mgt 326 ch 8:investment decision rules (bdh2e) 1 project decision making learning objectives: ...

TRANSCRIPT

MGT 326 Ch 8:Investment Decision Rules (bdh2e)

1

Project Decision Making

Learning Objectives:

Explain the Cost-Benefit Analysis ConceptCompute the NPV of a ProjectConduct NPV Analysis of Projects With Unequal LengthsCompute the NPV of a Project Using Risk Adjusted Discount RateCompute the IRR of a ProjectCompute the Payback Period of a ProjectCompute the Discounted Payback Period of a ProjectCompute the MIRR of a ProjectUse the Above Methods to Make a Project Investment DecisionUnderstand the Limitations of the Above MethodsInterpret NPV ProfilesExplain Why WACC is Used as the Discount Rate For NPV Calculations

MGT 326 Ch 8:Investment Decision Rules (bdh2e)

2

Project Decision Making

The process of planning and evaluating expenditures of capital for assets whose resulting cash flows are expected to extend beyond one yearTheis decision process is also called “Capital Budgeting”Used to decide which projects to adoptInvolves Long-term / Strategic Decisions

Project duration of several years Errors in forecasting requirements have long lasting effects

Projects in question typically involves large capital expenditures The larger the firm, the larger the expenditures

Typically involves the purchase of fixed assets (i.e. plant & equipment) that will produce some sort of future cash flow stream

However, the capital budgeting process can be applied to any outflow of cash that produces a series of future cash flows

transportation, automation/MIS, R&D, etc.costs of market expansion efforts, new product lines, etc.outsourcingmarketing

Used to evaluate a single project or choose between 2 or more projects

Importance of Capital Budgeting:Since the results of capital budgeting decisions last many years…

the firm loses some financial flexibility they are strategic decisions

Erroneous forecasts of requirements can have serious consequences if too much is invested the firm will incur unnecessarily high depreciation and other expenses if not enough is invested:

purchased equipment may not be modern enough to enable the firm to be competitiveif capacity is in adequate, the firm may lose market share

Timing is important; the firm must acquire and bring into operation assets when needed; must be pro-active

MGT 326 Ch 8:Investment Decision Rules (bdh2e)

3

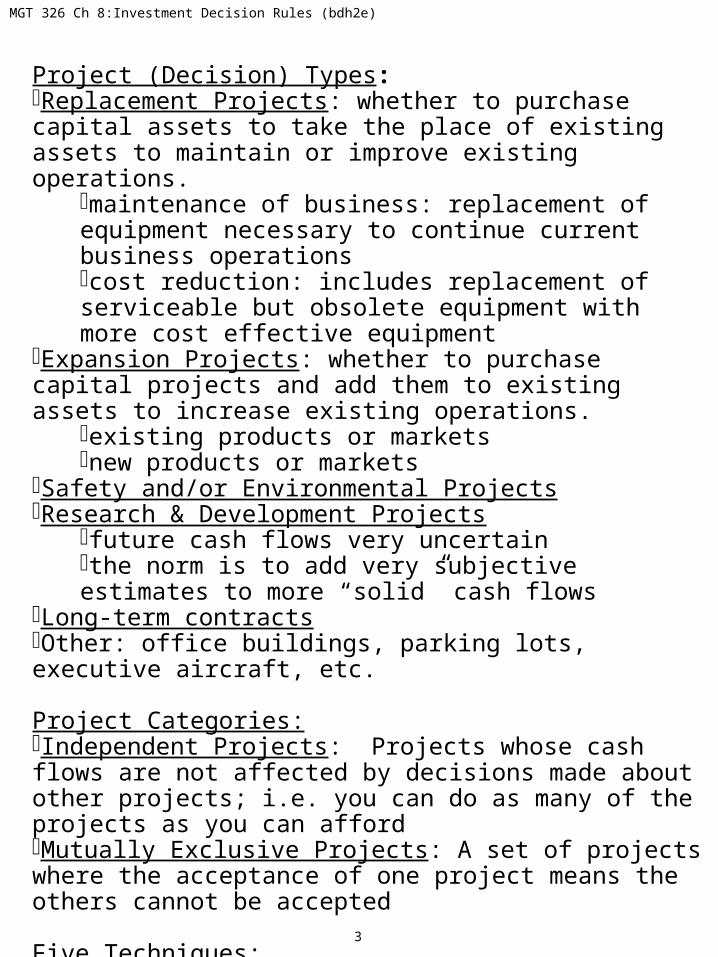

Project (Decision) Types:Replacement Projects: whether to purchase capital assets to take the place of existing assets to maintain or improve existing operations.

