microfinance

DESCRIPTION

ÂTRANSCRIPT

IPCRI

פלסטין למחקר ולמידע/מרכז ישראל مرآز إسرائيل فلسطين لألبحاث و المعلومات

Israel/Palestine Center for Research and Information

MICROFINANCE IN PALESTINE IN 2005

OVERVIEW OF IMPACT AND POTENTIAL

RECOMMENDATIONS TO THE MAIN ACTORS OF THE SECTOR

A research funded by Harvard University, Kennedy School of Government,

the Center for International Development and the Women and Public Policy Program

Conducted by: Luc Roullet

for IPCRI, Israel Palestine Center for Research and Information

August 2005

i

This report is dedicated to the children and teenagers of Nablus

who opened my eyes on the character and the needs of the Palestinians

Special thanks to the members of the Palestinian Network for Small and Microfinance who

shared their experiences, documents and expertise, making this report possible

ii

Executive Summary In time of Intifada, the vibrant Palestinian microfinance sector has spectacularly demonstrated its potential to contribute to the socio-economic survival if not progress of the Palestinian society, with a growing number of clients (approaching 30,000 by end 2005), and with at least one of the main institutions reaching excellent repayment ratios, approaching the standards of international best practices. This performance has been achieved in spite of the sharp economic downturn generated by the second Intifada: after a five-year delay, the performance of the sector is back to the level of the pre-Intifada, thanks to the remarkable adjustments made by the most flexible and specialized institutions, the only microfinance programs that could survive. In the perspective of a potential and gradual phasing out of the Israeli occupation, microfinance is clearly a tool to be developed in order to distribute an hypothetic economic growth to all sectors of the Palestinian societies: the entrepreneurship qualities demonstrated by tens of thousand of women and men mostly from the informal sector has to be supported through adequate microfinance, itself promoted by the Palestinian government and non-government agencies, the national and international financial sector as well as the international donors. Whatever is the pace of the political evolution that would lead to an autonomous Palestinian State, the main challenge for the microfinance stakeholders is to bring this young sector to maturity. Based on comparison with post-conflict Bosnia, or culturally comparable Middle East neighbors, a well-implemented microfinance framework could help MFIs (MicroFinance Institutions) serve as many as 100,000 micro and small entrepreneurs within 4 to 6 years – in the hypothesis of a gradually improving political situation, meaning further Israeli disengagement and improved Palestinian law and order. This would represent 800,000 Palestinians (roughly 20% of the population) benefiting from the socio-economic support of microfinance. The available micro and small lending supply (currently $30Mio outstanding loans), the need of additional loan capital (around $100Mio in order to reach the previous target) is not high compared to what many donors are ready to invest into microfinance and also compared to what commercial banks and international

iii

investors would be ready to invest in financially sustainable MFIs. Furthermore, the number of beneficiaries, the amount to be dedicated to microfinance is really low in the framework of the total aid that will be available for the building of the Palestinian State. Four main challenges must be addressed:

1. The challenge of culture change: “from NGO mindset to financial autonomy” 2. The challenge of capacity-building for all actors of the sector 3. The challenge of the adequate institutional and regulatory framework 4. The challenge of the appropriate increase of lending capital

These four challenges are interrelated, but they must be addressed in the order of priority indicated above. The natural tendency of donors to add a generous amount of capital in a sector has to be balanced in order to accompany a sector that is at the very beginning of its maturation and could be overflowed and damaged by excess capital supply, as it happened in other areas in crisis such as the South of the Philippines in the 1990’s. The first challenge for the microfinance players is to resolve the apparent paradox of “financial sustainability vs. social profitability”. In order to fulfill their mission of social profitability, the financial sustainability of MFIs has to be achieved. The challenge of commercialization cannot be solved by only technical or institutional solutions. It has to go together with a deepening of the effort of capacity-building, following the example of the leading MFIs: Faten and UNWRA. The needs are numerous and regard every single player of the sector: from the loan officers to the management teams and the Boards of Directors. This report recommends, therefore, creating a Palestinian Microfinance Training Center. The Palestinian Monetary Authority (PMA) Governor, as well as the key actors of the sectors, have expressed their willingness to help establishing such a center. Beyond the Training Center, the collaboration between PMA and MFIs would also help to move on the challenge of the institutional framework, promoting a deeper understanding of the differences and complementarily between banks and MFIs. On the mid term, the recommendation is to expand the banking law (through PMA orders, rather than legislative process involving the Palestinian Legislative Council), in order to open banking facilities to MFIs (mostly refinancing and saving mobilization – both requiring adequate supervision). For the short term, the recommendation is to change the rules that govern the current

iv

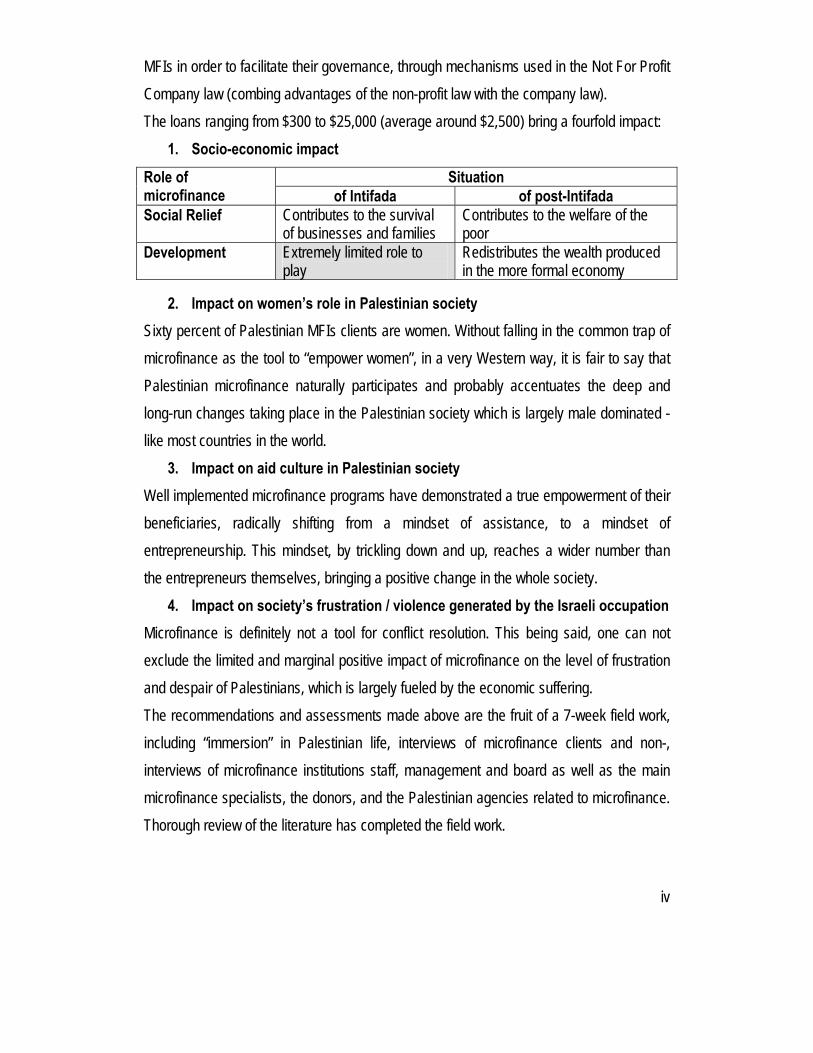

MFIs in order to facilitate their governance, through mechanisms used in the Not For Profit Company law (combing advantages of the non-profit law with the company law). The loans ranging from $300 to $25,000 (average around $2,500) bring a fourfold impact:

1. Socio-economic impact Situation Role of

microfinance of Intifada of post-Intifada Social Relief Contributes to the survival

of businesses and families Contributes to the welfare of the poor

Development Extremely limited role to play

Redistributes the wealth produced in the more formal economy

2. Impact on women’s role in Palestinian society Sixty percent of Palestinian MFIs clients are women. Without falling in the common trap of microfinance as the tool to “empower women”, in a very Western way, it is fair to say that Palestinian microfinance naturally participates and probably accentuates the deep and long-run changes taking place in the Palestinian society which is largely male dominated - like most countries in the world.

