michelle korsmo ceo american land title association 202-261-2939 [email protected]

TRANSCRIPT

STAYING AHEAD OF POLITICIANS AND REGULATORS

PREPARING FOR THE NEW MARKETPLACE

Michelle KorsmoCEO

American Land Title Association202-261-2939

Compliance Consumer Protection

Market Drivers:

Economic, Regulatory, andPolitical Environments

Economic Environment

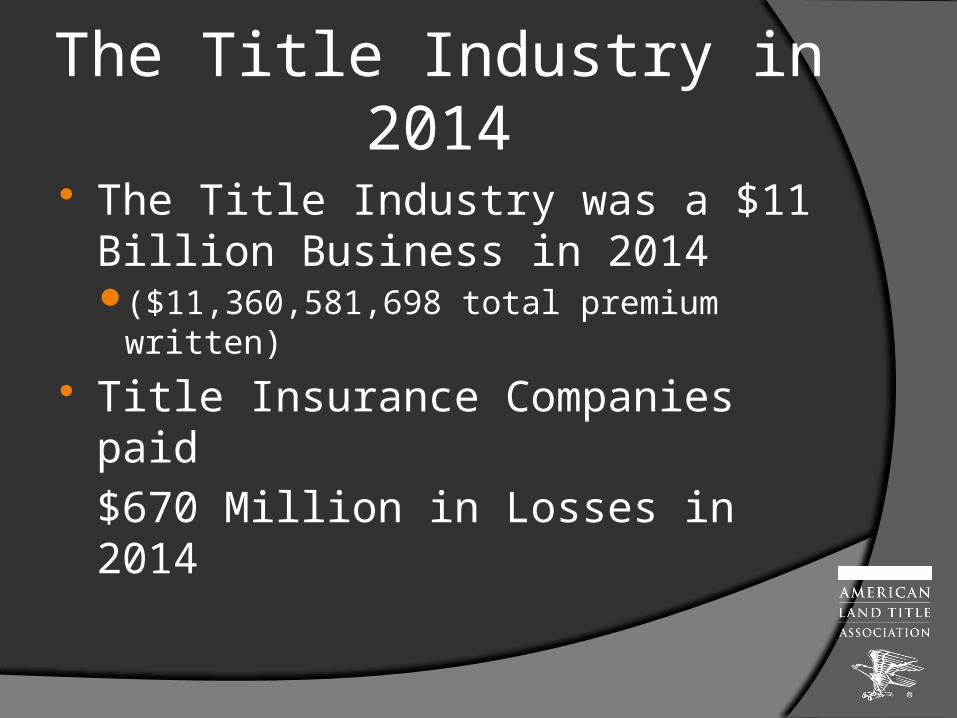

The Title Industry in 2014

The Title Industry was a $11 Billion Business in 2014 ($11,360,581,698 total premium written)

Title Insurance Companies paid

$670 Million in Losses in 2014

The Title Industry in 2014 2014 was a challenging year

Premiums Written down 10.9% from 2013Total Operating Income down 9.1%

However, Operating Expenses down 10.6% Loss and Loss Adjustment Expenses down 10.5%

Resulting in Net Operating Gain improving by almost 17.5%. Factor in a reduction of 25.4% in Net Investment

Gain 8.4% Increase in Net Income ($799.8 Million)

What Matters In the Economy:Am I Secure in My Job?

Consumer ConfidenceUp 2.5 points in March 2015

UnemploymentUnchanged at 5.5% in March 2015

Workforce Participation62.7% in March 2015

○ 37 year low for the past 11 months

(Pre-Housing Crash around 67%)

Policy Makers Will Not Help Until January

20th, 2017

(Maybe)

Americans Still Care About Homeownership

ALTA and our Coalition Partners are Spreading that Message and Using Our

Influence to Affect ChangeMortgage Bankers AssociationNational Association of RealtorsAmerican Bankers AssociationCommercial Bankers AssociationIndependent Community Bankers AssociationAmerican Bar AssociationFinancial Services RoundtableHousing Policy CouncilU.S. Chamber of CommerceNational Association of Insurance Commissioners

Regulatory Environment

Regulatory Forces Federal Regulators Remind Lenders of Their Liability

Office of Comptroller of Currency (OCC): Bulletin on third-party relationships and risk management principles – 2001