maintenance of business: replacement of equipment necessary to continue current business operationscost reduction: includes replacement of serviceable but obsolete equipment with more cost effective equipment

Expansion Projects: whether to purchase capital projects and add them to existing assets to increase existing operations.

existing products or marketsnew products or markets

Safety and/or Environmental ProjectsResearch & Development Projects

future cash flows very uncertainthe norm is to add very subjective estimates to more “solid” cash flows

Long-term contractsOther: office buildings, parking lots, executive aircraft, etc.

Project Categories:Independent Projects: Projects whose cash flows are not affected by decisions made about other projects; i.e. you can do as many of the projects as you can affordMutually Exclusive Projects: A set of projects where the acceptance of one project means the others cannot be accepted

Five Techniques: Payback Period Discounted Payback Period Net Present Value (NPV) Internal Rate of Return (IRR) Modified Internal Rate of Return (MIRR)

MGT 326 Ch 8:Investment Decision Rules (bdh2e)

4

Net Present Value (NPV) Method

Definition: The sum of all project cash flows is the Net Present ValueThe value of any financial asset is determined by discounting all future cash flows to the present (i.e. find the PV @ t = 0) and adding them upProcess: Discount all future expected cash flows to time zero (t = 0) then add them to any initial investmentsRationale:

An NPV > 0 means you make money; the profit is greater than the costAn NPV < 0 means you lose money; the cost is greater than the profitAn NPV of 0 means you break evenAccept only projects with NPV > 0When comparing mutually exclusive projects, the one with the highest NPV is the one with the highest potential benefit to the firm. If all the cash flows of mutually exclusive projects are negative, they will have negative NPVs. Still, you choose the project with the hichest NPV

Formula: t

tn

0t r1

CFNPV

The discount rate r for computing NPV is usually the Weighted Average Cost of Capital (WACC) (from Ch 12)The discount rate can be the Opportunity Cost of Capital (from Ch 5)

MGT 326 Ch 8:Investment Decision Rules (bdh2e)

5

Net Present Value (NPV) Method (continued)

