michigan public school employees...valuation report issued march 6, 2018. this presentation should...

TRANSCRIPT

Copyright © 2018 GRS – All rights reserved.

Michigan Public School Employees

Retiree Health Actuarial Valuation Results as of September 30, 2017

Retiree Health BenefitsThe Funding Issue

• Unlike pensions, health benefits have not been pre-funded for a long period of time

– Most plan sponsors nationwide have not pre-funded health benefits either

– Currently very little investment income to help pay benefits

• Costs rise as more members retire, and health inflation outpaces general inflation

• Pre-funding contributions have been calculated since 1999 – but pre-funding started only recently

2

Full Funding Employer Contribution

• Reported that full funding for MPSERS began in fiscal year (FY) 2013

• September 30, 2017 valuation establishes the required employer contribution for FY 2020

• Reflects 3% of payroll active member contributions required to participate in the defined benefit retiree health program

• Reflects plan changes resulting from Public Act 300 of 2012

• Reflects investment return assumption that was lowered from 7.50% to 7.15% in accordance with the recently adopted Dedicated Gains Policy

3

Governmental Accounting Standards Board

• Beginning with the 2007 CAFR, GASB Statements No. 43 and No. 45 specified how retiree health benefit liabilities and expenses were reported in financial statements– One annual valuation report for accounting and funding

purposes

• GASB Statement No. 74 became effective for the plan for the fiscal year ending September 30, 2017– Results are based upon:

� the September 30, 2016 actuarial valuation results “rolled-forward” to the September 30, 2017 measurement date

� the investment return assumption prior to the change resulting from the Dedicated Gains Policy (i.e., 7.50%)

– A separate report was issued December 21, 2017 containing the September 30, 2017 annual valuation for accounting purposes

4

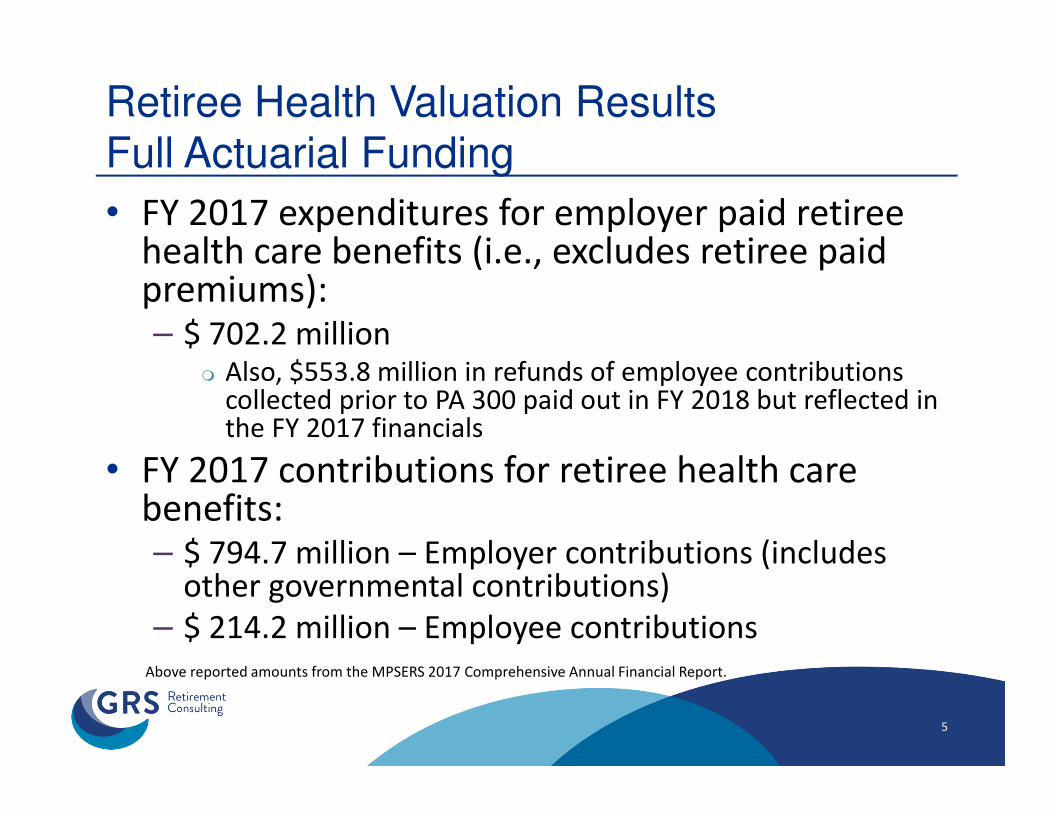

Retiree Health Valuation ResultsFull Actuarial Funding

• FY 2017 expenditures for employer paid retiree health care benefits (i.e., excludes retiree paid premiums):– $ 702.2 million

� Also, $553.8 million in refunds of employee contributions collected prior to PA 300 paid out in FY 2018 but reflected in the FY 2017 financials

• FY 2017 contributions for retiree health care benefits:– $ 794.7 million – Employer contributions (includes

other governmental contributions)

– $ 214.2 million – Employee contributions

5

Above reported amounts from the MPSERS 2017 Comprehensive Annual Financial Report.