Federal Deposit Insurance Corp (FDIC): third-party risk awareness – 2006 FDIC: managing third-party risk guidance – 2008 OCC: consent orders and bank supervision – 2011 49 State Attorneys General: national mortgage settlement – February 2012 CFPB: Service Provider Bulletin - April 2012 FDIC: compliance manual – December 2012 OCC: risk management guidance update – 2013 Federal Reserve Board: letter on managing outsourcing risk – December 2013

CFPB Enforcement Actions American Express - $85 million Discover - $200 million Capital One - $210 million

Lender Concerns

Financial Enforceme

nt Reputation

al

The Title Industry Responds

Title Insurance and Settlement Company

Best Practices1. Comply with All State and Local Licensing 2. Procedures and Controls Regarding Escrow Trust

Accounts – Reconciliation3. Physical and Network Security—Protecting

Confidential Customer Information and Trust Accounts4. Recording and Pricing Procedures5. Title Policy Delivery, Premium Reporting and

Remittance6. Errors and Omissions Insurance / Fidelity Coverage7. Dealing with Consumer Complaints

www.alta.org/bestpractices

What’s Next on Best Practices

Lender Support is Growing Wells Fargo letter to settlement agent network

“Wells Fargo supports ALTA's Best Practices, and considers them to be guidelines for sound business practices that should ideally already be in place for businesses providing title and closing services for our customers.”

Sun Trust Bank Bancorp South …more to come this summer

How to Show Best Practice Compliance is Taking Shape AICPA Guidance on CPA Reporting ALTA Compliance Management Program for “Self-Certification”

Why You Should Implement Now

The CFPB

Established as an Enforcement Agency

In 2010 Dodd-Frank Act

and Opened in July 2011

First Regulatory Body Focused on the

Consumer

Protecting the Consumer

Takes Center Stage

CFPB Complaint ProcessComplaint Portal on www.consumerfinance.gov Homepage

CFPB Director Cordray to U.S. Conference of Mayors – January 22, 2014

“Complaints are not only opportunities for us to help specific people; they also make a difference by informing our work and helping us identify and prioritize problems. We know that if we hear about a particular problem from fifty consumers, it likely looms larger than if we hear about it from two. We know that if we begin to see a disturbing trend, we should consider allocating some of our limited resources to combat that particular problem.”

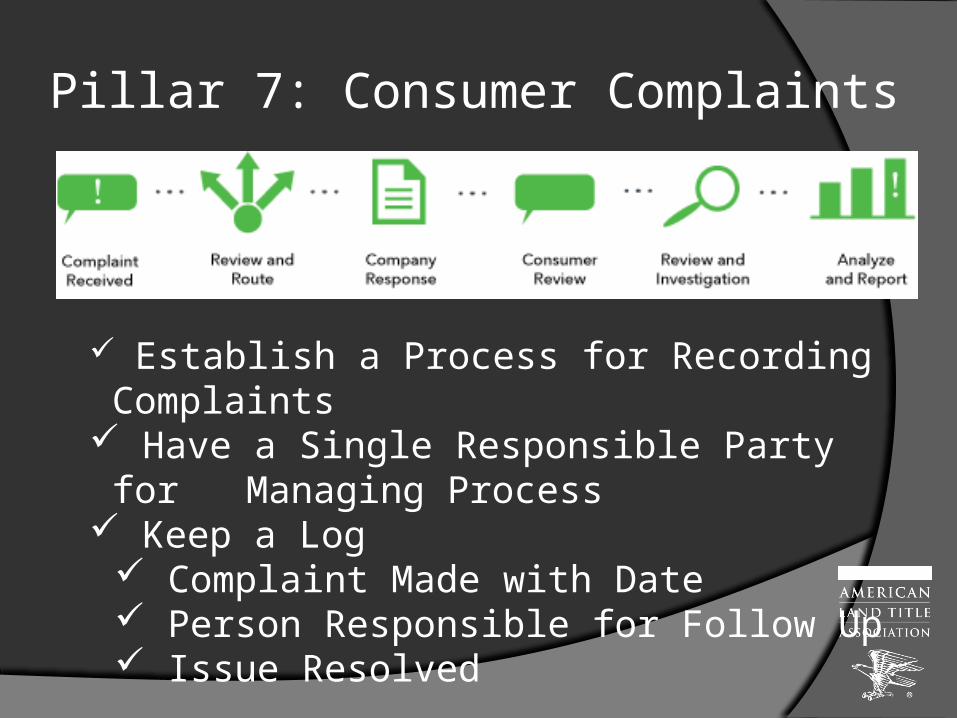

Pillar 7: Consumer Complaints

Establish a Process for Recording Complaints Have a Single Responsible Party for

Managing Process Keep a Log Complaint Made with Date Person Responsible for Follow Up Issue Resolved

