mexico - iuj.ac.jp · the aztec empire was brought to an end by the spanish conquistadores who made...

TRANSCRIPT

COUNTRY PROFILE 2001

MexicoThis Country Profile is a reference tool, which providesanalysis of historical political, infrastructural and economictrends. It is revised and updated annually. The EIU’squarterly Country Reports analyse current trends andprovide a two-year forecast

The full publishing schedule for Country Profiles is nowavailable on our website at http://www.eiu.com/schedule

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

The Economist Intelligence UnitThe Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through our digital portfolio, where our latest analysis isupdated daily; through printed subscription products ranging from newsletters to annual referenceworks; through research reports; and by organising seminars and presentations. The firm is a member ofThe Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1007Fax: (44.20) 7499 9767E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

Hong KongThe Economist Intelligence Unit25/F, Dah Sing Financial Centre108 Gloucester RoadWanchaiHong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

Website: http://www.eiu.com

Electronic deliveryThis publication can be viewed by subscribing online at http://store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, on-linedatabases and as direct feeds to corporate intranets. For further information, please contact your nearestEconomist Intelligence Unit office

London: Jan Frost Tel: (44.20) 7830 1183 Fax: (44.20) 7830 1023New York: Dante Cantu Tel: (1.212) 554 0643 Fax: (1.212) 586 1181Hong Kong: Amy Ha Tel: (852) 2802 7288/2585 3888 Fax: (852) 2802 7720/7638

Copyright© 2001 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author’s and the publisher’s ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-5596

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

!

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Comparative economic indicators,

1

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Contents

3 Basic data

4 Political background4 Historical background9 Constitution and institutions

10 Political forces13 International relations and defence

14 Resources and infrastructure14 Population15 Education16 Health17 Natural resources and the environment18 Transport and communications20 Energy provision

22 The economy22 Economic structure23 Economic policy26 Economic performance28 Regional trends

29 Economic sectors29 Agriculture, forestry and fishing30 Manufacturing32 Mining and semi-processing33 Construction34 Financial services37 Other services

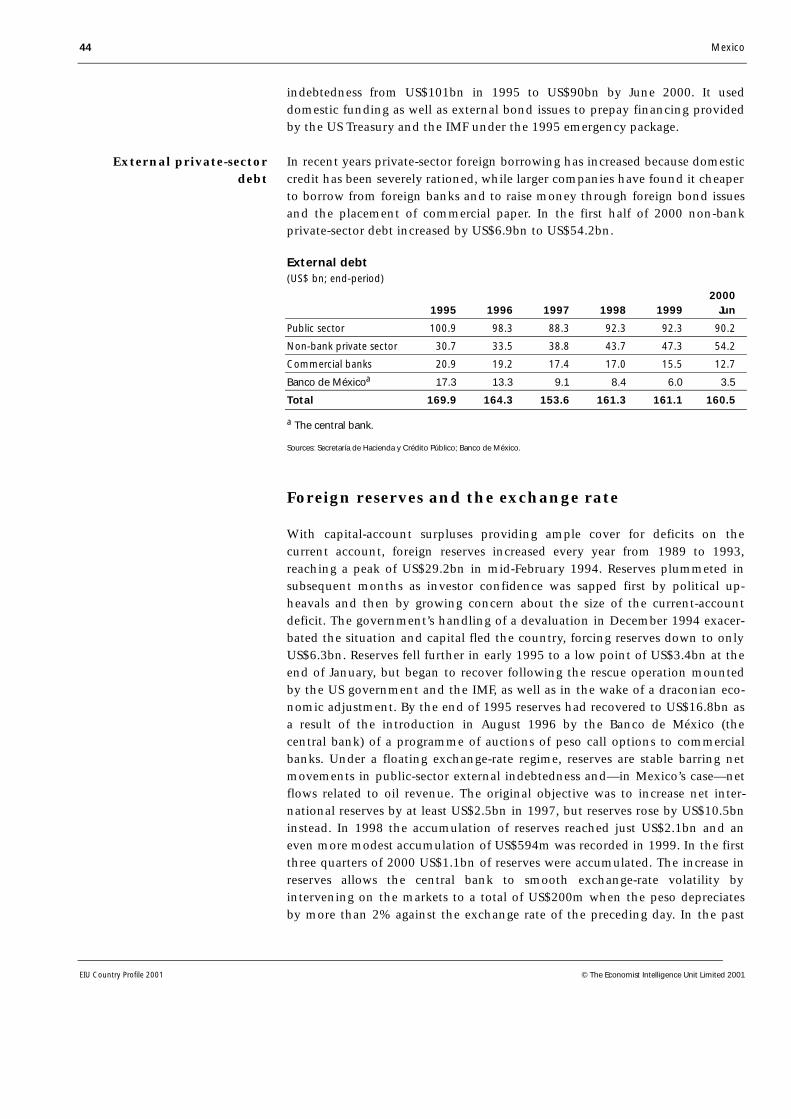

38 The external sector38 Trade in goods40 Invisibles and the current account42 Capital flows and external debt44 Foreign reserves and the exchange rate

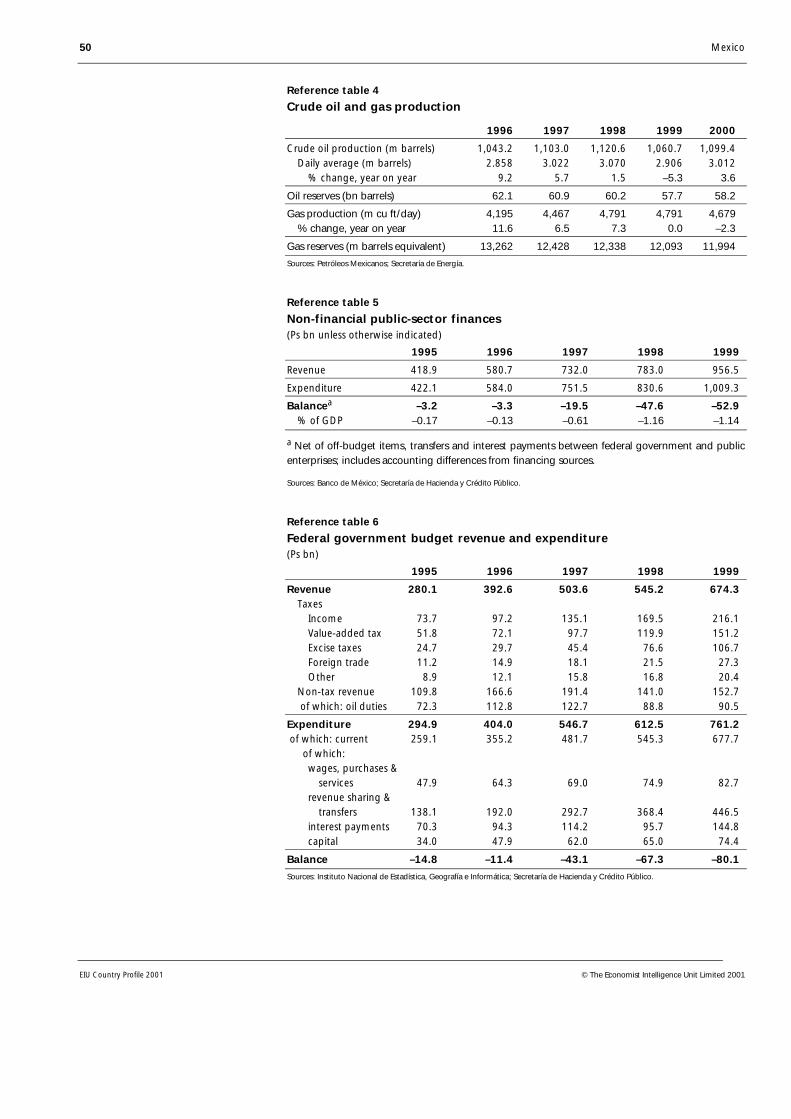

46 Appendices46 Sources of information49 Reference tables49 Population49 Labour force49 Unemployment rates in urban areas50 Crude oil and gas production50 Non-financial public-sector finances50 Federal government budget revenue and expenditure51 Money supply and credit51 Interest rates51 Gross domestic product52 Gross domestic product by sector52 Gross domestic product by expenditure52 Prices and earnings

2

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

53 Production of principal crops53 Livestock production53 Manufacturing production54 Minerals production54 Stockmarket indicators54 Merchandise sales54 Tourism55 Main exports and imports55 Main trading partners56 Direction and composition of trade, 199957 Balance of payments, national statistics57 Balance of payments, IMF estimates58 Total foreign investment58 External debt, World Bank estimates58 Gross external debt, national estimates59 Amortisation schedule of global external debt59 Foreign reserves59 Exchange rates

Mexico 3

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Mexico

Basic data

1,953,162 sq km

97.4m (February 14th 2000, preliminary estimate from Instituto Nacional deEstadística, Geografía e Informática 2000 census)

Population (m), 2000

Mexico City (capital) 17.8Guadalajara 3.7Monterrey 3.2

Tropical in the south, temperate in the highlands, dry in the north

Hottest month, May, 12-26°C (average daily minimum and maximum); coldestmonth, January, 6-19°C; driest month, February, 5 mm average rainfall; wettestmonth, July, 170 mm average rainfall

Spanish is the official language. Over 60 indigenous languages are also spoken,mainly Náhuatl, Maya, Zapoteco and Mixteco

Metric system; also old Spanish measures

Peso. Average exchange rate in 2000: Ps9.46:US$1; exchange rate at end-January 2001: Ps9.68:US$1

Six hours behind GMT in Mexico City

January 1st, February 5th, March 21st, Maundy Thursday, Good Friday, May 1stand 5th, September 16th, October 12th, All Souls’ Day (partial), November20th, December 12th (partial) and 25th

Land area

Population

Main towns

Climate

Weather in Mexico City(altitude 2,309 metres)

Languages

Measures

Currency

Time

Public holidays

4 Mexico

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Political background

The election of Vicente Fox Quesada of the Partido Acción Nacional (PAN) aspresident in July 2000 signified the start of a new era in Mexico’s political life,ending seven decades of domination of the political system by the PartidoRevolucionario Institucional (PRI). Mr Fox will maintain the disciplinedmarket-oriented policies pursued by the past three PRI governments. The newpresident will have to work with opposition parties to pass legislation as for thefirst time in the country’s history no political party has an absolute majorityeither in the Chamber of Deputies (for the 2000-03 legislature) or in the Senate(for the 2000-06 legislature).

