metso annual review 2005 - ku leuven · metso minerals, inventories grew and receivables increased,...

TRANSCRIPT

Annual Review 2005

Sustainability Report 2005Annual Review 2005 Financial Statements 2005

For further information, visit www.metso.com

A n n uA l R e v i e w

– i ntro duc tion

– Strategy

– Business areas

– i nvestor information

F i n A n c i A l S tAt e m e n t S

– Financial statements and notes

– Shares and shareholders

S u S tA i n A B i l i t y R e p o R t

– m etso and sustainable development

– economic resp onsibi l it y

– S o cial resp onsibi l it y

– environmental resp onsibi l it y

Metso is a global engineering and technology corporation with 2005 net sales of approximately EUR 4.2 billion. Its 22,000 employees in more than 50 countries serve customers in the pulp and paper industry, rock and minerals processing, the energy industry and selected other industries.

Metso’s Annual Reports 2005

Table of Contents

i n t r o d u c t i o n

METSO CORPORATION 2–3

FINANCIAL PERFORMANCE IN 2005 4–5

s t r a t e g y

FROM THE CEO 6–7

VISION AND STRATEGY 8–9

FINANCIAL TARGETS 10–11

VALUES AND ETHICAL PRINCIPLES 12–13

OPERATING ENVIRONMENT 14–19

RISKS AND RISK MANAGEMENT 20–25

b u s i n e s s a r e a s

METSO PAPER 28–35

METSO MINERALS 36–43

METSO AUTOMATION 44–49

METSO VENTURES 50–53

i n v e s t o r i n f o r m a t i o n

CORPORATE GOVERNANCE 56–61

BOARD OF DIREC TORS 62–63

EXECUTIVE TEAM 64–65

STOCK EXCHANGE RELEASES AND ANNOUNCEMENTS IN 2005 66

INVESTOR RELATIONS 67–69

INFORMATION TO SHAREHOLDERS 70–71

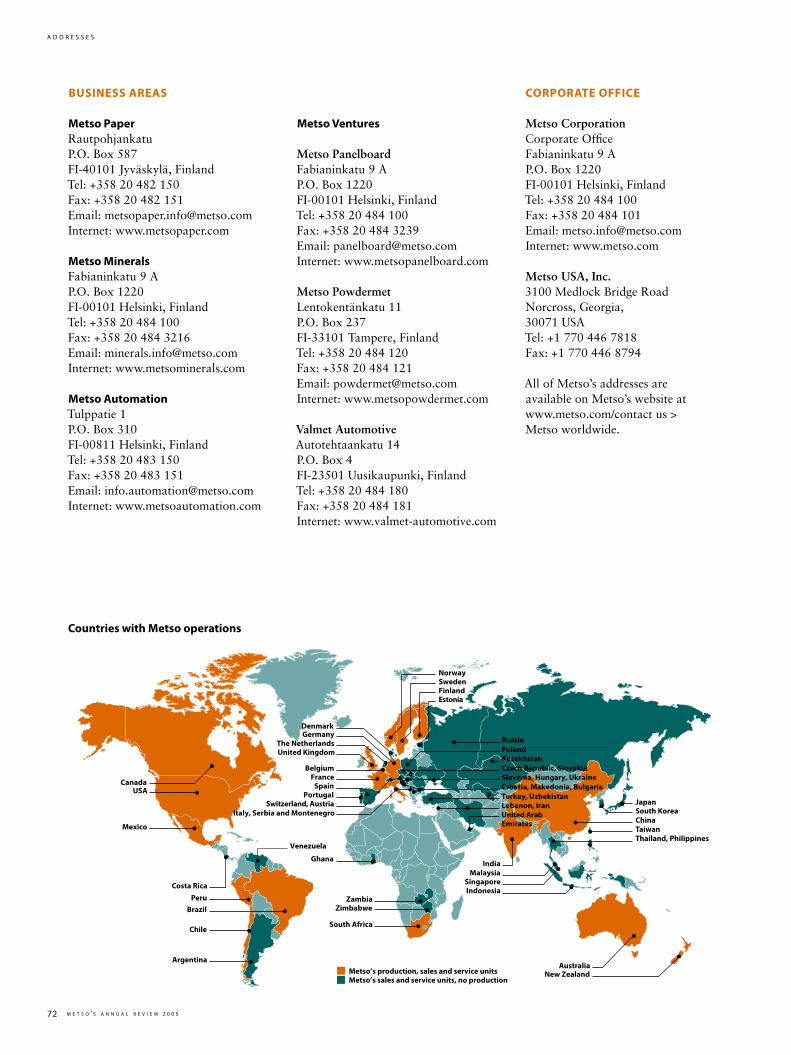

ADDRESSES 72

M E T S O ’ S A N N U A L R E V I E w 2 0 0 5 1

Metso CorporationMetso is an international engineering and technology corporation that serves customers in the pulp and paper industry, rock and minerals processing, energy industry and other selected industrial sectors. Metso Corporation comprises four business areas: Metso Paper, Metso Minerals, Metso Automation and Metso Ventures.

In 2005, Metso Corporation’s net sales totaled some eur 4.2 billion. Metso has business operations in over 50 countries, and some 22,000 employees.

Metso has production on all continents. The main market areas are Europe and North America, which account for some 60 percent of net sales. However, Asia and South America are becoming increasingly important.

Metso is listed on the Helsinki and New York stock exchanges.

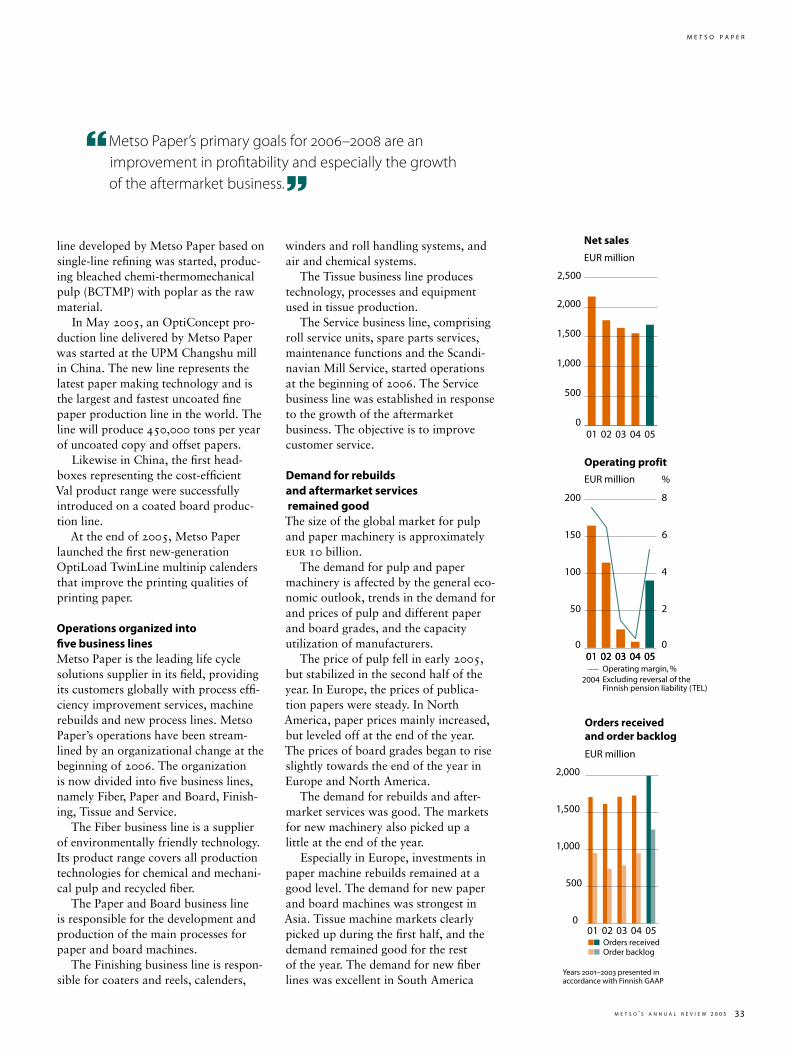

metSo pApeR

net SAleS in 2005� – eur 1,702 million

peRSonnel, DecemBeR 31, 2005� – 8,201

pRoDuctS AnD SeRviceS – Equipment and machinery for mechanical and chemical pulp production, paper machines, tissue machines, board machines, paper finishing systems, and knowhow, maintenance and aftermarket services

cuStomeRS – Mechanical and chemical pulp makers, and paper, tissue and board producers

mARket poSition – Global market leader of papermaking lines, and one of the leading suppliers of boardmaking machines and pulping lines

tARget mARket – approximately eur 10 billion

lARgeSt mARket AReAS – Europe, North America and Asia

mAin competitoRS – Voith Paper from Germany, Andritz from Austria and Mitsubishi from Japan

