message from - century 21 saudicentury21saudi.com/public/uploaded/riyadh-real...audi arabia...

TRANSCRIPT

Al Waleed BinzoumanGeneral Manager

2013 was highly productive year for KSA real estate sector. We observed completion of several projects and in parallel we witnessed announcements for several new residential and commercial developments. In 2014 real estate sector will maintain its solid growth momentum.

Since inception, Century21Saudi has stood as one of the most trusted and reputable real estate marketing and consultancy firm, serving through its six fully operational offices across KSA.

Century21Saudi has continued to grow and evolve with the changing time and continues to be at the forefront of real estate marketing and consultancy industry. Century21Saudi’s dedication and commitment to its clients remain and will continue to be the very essence of the company. We always put ourselves in the shoes of our clients and offer our services to meet and even exceed their demands.

After a wide acceptance and appreciation of our “Riyadh Real Estate Market Overviews” and after receiving a lot of requests to have same sort of report for other major cities of KSA, Cenury21Saudi is glad to present “KSA Real Estate Market Overview H1-2014”. The underneath report will cover real estate markets of Riyadh, Jeddah, and Dammam/Al Khobar. This issue of KSA Real Estate Market Overview will provide you a snapshot of real estate activities during first half of 2014.

In the years ahead, the force of rapid technological & demographical changes will bring new challenges for the real estate sector. I, together with our staff look forward to taking on new challenges in the future with the continued support of our clients and business partners.

Message fromGeneral Manager

4 CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

ECONOMY

KSA

Saudi Arabia continued its strong economic growth during first half of 2014, backed by elevated government spending, and thriving petroleum sector. Saudi Arabia, set its 2014

budget spending at a record SR 855 billion which is equal to country’s projected revenue. Budgeted spending is at another all-time high in 2014, as the government continues with its program to upgrade the human and physical infrastructure, and meet the demand of a rapidly growing population. Greater execution of government investment projects, especially in the infrastructure sector, means that non-oil growth will maintain the current solid performance.

2014 is a healthy year for KSA economy with the forecasted GDP growth rate of 3.6%. Construction, retail and transportation in non-oil private sector are showing strong growth followed by communication and manufacturing sectors. Non-Oil GDP growth is expected to be above 5% during 2014.

Inflation rate fell with a significant proportion and reach at 2.6% during first half of 2014. Lower food prices inflation is the main reason of this decline. Rental inflation picked up slightly during H1-2014. The surge in consumer spending resulting from higher government sector wages and other labor market reform initiatives has their impact on inflation.

It is expected that in 2014 the Economy will maintain its solid growth impetus. Progress of government initiated infrastructure projects will have a positive effect on non-oil sector growth. Government spending will remain a key factor to support non-oil economy.

KSA Economic Overview

Year Revenue Expenditure Surplus/Deficit

Projected Actual Projected Actual Projected Actual

2011 540 1110 580 804 - 40 206

2012 702 1240 690 853 12 387

2013 829 1131 820 925 9 206

2014 855 - 855 - - -

KSA Annual Budget ( Projected VS Actual - SR Billion )

Nominal & Real GDP Growth (SR Billion)

2010 2011 2012 2013 2014 (F)

Nomimal GDP (SR Billion) 1,950 2,500 2,650 2,750 2,850

GDP Growth Rate (%) 6.8% 8.6% 7.0% 4.2% 3.8%

0.0%

2.3%

4.5%

6.8%

9.0%

0

875

1750

2625

3500

2010 2011 2012 2013 2014 (F)

Nomimal GDP (SR Billion) GDP Growth Rate (%)

April

0

25

50

75

100

Region 1 Region 2

5CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW KSAREAL ESTATE

During first half of 2014, the country’s real estate market experienced sustained growth, underpinned by robust economic development and large government spending. Because of strong macroeconomic drivers of KSA the market is expected to expand further, in the short-to-medium run. Housing and infrastructure are

forecasted to expand the fastest, while the commercial segment will experience limited growth.

Residential Sector:It is obvious that in KSA real demand lies in residential sector where, because of favorable market fundamentals, demand is surpassing supply. Century21Saudi witnessed successful completion of several residential projects during H1-2014, “Bayt Al Hur Residential Project” and “Masharif Hills” are two major under execution projects of 2014 in the residential sector. High expectations of middle class are attached with the first phase low cost housing units announced by the government. Even with these 500,000 units, this housing stock expansion may not be sufficient to meet demand.

Because of undersupplied market sale prices and rental rates showed an escalating trend during first half of the year. Sale prices of residential units increased with a healthy ratio ranges between 4% to 6% in all major cities. Rental rates also showed an increasing trend which ranged between 3% to 6%.

During 2013 government has announced “EJAR” system to regulate the rentals escalation trends and to regulate tenants and landlords rights and obligations. Until now we are unable to track any impact of “EJAR” system on rental market but it is expected that in near future this system will be helpful to regularize the rental market.

Office Sector:In office sector slower development trend was noticed during H1-2014. The major reason behind this trend was oversupplied office market in major cities like Riyadh and Jeddah. A number of new office buildings entered in the market during firt half of 2014, increasing office stock by more than 145,000 square meters. Also, a major shift in tenant’s preference has been witnessed during the year as several multinational firms moved from CBD to newly developed business parks to get the benefits of more professional business environment and smart offices concept. Government and financial institutes remained major demand generator for the office market.

Rental rates in Riyadh showed a diminishing trend during the year while Jeddah & Dammam/Al Khobar market showed stable rental rates with increasing trends at prime locations.

KSA Real Estate Sector

KSA Addressable Market -‐ New Housing Demand

20,000

62,500

105,000

147,500

190,000

20,000

50,000

80,000

110,000

140,000

2010 2011 2012 2013 2014 2015

Saudi naEonals Expatriate KSA Total Demand

KSA

Tota

l Hou

sing

Dem

and

6 CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEWKSAREAL ESTATE

Hospitality Sector:Saudi Arabia’s hotel and hospitality industry is set to grow with inbound travel that continues to increase, thanks to pilgrims and business visitors. Kingdom is already witnessing a boom in the hotel and hospitality sector during last a few years as plans are being executed for increasing hotel rooms, furnished apartments, leisure resorts, restaurants and food outlets.

KSA hospitality market showed signs of stability during H1-2014 as the occupancy rate increased with better RePAR & ADR.

Several international hotels are in construction phase and expected to be operational during 2014-16 which will increase the number of hotel rooms with a substantial amount.

Government recent crackdown on illegal workers resulted in the labor shortage which effected the market and delay in completion of many under construction projects is expected. Also, the developers are revising feasibility studies for future projects as increase in labor cost is effecting their earlier calculations of returns.

Retail Sector:In retail sector the concept of strip retail centers is getting popularity and several strip retail developments are ongoing in Riyadh and Jeddah.

During H1-2014 no major opening has been witnessed in retail sector.

Retail sector has enjoyed better occupancy rates during first half of 2014 because of expansion of existing retailors coupled with entrance of new brands in KSA retail market.

Most of the new developments have better occupancy as the developers managed to prelease a major proportion of their properties.

Retail rentals showed a positive trend during H1-2014 for both strip retail and fully serviced shopping malls.

RiyadhReal Estate Market Overview

8 RIYADH CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

RESIDENTIAL

Riyadh Residential Market is severely under supplied and it seems to be persisting in medium to long run. This is due to a historic dearth of private sector development activity and insufficient provision by the government entities. Although Ministry of Housing commenced work to supply King’s announced 500,000 affordable

housing units for the nationals but it will take several years to be delivered.

Demand for housing is mainly driven by population growth coupled with reduction in average household size and upsurge in disposable income. Inadequate supply is unable to cater mounting demand from Saudi nationals and expatriates as well. This increasing demand supply gap might cause a housing crisis in coming years.

Riyadh Residential Market Overview

Supply & DemandRiyadh residential stock has augmented by 2% during H1-2014 and reached around 955,000 units while more than 90,000 units are due to be delivered in coming years which will surge housing stock up to 1,050,000 units by the end of 2016.

Most of the projects which were scheduled to be delivered in 2013 & H1-2014 are delayed and expected to be completed in H2-2014 and 2015.

Major completion during last year was “Al Rabia Project” which delivered 225 residential units. Moreover 40% of “Ritaj Villas Project” has also been completed and launched for sale.

Recently two new projects “Bayt Al-Hurr” and “Masharif Hills (Phase-I)” were initiated which will deliver 216 and 169 residential units respectively in the coming years. In addition, some high end residential projects are also under construction which will deliver around 500 luxurious villas during 2014-15.

A new mix use development is expected to be announced by end of 2014 which will deliver more than 500 residential units in north of the city.

Project Name No of Units Expected Completion

Rafal Tower 420 2014Manazil Al Qurtuba (Phase-2) 1300 2014

Ritaj Villas 292 2014

Addiyar 1050 2015

Sunset Project 300 2015

Bayt Al Hurr 216 2015Masharif Hills (Phase-1) 169 2015

Anticipated Supply

9RIYADH CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

RESIDENTIAL

Market Performance Riyadh residential market has witnessed a sturdy growth during first half of 2014. Market noticed a steady rise in sale prices and rental rates of residential units due to supply demand gap.

Average sale prices of villas have increased with a ratio of 4% to 6% across most of the districts of Riyadh during H1-2014. While apartment sale prices surged with an average ratio of 4% to 7% in all districts of the city.