Historical background

Mexico’s early history was characterised by the rise and fall of several civilis-ations, including the Olmecs, the Mayas and the Aztecs. The Aztec empire wasbrought to an end by the Spanish conquistadores who made New Spain, com-prising the states of the US south-west, Mexico and Central America, a colonyin 1521. Independence from Spain was achieved in 1821.

Independence did not signal peace and prosperity. For more than a generationMexico was subject to civil wars and predatory incursions. Texas seceded fromMexico in 1835-36. In 1845 a war broke out with the US, which was to costMexico the additional loss of California, Arizona and New Mexico. In 1864France imposed a Hapsburg archduke, Maximilian, as emperor. However, afterthe withdrawal of French troops in 1867, the archduke was quickly overthrownand executed. Under the dictatorship of Porfirio Díaz (1876-1911) order wasimposed and the economy developed. But when General Díaz engineered hisown re-election for the seventh time in 1910, opposition forces led byFrancisco Madero resorted to arms. They were joined by rebel peasants underthe leadership of Emiliano Zapata. General Díaz was forced into exile in 1911and Mr Madero became president, but he was ousted and killed in 1913. Newrebellions followed and although the rebels were crushed, their ideals, in-cluding land reform, were incorporated into a new constitution in 1917.

Plutarco Elías Calles, president between 1924 an 1928, did much to shapefuture political developments, particularly through the creation of the PartidoNacional Revolucionario (PNR). Another important presidency was that ofLázaro Cárdenas (1934-40), who carried out extensive land redistribution andexpropriated foreign oil companies. In 1945 the party was renamed the PRI.For many years sustained economic growth ensured the PRI a high degree ofpopular support. A corporatist system was developed as the regime co-optedany potential opponents such as the labour and peasant movements. When itconsidered it necessary, the PRI resorted to electoral fraud in order to ensure anabsolute monopoly of power. Political stability came under strain in the late1960s when intellectuals and students, influenced by left-wing ideals, soughtmore political openness, but were repressed by the state. A deterioration in

Instability and dictatorshipfollow independence

The PRI created

Mexico 5

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

economic policy in the 1970s precipitated an external debt crisis in 1982 andthe president, Miguel de la Madrid (1982-88), was forced to embark on apolitically costly process of structural economic reform.

Important recent events

January 1994: North-American Free Trade Agreement (NAFTA) commences.Peasant rebel uprising in Chiapas, but the military threat is quickly contained.

March 1994: Assassination of Luis Donaldo Colosio, presidential candidatefor the ruling PRI. Ernesto Zedillo Ponce de León is nominated as the party’sreplacement candidate and is elected president in August.

December 1994: Mr Zedillo takes office. Precipitous devaluation of the pesoleads to a banking crisis and deep recession in 1995.

July 1996: All political parties in Congress agree on constitutional changes toimplement a radical electoral reform, passed later in the year.

July 1997: National elections. For the first time in nearly 70 years, the PRIloses majority control of the Chamber of Deputies. The election for the govern-orship of Mexico City, the first held since 1928, is won by CuauhtémocCárdenas of the Partido de la Revolución Democrática (PRD). The PAN alsomakes important advances, winning the governorships of Querétaro and theimportant industrial state of Nuevo León.

September 1997: The four opposition parties in Congress unite to outvotethe PRI on major issues, creating a counterweight to the executive.

1998-99: The opposition continues to advance, but the PRI proves resilient. Of17 governorships contested in 1998-99, just five go to the opposition, includingthree to the PRD, its first state governorships. Francisco Labastida wins the first-ever PRI presidential primary held at the end of 1999.

July-December 2000: National elections. Vicente Fox Quesada, the PAN’spresidential candidate, defeats Mr Labastida, ending 71 years of PRI rule. ThePRD wins Mexico City again, as well as the governorship of the state ofChiapas in coalition with the PAN. After an uneventful transition period,Mr Fox takes office on December 1st, appointing a mostly non-partisan pro-business cabinet.

PRI presidential candidates were traditionally chosen by the outgoing pres-ident. In a bid to influence the decision, a section of the party led by a formerPRI president, Porfirio Muñoz Ledo, and a former governor of Michoacán,Cuauhtémoc Cárdenas, son of Lázaro Cárdenas, formed the CorrienteDemocrática (CD). When Mr de la Madrid selected Carlos Salinas de Gortari asthe PRI’s candidate in the 1988 election, the CD split from the PRI. Mr Cárdenasstood in the election and managed to attract the support of most of the left forhis Frente Democrático Nacional (FDN) alliance. The official results, alleged tobe fraudulent, gave Mr Salinas victory with only 50.4% of the vote. PRIgovernments had rarely announced victories of less than 85% before 1982.

The 1988 election marredby allegations of fraud

6 Mexico

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

During his presidency (1988-94) Mr Salinas restructured the economy and per-mitted some electoral gains by the opposition, for example, of governorships,which had previously been monopolised by the PRI. An uprising in Chiapasstate in January 1994 by the Ejército Zapatista de Liberación Nacional (EZLN)highlighted the fact that despite economic progress, social tensions weremounting. Consequently, as well as negotiating with the EZLN, the govern-ment enacted comprehensive electoral reform, including the granting of auto-nomy to the Instituto Federal Electoral (IFE, the electoral authority), along withother measures to diminish the possibility of electoral fraud. Elections held inAugust 1994 were recognised generally as transparent. Ernesto Zedillo Ponce deLeón of the PRI won the presidential contest with 50.2% of the valid votes cast.Diego Fernández de Cevallos of the right-wing PAN polled 26.7%.Mr Cárdenas, who stood for the left-wing Partido de la RevoluciónDemocrática (PRD), took 17.1% of the vote. In Congress the PRI held on to itsmajority, but lost seats to both the PAN and the PRD.

Mr Zedillo (1994-2000) continued the process of political change. Progress onelectoral reform was slow, but a breakthrough was finally achieved in July 1996when representatives of all four parties in Congress—the PRI, the PAN, the PRDand the left-wing Partido del Trabajo (PT)—agreed to new election rules andapproved the necessary constitutional changes. However, the specific legis-lation was approved by the PRI alone, because of disagreements about the levelof public funding permitted for political parties and restrictions placed on theformation of political coalitions.

The new rules were introduced in time for the 1997 mid-term congressionalelections. The governorships of six states and Mexico City were also disputed.For the first time in almost 70 years, the PRI lost its majority in the Chamber ofDeputies. The most important gains were made by the PRD, which became thesecond most important force in the new Congress and won the governorshipof Mexico City. The PAN also won congressional seats and the governorships ofNuevo León and Querétaro, thereby gaining control of six of 31 states. Thefour opposition parties that won seats in the Chamber of Deputies in July 1997united to control it, but the alliance proved fragile. The PAN at times joinedwith the PRI to approve important economic legislation, with the PRDcategorically opposed to the government.

Of the 17 governorships contested in 1998-99, 12 were won by the PRI, one bythe PAN, three by the PRD—each of them in former PRI strongholds, withestranged PRI members as candidates—and one by a coalition headed by thePAN and the PRD. Thus by the beginning of 2000 the opposition held the gov-ernorships of ten states. Confidence in clean elections had increased and can-didates and regional issues had become more important.

The elections held in July 2000, the most open and democratic to date, broughtsweeping political change when Mr Fox, the candidate of the coalition formedby the PAN and the green Partido Verde Ecologista de México (PVEM), defeatedthe PRI’s candidate, Francisco Labastida, ending the party’s 71-year reign.Mr Fox won the presidency with 42.5% of the vote (there are no run-offs in

Reforms accelerate inresponse to unrest in 1994

Patchy progress onpolitical reform in 1995-96

Gains for the oppositionin 1997

A multiparty democracyemerges

The PRI loses the 2000presidential election

Mexico 7

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

federal elections). Although Mr Fox’s share of the vote was the lowest everobtained by a winning presidential candidate, this outcome did not affect hislegitimacy as he defeated the PRI by a substantial margin. Mr Labastidaobtained 36.1% of the vote, while Mr Cárdenas, supported by a five-party coal-ition headed by the PRD and the PT, took third place with 16.6% of the vote.

Presidential election results, 2000

Votes Candidate Party or coalition No. (m) % of totala

Vicente Fox Quesada Alianza por Cambiob 16.0 42.5

Francisco Labastida Ochoa Partido Revolucionario Institucional 13.6 36.1

Cuauhtémoc Cárdenas Solórzano Alianza por Méxicoc 6.3 16.6

Gilberto Rincón Gallardo Partido Democracia Social 0.6 1.6

Manuel Camacho Solís Partido del Centro Democrático 0.2 0.6

Porfirio Muñoz Ledod Partido Auténtico de la RevoluciónMexicana 0.2 0.4

Annulled votes 0.8 2.1

Total 37.6 100.0

a A minimum 2% of the vote is required to retain legal registration as a political party. b Coalitionformed by the Partido Acción Nacional and the Partido Verde Ecologista de México. c Coalitionformed by the Partido de la Revolución Democrática, Partido del Trabajo, Partido de la SociedadNacionalista, Partido Alianza Social and Convergencia por la Democracia. d Declined shortly beforethe election to support Vicente Fox.

