mexico’s energy regulatory commission · electricity generation from clean energy by 2024. •...

TRANSCRIPT

www.gob.mx/cre @CRE_Mexico

Meney de la Peza Regulation Unit

Mexico’s Energy Regulatory Commission

NAESB Board of Directors Dinner Houston, Texas December, 2016

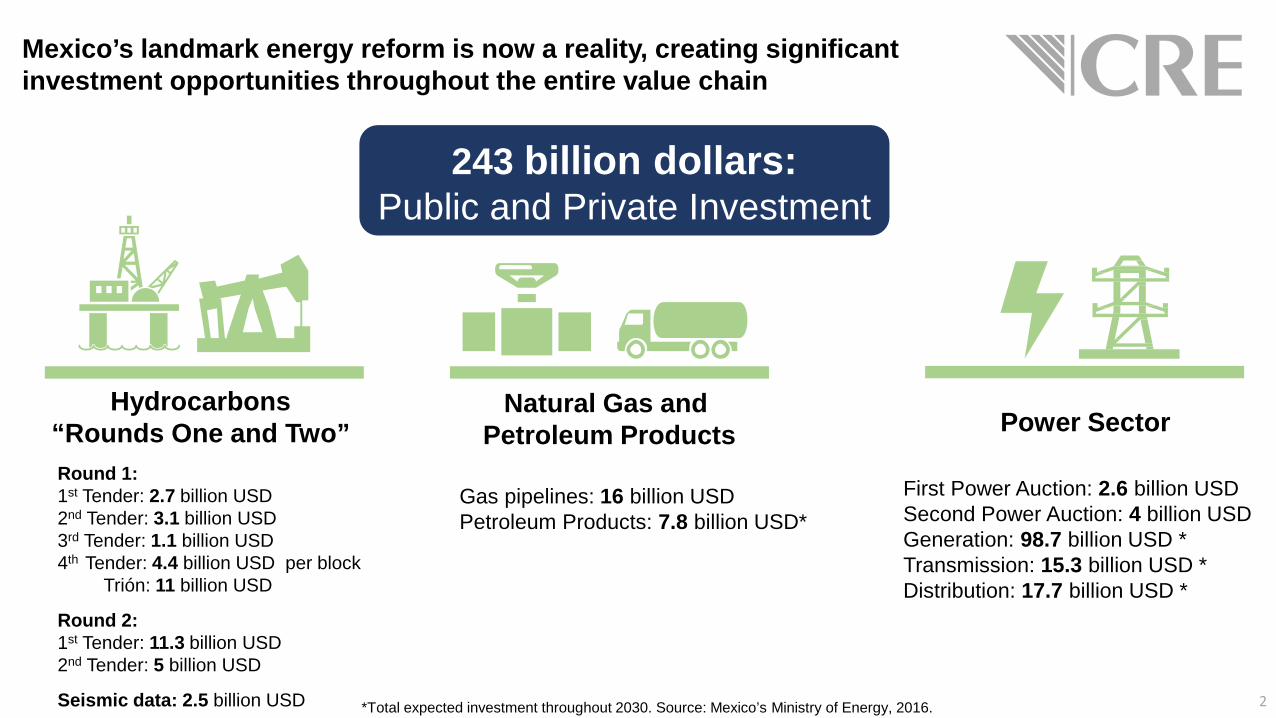

First Power Auction: 2.6 billion USD Second Power Auction: 4 billion USD Generation: 98.7 billion USD * Transmission: 15.3 billion USD * Distribution: 17.7 billion USD *

Mexico’s landmark energy reform is now a reality, creating significant investment opportunities throughout the entire value chain

Round 1: 1st Tender: 2.7 billion USD 2nd Tender: 3.1 billion USD 3rd Tender: 1.1 billion USD 4th Tender: 4.4 billion USD per block Trión: 11 billion USD

Round 2: 1st Tender: 11.3 billion USD 2nd Tender: 5 billion USD

Seismic data: 2.5 billion USD

Gas pipelines: 16 billion USD Petroleum Products: 7.8 billion USD*

Hydrocarbons “Rounds One and Two”

Natural Gas and Petroleum Products Power Sector

*Total expected investment throughout 2030. Source: Mexico’s Ministry of Energy, 2016.