Median sale price of a small size villa/duplex ranges between SR 1.3 million to SR 1.8 million, while sale price of a medium size apartment ranges between SR 400,000 to SR 800,000.

Residential Market Trends Total Inventory Supply in Pipeline (Units) Average 3 Bed Apartment Sale Price (SR)

Average Villa/Duplex Sale Price (SR)

Total 955,000 90,000 400,000 to 800,000 1.3m to 1.8m

Market Trends

in Villas Sale Priceincrease

Average Sale prices of Villas (250 -‐ 350 sq m)

Area Min MaxRiyadh East 1,350,000 1,900,000

Riyadh West 1,350,000 1,700,000

Riyadh North 1,450,000 1,850,000

Riyadh South 800,000 1,450,000

Riyadh Central 1,450,000 1,850,000

Average Sale prices of Villas (250 -‐ 350 sq m)

Area Min MaxRiyadh East 1,350,000 1,900,000

Riyadh West 1,350,000 1,700,000

Riyadh North 1,450,000 1,850,000

Riyadh South 800,000 1,450,000

Riyadh Central 1,450,000 1,850,000

Average Sale prices of Villas/Duplexes (250 -‐ 350 sq m)

0

500,000

1,000,000

1,500,000

2,000,000

Riyadh East Riyadh West Riyadh North Riyadh South Riyadh Central

Min Max

10 RIYADH CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

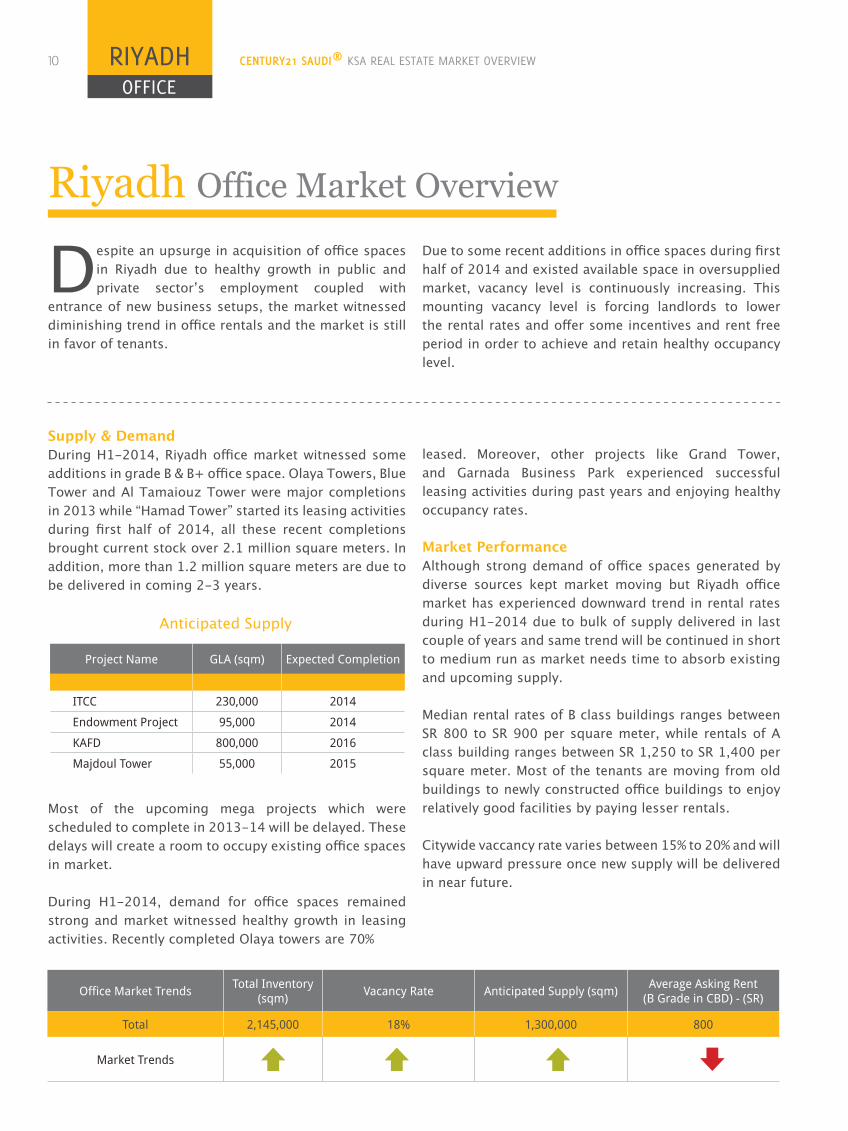

OFFICE

Riyadh Office Market Overview

Despite an upsurge in acquisition of office spaces in Riyadh due to healthy growth in public and private sector’s employment coupled with

entrance of new business setups, the market witnessed diminishing trend in office rentals and the market is still in favor of tenants.

Due to some recent additions in office spaces during first half of 2014 and existed available space in oversupplied market, vacancy level is continuously increasing. This mounting vacancy level is forcing landlords to lower the rental rates and offer some incentives and rent free period in order to achieve and retain healthy occupancy level.

Supply & DemandDuring H1-2014, Riyadh office market witnessed some additions in grade B & B+ office space. Olaya Towers, Blue Tower and Al Tamaiouz Tower were major completions in 2013 while “Hamad Tower” started its leasing activities during first half of 2014, all these recent completions brought current stock over 2.1 million square meters. In addition, more than 1.2 million square meters are due to be delivered in coming 2-3 years.

Most of the upcoming mega projects which were scheduled to complete in 2013-14 will be delayed. These delays will create a room to occupy existing office spaces in market.

During H1-2014, demand for office spaces remained strong and market witnessed healthy growth in leasing activities. Recently completed Olaya towers are 70%

leased. Moreover, other projects like Grand Tower, and Garnada Business Park experienced successful leasing activities during past years and enjoying healthy occupancy rates.

Market Performance Although strong demand of office spaces generated by diverse sources kept market moving but Riyadh office market has experienced downward trend in rental rates during H1-2014 due to bulk of supply delivered in last couple of years and same trend will be continued in short to medium run as market needs time to absorb existing and upcoming supply.

Median rental rates of B class buildings ranges between SR 800 to SR 900 per square meter, while rentals of A class building ranges between SR 1,250 to SR 1,400 per square meter. Most of the tenants are moving from old buildings to newly constructed office buildings to enjoy relatively good facilities by paying lesser rentals.

Citywide vaccancy rate varies between 15% to 20% and will have upward pressure once new supply will be delivered in near future.

Office Market Trends Total Inventory(sqm) Vacancy Rate Anticipated Supply (sqm) Average Asking Rent

(B Grade in CBD) - (SR)

Total 2,145,000 18% 1,300,000 800

Market Trends

Project Name GLA (sqm) Expected Completion

ITCC 230,000 2014

Endowment Project 95,000 2014

KAFD 800,000 2016

Majdoul Tower 55,000 2015

Anticipated Supply

11RIYADH CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

RETAIL

Riyadh Retail Market Overview

KSA’s retail sector witnessed a robust growth during last decade and became the largest in GCC followed by UAE and Qatar. This growth has

vastly attributed to healthy economic growth, increase in disposable income, relatively young population and rapid urbanization in recent years.

Riyadh is one the favorite destination for international brands and hosting number of high end luxury brands. Moreover Riyadh has one of the highest densities of retail outlets and also seen the highest growth rate of retailers as compare to other developed cities.

Supply & DemandNo major addition in retail malls segment has been witnessed during last six months. Other than Ethra mall no significant mall based retail activity was monitored in 2013. Balancia Bazar is at final stages of completion and already started its leasing activities.

A considerable increase has been noticed in retail stock by strip retail centers during 2013. In addition, number of new strip retail centers including “Telal Center”, “Alia Plaza”, “Yarmouk Center”, and “Yasmeen Center” are under construction which will be completed in coming 6-8 months.

The total stock of retail space in Riyadh will cross 3 million square meters after completion of KAFD & ITCC as these projects will offer more than 150,000 square meter of quality retail space. Total shopping malls based stock will reach to 1.5 million square meter by the end of 2015.

Project Name GLA (sqm) Expected Completion

Balancia Bazar 35,000 2014

Nakheel Mall 66,329 2014

Malaz Mall 71,225 -

Average Showroom Rental Rate (Outside Mall) -‐ (SR/sqm)

Area Min MaxRiyadh East 550 1,200

Riyadh West 500 1,000

Riyadh North 550 1,200

Riyadh South 450 850

Riyadh Central 750 2,200

Average Showroom Rental Rate (Outside Mall) -‐ (SR/sqm)

0

550

1,100

1,650

2,200

Riyadh East Riyadh West Riyadh North Riyadh South Riyadh Central

Min Max

Retail Market TrendsCurrent Retail Space (sqm)

Vacancy Rate Future Supply (sqm)Average per sqm Asking Rents in

CBD (Outside Malls)

Total 2,600,000 10% - 20% 475,000 SR 1,100 – SR 2,100

Market Trends

Market PerformanceMedian rental rates remained stable in most areas of the city, while a slight increase in rentals have been witnessed at the prime locations during H1-2014.

Rental rates of strip retail ranges between SR 1,100 per square meter to SR 2,100 per square meter in CBD and Northern areas of Riyadh.

Riyadh North and East will host most of the upcoming retail supply, while Western areas are lacking in good quality retail space.