3. Impact on aid culture in Palestinian society Well implemented microfinance programs have demonstrated a true empowerment of their beneficiaries, radically shifting from a mindset of assistance, to a mindset of entrepreneurship. This mindset, by trickling down and up, reaches a wider number than the entrepreneurs themselves, bringing a positive change in the whole society.

4. Impact on society’s frustration / violence generated by the Israeli occupation Microfinance is definitely not a tool for conflict resolution. This being said, one can not exclude the limited and marginal positive impact of microfinance on the level of frustration and despair of Palestinians, which is largely fueled by the economic suffering. The recommendations and assessments made above are the fruit of a 7-week field work, including “immersion” in Palestinian life, interviews of microfinance clients and non-, interviews of microfinance institutions staff, management and board as well as the main microfinance specialists, the donors, and the Palestinian agencies related to microfinance. Thorough review of the literature has completed the field work.

v

Table of content EXECUTIVE SUMMARY...................................................................................................................................II

ACKNOWLEDGEMENTS .................................................................................................................................1

PRELIMINARY..................................................................................................................................................2

I. INTRODUCTION.....................................................................................................................................3

A. OBJECTIVES AND LIMITS OF THE RESEARCH ...........................................................................................3 B. ANALYTICAL FRAMEWORK.....................................................................................................................5

1. A framework of conflict or occupation?.........................................................................................5 2. Political and economic framework ................................................................................................5

C. METHODOLOGY....................................................................................................................................7

II. MICROFINANCE IN PALESTINE – A QUICK OVERVIEW...................................................................9

A. DEFINITION OF MICROFINANCE ..............................................................................................................9 B. KEY FACTS ABOUT MICROFINANCE IN PALESTINE....................................................................................9 C. PALESTINIAN MICROFINANCE SECTOR READY FOR THE EXPANSION PHASE..............................................10

III. FINDINGS - DEMAND SIDE.................................................................................................................12

A. SOCIO-ECONOMIC AND POLITICAL SITUATION........................................................................................12 1. Socio-Economic situation ...........................................................................................................12 2. Socio-political framework............................................................................................................14 3. Gender issues ............................................................................................................................15

B. THE IMPACT OF MICROFINANCE IN PALESTINE ......................................................................................16 1. Socio-economic impact ..............................................................................................................16 2. Impact on women’s role in Palestinian society ...........................................................................17 3. Impact on aid culture in Palestinian society................................................................................18 4. Impact on society with regards to frustration and violence generated by the Israeli occupation18

IV. FINDINGS - SUPPLY SIDE ..................................................................................................................20

A. PERFORMANCE OF THE SECTOR:.........................................................................................................20 1. Outreach.....................................................................................................................................20 2. Impact.........................................................................................................................................22 3. Financial sustainability................................................................................................................23 4. Governance – institutionalization................................................................................................24

B. KEY ACTORS......................................................................................................................................25 1. MFIs............................................................................................................................................25 2. Role of banks – role of Palestinian Banking Corporation ...........................................................27 3. Role of government and Palestinian Monetary Authority ...........................................................28

C. LENDING METHODOLOGIES .................................................................................................................29 1. Main Lending Products...............................................................................................................29 2. The case of Islamic lending ........................................................................................................29

vi

D. OTHER FINANCIAL PRODUCTS .............................................................................................................31 1. Microsaving ................................................................................................................................31 2. Microinsurance ...........................................................................................................................32 3. Money transfer............................................................................................................................32

V. POTENTIAL OF MICROFINANCE AND RECOMMENDATIONS ON THE MAIN CHALLENGES.....33

A. POTENTIAL OF MICROFINANCE............................................................................................................34 B. THE CHALLENGE OF “COMMERCIALIZATION”..........................................................................................36 C. THE CHALLENGE OF CAPACITY-BUILDING..............................................................................................36 D. THE CHALLENGE OF THE INSTITUTIONAL FRAMEWORK...........................................................................37 E. THE CHALLENGE OF THE APPROPRIATE INCREASE OF LENDING CAPITAL .................................................38

VI. ANNEXES.............................................................................................................................................40

A. ANNEX I. ABBREVIATIONS AND ACRONYMS ..........................................................................................40 B. ANNEX II: BIBLIOGRAPHY....................................................................................................................42 ANNEX III: MAIN INTERVIEWS.........................................................................................................................44

1. In Ramallah ................................................................................................................................44 2. In Jerusalem...............................................................................................................................44 3. In Qalqilya...................................................................................................................................45 4. In Tulkarem and Betlit.................................................................................................................45 5. In Nablus ....................................................................................................................................45 6. In Jenin .......................................................................................................................................45 7. In Bethlehem ..............................................................................................................................45

1

Acknowledgements This report would not have been possible without the trust expressed in the topic of my research by the Center for International Development and the Women and Public Policy Program at the Kennedy School of Government at Harvard University. The manifested interest for microfinance by Lucy Nusseibeh, executive director of MEND (Middle East Nonviolence and Democracy) was instrumental in the definition of the topic of my research. The confidence of the two executive directors of IPCRI in my ability to draw actionable conclusions from my research was a key success factor in my motivation to interview countless entrepreneurs, microfinance staff, management and board members, as well as a variety of policy makers. All the staff at IPCRI has been very inspiring and intellectually challenging to help me bring microfinance at the level of attention it deserves. Among them, the warm support and bold visions of my colleague and friend Maria Teresa Mammi gave me the drive and enthusiasm necessary to overcome the difficulties associated with the exposure to the daily life in Palestine. Last but not least, the report reached this extension thanks to the passion for a better Palestine that was communicated to me during each encounter with the microfinance people. Board members, executive directors, loan officers and micro entrepreneurs, especially in Ramallah, Nablus and Jenin, gave me their trust by sharing their best insights: beyond the probable approximations and personal opinions with which they may disagree, I hope this report will be at the level of their trust, and will in turn communicate the same belief that well-implemented microfinance can be one of the instruments of change for a better Palestine.

2

Preliminary This research is funded by Harvard University, more specifically by two centers of the Kennedy School of Government:

• The Center for International Development

• The Women And Public Policy Program (WAPPP), through the Nancy Germeshausen Klavans Cultural Bridge Fellowship

This academic funding allows this report to be independent from the political constraints that usually frame the tone of reports from national or international aid institutions. Therefore, this paper’s primary target is to make a truthful assessment of the impact and potential of the microfinance sector in the context of the Israeli occupation of East Jerusalem, West Bank and Gaza (till August 2005), at a time when the uncertain political evolutions can fast change the socio-economic situation, especially in Gaza. The independence of the report as well as the bottom-up methodology of the research gives its unique character, ensuring a complementarity with other reports being written in the same period for IFC, World Bank and the Quartet Envoy team. Contrarily to what some donors would rather believe, microfinance should neither be considered as an economic panacea, nor as a substitute to any political final settlement that will end the Israeli occupation. The end of the military occupation is the single most important action that will free the potential of the Palestinian economy. This report uses the word “Palestine” since it is more convenient than mentioning East Jerusalem, West Bank and Gaza. In other words, the geographical definition of Palestine in this report corresponds to the vision enshrined in the framework of the 2003 Road Map1 that was agreed upon by the Palestinian Authority, the Israeli Government and the international community. The word Intifada is used to describe the current situation in Palestine: the Palestinian uprising and corresponding Israeli repression that started in September 2000 and which is still on-going in August 2005, despite the decrease in number of violent acts on both sides.

