methodology review seminar - am bestseminar etc.venues st.paul’s, london 15 november 2017 1...

TRANSCRIPT

Methodology Review Seminar

etc.venues St.Paul’s, London

15 November 2017

1

Agenda: Methodology Review Seminar 14:15 Welcome & Introduction Overview of the Revised Best's

Credit Rating Methodology Greg Carter, Managing Director, Analytics – EMEA

14:25 Best’s Capital Adequacy Ratio (BCAR) – Key Changes & Impacts Mathilde Jakobsen, Director, Analytics

14:40 Mature Markets Benchmark Analysis - Building Block Approach Carlos Wong-Fupuy, Senior Director

15:00 Emerging Markets Benchmark Analysis - Building Block Approach Mahesh Mistry, Senior Director, Analytics

15:20 Q&A: Interactive Discussion 16:00 Close

2

Disclaimer © AM Best Company (AMB) and/or its licensors and affiliates. All rights reserved. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY COPYRIGHT LAW AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT AMB’s PRIOR WRITTEN CONSENT. All information contained herein is obtained by AMB from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. Under no circumstances shall AMB have any liability to any person or entity for (a) any loss or damage in whole or in part caused by, resulting from, or relating to, any error (negligent or otherwise) or other circumstance or contingency within or outside the control of AMB or any of its directors, officers, employees or agents in connection with the procurement, collection, compilation, analysis, interpretation, communication, publication or delivery of any such information, or (b) any direct, indirect, special, consequential, compensatory or incidental damages whatsoever (including without limitation, lost profits), even if AMB is advised in advance of the possibility of such damages, resulting from the use of or inability to use, any such information. The credit ratings, financial reporting analysis, projections, and other observations, if any, constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements of fact or recommendations to purchase, sell or hold any securities, insurance policies, contracts or any other financial obligations, nor does it address the suitability of any particular financial obligation for a specific purpose or purchaser. Credit risk is the risk that an entity may not meet its contractual, financial obligations as they come due. Credit ratings do not address any other risk, including but not limited to, liquidity risk, market value risk or price volatility of rated securities. NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY AMB IN ANY FORM OR MANNER WHATSOEVER. Each credit rating or other opinion must be weighed solely as one factor in any investment or purchasing decision made by or on behalf of any user of the information contained herein, and each such user must accordingly make its own study and evaluation of each security or other financial obligation and of each issuer and guarantor of, and each provider of credit support for, each security or other financial obligation that it may consider purchasing, holding or selling.

3

Disclaimer US Securities Laws explicitly prohibit the issuance or maintenance of a credit rating where a person involved in the sales or marketing of a product or service of the CRA also participates in determining or monitoring the credit rating, or developing or approving procedures or methodologies used for determining the credit rating.

No part of this presentation amounts to sales / marketing activity and A.M. Best’s Rating Division employees are prohibited from participating in commercial discussions.

Any queries of a commercial nature should be directed to A.M. Best’s Market Development function.

4

Update on Best's Credit Rating Methodology (BCRM)

Greg Carter Managing Director, Analytics - EMEA

5

BCRM Building Blocks

6

BCRM Building Blocks

Assessment

Strongest

Very Strong

Strong

Adequate

Weak

Very Weak

Assessment

Very Strong +2

Strong +1

Adequate 0

Marginal -1

Weak -2

Very Weak -3

Assessment

Very Favorable +2

Favorable +1

Neutral 0

Limited -1

Very Limited -2

Assessment

Very Strong +1

Appropriate 0

Marginal -1

Weak -2

Very Weak -3/4

7

EMEA – Balance Sheet Strength

Strongest 8.3%

Very Strong 64.5%

Strong 23.7%

Adequate 3.6%

EMEA – Balance Sheet Strength Distribution

0

10

20

30

40

50

60

70

80

VaR 95% VaR 99% VaR 99.5% VaR 99.6% VaR 99.8%

Med

ian

BC

AR S

core

Strongest Very Strong Strong Adequate

EMEA – Median BCAR Score by Balance Sheet Strength

Source: A.M. Best data and research

8

EMEA – Balance Sheet Strength

8 6 14 24 28

46

100 100 75

80 65

72

42

100

16 12 4

0

10

20

30

40

50

60

70

80

90

100

aa aa- a+ a a- bbb+ bbb bbb-

(%)

