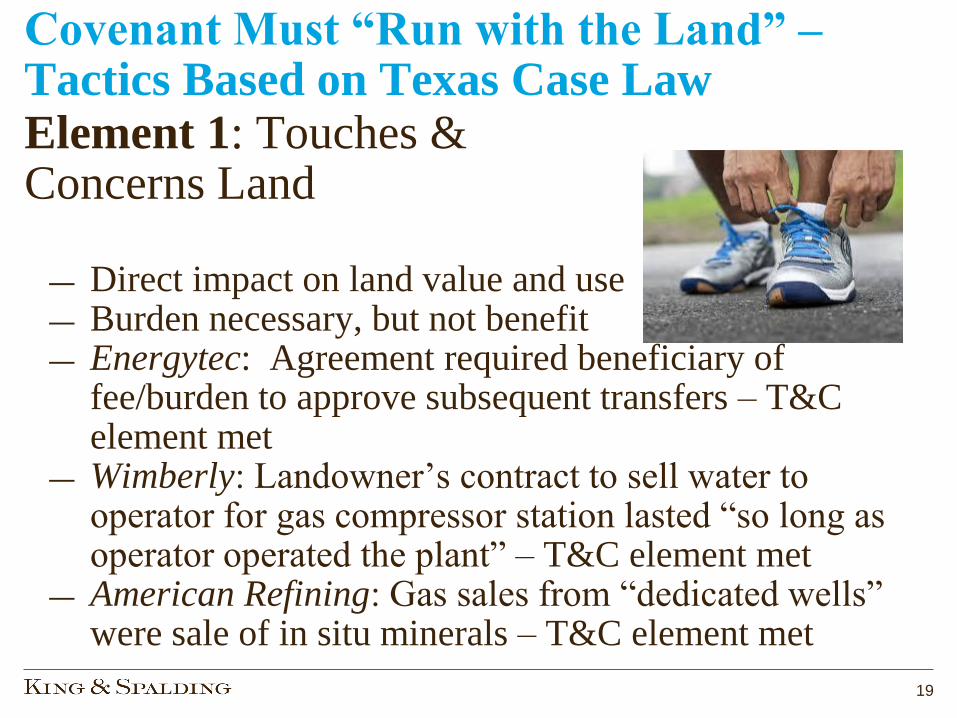

Covenant Must “Run with the Land” – Tactics Based on Texas Case Law Element 1: Touches & Concerns Land

― Direct impact on land value and use ― Burden necessary, but not benefit ― Energytec: Agreement required beneficiary of

fee/burden to approve subsequent transfers – T&C element met

― Wimberly: Landowner’s contract to sell water to operator for gas compressor station lasted “so long as operator operated the plant” – T&C element met

― American Refining: Gas sales from “dedicated wells” were sale of in situ minerals – T&C element met

19

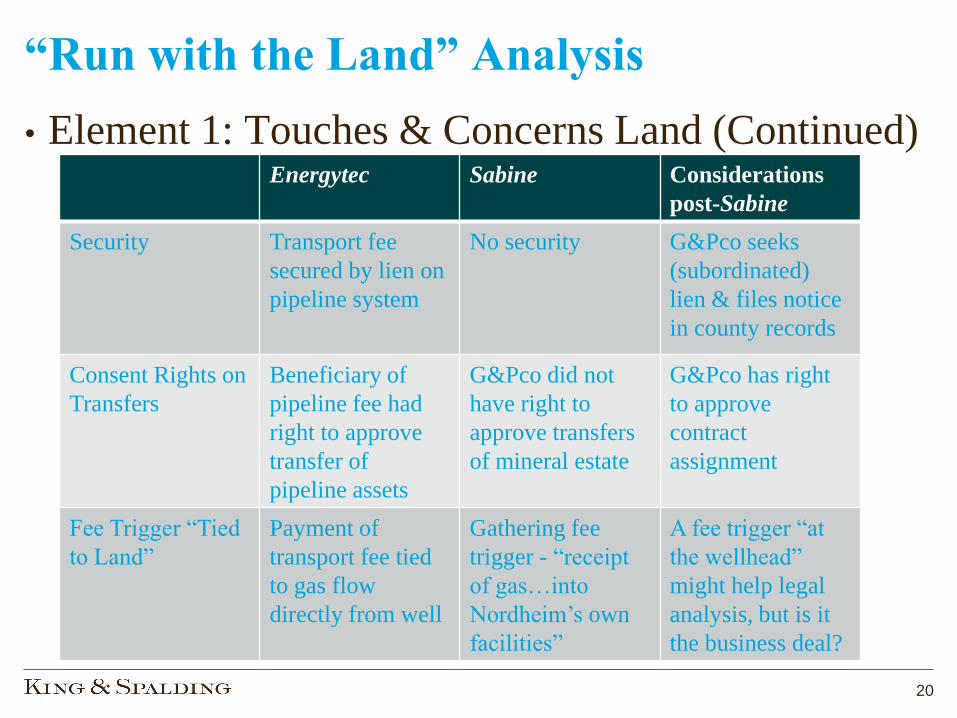

“Run with the Land” Analysis

• Element 1: Touches & Concerns Land (Continued)