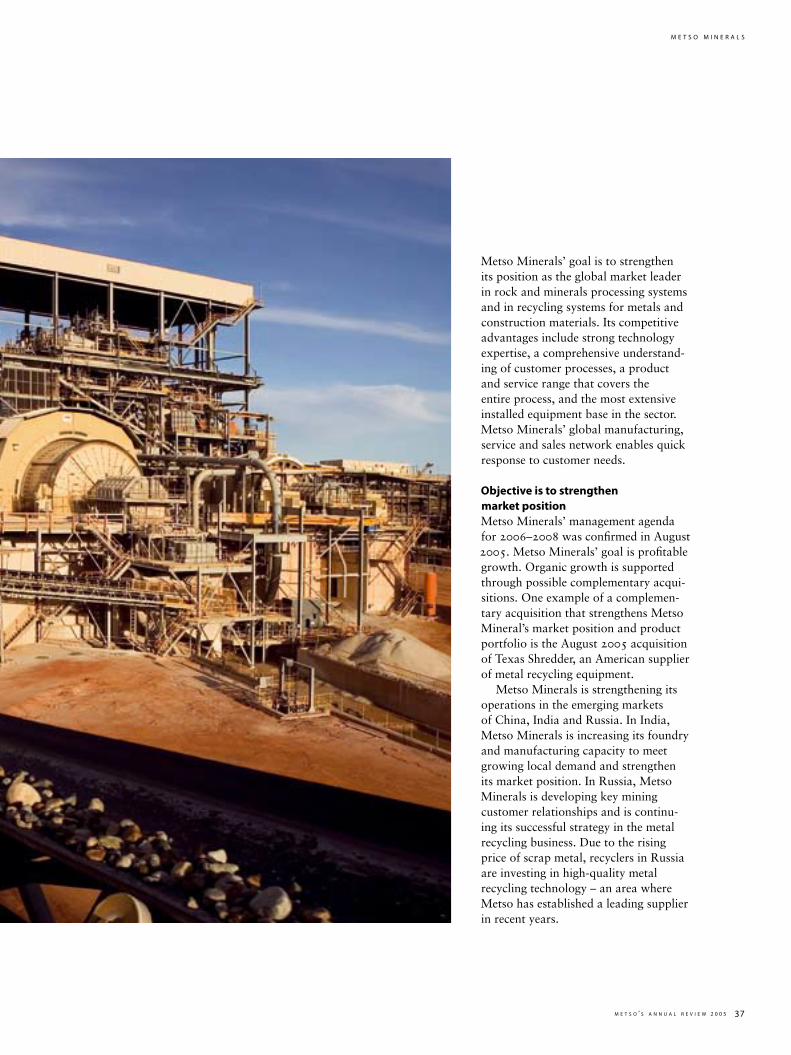

metSo mineRAlS

net SAleS in 2005� – eur 1,735 million

peRSonnel, DecemBeR 31, 2005� – 8,521

pRoDuctS AnD SeRviceS – Rock and minerals processing systems, crushers, screens and conveyors, mobile crushing and screening equipment, grinding mills, separation equipment for minerals, recycling systems for metals, wear protection products and conveyor belts, wear and spare parts and aftermarket services

cuStomeRS – Mining, quarries and contractors, civil engineering and construction, and recycling of metals and construction materials

mARket poSition – Global market leader in rock and minerals processing systems and recycling systems for metals and construction materials

tARget mARket – approximately eur 12 billion

lARgeSt mARket AReAS – Europe and North America; South America and Asia are increasingly important

mAin competitoRS – Terex and Astec from the USA, Sandvik from Sweden, Krupp Polysius from Germany, FLSmidth from Denmark and Outokumpu Technology from Finland

2 M E T S O ’ S A N N U A L R E V I E w 2 0 0 5

Net sales by business area

Metso Paper 39%[2004: 42%]

Metso Minerals 40%[2004: 37%]

Metso Automation 14%[2004: 15%]

Metso Ventures 7%[2004: 6%]

Finland 8% [2004: 9%]

Other Nordic countries 12% [2004: 8%]

Other European countries 25% [2004: 25%]

North America 21% [2004: 21%]

South and Central America 12% [2004: 8%]

Asia-Pacific 17% [2004: 23%]

Rest of the world 5% [2004: 6%]

Net sales by market area

Personnel by business area

Metso Paper 37%[2004: 40%]

Metso Minerals 39%[2004: 37%]

Metso Automation 14%[2004: 15%]

Metso Ventures 9%[2004: 7%]

Corporate Office and Shared Services 1%[2004: 1%]

metSo AutomAtion

net SAleS in 2005� – eur 584 million

peRSonnel, DecemBeR 31, 2005� – 3,169

pRoDuctS AnD SeRviceS – Process industry automation and information management application networks and systems, production process measurement systems and equipment, control valves, and support and maintenance services

cuStomeRS Mechanical and chemical pulp makers, paper and board producers, and the energy, oil and gas industries

mARket poSition – Global market leader of special catalytic equipment, consistency transmitters and control and automated valves, thirdlargest supplier of automation solutions for the pulp and paper industry, and one of the largest European suppliers of power plant automation

tARget mARket – approximately eur 10 billion

lARgeSt mARket AReAS – Europe and North America

mAin competitoRS – ABB from Switzerland, Emerson, Honeywell and Flowserve from the USA, Invensys from the UK and Siemens from Germany For further information,

visit www.metso.com

metSo ventuReS

net SAleS in 2005� – eur 284 million

peRSonnel, DecemBeR 31, 2005� – 1,993

The business area comprises four business groups: Metso Panelboard, Metso Powdermet, Foundries and Valmet Automotive

pRoDuctS – Production lines, equipment and aftermarket services for the panelboard industry, industrial castings, material technology expert services, and the contract manufacture of specialty cars

cuStomeRS – Construction and furniture industries, producers of packaging material, paper and board producers, rock and minerals processing, the engineering industry, and car makers

mARket poSition – Metso Panelboard is among the three largest equipment suppliers for the panelboard industry in the world. Valmet Automotive is one of Europe’s leading contract manufacturers of specialty cars n

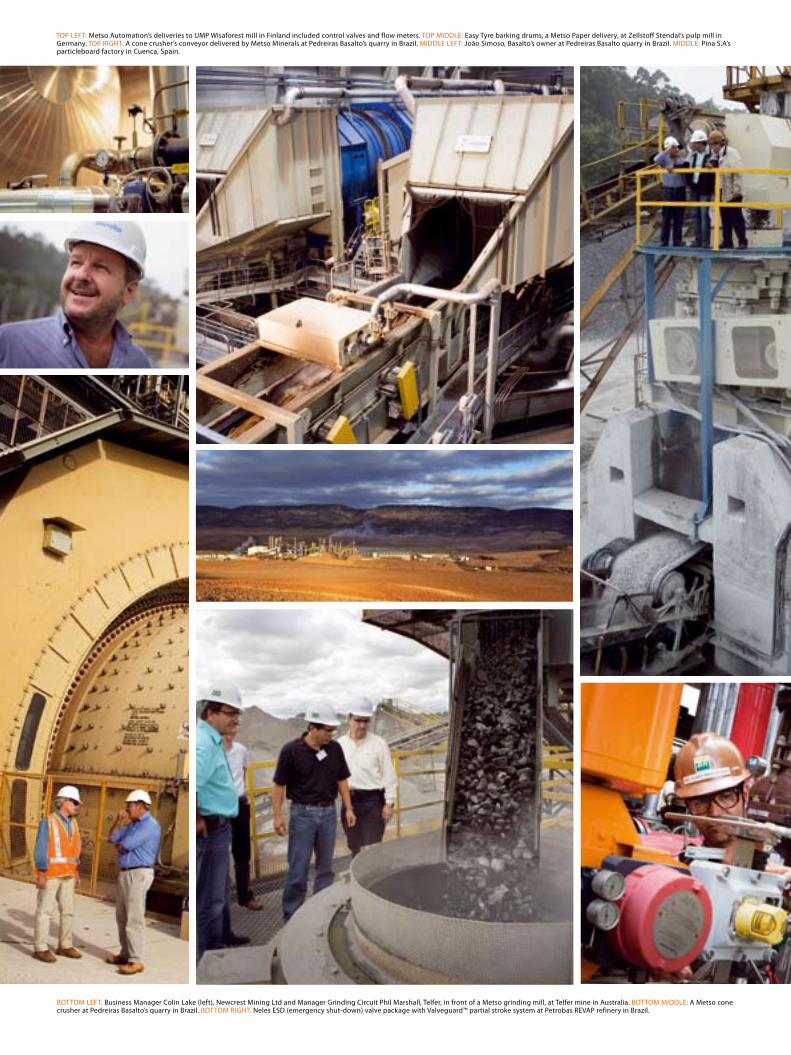

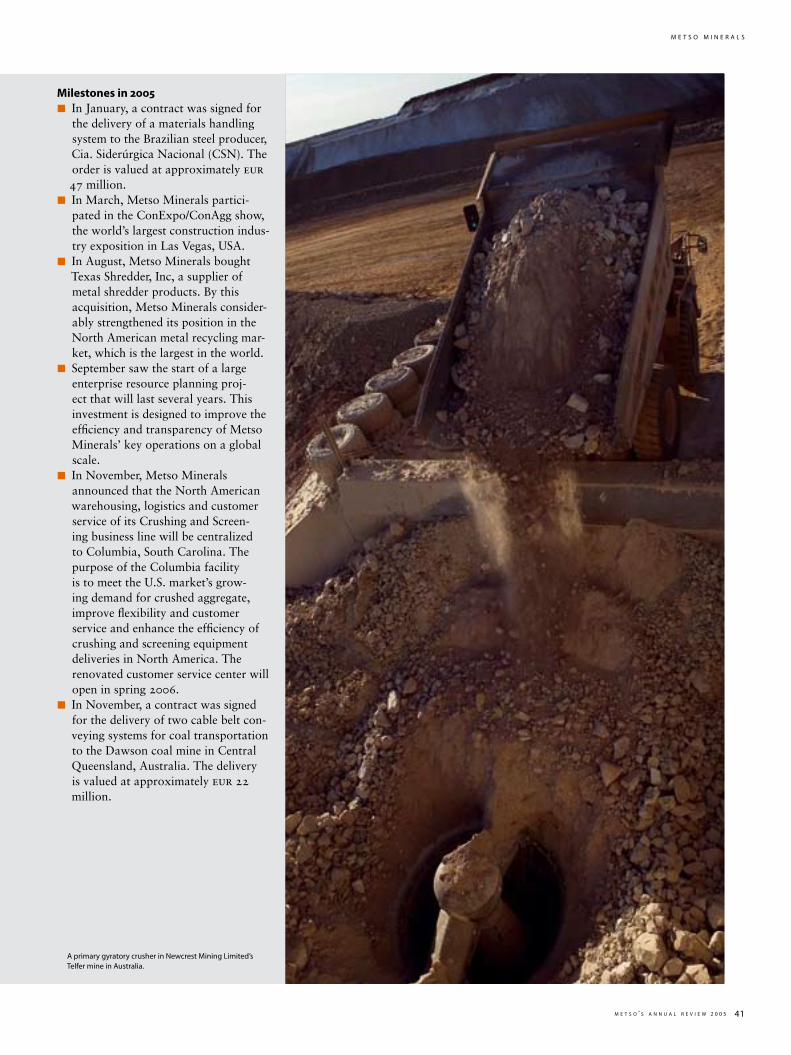

METSO PAPER: The PM2 paper machine at SP Newsprint’s Dublin mill in Georgia, USA. The machine produces high-quality newsprint from recycled fiber.METSO MINERALS: Paul Bernhardt, who is in charge of Metso Minerals’ service operations at Newcrest Mining Limited’s Telfer mine in Australia.METSO AUTOMATION: Petrobras’ Technical Assistant Rui Nunes Mascarenhas (left) and Metso Automation’s Process and Energy Automation Maintenance Technician Isaias do Espírito Santo at the Petrobras oil refinery in Brazil.METSO VENTURES: Mill Manager Manuel Casáis (left) and Metso Panelboard’s Sales Manager Berbado Alvarez de Prado (right) taking part in a conversation at Pina S.A. particleboard mill in Cuenca, Spain.