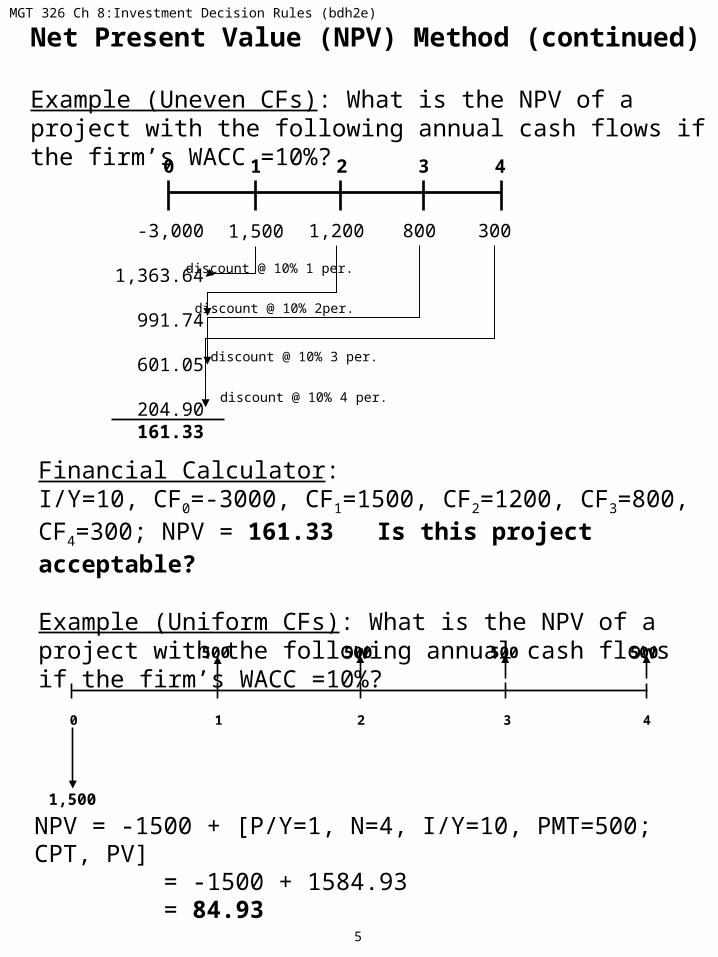

Example (Uneven CFs): What is the NPV of a project with the following annual cash flows if the firm’s WACC =10%?

1,500 8001,200-3,000

1,363.64

991.74

601.05

204.90161.33

300

0 1 2 3 4

Financial Calculator:I/Y=10, CF0=-3000, CF1=1500, CF2=1200, CF3=800, CF4=300; NPV = 161.33 Is this project acceptable?

Example (Uniform CFs): What is the NPV of a project with the following annual cash flows if the firm’s WACC =10%?

discount @ 10% 1 per.

discount @ 10% 2per.

discount @ 10% 3 per.

discount @ 10% 4 per.

0 1 2 3 4

500500 500

1,500

500

NPV = -1500 + [P/Y=1, N=4, I/Y=10, PMT=500; CPT, PV] = -1500 + 1584.93 = 84.93

CE 350 Project Decison Making

6

Net Present Value (NPV) Method (continued)

Example: What is the NPV of a project with the following monthly cash flows if the firm’s WACC =6.0000%?

0 4 5 61 2 3

$350 $390 $480 $660 $820 $940-$2,000x $1,000

CE 350 Project Decison Making

7

Net Present Value (NPV) Method (continued)

Example: What is the NPV of a project with the following quarterly cash flows if the firm’s WACC = 8.0000%?