Sources: Instituto Federal Electoral; EIU.

Since taking office Mr Fox has followed a radically different form of govern-ment from that traditionally adopted by the PRI. His cabinet and close circle ofcollaborators are mostly drawn from the private sector and academia. Few PANheavyweights were invited to join the cabinet. Only one PRI member,Francisco Gil Díaz, was appointed to a cabinet post as minister of finance andpublic credit in recognition of his experience and sound reputation on fin-ancial matters. Mr Fox’s presidential style is informal in sharp contrast to thesolemnity customarily attached to his office. A devout Roman Catholic, he hasalso broken with the convention followed since the mid-19th century thatestablished a clear distance between the government and the church.

Although Mexico’s political system has long been considered to be one that isdominated by the president, constitutionally the relationship between theexecutive and the legislature is similar to that of the US. The legislature repre-sents a powerful counterweight to the executive, a feature of the politicalsystem that had remained hidden as a result of the PRI’s dominance of thelegislature and the party’s subordination to the president. The governabilityissue will undoubtedly be a dominant theme in the next few years as for thefirst time no political party holds a working majority in either congressionalchamber. This situation will not change in the short term as the next federalelection is not due until 2003, when all seats in the Chamber of Deputies willbe contested. The Senate will remain in its present form until 2006.

Congress finds new power

Mr Fox establishes a newstyle of government

8 Mexico

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

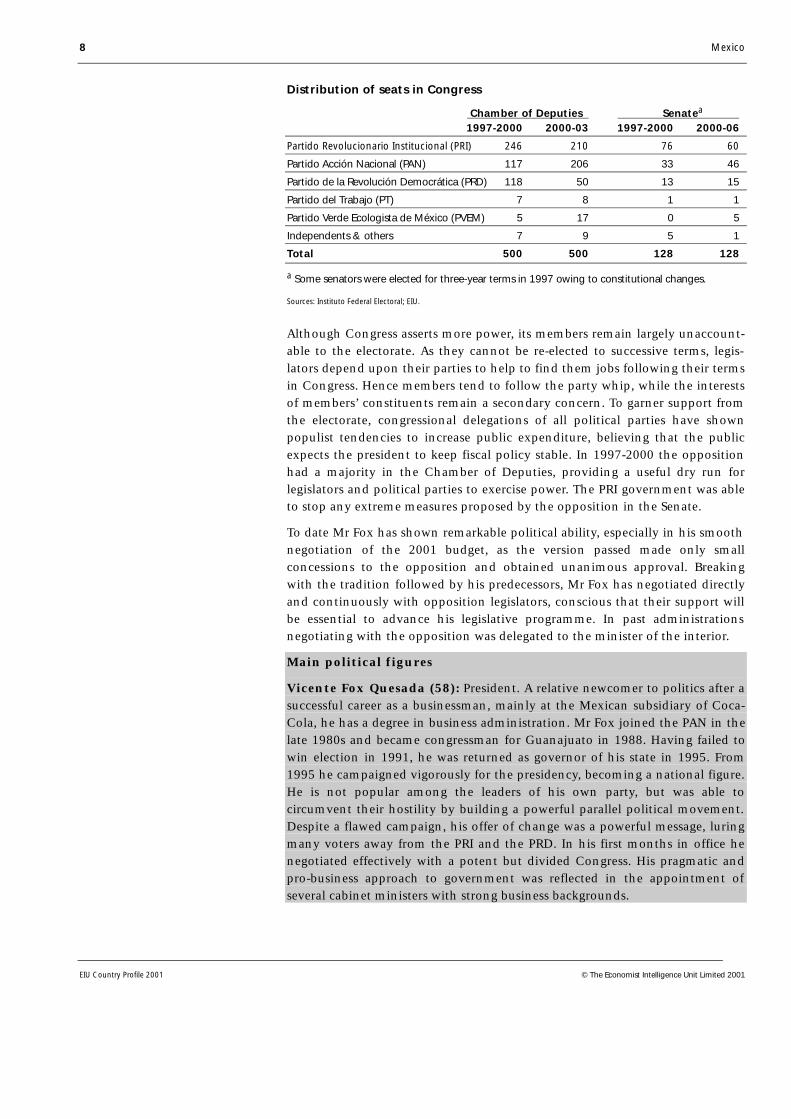

Distribution of seats in Congress

Chamber of Deputies Senatea

1997-2000 2000-03 1997-2000 2000-06

Partido Revolucionario Institucional (PRI) 246 210 76 60

Partido Acción Nacional (PAN) 117 206 33 46

Partido de la Revolución Democrática (PRD) 118 50 13 15

Partido del Trabajo (PT) 7 8 1 1

Partido Verde Ecologista de México (PVEM) 5 17 0 5

Independents & others 7 9 5 1

Total 500 500 128 128

a Some senators were elected for three-year terms in 1997 owing to constitutional changes.

Sources: Instituto Federal Electoral; EIU.

Although Congress asserts more power, its members remain largely unaccount-able to the electorate. As they cannot be re-elected to successive terms, legis-lators depend upon their parties to help to find them jobs following their termsin Congress. Hence members tend to follow the party whip, while the interestsof members’ constituents remain a secondary concern. To garner support fromthe electorate, congressional delegations of all political parties have shownpopulist tendencies to increase public expenditure, believing that the publicexpects the president to keep fiscal policy stable. In 1997-2000 the oppositionhad a majority in the Chamber of Deputies, providing a useful dry run forlegislators and political parties to exercise power. The PRI government was ableto stop any extreme measures proposed by the opposition in the Senate.

To date Mr Fox has shown remarkable political ability, especially in his smoothnegotiation of the 2001 budget, as the version passed made only smallconcessions to the opposition and obtained unanimous approval. Breakingwith the tradition followed by his predecessors, Mr Fox has negotiated directlyand continuously with opposition legislators, conscious that their support willbe essential to advance his legislative programme. In past administrationsnegotiating with the opposition was delegated to the minister of the interior.

Main political figures

Vicente Fox Quesada (58): President. A relative newcomer to politics after asuccessful career as a businessman, mainly at the Mexican subsidiary of Coca-Cola, he has a degree in business administration. Mr Fox joined the PAN in thelate 1980s and became congressman for Guanajuato in 1988. Having failed towin election in 1991, he was returned as governor of his state in 1995. From1995 he campaigned vigorously for the presidency, becoming a national figure.He is not popular among the leaders of his own party, but was able tocircumvent their hostility by building a powerful parallel political movement.Despite a flawed campaign, his offer of change was a powerful message, luringmany voters away from the PRI and the PRD. In his first months in office henegotiated effectively with a potent but divided Congress. His pragmatic andpro-business approach to government was reflected in the appointment ofseveral cabinet ministers with strong business backgrounds.

Mexico 9

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Cuauhtémoc Cárdenas Solórzano (67): Three times presidential candidateand despite his lacklustre performance in the 1994 and 2000 elections, theundisputed leading voice of the PRD. He was a PRI senator in 1976, under-secretary for agriculture in 1976-80 and governor of Michoacán in 1980-86.When he left the PRI to run for president in 1988 he successfully united whathad been a fragmented left-wing opposition. Having lost an election marred byfraud, his stature declined under the Salinas administration and he achievedonly third place in a relatively clean election in 1994. Making an impressivepolitical comeback, Mr Cárdenas won the 1997 Mexico City election by a land-slide. However, his uninspiring performance once in office and his inability toappeal to voters in the middle ground eliminated any chance he might havehad of winning the presidency. His determination to remain the PRD’s mainfigurehead is causing divisions within the organisation, but no other partymember has the stature to challenge him.

Santiago Creel Miranda (47): Interior minister. Mr Creel, a lawyer in pri-vate practice with links to academia, received the PAN’s nomination to becomea member of the IFE in 1994, just as that organisation had been granted fullautonomy. He became a deputy for the PAN in 1997, although he was notofficially a party member until 1999, building his political reputation as one ofthe main leaders of the opposition bloc that held a majority in the Chamber ofDeputies. In 2000 he stood as the PAN’s candidate in the contest for the gov-ernorship of Mexico City and came a close second to the PRD. In his role asinterior minister Mr Creel has dealt skilfully with opposition parties, helped byhis legislative experience.

Roberto Madrazo Pintado (50): In 1999 Mr Madrazo stood for the PRIpresidential nomination against the eventual winner, Mr Labastida, gainingstanding as a party heavyweight. He is popular among the PRI’s grassroots ashe has had a long career in the party, having risen from being a leader of itsyouth movement to the post of party secretary. Mr Madrazo was governor ofTabasco in 1995-2000 and has been twice been elected to the Chamber ofDeputies—in 1976-79 and in 1991-94—and to the Senate in 1988-91.

Felipe Calderón Hinojosa (38): PAN leader in the Chamber of Deputies.Despite his youth Mr Calderón is one of the main leaders within his party,having been head of its youth movement in 1987-89, secretary-general in1993-95 and president in 1996-99. A local congressman in the Mexico Cityassembly in 1988-91, he was first elected to Congress in 1991-94 and is nowserving his second term as a federal congressman. As PAN leader in the lowerhouse he treads a fine line: never a supporter of Mr Fox, he has statedrepeatedly that the president does not have the unquestioning support of PANlegislators, while recognising that he cannot obstruct the first PAN adminis-tration in history too militantly.