Strongest Very Strong Strong Adequate

EMEA – Balance Sheet Strength by Long-Term Issuer Credit Rating

Source: A.M. Best data and research

9

BCRM Building Blocks

Assessment

Strongest

Very Strong

Strong

Adequate

Weak

Very Weak

Assessment

Very Strong +2

Strong +1

Adequate 0

Marginal -1

Weak -2

Very Weak -3

Assessment

Very Favorable +2

Favorable +1

Neutral 0

Limited -1

Very Limited -2

Assessment

Very Strong +1

Appropriate 0

Marginal -1

Weak -2

Very Weak -3/4

10

EMEA – Operating Performance

Strong +1 42.0%

Adequate 0 48.5%

Marginal -1 9.5%

EMEA – Operating Performance Notch Distribution

18 22

4 13

34

66

53 39 58

100 100 88

66

32 29 39 38

0

10

20

30

40

50

60

70

80

90

100

aa aa- a+ a a- bbb+ bbb bbb-

(%)

Strong +1 Adequate 0 Marginal -1

EMEA – Operating Performance Notch by Long-Term Issuer Credit Rating

Source: A.M. Best data and research

11

EMEA – Operating Performance

87.5 96.6

106.2

0

20

40

60

80

100

120

+1 0 -1

Strong Adequate Marginal

Med

ian

5-Yr

. Avg

. Com

bine

d R

atio

(%)

EMEA – Median 5-Year Average Combined Ratio by Operating Performance Notch

7.3 7.7

15.7

0

2

4

6

8

10

12

14

16

18

+1 0 -1

Strong Adequate Marginal

Med

ian

10-Y

r. C

ombi

ned

Rat

io S

TD (%

)

EMEA – Median 10-Year Combined Ratio Standard Deviation by Operating Performance Notch

Source: A.M. Best data and research

12

BCRM Building Blocks

Assessment

Strongest

Very Strong

Strong

Adequate

Weak

Very Weak

Assessment

Very Strong +2

Strong +1

Adequate 0

Marginal -1

Weak -2

Very Weak -3

Assessment

Very Favorable +2

Favorable +1

Neutral 0

Limited -1

Very Limited -2

Assessment

Very Strong +1

Appropriate 0

Marginal -1

Weak -2

Very Weak -3/4

13

EMEA – Operating Performance

12.0

7.1

3.5

0

2

4

6

8

10

12

14

+1 0 -1

Strong Adequate Marginal

Med

ian

5-Yr

. Avg

. RO

E (%

)

EMEA – Median 5-Year Average ROE by Operating Performance Notch

6.2

8.1

12.9

0

2

4

6

8

10

12

14

+1 0 -1

Strong Adequate MarginalM

edia

n 10

-Yr.

RO

E ST

D (%

)