$ x $1,000

1 2 34 35 36

$500

0

$11,000.00

CE 350 Project Decison Making

8

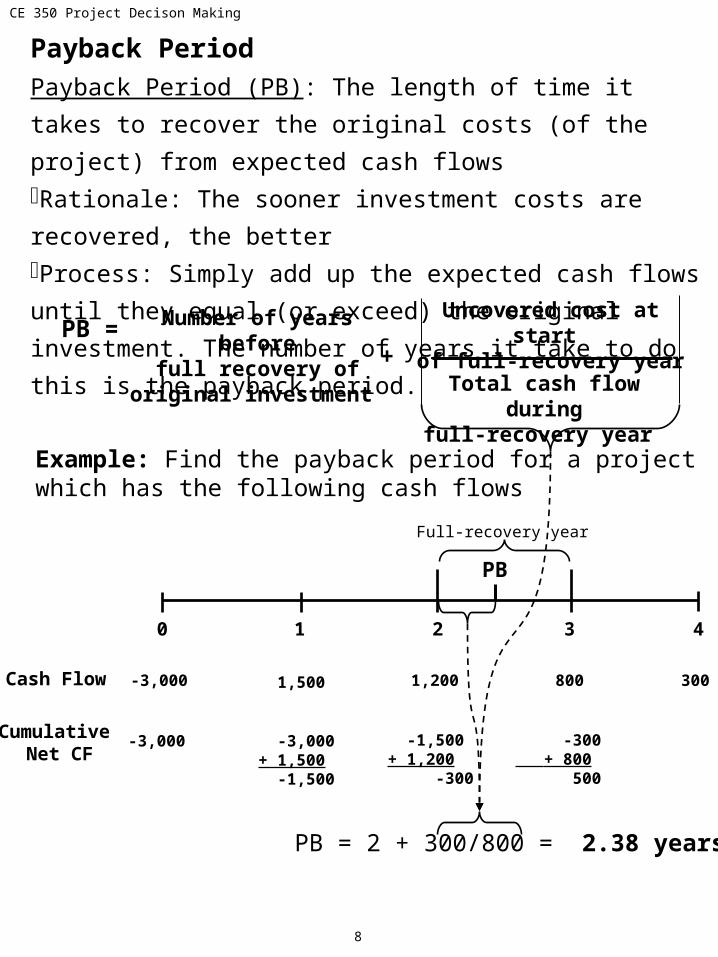

Payback Period

Payback Period (PB): The length of time it takes to recover the

original costs (of the project) from expected cash flows

Rationale: The sooner investment costs are recovered, the better

Process: Simply add up the expected cash flows until they equal (or

exceed) the original investment. The number of years it take to do this

is the payback period.

PB = Number of years beforefull recovery of

original investment

Uncovered cost at start of full-recovery year

Total cash flow duringfull-recovery year

+

Cash Flow

Cumulative Net CF

1,500 8001,200-3,000 300

PB

0 1 2 3 4

Example: Find the payback period for a project which has the following cash flows

PB = 2 + 300/800 = 2.38 years

Full-recovery year

-3,000 -3,000+ 1,500 -1,500

-1,500+ 1,200 -300

-300 + 800 500

MGT 326 Ch 8:Investment Decision Rules (bdh2e)

9

Payback Period (continued)

Payback Period Decision Rule:When evaluating a single project, the project is acceptable if the Payback Period is less than any pre-specified time limitWhen evaluating 2 or more mutually exclusive projects, the one with the shortest Payback Period is preferrable, assuming that it is less than any pre-specified time limit

Strengths & Weaknesses of the Payback Method:Strengths Provides an indication of a project’s liquidity risk (how long will invested capital be tied up)

Weaknesses Ignores the Time Value of Money Ignores the CFs occurring after the payback period

Example: Consider two projects who’s annual cash flows are shown below:

450

100100100100100100

0 2 3 41 5 6Project A

Project B

PB = 4.5 yrs

450

2009090909090

0 2 3 41 5 6

PB = 5 yrs

Project A has a shorter PB period but is it really the more preferable project? Compute NPV of each project (assume WACC = 8%):

NPVA =12.28

NPVB = 35.38

CE 350 Project Decison Making

10

Discounted Payback Period (not covered in your textbook)

Similar to Payback Period MethodExpected future cash flows are discounted by the project’s cost of capitalThus the discounted payback period is defined as the number of years required to recover the investment from discounted net cash flowsExample: A project has the following annual cash flows. Find the discounted payback period

10

8060

0 1 2 3

-100

r =10%

PVCFt=0 -100 9.09 49.59 60.11

Cum. NET Discounted Cash Flows

DiscountedPayback = 2 + 41.32/60.11 = 2.69 yrs

Strengths & Weaknesses of the Discounted Payback Method:Strengths

Provides an indication of a project’s liquidity risk Recognizes time value of money Recognizes WACC