1 Annex attached to the 07/05/2003 UN Secretary-General letter to the President of the UN Security Council.

3

I. Introduction Microfinance, if well implemented, can increase or at least limit the decrease of the well-being of the least privileged population, even in situation of crisis. The author of the report has built this conviction both from the growing literature on the topic and from its personal experience especially in Bosnia where he conducted a research for one of the pioneer Bosnian institutions. This institution started microfinance as soon as 1996, few months after the signing of Dayton agreement; its success opened up the way for a vibrant microcredit sector, which remains as of today one of the few lasting economic successes in the post-Dayton agreement Bosnia. Beyond Bosnia, the experiences of tens of microfinance institutions (MFIs) in crisis or post-crisis areas have shown that microfinance can work even in difficult settings2. The numerous failures also tend to demonstrate that (1) microfinance does not fit all situations, and (2) that whatever the environment, success of microfinance necessitates:

• a very high degree of understanding of the real needs of the targeted populations

• the mastery of the different tools required for microfinance (notably adequate lending methodology, financial management, human resources training, good governance and internal control).

A. Objectives and limits of the research Taking into account the context of the Intifada and the fast evolving political situation, this research aims at assessing the impact and potential of microfinance in Palestine if any. It looks especially at the socio-economic situation of the clients and potential clients of the MFIs, as well as the gender issues involved in the implementation of microfinance programs. It builds on the existing state-of-the-art of microfinance in Palestine, as well as draws inspiration from Bosnia, other Middle-Eastern countries, and the rest of the countries where microfinance has been successfully implemented.

2 See especially: Supporting Microfinance in Conflict-Affected Areas, CGAP, Donor Brief n.21, and Geetha Nagarajan, Michael McNulty, Microfinance Amid Conflict: Taking Stock of Available Literature, USAID, both published in 2004.

4

This report is written for the Palestinian microfinance community, for the Palestinian Monetary Authority and the Palestinian Authority, who are all in charge of implementing if not microfinance at least the framework that is conducive for an inclusive financial sector. This report also targets the following actors:

• the international community (especially donors, local embassies, and the Quartet Special Envoy team).

• the Palestinian Legislative Council, which may have, in the mid-term, to pass or amend a law to support and regulate microfinance.

This research is limited in scope since it did not include funding for focus groups and additional surveyors. However the progressive bottom-up approach (see chapter I.C on methodology) anchors the survey in the demand expressed by Palestinians from the villages, cities and refugee camps of the West Bank. The most recent publications and researches on the topic provide more in-depth and academic aspects of the survey. The research has targeted to answer the following questions:

• In the context of the Israeli occupation, can microfinance have any role?

• If yes, what are the types of support that microfinance can bring to the Palestinians?

o Is microfinance effective in building or rebuilding economic assets and activities in West Bank and Gaza?

o Is there any role for microfinance to participate to the economic autonomy of a viable Palestinian State?

o Is there any role for microfinance to decrease social unrest that leads to anger and violence?

o Is there any role for microfinance to contribute positively to the societal changes linked to gender issues, as well to a hypothetical Israeli pullout beyond Gaza?

• What should be the main concrete steps for the NGO community, in coordination with the PA, the Israeli government and the international community?

5

B. Analytical Framework The economic status of Palestine is fully entangled with the political situation. The framework presented below helps disentangling the political from the economic situation, and at the same time emphasizing the vicious and virtuous circles..

1. A framework of conflict or occupation? A recent and growing literature exists on microfinance in conflict and post-conflict areas. Even if each conflict is unique and comparison with other conflicts should be limited, the characteristics of the “Israeli-Palestinian conflict” do not fit, neither with the usual representation of war, nor with what both the Israeli and Palestinian are debating every day: the question of the “Israeli occupation”. In this framework of occupation rather than conflict, it is easier to understand the power asymmetry at stake, and how this asymmetry affects microfinance in a way which is different from Bosnia or Sierra Leone to take the most quoted examples of microfinance in (post-) conflict. Indeed, there are not the usual features of the conflict: two sides more or less equal, represented by their belligerent leaders struggling to gain over the other side through military forces. For decades the Israeli-Palestinian framework is the vicious circle “occupation-violence” where occupation breeds violence, which justifies occupation, which breeds violence, etc. In the middle of this cycle, the economic development is limited, and depends on how tight the military occupation is: number and fluidity of checkpoints, degree of curfews, etc. (restrictions which are related to the extent of Palestinian attacks against Israel). It is important to consider the specificity of the Palestinian situation: rather than impact of the conflict, this report will deal with the economic impacts of occupation.

2. Political and economic framework Since the Palestinian state is the goal agreed upon by the international community, the Palestinian Authority and the Israeli government (the Road Map3), this study sets the mid-term future of microfinance, as a viable economic sector of a potentially sovereign state, eventually having its own central bank and unified laws on all its territory.

3 Id.

6

However, since this is a merely hypothetical future, this study envisages the two simplified political scenarios that directly affect microfinance:

1. Intifada situation with its corresponding “economic repression”4: it is the level of occupation that followed the beginning of the intifada, and that, even if milder, still prevails in West Bank and in Gaza, at least up to the disengagement plan.

2. Post-Intifada situation: the Israeli occupation would fade away in the perspective of a final settlement, giving back to the Palestinians their freedom of movements inside the West Bank, Gaza and East Jerusalem, and also the freedom to cross outside borders.

The main impacts of Intifada related to microfinance are5:

• the injuries and the death toll that have been affecting the Palestinians, including MFI staffs and clients. Besides the direct casualties, there is a permanent trauma due to the material and human cost of violence: the emotional impact of the intifada situation (like any large-scale military operations) would necessitate psycho-social treatments that are far from being provided.

• the “economic repression” which is the result of closures of cities, incursion of the army, house demolitions, weeks-long curfews, flying check-points, and the security barrier (wall or fence) that isolate Palestinians from their livelihood (confiscated agricultural land, inability to access suppliers, markets, etc.)

• beyond the casualties and the emotional and economic aspects mentioned above, the law and order situation during the intifada has been seriously deteriorating with a decrease in the law enforcement and the rise in crime, due to the complete of partial prohibition of Palestinian security forces, leading to their de-legitimization and to the reinforcement of paramilitary if not mafia-like groups.

4 Term used by the United Nations Relief and Works Agency for Palestine Refugees in the Near East (UNWRA). See for instance the 2005 brochure for the Microfinance and Microenterprise Programme. 5 MAS & PCBS Quarterly Economic and Social Monitor - Volume 2, July 2005

7

C. Methodology I was not trying to solve global problems, I was no longer trying to

solve even national problems, I abandoned the bird's eye-view

that let you have knowledge of everything that you see from

above, from the sky. I assumed the worm's eye-view, trying to

find whatever comes right in front of you, smell it, touch it, see if

you can do something about it.6

Taking inspiration from these words of Professor Muhammad Yunus, one of the fathers of microfinance, this research has been structured in a way that privileged the field experience, and the first-hand contact with the Palestinian daily life in the West Bank and in East Jerusalem. The research is based on a bottom-up approach, borrowing tools from complementary fields:

Figure 1

6 Yunus, Muhammad. Speech given at the State of the World Forum. San Francisco, October 4, 1996.

Time period Main activities Type of research Weeks 1-2 Interviews in West Bank cities,

refugee camps and villages, MFI clients and not.