EMEA – Median 10-Year ROE Standard Deviation by Operating Performance Notch

Source: A.M. Best data and research

14

BCRM Building Blocks

Assessment

Strongest

Very Strong

Strong

Adequate

Weak

Very Weak

Assessment

Very Strong +2

Strong +1

Adequate 0

Marginal -1

Weak -2

Very Weak -3

Assessment

Very Favorable +2

Favorable +1

Neutral 0

Limited -1

Very Limited -2

Assessment

Very Strong +1

Appropriate 0

Marginal -1

Weak -2

Very Weak -3/4

15

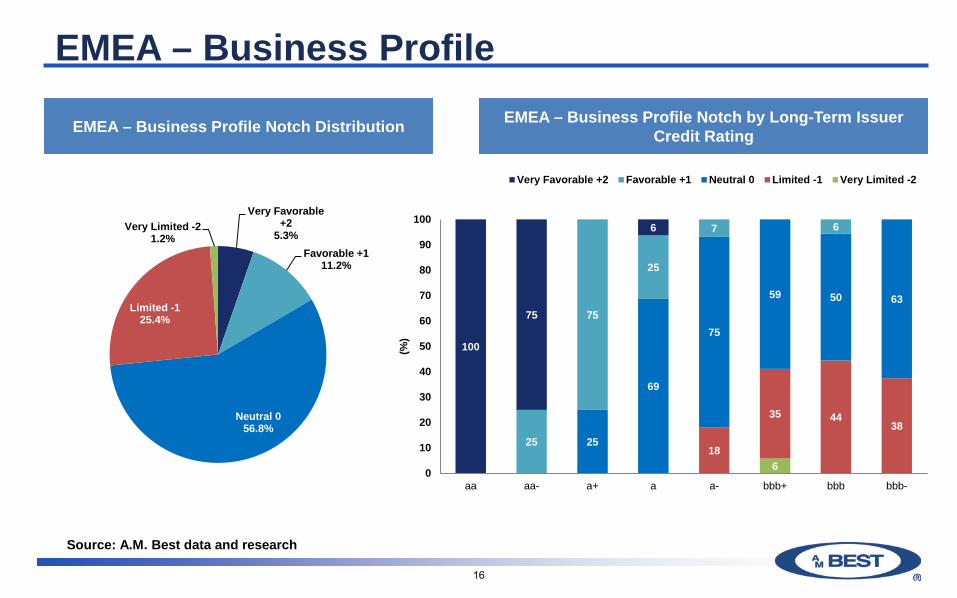

EMEA – Business Profile

Very Favorable +2

5.3% Favorable +1

11.2%

Neutral 0 56.8%

Limited -1 25.4%

Very Limited -2 1.2%

EMEA – Business Profile Notch Distribution

6 18

35 44 38

25

69

75

59 50 63

25

75

25

7 6

100

75

6

0

10

20

30

40

50

60

70

80

90

100

aa aa- a+ a a- bbb+ bbb bbb-

(%)

Very Favorable +2 Favorable +1 Neutral 0 Limited -1 Very Limited -2

EMEA – Business Profile Notch by Long-Term Issuer Credit Rating

Source: A.M. Best data and research

16

BCRM Building Blocks

Assessment

Strongest

Very Strong

Strong

Adequate

Weak

Very Weak

Assessment

Very Strong +2

Strong +1

Adequate 0

Marginal -1

Weak -2

Very Weak -3

Assessment

Very Favorable +2

Favorable +1

Neutral 0

Limited -1

Very Limited -2

Assessment

Very Strong +1

Appropriate 0

Marginal -1

Weak -2

Very Weak -3/4

17

EMEA – Enterprise Risk Management

Very Strong +1 5.3%

Appropriate 0 71.6%

Marginal -1 14.8%

Weak -2 8.3%

EMEA – Enterprise Risk Management Notch Distribution

17 9

18

28

25 50

88

84 98

82

67 58

100

50

13 6

0

10

20

30

40

50

60

70

80

90

100

aa aa- a+ a a- bbb+ bbb bbb-

(%)

Very Strong +1 Appropriate 0 Marginal -1 Weak -2

EMEA – Enterprise Risk Management Notch by Long-Term Issuer Credit Rating

Source: A.M. Best data and research

18

Best's Capital Adequacy Ratio (BCAR)

Mathilde Jakobsen Director, Analytics

19

• Overview of BCAR • Interpreting BCAR scores • Model differences

Agenda

20

Summary of Model Changes

• Stochastic-based risk factors applied within the model – Factors generated using stochastic simulations from

probability curves and ESG • Basis of risk measurement is Value at Risk (VaR) • 5 scores calculated instead of 1

– Net Required Capital calculated at 95%, 99%, 99.5%, 99.6%, and 99.8% confidence levels

21

Summary of Model Changes

22

BCAR Assessment VaR Confidence Level (%)