M E T S O ’ S A N N U A L R E V I E w 2 0 0 5 3

M E T S O C O R P O R A T I O N

Financial performance in 2005

order backlog bolstered by 38 percent n The demand for Metso’s products

remained good in 2005 in the mining, civil engineering, energy and oil industries and improved during the year also in the pulp and paper industry. Orders received increased by 19 percent, with the strongest growth being in Metso Minerals and Metso Paper. Metso’s order backlog was 38 percent stronger than one year earlier.

net sales increased by 17 percentn Metso’s net sales grew by 17 percent,

and this growth was almost entirely organic. It was due to the good market situation, improved competitiveness and the increasingly strong focus on customer orientation after the restructuring.

n Deliveries increased in all business areas. Growth was strongest at Metso Minerals (27%). The relative share of the aftermarket business decreased slightly, as project and equipment deliveries increased substantially. In terms of euros, the volume of the aftermarket business grew by 11 percent.

greater efficiency and a stream-lined cost structure as plannedn The improvement of Metso’s

profitability is due not only to a more active market, but also to the significant efficiency improvement programs and business restructuring of recent years, which have helped to streamline the cost structure altogether by nearly eur 150 million annually.

n The first efficiency improvement program, the Corporationwide M100 commenced in 2003, was completed at the end of 2004. The program’s

savings of eur 100 million materialized in 2005 results.

n The MP50 program, which was started in September 2004, aimed at renewing Metso Paper’s business model and streamlining its cost structure. The program was concluded in 2005. The measures carried out under the program in 2005 were mainly targeted at improving the profitability of the Tissue business line. The annual savings generated by the program are estimated at more than eur 43 million. Three quarters of these materialized already in 2005.

n Thanks to the efficiency improvement measures, outsourcing and the development of the subcontractor network, Metso’s cost structure is today more competitive and flexible. Consequently, profit performance is on a more sustainable basis. The streamlined cost structure helps to better withstand business cycle variations.

Substantial profit improvementn The Corporation’s operating profit

improved substantially to eur 335 million. The improvement in operating profit was due to increased delivery volumes, a streamlined cost structure and improved productivity. The operating margin was 7.9 percent, clearly exceeding the 6 percent target set for 2005. Apart from Metso Ventures, all business areas achieved their operating profit targets.

n Profit from continuing operations before taxes was eur 292 million. The Corporation’s tax rate was low (24.6%). With the result of Metso’s U.S. operations turning clearly positive, Metso was able to utilize tax losscarry forwards from prior years, for which Metso has not recognized

any deferred tax assets. The tax rate is expected to be below the regular level also in 2006–2007.

n The profit attributable to equity shareholders, i.e. the profit for the financial year, was eur 236 million, and earnings per share were eur 1.69. The return on capital employed (ROCE) was 18.8 percent, which clearly exceeded the target of 12 percent set for 2005. Return on equity (ROE) was 20.9 percent.

gearing decreased furthern Metso Corporation’s cash flow from

operations decreased to eur 164 million, as the growth in net sales increased net working capital, particularly in Metso Minerals. At Metso Minerals, inventories grew and receivables increased, but the turnover of net working capital remained on par with the previous year. A total of eur 170 million was tied up in net working capital in the Corporation.

n Metso’s gross capital expenditure was eur 107 million. Free cash flow was eur 106 million. At the end of the year, the liquid assets totaled almost eur 500 million. Investments (excluding acquisitions) in 2006 are estimated at approx. eur 120 million.

n Net interestbearing liabilities decreased and were eur 289 million at the end of the year. eur 93 million in bonds and other loans were prematurely repaid during the year.

n Gearing, i.e. the ratio of net interest bearing liabilities to shareholders’ equity, decreased further to 22.4 percent. Shareholders’ equity increased, as a result of both the improved profit performance and a capital increase of eur 72 million arising from stock option programs.

In June 2004, Metso’s management focus was set on the improvement of profitability and the strengthening of the balance sheet. The efficiency improvement programs were completed in 2005, and the restructuring measures began to generate results, which were reflected in a clear improvement in profitability. As a result of these positive developments, Metso’s management focus has shifted towards profitable growth.

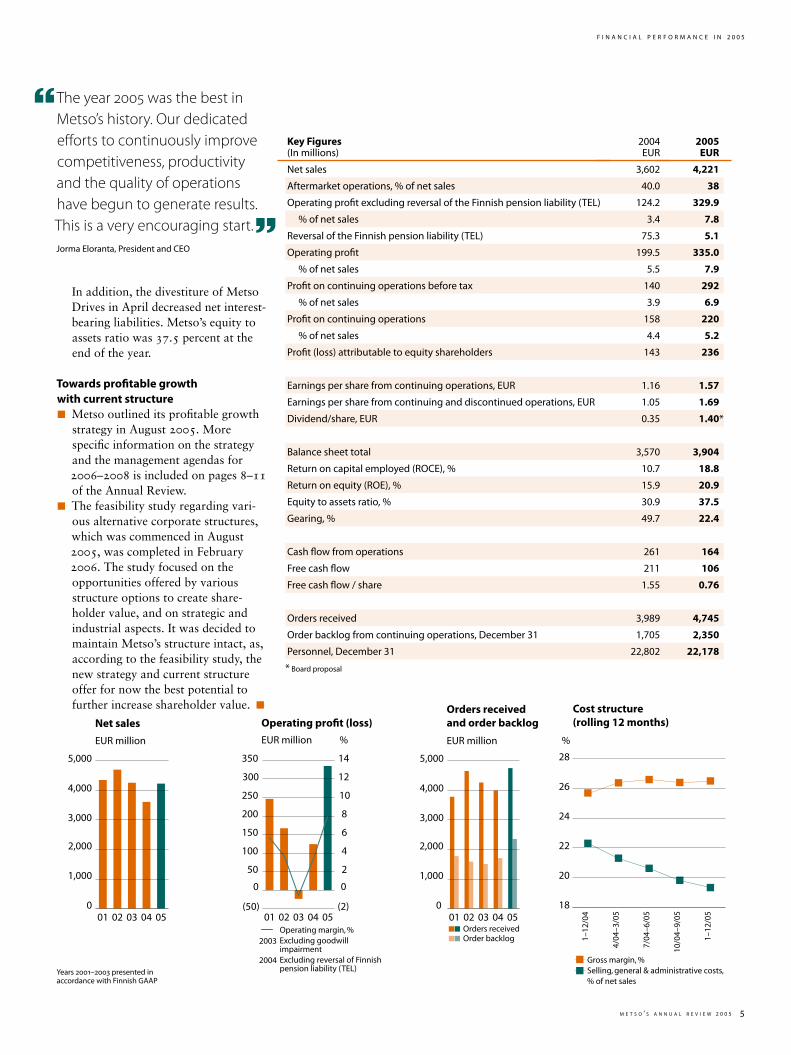

4 M E T S O ’ S A N N U A L R E V I E w 2 0 0 5

F I N A N C I A L P E R F O R M A N C E I N 2 0 0 5

(50)

0

50

100

150

200

250

300

350

0504030201(2)

0

2

4

6

8

10

12

14

Operating profit (loss)

EUR million %

Operating margin, %Excluding goodwillimpairmentExcluding reversal of Finnish pension liability (TEL)

2003

2004

0

1,000

2,000

3,000

4,000

5,000

0504030201Orders receivedOrder backlog

Orders received and order backlog

EUR million

0

1,000

2,000

3,000

4,000

5,000

0504030201

Net salesEUR million

Years 2001–2003 presented in accordance with Finnish GAAP

18

20

22

24

26

28

1–12

/05

10/0

4–9/

05

7/04

–6/0

5

4/04

–3/0

5

1–12

/04

%

Cost structure(rolling 12 months)

Gross margin, % Selling, general & administrative costs, % of net sales

Key Figures (In millions)

2004 EUR

2005 euR

Net sales 3,602 4,221

Aftermarket operations, % of net sales 40.0 38

Operating profit excluding reversal of the Finnish pension liability (TEL) 124.2 329.9

% of net sales 3.4 7.8

Reversal of the Finnish pension liability (TEL) 75.3 5.1

Operating profit 199.5 335.0

% of net sales 5.5 7.9

Profit on continuing operations before tax 140 292

% of net sales 3.9 6.9

Profit on continuing operations 158 220

% of net sales 4.4 5.2

Profit (loss) attributable to equity shareholders 143 236

Earnings per share from continuing operations, EUR 1.16 1.57

Earnings per share from continuing and discontinued operations, EUR 1.05 1.69

Dividend/share, EUR 0.35 1.40*

Balance sheet total 3,570 3,904

Return on capital employed (ROCE), % 10.7 18.8

Return on equity (ROE), % 15.9 20.9

Equity to assets ratio, % 30.9 37.5

Gearing, % 49.7 22.4

Cash flow from operations 261 164

Free cash flow 211 106

Free cash flow / share 1.55 0.76

Orders received 3,989 4,745

Order backlog from continuing operations, December 31 1,705 2,350

Personnel, December 31 22,802 22,178

* Board proposal

In addition, the divestiture of Metso Drives in April decreased net interest bearing liabilities. Metso’s equity to assets ratio was 37.5 percent at the end of the year.

towards profitable growth with current structure n Metso outlined its profitable growth

strategy in August 2005. More specific information on the strategy and the management agendas for 2006–2008 is included on pages 8–11 of the Annual Review.

n The feasibility study regarding various alternative corporate structures, which was commenced in August 2005, was completed in February 2006. The study focused on the opportunities offered by various structure options to create shareholder value, and on strategic and industrial aspects. It was decided to maintain Metso’s structure intact, as, according to the feasibility study, the new strategy and current structure offer for now the best potential to further increase shareholder value. n

“�The year 2005 was the best in Metso’s history. Our dedicated efforts to continuously improve competitiveness, productivity and the quality of operations have begun to generate results. This is a very encouraging start.”�Jorma Eloranta, President and CEO

M E T S O ’ S A N N U A L R E V I E w 2 0 0 5 5

F I N A N C I A L P E R F O R M A N C E I N 2 0 0 5

6 M E T S O ’ S A N N U A L R E V I E w 2 0 0 5

F R O M T H E C E O

Dear shareholder,2005 was a successful year for Metso. We strengthened our position as the global market and technology leader in several of our main products, both in our traditional markets as well as in emerging markets.