Market research, sociology

Weeks 3-5 Interviews with MFI staff and management

Management consulting, financial analysis

Weeks 6-7 Interviews with academics, Palestinian, Israeli and International Institutions officials (including PMA governor and Quartet Special Envoy team)

Policy recommendation based on politics, economics and human capital analysis

8th week and beyond

Writing of the report Synthesis of the 3 previous phases

8

In the first 2 weeks, the Palestinian hospitality, especially of the NGO MEND (Middle East Nonviolence and Democracy), provided the experience of daily life in the cities of Nablus, Qalqilya and Tulkarem. Contacts in the Ministries of Youth and Sport and Education also helped in Hebron, Jenin and Bethlehem, as well in the refugee camps attached to Jenin and Bethlehem. Experiencing night and day the military occupation in these places, meeting with various groups, including women’s, as well as playing sport and teaching French to groups of youth allowed a better understanding of the daily struggle in cities like Qalqilya and Nablus. In addition to the interviews, a thorough review of the literature has been conducted. The literature brings the more quantitative elements to the research.

9

II. Microfinance in Palestine – a quick overview

A. Definition of microfinance Quoting the recent Microfinance in the Arab States7 report:

Microfinance is the provision of financial services such as credit,

savings, cash transfers, and insurance to poor and low-income

people. These services are generally characterized by:

- Focus on the entrepreneurial poor (…)

- Client-appropriate lending – simple and convenient access to

small, short-term, and repeat loans, with the use of collateral

substitutes (for example, group guarantees or compulsory

savings) to motivate repayment.(…)

Microfinance is widely seen as a two-pronged tool, both working as social relief, and contributing to the development of a country, through the support provided to the entrepreneurial poor section of its population. Two main observations have to be made though:

1. In this double role, microfinance is NOT a miracle tool. It should not be perceived as replacing social provisions, especially for the most vulnerable, neither should microfinance be expected to stimulate macroeconomic development: it can accompany it and amplifies it at most.

2. On the other hand, microfinance can be seen as simply giving the right to financial services for the poorest section of the population: giving the choice to use such a tool is a way to decrease inequalities in the access of resources.

In other words, refusing a naïve enthusiasm, microfinance should be done promoted as one of the components of a modern, just and inclusive financial sector.

B. Key facts about microfinance in Palestine MFIs in Palestine provide loans from $300 to $25,000, with the 8 main MFIs serving 23,000 clients in March 2005, roughly 60% of them being women. Taking into account the

7 Microfinance in the Arab States, building inclusive financial sectors by Judith Brandsma, Deena Burjorjee, for UNCDF, United Nations Capital Development Fund

10

current growth of the main MFIs and microfinance provided by other players, the threshold of 30,000 clients might be approached by the end of 2005 or 2006. The average loan is at $2500, gradually increasing, due to the development of products targeting not only micro but also small businesses. Some consider that “micro” finance ranges from $300 to $5,000, while “small” finance goes from $5,000 to $25,000. However, it is fair to say that the whole range represents the “micro” finance sector in Palestine, since the operators have developed their expertise all over it: the deep contrasts in standards of living between Ramallah and the countryside, suggest that there is more difference between urban and rural businesses than between the so-called “small” and “micro” finance.

C. Palestinian microfinance sector ready for the expansion phase In a simplification of the usual patterns observed in the creation of a mature financial sector, the report “Microfinance in the Arab States”8 presents 4 successive phases that can be observed, in the Arab States and beyond:

1. Start-up 2. Expansion 3. Consolidation 4. Integration For more information on these four phases, the box next page presents excerpts from the

report “Microfinance in the Arab States”.

In this framework, it is fair to say that in 2005, like in 2000 before the beginning of the intifada, the Palestinian microfinance sector is engaged in its second phase. At least two players have well started their expansion (Faten and UNWRA), leading the sector in a growth that is shaped and limited by the unique conditions of the Israeli occupation and by the Intifada in the recent years. If these two leaders can already behave like players of the phase 3., the rest of the players are still in phase 2. or even 1. The purpose of the report is to propose recommendations on the main challenges of the sector as a whole to move along these phases 2, 3 and 4.

8 Id.

11

Figure 2: a framework of analysis for a microfinance sector growth

The Development of the Lower Segments of the Financial Sector9 Although each country has its own unique characteristics, by and large microfinance sectors develop through distinct phases, namely start-up, expansion, consolidation, and integration.

Start-up Phase In the start-up phase, semiformal microfinance activities are introduced as experimental pilot projects. In this phase initial products are developed and tested in the market. The emphasis is on building a human resource base capable of delivering credit products that ensure good repayment. Also in this phase, awareness is built that micro- and small-business entrepreneurs can be credit-worthy. Some pilot projects have failed because of low repayment; they have not discovered techniques applicable to the local context that help ensure repayment.

Expansion Phase In the expansion phase, successful MFIs mostly concentrate on expanding the scale of their existing operations. The success of their business model allows them to expand their activities and to capture a large share of the potential market. Their success leads to replication by other microfinance operators. The emphasis in this stage is on expansion of existing activities and on resource mobilization to finance the expansion. At this stage, MFIs are still subsidized by grants and soft loans to finance the expansion. The increased scale of operations requires further institutional strengthening, particularly in the areas of management systems and procedures. At the end of this phase MFIs have captured a large part of the market with their existing products. (…)

Consolidation Phase In the consolidation phase successful MFIs start to focus on their overall sustainability. (…) The microfinance sector also becomes more formal by gradually establishing generally accepted industry norms. Donor subsidies in the sector diminish in order to avoid continuous subsidization of institutional development. At this stage, the penetration rate of the existing target markets has become high. New products such as insurance, consumer lending, or house-improvement finance are introduced. In order for the sector to enter into the integration phase, it is important that by the end of the consolidation phase a special regulatory framework be in place that is conducive to the development of the microfinance sector and allows for effective prudential regulation by the Central Bank or another relevant agency.

Integration Phase In the integration phase, leading MFIs have become an integral part of the formal financial sector, regulated by the Central Bank or other relevant agency, and offering a range of demand-oriented products for the lower segments in the market. (…) This integration is required for the sector to be able to further finance its growth by attracting capital from commercial sources (savings deposits, loans, and equity). The integration phase is characterized by transformation of MFIs into regulated financial institutions; the disappearance of subsidies for the microfinance sector; and the upscaling of microfinance institutions and the downscaling of commercial banks that, due to an unsubsidized microfinance sector, are now able to operate on a level playing field. (…)

9 Excerpts from Microfinance in the Arab States, building inclusive financial sectors by Judith Brandsma, Deena Burjorjee, for UNCDF, United Nations Capital Development Fund

12

III. Findings - demand side

A. Socio-economic and political situation

1. Socio-Economic situation Palestine ranks 102 out of 177 countries in the UNDP Human Development Index of 2005, close to Viet-Nam and Dominican Republic. Among the 20 Arab countries, it ranks 11th10. It is estimated that the population is growing at a rate of 3.57% on the period 2000-200511, with 5.6 births per woman, making Palestine the fastest growing country in the Arab World after Somalia. 46% of the population is younger than 15 years old in 2004, while 71% live in urban areas. The GDP per capita went down from $1620 in 1999 to $1184 in 2003, due to the impact of the intifada. It is back slightly above $1200 in 2004 and in 2005 forecasts12. The unemployment rates ranges from 26% to 50% according to estimates, while the poverty rate has jumped from 21% in 1999 to 67% in 200513 (more than 80% in Gaza). A direct consequence of the Intifada is the growth of the informal economy:

While the micro enterprise sector – composed of sole-proprietorships and tiny

enterprises employing less than five persons - is both the dominant and

traditional entrepreneurial feature of the economy, constituting 95 percent of all

businesses, there has been significant economic restructuring and growth of the

sector by a large influx of men and women joining the economy by creating

informal micro enterprises to provide income-generating coping and survival

mechanisms in the absence of reliable or stable labour market options. Thus,

informality is playing in an increasing visible and substantial role in the

economy.14 In the banking sector, the ratio of credit to deposits increased during the first quarter of 2005, to become 39.7% compared to 35.9% during the fourth quarter of 200415. This ratio is still abnormally low compared to neighboring countries (60 to 70%) and a well-

10 Arab Human Development Report 2004, UNDP 11 Id. 12 MAS & PCBS Quarterly Economic and Social Monitor - Volume 2, July 2005 13 Id. 14 “Microfinance Note”, June 2005, Palestinian Network for Small and Microfinance. 15 MAS & PCBS Quarterly Economic and Social Monitor - Volume 2, July 2005

13

performing banking sector: banks are afraid of lending in the current political context, and therefore restrict their credit facilities (as well as they follow a reduced demand). Estimates of the number of Palestinians in the world in mid-2005 place them at around 10 million, more than half of whom live in the Diaspora.