Anticipated Supply

12 RIYADH CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

HOSPITALITY

Riyadh Hospitality Market Overview

KSA Hospitality sector is continuously growing and contribution of hospitality market in GDP witnessed a modest upsurge in H1-2014. In an

effort to achieve its economic diversification, the KSA government is taking numerous initiatives including expansion of Holy Mosques, expansion of international airports, and arrangement of cultural events in different cities.

The government has made enormous investments to develop the sector in order to boost both religious and cultural tourism in the country.

Riyadh is accommodating 5% of total number of FAU and hotel rooms of the Kingdom, where more than 65% of existing facilities fall in 4 & 5 star categories.

Supply & DemandWith the opening of Burj Rafal Hotel Kempinski, Narcissus Hotel and Courtyard by Marriott, around 1,000 keys were added during 2013 and first half of 2014. Including this addition Riyadh hotel room count is now more than 10,000.

Starwood Hotels & Resorts introduced its brand named “Four Points” by Sheraton in KSA by opening their first hotel in Riyadh in 2013 and “Mena Grand Khaldia Hotel” was rebranded as “Four Points”.

By the end of 2014, a mix use development is expected to be announced which will deliver total 294 rooms including 192 hotel rooms and 102 furnished apartment units in north of Riyadh.

Market PerformancePrior to 2013, Riyadh hospitality market experienced a dwindling trend after global financial crises. In 2013, market showed signs of stability as occupancy rates and average daily rates witnessed a moderate increase. During H1-2014 hospitality market showed stable performance in terms of occupancy rates as it increased with a modest ratio but average daily rates witnessed a slight decline which caused reduction in RevPAR.

This stability is attributed to slight growth in demand and limited supply during 2013 as many of scheduled projects are delayed and will be delivered in 2014-15.

Hospitality Market Trends Total Inventory Occupancy Rate Supply in Pipeline (Rooms)Average Daily Rate (4 & 5 Star Hotels)

Total 10,500 65% 7,500 SR 995

Market Trends

Name of Hotel No. of Rooms Opening Year

Fairmont hotel(Riyadh Business Gate) 287 2014

Movenpick Riyadh 445 2014

Hilton Riyadh Hotel & Residence 830 2014

Hyatt Regency Olaya Riyadh 294 2014

Intercontinental Hotel (KAFD) 218 2016

Wyndham Hotel (KAFD) 210 2016

Riyadh Hotel Occupancy Rates & ADR

2008 2009 2010 2011 2012 2013 2014 (F)

Occupancy Rate 75% 68% 59% 63% 60% 63% 67%

ADR (SR) 938 1,050 975 1,031 994 1,013 935

74 62 59 64 57 56

241 265 248 264 256 255

903.75 993.75 930 990 960 956.25

Riyadh Hotel Occupancy Rates & ADR

0%

20%

40%

60%

80%

100

340

580

820

1,060

2008 2009 2010 2011 2012 2013 2014 (F)

Occupancy Rate ADR (SR)

Anticipated Supply

13RIYADH CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

LANDS

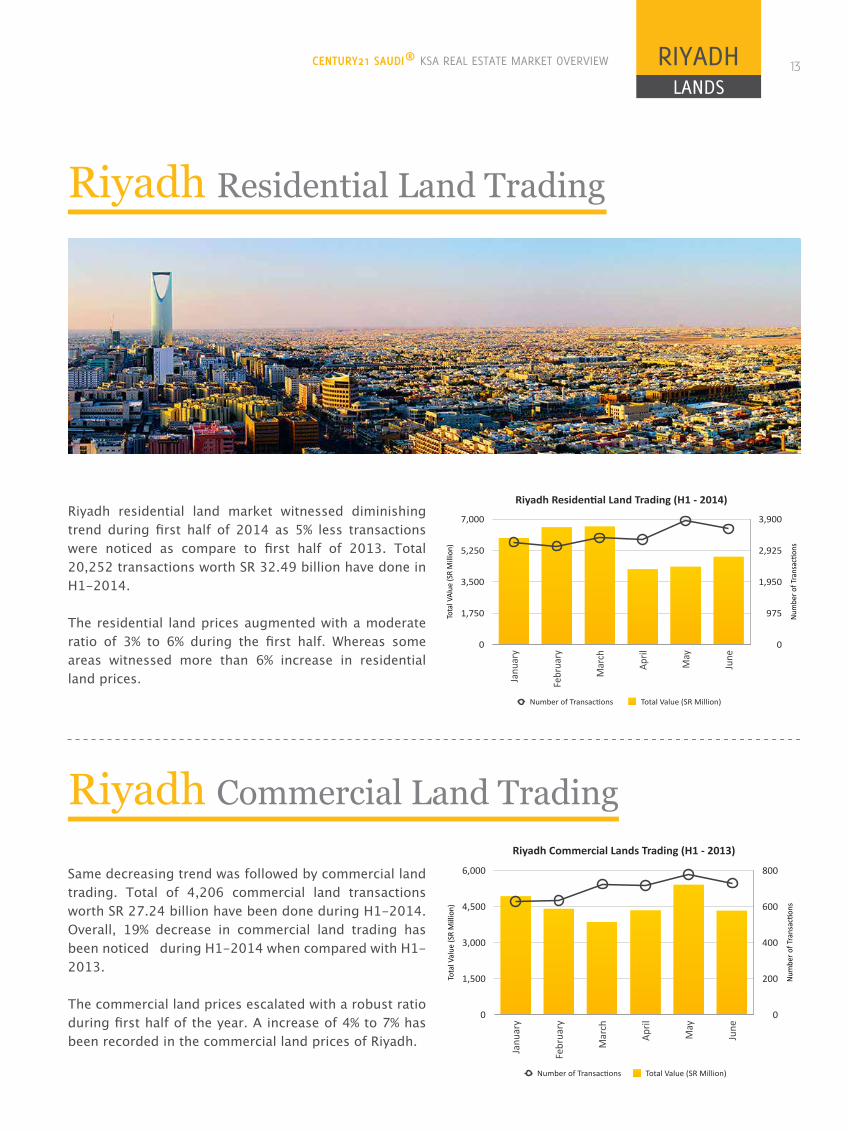

Riyadh Residential Land Trading

Riyadh Commercial Land Trading

Riyadh residential land market witnessed diminishing trend during first half of 2014 as 5% less transactions were noticed as compare to first half of 2013. Total 20,252 transactions worth SR 32.49 billion have done in H1-2014.

The residential land prices augmented with a moderate ratio of 3% to 6% during the first half. Whereas some areas witnessed more than 6% increase in residential land prices.

Same decreasing trend was followed by commercial land trading. Total of 4,206 commercial land transactions worth SR 27.24 billion have been done during H1-2014. Overall, 19% decrease in commercial land trading has been noticed during H1-2014 when compared with H1-2013.

The commercial land prices escalated with a robust ratio during first half of the year. A increase of 4% to 7% has been recorded in the commercial land prices of Riyadh.

January February March April May June

Number of Transac+ons 627 633 724 715 778 729

Total Value (SR Million) 4,920 4,404 3,842 4,346 5,399 4,327

Riyadh Commercial Lands Trading (H1 -‐ 2013)

Num

ber o

f Tra

nsac

/ons

0

200

400

600

800

Tota

l Val

ue (S

R M

illio

n)

0

1,500

3,000

4,500

6,000

Janu

ary

Febr

uary

Mar

ch

April

May

June

Number of Transac/ons Total Value (SR Million)

January February March April May June

Number of Transac+ons 3,183 3,058 3,310 3,260 3,843 3,598

Total Value (SR Million) 5,946 6,549 6,581 4,191 4,333 4,898

Riyadh Residen+al Land Trading (H1 -‐ 2014)

Num

ber o

f Tra

nsac

/ons

0

975

1,950

2,925

3,900

Tota

l VAl

ue (S

R M

illio

n)

0

1,750

3,500

5,250

7,000Ja

nuar

y

Febr

uary

Mar

ch

April

May

June

Number of Transac/ons Total Value (SR Million)

14 RIYADH CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

PRICES

Average Annual Rents for Apartments(130 - 160 sq m) (SR)

Area Min MaxRiyadh East 20,000 30,000

Riyadh West 19,000 35,000

Riyadh North 30,000 40,000

Riyadh South 17,500 25,000

Riyadh Central 32,000 45,000

Average Sale Prices of Apartments(130 - 160 sq m) (SR)

Area Min MaxRiyadh East 450,000 600,000

Riyadh West 375,000 650,000

Riyadh North 500,000 750,000

Riyadh South 300,000 450,000

Riyadh Central 550,000 850,000

Average Sale prices of Villas(250 - 350 sq m)

Area Min MaxRiyadh East 1,200,000 1,650,000

Riyadh West 1,350,000 1,700,000

Riyadh North 1,450,000 1,850,000

Riyadh South 800,000 1,300,000

Riyadh Central 1,450,000 1,950,000

Retail Showrooms Rental Rates( Line Shops -Outside Malls) ( SR/Sq m)