The efficiency improvement measures made in previous years and the good market situation also carried our profitability to a significantly improved level. Metso’s balance sheet is now strong, too. Profitability development was favorable in all our business areas. Particularly at Metso Minerals and Metso Automation, their new way of operating emphasizing continuous improvement and costconsciousness produced outstanding results. Metso Paper also reached the profit targets set for 2005.

The favorable profit development and our strengthened balance sheet were mirrored in the price increase and heavier trading of Metso’s shares on the stock exchanges. Metso’s market capitalization had risen to over four billion euros by February 2006, from less than two billion euros one year ago. Considering both the increase in the share price and the dividends paid, the return on Metso’s share amounted to 101 percent in 2005. The positive development influenced the spring dividend proposal of eur 1.40.

We are continuing Metso’s longterm development from this platform and aiming for profitable growth. Achieving and maintaining profitable growth over the longterm isn’t easy; it requires a lot of effort. However, I have strong confidence in Metso employees and in our knowhow. Continuous improvement of our own operations and competitiveness has taken root as our way of operating. Now we are sharpening our focus on strengthening customer satisfaction.

Metso’s purpose statement – Engineering Customer Success – expresses

the direct correlation between our success and our customers’ success. We are in the business of providing our customers with the knowhow and technology that will help them improve their competitiveness and the productivity of their industrial processes.

Customer satisfaction is of critical importance in achieving our target of annual net sales growth of 10 percent. The aim is to achieve about half the growth organically and the other half through carefully selected, complementary acquisitions.

Our customers operate in growth sectors: Mining industry production, for example, is expected to grow 37 percent in 2004–2012. Production of aggregates, the world’s most common raw material, is expected to grow over 40 percent during the same time period, and pulp, paper and board production by 20 percent.

Geographically, growth and investments in new machines will be concentrated to the emerging markets, such as China, India, Brazil and Russia. Metso Paper, for example, intends to strengthen its presence in China by increasing local manufacturing and purchasing. The conditional agreement on the acquisition of a Chinese paper machine manufacturer is evidence of this. This agreement was announced in February 2006. Metso Automation has strengthened its technology and maintenance services in Brazil, and Metso Minerals has increased its foundry and manufacturing capacity in Brazil and India.

We believe the demand for machine and production line rebuilds will continue to be strong in Europe and North America. About twothirds of Metso’s net sales will continue to come from these markets, and success requires continuous development of the service network and service offering.

Our vision is to become the industry benchmark – measured in terms of customer satisfaction, operational efficiency, desirable workplace, or the creation of shareholder value. Achieving our vision requires us to be ready to renew our own ways of operating and to pursue profitable growth by listening to our customers’ needs.

An element in Metso’s renewal is the letter of intent signed in February 2006 to acquire Aker Kvaerner’s Pulping and Power business. Realization of the transaction will make Metso a significant supplier of comprehensive pulp mills – thereby fulfilling particularly customer demand in South America.

A strong and successful company is able to grow on its own terms. This view is supported also by the February 2006 feasibility study on alternative Metso structures. Based on the findings of the study, Metso’s Board of Directors decided to keep Metso’s current structure intact to continue executing its strategy of profitable growth.

Metso’s performance in 2005 demonstrated the high caliber of the company, but we have set our goals even higher. Metso employees all over the world have also committed to these goals. Through continuous, longterm development, we can create genuine and sustainable value for our shareholders.

I want to thank our customers for the fruitful cooperation and our partners for their desire to play a role in developing Metso. I also acknowledge the courage of Metso employees to meet the challenges of renewal, and thank our shareholders for the confidence they have shown. We hope that we can continue to be worthy of their trust also in the future.

Jorma Elorantap R e S i D e n t A n D c e o

m e t S o co R p o R At i o n

Renewing Metso

M E T S O ’ S A N N U A L R E V I E w 2 0 0 5 7

F R O M T H E C E O

Vision and strategy

puRpoSeMetso’s purpose, Engineering Customer Success, combines Metso’s strong engineering knowhow and customer success. Customer satisfaction is the prerequisite for Metso’s growth.

Metso’s customers are industrial companies that expect of their machinery and equipment suppliers longterm commitment and responsibility for delivered processes. Customer investments are typically large, and have long life cycles. Investments should yield a sufficient return on capital, which can be enhanced by cooperation between Metso and the customer throughout the process life cycle. Customers operate globally, and expect their suppliers to have a local presence. Metso’s strong

OUR PURPOSE IS

n Engineering Customer Success

OUR VALUES

4Customer’s success 4Profitable innovation 4Professional development 4Personal commitment

COMMON STRATEGIC GOALS TOWARDS THE VISION:

CUSTOMER SATISFAC TION

4�Solutions that best meet the customer needs throughout the process life cycle

4Customer-oriented approach in all operations

4Strong local presence globally

4Leading technology

OPERATIONAL EXCELLENCE

4�Continuous productivity and quality improvement

4�World-class business, management and people processes

4Profitability and growth exceeding our peers

4A great place to work

Metso’s strategic goal for 2006–2008 is to achieve sustainable profitable growth. Profitable growth will be attained through improved customer satisfaction and operational excellence.

8 M E T S O ’ S A N N U A L R E V I E w 2 0 0 5

V I S I O N A N D S T R A T E G Y

network makes it possible to serve customers on all continents.

Metso strives to produce increasingly competitive and efficient solutions, equipment and services, based on close customer cooperation, and technology and process expertise. Metso’s strengths also include wellknown product brands and a good reputation.

Metso delivers its purpose through its values and its ethical principles. For more information on values and ethical principles, please refer to pages 12–13.

viSionMetso’s vision is to become the industry benchmark. It challenges each Metso employee to reflect what he or she can personally do to better meet the expec

VISION

nWe want to become the industry benchmark

tations of customers, colleagues and shareholders.

For metso, being the industry benchmark means that n Metso’s solutions best meet the

customer needs. n Metso is the market and technology

leader in its chosen industries. n Metso is the leading company in

operational excellence. n Metso is the preferred employer. n Metso generates the best shareholder

value in its peer group.

StRAtegic goAlSMetso’s strategic goals are based on Metso’s purpose statement, values and ethical principles. Strategic goals form the roadmap that guides Metso towards its vision.

The strategic goals relate to customer satisfaction and operational excellence.

customer satisfaction n Solutions that best meet the customer

needs throughout the process life cycle.

n A customeroriented approach in all operations.

n A strong local presence, globally. n Leading technology.

operational excellence n Continuous improvement in

productivity and quality. n Worldclass business, management

and people processes. n Profitability and growth exceeding

our peers. n A great place to work.

The strategic goals form a permanent foundation on which the shortterm management agenda is built.

mAnAgement AgenDA 2006–2008Metso’s Management Agenda for 2006–2008 defines the focus areas and priorities in customer satisfaction

development and operational excellence, which are required to attain profitable growth in the strategy period 2006–2008. Metso’s growth will support the sustainable profitability development and strengthen its market leadership position.

the key focus areas in customer satisfaction are: n Strengthen the leading position in all

its market areas, n Complement life cycle offering both

through Metso’s own development and by complementary acquisitions, and

n Develop closer customer relationships by bringing sales, service, purchasing and manufacturing closer to customers. This is especially true in the emerging markets of Asia, South America and Russia.

the key focus areas in operational excellence are: n Continuous improvement of

productivity and quality. The focus will in particular be on the development of worldclass business processes and systems enabling organic growth.

n Develop supply chain management to increase flexibility, cost competitiveness, and quality.

In implementing the management agenda, Metso will rely on handson leadership and the results will be monitored regularly. Metso will also ensure that it has the right people in the right places, and that the competences and knowledge are constantly developed. The Business Area Management Agendas form a basis for concrete action plans and programs.