Figure 3: distribution of Palestinian population in 200516

The number of inhabitants in the West Bank was around 2.372 million, and in the Gaza Strip 1.390 million. Refugees and their descendants constitute 43% of Palestinians in the West Bank and Gaza Strip17. The refugee status of this population condemns them to permanent and legitimate claims to reparations, as long as a final settlement is not agreed with Israel: since economic opportunities are limited in the camps, many of the most skilled workers emigrate, leaving the least skilled parts of the population struggling with a hopeless situation. The dependency on aid provided by the UN and the international community has negatively affected the mindset of entire populations who were supposed to be in temporary camps: the poor management, if not outright corruption associated with this aid has negatively affected Palestine as a whole, but the level of demand for change has never been as high as it is in 2005. Deep changes in the Palestinian cultures are at stake and can be amplified by adequate policies.

16 Palestinian Central Bureau of Statistics, 2005 17 Id.

14

2. Socio-political framework Beyond the meaning of the military occupation in the daily Palestinian life and its impact on the economic and psycho-social well-being of the population, Palestine is handicapped by two major hurdles that reinforce each other:

• The temporary status of the Palestinian institutions linked to Oslo agreements (a Palestinian Legislative Council instead of a real Parliament, a Palestinian Monetary Authority linked to the Israeli Central Bank, instead of a Palestinian Central Bank, etc.)

• The only recent emergence of a civil service and a political class, whose leaders have been often more recruited for their results in the national struggle than for their administrative and political skills.

The credibility of the Palestinian Authority is damaged by the continuous Israeli occupation, if not outright annexation of West Bank territories, as well as by the level of corruption: Palestine ranks 108 out of 145 countries in the 2004 Corruption Perception Index of Transparency International. Beyond these bleak facts, the recent changes for the PA president, and as a consequence, for the president of the Palestinian Monetary Authority, have brought more skills in the socio-economic management of the country, on which the microfinance can build to construct itself.

15

3. Gender issues In spite of the limited number of data available, it is fair to say that the inequalities between genders in Palestine are below the average of the Arab world. According to the UNDP Arab Development Report 200418, the combined gross ratio for primary, secondary and tertiary level schools slightly higher for female than for male (81% vs. 78%); it is also one of the highest in the Arab World. However the economic activity rate shows a dramatic difference between men (66%) and women (10%). These figures cover the period from 1986 to 2001: the latest figures suggest that the impact of intifada has increased the participation of women in economic activities (most of them informal) in order to add a new income to the household: out of the 134,000 Palestinian (mostly men) working in Israel in 1999, only 60,000 still do so in 200519, with the bleak prospect of borders fully closed to Palestinian workers by 2008. At a more societal level, the MAS & PCBS Quarterly Economic and Social Monitor of June 2005 mentions the following:

Officials from the Palestinian Ministry for Women Affairs (as

quoted in the British Guardian newspaper on 23 June) stated

that 20 women and girls were killed during the past year within the

framework of what is called ‘crimes of honour’. They added that

50 girls committed suicide (probably under family pressure) to

clear a perceived blemish on family honour due to suspicions of

sexual relations outside marriage, or in order to avoid an imposed

marriage, or to escape from a hated marital relationship. The

officials said that also 15 girls escaped killing attempts related to

crimes of honour during the previous year.

It is worth mentioning that laws inherited from the Jordanian era

treat women as ‘minors’ that fall under the protection of their male

relatives. Such laws impose a maximum punishment of 6 months

18 UNDP Arab Development Report 2004 19 MAS & PCBS Quarterly Economic and Social Monitor - Volume 2, July 2005

16

imprisonment for homicide if it is a ‘crime of honour’. Women’s

organizations have asked the Legislative Council to amend the

law, but are facing opposition from some members of parliament

who think that abrogation of those laws will destroy the tissue of

moral values governing Palestinian society.

Even if these facts are fairly disconnected from microfinance, it is worth mentioning them, since they relate in a nutshell to the interviews conducted with MFI clients and staff: most men and women interviewed underlined the hope that Palestinians would shape a society that would gradually give women more rights than currently.

B. The impact of microfinance in Palestine As expressed by Mr. Naser Abdelkarim, Professor at Bir-Zeit University and member of the board of Faten, there has been no impact survey conducted in Palestine that proves the extent and limits of microfinance. However, he continues, it is beyond doubt that microfinance since it started in Palestine, has positively contributed to the well-being of its clients. This chapter will underline that the impact observed in Palestine, is surely below what the most microfinance enthusiasts believe, but is nevertheless worth the promotion of well-implemented microcredit programs. In Palestine like in other countries, there is a sharp contrast between the needs of economists for tangible quantitative, and the availability of measured or even measurable variables. The following presentation of various categories of impact underline the fact that microfinance contributions go beyond increased income and assets building, to provide the building a variety of intangible assets. These intangible assets (cultural and societal) are the basis for future investments that will provide returns for the society, both economic and social returns.

1. Socio-economic impact In front of the enthusiasm generated by microcredit, especially in the context of the UN 2005 microcredit year, it is important not to see microfinance as the “miracle tool” for poverty alleviation and economic development. For instance, it will not replace the necessary investments in infrastructure and education that should guarantee a long-term

17

economic growth. On the other hand, it is important to recognize its contribution to the socio-economic well-being of families, due to a slight increase of their income, which can improve health and education among other. Microfinance is a tool that will address the need of a limited but fairly large fraction of the population (20% as estimated earlier), the most vulnerable families which run a business on their own. The gains from microfinance can be summarized in the following way:

Figure 4: the simplified role of microfinance in Palestine

Situation Role of microfinance of Intifada of post-Intifada Social Relief Contributes to the survival

of businesses and families Contributes to the welfare of the poor

Development Extremely limited role to play

Redistributes the wealth produced in the more formal economy

Like in other conflict or post-conflict areas, the disarmament and demobilization of armed militants is a painful process and microfinance can be used as a tool to provide new livelihood to demobilized forces. At a time when the Palestinian Authority is consolidating its grasp on the various military and paramilitary forces, interviews and studies show that economic considerations are a key issue in the unification and streamlining of the military and police forces: alongside other tools favoring employment, microfinance can be used as an incentive for the military militants to demobilize and stay demobilized.

2. Impact on women’s role in Palestinian society To those donors who say that microfinance is the ideal tool to reform the Muslim or Arab society, especially “to empower women”, it is important to remind them that:

• such a belief has neocolonial accents and does not take into accounts the needs and specific forces at stake in the Palestinian society.

• if many women work during the second intifada, it is because they are forced to do so for survival, and that as soon as their husbands could go back to work, both wives and husbands could be happy to go back to their more traditional distribution of roles.