Area Min MaxRiyadh East 550 950

Riyadh West 500 1,000

Riyadh North 800 1,200

Riyadh South 400 750

Riyadh Central 1,100 2,100

Area Min Max

Riyadh EastAl Hamra 2,350 2,950

Al Yarmook 1,600 1,950

Al Naseem 1,000 1,400

Riyadh WestWadi Laban 1,700 2,200

Arqa 1,800 2,100

Riyadh NorthAl Qeerwan 1,700 1,900

Al Rabeeh 2,600 3,000

Al Wadi 1,800 2,200

Riyadh SouthDar Albaiza 900 1,100

Al Mansooriah 1,100 1,400

Taweeq 800 1,000

Riyadh CenteralAl Rabwa 2,000 2,500

King Fahad 2,000 2,500

Salahuddin 2,500 3,000

Area Min Max

Riyadh EastEastern Ring Road 4,500 6,000

Omar Bin Abdulaziz Road 4,000 4,500Imam Saud bin Abdul Aziz Road 4,000 4,500

Riyadh WestWestern Ring Road 3,500 4,500

Madina Al-Munawrah Road 4,000 4,500

Riyadh NorthNorthern Ring Road 7,500 10,000

Anas bin Malik Road 5,000 7,000

Al Khair Road 4,000 5,000

Riyadh SouthKharj Road 1,800 2,000Ayesha bint Abu Bakkar Road 3,500 4,500

Riyadh CenteralKing Fahad Road 17,000 22,000

King Abdul Aziz Road 8,000 8,500

Salah-U-Din Road Malaz 8,000 10,000

Average Sale Prices of Residential Lands (SR/sq m)

Average Sale Prices of Commercial Lands (SR/sq m)

JeddahReal Estate Market Overview

16 JEDDAH CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

RESIDENTIAL

Jeddah residential market is in immense need of vast supply of new housing. This severe shortage in residential supply is because of expanding population

and current government initiatives to resettle the people living in unplanned settlements.

Jeddah Development & Urban Regeneration Co (JDURC) is playing very active role to transform the life quality of Jeddah residents through large scale urban regeneration, housing and infrastructure projects. JDURC is mainly active in development of affordable housing for low income nationals with the aim to fill the demand supply gap for affordable housing.

Projects initiated by private developers are mainly targeting upper middle class segment because of better financial returns.

Jeddah Residential Market Overview

Supply & DemandIt is estimated that in Jeddah above 40,000 new housing units are required annually. Approximately half of the residential demand in Jeddah is from low income residents. North of Jeddah is attributed to have highest residential demand from upper middle class as the area is developing its image as well refined residential area with all required services.

Around 9,000 residential units were completed in Jeddah during H1-2014. Most of the supply was delivered by small and medium developers. A few relatively bigger projects were also part of the supply including “Diyar Jeddah” and “Masharef” projects.

It is expected that around 75,000 residential units will be delivered during coming three to five years. Major upcoming developments will be done by JDURC which collectively will deliver more than 20,000 residential units.

Further, Dar Al Arkan is actively working on “Shams Al Arous Project” and it is expected that the project will add substantial number of residential units in Jeddah residential supply in coming years.

units are requiredannually

NewHousing

17JEDDAH CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

RESIDENTIAL

Market PerformanceResidential sale prices generally displayed stability or increased with decreasing proportion in western and southern areas while central and western parts witnessed a healthy increase in unit prices. High end waterfront projects showed a better acceptance in the market despite of having high prices.

Residential rental rates of apartments and villas showed an increasing trend in north and west with an average escalation of 3% to 6% during first half of 2014 while rental rates in south and east remained stable. Rental market in southern part of Jeddah has been suffering because of current government initiatives and crack down on illegal workers as south of Jeddah is home for most of low income labors.

Residential Market Trends Total InventorySupply in Pipeline

(Units)Average 3 Bed Apartment

Sale Price (SR)Average Villa/Duplex Sale

Price (SR)

Total 768,000 70,000 480,000 to 650,000 1.3m to 2.2m

Market Trends

RentVilla Apartment (130-‐160 sqm)

Jeddah East 60,192 24,423 Jeddah West 116,607 40,625 Jeddah North 118,929 40,000 Jeddah South 60,000 26,094 Jeddah Central 90,357 35,455

SaleVilla Apartment (130-‐160 sqm)

Jeddah East 1,494,231 417,308 Jeddah West 2,975,000 678,125 Jeddah North 2,282,143 662,500 Jeddah South 1,530,000 434,667 Jeddah Central 2,271,429 565,455

Land prices per sqm

Jeddah East 1,985 Jeddah West 5,214 Jeddah North 5,625 Jeddah South 3,921 Jeddah Central 4,846

Residen'al Rental Prices

0

30,000

60,000

90,000

120,000

Jeddah East Jeddah West Jeddah North Jeddah South Jeddah Central

Villa Apartment

Residen'al Sale Prices

0

750,000

1,500,000

2,250,000

3,000,000

Jeddah East Jeddah West Jeddah North Jeddah South Jeddah Central

Villa Apartment

RentVilla Apartment (130-‐160 sqm)

Jeddah East 60,192 24,423 Jeddah West 116,607 40,625 Jeddah North 118,929 40,000 Jeddah South 60,000 26,094 Jeddah Central 90,357 35,455

SaleVilla Apartment (130-‐160 sqm)

Jeddah East 1,494,231 417,308 Jeddah West 2,975,000 678,125 Jeddah North 2,282,143 662,500 Jeddah South 1,530,000 434,667 Jeddah Central 2,271,429 565,455

Land prices per sqm

Jeddah East 1,985 Jeddah West 5,214 Jeddah North 5,625 Jeddah South 3,921 Jeddah Central 4,846

Residen'al Rental Prices

0

30,000

60,000

90,000

120,000

Jeddah East Jeddah West Jeddah North Jeddah South Jeddah Central

Villa Apartment

Residen'al Sale Prices

0

750,000

1,500,000

2,250,000

3,000,000

Jeddah East Jeddah West Jeddah North Jeddah South Jeddah Central

Villa Apartment

6%Apartments&Villas Sale Price

Incrasein

18

OFFICE CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEWJEDDAH

Jeddah Office Market Overview

With the completion of number of large scale projects since last two years, tenants have better opportunities to upgrade their work place with enhanced services. Jeddah office market showed stability during H1-2014 as the rental rates increased at prime business locations with better occupancy rates.

The office market vacancy rate reduced from 15% to 12% during first half of the year. This reduction was mainly due to strong demand from both public and private sector.

Supply & DemandDuring H1-2014, Office demand was mainly driven by companies working as a contractor or sub-contractor for infrastructure, health, and educational projects. Also expansion of some multinationals and local players acted as a demand booster during first half of the year.

Around 28,000 square meters of office stock has been completed during H1-2014. “Sabah Center” is one the major completions during first half. The office market will have a significant increase in supply with the completion of “The Headquarter Business Park” which will add 75,000 square meters in the office space. The project is expected to be completed during second half of 2014.

Market Performance Jeddah office market remained stable during the year and an escalation in the rental rates has been witnessed in grade “A” & “B” class offices. This increase was stronger in “A” class offices at prime business locations. Rental appreciation was mainly because of healthy demand and decrease in vacancy rate.

Average grade “A” office rentals ranged between SR 1,000 to SR 1,250 per square meter while grade “B” rentals ranged between SR 600 to SR 800 per square meter.

As a result of substantial increase in new office space the vacancy rate in older buildings is expected to increase with higher ratio.

Office Market Trends Total Inventory(sqm) Vacancy Rate Y-T-D completed Stock (sqm) Average Asking Rent

(B Grade Offices in CBD)

Total 775,000 12% 28,000 750

Market Trends

District Names 2013Minimum Maximum

Jeddah East 300 850Jeddah West -‐ A Class Office 1000 1250Jeddah West -‐ B Class Office 300 700Jeddah North -‐ A Class Offices 850 1100Jeddah North -‐ B Class Offices 450 800Jeddah South 400 600Jeddah Central -‐ A Class Offices 1100 1350Jeddah Central -‐ B Class Offices 400 950

District Names Minimum(SR/sqm)

Maximum(SR/sqm)

Jeddah East 300 850Jeddah West 300 700Jeddah North 450 800Jeddah South 400 600Jeddah Central 400 950

District Names Minimum(SR/sqm)

Maximum(SR/sqm)

Jeddah West 1000 1250Jeddah North 850 1100Jeddah Central 1100 1350

B Class Office Rentals

0

250

500

750

1000

Jeddah East Jeddah West Jeddah North Jeddah South Jeddah Central

Minimum(SR/sqm) Maximum(SR/sqm)

A Class Office Rentals

0

350

700

1050

1400

Jeddah West Jeddah North Jeddah Central

Minimum(SR/sqm) Maximum(SR/sqm)

District Names 2013Minimum Maximum

Jeddah East 300 850Jeddah West -‐ A Class Office 1000 1250Jeddah West -‐ B Class Office 300 700Jeddah North -‐ A Class Offices 850 1100Jeddah North -‐ B Class Offices 450 800Jeddah South 400 600Jeddah Central -‐ A Class Offices 1100 1350Jeddah Central -‐ B Class Offices 400 950

District Names Minimum(SR/sqm)

Maximum(SR/sqm)

Jeddah East 300 850Jeddah West 300 700Jeddah North 450 800Jeddah South 400 600Jeddah Central 400 950

District Names Minimum(SR/sqm)

Maximum(SR/sqm)

Jeddah West 1000 1250Jeddah North 850 1100Jeddah Central 1100 1350

B Class Office Rentals

0

250

500

750

1000

Jeddah East Jeddah West Jeddah North Jeddah South Jeddah Central

Minimum(SR/sqm) Maximum(SR/sqm)

A Class Office Rentals

0

350

700

1050

1400

Jeddah West Jeddah North Jeddah Central

Minimum(SR/sqm) Maximum(SR/sqm)

19CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW JEDDAH RETAIL

Jeddah Retail Market Overview

Retail is the fourth-largest industry in KSA after oil, banking and telecom industries. Jeddah continues to be one of the largest retail markets in Saudi

Arabia. The size of population, high proportion of young people and influx of tourists made Jeddah retail market one of the fastest growing markets for consumer products.