Constitution and institutions

The constitution of 1917, which is still in force, was a far more social docu-ment than that written in 1857. Apart from subordinating the rights of privateproperty to the public interest and making specific provision for land reform, it

A resilient constitution

10 Mexico

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

stressed the rights of labour and also curtailed greatly the power and influenceof the clergy. The constitution also established the framework for a federalsystem of government covering 31 states and the Distrito Federal (the FederalDistrict, which includes Mexico City) and provided for the separation of exec-utive, legislative and judicial powers. In practice government has been central-ised and the president has had far greater powers than Congress, as well as con-siderable influence over the judiciary. The dominance of the president hasstarted to diminish recently. Reforms implemented in the mid-1990s gave theSupreme Court greater autonomy and Congress has also emerged as a moreimportant political force since the PRI lost majority control of the Chamber ofDeputies in 1997. Mr Fox called for a thorough revision of the constitution inFebruary 2001, but it is highly improbable that Congress would agree to anyradical overhaul in the near term.

Congress comprises the Senate and the Chamber of Deputies. Senators servefor six years and deputies for three years. In the Chamber of Deputies 300 seatsare allocated using the first-past-the-post system and 200 by proportionalrepresentation. In the Senate 96 seats are elected directly, while 32 are electedby proportional representation. Of the directly elected seats in the Senate, 64are elected on a first-past-the-post basis and 32 are elected using the first min-ority principle. Reforms approved by Congress in 1996 made it easier for asingle party to gain a working majority in Congress, but impossible for any oneparty to achieve the two-thirds majority necessary to change the constitution.Despite these reforms, the 2000 election result was unprecedented in that noone party enjoys a working majority in either house.

The most important political post in the cabinet is that of interior minister asthe Ministry of the Interior is charged with preserving the country’s politicalstability. The Ministry of Finance and Public Credit is responsible for economicpolicymaking at the highest level, although the Ministry of the Economy(formerly the Ministry for Trade and Industry) also plays a major role.

Political forces

Three parties dominate the political landscape: the PAN, the PRI and the PRD.After more than 60 years in opposition, the PAN won the presidency in theJuly 2000 election. The PAN was founded in 1939 and has built up a supportbase mainly in northern and central states and among the urban middleclasses, although it has widened slightly beyond these groups since the early1990s. Although inclined to free-market policies, the party has also shownsome populist tendencies. The leadership of Luis Felipe Bravo Mena, who waselected president of the party in March 1999, has been undermined by theauthority of the party chiefs in Congress and by the powerful personality ofMr Fox. PAN members are divided in their support for Mr Fox. Although nearlyall members are pleased that the PAN nominee won the presidency, asignificant number also feel that Mr Fox hijacked the party as a vehicle tofurther his personal ambition. In the main Mr Fox shares the party’s policyorientation, notably in his strong support for free-market policies, but he has

Composition of Congress

Ranking of ministries

Political parties and groups

Mexico 11

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

never presented himself as a loyal party servant and may break from PANpositions on occasion. As a result of his uncertain loyalty to the party line, thePAN cannot count on Mr Fox to put its interests first. Conversely, the presidentcannot count on the full support of his own party for his legislative initiatives.But this apparent disadvantage has helped the government to work more easilywith opposition parties.

For the first time since it was established in 1929, the PRI is in opposition atthe federal level, a reality that has proved difficult for most of its members toaccept. Detached from presidential power, the PRI is struggling to reinventitself. Having lacked any coherent ideology for decades, the party became ameans of winning and exercising power, and largely followed the direction setby the president. In addition, since the early 1980s a clear separationdeveloped between the party’s traditionalists, who are mostly positioned in thelegislature and local government, and its technocrats, who although only aminority hold important positions in the executive. Following the loss of thepresidency, a battle for control of the party will take place in 2001, aconfrontation that may well bring important defections and splinters. Mostprobably the PRI will evolve into a party of the centre-left with a socialdemocratic agenda. But if the party manages to stay together, it will remain apowerful political force and could regain the presidency in 2006. Currently thePRI has 18 of the 31 state governorships and the biggest parliamentary groupsboth in the Chamber of Deputies and the Senate.

The PRD was formed in 1989 by the groups that had supported Mr Cárdenas’spresidential bid in 1988. After his defeat in the 1994 election, the party suffereda temporary decline in importance. Between 1996 and 1999 under theleadership of Andrés Manuel López Obrador the party’s electoral fortunes im-proved, partly owing to the significant protest vote against the governmentduring the economic crisis. When Mr Cárdenas won the governorship ofMexico City with ease in 1997, the PRD became the second most importantforce in Congress. The party diversified its base by embracing disaffected PRImembers, wresting from its control states that had previously been consideredimpregnable. The PRD made important gains by opposing almost any measureproposed by the government. The March 1999 internal election to choose itsnew president was marred by fraud and had to be annulled. After another con-troversial election, senator Amalia García was elected party leader in August1999. Mr Cárdenas managed a distant third place in the 2000 presidentialelection as many of his supporters defected to vote for Mr Fox, while the partyalso suffered broad losses in Congress. The PRD will hold a nationwide partycongress in April 2001. With rival groups emerging, some splintering is likelywhether or not Mr Cárdenas manages to retain his overarching influence.

A three-party system has evolved since 1997, with the small PT and the greenPVEM on the fringes, which occasionally form alliances with the PAN or thePRD on antiPRI electoral tickets. Support from PT and PVEM deputies wascritical to PAN and PRD majorities in the lower house of the legislature in the1997-2000 term as it enabled both parties to enjoy a certain amount ofinfluence in government. Both the PT and the PVEM have lost influence in thenew legislature, while the PVEM did not benefit from having backed Mr Fox’s

12 Mexico

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

presidential bid as he refused to give the party a cabinet post. Six additionalpolitical parties were granted official registry by the electoral authorities at theend of 1999: the Partido de la Sociedad Nacionalista (PSN), the Covergenciapor la Democracia (CPD), the Partido Alianza Social (PAS), the Partido delCentro Democrático (PCD), the Partido Auténtico de la Revolución Mexicana(PARM) and the Partido Democracia Social (PDS). Both the CPD and the PCDare small splinter groups of the PRI. The PSN, the CPD and the PAS joined thePRD and the PT to form the Alianza por México, to support Mr Cárdenas’spresidential candidacy. The PCD, the PARM and the PDS nominated their ownpresidential candidates, but failed to obtain the 2% of votes necessary to keeptheir parties registered. The CPD, the PAS and the PSN managed to win someseats in the Chamber of Deputies as a result of an alliance with the PRD, buttheir numbers are minimal and as the PRD will almost certainly reject forminga coalition with them again, these parties may disappear in the 2003 election.

Civic organisations have developed a degree of strength in recent years. Amongthem is the Barzón (Yoke) movement, which has been at the forefront of adebtors’ revolt. In addition, Mexico has two rebel groups: the EZLN, which isbased in the state of Chiapas, and the Ejército Popular Revolucionario (EPR),based in Guerrero, which divided into splinter groups in 1998-99. No formalpeace negotiations have taken place since 1996 as both the government andthe EZLN have been unwilling to cede on certain questions.

The EZLN, cornered militarily, has a small political base but a formidable prop-aganda machine. In September 1997 a political front, the Frente Zapatista deLiberación Nacional (FZLN), was established to mobilise national support forthe principles of the Zapatistas, but it will not participate in elections. Theprominence of the EZLN has increased since the start of Mr Fox’s presidency ashe is determined to negotiate a peace settlement with the movement. Thepresident removed the army unilaterally from several major positions, liberatedimprisoned EZLN members and most importantly has sent a constitutional in-itiative to Congress that if passed would increase the autonomy of indigenousgroups. However, the Zapatistas have refused to negotiate a final peace accorduntil the legislation is approved, although it is unlikely to be passed byCongress soon. Meanwhile, the EZLN leadership has captured the limelight,although it is unclear whether it aims to become a political force.

Neither the church nor the military are major participants in politics. In 1992the constitution was modified to give official recognition to the RomanCatholic Church. Since then several church leaders have made intermittentattempts to influence public policy, particularly on education, but have beenrebuffed by politicians. The military has also become more prominent incivilian affairs. The institutional loyalty of the armed forces was tested in the2000 political transition, but proved to be strong when Mr Fox appointed aminister of defence of his choosing over several more senior generals.

Forces outside parliament

Mexico 13

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

International relations and defence

Mexico’s foreign policy is defined by its historical relationship with the US, towhich it lost almost one-half of its original territory in the mid-19th century.AntiUS sentiment has remained strong since then, although relations have im-proved in the past decade. Under the Salinas government Mexico into Mexicobecame a signatory to the North American Free-Trade Agreement (NAFTA), theprovisions of which came into force on January 1st 1994. The US adminis-tration of Bill Clinton was quick to offer help when Mexico ran into seriousfinancial difficulties at the end of 1994 by making US$20bn available from theUS Treasury. Relations between the two countries have remained strong,despite the persistent and thorny issues of illegal migration, drug-trafficking,money-laundering and Cuba. The relationship between the US and Mexico isset to become stronger under the presidencies of Mr Fox and George W Bush.The Fox administration espouses an activist foreign policy, a reversal of thenon-interventionist stance adopted by PRI governments since the 1930s, andone that largely supports US initiatives. Mr Bush visited Mexico in February2001 in his first trip outside the US as president, a sign of the increased close-ness between the two countries that started when he was governor of Texas.