The development of business will be monitored through the financial targets set for the 2006–2008 strategy period. For further information, see pages 10–11. n

M E T S O ’ S A N N U A L R E V I E w 2 0 0 5 9

V I S I O N A N D S T R A T E G Y

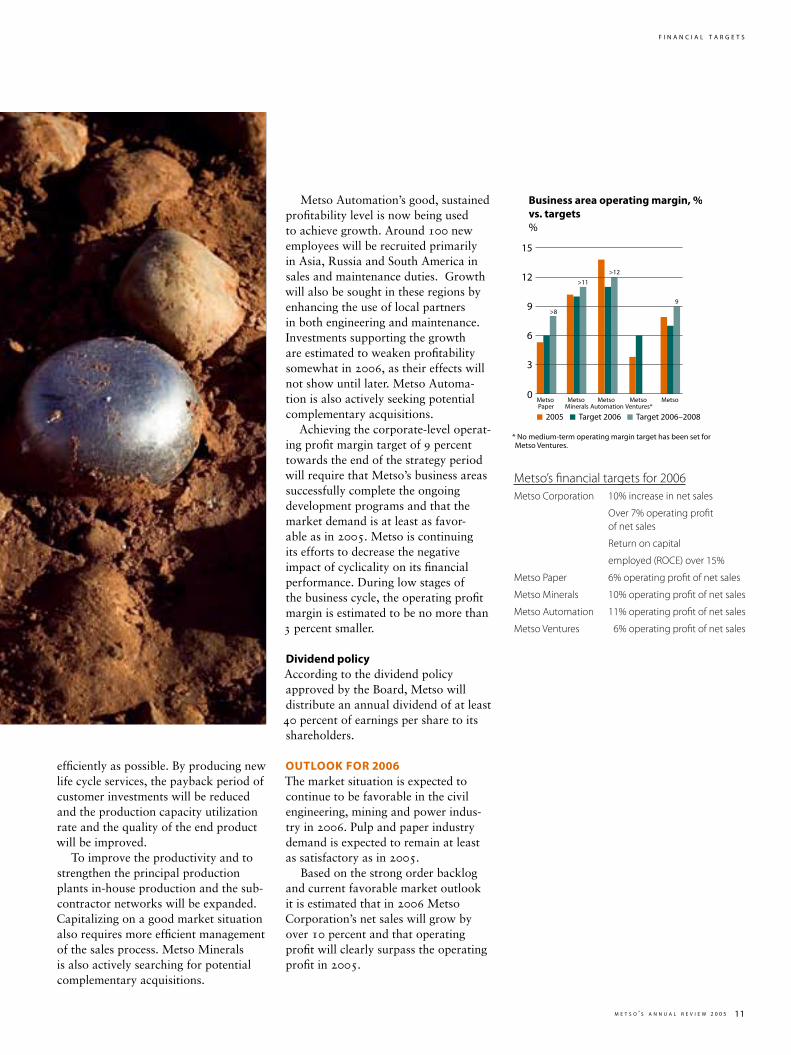

FinAnciAl tARgetS FoR 2006–2008 In the 2006–2008 strategy period, some 10 percent annual increase in net sales is targeted. Around half of the growth is expected to be attained organically, and the rest through complementary acquisitions. The profitability target is a 9 percent operating profit margin at the end of the strategy period.

Moreover, Metso seeks a return on capital employed (ROCE%) exceeding 15 percent regardless of the business cycle. In a situation of favorable demand, the annual ROCE% is expected to clearly surpass 15 percent.

It is strategically important for Metso to regain and retain a solid investment grade status. Consequently, gearing and free cash flow, among others, are monitored.

operating profit targets by business areaThe business areaspecific operating profit margin targets towards the end of the strategy period in 2008 are: over 8 percent for Metso Paper, over 11 percent for Metso Minerals and over 12 percent for Metso Automation. No mediumterm operating margin target has been set for Metso Ventures.

The strategic and financial targets will be reached through hundreds of operational measures and programs.

At Metso Paper, for instance, determined efforts to halve quality costs are under way. At present, quality costs account for 3–4 percent of net sales. The forming of a separate Service business line as of the beginning of 2006 enables a more focused range of aftermarket products and services to be developed. The aim is to increase the net sales of the aftermarket business by over eur 100 million in 2006–2008. Production and purchasing are being strengthened in the rapidly growing Asian and South American markets. For example in China, Metso Paper is strengthening its presence by acquiring ShanghaiChenming Paper Machinery Co. Ltd, a Chinese manufacturer of paper machines. The agreement

Metso’s progress in imple-menting the profitable growth strategy is reflected against the financial targets, among other indicators. The key indicators of Metso’s financial performance in 2006–2008 are increase in net sales, return on capital employed and operating profit margin. As the level of capital employed varies between the business areas, it is important to monitor both indicators simulta-neously when evaluating Metso’s performance.

Financial targets

was signed in February 2006, and the finalization of the transaction is subject to approval by the Chinese authorities.

In February 2006, Metso Paper and Aker Kvaerner signed a letter of intent whereby Metso intends to acquire Aker Kvaerner’s Pulping and Power business. When completed, the transaction will expand Metso’s product offering.

Another goal for Metso Paper in 2006 is to make the Tissue business line profitable.

Metso Minerals is developing global procurement and logistics to make the global network to serve customers as

10 M E T S O ’ S A N N U A L R E V I E w 2 0 0 5

F I N A N C I A L T A R G E T S

0

3

6

9

12

15

Metso Ventures*

Metso Metso Automation

Metso Minerals

Metso Paper

Business area operating margin, % vs. targets%

2005 Target 2006 Target 2006–2008

>8

>11

>12

9

Metso’s financial targets for 2006Metso Corporation 10% increase in net sales

Over 7% operating profit of net sales

Return on capital

employed (ROCE) over 15%

Metso Paper 6% operating profit of net sales

Metso Minerals 10% operating profit of net sales

Metso Automation 11% operating profit of net sales

Metso Ventures 6% operating profit of net sales

Metso Automation’s good, sustained profitability level is now being used to achieve growth. Around 100 new employees will be recruited primarily in Asia, Russia and South America in sales and maintenance duties. Growth will also be sought in these regions by enhancing the use of local partners in both engineering and maintenance. Investments supporting the growth are estimated to weaken profitability somewhat in 2006, as their effects will not show until later. Metso Automation is also actively seeking potential complementary acquisitions.

Achieving the corporatelevel operating profit margin target of 9 percent towards the end of the strategy period will require that Metso’s business areas successfully complete the ongoing development programs and that the market demand is at least as favorable as in 2005. Metso is continuing its efforts to decrease the negative impact of cyclicality on its financial performance. During low stages of the business cycle, the operating profit margin is estimated to be no more than 3 percent smaller.

Dividend policyAccording to the dividend policy approved by the Board, Metso will distribute an annual dividend of at least 40 percent of earnings per share to its shareholders.

outlook FoR 2006 The market situation is expected to continue to be favorable in the civil engineering, mining and power industry in 2006. Pulp and paper industry demand is expected to remain at least as satisfactory as in 2005.

Based on the strong order backlog and current favorable market outlook it is estimated that in 2006 Metso Corporation’s net sales will grow by over 10 percent and that operating profit will clearly surpass the operating profit in 2005.

efficiently as possible. By producing new life cycle services, the payback period of customer investments will be reduced and the production capacity utilization rate and the quality of the end product will be improved.

To improve the productivity and to strengthen the principal production plants inhouse production and the subcontractor networks will be expanded. Capitalizing on a good market situation also requires more efficient management of the sales process. Metso Minerals is also actively searching for potential complementary acquisitions.

* No medium-term operating margin target has been set for Metso Ventures.

M E T S O ’ S A N N U A L R E V I E w 2 0 0 5 11

F I N A N C I A L T A R G E T S

vAlueSThe values behind Metso’s operations were defined in 2001, and since then they have been the guideline for business operations and everyday work. These values will also guide Metso’s operations in the longterm.

customer’s successProfitable business is possible only through our customers’ success. We develop solutions that anticipate our customers’ future needs and take environmental factors into account. In serving customers we commit ourselves to high standards and professional performance.

profitable innovationWe create added value for our customers and owners through innovation. We are ready to question present practices and abandon obsolete ones. We utilize and combine the vast and diverse knowledge of the entire organization. Metso’s growth is based on creativity and healthy risktaking in a working environment that encourages and rewards innovation.

personal commitmentAs we finish what we undertake and accept ownership of and responsibility for our actions, we can always be trusted. We are direct and honest in our communication and respect cultural

differences. Even though we openly express our views, we work diligently to achieve mutually agreed targets.

professional development We are willing to learn – and that includes from each other. We regard professional development as an integral part of our work. We welcome new challenges and tackle them to the best of our abilities. The wellbeing of our working community is of paramount importance to us.

etHicAl pRincipleS Ethical standards and principles support Metso’s sustainability and provide Metso and its stakeholders with commonly accepted guidelines and perspectives for future decisions. They create uniformity in all business transactions and work assignments.

Metso’s ethical principles also describe company culture, commonly accepted practices, and commitment to comply with laws and regulations. Instead of creating new obligations, they define, confirm and document Metso’s best practices.

All Metso’s employees should know the ethical principles and also put this knowledge into practice. Consistency in applying these principles is also a way to earn a reputation as a credible corporate citizen.

Values and ethical principles ensure consistency in Metso operations

Metso complies with applicable laws, regulations and generally accepted business practices. Metso’s operations are also guided by its values, ethical principles and good governance practices. The values and ethical principles ensure that Metso’s operations are consistent and uniform, independent of the country and business area. Metso strives to be a good corporate citizen in all its operations.

12 M E T S O ’ S A N N U A L R E V I E w 2 0 0 5

V A L U E S A N D E T H I C A L P R I N C I P L E S

integrityIntegrity is fundamental to all of Metso’s dealings, actions, statements and reporting, and is an essential aspect of sustainability. Metso respects its promises and commitments.

compliance with laws and regulationsMetso is committed to full compliance with all applicable national and international laws, regulations and generally accepted practices. Should these prove to be insufficient or open to interpretation, the best available experts will be consulted.

transparency and opennessMetso is a public company whose shares are quoted on the Helsinki and New York Stock Exchanges. Metso provides its stakeholders with information on its status and performance simultaneously and equally, transparently and openly, without preference or favor for any group or individual, and in compliance with the law, the regulations of the mentioned exchanges and the accepted practices of the equities market. Metso’s employees do not use insider information directly or indirectly in stock trading.

Metso considers it highly important to continuously interact with the authorities and nongovernmental organizations in order to develop and sustain open and direct contact with society.

Human rightsMetso supports and respects the protection of human rights as expressed in the UN Declaration of Human Rights. As an employer, Metso accepts the basic labor rights stated by the International Labor Organization (ILO): freedom of association, the effective recognition of the right to collective bargaining, abolition of forced labor, and equality of opportunity and treatment.