Actuarially Computed Employer ContributionFY 2020 ($ in Millions)

6

• Actuarially computed employer contribution for FYE

September 30, 2020:

• Once fully funded, the annual employer contribution

requirement decreases to the normal cost

Employer Normal Cost $ 34.2

Amortization of UAAL1

604.2

Actuarially Computed

Employer Contribution $ 638.4

FY 2020

1 Unfunded Actuarial Accrued Liabilities (UAAL) were amortized over 19 years from October 1, 2019.

Actuarial Gain/(Loss) ($ in Millions)

7

1. Premiums. Gains and losses resulting from

actual premiums in valuation year versus

that assumed from prior valuation. $ 1,434.4

2. Investment Income. If there is greater

investment income than assumed, there is a

gain. If less income, a loss. 259.5

3. Demographic and Other. Gains and losses

resulting from demographic experience,

data adjustments, timing of financial

transactions, etc. 67.1

4. Composite Gain/(Loss) During Year. $ 1,761.0

Gain/(Loss)

Circumstances That Would Increase Projected Costs

• Medicare funding reductions or cost shifting

• Unexpected new benefit recipients (from health benefit cutbacks of

other employers)

• Medical inflation worse than assumed; the actual future

contributions will depend on future per capita health cost increases

(health inflation)*

• Active member population decline (contribution rates as a

percentage of payroll would increase)

• Lower than expected investment returns; bigger impact as plan

assets grow

• This is not a complete list

8

* Per capita costs are projected to increase 7.5% the first year, graded down to 3.5% in the twelfth and

later years.

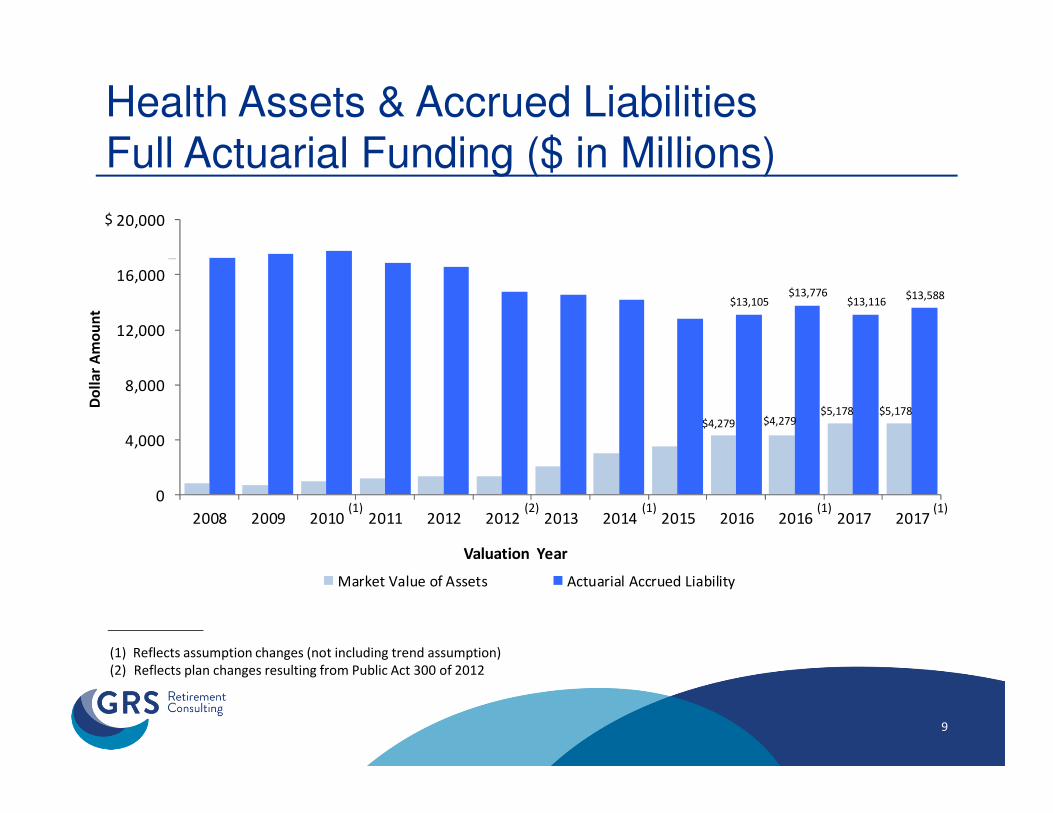

Health Assets & Accrued Liabilities Full Actuarial Funding ($ in Millions)

9

$4,279 $4,279$5,178 $5,178

$13,105$13,776

$13,116$13,588

0

4,000

8,000

12,000

16,000

20,000

2008 2009 2010 2011 2012 2012 2013 2014 2015 2016 2016 2017 2017

Valuation Year

Market Value of Assets Actuarial Accrued Liability

Do

lla

r A

mo

un

t

(1) Reflects assumption changes (not including trend assumption)

(2) Reflects plan changes resulting from Public Act 300 of 2012

(1)

$

(1) (2) (1) (1)