Mexico has also strengthened ties with other countries and economic blocs.The country was admitted as a full member of the Asia-Pacific EconomicCo-operation forum in 1993 and to the OECD in 1994, having joined what isnow known as the World Trade Organisation in 1986. Mexico has also pursuedgreater regional integration by entering into free-trade agreements (FTAs) withCosta Rica, Bolivia, Venezuela and Colombia (1995), Nicaragua (1998), Chile(1992 and 1998), Israel and the EU (2000). In addition, Mexico trades withEuropean Free-Trade Area signatories and is a member of the Triangulo delNorte (Northern Triangle) trade bloc alongside Guatemala, Honduras and ElSalvador. The new administration is set to continue to negotiate new FTAs suchas that currently being negotiated with Singapore and preliminary negotiationswith Japan have begun. Mr Fox has also expressed interest in reachingagreement with the Mercado Común del Sur (Mercosur, the southern customsunion), although similar efforts have failed in the past owing to trade conflictsbetween Mexico and Brazil.

Although the armed forces are ill-equipped to defend Mexico from externalaggression, their role in domestic affairs has increased in the past few years. Inaddition to waging a perennial war against drug-traffickers, they have beencalled on to contain guerillas from both the EZLN and the EPR, and even totake on policing duties. But scandals related to corruption and human rightsabuses have tarnished the army’s image. For the 2001 (January-December)fiscal year Congress authorised defence spending, including that for the navy,for a sum equivalent to 0.5% of GDP.

Armed forces, 2000

Active force: 192,770

Reserve force: 300,000

Relations with the USimproving

Priorities of the armedforces

14 Mexico

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Army: 140,000 soldiers, of which 60,000 are conscripts. There are 12 militaryregions with garrisons in 44 zones. Each garrison comprises 81 infantrybrigades, one of which is mechanised, 19 motorised cavalry brigades, threeartillery regiments and one air-mobile unit. The strategic reserve includes fourarmoured brigades and one presidential guard brigade.

Navy: 37,000 seamen, including 8,600 marines and 1,100 naval air personnel.There are 17 naval regions, six in the Gulf of Mexico and 11 in the PacificOcean. The navy possesses three destroyers and eight frigates.

Air force: 11,770 airmen, including one squadron with ten fighters and 71armed helicopters.

Resources and infrastructure

Population

Mexico’s estimated population in mid-February 2000 stood at 97.4m, acc-ording to preliminary results from the year’s census. The rate of populationgrowth has slowed from more than 3% per year in the early 1970s to just 1.5%per year in the late 1990s. This deceleration reflects declining fertility rates aswell as improved healthcare, which has lowered infant mortality rates. Annualpopulation growth is expected to be 1.4% in 2001. (For historical data on pop-ulation see Reference table 1.)

At the end of 1997 an estimated 34.9% of the population was 14 years orunder. Inevitably this distribution results in pressures on the education systemand the labour market. In 1997 146,865 Mexicans migrated legally to the US,compared with 163,572 in 1996, while between 1988 and 1996 an estimatedaverage of 150,000 people per year migrated there illegally. In 1990 the numberof people of Mexican extraction living in the US was estimated at 13.5m, 4m-5m of whom were born in Mexico. By the end of 1996 an estimated 2.7millegal immigrants from Mexico were living in the US. In October1999-September 2000 1.6m people were apprehended by US border patrols,although this number is inflated by overcounting as many people return to theUS as soon as they are expelled; also, not all of those persons apprehended areof Mexican origin. In October 2000-January 2001 the number of peopleapprehended fell to 330,325, a sharp decline compared with the 425,002people apprehended in the year-earlier period. (For historical data on employ-ment see Reference tables 2 and 3.)

Rural areas show a high level of population dispersion: 96% of the country’stowns and villages have fewer than 1,000 inhabitants and seven out of ten ofthese suffer from high to very high levels of poverty, a factor partly attributableto geographical marginalisation. Within Mexico the search for better livingstandards has led to rural to urban migration, especially to Mexico City and thecities of Monterrey and Guadalajara, but also in more recent times to northernmaquiladora (in-bond assembly for re-export) towns such as Tijuana and

Emigration to the US hasbeen substantial

Internal migration

Mexico 15

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Ciudad Juárez, as well as to tourist centres such as Cancún. In 1990 some 71%of the population lived in urban areas. According to preliminary estimatesfrom the 2000 census, 47.3% of the total population live in urban areas with atleast 100,000 inhabitants.

Immigrant population of statesa, 1995(% of state population that is immigrant)

Quintana Roo 53.4

Baja California 49.5

Estado de México 38.5

Morelos 35.4

Colima 34.7

Baja California Sur 33.7

Campeche 30.3

Distrito Federal (Federal District incl Mexico City) 30.1

a States where immigrants form at least 30% of the population.

Source: Instituto Nacional de Estadística, Geografía e Informática, Conteo de Población y Vivienda.

Roughly 6% of the population are pure Indian. There are over 60 recognisedethnic and language groups, and around 1% of the total population does notspeak any Spanish. The most numerous indigenous groups are the Náhuatl,with 1.2m speakers, the Maya (714,000), the Zapotec (403,00) and the Mixtec(387,000). Indigenous people’s customs and languages differ greatly from onegroup to another, but they have suffered generally from exploitation, margin-alisation and poverty.

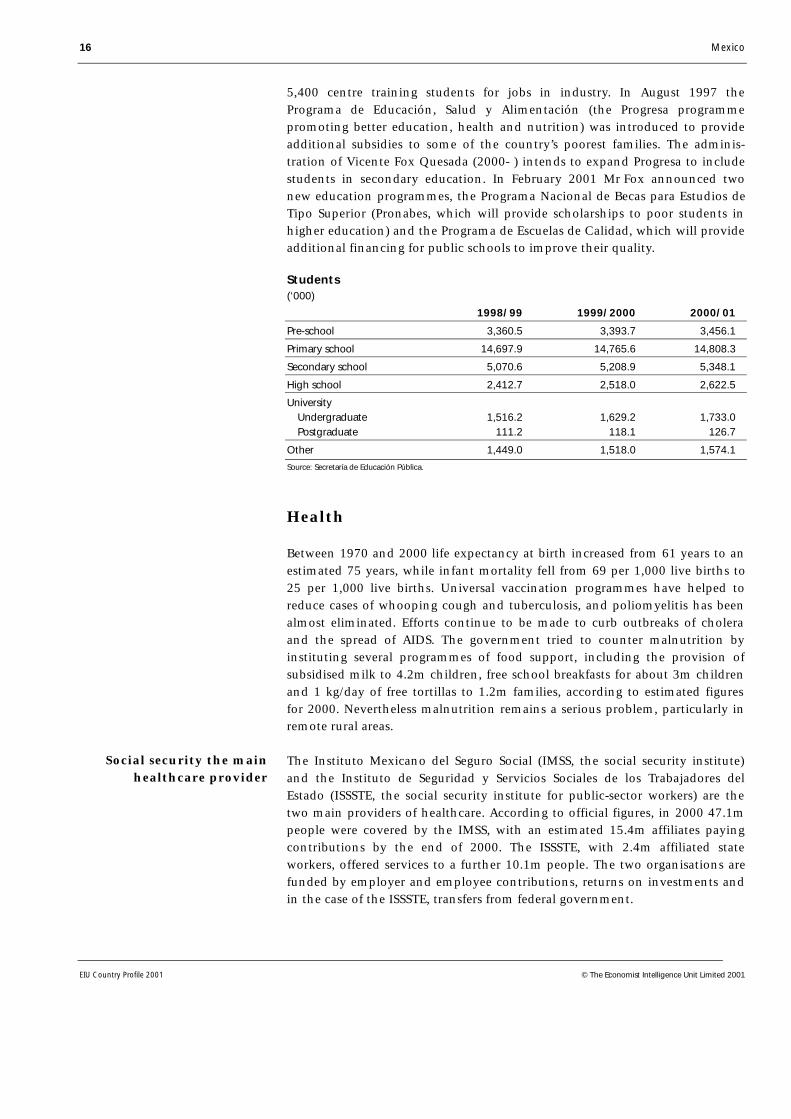

Education

In 2000 9.6% of the population of 15 years or over was illiterate. The averagenumber of years of schooling per child stood at 7.6 years, compared with6.5 years in 1990. Although primary education for children age between fiveand 11 years is both free and compulsory, in 2000 only 70.3% of the popul-ation age 15 years or over had completed the primary level. Attendance atsecondary level has been limited and only a very small proportion of studentsgo on to higher education. Less than one-half of the population—46.1%—age15 years or over had completed secondary school or completed studies at atechnical school. In the 2000/01 academic cycle Mexico had only1,860 students in higher education per 100,000 of the population, comparedwith 5,500 per 100,000 in the US. Education spending is around 5% of GDP,compared with 7% in the US and Canada.

The government has increased its budget allocations for education and init-iated a programme to bring basic education up to date by revising the syllabusand improving teachers’ training and pay. Secondary schooling for childrenage 11-14 years has been made compulsory and technical training facilitieshave been expanded. For the 2000/01 academic cycle there were more than

The Indian population

A poorly educatedworkforce

Educational reforms

16 Mexico

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

5,400 centre training students for jobs in industry. In August 1997 thePrograma de Educación, Salud y Alimentación (the Progresa programmepromoting better education, health and nutrition) was introduced to provideadditional subsidies to some of the country’s poorest families. The adminis-tration of Vicente Fox Quesada (2000- ) intends to expand Progresa to includestudents in secondary education. In February 2001 Mr Fox announced twonew education programmes, the Programa Nacional de Becas para Estudios deTipo Superior (Pronabes, which will provide scholarships to poor students inhigher education) and the Programa de Escuelas de Calidad, which will provideadditional financing for public schools to improve their quality.