18

• the last 30 years in Palestine have seen the role of women alternatively increase and decrease due to societal, religious and political forces which are much more powerful than those generated by microfinance.

On the other hand, the majority of women clients of MFIs, like the staff and management, express that, if not for themselves, at least for their daughters, their new role of working women will affect their society, albeit gradually and on the long term. They are the first ones to recognize the importance of a higher participation of women in all compartments of public and professional life, as well as the need to respect the pace of change of their society. In this context, when microfinance provides loans to a majority of women, it is fair to say that it participates and probably accentuates the deep, long-run and often painful changes at stake in the society.

3. Impact on aid culture in Palestinian society The most enthusiastic supporters of microfinance underline the fact that while traditional aid “gets lost”, microcredit is self-sustainable. This should not be overstated, and should not bring blame to other types of aid. Both microfinance and any kind of aid can be mismanaged and eventually not benefit the targeted population. On the other hand, it is true that the international community assistance that has been lasting since 1948 and at a higher degree since 1967 has in the words of many Palestinians “corrupted” the Palestinian culture from the top of society to all levels of the population by trickling down effect. Moreover, poorly-implemented microfinance programs have in the past created “credit pollution”; when it was tolerated that the beneficiaries would not fully pay back their loans. In this context, well implemented microfinance programs have demonstrated a true empowerment of their beneficiaries, who have shifted from a mindset of assistance, to a mindset of entrepreneurship. By trickling down and up onto their family and neighbors, the self-sufficiency mindset of microfinance gives hope to a wider number than the entrepreneurs themselves.

4. Impact on society with regards to frustration and violence generated by the Israeli occupation

The most enthusiastic supporters of microfinance underline the fact that it is a tool for conflict resolution. The most extreme examples in Bosnia have shown donors imposing

19

the inclusion of women from different ethnicities in solidarity groups. Unfortunately for these donors, microfinance is definitely not a tool for conflict resolution. At most, and under specific conditions, it can be used in conflict or post-conflict settings. For more background information on this topic, the bibliography (chapter VI.B) proposes the latest papers on the topic. Moreover, as argued in chapter I.B.1, Palestine is primarily not under conflict, but under occupation: there is only very limited comparison to do with Rwanda, Sierra Leone or Bosnia, where microfinance has been successfully implemented. This being said, one can not exclude the limited and marginal positive impact of microfinance on the level of frustration and despair of Palestinians. A society where every citizen has got some economic perspectives, which secure possibilities of better health, education, etc., is a society where the emotional burden to carry is decreased. In the economic package that has been promised to the Palestinians to prepare the creation of an autonomous state, microfinance has therefore its place, to contribute to the well-being of a fraction of the society: microfinance can marginally contain the frustrations and angers, which can degenerate in violence and lawlessness against Israelis and Palestinians themselves. Furthermore, in the perspective of an hypothetical end of Israeli occupation, the “day after” has to be actively prepared: after a pullout, as massive as it might be, it will not be the end of the economic difficulties, and there will not be any more check points or curfews to blame for the “economic repression”. Microfinance will help prepare the transition by having tens of thousand of self-employed Palestinians having faith in their own capabilities to generate income, on their own, or in new companies to be created: shifting the attention from the past (equating to repression) to the future (equating to economic, social and national opportunities) is one of the key intangible returns that microfinance can provided to the Palestinians.

20

IV. Findings - supply side This chapter reviews some of the themes introduced in the chapter on the demand side, taking into account the point of view of the players / suppliers of microfinance.

A. Performance of the sector:

1. Outreach Most of the microfinance supply in Palestine is provided by the 8 major MFIs regrouped under the Palestinian Network for Small and Microfinance. As they put it, “over the past decade these institutions have invested an impressive $US180 million in 170,000 loans; equivalent to three loans for every Palestinian enterprise”20. On next page, the table published by the Network shows that these 8 MFIS are serving 23,000 clients as of March 2005, with close to US$30 million outstanding loans, corresponding to an average of $1,274 per outstanding loan (and more or less the double for the average amount of loan released). These amounts are gradually increasing with a shift of the main actors towards the so-called “small” finance that complements their activity of “micro” finance. Geographically, the 75 offices cover most of the main towns and villages of the West Bank and Gaza. As shown in the table, the MFIs offer an increasing number of loan products. Even if housing and consumer/personal loans have been gradually introduced in the last years, the bulk (more than 90%) of the loans remain working capital for microentrepreneurs (through group or individual lending). In addition to the microentrepreneurs, loans to SME have to be taken into account. However, from the point of view of the Palestinian MFIs, the difference between micro and SME (which may seem obvious to donors such as IFC or World Bank), is blurred, due to the true continuum between these 2 types of businesses, and to the similar way the individual lending methodology serve these entrepreneurs.

20 “Microfinance Note”, June 2005, Palestinian Network for Small and Microfinance.

21

Figure 5: main indicators for the eight MFIs of the Palestinian Network for Small and Microfinance Network21 Microfinance Institutions in the Occupied Palestinian Territories

Outreach Indicators ACAD ASALA CHF FATEN PARC PDF/PBC UNRWA YMCA Total No. of Active Loans 1,148 1,845 2,887 3,521 1,744 262 10,511 1,702 22,990 Outstanding balance (US$) 2,662,200 1,487,758 9,112,000 2,969,005 1,205,575 2,321,212 6,259,396 3,264,748 29,281,894 Ave. outstanding balance (US$ 2,319 806 3,156 843 691 8,859 596 3,045 1,274 No. of loans disbursed (2004) 684 2,059 1,120 5,873 1,183 107 14,852 192 26,070 Value of loans disbursed (2004) 2,111,700 1,300,600 5,309,000 4,356,010 1,248,774 1,344,500 12,590,366 1,094,950 29,355,900 Average loans size (US$) 1,276 632 4,732 741 1,056 12,565 848 5,702 1,126 Total No. of loans disbursed 1,655 7,953 7,100 65,076 2,752 312 83,852 2,050 170,750 Cumulative disbursements (US$)

6,712,518 6,134,070 32,850,000 28,742,920 2,534,312 4,571,060 88,999,475 10,000,000 180,544,355

No. of offices 8 8 8 15 15 3 11 7 75 Products SME √ √ √ √ √ √ √ Microenterprise √ √ √ √ √ √ Group lending √ √ √ √ Housing √ √ √ June 05 √ Consumer/personal √ √ All Figures are referring to March 2005, unless otherwise indicated

21 “Microfinance Note”, June 2005, Palestinian Network for Small and Microfinance.

22

2. Impact As mentioned on the demand side, the impact, even though hard to prove with numbers, is perceived as overall positive by the board of directors, the managers and loan officers. Beyond the direct “micro-impact” on the families and the communities, they insist on what they perceive as a good change of mentality for their country:

• Change of the mindset linked to traditional aid provided for relief and hypothetical development.

• Change of the mindset even in the banking sector. On the first point, a number of interviewees expressed anger at the way the continuous international aid since 60 years has polluted and corrupted the Palestinian mentalities, by creating expectations for easy money, with low control on the usage of it. On the other hand, microfinance implies at all levels (from the donor down to the MFI client, and even his or her clients) a great rigor in the management of money disbursements and allocation of income for differentiated purposes. In other words, microfinance has an indirect educative role for Palestinian families, other NGOs as well as donors which are stricter in disbursing funds to MFIs. In that respect MFIs are victims of their own success: the increased expectations of the donors’ community for their own performance, in such a way that the underperforming ones are and will be in dire straits unless they review their operations (see chapter V. for recommendations on this regard). On the second point, MFI managers, banking managers and banking supervising bodies insist on the fact that the banking sector has not been enough geared towards financing enterprises (big, small and very small): the success of microfinance is now encouraging some banks to lend not only for housing and consuming purposes, but also for increase in working capital. In other words, microfinance contributes to the reshaping of the whole financial sector in Palestine.