Energytec Sabine Considerations

post-Sabine

Security Transport fee

secured by lien on

pipeline system

No security G&Pco seeks

(subordinated)

lien & files notice

in county records

Consent Rights on

Transfers

Beneficiary of

pipeline fee had

right to approve

transfer of

pipeline assets

G&Pco did not

have right to

approve transfers

of mineral estate

G&Pco has right

to approve

contract

assignment

Fee Trigger “Tied

to Land”

Payment of

transport fee tied

to gas flow

directly from well

Gathering fee

trigger - “receipt

of gas…into

Nordheim’s own

facilities”

A fee trigger “at

the wellhead”

might help legal

analysis, but is it

the business deal?

20

“Run with the Land” Analysis

Element 2: Relation to Thing in

Existence (in esse) or Specifically

Binds Parties & Assigns

- Beckham: Promise to construct

flume for irrigation, which was

constructed, but not maintained

- But see Gulf: Fence that was to built,

but was never built

- Include schedule with particular

description of relevant facilities

21

“Run with the Land” Analysis

Element 3: Original Intent to Run

with the Land

- Energytec: Include statement parties intend

for covenant to “run with the land”

- Include contract language that contract is

binding upon parties’ “successors and

assigns”

- Evidence of intent is bolstered by filing the

agreement in county deed records

22

“Run with the Land” Analysis

Element 4: Successor to Burden

Has Notice

- Constructive Notice – filing in

County records

- Actual Notice - acknowledgement

letter agreement between successor

and G&P company, potentially

addressing indemnity and release

issues

23

THE “FIFTH” ELEMENT

Vertical / Horizontal Privity of

Estate - The “Traditional Paradigm” –

conveyance of real estate (surface,

mineral, water rights), subject to

reservation of interest

- On the other hand, a personal covenant,

such as a promise to provide utility

service or environmental indemnity, does

not involve a transfer of real estate, does

not survive bankruptcy challenge 24

“Further Assurances”

- Many gathering agreements entitle G&P companies to request producers provide further assurances related to creditworthiness and dedication of assets.

- Further assurances of creditworthiness –

information rights, parent guaranty, notices from lenders, approval of successors.

- Producer grant of security (liens, mortgages) in

mineral estate or other assets to G&P not historically market, but may be possible in some limited circumstances (see Energytec).