Students(‘000)

1998/99 1999/2000 2000/01

Pre-school 3,360.5 3,393.7 3,456.1

Primary school 14,697.9 14,765.6 14,808.3

Secondary school 5,070.6 5,208.9 5,348.1

High school 2,412.7 2,518.0 2,622.5

University Undergraduate 1,516.2 1,629.2 1,733.0 Postgraduate 111.2 118.1 126.7

Other 1,449.0 1,518.0 1,574.1

Source: Secretaría de Educación Pública.

Health

Between 1970 and 2000 life expectancy at birth increased from 61 years to anestimated 75 years, while infant mortality fell from 69 per 1,000 live births to25 per 1,000 live births. Universal vaccination programmes have helped toreduce cases of whooping cough and tuberculosis, and poliomyelitis has beenalmost eliminated. Efforts continue to be made to curb outbreaks of choleraand the spread of AIDS. The government tried to counter malnutrition byinstituting several programmes of food support, including the provision ofsubsidised milk to 4.2m children, free school breakfasts for about 3m childrenand 1 kg/day of free tortillas to 1.2m families, according to estimated figuresfor 2000. Nevertheless malnutrition remains a serious problem, particularly inremote rural areas.

The Instituto Mexicano del Seguro Social (IMSS, the social security institute)and the Instituto de Seguridad y Servicios Sociales de los Trabajadores delEstado (ISSSTE, the social security institute for public-sector workers) are thetwo main providers of healthcare. According to official figures, in 2000 47.1mpeople were covered by the IMSS, with an estimated 15.4m affiliates payingcontributions by the end of 2000. The ISSSTE, with 2.4m affiliated stateworkers, offered services to a further 10.1m people. The two organisations arefunded by employer and employee contributions, returns on investments andin the case of the ISSSTE, transfers from federal government.

Social security the mainhealthcare provider

Mexico 17

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

In addition to the IMSS and the ISSSTE, some healthcare services are provided bythe Ministry of National Defence, the Ministry for the Navy, Petróleos Mexicanos(Pemex, the state oil company) and by state organisations such as the InstitutoNacional Indigenista (INI, the Institute for Indigenous People) and DesarrolloIntegral de la Familia (DIF, an agency promoting family development), as well asby private institutions. About 4% of the population have private medicalcoverage. Those people who are not contributors to the national social securitysystem nor members of private schemes can obtain free healthcare from eitherthe Ministry of Health or the IMSS-Solidaridad antipoverty programme.

Hospital units, 2000

Type No.

Open to allMinistry of Health 431Instituto Mexicano del Seguro Social-Solidaridad (IMSS-Solidaridad)a 69

Open to beneficiaries onlyInstituto Mexicano del Seguro Social (IMSS) 267Instituto de Seguridad y Servicios Sociales de los Trabajadores del Estado (ISSSTE) 103Petróleos Mexicanos (Pemex) 23Ministry of National Defence 42Ministry for the Navy 32

a Hospitals funded under the IMSS-Solidaridad antipoverty programme.

Source: Presidencia de la República, Sexto Informe de Gobierno.

Natural resources and the environment

Covering an area of 1.95m sq km, Mexico is the 14th largest country in theworld. It is bounded by the US to the north along a 3,118-km frontier and tothe south by Guatemala (943 km) and Belize (249 km). The country’s westernlimit is the Pacific coast (7,360 km) and its eastern limit the Gulf of Mexico andthe Caribbean coast (2,780 km).

The country’s topography is complex, ranging from coastal plains to volcanoesstanding over 5,000 metres above sea level. More than one-half of the land areais over 1,000 metres above sea level.

Climatic conditions vary considerably on account of the topography, butmuch of the country is dry and there are few large rivers. Water resources areunevenly distributed.

Climate(% of total area)

Hot & humid 4.8

Hot & dry 23.0

Temperate 23.1

Dry 28.3

Very dry 20.8

Source: Instituto Nacional de Estadística, Geografía e Informática.

Topography

Climate

18 Mexico

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Owing to topography and climate, only about 21% of the country is suitablefor arable farming and a further 57% for pasture. Forests and woodland coveraround 17% of the land. There is great potential for fishing to be developed.

As a signatory to the North American Free-Trade Agreement (NAFTA) Mexico isunder pressure to raise its environmental standards. Air pollution is a seriousproblem in Mexico City, Guadalajara and Monterrey, and northern borderareas also suffer a high degree of pollution and other environmental problems.In the 1980s the authorities became aware of the need to tackle environmentaldegradation, but the General Law of Ecological Balance and EnvironmentalProtection was not enacted until 1988. Under the administration led byErnesto Zedillo Ponce de León (1994-2000) the Ministry for Fisheries becamethe Ministry of Environment, Natural Resources and Fisheries. Amendments tothe law in 1996 delegated important enforcement functions to both state andlocal governments and introduced the concept that polluters should pay.Mr Fox has transferred the fisheries’ brief to the Ministry of Agriculture.Owners of old cars in Mexico City are required to leave their cars at home onone day each week and on two days a week during environmental emergencies.Moves are being made to substitute natural gas for diesel in power stations andindustry, and environmental policing is being stepped up generally, althoughenforcement remains lax.

Transport and communications

Private companies were offered concessions to build and to operate toll roadsunder the administration of Carlos Salinas de Gortari (1988-94). A lower thanexpected volume of traffic and economic crisis from December 1994 caused thegovernment to revoke 23 of the concessions, while also offering financialassistance to the companies involved. Some roads are to be privatised and newconcessions are to be offered under the Fox administration.

Integral port administrators were created in 1993. The administration of eachseaport was awarded by concession to an administrator, who operates port ter-minals and facilities, providing related port services. The privatisation of portadministration began in 1995 and continued under the Zedillo administration.Foreign investors may hold up to 49% equity in a port administrator and up to100% equity in ventures providing some port services.

The Salinas government managed to cut the losses of the FerrocarrilesNacionales (Ferronales, the state-owned railway company); the Zedillo admin-istration split it into regional companies and in 1997-98 transferred themanagement of most of these companies to the private sector under 50-yearconcessions. Small loss-making segments were excluded from the sale, alongwith the railway running through the Tehuantepec isthmus, owing to its pol-itical sensitivity. Three regional railway companies, Noreste, Pacífico-Norte andSureste, as well as four short lines, were under private-sector management bythe end of 2000.

Environmental standards

Road improvements

Port facilities

Railways

Land use

Mexico 19

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

The Airports Act became law in December 1995. The process of privatising thecountry’s 35 airports, which deal with 97% of total passengers, started in 1998.The airports were divided into three groups for auction according to theirgeographical location, with the addition of a special group for Mexico City. Aminority but controlling share, usually of 15%, was offered to strategicinvestors, who must include a foreign investor with experience in airport man-agement, while the rest of the shares are supposed to be offered to the publicon the stock exchange. The Airports Act permits up to 49% of investment inenterprises to be from external sources, although authorisation for a higherpercentage may be obtained from the Comisión Nacional de InversionesExtranjeras (CNIE, National Commission for Foreign Investment).

Transport and communications, 2000

Roads (km) 331,635a

Paved roads (km) 110,918a

Registered vehicles (m) 15.29b

Railway track (km) 26,622

Rail passengers (m) 0.25a

Rail freight (‘000 tonnes) 78,141b

International airports (no.) 55

Domestic airports (no.) 29

Air passengers (m) 33.86b

Air freight (‘000 tonnes) 422b

Ports (no.) 108

Port facilities (sq km) 183a

Maritime passengers (m) 8.91b

Shipping (‘000 tonnes) 241,115b

Telephone lines (‘000) 12,333

Cellular telephones (‘000) 12,119c

Internet users (‘000) 2,938

a Estimates from Presidencia de la República, Sexto Informe de Gobierno. b Figure from October2000. C Figure from September 2000.

Sources: Banco de México; Instituto Nacional de Estadística, Geografía e Informática; Secretaría de Comunicaciones y Transportes;Aeropuertos y Servicios Auxiliares; Caminos y Puentes Federales de Ingreso; Comisión Federal de Telecomunicaciones; Presidencia de laRepública, Sexto Informe de Gobierno.

In 1998-2000 three airport groups were privatised. Aeropuertos del Sureste,manager of nine airports in six states, of which Cancún is the jewel in thecrown, was the first group to be auctioned. Control was won by a consortiumwith Mexican, Danish, French and Spanish capital in December 1998. A con-sortium of Mexican and Spanish capital won the bidding to manageAeropuertos del Pacífico, a group of 12 airports, including Guadalajara andTijuana, in August 1999. Control of Aeropuertos del Centro-Norte, a group of13 airports, including those serving Acapulco and Monterrey, was won by aconsortium with Mexican and French capital in May 2000. The privatisation ofMexico City airport has been delayed because the government has still todecide on the location for a new airport, which will be either at Texcoco, nearthe existing one, or in the Tizayuca Valley in Hidalgo. The respective state

Airports

20 Mexico

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

governments have each lobbied strongly for the airport to be build in theirregions. The decision passed to the Fox administration, which will announcethe winner in the first half of 2001. The placement of 85% of shares in pri-vatised airport groups on the stock exchange has been delayed several times.Shares in the Sureste group were placed on the Mexico City and New Yorkstock exchanges in September 2000. Shares for the other airport groups mayalso be placed on those stock exchanges in 2001.

In 1990 the government privatised Teléfonos de México (Telmex), which hassince greatly expanded the telephone network. The number of telephone linesincreased by 130% between 1990 and 2000, when density rose from 6.4 linesper 100 people to 12.5 lines per 100 people. With privatisation came con-cessions for cellular telephone operations and in August 1996 the long-distancemarket was opened to competition. A total of 24 concessions were granted and19 companies had won concessions to compete against Telmex in the localtelephone service market by the end of 2000. An important agreement settlingdisputed issues such as interconnection fees was reached between Telmex andits competitors in January 2001.