TILA-RESPA Integrated Mortgage Disclosures-TRID

Also Brought to You by the Dodd-Frank Act

KNOWN KNOWNSKNOWN

UNKNOWNSUNKNOWN

UNKNOWNS

Known Knowns

The New Integrated Mortgage Disclosures will take affect on August 1st, 2015

These are not just new forms; this is a significant change to the business process to finance real estate

Known Unknows Will we be ready? Will our business partners

be ready? Will the software and automation portals?

How will we disagree on interpretation of Mortgage Disclosure Rule?

Enforcement fear is paralyzing for creditors. How does that affect our business and the process?

Are the Closing Disclosure forms going to accurately reflect our local practice and customs? e.g. seller paid jurisdictions

Unknown Unknowns What is the market going to look like?

Leading up to August 1st

August 1st through the balance of 2015 How will our industry change? grow?

utilize technology? How will we be valuable partners in the

process financing and conducting real estate settlement?

Your Market is Changing

Biggest Competitor for Big Banks?

----

Community Banks

THE ONLY ANSWER IS TO BE

PREPARED

TRID Prepare, Ask Questions, Train

Have you set expectations for all involved (consumers, lenders, title, real estate agents)?

How will lenders get title rates before the LE is delivered? Owner’s Title Insurance is listed as “Optional” on the LE;

what are you doing to get to consumers before they come to closing?

Who (lender/settlement agent) will prepare the CD? How will information on the CD be exchanged? How are you demonstrating evidence of compliance? How will simultaneous issue title rates be disclosed? Are your Closers trained on what to say about the value of

title insurance? Are your Closers trained on what to say to various versions of

the CD? How are you providing lenders actuals for a final CD?

Our Biggest TRID Challenges

TILA Liability Rest with Creditor Includes Private Right of Action

Inaccurate Disclosure of Title Policy Fees We Can Figure Out How to Handle the Calculation Will the Consumer Understand? Do You Have a Plan to Get to the Consumer in

Time? ALTA Created a Model “ALTA Settlement Statement” We are preparing our case for a post-

implementation change

Owner’s Title Insurance is Optional

ALTA Universal IDConsumer Message Campaign

Two Important ALTA Initiatives

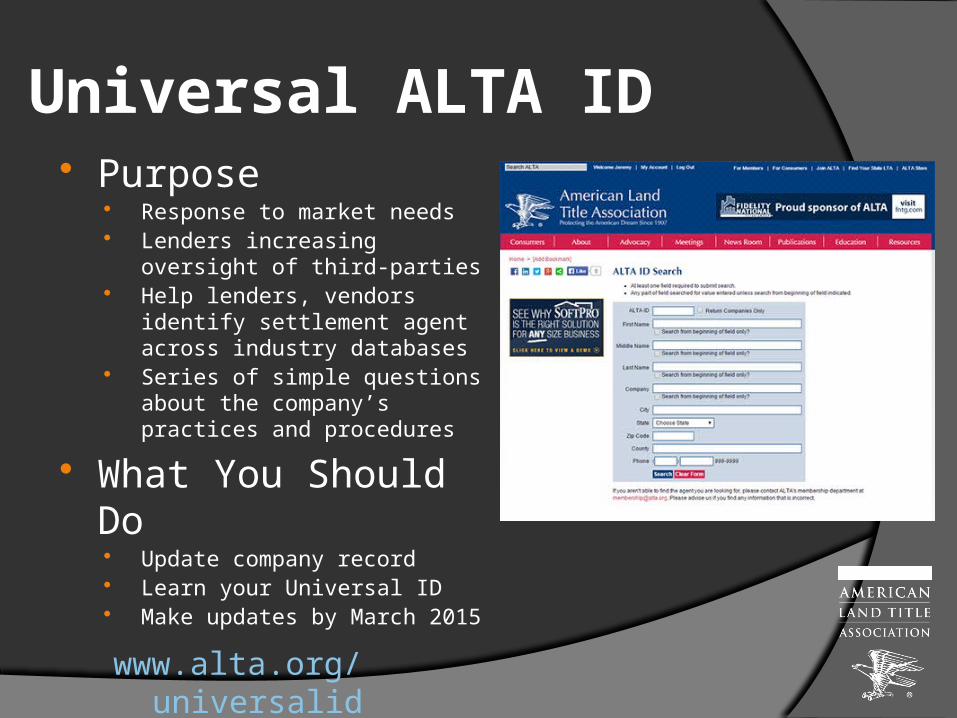

Universal ALTA ID Purpose

Response to market needs Lenders increasing oversight of

third-parties Help lenders, vendors identify

settlement agent across industry databases

Series of simple questions about the company’s practices and procedures

What You Should Do Update company record Learn your Universal ID Make updates by March 2015