243 billion dollars: Public and Private Investment

2

2012 2016

El Encino

Aguascalientes

Zacatecas

Puerto Libertad

Los Ramones

Guaymas

Huexca Ciudad Pemex

Nuevo Pemex

Nativitas

2019

Cempoala

Acapulco

Lázaro Cárdenas

El Oro Topolobampo

Mazatlán

Apaseo el Alto

San Luis

Potosí

La Laguna

Tuxpan Tula

Samalayuca

Jáltipan

Salina Cruz

Guadalajara

Durango

Source: Five Year Gas Pipeline Plan 2015-2109, http://www.gob.mx/sener/acciones-y-programas/plan-quinquenal-de-gas-natural-2015-2019

“El Cabrito” Compression Station, included in the Plan

Regasification Terminal

Operating Gas Pipeline

Concluded Gas Pipelines (2013/2014/2015)

Gas Pipelines under Construction (2015/2016)

Strategic Gas Pipelines included in the Five Year Plan

Escobedo

Altamira

Naranjos

Tapachula Centroamérica

Social Gas Pipelines, included in the Plan

Interconnections

Naco Cd. Juárez

KM Monterrey Reynosa Argüelles Río Bravo Piedras Negras

Camargo

Sur de Texas

Sásabe

Colombia

Los Algodones Los Algodones bis

San Isidro

Ojinaga

Mexicali

Nogales

Agua Prieta Gloria a Dios

Cd. Acuña

Mexico’s Gas Pipeline Network will expand considerably from 2012 to 2019

New transportation infrastructure by 2019, according to the Five Year Gas Pipeline Plan: • 10 new strategic gas pipelines • 2 social coverage gas pipelines • 7 interconnection points with the US • 1 interconnection with Central America

16 billion dollars

Total expected investment 1

3

2

4

Pipelines*

Kinder Morgan (operating) KM Gasoductos de Chihuahua (operating) Sempra Energy Transportadora de Gas Natural de Baja California (operating) Sempra Energy Gasoducto Rosarito (operating) Sempra Energy Gasoductos del Noreste (operating) Sempra Energy Gasoducto de Aguaprieta (operating) Sempra Energy Gasoductos de Tamaulipas (operating) Sempra Energy Gasoducto de Aguaprieta- Sonora (operating) Sempra Energy TAG Pipelines Norte (operating) Sempra Energy/Pemex Arguelles Pipeline (operating) Energy Transfer Partner Gasoducto de Aguaprieta -San Isidro- (operating) Sempra Energy Gasoducto de Aguaprieta –Ojinaga- (operating) Sempra Energy Midstream de México (operating) Howard Midstream Energy Partners

2 1

3

4

5

6

7

8

9

10

11

12

13

5

6

7

8

9

11

12

13

10

*Participation of American capital in Mexico’s Gas Pipeline Network 3

Hyd

roca

rbon

s El

ectr

icity

Exploration / Extraction

Refining / Processing

Transportation Storage Distribution Retailing & Commercialization Transportation

Generation System and Market

Operation (ISO)

Transmission Distribution

Retailing & Commercialization

System Operator

The Energy Regulatory Commission (CRE) has effectively become the regulator of the mid and downstream segments of the oil and gas value chain, as well as the entire electricity supply chain

4

1. Enhance natural gas availability throughout the country

2. Separate pipeline

transportation from natural gas

commercialization

3. Establish open access and pipeline capacity

reserve conditions

4. Issue asymmetric

regulation for participants with

high market concentration

5. Publish volumes, prices,

discounts, locations and trade information for

retailing and commercialization of

natural gas

The energy reform laid the foundations for an open and competitive natural gas market, contributing to:

5

6

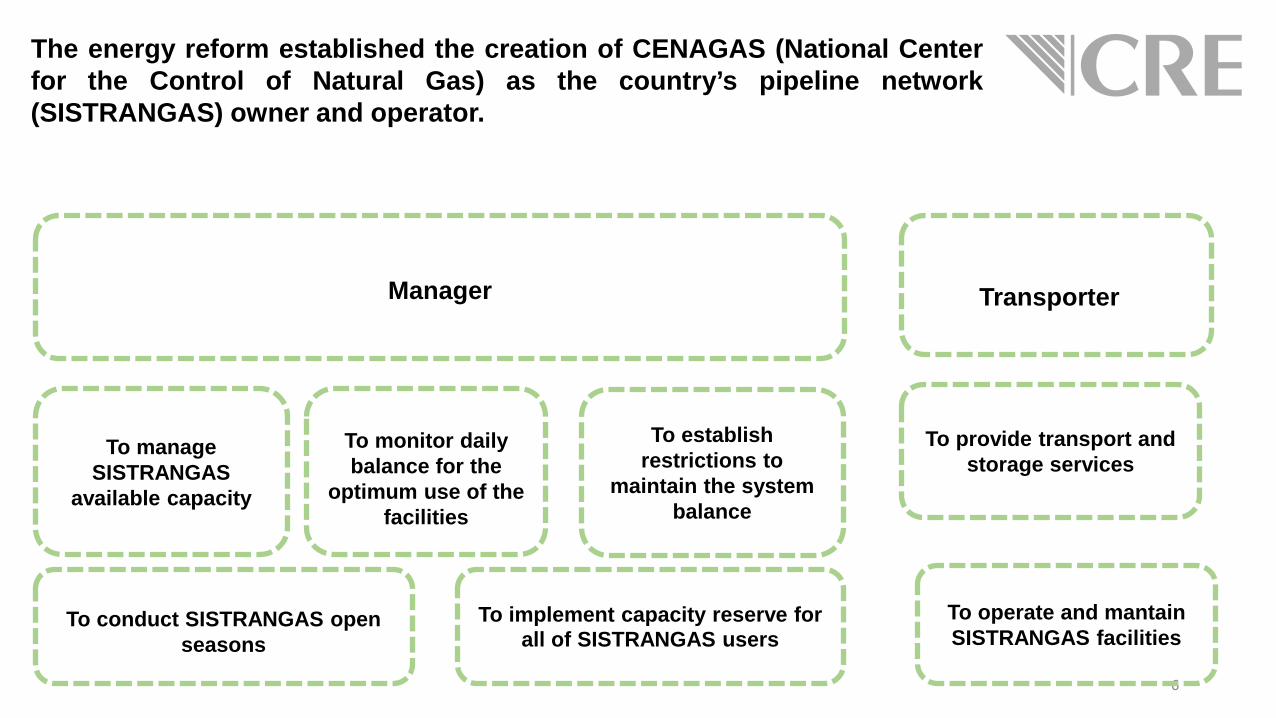

To manage SISTRANGAS

available capacity

To implement capacity reserve for all of SISTRANGAS users

Manager

Transporter

To conduct SISTRANGAS open

seasons

To monitor daily balance for the

optimum use of the facilities

To provide transport and storage services

To establish restrictions to

maintain the system balance

The energy reform established the creation of CENAGAS (National Center for the Control of Natural Gas) as the country’s pipeline network (SISTRANGAS) owner and operator.

To operate and mantain SISTRANGAS facilities

Capacity reserve for State Productive

Enterprises (EPE, for its Spanish acronym)

CRE determined the maximum capacity that

Pemex and CFE may reserve in the pipeline

network for their transformation and

generation activities, respectively

Open Season of pipeline network

CRE approved CENAGAS’s open

season proposal, which is currently being

implemented

Import Pipelines CRE has worked

coordinately with SENER and CENAGAS to design

a mechanism that enables CENAGAS to

manage the interconnection

pipelines currently contracted by Pemex

and CFE

Flexibilization of First-Hand Sales

Prices CRE will determine the regions where price will be set by the market as of 2017, as well as the

applicable price methodology for the

areas where the maximum price will be

maintained

CAPACITY RESERVE COMPETITION IN COMMERCIALIZATION/MARKETING

2016 2017 4T

Gas Release Program

CRE is designing the procedure to implement

the release by Pemex of up to 70% of its natural gas commercialization

volume

4T 1T 2T 3T 3T

7

In July 2016, the Energy Ministry (SENER) announced a comprehensive public policy for the implementation of a natural gas competitive market. In line with this public policy, CRE has had an active role in the following short and medium term actions:

SISTRANGAS open season has the following characteristics:

8

• Open season guarantees open access and non-discriminatory principles for all users. • All users, including state productive enterprises, will compete under equal circumstances.

• Open season gives preference to current holders of capacity rights.