Energy provision

Mexico, the world’s fifth largest oil producer in 2000, produced an average of3.5m barrels/day of crude oil and liquid gas equivalent. The country producesthree types of oil: heavy Maya, at 22.3° American Petroleum Institute (API),Isthmus (34.6° API) and Olmeca (39.1° API). Official hydrocarbons reserves atthe start of 2000 stood at 58.2bn barrels, of which 46.2bn were crude oil andcondensates, and 12bn gas equivalent. Reserves have declined steadily in thepast 15 years, reflecting a contraction in exploratory activity. About 56% ofreserves are in the Gulf of Mexico, 24% in the Chicontepec region and 15% inChiapas and Tabasco.

Oil exports did well in 1996-97 as a result of higher volumes and prices, ex-ceeding earnings of US$10bn for the first time since 1985. However, oil pricesstarted to plunge in December 1997 and remained extremely depressed, thelowest in real terms since Mexico became an important oil exporter, untilFebruary 1999. This outcome caused a negative shock as crude oil is the secondmost important export as Pemex, the state oil company, accounts for morethan one-third—34.9% in the first three quarters of 2000—of federal govern-ment revenue. Prices started to recover in February 1999 in response to astrengthening of global demand and in light of OPEC production curbs. In1999-2000 average prices were comfortably above government budget est-imates, generating substantial windfalls for the country.

Outside companies have been brought in to undertake drilling operations forPemex, although to date they have been doing so under limited service andperformance contracts, given that the constitution severely limits the circum-stances under which payment can be made to third parties. (For historical dataon oil and gas production and reserves see Reference table 4.)

Oil production

Communications

Mexico 21

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

There has been a steady reduction of the company’s monopoly over the prod-uction of petrochemicals. Modifications to the constitution in November 1996restricted the state’s exclusive production rights to only eight basic petro-chemicals. The private sector may now participate in the production of petro-chemicals other than those eight reserved for the state and may own 100% ofthe equity of a producing company, but only 49% of the equity in plantsowned by Pemex. This restriction has deterred investors and an attempt topart-privatise some complexes foundered in 1999. It is unclear what steps theFox administration will take regarding the plants.

Oil and gas production

1999/20002000 % change

Crude oil incl liquid gas (‘000 barrels/day) 3,450 3.2

Gas (m cu ft/day) 4,679 –2.3

Source: Petróleos Mexicanos.

In May 1995 Congress approved legislation permitting the private ownershipand operation of natural gas transport, storage and distribution facilities. Thelaw permitted facilities in urban areas to be auctioned from 1996, although thecorresponding permits for Mexico City were not granted until August 1998. Anopen access policy on Pemex’s pipelines was also implemented from 1996. Theprocess has continued in 1999-2000.

Energy balance, 1999(m tonnes oil equivalent)

Oil Gas Coal Electricity Other Total

Primary supplyPrimary production 169.5 31.6 4.7 10.7a 8.2 224.7Imports 15.5 1.7 1.3 0.1a 0.0 18.6Exports –89.5 –1.4 0.0 0.0a 0.0 –90.9Total 95.5 31.9 6.0 10.8a 8.2 152.4Output basis – – – 4.2 – 145.8

Processing & transformationInput to refining –70.0 0.0 0.0 0.0 0.0 –70.0 Input to transformation –22.5 –6.1 –4.0 –10.8a 0.0 –43.4 Refining & transformation output 70.0 0.0 0.0 16.8b 0.0 86.8 Energy industry fuel & losses –10.5 –11.2 0.0 –3.6b 0.0 –25.3

Final consumptionTransport fuels 37.0 0.0 0.0 0.1b 0.0 37.1 Industrial fuels 8.5 12.6 2.0 8.1b 2.3 33.5 Residential & other uses 12.0 0.8 0.0 5.0b 5.9 23.7 Non-energy uses 5.0 1.2 0.0 0.0 0.0 6.2 Total 62.5 14.6 2.0 13.2b 8.2 100.5

a Input equivalents on an assumed generating efficiency of 38.5%.

Source: Energy Data Associates.

Pemex and thepetrochemical industry

Natural gas

22 Mexico

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

The economy

Economic structure

In the past two decades the services sector has accounted consistently foraround two-thirds of GDP, while industry has accounted for between 25% and30%. In January-September 2000 services accounted for 67.8% of GDP, withcommunity and social services representing 21.4% of GDP, financial services13% and transport and communications 11.4%. Industry generated 26.8% ofGDP. Manufacturing dominates industrial production, accounting for 20.8% ofGDP, followed by construction, with 4.8%. Manufacturing is not only the mostimportant productive sector, but is also the main source of exports. Manu-facturing accounted for 87.3% of total exports in 2000. One-half of that totalwas produced in maquiladoras (in-bond assembly plants).

Main economic indicators, 2000

Real GDP growth (%; based on constant 1993 prices) 6.9

Consumer price inflation (year-end; %) 9.0

Current-account balance (US$ bn) 18.2a

External debt (US$ bn) 171.5a

Exchange rate (av; Ps:US$) 9.46

Population (m) 97.4b

a EIU estimate. b Preliminary estimate from the 2000 census.

Sources: Banco de México; Consejo Nacional de Población.

Agriculture accounted for 4.2% of GDP in the first nine months of 2000,employing about 23% of the total workforce. Mining accounted for just 1.2%of GDP, a proportion that heavily understates the importance of oil productionto the economy, particularly in terms of government revenue. After therecovery in oil prices in 1999-2000, oil exports represented 7.3% of totalexports in the first three quarters of 2000 and 9.8% of total exports for the yearas a whole. Oil-related government revenue as a percentage of total govern-ment revenue in 1999-2000 reached 32.5% in the first three quarters of 2000and 34.9% for the year as a whole.

The results of the first systematic attempt to measure informal economic activ-ities were published by the Instituto Nacional de Estadística, Geografía eInformática (INEGI, the National Institute of Statistics, Geography andInformatics) in August 2000. According to the results, the informal sector—excluding illegal activities—had a value of Ps445.5bn (US$47bn), equivalent to12.7% of GDP, and provided 17% of the profits generated by the economy. Ofnon-agricultural jobs, 28.5% of the total are in the informal sector. Commerceand restaurants employ the greatest number of workers informally, estimatedat around 30.8% of the total, followed by personal services (11.5%), manu-facturing (6.1%), transportation (4.6%) and construction (3.3%).

Services sector dominatesGDP

Mexico 23

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Although much of the growth in external trade is largely attributable to thedynamism of the maquiladora (in-bond assembly for re-export) industry, therate of increase has been impressive. The collapse in domestic demand in 1995forced producers to redirect their production to overseas markets, an outcomefacilitated by the North American Free-Trade Agreement (NAFTA), whichprovided privileged access to markets in the US and Canada, both of whichcountries experienced strong sustained growth in the second half of the 1990s.Combined exports and imports soared, from US$117bn in 1993 to US$341bnin 2000.

Comparative economic indicators, 2000(US$ bn unless otherwise stated)

Mexico US Brazil Argentina Venezuela

GDP 561.2 9,966.0 622.4 281.7 103.8

GDP per head (US$) 5,763 36,165 3,751 7,605 4,293

Consumer price inflation (av; %) 9.5 3.4 7.0 –0.9 16.2

Current-account balance –18.2 –437.6 –25.5 –11.2 12.9 % of GDP –3.2 –4.4 –4.1 –4.0 12.5

Exports of goods fob 166.4 775.9 55.1 26.3 34.0

Imports of goods fob –174.5 –1,222.8 –55.8 –24.4 –16.1

External debt 171.5 n/a 235.5 153.1 34.1

Debt-service ratio, paid (%) 23.1 n/a 64.8 75.6 17.4

Source: EIU CountryData.

Economic policy

Under the presidency of Carlos Salinas de Gortari (1988-94) the economy wasmodernised and opened to market forces, and the role of the state was reduced.Many economic activities were deregulated and the number of state-ownedenterprises fell from 1,155 in 1982 to 412 in 1988 and further, to 215, in 1994.The process of trade liberalisation begun by Mr Salinas’s predecessor, Miguel dela Madrid, was consolidated and enhanced by free-trade pacts, notably NAFTA,and foreign investment rules were made more attractive.

The Salinas government was successful in reducing the rate of inflation from52% in 1988 to 7% in 1994 through the use of a pegged exchange rate. Thegovernment also exploited the Partido Revolucionario Institucional’s (PRI)corporatist structure to extract concessions from the main labour unions andpeasant and business organisations on fiscal cuts and wages restraint in theform of an incomes policy known as the pacto. A public-sector borrowingrequirement of 12.5% of GDP in 1988 was turned into a surplus of 0.5% ofGDP by 1992, or 3.2% if privatisation revenue is included, although there wassome fiscal relaxation in 1992-94. Lower inflation led to lower interest rates,which in turn helped the fiscal accounts by lowering the cost of domestic debtservice. (For details of public-sector finances see Reference tables 5 and 6.)

A reduction in interest rates was also assisted by liberalisation of the financialmarkets, specifically the lifting of interest-rate controls and the gradual phasingout of cash reserve requirements. In 1991-92 the government privatised its 18

Integration with worldeconomy deepens

Mr Salinas liberaliseseconomic policy

24 Mexico

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

commercial banks and in 1993 allowed new domestic banks to be established.In 1994 market access was granted to foreign banks, albeit only those operatingin the US and Canada, the object being to improve the availability of creditand to drive intermediation margins down through competition. In April 1994the Banco de México (the central bank) became independent. However, theMinistry of Finance retained control of exchange-rate policy, creating apossible source of conflict. A proposal put to Congress in 1998 by the pres-ident, Ernesto Zedillo Ponce de León, to give the central bank full control ofexchange-rate policy was never passed. (For historical data on money, creditand interest rates see Reference tables 7 and 8.)