25

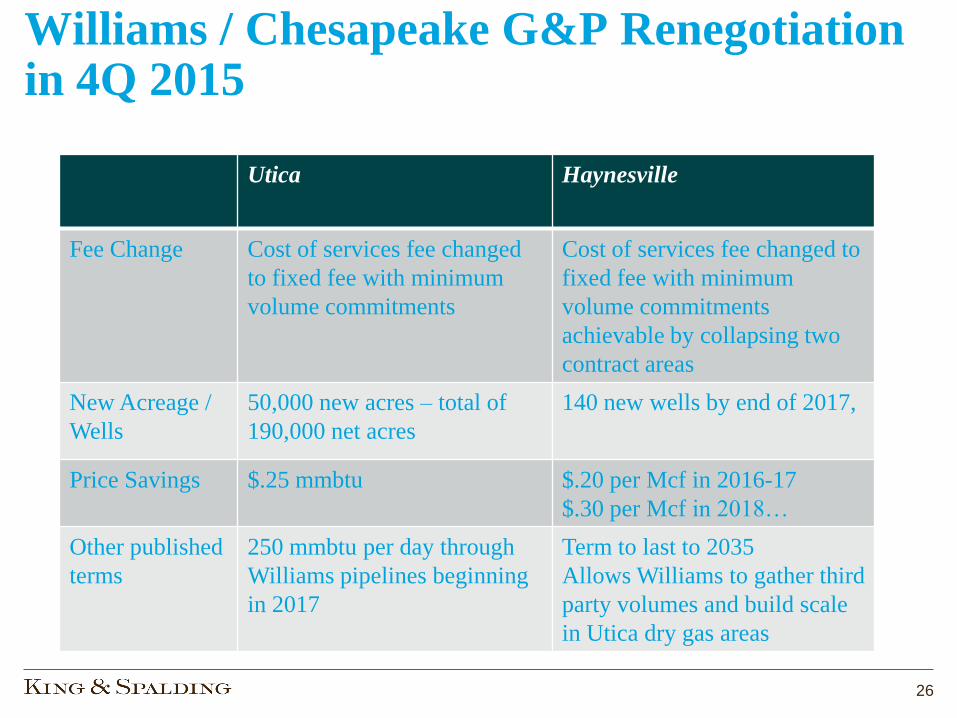

Williams / Chesapeake G&P Renegotiation in 4Q 2015 Utica Haynesville

Fee Change Cost of services fee changed

to fixed fee with minimum

volume commitments

Cost of services fee changed to

fixed fee with minimum

volume commitments

achievable by collapsing two

contract areas

New Acreage /

Wells

50,000 new acres – total of

190,000 net acres

140 new wells by end of 2017,

Price Savings $.25 mmbtu $.20 per Mcf in 2016-17

$.30 per Mcf in 2018…

Other published

terms

250 mmbtu per day through

Williams pipelines beginning

in 2017

Term to last to 2035

Allows Williams to gather third

party volumes and build scale

in Utica dry gas areas

26

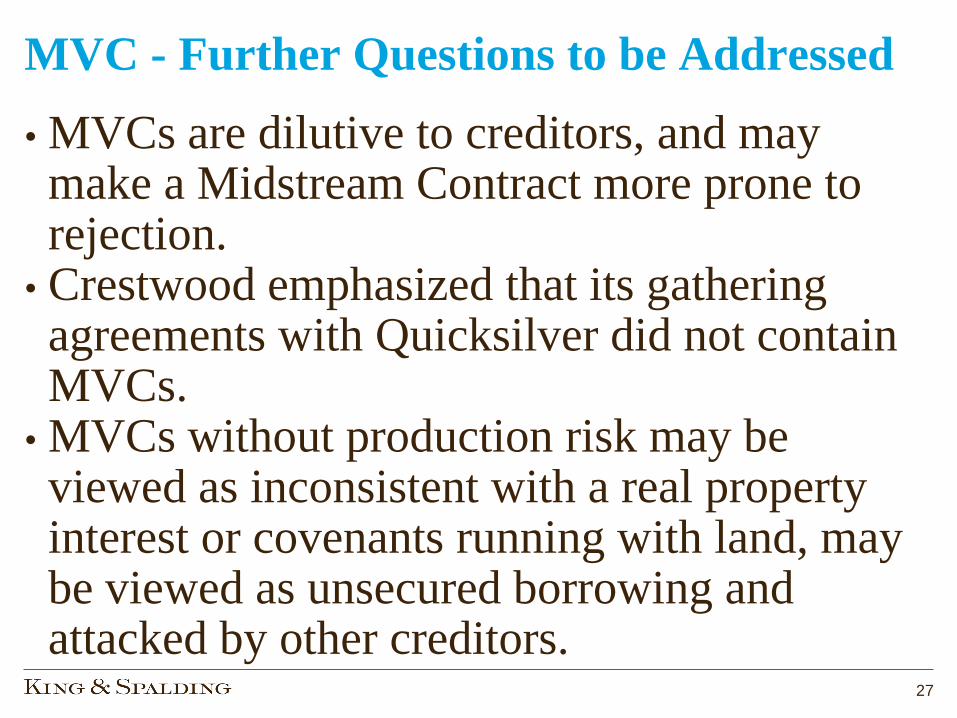

MVC - Further Questions to be Addressed

• MVCs are dilutive to creditors, and may make a Midstream Contract more prone to rejection.

• Crestwood emphasized that its gathering agreements with Quicksilver did not contain MVCs.

• MVCs without production risk may be viewed as inconsistent with a real property interest or covenants running with land, may be viewed as unsecured borrowing and attacked by other creditors.