Since last few years Jeddah retail sector revolutionized because of several new developments of regional and community malls. These malls get huge market acceptance by Jeddah residents and inbound and domestic tourists.

During H1-2014 Jeddah retail market remained stable and marginal increase in rental rates has been noticed across all types of retail centers.

Supply & DemandAfter the opening of “Flamingo Mall” during 2013 at “Prince Majid Road”, Century21 did not witness any other major opening in retail sector. The mall is enjoying a healthy occupancy rate because of desirable location and presence of strong anchor tenant (Carrefour).

Strip retail centers are preforming well in the city and couple of new strip retail centers are expected to be opened during 2014. Dallah Center & La Prestige are two major upcoming attractions in community centers.

There has been a very visible shift of tenants from strip retail shops to modern shopping malls, creating demand for more regional and community malls.

Demand from international and domestic brands as well as from retailers continued to strengthen during H1-2014 which is the main demand generator for quality retail space in prime shopping malls and strip retail centers.

Retail Market TrendsCurrent Retail Space (sqm)

Vacancy Rate Future Supply (2014-2017) (sqm)Average per sqm Asking Rents in

CBD (Outside Malls)

Total 890,000 8% - 14% 200,000 SR 1100 – SR 1800

Market Trends

Market PerformanceAverage retail rentals remained stable during first half of 2014. Rental escalation of moderate 4% to 7% has been noticed in the regional malls in north and central sides of Jeddah because of higher demand. Average rental rate for retail space in modern shopping malls varied between SR 1,600 to SR 2,900 per square meter. Fast food chains remained highest paying tenants in shopping malls.

Strip retail centers/shops around CBD performed well during H1-2014 and healthy demand has been witnessed from retailers in strip retail segment. The strip retail rentals remained stable during first half of the year.

Year Strip Retail Showroom Community Mall Regional Mall Super Regional Mall2012 1100 1800 2250 24502103 1170 1910 2420 26202014F 1220 1960 2490 2700

Average Rental Rates

0

700

1400

2100

2800

2012 2103 2014F

Strip Retail Showrooms Community Mall Regional Mall Super Regional Mall

20 CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

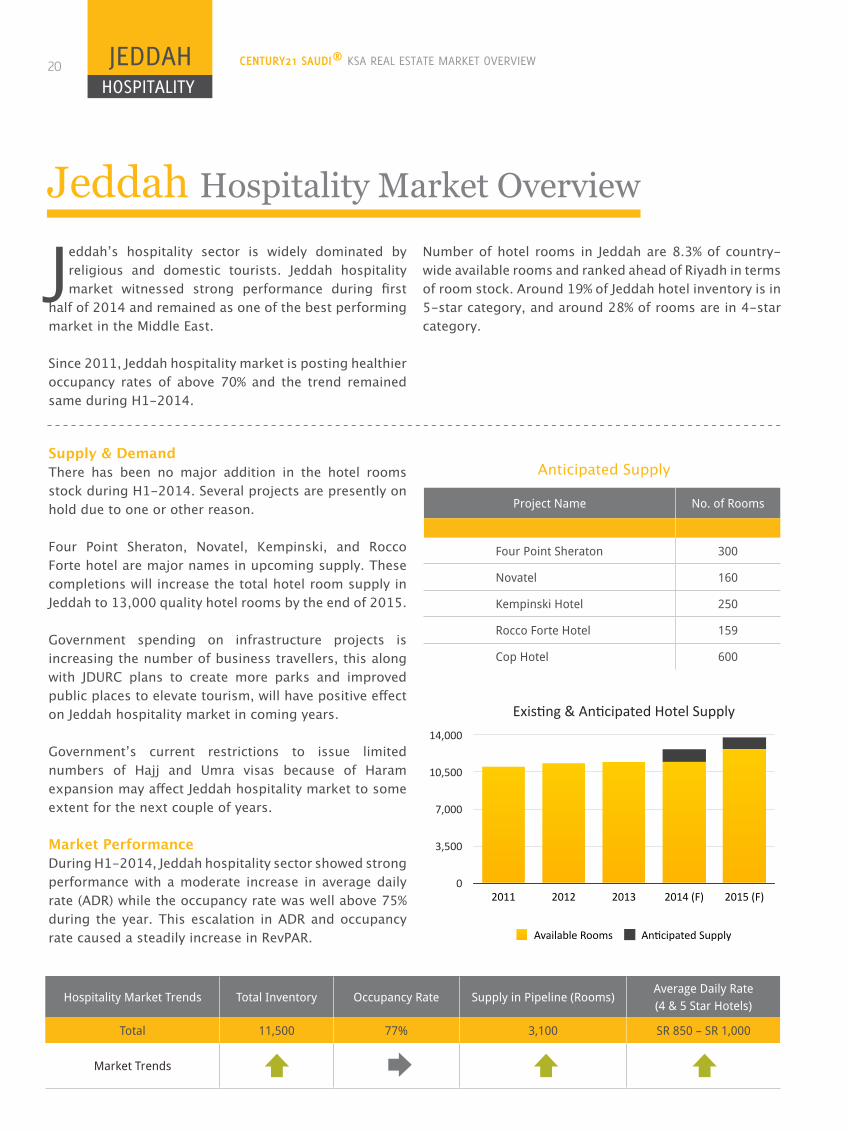

HOSPITALITY

JEDDAH

Supply & DemandThere has been no major addition in the hotel rooms stock during H1-2014. Several projects are presently on hold due to one or other reason.

Four Point Sheraton, Novatel, Kempinski, and Rocco Forte hotel are major names in upcoming supply. These completions will increase the total hotel room supply in Jeddah to 13,000 quality hotel rooms by the end of 2015.

Government spending on infrastructure projects is increasing the number of business travellers, this along with JDURC plans to create more parks and improved public places to elevate tourism, will have positive effect on Jeddah hospitality market in coming years.

Government’s current restrictions to issue limited numbers of Hajj and Umra visas because of Haram expansion may affect Jeddah hospitality market to some extent for the next couple of years.

Market PerformanceDuring H1-2014, Jeddah hospitality sector showed strong performance with a moderate increase in average daily rate (ADR) while the occupancy rate was well above 75% during the year. This escalation in ADR and occupancy rate caused a steadily increase in RevPAR.

Jeddah Hospitality Market Overview

Jeddah’s hospitality sector is widely dominated by religious and domestic tourists. Jeddah hospitality market witnessed strong performance during first

half of 2014 and remained as one of the best performing market in the Middle East.

Since 2011, Jeddah hospitality market is posting healthier occupancy rates of above 70% and the trend remained same during H1-2014.

Number of hotel rooms in Jeddah are 8.3% of country-wide available rooms and ranked ahead of Riyadh in terms of room stock. Around 19% of Jeddah hotel inventory is in 5-star category, and around 28% of rooms are in 4-star category.

Project Name No. of Rooms

Four Point Sheraton 300

Novatel 160

Kempinski Hotel 250

Rocco Forte Hotel 159

Cop Hotel 600

Years Available Rooms An%cipated Supply

2011 11,000

2012 11300 0

2013 11450 0

2014 (F) 11450 1200

2015 (F) 12650 1100

Exis%ng & An%cipated Hotel Supply

0

3,500

7,000

10,500

14,000

2011 2012 2013 2014 (F) 2015 (F)

Available Rooms An%cipated Supply

Hospitality Market Trends Total Inventory Occupancy Rate Supply in Pipeline (Rooms)Average Daily Rate (4 & 5 Star Hotels)

Total 11,500 77% 3,100 SR 850 – SR 1,000

Market Trends

Anticipated Supply

21CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

LANDSJEDDAH

Jeddah Residential Land Trading

Jeddah Commercial Land Trading

When compared with H1-2013, first half of 2014 was a slower period for residential lands trading. In H1-2014, total 17,423 transactions worth SR 28.2 billion have been done, with a decline of 18% as compare to H1-2013.

During H1-2014, residential land prices witnessed a modest increase in different districts of Jeddah. The price escalation was highest in North and central part of Jeddah where the prices increased by 2% to 5%, while south have the minimum price increase.

Commercial lands trading follow the decreasing trend during first half of 2014 as the number of commercial land transactions during first half of 2014 were 5% less than the number of transactions happened during H1-2013. During H1-2014, total 3,817 transactions worth SR 22.1 billion have been done. Highest numbers of transactions happened during the first quarter of the year.

During H1-2014 commercial land prices witnessed a modest increase in different districts of Jeddah. The price escalation was highest in North and central part of Jeddah where the prices increased by 3% to 6%, while south have the minimum price increase.