Weaknesses Ignores the CFs occurring after the payback period

-100+ 9.09-90.91

-90.91+ 49.59 -41.32

-41.32 + 60.11 18.79

CE 350 Project Decison Making

11

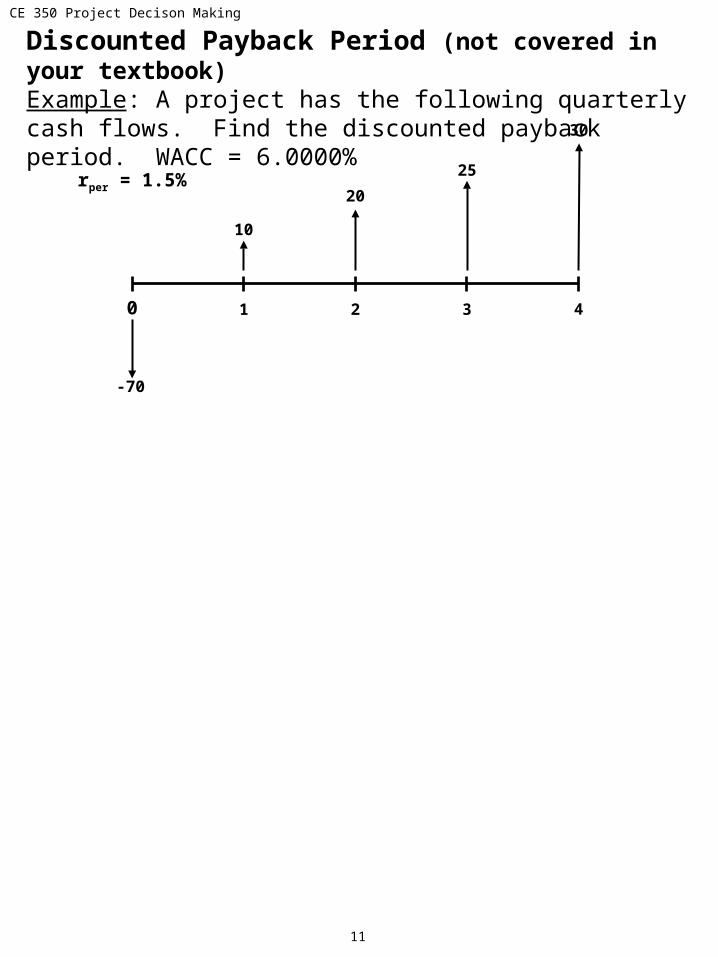

Discounted Payback Period (not covered in your textbook)Example: A project has the following quarterly cash flows. Find the discounted payback period. WACC = 6.0000%

10

30

25

-70

rper = 1.5%

0 1 2 3 4

20

MGT 326 Ch 8:Investment Decision Rules (bdh2e)

12

Internal Rate of ReturnDefinition:

The discount rate that forces the PV of a project’s expected cash flows to equal its initial costIt is also the discount rate that forces the project’s NPV to equal 0 (do some algebra; subtract the initial cost form both sides of the equation and you get an NPV equation)

The IRR is the ROR of the projectA project is internal to a firm; it is an internal investmentRationale: Projects that have an IRR greater than r (the opportunity cost) are acceptable investments

The project produces returns in excess of that which is required

1,500 8001,200-3,000 300

0 1 2 3 4

Example: What is the IRR of a project with the following cash flows?

3000 = 1,500 + 1,200 + 800 + 300 (1+IRR) (1+IRR)2 (1+IRR)3 (1+IRR)4

NPV = 0 = -3000 + 1,500 + 1,200 + 800 + 300(1+IRR) (1+IRR)2 (1+IRR)3 (1+IRR)4

Solve for IRR (the discount rate that satisfies (results in, fits) either of above equations

CF, 2nd CLR WORK (Clear cash flow worksheet)-3000, ENTER↓, 1500, ENTER↓, ↓, 1200, ENTER↓, ↓, 800, ENTER↓, ↓, 300, ENTERIRR, CPT: 13.1140%

MGT 326 Ch 8:Investment Decision Rules (bdh2e)

13

Internal Rate of Return (continued)

3000 = 1,500 + 1,200 + 800 + 300 (1+IRR) (1+IRR)2 (1+IRR)3 (1+IRR)4

IRR is similar in concept to the Yield to Maturity of a bond

If IRR = 13.114% then:$3000 = $1,326.10 + $937.88 + $552.77 + $183.25

Period PV0 @ 13.114%

1 1500 $1,326.10

2 1200 $937.88

3 800 $552.77

4 300 $183.25

$3,000.00

Future Expected Cash Flow

Sum of Discounted Cash Flow s:

If the initial cost of the project is $3,000 and it produces a 13.114% ROR, then the firm will break even (the initial investment is matched by the sum of the discounted future cash flows)

If each of the discounted CFs are compounded at IRR (13.114%) for the respected number of periods, it produces the project’s CF stream:

Period

1 $1,326.10 $1,5002 $937.88 $1,2003 $552.77 $8004 $183.25 $300

FV of CFs Compounded @ IRR (13.114%

PV0 of Cash Flows

1,500 8001,200-3,000 300

0 1 2 3 4

MGT 326 Ch 8:Investment Decision Rules (bdh2e)

14

Internal Rate of Return (continued)If a project’s IRR exceeds the WACC (or opportunity cost of capital), the firm makes moneyIf a project’s IRR is less than the WACC (or opportunity cost of capital) , the firm will lose moneyIf a project’s IRR equals the WACC (or opportunity cost of capital), the firm “breaks even” Thus the project’s required ROR is the firm’s WACC

When comparing two mutually exclusive projects, the one with the higher IRR is preferred

Some notes on using NPV and IRR methods1. Reinvestment Rate AssumptionWhich one of these methods (NPV or IRR) is a safer bet? (i.e. more reliable and predictable)The answer depends on the interest rate at which cash flows can be reinvested

the NPV method assumes that they can be reinvested at r, the IRR implies that they can be reinvested at a rate equal to a project’s IRRboth methods rely on expected (thus estimated) future cash flowshowever with NPV, we know what rate these CFs will be reinvested at; it’s the opportunity cost of capitalwe create the IRR by forcing the NPV of the expected cash flows to equal zerothus the IRR we come up may be much greater than the opportunity cost of capital, thus establishing an unrealistic reinvestment rate for project CFs

MGT 326 Ch 8:Investment Decision Rules (bdh2e)

15

Some notes on using NPV and IRR methods (continued)2. The IRR method is not suitable when a project has “unconventional” cash flowsA conventional CF has a large outflow of cash at the beginning of the life span and several inflows of cash throughout the rest of the projectAn unconventional CF has an initial negative CF, followed by a series of positive CFs which are interrupted by a negative CF.

This will produce 2 or more IRRs (one for each period in which the sign of the CF changes) (trust me on this; you don’t want to see the math)(you can use a calculator but the IRR will be meaningless)Which IRR will you use?

0 4 5 61 2 3

$50k

$370k

$89k$130k $145k

$170k

$94k

Unconventional Cash Flows:

What to do? Answer: Modify the cash flows so that there is only one negative cash flow then do IRR. This is the Modified IRR method.

0 4 5 61 2 3

$50k

$89k$130k $145k

$170k

$94k

WACC = 9.5000%

P/Y=1, N=1, I/Y=9.5, FV=50; CPT PV; PV = 45.66k

CF0=-370, C01=130, C02=43.34, C03=0, C04=145, C05=170, CO6=94; IRR =

13.4800%

$45.66k

$370k

= $89K - $45.66k

MGT 326 Ch 8:Investment Decision Rules (bdh2e)

16

Notes on NPV and IRR (continued)

Why use IRR?Answer: It suits those who want to directly express the benefits of a project as a rate of return (Corporate operation types selling a project to non-finance guys)It gives some indication of safety if future cash flows fall short of expectations:

WACC is only an estimate of the of a firm’s true cost of capitalWhat if WACC is too low of an estimate of a firm’s cost of capital? Projects with relatively high IRR have greater margins of safety the than projects whose IRRs barely exceed a firm’s WACC

Conclusions: When evaluating which of 2 or more mutually exclusive projects, NPV is preferred over IRR

Prof. Jim’s Recommendations: Always use NPV firstUse IRR and Discounted Payback Period as tie breakers

MGT 326 Ch 8:Investment Decision Rules (bdh2e)

17

NPV ProfilesLet’s examine two projects with differing cash flows

Project S

Project L

If we plot NPVs of each project against various values for r, we can see how the NPVs will change when r changes

600 300400 200

0 1 2 3 4

-1,000

5

100

200 400200 400

0 1 2 3 4

-1,000

5

600

Key Points:The crossover point is the r that produces equal NPVs. At r greater than 9.55%, Proj S has higher NPV. At r less than 9.55%, Proj L has higher NPV. Note: IRR suggests Proj S is always superiorIf the profiles don’t cross, one project dominates the other