23

3. Financial sustainability It is hard to demand positive financial return from NGOs struggling for their own survival in the service of families that may have lost members or even houses. On the other hand, what is amazing in the Palestinian microfinance sector is that at least one NGO has reached close to international standards in terms of quality of portfolio and financial ratios like the PAR (Portfolio at Risk): as of June 2005, only 3.89% of Faten portfolio is delayed of one day or more. One of the paradoxes of microfinance under occupation, is that it works “because it is micro” to use the words of Harvard Economics Professor Robert Lawrence: while most sectors of the Palestinian economy suffer from the “economic repression”, consequence of curfews and roadblocks, the smallest sectors that work on the smallest markets are those which see the least disruption in their activities, since their clients may anyway be inside the almost autarkic market imposed by checkpoints. This view has to be nuanced by the fact that many microentrepreneurs still need access to suppliers and markets that might be behind the checkpoints closing their cities, which means that they suffer like other entrepreneurs. In that respect, one can ask the purely rhetorical question: is the economic repression linked to the intifada a chance or an obstacle for the development of microfinance? It is an obstacle for the obvious reasons mentioned earlier, especially in chapter III.A presenting the socio-economic and political situation. But, if one wants to see the more encouraging side of the coin, it has also been a chance because:

• It increased professionalism of the operations, generated by the need of survival

• It increased a sense of unity of the staff, management, board, and even between MFIs.

• It accelerated the awareness that microfinance has to be sustainable in order to survive.

On this last point, it is crucial to admit that some MFIs fully understood it, while some take the excuse of the economic consequences of intifada to delay the necessary improvement of their operations.

24

4. Governance – institutionalization Three levels can be observed:

1. Governance of each NGO 2. Governance of the MFI community by itself 3. Governance of the MFI community by external players

On the first point, only too few MFIs have the necessary “trio”: a truly active Board of Directors, an Executive Director with a strong leadership team, and an Internal Audit reporting to the Board of Directors. Even if some are in the process of building such an organizational structure, there is a long way to have it implemented and properly working, adapted to the specific institutional framework of each MFI. Only the MFIs that differ from the most commonly used incorporation (Non-for-Profit organization), have been able to go a rather long way on this direction: UNWRA, which is a UN project and Faten which is a Non-Profit Company registered as such in Gaza, under the old Egyptian law at a time when it was still possible. Some (including many MFI executive directors) believe that the remedy to their governance issue is to change their legal status (new incorporation); if this is true, it is also even more relevant to generate the will to improve governance, inside the MFI (starting from the Board of Directors – which are sometime very reluctant to go in a direction where they may lose their traditional power). Regarding the governance of the MFI community by itself, the Palestinian Network is a good step towards a higher advocacy of microfinance, better exchange of best practices, etc. However, there are tensions on the way to proceed, and especially on how to allocate limited resources among MFIs (additional capital being the main among them). These tensions should be resolved by admitting that every MFI has a different competitive advantage, that the international and national communities will provide any support (financial and non) to those who will be able to demonstrate the highest capacity to use it. In other words, the newly created Palestinian Network has to find its role and voice, and be careful not to fall in the temptation of regulating too much, especially the allocation of funds: by doing this, they will maybe help on short-run the MFIs in need of support, but this

25

will not help the whole sector on the long-run. Further recommendations on the role of the Palestinian Network are given in chapter V. As for the governance of the MFI community by external players is concerned, two main groups have to be considered: national authorities and international player. The national authorities have played an irrelevant role so far: both the Ministry of Finance and the Palestinian Monetary Authority (the main 2 possible authorities intervening in the market) have been bystander till recently. It is time for the PMA to play a more active role, as proposed in paragraph IV.B.3. As far as international actors are concerned, they are mostly donors, from the Arab world, and from the Western world (which includes both donor agencies, and multilateral agencies based in Washington and New York). In Palestine, like in other parts of the world, these donors have the tendency to give too quickly, without having understood enough the sector and its constraints, and imposing conditionalities that might disrupt profoundly the fragile equilibrium where MFIs operate. MFIs in need of additional capital might not have the capacity to tell these agencies that they are most welcome to help, but that some of their plans might not be the most adequate. Donors should demonstrate a careful understanding of the specific needs of the Palestinian MFIs and of the broad requirements of microfinance in general. The recently created CGAP hub in Jordan will contribute to the donors’ training, with its focus on microfinance in the Middle East and North Africa.

B. Key actors

1. MFIs Two MFIs represent close to 80% of the number of microfinance loans released in the last decade in Palestine, and 70% in amount: Faten and UNRWA. Faten has benefited from the expertise and financial support of Save the Children USA that started the program, while UNRWA from the UN system expertise and financial capacity. While Faten is as of today entirely Palestinian, UNWRA is more international with its Scottish Executive Director and international board (even if the staff in Palestine is entirely Palestinian). This being said, the success of both MFIs is based on the intimate

26

knowledge of the needs of the clients, as well as a very high demand from the management and the main stakeholders in terms of repayment. Prison for contract enforcement is in both case the example that illustrates how serious they are about implementing a strict methodology where the individual is responsible for his/her own loan, and if not him or her, the group or warrantors who signed the contracts with him. Both MFIs take legitimate pride in having transformed the mindset of their clients, in communities “credit polluted” by less scrupulous loan assistance programs. The key success of Faten is in its very low Portfolio at Risk (PAR) ratio: only 3.89% of its portfolio is delayed of one day or more as of June 2005. The same ratio goes down to 1.48% when calculated for the portfolio delayed of 30 days or more: ranging from 6.13% in Jenin branch down to 0.56% in Rafah branch in Gaza22. This astounding result comes from the translation of very strict credit discipline in simple and effective policies: for instance for the individual loans, the guarantor has to receive a regular salary and to sign a contract with Faten and the bank that authorizes the bank to debit from its salary whatever amount would be late from Faten’s client for whom s/he is guarantor. However, this level of quality of portfolio, combined with a medium-sized portfolio does not secure yet financial sustainability: Faten has reached the so-called Operational Self-Sufficiency by mid-2005, but not the Financial Self-Sufficiency. The first one gives the indication of covering its own costs under current operations, the other one signifies the covering of its costs including the financial cost linked to hypothetical commercial loans. The key feature of UNWRA is to be found in its growth beyond Gaza and West Bank: the Intifada led UNWRA to concentrate on other Palestinian refugees, in Jordan and Syria. Replicating the success encountered with microentreprise loans (individual and group) UNWRA is expanding its operations. As of March 2005, UNWRA had 10,511 active loans in Palestine (more than 40% of the total active loans in Palestine), to which more than 2,000 should be added for the two other countries. If the extension over 3 countries is justified by the population targeted by UNWRA, it remains very exceptional for an MFI to

22 Financial Indicators, June 2005, Faten.

27

take this risk: main obstacles to successfully manage a program on 3 different countries include the different legal and political frameworks, the different economic cycles, as well as the key constraint of management and control over operations which are beyond borders. Behind the outstanding performance of both actors, numerous challenges must still be overcome. Like for any other Palestinian economic actor, the most unpredictable challenge is the evolution of the political situation, especially in Gaza after the pullout of the Israeli settlers and army.