Jeddah Residen+al Lands Trading (H1-‐2014)

Num

ber o

f Tra

nsac

/ons

0

825

1,650

2,475

3,300

Tota

l Val

ue (S

R M

illio

n)

0

2,500

5,000

7,500

10,000Ja

nuar

y

Febr

uary

Mar

ch

April

May

June

Number of Transac/ons Total Value (SR Millions)

Jeddah Commercial Lands Trading (H1 -‐ 2014)Nu

mbe

r of T

rans

ac/o

n

0

175

350

525

700

Tota

l Val

ue (S

R M

Illio

n)

0

1,500

3,000

4,500

6,000

Janu

ary

Febr

uary

Mar

ch

April

May

June

Number of Transac/ons Total Value (SR Million)

Jeddah Residen+al Lands Trading (H1-‐2014)

Num

ber o

f Tra

nsac

/ons

0

825

1,650

2,475

3,300

Tota

l Val

ue (S

R M

illio

n)

0

2,500

5,000

7,500

10,000

Janu

ary

Febr

uary

Mar

ch

April

May

June

Number of Transac/ons Total Value (SR Millions)

Jeddah Commercial Lands Trading (H1 -‐ 2014)

Num

ber o

f Tra

nsac

/on

0

175

350

525

700

Tota

l Val

ue (S

R M

Illio

n)

0

1,500

3,000

4,500

6,000

Janu

ary

Febr

uary

Mar

ch

April

May

June

Number of Transac/ons Total Value (SR Million)

22 CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

PRICESJEDDAH

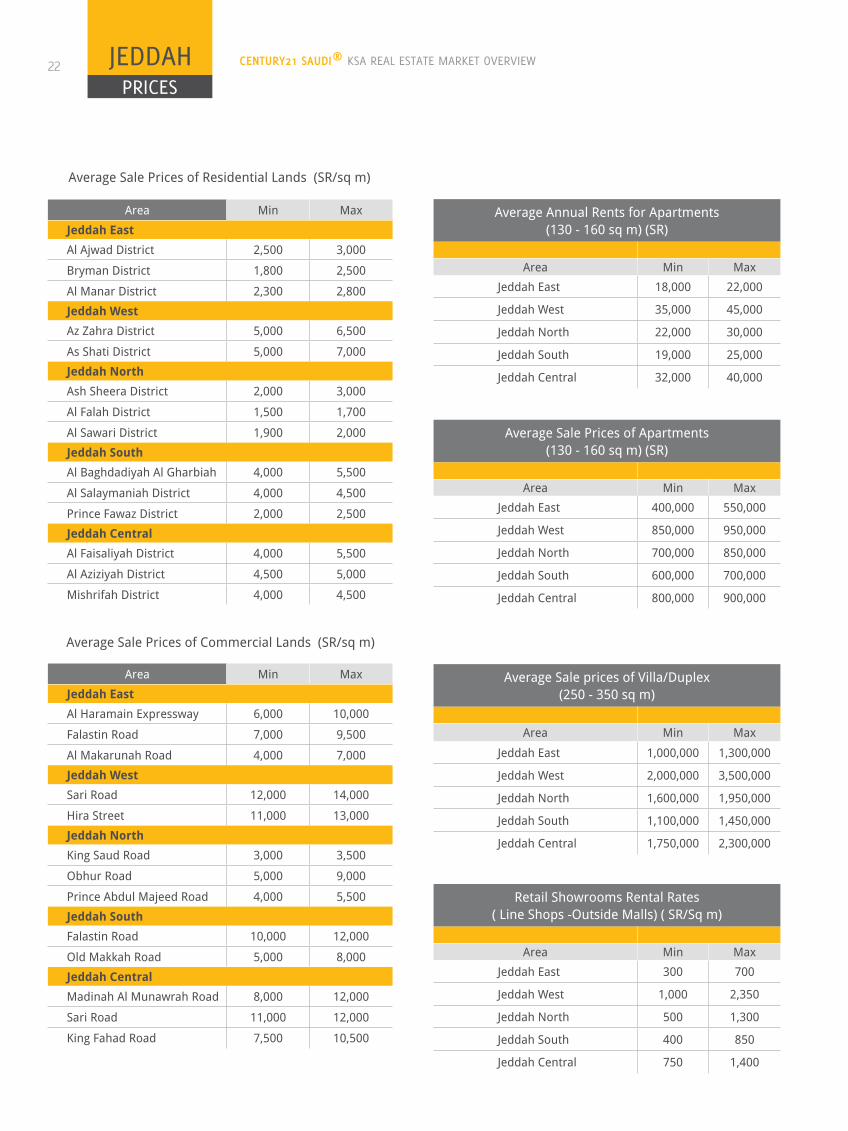

Average Annual Rents for Apartments(130 - 160 sq m) (SR)

Area Min MaxJeddah East 18,000 22,000

Jeddah West 35,000 45,000

Jeddah North 22,000 30,000

Jeddah South 19,000 25,000

Jeddah Central 32,000 40,000

Average Sale Prices of Apartments(130 - 160 sq m) (SR)

Area Min MaxJeddah East 400,000 550,000

Jeddah West 850,000 950,000

Jeddah North 700,000 850,000

Jeddah South 600,000 700,000

Jeddah Central 800,000 900,000

Average Sale prices of Villa/Duplex(250 - 350 sq m)

Area Min Max

Jeddah East 1,000,000 1,300,000

Jeddah West 2,000,000 3,500,000

Jeddah North 1,600,000 1,950,000

Jeddah South 1,100,000 1,450,000

Jeddah Central 1,750,000 2,300,000

Retail Showrooms Rental Rates( Line Shops -Outside Malls) ( SR/Sq m)

Area Min MaxJeddah East 300 700

Jeddah West 1,000 2,350

Jeddah North 500 1,300

Jeddah South 400 850

Jeddah Central 750 1,400

Area Min Max

Jeddah EastAl Ajwad District 2,500 3,000

Bryman District 1,800 2,500

Al Manar District 2,300 2,800

Jeddah WestAz Zahra District 5,000 6,500

As Shati District 5,000 7,000

Jeddah NorthAsh Sheera District 2,000 3,000

Al Falah District 1,500 1,700

Al Sawari District 1,900 2,000

Jeddah SouthAl Baghdadiyah Al Gharbiah 4,000 5,500

Al Salaymaniah District 4,000 4,500

Prince Fawaz District 2,000 2,500

Jeddah CentralAl Faisaliyah District 4,000 5,500

Al Aziziyah District 4,500 5,000

Mishrifah District 4,000 4,500

Area Min Max

Jeddah EastAl Haramain Expressway 6,000 10,000

Falastin Road 7,000 9,500

Al Makarunah Road 4,000 7,000

Jeddah WestSari Road 12,000 14,000

Hira Street 11,000 13,000

Jeddah NorthKing Saud Road 3,000 3,500

Obhur Road 5,000 9,000

Prince Abdul Majeed Road 4,000 5,500

Jeddah SouthFalastin Road 10,000 12,000

Old Makkah Road 5,000 8,000

Jeddah CentralMadinah Al Munawrah Road 8,000 12,000

Sari Road 11,000 12,000

King Fahad Road 7,500 10,500

Average Sale Prices of Residential Lands (SR/sq m)

Average Sale Prices of Commercial Lands (SR/sq m)

Dammam &Al KhobarReal Estate Market Overview

24

DAMMAMAL KHOBAR CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

RESIDENTIAL

Supply & DemandDammam/Al Khobar residential market is undersupplied due to widening gap between supply and demand as market is unable to deliver required units.

The real estate market of Dammam has focused on the residential sector, while Khobar has been more slanting towards commercial sector in last few years. However, number of new residential developments have perceived in Al Khobar as well. “Khobar Lakes” is one of the major projects in the region by EMAAR, which will deliver 2,100 house hold units during next couple of years. Despite of these recent investments in Al Khobar residential sector, Dammam seems to remain favored destination for residential investments because residential land prices in Al Khobar are higher than those in Dammam.

An apparent trend in residential sector is development of vertical high rise buildings, which indicate the decreasing stock of residential lands in central areas of Dammam and Al Khobar. Albeit, villas and duplexes are still preferred types of accommodations for Saudi families.

Most of the upcoming supply is targeting upper middle class while major proportion of demand comes from mid-income level of the population.

82,000

Dammam and Al Khobar are twin cities and considered as the third largest metropolis in Saudi Arabia. Being a hub of oil production and hosting the world largest oil company, Dammam/Al-Khobar residential market is prominent.

Twin cities have seen a dramatic increase in its population since last decade. This vigorous growth in population and reduction of household size are primary drivers of demand for residential units in these cities.

Dammam/Al Khobar Residential Market Overview

Project Name No of Units Completion

Murjana 400 2014

Masaken Homes 250 2014

Dammam Hills 700 2015

Abraj al-Salam 850 2015

Khobar Lakes 2,100 2017

AverageVilla’s Rental

SRAnticipated Supply

25

DAMMAMAL KHOBARCENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

RESIDENTIAL

Market Performance Residential market of Dammam and Al Khobar is under-supplied. This gap between supply and demand is main reason behind brisk increase in sale prices and rental rates of residential properties.

Sale prices and annual rents of residential properties vary among different areas of Dammam and Al-Khobar. Prices are comparatively higher in Al Khobar because of higher prices of residential land.

Median sale price of small size villas (230-260 sq m) ranges between SR 950,000 to SR 1,400,000, while average annual rental ranges between SR 60,000 to SR 105,000 per annum.