Metso does not use child labor or engage subcontractors or suppliers that do so. Metso does not allow behavior that is physically coercive, threatening, abusive or exploitative.

equal opportunities and non-discriminationMetso selects and appoints employees according to their personal qualifications and skills for the job. Metso does

not engage in or support discrimination in hiring, compensation, selection to training, promotion, termination of employment, or retirement based on, but not limited to, race, caste, national origin, religion, disability, gender, sexual orientation, union membership or political affiliation.

intellectual propertyMetso values the creation and protection of knowledge and intellectual property. Accordingly, Metso’s employees act to safeguard the company’s intellectual property and do not allow unauthorized access to it by outsiders. Conversely, Metso employees respect the intellectual property held by outsiders and do not try to obtain it by illegal means. Metso encourages and supports its employees’ commitment and efforts to increase the company’s intellectual property and thus to contribute to the profitability of the company.

Rejection of corruption and briberyMetso’s management and employees are expected to act in the corporation’s best interests at all times. Employees do not become involved in business relationships that may lead to conflicts of interest. Metso and its employees do not pay bribes or illegal payments to obtain or retain business. Employees do not pay to facilitate favorable decisions or services from authorities.

Metso employees do not accept gifts from business partners exceeding normal standards of hospitality. If the acceptance of a gift or favor contains the remote possibility of a conflict of interest, the employee must clarify the situation with management in advance.

Health and safetyMetso strives to provide a safe and healthy working environment. Metso works to prevent accidents and injuries by executing policies and actions that minimize, as far as is reasonably practicable, the causes of hazards inherent in the working environment. Metso establishes and maintains systems to detect, avoid or respond to potential threats to the health and safety of all personnel.

community involvement and sponsorshipMetso encourages its units and personnel to participate in community

programs promoting the common good. Metso primarily supports programs related to youth activities, science and research, culture as well as environmental protection and conservation.

protection of the environmentMetso contributes to ecological sustainability in all its activities. Metso anticipates the environmental concerns of its customers and the expectations of the public. Metso cooperates with customers and partners to develop best practices and processes for the efficient and sustainable use of energy and materials and for the prevention of pollution.

ethical standards of suppliersMetso expects its suppliers and contractors to demonstrate similar high ethical standards and, accordingly, this criterion is of prime importance when establishing or continuing business relationships.

Application of ethical principles Metso’s ethical principles govern the actions of Metso’s management and all employees in their business operations and employment relationships. Metso ensures that these ethical principles are effectively communicated to all employees and requires all employees to adopt and apply these ethical principles.

Assurance of right and ethically sustainable working practicesA review of Metso’s ethical principles in 2005 showed that they remain relevant and sufficiently comprehensive in their original form. However, it was decided to supplement the more detailed internal instructions related to their use with, for example, prohibitions of insider trading and of participation in any activity that restricts competition. In compliance with the SarbanesOxley Act that regulates Metso as a public company listed on U.S. stock exchanges, internal control and monitoring systems have been developed. These systems have been widely tested and related training has been arranged. One objective has been to make the system relating to the treatment of suspected financial misconduct better known. n

M E T S O ’ S A N N U A L R E V I E w 2 0 0 5 13

V A L U E S A N D E T H I C A L P R I N C I P L E S

14 M E T S O ’ S A N N U A L R E V I E w 2 0 0 5

O P E R A T I N G E N V I R O N M E N T

Operating environment

FActoRS AFFecting pRoFitABilityThe demand for Metso’s products and its financial position are affected by business cycles, and the demand of customer industries’ products, as well as the customer industries’ profitability and willingness to invest. Other factors include major changes in exchange rate and the relative competitiveness of Metso’s products and services.

customer industries and business cyclesThe pulp and paper industry is Metso’s most important customer industry, because the entire net sales of Metso Paper and approximately half of the net sales of Metso Automation derive from deliveries to this customer industry. The business of Metso Paper and Metso Automation is affected by changes in pulp and paper consumption, price trends in pulp and different paper and board grades, investments by the pulp and paper industry, manufacturers’ capacity utilization and changes, among other things, in environmental legislation.

Metso’s secondlargest customer industry is the civil engineering industry, which accounts for almost half of Metso Minerals’ net sales. The development of the civil engineering industry is affected especially by the amount of infrastructure investments, which is reflected directly in the demand for aggregates.

The thirdlargest customer industry is the mining industry, whose business cycles affect Metso Minerals’ operations. Almost 40 percent of Metso Minerals’

net sales derive from industry products and services to the mining industry. The mining industry’s willingness to invest is affected by changes in the demand for and price of metals.

Metso’s fourthlargest customer industry is the energy industry. The market outlook for the energy, oil and gas industry is very important to Metso Automation, because about half of Metso Automation’s business consists of deliveries to this customer industry. Metso Automation’s operations are also affected by changes in oil and energy prices.

In the longterm, the effects of cyclical fluctations are offset by the geographical diversity of Metso’s operations, the wide range of customer industries served, and the growing importance of the aftermarket business, process improvements and machine rebuilds. Orders for new equipment are more sensitive to changes in business cycle than the aftermarket business, process improvements and rebuilds.

exchange rate changesMore than onehalf of Metso’s net sales originate from outside the euro zone. Alongside the euro, the most important invoicing currencies used are the U.S. dollar and the Swedish krona. Metso also has major exports from Brazil and South Africa. The wide geographical spread of Metso’s operations reduces the significance of individual currencies, and Metso strives to manufacture products in different currency areas near the end markets.

During 2005, the average exchange rates of currencies most relevant to Metso, except to Brasilian real, remained at almost the previous year’s level, so the translation effect was not significant in terms of income statement comparison. Exchange rate variations can have a direct impact also on the prices of raw materials and production commodities purchased in nondomestic currencies and in the prices of end products for export, in which the invoicing currency is different from the currency of the manufacturing costs (transaction effect). The foreign exchange positions that are based on binding delivery and purchase agreements are hedged in full. Future currency cash flows are hedged for periods that do not normally exceed two years. Therefore, the majority of future currency cash flows related to the order backlog are hedged.

The fact that the Chinese yuan was allowed to fluctuate against a currency basket and was revalued during 2005 did not have any significant effect on Metso’s operations. Metso is a net importer to China, but also has local manufacturing in China. If the yuan were to be revalued further, it is estimated that this would have a positive effect on the demand for Metso’s export products.

competitive situation in the business areasWith respect to pulp and paper machines and whole production lines, there are only a few competitors in Metso Paper’s sector. In the aftermarket

M E T S O ’ S A N N U A L R E V I E w 2 0 0 5 15

O P E R A T I N G E N V I R O N M E N T

0 20 40 60 80 100Share of consumption in 2004, %

source: Jaakko Pöyry

Demand growth %/a

1

0

5

6

4

3

2

The estimated demand growth for paper and board through 2020

Average 2,1 %/a

AfricaRest of Asia

OceaniaWestern Europe

North America Japan

Eastern EuropeMiddle East

Latin America

IndiaRussia

China

Source: Jaakko Pöyry

business and tissue machines, there are several competitors.

In new paper machine sales, the machines are designed according to the customer’s specifications. Deciding factors for the sale of paper, board and tissue machines include machine performance and technology, supplier’s process knowhow, delivery time, price, service availability and previous reference deliveries. In the aftermarket business, the key competitive factors are local presence and operations near the customer, as well as price, availability and technology.

Metso Minerals’ main competitors for sales of new machines and whole production lines are global companies. In addition, there are also many local competitors especially for lighter equipment. The competitive field for the aftermarket business is fragmented and the competitors are mainly local and regional operators. The key competitive factors are solutions’ performance, technology, reference deliveries, operations near the customer, project competence and price and availability.

Process automation systems are competed for globally and the competitors are mainly multinational companies. The competitive factors are reliability and usability of equipment and systems, applications expertise, technical development, ease of installation and configuration, price, availability of customer support, reputation and references. Field equipment systems, especially valves, are manufactured by numerous companies, but many of them have specialized in a narrow product

“�The pulp and paper industry is the most important of Metso’s customer industries, because the entire net sales of Metso Paper and about half of the net sales of Metso Automation derive from deliveries to this customer industry.”

branch or application area. Metso Automation’s control, shutoff and emergency shutoff valves, and intelligent equipment and software, are widely used in the pulp and paper industry and in the energy, oil and gas industry.

long-teRm mARket DevelopmentMetso operates on growing markets and the production volumes of all main customer industries are estimated to be increasing. By 2012, ore production is estimated to grow by an average of almost four percent a year, aggregates by over four percent, paper, board and fiber by over two percent and energy by about two percent a year.

metso paper’s operating environmentMetso Paper’s target markets are approx. eur 10 billion in size, depending on the business cycle. Aftermarket

business amounts more than a half of the total target market size. Also the majority of Metso Paper’s net sales derive from services related to rebuilds, process improvements, maintenance and aftermarket. More than onethird of net sales derive from the sale of new machines.

In 2000, Metso Paper bought Beloit’s service business, after Beloit had gone bankrupt. Metso Paper and Beloit have jointly delivered about half of the world’s paper machine capacity in use, some 40 percent of the tissue machine capacity and about a third of the pulping line and board machine capacity. Most of Metso Paper’s net sales still originate from Scandinavia, Western Europe and North America, but demand for paper and board is increasing faster than average in Eastern Europe, Asia, South America and Africa. It is estimated that pulp, paper and

16 M E T S O ’ S A N N U A L R E V I E w 2 0 0 5

O P E R A T I N G E N V I R O N M E N T

95

100

105

110

115

120

125

130

135

140

145

Output of customer industries

2012f2005Sources: Jaakko Pöyry, Raw Materials Group, Freedonia, International Energy Agency

Index (2005 = 100)

Paper, board and papermaking fiber 2–3%/aGrowth ~20%

Aggregates 4–5%/aGrowth ~40%

Metal ore 3–4%/aGrowth ~30%

Energy 2%/aGrowth ~15%

2012f2005Sources: Jaakko Pöyry, Freedonia

Index (2005 = 100)

90

100

110

120

130

140

150

160

170

180

Aggregates and fiber, paper & board production growth in China

Aggregates 7.0%/aGrowth 61%

Paper & Board 5.7%/a Growth 47 %

Papermaking fiber 4.4%/aGrowth 35%

Sources: Jaakko Pöyry, Raw Materials Group, Freedonia, International Energy Agency Sources: Jaakko Pöyry, Freedonia

board production will grow by over two percent per year on average by 2012. Tissue and board production is forecast to grow slightly more quickly than average.