2. Role of banks – role of Palestinian Banking Corporation As stated by a Palestinian MFI executive director, “banks provide bank accounts and consumer and housing lending, while microfinance provides lending to entrepreneurs”. If this may be true in Palestine, it is certainly changing, and it does not take much to predict that, like in other countries (Middle Eastern and beyond), there will be a gradual convergence of the services provided by MFIs and banks: some MFIs will probably incorporate into banks, and some banks will more systematically include lending to small if not micro-entrepreneurs. While IFC has been financing banks for microfinance lending till the beginning of the Intifada, other schemes are possible for banking microfinance: IFAD has provided ANERA with a fund of around $4Mio. This capital is used as a guarantee for 75% of the loans released by the bank working in partnership with ANERA. Although this scheme is interesting to distribute the risk and the expertise, it has not yet shown how scalable it can be. Unlike other MFIs that exploit most of their lending capacities, this scheme does not disburse more than 15% of their capacity as of the summer 2005. For the bank, this comes from the lack of “sound” clients under the conditions of the Intifada, but it also probably comes from the lack of specialization in an adequate lending methodology, as Faten has been able to demonstrate the feasibility. The only bank that is still doing microfinance, even though at a small scale compared to Faten and UNWRA, is PBC: Palestinian Banking Corporation. This unique development bank on the Palestinian market, financed mostly with European grants, positions itself very naturally between MFIs and commercial banks. However, the bank has not been

28

performing as it should have: to make it short, its poor performance has led to a change in the management, with the objective to “mend the balance sheet” as well as to re-focus the mission of the bank. This last point is the most critical result of the contrasting interests of the former European management, the European donor (the EU), and the Palestinian members of the board. With a new management since early 2005, the bank gave itself till the end of the year to re-define a clear mission based on its assets and the development needs of Palestine. Financing MFIs with international loans or grants that they would manage on a commercial basis is definitely one the missions that they should consider taking on, as long as they retain to have - or to be able to hire - the expertise to do so (from their board down to the lending team).

3. Role of government and Palestinian Monetary Authority Most interviews, be it with government, PMA, and microfinance actors concluded that it was better for the government not to intervene directly in the microfinance sector: the dynamics of the sector, financed mostly by external donors, would not benefit from the intervention of a third party that is not knowledgeable enough (because no agency has developed the expertise yet). This being said, at least in the Ministry of finance, some expertise should be gradually accumulated, in order to assist the sector to simplify the incorporation process of MFIs, into the most suited legal status. As far as the PMA is concerned, during the 2005 meeting between the newly appointed Governor and the representatives of the Palestinian Network, the main messages were:

• From the MFIs representatives: “we need your help to draft a law on microfinance in Palestine, and here is a proposal”.

• From the PMA governor: “microfinance is a sector that is good for Palestine, we are dedicating more resources to monitor it, but it has to grow before we see the need for us to help you in drafting a law”.

In other words, the PMA and the MFI sector are in the process of learning from each other, which is very similar to what happens in other countries where the microfinance sector emerges. In spite of the limited outcome of this first encounter, the mutual interest

29

expressed at the meeting is a good beginning on which the sector (practitioners and policy-makers) will build on. For more specific recommendations see chapter V.

C. Lending methodologies

1. Main Lending Products As discussed earlier and shown in Figure 5: main indicators for the eight MFIs of the

Palestinian Network for Small and Microfinance Network, the level of diversification of the sector is pretty high in terms of lending products, but no saving or insurance products have been introduced yet. However, only Faten and UNWRA have developed the full range of lending products (from micro to small enterprises, from lending to consumer through housing loans). The level of interest rates is in line with other countries for the group lending methodologies (around 2% monthly for group loans and 1% for individual loan). Following the economic law on diminishing return, interest rates decrease with the increase in the amount of loan, reaching as low as 5 to 8% yearly (on initial balance), rates competitive with the banks’. In other words, the bridge between the pure microfinance and pure banking finance has been established: what is interesting in the case of Palestine is that MFIs have been quicker than banks to bridge the gap, showing how professional they are.

2. The case of Islamic lending Practitioners differ in their perception of the role of Islamic lending. Before debating the pros and cons, few facts about Islamic lending:

• Main characteristics deal with the prohibition of interest by Islam. Islamic microfinance like Islamic banking proposes “profit sharing” rather than “interest:”, and beyond the interest, impose that the money is not released directly to the client, but to the party from which they would purchase goods or services with the proceeds of the loan.

• Microfinance lending has started in a formalized and larger scale way in 2005 with the funds provided by the Islamic Development Bank to the main MFIs, most of

30

them ready to accept additional loan, even if they did not know yet how to provide Islamic loans.

On the “cons” side, some argue that Islamic microfinance is not optimal because:

• The additional administrative requirements make it a more costly product: either the MFI earns less money and struggles to reach break-even on this product, or the rate is higher than for comparable “regular” loans, bringing a burden on the clients.

• Some, especially western donors and practitioners, see microfinance lending as a way to promote Islam and therefore refuse the mixture of religion and finance.

On the “pros” side, some argue that:

• Even though the cost might be slightly higher than for an equivalent “regular loan”, the choice is provided to the client, and therefore it is his or her personal rationale choice to best seek for a form of funding, which is compatible with his/her own beliefs.

• Beyond the hypothetical risk of “Islamization” of microfinance, some believe that Islamic lending has to be seen as one of the various products provided to clients: the more fitted the products are to the demand, the larger the market.

Interviews with clients suggest that some of them struggle with the contradiction linked to the paying of interest: this is something prohibited by the Koran, but at the same time it is necessary for them to get a loan for the survival of their business and their families. Overall, and beyond ideological or religious considerations, Islamic lending can be proposed, in order to expand microfinance impact. Taking comparison with other Middle Eastern and North African countries, it is fair to expect a share of Islamic lending in the same order of magnitude, or slightly lower, since Palestinians are rather less conservative than their neighbors. Mohammed Khaled, former executive director of Faten, estimates that the percentage of Islamic lending on the total is in the lower range or below the 25-30% potential market observed in other Middle Eastern

31

countries, while the study23 conducted between November 2001 and April 2002 by Massar Associates for ISAMI and USAID suggests the figure of 26%.

D. Other financial products

1. Microsaving Not yet mobilized in Palestine by MFIs, microsaving is probably the next financial tool to be considered in order to provide a better support to clients (demand side), as well as to generate more lending capital (supply side). On the first point, it is clear that the available liquidity in Palestine is not as high as in other developing countries, seen the socio-economic conditions generated by the intifada. Furthermore, for clients living in villages remote from banks, the demand for a saving account is lower than in economically comparable societies: the roadblocks and curfews that regularly block the entry to and exit from cities are a major incentive to keep savings at home. This being said, market research would probably show that at least some fractions of the market (probably in cities) would be interested in short term saving products, such as for instance blocked saving accounts that would allow business loans with preferential interest rates: the combination of loan and saving is a common and financially sound way to generate additional revolving capital for MFIs, and increase social impact for the clients. On the supply side, the current laws in Palestine do not allow MFIs to mobilize saving, unless they transform into banks (some have begun working on such plans). Therefore the promotion of microsaving has to be done in the context of a potentially evolving regulatory context. As it will be discussed in chapter V.D, the earlier the sector prepares this logical market evolution, the better. A vision to explore for the mid-term future is the potential partnerships between MFIs and banks. The MFIs would promote savings on behalf of banks that would in return provide them with preferential loans: MFIs would fuel the growth of banks by increasing their

23 Assessment of Demand and Supply of Small and Microcredit in the West Bank and Gaza Under Current Political Situation

32

deposits, which would in turn be lent to themselves, in order to increase their loan portfolios.

2. Microinsurance Speaking of microinsurance in the uncertain framework of the Intifada may sound provocative. However, like for microsaving, the sector could gradually prepare for an end of the Intifada and provide simple products. We can distinguish between 2 main types of microinsurance:

• microinsurance on the reimbursement of the loan, paid upon release of the loan.

• microinsurance on risks independently from the loan (health, property, pension fund, etc.)