-$400

-$200

$0

$200

$400

$600

$800

$1,000

0% 5% 10% 15% 20% 25% 30%

Crossover Point: NPVS = NPVL @ r = 9.55%

IRRL = 18.9%

IRRS = 25.7%

NP

V

Discount Rate (r)

PROJ L

PROJ S

MGT 326 Ch 8:Investment Decision Rules (bdh2e)

18

NPV Profiles (continued)

Two reasons why profiles cross:Size (scale) differences. Smaller projects demand less funds at t = 0 thus leave more funds available for other investments. The higher the opportunity cost, the more valuable these funds are, so high r favors small projects.Cash Flow Timing differences. Project with faster payback provides more CF in early years for reinvestment.

Use both methods (NPV & IRR) to determine sensitivity to rFind NPV and IRR of both projects. Construct NPV profiles and find the crossover pointAccept the project that has the highest NPV with respect to r

MGT 326 Ch 8:Investment Decision Rules (bdh2e)

19

Comparison of Projects with Unequal Lives

Example: A company is planning to modernize its production facilities and is considering either a conveyor system (Proj C) or some forklift trucks (Proj F)

7,000 12,00013,000

0 1 2 3-20,000

0 1 2 3 4 5 6-40,000

8,000 13,00014,000 12,000 10,00011,000

Proj F

Proj Cr =11.5%

NPVC = $7,165, IRR = 17.5%

NPVF = $5,391, IRR = 25.2%

The NPV results hide the fact that Proj F affords the opportunity to make a similar investment at t =3, thus producing another 3 years of cash flowsTo compensate for this we must use the replacement chain or common life approach

this simply means extending the cash flows of the shorter project out to the life of the longer project and then computing NPV of the shorter project

7,000 12,00013,000

-20,000

Proj FReplacementChain

NPVF = $9,281

0 1 2 3 4 5 6

7,000 12,00013,000

-20,000

This is only an issue for mutually exclusive projectsIgnore the Equivalent Annual Annuity approach as discussed in your text book

r =11.5%

CE 350 Project Decison Making

20

Comparison of Projects with Unequal Lives (continued)

Year 0 1 2 3 4 5 6Project A CFs -$60.00 $18.00 $18.00 $18.00 $18.00 $18.00 $18.00

Project B CFs -$45.00 $30.00 $30.00

Example: A firm is considering two mutually exclusive projects that have the annual cash flows shown below. Based on NPV analysis, which project should be accepted? The required rate of return is 7.0000%

21

Risk-Adjusted Discount Rate (not in your text book)Definition: The discount rate (required rate of return) that applies to a particular risky projectUsed to determine a project’s NPVApplies the concept of risk aversion to project decisionsVery subjective; there is no reliable technique for determining appropriate risk premiums for projects

“Benchmark”; use what other firms (in same industry) useShould be consistently applied throughout the firm

ProcessDetermine the overall required rate of return for the average project(i.e. opportunity cost of capital)Classify all projects into three categories: low risk, moderate risk and high riskDetermine appropriate risk adjustmentsmodify required rate of return appropriately

Results: riskier projects will have their NPVs artificially lowered because (according to the concept of risk aversion) riskier assets should have lower value compared to less risky assets

Example: A firm is considering two mutually exclusive projects. Project A is a low risk project, Project B is moderately risky while Project C is considered to have a high degree of risk. The firm’s rrequired is 7.30%. The firm uses the risk-adjusted discount rate method to account for project risk. Projects posing minimal risk are evaluated using rrequired for the discount rate. 1.25% is added for moderately risky projects and 2.50% is added for significantly risky projects. What discount rates should be used for NPV calculations of Projects A, B and C? rProject A = rrequired = 7.30% rProject B = rrequired + 1.25% = 7.30% + 1.25% = 8.55% rProject C = rrequired + 2.50% = 7.30% + 2.50% = 9.80%

MGT 326 Ch 8:Investment Decision Rules (bdh2e)