The number of new paper machines startups has been falling since 1999, and it is expected that fewer than ten new, wide paper machines will be started up per year globally from now on. On the other hand, the size and speed of the machines have correspondingly increased. Customers making investment decisions increasingly place value on their return on investment.

As the real price of pulp and paper is falling, the objective of the pulp and paper industry is to continually reduce the operating and investment costs of production lines. Interest in cooperation with suppliers throughout the entire life cycle has increased, and, in addition to major capital investments, there is

more and more need for smallerscale rebuilds and process improvements, and maintenance services.

As the investments to increase capacity are diminishing in Europe and North America, China has become the main market area for new paper machines. In recent years, about half of the world’s new paper and board production capacity has been concentrated on China.

Especially in South America, investments are being made in new chemical pulping lines that use for example, locally grown shortfiber eucalyptus trees as raw material. Moreover, labor costs in South America are much lower than in Europe and North America. Asia is also a growing market for pulping lines.

The consumption of packaging board will grow especially in China, because the packagingintense export industry

has moved there from the Western countries and Japan. Packaging board is also becoming lighter. This trend is clear in Europe, where machines are being developed to produce lighter grades. Development of the converting and printing methods related to packaging materials has led to stricter quality requirements, which is reflected in the demand for board machine rebuilds. An increase in the demand for daily consumer goods in the emerging markets requires an increase in the production of interior packaging materials in these areas.

Demand for tissue machines is expected to grow especially in the emerging markets, most of all in Asia. In these markets, demand has been greatest for small and less expensive machines. Demand for the larger ThroughAir Drying (TAD) machines is expected to pick up in a few years in North America.

“�Sales of new machines account for over a third of Metso Paper’s net sales. Most of the net sales derive from products and services related to rebuilds, process improvements, maintenance and aftermarket business.”

M E T S O ’ S A N N U A L R E V I E w 2 0 0 5 17

O P E R A T I N G E N V I R O N M E N T

metso minerals’ operating environmentMetso Minerals’ target markets are approx. eur 12 billion in size. Metso Minerals has supplied over half of the world’s grinding mills in use, about 30 percent of the crushers, over 20 percent of metal crushers, and 5–10 percent of the screens. During the next five years, aggregates production is forecast to grow annually by 4–5 percent, mining industry production by 3–4 percent and the metal recycling industry by 3–4 percent.

Crushed rock is the most commonly used raw material in the world. For example, the construction industry annually uses approximately 18 billion tons of aggregates. GDP and population growth increase infrastructure construction, which affect the demand for aggregates. Stricter environmental requirements have limited the use of natural gravel and sand, but at the same time increased the use of crushed rock and also recycled aggregates.

Aggregates demand is forecast to grow especially in China, India, Russia, the United States and Eastern Europe. For example, the Chinese government plans to build 50,000 kilometers of fourlane roads by 2020. In Russia, aggregates production is expected to rise steadily by about 7 percent a year. Aggregates production is increasing also in the United States. In July 2005, Congress approved a new Transportation Equity Act (SAFETEALU), reserving almost usd 300 billion for the development of the country’s transportation infrastructure until 2009, an increase of 30 percent compared to the previous

“�Metso operates in growing markets, and the production volumes of all its main customer industries are estimated to be increasing.”

18 M E T S O ’ S A N N U A L R E V I E w 2 0 0 5

O P E R A T I N G E N V I R O N M E N T

“�Metso Minerals has supplied over half of the world’s grinding mills in use, about 30 per cent of the crushers, over 20 per cent of the metal crushers, and 5–10 per cent of the screens.”

sixyear period. It is believed that this project will have a positive effect on Metso Minerals’ business especially during the first three years. Road construction projects in Eastern Europe supported by the European Union are also expected to increase the demand for Metso Minerals’ aggregates production equipment.

The mining industry processes approximately 5 billion tons of metal ores and 3 billion tons of industry minerals a year. In North America and Europe, demand for Metso Minerals’ products in the mining industry is weighted towards the aftermarket and service business. New mining projects are being started mainly in the southern hemisphere. The most significant factor affecting raw material demand has been the rapid growth of the Chinese economy, making the country the world’s leading consumer of metals.

Customers’ high capacity utilization during a good price and demand situation has also increased demand for Metso Minerals’ products. Mining companies have tried to respond to higher demand especially by increasing their material handling capacity. However, the lack of resources, and especially of experienced project managers and engineering personnel, will level out demand in the coming years, and investment project schedules have, in some cases, been lengthened.

The demand for scrap metal is expected to remain strong in the next few years. Steel companies are using increasingly more scrap metal for production instead of virgin raw mate

rial. The amount of recycled scrap metal is expected to grow annually by 5 to 6 percent by 2025.

metso Automation’s operating environmentThe size of Metso Automation’s target market is approx. eur 10 billion. Metso Automation is one of the world’s leading companies making measurement equipment and automation systems for the pulp and paper industry, and the world’s largest supplier of automatic shutoff valves for the pulp and paper industry. In the long run the markets for automation systems, valves and analyzers used in the pulp and paper industry are expected to grow by about 3 percent a year. The market growth in automation and information systems for the energy, oil and gas industry is estimated to be almost 4 percent, while the market growth for valves is estimated to be over 3 percent a year.

New pulp and paper industry investments are focused mainly in Asia and South America. The aging machine and equipment base in Europe and North America is increasing the demand for performanceenhancing solutions and services. This will increase the significance of automation solutions, such as preventive condition monitoring.

Demand for oil has outpaced the producers’ ability to boost their capacity, and nowadays oil refining capacity is insufficient in relation to the demand for end products. The resulting sharp rise in the price of crude oil and petroleum products is expected to lead to the construction of new refining capacity

and the modernization of existing production plants. Since the demand for oil and petroleum products is greater than the supply, the demand for valves will increase and the valve market is expected to remain good. Moreover, the energy and process industry is expected to increase its investments in automation systems. n

Market information sources: Jaakko Pöyry Consulting, Raw Materials Group, Freedonia and International Energy Agency.

M E T S O ’ S A N N U A L R E V I E w 2 0 0 5 19

O P E R A T I N G E N V I R O N M E N T

Risk management is an integral part of Metso’s business management. Metso’s Board of Directors approves the risk management principles. It also ensures that the planning, information and control systems in place for risk management are sufficient and support the attainment of business goals. The Board’s Audit Committee reviews risk management and ensures its compliance with Metso’s Corporate Governance principles.

The Corporate Risk Management Team confirms the business areaspecific Risk Management Program, on which risk management implementation is based. The Risk Management Team is chaired by the Corporation’s Executive Vice President and CFO and consists of nominated business area representatives.

The Corporate Risk Management function is responsible for the implementation of the risk management program and policy, and for the development of Corporationwide risk management methods and guidelines so that they support the objectives and continuity of Metso’s business. The Risk Management function reports to the Corporation’s Executive Vice President and CFO. The business area presidents are responsible for the management of risks related to the operations of their respective business areas.

Metso’s all business areas make annually a risk assessment. Metso’s Risk Management function cooperates with an external insurance broker to conduct risk management evaluations of Metso’s key units in accordance with a 5year plan. The evaluations are presented to

the Risk Management Team, which determines the necessary measures.

Metso has prepared for property, business interruption, transport and liability risks through global insurance schemes. Liability risks include damage caused by Metso’s operations and products, and management liabilities. The insurance coverage consists of property, transport and liability insurance schemes and their local applications. The Corporation’s total riskbearing capacity is taken into consideration when setting the amount of deductibles. Metso’s captive insurance company acts as a partial reinsurer in some of the Corporation’s own insurance programs.

The following describes the business risks, financial risks, operational risks and hazard risks that are the most significant for Metso’s operations. Metso monitors these risks actively. Metso’s view is that, when properly controlled, business and financial risks also create opportunities for the development of Metso’s business, but that any materialized operational risks and hazard risks have a negative effect on Metso’s business.

Despite the actions taken to manage and limit the effects of the risks, there can be no assurance that such risks, if materialized, will not have a material adverse effect on Metso’s business, financial condition or operational result.

BuSineSS RiSkS

Business development risksThe longterm development of Metso’s business is affected by business devel

opment risks that are related to new markets and business potential and also involve risks related to the Metso brand and values. When planning and implementing new business, Metso takes into account not only the development potential and availability of new products and technological solutions, but also the different life cycle stages of the customers’ and Metso’s products and production plants.

Business development risks also include the risks related to mergers and acquisitions, which Metso takes into account by using Metso acquisition Process (MAP) accepted in the beginning of 2006 and through the due diligence process. The business to be acquired has to fulfill both strategic and financial targets. Also the risks related to the business to be acquired, including product liabilities and environmental responsibilities, and risks related to reputation and the personnel, are taken into account. Additionally, business development risks include the risks related to the supply and availability of natural resources, raw materials and power.

The development of personnel competence and the utilization of personnel potential are critical for business development. Metso annually carries out an evaluation related to management resources, in which Metso’s key executives, their possible deputies, successors and any necessary new management resources are surveyed. In 2005, this evaluation covered 350 persons. Metso also monitors the age structure of the personnel to avoid risks

Risks and risk management

20 M E T S O ’ S A N N U A L R E V I E w 2 0 0 5

R I S K S A N D R I S K M A N A G E M E N T

M E T S O ’ S A N N U A L R E V I E w 2 0 0 5 21

R I S K S A N D R I S K M A N A G E M E N T

related to people retiring, for example. Metso’s management is currently not aware of any possible risks related to the personnel’s age or retirement that would be material for the Corporation’s business development.

Business environment risksBusiness cycles in the global economy and in customer industries influence the demand for Metso’s products and its financial position, especially in the shortterm. Metso Paper and Metso Automation are affected by the development of the pulp and paper industry. In addition, Metso Automation is affected by the energy, oil and gas industry cycles. Metso Minerals’ operations are dependent especially on the outlook of the civil engineering industry, and most significantly on the level of infrastructure investments. Metso Minerals is also affected by business cycles in the mining industry.