BCAR BCAR Assessment

99.6 >25 at 99.6 Strongest

99.6 > 10 at 99.6 & ≤ 25 at 99.6 Very Strong

99.5 > 0 at 99.5 & ≤ 10 at 99.6 Strong

99 > 0 at 99 & ≤ 0 at 99.5 Adequate

95 > 0 at 95 & ≤ 0 at 99 Weak

95 ≤ 0 at 95 Very Weak

23

BCARs Support Strong Balance Sheet Assessments

-20

-10

0

10

20

30

40

50

60

70

80

VaR 95% VaR 99% VaR 99.5% VaR 99.6% VaR 99.8%

Med

ian

BC

AR S

core

Strongest Very Strong Strong Adequate

EMEA Mature Markets – Median BCAR Score by Balance Street Strength

Source: A.M. Best data and research

24

Interpreting BCARs

-120-100

-80-60-40-20

020406080

100VAR 95 VAR 99 VAR 99.5 VAR 99.6 VAR 99.8

BCAR

Company A: Available Capital is 4*NRC at VAR 95 Company B: Available Capital = 3* NRC at VAR 95

Company C: Available Capital = 2* NRC at VAR 95 Company D: Available Capital = 1*NRC at VAR 95

• Net required capital (NRC) is the same for companies A, B, C and D at all VARs • The slope becomes steeper, as the BCAR at VAR 95 reduces

25

Model Differences…

… that can now drive a different assessment of risk-adjusted capitalisation, as measured by BCAR Difference Potential Effect Higher charges for equity and for low credit quality fixed income, especially with long durations

A lower BCAR assessment where net required capital is driven by investment risk

Lower charge for non-rated reinsurance recoverables

A higher BCAR assessment where net required capital is driven by counterparty credit risk

Catastrophe risk included within covariance adjustment

A higher BCAR assessment for catastrophe-exposed companies

26

Mature Markets Benchmark Analysis -

Building Block Approach

Carlos Wong-Fupuy Senior Director

27

EMEA – Mature Markets / Building Block Approach

• Country Risk Tiers 1 and 2 Europe, Middle East and Africa covered from the London office

Source: Best's Credit Rating Methodology

28

EMEA – Mature Markets / Balance Sheet Strength

• No cases of “Weak” or “Very Weak”.

• BCAR ≠ Balance sheet strength assessment.

• Negative BCARs in only a few cases.

Strongest 9.0%

Very Strong 73.0%

Strong 13.5%

Adequate 4.5%

-20-10

01020304050607080

VaR 95% VaR 99% VaR 99.5% VaR 99.6% VaR 99.8%

Med

ian

BC

AR S

core

Strongest Very Strong Strong Adequate

EMEA Mature Markets – Balance Sheet Strength Distribution

EMEA Mature Markets – Median BCAR Score by Balance Sheet Strength

Source: A.M. Best data and research

29

EMEA – Mature Markets / Balance Sheet Strength

100

8 19 22

50

100 100 81 75 67

50

100

8 11

0

10

20

30

40

50

60

70

80

90

100

aa aa- a+ a a- bbb+ bbb bbb-

(%)

Strongest Very Strong Strong Adequate

EMEA Mature Markets – Balance Sheet Strength by Long-Term Issuer Credit Rating

• Sector strongly capitalised • Wide variety of companies

• Strong correlation between balance sheet assessment and ICRs, but with some exceptions

Source: A.M. Best data and research

30

EMEA – Mature Markets / Operating Performance

• Small proportion of “Marginal” assessment

• In general, positive correlation with ICRs

• “bbb-” category an exception: subsidiaries with balance sheet strength pressures

Strong +1 40.5%

Adequate 0 52.8%

Marginal -1 6.7%

33 50

13

38

81

67 50

100 100 100 88

62

16

0102030405060708090

100

aa aa- a+ a a- bbb+ bbb bbb-(%

)

Strong +1 Adequate 0 Marginal -1

EMEA Mature Markets – Operating Performance Notch Distribution

EMEA Mature Markets – Operating Performance Notch by Long-Term Issuer Credit Rating

31

EMEA – Mature Markets / Operating Performance

• Good average combined ratios despite market pressures

• No cases under extreme categories of “Very Strong”, “Weak” or “Very Weak”