• The open season procedure will be carried out through an auction mechanism.

• Allocation criterion guarantees all users pay the same price.

• The terms of the service agreements shall be for one year (to allow the market to adjust). • The agreements may be renewed after the first year if capacity is actually used by its holders.

CENAGAS will manage the interconnection pipelines currently contracted by Pemex and CFE

9

• CENAGAS will manage capacity through an electronic board.

• CFE and PEMEX must publish their available capacity in the electronic board.

• CENAGAS will auction available capacity.

• Capacity will be assigned to participants offering the highest price.

• Participants must have a capacity reserve in SISTRANGAS.

• CENAGAS will publish

results in the electronic board.

• CFE and PEMEX will maintain their contractual relationship with the US transporter.

10

Pemex must:

As a result of asymmetric regulation, Pemex will have to release to the market at least 70% of its natural gas sales contracts in the following two years

All traders will be able to:

Offer users at least the same conditions as those provided by

Pemex

Seek and negotiate with

users

Reserve capacity for themselves in the

open season and use it to provide the service to their

customers

Publish its commercialization

conditions and keep them for the duration

of the program

Have a standard commercialization

contract

Establish a clause of non-onerous

exit in all contracts

All users will be able to:

Accept offers from private traders and sign contracts with any of them

from the start of the program

Reserve capacity for themselves in the open season

and transfer it temporarily to any trader in order to receive

the service

Self-supply

Continue with Pemex (non-default option)

11

First Hand Sales Prices are currently regulated by CRE throughout the country. The methodology seeks to reflect the opportunity cost of gas in the international market.

Sur de Texas (ST)

Henry Hub

Houston Ship Channel

Reynosa

Punto de Arbitraje Ciudad Pemex

ST ≈ (HH,HSC)

+ Transporte ST Reynosa

(TF)

±Netback Reynosa Arbitraje

Arbitraje Cd. Pemex

. PRICE IN REYNOSA =

PRICE IN CIUDAD PEMEX =

Transportation cost in US to

Mexico Border Price in SouthTexas

Price in Reynosa Adjusted transport cost

Natural gas traders (companies with CRE permit) will report every day transactions to CRE through the Natural Gas Daily Trading System. Anyone will be able to check daily the average price of gas registered in 14 regions, through an interactive map.

It plans to start operating early 2017

12

• 2015-2019 Natural Gas Prospective published by SENER projects natural gas consumption for 2029 to be

10,390.3 bcf and national production to be 6,451.9 bcf at the most, which implies imports will represent more than one

third of national consumption and around three times the current imports from the US.

• SISTRANGAS expansion plan will allow the country’s natural gas pipeline network to accommodate higher levels of

natural gas imports from the US. The plan proposed 12 pipeline additions and a new compression station, increasing

the existing network capacity and adding more than 3,200 miles of new pipeline through Mexico.

• Contracts have been awarded for 7 of the 12 pipeline projects. The largest and most expensive of the awarded projects

is the Sur de Texas-Tuxpan pipeline, which aims to supply the Mexican states of Tamaulipas and Veracruz with natural

gas from southern Texas via an underwater route through the Gulf of Mexico. The pipeline will extend nearly 500 miles

and provide a total transport capacity of 2.6 Bcf/d. The remaining projects are under review and will move forward if

market conditions support their economic viability.

13

Mexican imports of US natural gas are projected to continue growing in future years

• The country is meeting its growing electricity demand with generation from new

natural gas-fired plants, using mainly natural gas imported by pipeline from the

US.

• The Energy Transition Law, approved in December 2015, sets a target of 35% of

electricity generation from clean energy by 2024.

• The International Energy Agency’s special report “Mexico Energy Outlook”

projected that both gas and renewables increase their share in electricity

generation in the following decades.

Growth in Mexico’s domestic electricity consumption has been a primary driver of the country’s natural gas usage, and will continue to be so

14

15

• Harmonization of standards supporting trans-border transactions

• Best practices regarding operational protocols or network codes

• Standardization of contracts

The CRE is looking forward to continued collaboration with NAESB on several topics

www.gob.mx/cre @CRE_Mexico

Meney de la Peza Regulation Unit

Mexico’s Energy Regulatory Commission

NAESB Board of Directors Dinner Houston, Texas December, 2016