www.alta.org/universalid

Consumer Message Campaign

Critical to educate consumers about title insurance EARLY

EARLY education has quantifiable impact

Use examples people believe might actually happen

Homebuyers want info about title insurance EARLY in the process

Key messages include: “protects your financial investment for as long as you own your home” and “one-time fee”

Political Environment

The Tenor of the Campaign Matters

…especially to business professionals

Priorities Congressional oversight of the

CFPB’s integrated mortgage disclosures

Small business advisory board Advisory opinion process Clear guidance from Reform

bulletins, press releases & enforcement

Tax Reform GSE Reform FHA Rules NAIC – Data Calls

Priorities Managing the Conversation

Around Points and Fees Legislation“…70 cents on every dollar is pure commission for the title agents.” – Senator Warren, April 2015

“Title insurance is already an uncompetitive market rife with reverse competition where the seller decides what the buyer purchases….Consumers have little or no influence over the price of title insurance but have not choice to purchase it….state law alone does not offer adequate protection.” – Congressman Ellison, April 2015

New Legislation from Congressman Ellison

Your Participation Counts

Title Insurance Political Action Committee (TIPAC)

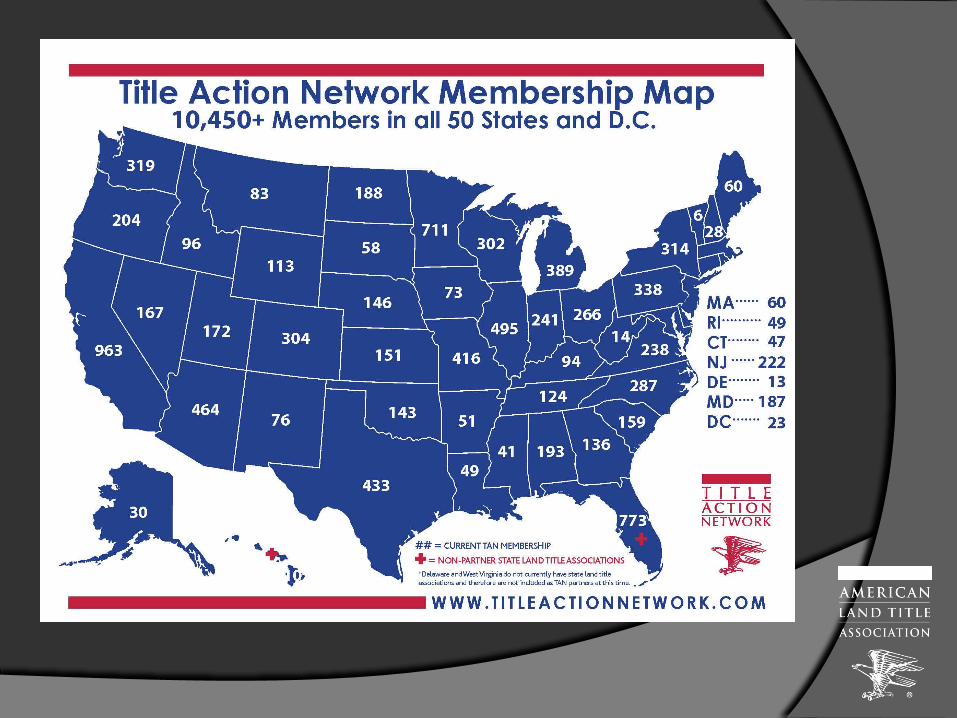

Title Action Network Join at www.titleactionnetwork.com

National Title Professional

ALTA Congressional Liaisons

Protecting the Consumer is about Compliance

Compliance is the Market Driver

Twitter twitter.com/altaonline

Facebook facebook.com/altaonline

LinkedIn linkedin.com search for the group American Land Title Association

Pinterest pinterest.com/altaonline

YouTube youtube.com/altavideos