• Adaptability to pressures on profit margins will be key going forward

• Volatility is another important factor in the O/P assessment

• A few “marginal” cases: small, niche or subsidiaries under re-structuring

86.0

94.9

103.2

75

80

85

90

95

100

105

+1 0 -1

Strong Adequate Marginal

Med

ian

5-Yr

. Avg

. Com

bine

d R

atio

(%)

6.0 7.6

14.4

0

2

4

6

8

10

12

14

16

+1 0 -1

Strong Adequate Marginal

Med

ian

10-Y

r. C

ombi

ned

Rat

io S

TD (%

)

Mature Markets – Median 5-Year Average Combined Ratio by Operating Performance

Notch

Mature Markets – Median 10-Year Combined Ratio Standard Deviation by Operating

Performance Notch

Source: A.M. Best data and research

32

EMEA – Mature Markets / Business Profile

Very Favorable

+2 9.0%

Favorable +1

18.0%

Neutral 0 59.5%

Limited -1 13.5%

13

44

100

25

73

78

56

100

25

75

23

9

100

75

0

10

20

30

40

50

60

70

80

90

100

aa aa- a+ a a- bbb+ bbb bbb-

(%)

Very Favorable +2 Favorable +1 Neutral 0 Limited -1

EMEA Mature Markets – Business Profile Notch Distribution

EMEA Mature Markets – Business Profile Notch by Long-Term Issuer Credit Rating

• Positive correlation with ICRs

• “bbb-” the exception: cases where balance sheet pressures are dominant

Source: A.M. Best data and research

33

EMEA – Mature Markets / Business Profile

• Market position, a key factor within the business profile assessment

• But it needs to be seen alongside the degree of competition in the market where the company operates

Assessment Notch Positive Neutral Negative Very Favourable +2 12.5 37.5 50.0

Favourable +1 25.0 31.3 43.7

Neutral 0 17.0 40.4 42.6

Limited -1 - 40.0 60.0

Very Limited -2

Assessment Notch Positive Neutral Negative Very Favourable +2 87.5 12.5 -

Favourable +1 93.8 6.2 -

Neutral 0 34.0 55.4 10.6

Limited -1 10.0 50.0 40.0

Very Limited -2

EMEA Mature Markets – Market Position by Business Profile Notch

EMEA Mature Markets – Degree of Competition by Business Profile Notch

Source: A.M. Best data and research

34

EMEA – Mature Markets / Enterprise Risk Management

• Maximum of +2 notches in cases of “Very Favorable” business profile and “Very Strong” ERM assessment

• EMEA – mature markets in general highly regulated / Solvency II regime

• Some leading players and pioneers in developing ERM

• “Marginal” cases driven by significant volatility in underwriting results offset by strong capitalisation and / or parental support

Very Strong +1 10.1%

Appropriate 0 87.7%

Marginal -1 2.2%

EMEA Mature Markets – Enterprise Risk Management Notch Distribution

Source: A.M. Best data and research

35

EMEA – Mature Markets / Conclusions

• Main features: very robust balance sheets, adequate and strong operating performance,

neutral business profiles and appropriate ERM

• About 3% of companies under review as a result of the updated BCRM

Stable 86.6%

Positive 2.2%

Negative 4.5%

Under Review

6.7%

EMEA Mature Markets – Long-Term Issuer Credit Rating Outlooks

EMEA Mature Markets – Long-Term Issuer Credit Rating Distribution

Source: A.M. Best data and research. The ICR rating distribution is shown as of October 17, 2017

Superior 'aa' 11.2%

Excellent 'a' 76.4%

Good 'bbb' 12.4%

36

Emerging Markets Benchmark Analysis -

Building Block Approach

Mahesh Mistry Senior Director

37

Emerging - EMEA Markets / Country Risk • Emerging EMEA:

Country Risk Tiers 3, 4 and 5 (Europe, Middle East and Africa covered from the London office)

• Country risk is incorporated into the assessment of balance sheet strength, operating performance and business profile

• Country specific factors that will adversely affect an insurer’s ability to meet its financial obligations: economic risk, political risk, and financial system risk

• Greater uncertainty, volatile external conditions, developing regulatory regimes