Median sale price of medium size apartment (100-130 sq m) ranges between SR 400,000 to SR 750,000, while average annual rental ranges between SR 25,000 to SR 45,000 per annum.

Al Hamra district in Dammam and Al Hada, Al Hizam Aldhahbi and Al Hizam Alakhdar districts in Al Khobar are hosting mostly upper middle and high end residents, where a medium size villa sale price ranges between SR 1.5 million to SR 3.2 million.

Residential Market Trends

Supply in Pipeline (Units)

Average 3 Bed Apartment Sale Price (SR)

Average Villa/Duplex Sale Price (SR)

Average 3 Bed Apartment Rentals

(SR)

Average Villa/Duplex Rentals

(SR)

Total 46,500 450,000 to 600,000 1.2m to 2.0m 28,000 to 41,500 78,000 to 125,000

Market Trends

Average Sale prices of Villa/Duplex (250 -‐ 350 sq m)

2013Area Min Max

Dammam North 1,250,000 1,600,000

Dammam West 950,000 1,250,000

Dammam South 1,000,000 1,300,000

Al Khobar East 1,650,000 2,100,000

Al Khobar South 1,000,000 1,300,000

Average Sale prices of Villa/Duplex (250 -‐ 350 sq m)

0

550,000

1,100,000

1,650,000

2,200,000

Dammam North Dammam West Dammam South Al Khobar East Al Khobar South

Min Max

26

DAMMAMAL KHOBAR CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

OFFICE

Office space in twin cities is showing better performance as compared to the other markets of KSA like Riyadh and Jeddah. Office stock is continuously increasing and expected to grow with a ratio of 5% to 7% during 2014-2015.

Demand for office space has primarily been driven by the expansion of the oil and gas sector, and government sector. Tenants mostly like to acquire medium to large size office spaces. Office spaces in Al Khobar are more advanced as compared to Dammam.

Supply & DemandOffice stock in twin cities is increasing with moderate ratio since last couple of years. The existing supply is enough to match with demand requirement of the cities leaving a trivial gap between demand and supply. Whereas majority of available office spaces are of grade B & C.

Supply is likely to increase further in coming years and most of the upcoming supply is distributed across the cities and located beside various major highways linking the twin cities.

Existing supply is mostly occupied by government entities and private companies directly or indirectly related to oil sector.

Market Performance In Dammam/Al Khobar vacancy rate is considerably lower than Riyadh and Jeddah. The general occupancy rate of Dammam/Al Khobar office market varies between 80% to 85% while some prime locations are enjoying better occupancy rate of 90% to 95%. The high level of future stock which is due to come in coming years is expected to pressurize the market specially B-class office market.

Median annual rents of B-Class offices ranges between SR 550 to SR 750 per square meter, A-Class offices ranges between SR 850 to SR 1,000 per square meter while annual rent on prime location ranges between SR 1,000 to SR 1,200 per square meter.

Office Market Trends Vacancy Rate To Date Completed Stock (sqm)

Average Asking Rent(A Grade Offices in CBD)

Average Asking Rent(B Grade Offices in CBD)

Total 8% 22,000 1,000 750

Market Trends

Dammam/Al Khobar Office Market Overview

Annual Office Rents of Grade A, B, and C

0

300

600

900

1200

Grade A Grade B+ Grade B GradeC

Annual Rent (Per sq m)

27

DAMMAMAL KHOBARCENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

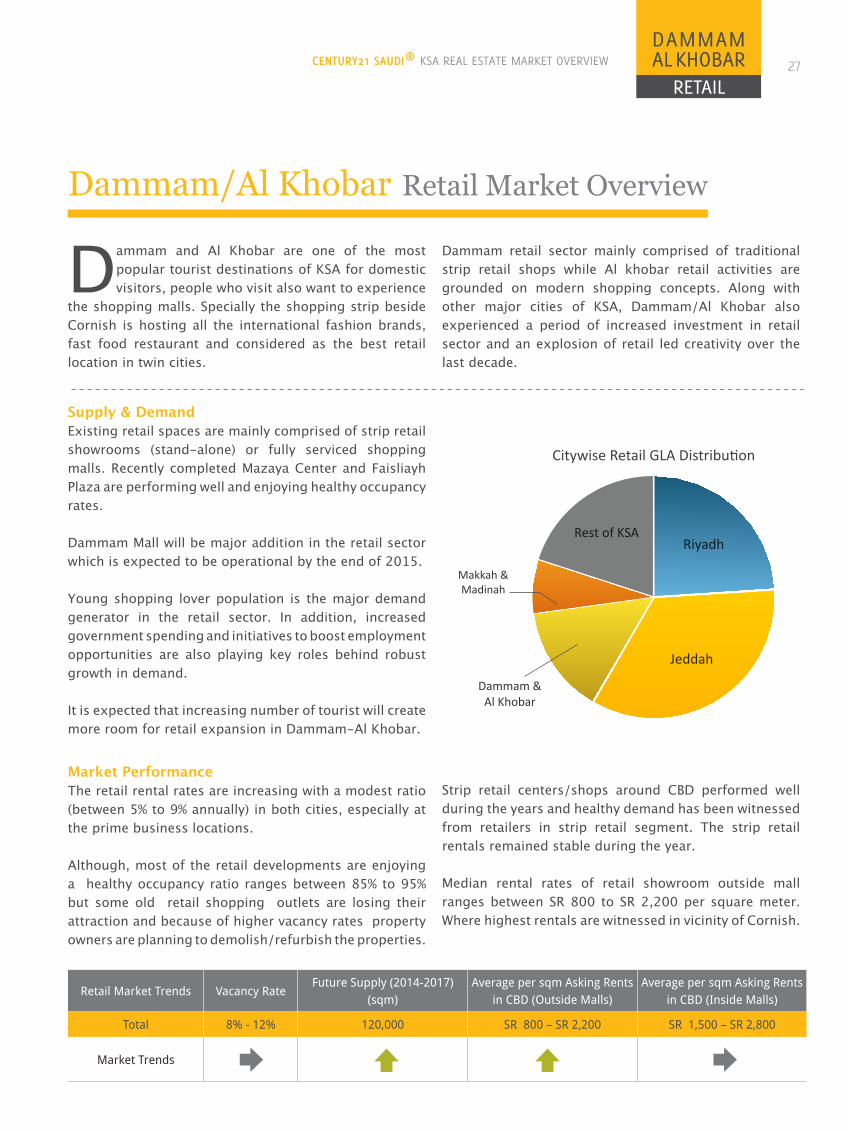

RETAIL

Supply & DemandExisting retail spaces are mainly comprised of strip retail showrooms (stand-alone) or fully serviced shopping malls. Recently completed Mazaya Center and Faisliayh Plaza are performing well and enjoying healthy occupancy rates.

Dammam Mall will be major addition in the retail sector which is expected to be operational by the end of 2015.

Young shopping lover population is the major demand generator in the retail sector. In addition, increased government spending and initiatives to boost employment opportunities are also playing key roles behind robust growth in demand.

It is expected that increasing number of tourist will create more room for retail expansion in Dammam-Al Khobar.

City Retail GLA

Riyadh 30%

Jeddah 43%

Dammam & Al Khobar 18%

Makkah & Madinah 9%

type -‐ 2

City Retail GLA

Riyadh 30%

Jeddah 43%

Dammam & Al Khobar 18%

Makkah & Madinah 9%

Rest of KSA 25%

Citywise Retail GLA Distribu3on

Rest of KSA

Makkah & Madinah

Dammam & Al Khobar

Jeddah

Riyadh

Market PerformanceThe retail rental rates are increasing with a modest ratio (between 5% to 9% annually) in both cities, especially at the prime business locations.

Although, most of the retail developments are enjoying a healthy occupancy ratio ranges between 85% to 95% but some old retail shopping outlets are losing their attraction and because of higher vacancy rates property owners are planning to demolish/refurbish the properties.

Strip retail centers/shops around CBD performed well during the years and healthy demand has been witnessed from retailers in strip retail segment. The strip retail rentals remained stable during the year.

Median rental rates of retail showroom outside mall ranges between SR 800 to SR 2,200 per square meter. Where highest rentals are witnessed in vicinity of Cornish.

Retail Market Trends Vacancy RateFuture Supply (2014-2017)

(sqm)Average per sqm Asking Rents

in CBD (Outside Malls)Average per sqm Asking Rents

in CBD (Inside Malls)

Total 8% - 12% 120,000 SR 800 – SR 2,200 SR 1,500 – SR 2,800

Market Trends

Dammam/Al Khobar Retail Market Overview

Dammam and Al Khobar are one of the most popular tourist destinations of KSA for domestic visitors, people who visit also want to experience

the shopping malls. Specially the shopping strip beside Cornish is hosting all the international fashion brands, fast food restaurant and considered as the best retail location in twin cities.

Dammam retail sector mainly comprised of traditional strip retail shops while Al khobar retail activities are grounded on modern shopping concepts. Along with other major cities of KSA, Dammam/Al Khobar also experienced a period of increased investment in retail sector and an explosion of retail led creativity over the last decade.

28

DAMMAMAL KHOBAR CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

HOSPITALITY

Dammam & Al Khobar are major tourist destination of Saudi Arabia. Arrival of tourist is continuously increasing year by year which are the main demand generators for twin cities hospitality sector.