In the longterm, the effects of business cycles are reduced by the geographical diversity of operations and by the range of customer industries served. New equipment orders tend to be more affected by business cycles than the demand for rebuilds, process improvements and aftermarket operations, for which Metso’s large global installed base offers a strong platform. In order to further reduce the risks of business cycles, Metso has actively promoted process life cyclerelated operations and longterm partnerships with customers. In addition, in recent years Metso has increased the flexibility of the cost base by outsourcing and by focusing its own operations on the manufacture and assembly of core components. The increase in outsourcing has been reflected, for example, in an increase in Metso’s purchases from suppliers.

market risksChanges in customers’ demand affect Metso’s operations. Such changes may be related to changes in customer companies’ strategy, product development and requirements, and environmental aspects, among other things. For exam

ple, some of Metso Paper’s customers are increasingly focusing on their core competence – the production of pulp, paper or board – and are outsourcing the mill service business to partners. Metso Paper’s objective is to conclude longterm service agreements with these customers, in which the main responsibility for process service is transferred to Metso Paper.

Metso has many competitors in different business areas and products. Metso aims to differentiate itself from competitors through quality, reliability, local presence and availability, and to provide highlevel technological competence and longterm commitment to the customer. Metso seeks competitive advantage through continuous product development based on research and cooperation with customers. Metso also aims to be flexible and costconscious in its operations.

To better serve its new customers, Metso aims to increase its own manufacturing and assembly capacity of components in fast growing market areas, such as China, India and Brazil. In these areas, the products and services developed by new local competitors are also monitored closely. Although Metso’s main competitors are still European and North American companies, some Asian suppliers are providing solutions that compete with their low prices. Metso protects the products and intellectual property rights related to its business through patents and trademarks.

technology risksMetso’s technology risks are related to technological competence, and research and technology development (R&D). In R&D, Metso manages the projects in accordance with the Metso Innovation Process, in which a business plan is created for a new product or concept and its profitability is evaluated at different stages of the development process. The business plan defines responsibilities and roles for all functions of product development and launch – such as service, sales, industrial design and marketing – from the very

beginning of the development process. The product’s intellectual property rights and environmental perspectives are also taken into account.

Use of new technology may increase qualityrelated costs. For example, the qualityrelated costs of Metso Paper represent some 3–4 percent of the business area’s net sales. An objective for 2006–2008 is to further improve the quality of deliveries and to halve these costs.

political, economic, cultural and legislative development trendsThe operations of both Metso and its customers are geographically widespread. Global political development, political unrest, terrorism and armed conflicts constitute risks to Metso’s operations. The company’s operations are also affected by cultural and religious factors, and by legislation

– particularly different countries’ environmental legislation.

Revisions of the environmental legislation in various countries often take a long time. Metso monitors laws that are under preparation and anticipates their effects on its own business and that of its customers. However, unanticipated legislative changes may have adverse effects on Metso’s business. Such a situation may arise, if, for example, a raw material that Metso uses in its production or that is contained in subcontracted components is prohibited. In such cases, production costs may increase due to the development of alternative solutions. Tighter environmental legislation may increase Metso’s manufacturing costs, but it also provides opportunities to offer customer industries new solutions that meet more stringent environmental standards.

Metso has its own manufacturing and supplier networks in many developing countries. In addition, the demand for new machinery and equipment increasingly comes from countries in Asia and South America. Sudden political, economic and/or legislative changes in these countries could have a material adverse effect on Metso’s business. For

22 M E T S O ’ S A N N U A L R E V I E w 2 0 0 5

R I S K S A N D R I S K M A N A G E M E N T

example, China has a significant direct and indirect effect on Metso’s net sales and, hence, any sudden political, economic or legislative changes in China could, especially in the shortterm, have an effect on Metso’s business. The risks related to these developing countries are somewhat reduced by the wide geographical and industry coverage, as well as the more stable aftermarket operations in Europe and North America.

phenomena related to climate change and environmentEmissions from Metso’s own production units are in compliance with the set permit limits. Risks related to climate change are accounted for in the planning of Metso’s energy consumption and raw materials for its products. Metso’s research and technology development gives appropriate consideration to increases in energy prices, and the goal is to reduce the energy consumption of new products.

The measures taken to control diseaserelated risks include personnel vaccinations.

FinAnciAl RiSkSThe task of Metso’s Corporate Treasury is to manage currency and other financial risks related to operations, and to safeguard the availability of the Corporation’s equity and debt capital under competitive terms. The Corporate Treasury functions act as the counterparty to the business areas’ operating units and centrally manage external funding. It is

also responsible for the management of liquid assets and the provision of proper hedging measures.

liquidityCash and committed revolving credit facilities are used to protect shortterm liquidity. Liquidity and financing costs are managed by balancing the proportion of shortterm and longterm loans, as well as the average remaining maturity of longterm loans. In the longterm risks in the availability of funds and pricing are also managed by diversifying funding between the money and capital markets and banks. Credit rating agencies assess Metso’s business and publish credit ratings.

interest rate risksChanges in market interest rates and interest margins may influence financing costs, returns on financial investments and valuation of derivative contracts. Interest rate risks are managed through the ratio of floatingrate to fixedrate loans and the average length of interest rate periods. Additionally, interest rate swaps and other derivative contracts may be used.

currency risksExchange rate changes affect Metso’s business, although the geographical diversity of operations decreases the significance of any individual currency. Exchange rate variations can have a direct effect on the prices of raw materials and production commodities purchased in nondomestic currencies

and in the prices of end products for export, in which the invoicing currency is different from the currency of the manufacturing costs (transaction effect). More than onehalf of Metso’s net sales originate from outside the euro zone. Alongside the euro, the most important currencies used in invoicing are the U.S. dollar and the Swedish krona. When the net sales and results of subsidiaries outside the euro zone are translated into euros, they may increase or decrease because of exchange rate changes, even though no real change in such net sales or results has occurred (translation effect). Exchange rate movements may also weaken the cost competitiveness of Metso’s products against the products of competitors manufactured in another currency area.

In accordance with Metso’s Treasury Policy, the operating units are required to hedge in full the currency exposures that arise from firm delivery and purchase agreements. In addition, the units can hedge anticipated foreign currency denominated cash flows by taking into account the significance of such cash flows, the competitive situation and other possibilities to adjust. Metso has operations in countries in which currency regulation affects the hedging of risks. The most important of these are Brazil and China. Hedging operations are centralized in Metso’s Corporate Treasury. Upper limits on the open currency exposures of the Corporate Treasury, calculated on the basis of their potential profit impact have been set. These limits cover net exposures

M E T S O ’ S A N N U A L R E V I E w 2 0 0 5 23

R I S K S A N D R I S K M A N A G E M E N T

from transfers between units and items arising from financing activities. Future currency cash flows are hedged for periods not normally exceeding two years. Accordingly, the majority of future currency cash flows related to the order backlog is hedged.

The equity of subsidiaries outside the euro zone is affected by exchange rate risks, which may lead to translation differences in the consolidated equity. These risks are hedged with respect to essential currencies in accordance with Metso’s Treasury Policy by using noneuro denominated loans and forward exchange agreements.

credit risks and other counterparty risksMetso’s operating units are primarily responsible for credit risks pertaining to sales activities. The business areas determine the guidelines for delivery and payment terms granted to customers, their supervision and enforcement, which are then implemented at the business line and operating unit level. Large projects also require corporate level handling. Metso’s Corporate Treasury provides centralized services related to customer financing and seeks to ensure that the principles of the Treasury Policy are adhered to with respect to terms of payment and the required collateral.

When investing cash assets and making derivative contracts, the Metso Corporate Treasury only accepts counterparties that fulfill the credit rating criteria defined in the Treasury Policy, or parties approved in advance by Metso’s Board of Directors. With respect to investments, derivative contracts and borrowing, counterpartyspecific limits

have been set to avoid risk concentrations.

Metso has agreed on extended payment terms with selected customers. In establishing credit arrangements, the creditworthiness of the customer and the timing of cash flows expected to be received under the arrangement are assessed. However, should the actual financial position of customers or general economic conditions differ from the expectations, the ultimate collectibility of such trade receivables may be required to be reassessed, which could result in a writeoff of these balances in future periods.

Metso’s ability to manage trade receivables exposures, customer financing, risk concentrations and financial counterpartyrelated risks depends on a number of factors, including Metso’s capital structure, market conditions affecting the counterparties and the ability to mitigate exposure on acceptable terms. The risks of individual customers or other counterparties are generally not significant compared to the magnitude of Metso’s business, and the aim is to reduce customer risks by exact sales contracts, payment terms and collateral, as well as by effective quotation control procedures.

opeRAtionAl RiSkSMetso’s operational risks include business interruption risks, organization and managementrelated risks, information security risks, production, process and profitability risks, project activity risks, contract and liability risks, product safety, crisis situations and illegal acts.

A crisis management organization was established within Metso in 2005

to maintain the Corporation’s crisis management readiness. In the event of any crisis, the crisis management organization will quickly assess what measures are needed for resolving the crisis and whether any external resources need to be used.

The methods used to prevent Metso employees from engaging in illegal activity include not only the company’s values and ethical principles, but also the ‘Whistleblower’ channel. The channel is operated by a third party and any Metso employee is able to report any actual or suspected misconduct with potential financial effects. Misconduct reports can be filed via the Internet, by email or by phone.

The most critical operational risks for Metso are profitability risks, business interruption risks, project activity risks and contract and product liability risks.

profitability risksOne of Metso’s key targets is profitable business. In largescale projects and equipment transactions there is a risk, however, that the actual costs of the transaction cannot be estimated accurately enough in the offer stage, and that therefore it is not possible to determine the right transaction price for Metso or to assess whether the market price level or Metso’s cost competitiveness are sufficient to conclude the transaction.

To manage risks related to pricing, Metso’s businesses apply various quality systems, operating guidelines and profitability analyses that take into account, among other things, the product to be sold, the customer and the payment terms. Internal approval procedures in

24 M E T S O ’ S A N N U A L R E V I E w 2 0 0 5

which pricing authorizations are linked with transaction values are also utilized in project and product pricing.