38

Emerging - EMEA Markets / Country Risk

39

Emerging - EMEA / Balance Sheet Strength

• Balance sheet strength assessment mainly “Very Strong” to “Strong” • No cases of “Weak” or “Very Weak” balance sheet assessments • Most companies have “Strongest” or “Very Strong” BCAR positions • Capital requirements generally driven by investment risk

Strongest 7.5%

Very Strong 55.0%

Strong 35.0%

Adequate 2.5%

Emerging Markets – Balance Sheet Strength Distribution

-20

0

20

40

60

80

100

VaR 95% VaR 99% VaR 99.5% VaR 99.6% VaR 99.8%

Med

ian

BC

AR S

core

Strongest Very Strong Strong Adequate

Emerging Markets – Median BCAR Score by Balance Sheet Strength

40

Emerging - EMEA / Balance Sheet Strength

• Sector strongly capitalised • Strong correlation between balance sheet assessment and ICRs • Country risk has a bearing on the outcome • Negatives: quality of assets, reinsurance dependence, reserve quality

33 25 21

50 60

75

50

67

50

92

62 79

45 40

25

50 50

8 13 5

0

10

20

30

40

50

60

70

80

90

100

a a- bbb+ bbb bbb- bb+ bb bb- b+

(%)

Strongest Very Strong Strong Adequate

Emerging Markets – Balance Sheet Strength by Long-Term Issuer Credit Rating

Source: A.M. Best data and research

41

Emerging - EMEA / Operating Performance

• Consider past and prospective performance • No companies have “Very Strong”, “Weak” or “Very Weak” assessment • In general, positive correlation with ICRs

Strong +1 43.8%

Adequate 0 43.8%

Marginal -1 12.4%

Emerging Markets – Operating Performance Notch Distribution

14 5

25

50 67

17 25

38

36 55

100

75

50 33

83 75

62 50

40

0

10

20

30

40

50

60

70

80

90

100

a a- bbb+ bbb bbb- bb+ bb bb- b+

(%)

Strong +1 Adequate 0 Marginal -1

Emerging Markets – Operating Performance Notch by Long-Term Issuer Credit Rating

Source: A.M. Best data and research

42

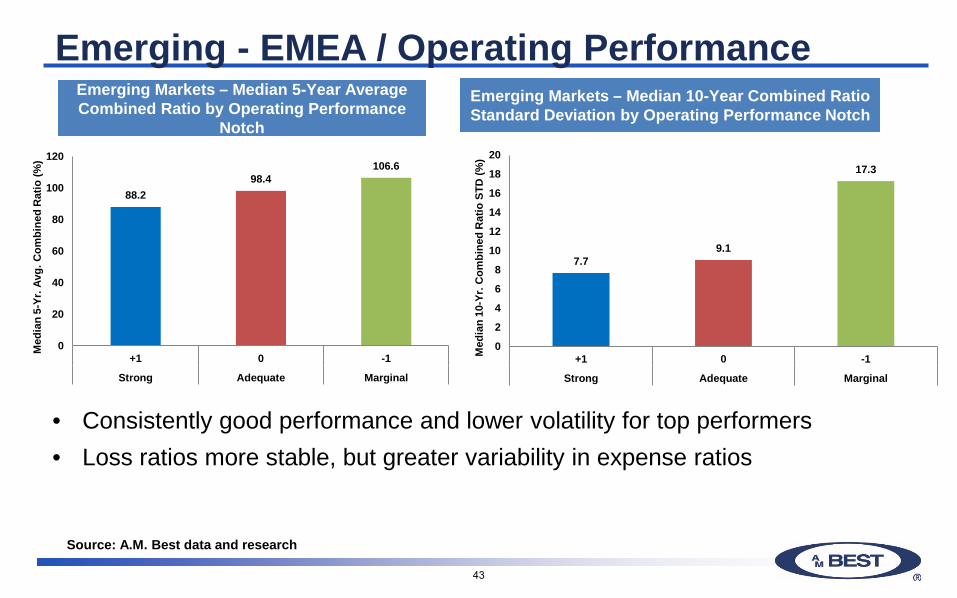

Emerging - EMEA / Operating Performance

• Consistently good performance and lower volatility for top performers • Loss ratios more stable, but greater variability in expense ratios