The exchange rate was unified in November 1991 and exchange controls wereabolished. The existing policy of a daily depreciation was retained, although itapplied only to the ceiling of the band in which the peso was allowed to float,a condition that allowed the real exchange rate to appreciate steadily under theSalinas administration. The government stuck resolutely to its exchange-ratepolicy even though overvaluation, trade liberalisation and economic growthproduced ever wider trade and current-account deficits. The administrationargued that the size of the current-account deficit was unimportant since itreflected dynamism in the private sector and that if capital were to cease toflow into the economy, the current account would adjust accordingly. In 1994the government rolled over domestic debt by issuing US$29.2bn of Tesobonos(US dollar-dominated bonds) to try to halt a loss of reserves. Investors becameincreasingly skittish as the euphoria that had built up about Mexico’seconomic prospects dissipated when political shocks struck in an election year.Eventually the exchange-rate policy ceased to be tenable. (For historical dataon the exchange rate see Reference table 30.)

On December 20th 1994, only three weeks into its term, the Zedillo govern-ment devalued by lifting the exchange-band ceiling by 15%. Billions of USdollars left the country in a few hours. With reserves depleted, the peso wasfloated, but it remained under speculative attack. From P3.107:US$1 at thebeginning of 1994, the peso had fallen to Ps5.325:US$1 by year-end. The pesocontinued to plunge in the first few weeks of 1995 as economic agents feared—correctly as it turned out—that the government lacked the resources to fundpayment of US$29bn of Tesobonos falling due in 1995. The solvency of thebanking system became another cause for concern. Banks faced a huge increasein external debt-servicing costs as a result of the devaluation as well as anescalation of bad debts as the government forced interest rates up to try to keepforeign and domestic capital in the country. In January 1995 the governmentagreed an emergency economic plan with labour and business comprisingtighter fiscal and monetary policy, and wages restraint. On the strength of thisplan the US contributed US$20bn, the Bank for International SettlementsUS$10bn and the IMF a total of US$17.8bn. However, the plan failed to restoreinvestor confidence and in March the government was forced to redouble itsadjustment efforts. The rate of value-added tax (VAT) was raised from 10% to15%, government-set prices were increased, public spending was cut and atight lid was kept on wage rises. Despite a contraction of 6.2% in GDP, a non-financial public-sector (NFPS) surplus of 0.7% of GDP was achieved, an

Exchange-rate policyproves to be flawed

Zedillo government forcedto devalue

Mexico 25

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

improvement on the previous year’s public-sector borrowing requirement(PSBR) of 3.4% of GDP. The PSRB included only a fraction of the cost of thebank bail-out. At the end of 2000 that cost, which will be absorbed eventuallyas internal public debt or written down over a 30-year period, was equivalentto 12.9% of GDP.

The government adhered to its policy of fiscal and monetary prudence in 1996.Inflation was nearly halved, from 52% at the end of 1995 to 27.7% at the endof 1996. Public finances almost reached balance, with the NFPS posting adeficit of just 0.1% of GDP. Discretionary spending had to be tightly controlledto compensate for the rising cost of supporting the banking system and fordefaults on tax payments. The central bank maintained its restrictive targets formonetary growth.

Although the government seemed to consider the free-floating peso as a trans-itional phase, over time confidence and reserves were restored and exchange-rate volatility gave way to extended periods in which the peso remainedrelatively stable. The inflation target for 1997 of 15% was almost achieved. Thepublic finances registered a deficit in 1997 slightly above the goal of 0.5% ofGDP. The deficit included costs related to reform of the social security systemincurred in the second half of the year,

The main feature of the new pensions system is that a worker’s pensionbenefits depends on the contributions made to his individual pension account.The accounts are managed by an administradora de fondos para el retiro (Afore, aretirement fund administrator) of the contributor’s choosing. In 1997 17Afores, most of them allied with foreign companies, started operation.

In 1998 the volatility of the peso increased markedly. Oil prices collapsed andMexico was also affected by the general loss of confidence in emerging marketsin the wake of the crisis in south-east Asia. The central bank tightenedmonetary policy several times during the year by restricting liquidity in themoney market. The government also tightened fiscal policy through three bud-get cuts totalling Ps36.2bn (US$4bn), equivalent to 1% of GDP, implementedin January, March and July respectively. Despite tight money and governmentspending cuts, the economy managed to grow by 4.9% in 1998, althoughmomentum was lost by the end of the year. At 1.25% of GDP, the NFPS deficitclosed precisely on target. However, the downward trend of inflation wasbroken and ended 1998 at 18.6%, well above the original target of 12%.

Although the peso was affected by the devaluation of the Brazilian Real inJanuary 1999, it quickly recovered and even regained some of the ground lostafter the Russian devaluation in 1998. Investors began to believe the gov-ernment’s repeated claims that Mexico was fundamentally stronger than otheremerging markets. The peso remained stable throughout the rest of 1999 as thegovernment managed to keep the fiscal accounts under control, aided by risingoil prices and a diminishing trade-account deficit. Inflation ended the year at12.3%, below the official target of 13%, but economic growth of 3.8%surpassed the 3% target. Both goals had been considered optimistic by privateanalysts at the beginning of 1999.

Little scope for relaxationin 1996

Mexico shows strongfundamentals in 1999-2000

26 Mexico

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

The peso remained remarkably stable in 2000, despite the political uncertaintygenerated by the presidential campaign, and was again bolstered by high oilprices and strong exports, although the trade deficit started to climb from Mayonwards. The central bank criticised what it considered to be the government’soverly loose fiscal policy, although the deficit was kept under control on theback of higher oil-related receipts and higher tax revenue as a result ofexceptionally strong economic growth.

Although he was unable to implement radical changes in 2000 because of anunco-operative Congress, Mr Zedillo did achieve his central aim for the year ofending the cycle of economic crises that coincided with changes of govern-ment. The inflation rate, which at 9% again fell short of the stated target, thistime of 10%, was the lowest annual rate since December 1994. At 6.9% realeconomic growth reached its highest level since 1981, outstripping the mostoptimistic expectations.

Orthodox economic policies, discredited by the 1994-95 crisis, regained publicsupport during the recovery and no major party is proposing a crediblealternative. The president, Vicente Fox Quesada, signalled his commitment tosound public finances with the appointment of a respected technocrat,Francisco Gil Díaz, as minister for finance and public credit. Although adivided Congress represents a potential problem for policymaking, the govern-ment has shown good negotiating skills to date. In a political first, the 2001budget was approved unanimously, with the government making only smallconcessions to Congress. The opposition, mainly the centre-left PartidoRevolucionario Institucional (PRI) and the left-wing Partido de la RevoluciónDemocrática (PRD), are unlikely to approve important structural changeswithout significant concessions.

Economic performance

In 1992 the delayed effects of recession in the US, together with an overvaluedpeso, held real growth of exports of goods and services to 5%, while imports ofgoods and services increased by 19.6% in real terms. The deterioration in thenet external balance was mainly responsible for a slowdown in GDP growth, to3.6%. In 1993 the arrival of a US new administration led by Bill Clintonbrought uncertainty with respect to the approval of NAFTA that exerted up-ward pressure on domestic interest rates and exacerbated the problem ofgrowing bad debts. Following a recovery in the US and slack domestic demand,exports grew by 8.1% in real terms and imports by 1.9%, while GDP growthstood at 1.9%. In 1994, an election year, public consumption grew by 2.9%and public investment by a similar amount. NAFTA helped to revive privateinvestment, which rose by 9.8% despite political upheavals, and to boostexports, which grew by 17.8% in real terms. A recovery in domestic demandboosted imports again, limiting GDP growth to 4.5%. (For historical data onGDP see Reference tables 9-11.)

The financial crisis at the end of 1994 had a profound effect on the economyin 1995. High real interest rates, tight monetary policy and the loss of businessconfidence choked off private investment. Large fiscal cuts precipitated sharp

Uneven growth in 1992-94

Recession follows in 1995

Mexico 27

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

falls in public investment and spending. In August the official and very narrowmeasure of open urban unemployment reached 7.6%, before falling to 5.2% inDecember, well above the 3.2% recorded at the end of 1994. Inflation, fuelledby the weakness of the peso, eroded wages, while private consumption col-lapsed. GDP contracted by 6.2% in the worst recession experienced by thecountry since the Great Depression of the 1930s. The only positive develop-ments were in the external sector, where a surge in exports was accompaniedby a fall in imports. An increase in exports helped to lift the economy out ofrecession in 1996. Private consumption was held back by declining real wagesand stubbornly high levels of unemployment. At the same time a huge debtoverhang depressed both private consumption and investment, and there wasa credit crunch as domestic banks struggled to deal with non-performing loansand to build up both capital and reserves. Inflation fell from 52% in December1995 to 27.7% at the end of 1996.

Gross domestic product(annual av; % real change; constant 1993 prices)

1990-95 1996 1997 1998 1999 2000a

Private consumption 2.1 2.2 6.5 5.4 4.3 9.7

Government consumption 2.5 –0.7 2.9 2.2 1.0 5.0

Gross fixed investment 2.0 16.4 21.0 10.3 5.8 10.7

Exports of goods & services 8.2 18.2 10.7 12.1 13.9 16.4

Imports of goods & services 11.9 22.8 22.7 16.5 12.8 22.8

GDP at market prices 2.2 5.2 6.8 4.8 3.7 7.1b

a Preliminary estimates from the Banco de México (the central bank). b The most recent globalestimate is 6.9%.

Sources: Instituto Nacional de Estadística, Geografía e Informática; Banco de México.