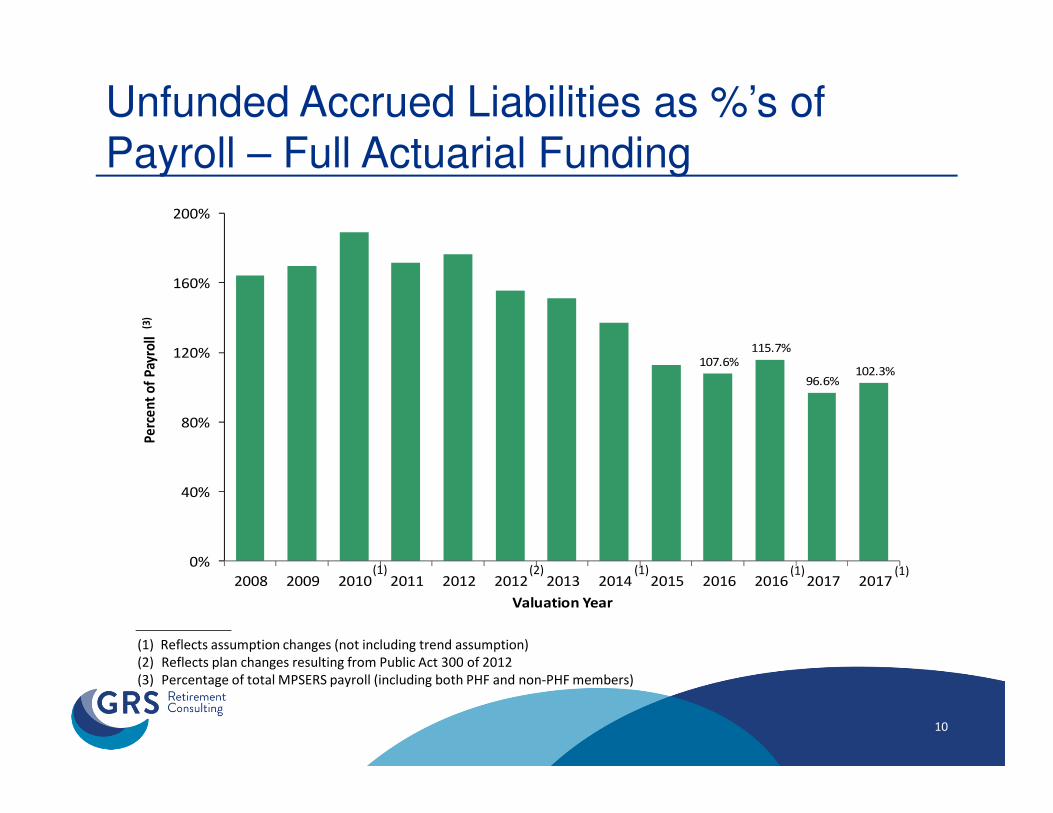

Unfunded Accrued Liabilities as %’s of Payroll – Full Actuarial Funding

107.6%115.7%

96.6%102.3%

0%

40%

80%

120%

160%

200%

2008 2009 2010 2011 2012 2012 2013 2014 2015 2016 2016 2017 2017

Pe

rce

nt

of

Pay

roll

(3)

Valuation Year

10

(1) Reflects assumption changes (not including trend assumption)

(2) Reflects plan changes resulting from Public Act 300 of 2012

(3) Percentage of total MPSERS payroll (including both PHF and non-PHF members)

(1)(1) (2) (1) (1)

Required Employer Contributions as Percents of Payroll (Full Actuarial Funding)

11

0.36% 0.31%0.52%0.07%

7.31%7.57%

6.43% 6.65%

0%

5%

10%

15%

20%

2008 2009 2010 2011 2012 2013 2014 2015 2016 2016 2017 2017

Empl

oyer

Con

trib

utio

n %

(3)

Valuation Year

Amortization Payments Normal Cost

(1) Reflects assumption changes (not including trend assumption)

(2) Reflects plan changes resulting from Public Act 300 of 2012

(3) Starting with the 2012 valuation year, (a) the normal cost is expressed as a percentage of non-PHF active member payroll, (b) the

Amortization Payment is expressed as a percentage of total MPSERS active member payroll (including PHF and non-PHF), and (c) the

required employer contribution is for the fiscal year beginning two years after the valuation date

(1) (1)(1) (2) (1)

Funded Percent

12

32.7%31.1%

39.5% 38.1%

0%

10%

20%

30%

40%

50%

2012 2013 2014 2015 2016 2016 2017 2017

Fun

ded

%

Valuation Year

(1) Reflects assumption changes (not including trend assumption)

(1) (1) (1)

Disclaimers

• This presentation is intended to be used in conjunction with the September 30, 2017 retiree health actuarial valuation report issued March 6, 2018. This presentation should not be relied on for any purpose other than the purpose described in the valuation report.

• This presentation shall not be construed to provide tax advice, legal advice or investment advice.

• The actuaries submitting this presentation (Mita Drazilov and Louise Gates) are Members of the American Academy of Actuaries and meet the Qualification Standards of the American Academy of Actuaries to render the actuarial opinions contained herein.

13