88.2 98.4

106.6

0

20

40

60

80

100

120

+1 0 -1

Strong Adequate Marginal

Med

ian

5-Yr

. Avg

. Com

bine

d R

atio

(%)

Emerging Markets – Median 5-Year Average Combined Ratio by Operating Performance

Notch

7.7 9.1

17.3

0

2

4

6

8

10

12

14

16

18

20

+1 0 -1

Strong Adequate Marginal

Med

ian

10-Y

r. C

ombi

ned

Rat

io S

TD (%

)

Emerging Markets – Median 10-Year Combined Ratio Standard Deviation by Operating Performance Notch

Source: A.M. Best data and research

43

Emerging - EMEA / Operating Performance

• Consistently good performance and lower volatility for top performers • Investment a key contributor to earnings; although adds volatility • Consider operating environment; interest rates, inflation, currency risk • Movements in ‘other comprehensive income’ adds further volatility

13.0

10.5

4.1

0

2

4

6

8

10

12

14

+1 0 -1

Strong Adequate Marginal

Med

ian

5-Yr

. Avg

. RO

E (%

)

4.8

9.0

15.9

0

2

4

6

8

10

12

14

16

18

+1 0 -1

Strong Adequate Marginal

Med

ian

10-Y

r. R

OE

STD

(%)

Emerging Markets – Median 10-Year return on equity Standard Deviation by Operating Performance Notch

Emerging Markets – Median 5-Year Average return on equity by Operating Performance

Notch

Source: A.M. Best data and research

44

Emerging - EMEA / Business Profile

• Less correlation between ICRs and business profile • Neutral: mainly leading positions in local market; small globally • Limited: mid-sized companies with good access to business;

no product differentiation

Very Favorable

+2 1.3%

Favorable +1

3.8%

Neutral 0 53.8%

Limited -1 38.6%

Very Limited -2

2.5%

Emerging Markets – Business Profile Notch Distribution

13

33 25

29 41

60

25

100 100

50

67 62 64

59

40

75 33

7 17

0

10

20

30

40

50

60

70

80

90

100

a a- bbb+ bbb bbb- bb+ bb bb- b+

(%)

Very Favorable +2 Favorable +1 Neutral 0 Limited -1 Very Limited -2

Emerging Markets – Business Profile Notch by Long-Term Issuer Credit Rating

Source: A.M. Best data and research

45

Emerging - EMEA / Enterprise Risk Management

• No companies given “Very Favorable” ERM assessment • Diverse ERM practices across emerging market companies • Difficult to mitigate all economic, political and financial system risks within

a country

Appropriate 0

53.7% Marginal -1

28.8%

Weak -2 17.5%

Emerging Markets – Enterprise Risk Management Notch Distribution

7 18 20 25

100

67

33

8 25

36 27

40

75

33

67

92 75

57 55 40

0

10

20

30

40

50

60

70

80

90

100

a a- bbb+ bbb bbb- bb+ bb bb- b+(%

) Appropriate 0 Marginal -1 Weak -2

Emerging Markets – Enterprise Risk Management Notch by Long-Term Issuer Credit Rating

Source: A.M. Best data and research

46

• Emerging - EMEA main features: robust balance sheets, strong to adequate operating performance, neutral to limited business profiles and appropriate to marginal ERM

• About 2% of companies under review as a result of the updated BCRM

Emerging - EMEA / Conclusions

Excellent 25.0%

Good 53.9%

Fair & Below 21.1%

Emerging Markets – Long-Term Issuer

Credit Rating Distribution

Stable 73.7% Positive

3.9%

Negative 13.2%

Under Review 9.2%

Emerging Markets – Long-Term Issuer Credit Rating

Distribution

Source: A.M. Best data and research. The ICR rating distribution is shown as of October 17, 2017

47

Methodology Review Seminar

etc.venues St.Paul’s, London

15 November 2017

48