27

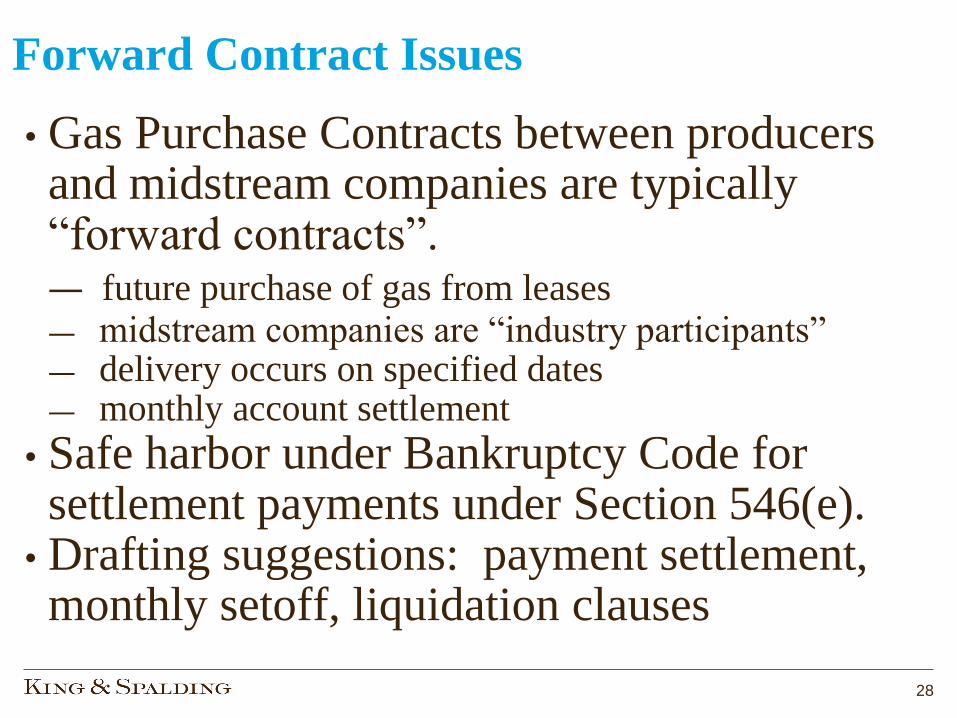

Forward Contract Issues

• Gas Purchase Contracts between producers and midstream companies are typically “forward contracts”. ― future purchase of gas from leases ― midstream companies are “industry participants” ― delivery occurs on specified dates ― monthly account settlement

• Safe harbor under Bankruptcy Code for settlement payments under Section 546(e).

• Drafting suggestions: payment settlement, monthly setoff, liquidation clauses

28

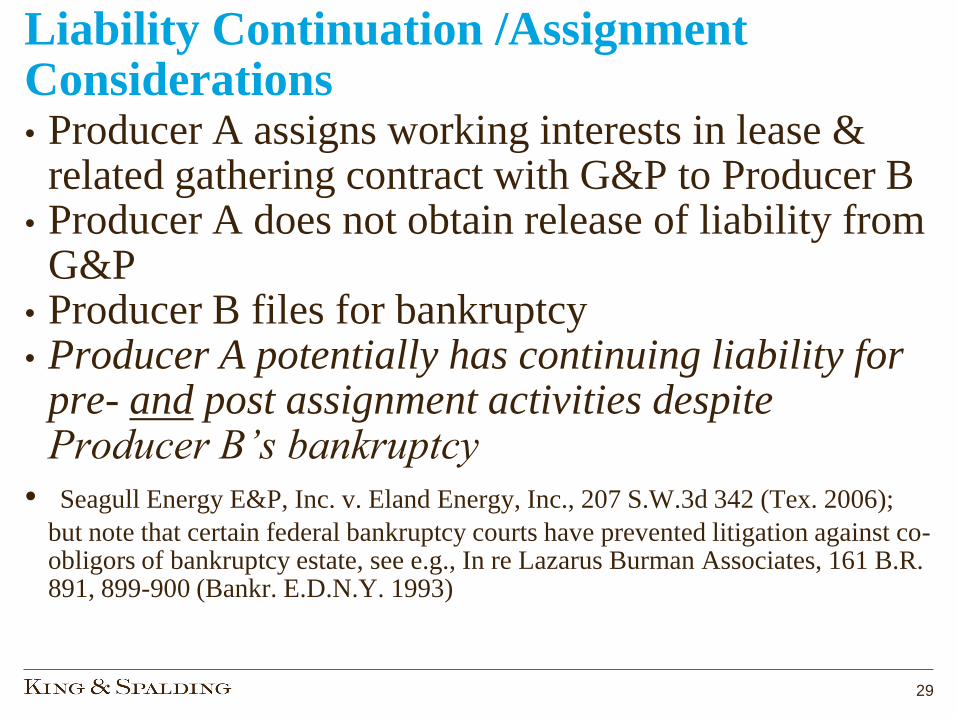

Liability Continuation /Assignment Considerations • Producer A assigns working interests in lease &

related gathering contract with G&P to Producer B • Producer A does not obtain release of liability from

G&P • Producer B files for bankruptcy • Producer A potentially has continuing liability for

pre- and post assignment activities despite Producer B’s bankruptcy

• Seagull Energy E&P, Inc. v. Eland Energy, Inc., 207 S.W.3d 342 (Tex. 2006);

but note that certain federal bankruptcy courts have prevented litigation against co-obligors of bankruptcy estate, see e.g., In re Lazarus Burman Associates, 161 B.R. 891, 899-900 (Bankr. E.D.N.Y. 1993)

29