Riyadh mainly caters corporate tourist, Makkah and Madinah contributes towards the religious demand while Jeddah, Dammam & Al Khobar markets are driven by both corporate visitors and leisure tourists which include families who visit the cities during weekends for the wonderful and well-kept beaches. Inbound tourists mostly belong to neighboring countries.

Dammam/Al Khobar Hospitality Market Overview

Supply & DemandThe Supply is expected to grow steadily with the addition of new four and five star hotels. Also an influx of budget hotels is noted in the Dammam/Al-Khobar Market.

4-star and 5-star hotel stock is rapidly increasing in twin cities and a healthy number of hotel rooms of 4-star and above will be delivered in the coming three years.

Delivery of these rooms in coming years may create a market dilution in the short to medium term. However, as the economy is growing, inbound and domestic tourism in the province is expected to sustain the market.

“Marriott Hotel” in Dammam, “Hilton Hotel & Residence” in Al Khobar are major upcoming attractions.

The demand of 4 & 5 star hotels is mainly driven by the various delegates and visitors to Saudi Aramco.

Name of Hotel No. of Rooms

Opening Year

Hilton Hotel (Jubail) 430 2014

Doubletree by Hilton (Al Khobar) 304 2014

Hilton Hotel & Residence (Al Khobar) 400 2014

Centro (Al Khobar) 250 2014

Marriott Executive Apartments (Dammam)

50 2015

Marriott Hotel (Dammam) 250 2015

Dammam Rayhaan 250 2015

Anticipated Supply

29

DAMMAMAL KHOBARCENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

HOSPITALITY

Hospitality Market Trends Occupancy RateSupply in Pipeline

(Rooms)Average Daily Rate (4 & 5 Star Hotels)

Average Daily Rate (3 Star & Budget Hotels)

Total 70% 2,500 SR 800 to SR 975 SR 400 to SR 600

Market Trends

Al Khobar Hotel Occupancy Rates & ADR

2008 2009 2010 2011 2012 2013 2014 (F)

Occupancy Rate 61% 62% 45% 49% 57% 59% 60%

ADR (SR) 859 874 724 698 806 825 830

74 62 59 64 57 56

229 233 193 186 215 220

3.75 3.75 3.75 3.75 3.75 3.75

858.75 873.75 723.75 697.5 806.25 825

Al Khobar Hotel Occupancy Rates & ADR

0%

18%

35%

53%

70%

-‐00

225

450

675

900

2008 2009 2010 2011 2012 2013 2014 (F)

Occupancy Rate ADR (SR)

Market Performance After a sharp decline in occupancy rate and average daily rate during global economic crises followed by arab spring, Dammam/Al Khobar hospitality market has revived with modest ratio during last couple of years.

Increment in occupancy rate coupled with augmented average daily rates put positive effect on RevPAR which increased with moderate ratio during first half of 2014.

825ADRDuring H1-2014

30

DAMMAMAL KHOBAR CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

LANDS

Dammam/Al Khobar Residential Land Trading

Dammam/Al Khobar Commercial Land Trading

Total 9,159 residential land transactions worth SR 14.46 billion have been carried out during H1-2014. The number of land transactions in Dammam

was more than double than the number of transactions in Al Khobar. Overall, 29% decline in land trading has been noticed during H1-2014 when compared with H1-2013.

The residential land prices escalated with a healthy ratio during first half of the year. A moderate increase of 4% to 6% has been recorded in the residential land prices of Dammam/Al Khobar.

Total 2,575 commercial land transactions worth SR 12.07 billion have been carried out during H1-2014. The number of land transactions in

Dammam was around 38% higher than the number of transactions in Al Khobar. Overall, 19% decline in commercial land trading has been noticed during H1-2014 when compared with H1-2013.

The commercial land prices escalated with a ratio of 3% to 6% during first half of the year. Al Khobar lands witnessed more robost increase as compare to Dammam.

Dammam Al Khobar Commercial Lands Trading (H1-‐2014)

Num

ber o

f Tra

nsac

/ons

0

123

245

368

490

Tota

l Val

ue (S

R M

illio

n)

0

850

1,700

2,550

3,400

Janu

ary

Febr

uary

Mar

ch

April

May

June

Number of Transac/ons Total Value (SR Million)

Dammam/Al Khobar Residen@al Lands Trding (H1-‐2014)

Num

ber o

f Tra

nsac

/ons

0

450

900

1,350

1,800

Tota

l Val

ue (S

R M

illio

n)

0

725

1,450

2,175

2,900Ja

nuar

y

Febr

uary

Mar

ch

April

May

June

Number of Transac/ons Total Value (SR Million)

Dammam Al Khobar Commercial Lands Trading (H1-‐2014)

Num

ber o

f Tra

nsac

/ons

0

123

245

368

490

Tota

l Val

ue (S

R M

illio

n)

0

850

1,700

2,550

3,400

Janu

ary

Febr

uary

Mar

ch

April

May

June

Number of Transac/ons Total Value (SR Million)

Dammam/Al Khobar Residen@al Lands Trding (H1-‐2014)

Num

ber o

f Tra

nsac

/ons

0

450

900

1,350

1,800

Tota

l Val

ue (S

R M

illio

n)

0

725

1,450

2,175

2,900

Janu

ary

Febr

uary

Mar

ch

April

May

June

Number of Transac/ons Total Value (SR Million)

31CENTURY21 SAUDI® KSA REAL ESTATE MARKET OVERVIEW

PRICES

DAMMAMAL KHOBAR

Average Annual Rents for Apartments(130 - 160 sq m) (SR)

Area Min MaxDammam North 28,000 40,000

Dammam Central 25,000 32,000

Dammam South 26,000 33,000

Al Khobar North 38,000 45,000

Al Khobar South 22,000 30,000

Average Sale Prices of Apartments(130 - 160 sq m) (SR)

Area Min MaxDammam North 500,000 650,000

Dammam West 420,000 500,000

Dammam South 470,000 600,000

Al Khobar North 650,000 850,000

Al Khobar South 500,000 600,000

Average Sale prices of Villa/Duplex(250 - 350 sq m)

Area Min MaxDammam North 1,250,000 1,600,000

Dammam West 950,000 1,250,000

Dammam South 1,000,000 1,300,000

Al Khobar East 1,650,000 2,100,000

Al Khobar South 1,000,000 1,300,000

Retail Showrooms Rental Rates( Line Shops -Outside Malls) ( SR/Sq m)

Area Min MaxDammam South 400 700

Dammam East 500 750

Al Khobar West 550 850

Al Khobar East 800 1,800

Al Khobar South 450 650

Area Min Max

DammamAl Faiha District 1,900 2,200

Al Anud District 2,000 2,500

Al Badiyah District 1,800 2,300

Uhud District 1,700 2,000

An Nuzha District 2,000 2,450

Al KhobarQurtaba District 2,300 2,700

Al Rawabi District 2,400 3,000

Thuqba District 3,000 3,800

Al Khozama District 1,800 2,300

Al Amwaj District 700 1,100

Area Min Max

DammamKhaleej Road 6,000 8,000Prince Nayf Bin Abdul Aziz Road 3,000 4,000

Al KhobarAl Riyadh Street 5,000 6,000

20th Street 5,000 6,500

Prince Sultan Street 6,000 7,500

Average Sale Prices of Residential Lands (SR/sq m)

Average Sale Prices of Commercial Lands (SR/sq m)

About Cenury21®

Century21® is one of the most recognized name in Real Estate Market with approximately 7,600 independently owned and operated franchised brokerage offices in 71 countries and territories worldwide and represented by more than 112,000 real estate experts.

Cenury21 Saudi is official representative of Century21® in the Kingdom of Saudi Arabia since 2005; specialized in Real Estate Evaluation (Appraisal), Marketing and Leasing Services, Real Estate Research & Advisory and Property Management.

Century21 Saudi’s Research & Advisory Department (CRA) has been established in 2009 and has a proven track record of providing a variety of research-based services to the business arena all over KSA market.

Services Equipped with highly qualified analysts & researchers, Century21 Saudi is capable of responding all major segments of Real Estate market (Residential, Commercial, Industrial and Hospitality) with professional decorum.

Our offered services are:

• Feasibility Studies.• Highest and Best Use Studies.• Strategy & Planning Advisory.• Pricing Strategies.• Market Research Analysis Studies.• Development Solutions.• Site Assessment.• Market Forecast.• Real Estate Market Review.

ContactsFor Assistance in development & marketing decisions please contact:

Eng. Alaa Al-Thagafi Deputy General [email protected]: 0558 199 194

Asif IqbalHead of Research and [email protected]: 0555 177 076

Saadat AliSenior Market [email protected]: 053 833 7600

Al Waleed Hamd BinzoumanGeneral [email protected]: 0555 194 919

DisclaimerIn order to prepare this report, Century21 Saudi collected the data from outside sources as well as by survey of Century21 Saudi research team. Century21 Saudi is confident about the reliability of published data. However, we do not guarantee the completeness and accuracy of the data.

This report is prepared for information only. The assessments and values articulated in this report are subject to change without any notice. Therefore, no investment decision should be made based on the information presented in this report. Century21 Saudi will not be responsible for any loss that may be sustained as a result of the information enclosed in this report.

About Us

Riyadh - Main OfficeP.O. Box : 300374 Riyadh : 11372 - Tel: +966 (11) 4000 360 - Fax: +966 (11) 485 7338 - www.century21saudi.com