merrill lynch conference - barloworld · pdf filemerrill lynch conference ... •13 x cat...

TRANSCRIPT

Merrill Lynch Conference

Sun City 16 – 18 March 2015

2

Group revenue and operating profit split – September 2014

50%

50%

Revenue

Equipment and Handling

Automotive and Logistics

58%

42%

Operating profit

Equipment and Handling

Automotive and Logistics

Divisional overview

Equipment southern Africa

4

Southern Africa revenue – Sept 2014

47%

43%

6%4%

Revenue by line of business

New equipment Product support

Used equipment Rental

28%

30%21%

9%

12%

New equipment sales by industry

Mining Construction

EMPR Power

Contract mining

5

Southern Africa sales history

37%

30%

28%

34%

46%

36%

33%

41% 43%

0

5

10

15

20

2006 2007 2008 2009 2010 2011 2012 2013 2014

Rbn

Equipment sales Product support

6

Argent- Shanduka(2016)

Orapa Cut 3 (2018)

Moatize exp- Mota Engil (2016)

7

8

Zambia | FQM Kalumbila

● Seventh Cat MD 6640 drill still to be

shipped

● 2 Rope shovels and 2 drills currently

undergoing final commissioning.

● Support team is in place that includes

9 local employees which are based on

site.

● Aftermarket opportunity

First Cat electric rope shovel to be delivered in Zambia

9

Namibia | Swakop Uranium – Husab Project

● All equipment commissioned and

handed over on time by December

2014 (2 units scheduled for Sep’15)

● Delivered fleet:

• 3 X Cat 7495 rope shovels

• 3 X 6060 hydraulic shovels

• 6 X blasthole drills

• 2 X electric motivators

● Customer support agreement in place

• Operator training onsite

• Technical training onsite

• Technical support team onsite

• Substantial parts investment on site

Components of the Cat 6060 in transit

Assembled shovel and Barloworld Equipment team on site

Total contract value

R1.3bn

10

● Firm deal for 8 Cat 793D trucks and 1 Cat

6090 hydraulic mining shovel -

approximate value US$ 42m

● Vale forecast is to have a total of 90 large

mining trucks by 2018 – doubling of the

existing fleet

● On site support structure of 90 people

● Investment of $11m in a new facility

● The initial fleet is in first Planned

Component Replacement cycle over the

next 18 months - significant aftermarket

opportunity

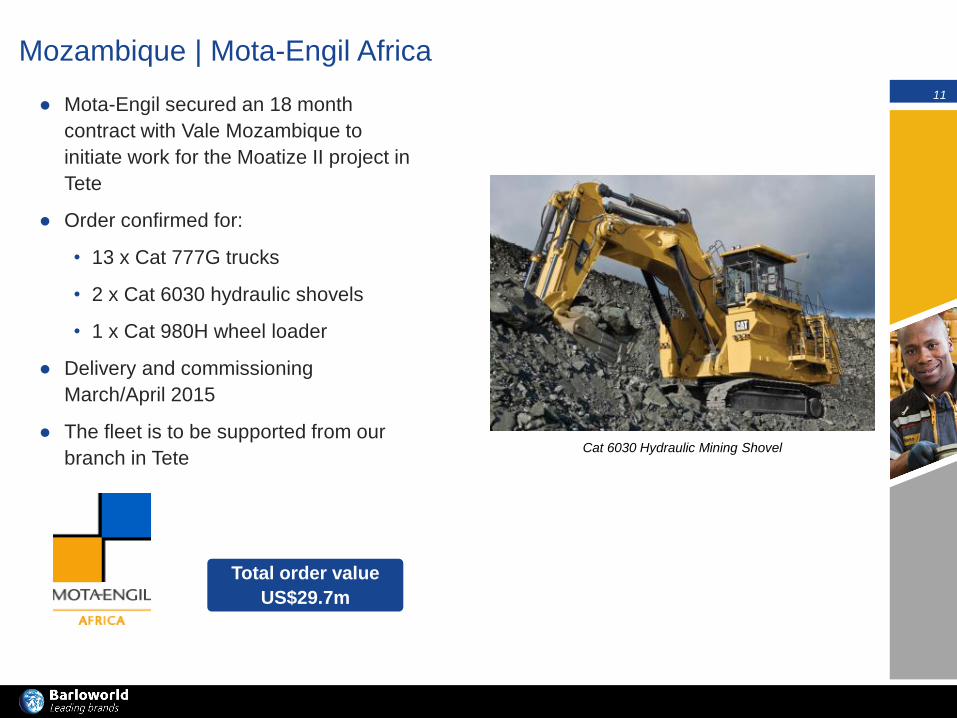

Mozambique | Vale Moatize Project

Cat 6090 Hydraulic Mining Shovel loading a Cat 797F truck

Barloworld Equipment Mozambique’s new branch in Tete

11

Mozambique | Mota-Engil Africa

● Mota-Engil secured an 18 month

contract with Vale Mozambique to

initiate work for the Moatize II project in

Tete

● Order confirmed for:

• 13 x Cat 777G trucks

• 2 x Cat 6030 hydraulic shovels

• 1 x Cat 980H wheel loader

● Delivery and commissioning

March/April 2015

● The fleet is to be supported from our

branch in Tete Cat 6030 Hydraulic Mining Shovel

Total order value

US$29.7m

Divisional overview

Equipment Russia

13

Russia revenue profile – Sept 2014

48%

46%

1% 5%

Revenue by line of business

New equipment Product support

Used equipment Rental

60%

17%

10%

3%

10%

New equipment sales by industry

Mining Construction Power

Oil and gas Other

14

Russia sales history

25%

24%

25%

29%36%

28%

27%33%

46%

0

100

200

300

400

500

600

2006 2007 2008 2009 2010 2011 2012 2013 2014

US$m

Equipment sales Product support

15

● Economic slowdown and difficult geopolitical situation continues

● Low oil price and weak rouble has adverse impact

● Limited direct impact of sanctions but increases complexity and compliance cost

● Aftermarket revenues continue to provide stable source of profitability

● Reduced headcount in selected areas

● Cost control initiatives and focused balance sheet management

● Positive cash flow generation driven by reduced working capital requirements

● EMPR continues to perform well on aftermarket side

Operational update – Equipment Russia

16

Surface mining – green field projects

Opportunity 2017 2018 2019

Units 90 106 84

US Dollars $172 m $293 m $280 m

17

Already Sold: to BDSK – 6 forestry units + 2 dozers to be delivered in March 2015

to PBR – 5 construction units

Estimated opportunity: 65 units in 2015 and 77 units in 2016

Power of Siberia opportunity

• Originally 3 major contractors

expected to oversee the project:

• Stroytransgaz

• Stroygazmontazh

• Stroygazconsulting

• Gazprom decided to break down the

project into smaller components and

consider bigger group of contractors:

• 17 companies in total

• Includes some of VT’s existing

customers such as PBR, Sibmost

and Irkutskneftegazstroy

• Further opportunity with sub-

contractors to these companies

• VT’s approach:

• Coverage on site and in Moscow

• Mobilise stock in Lensk

• Concentrate on popular models

• Offer new and used equipment

Divisional overview

Equipment Iberia

19

Iberia revenue profile – Sept 2014

39%

41%

17%

3%

Revenue by line of business

New equipment Product support

Used equipment Rental

8%

37%

7%

48%

New equipment sales by industry

Mining Construction

Other Power

20

Iberia sales history

32%

30%30%

34%

40% 37%33% 35%

41%

0

100

200

300

400

500

600

700

800

900

2006 2007 2008 2009 2010 2011 2012 2013 2014

EURm

Equipment sales Product support

21

0

5000

10000

15000

20000

198

1

198

2

198

3

198

4

198

5

198

6

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

Machine industry – Spain

Units

22

● Macro economic conditions continue to improve, construction sector lagging

● Restructuring in Spain concluded in 2014 is yielding projected savings

● Restructuring costs of €0.7m incurred in Q1 to restructure Portuguese operations

● Market leadership position maintained

● Aftermarket revenues continue to support profitability

● Currently on track to achieve breakeven result to half year

Operational update – Equipment Iberia

Divisional overview

Power systems

24

Long term prospects in Power remain positive

Major projects

Southern Africa Russia Iberia

• Large EP (gas &

liquid)projects in SA, Angola

and Moz

• Moz LNG in medium term

• Angola Sonaref refinery

•Power of Siberia pipeline

•Gas genset rentals

• Industrial Projects

•Data centres (Telefonica, PT)

• International oil & gas EPC

projects

•Marine engine and propulsion

system opportunities

• Industrial opportunities

● Sentiment affected by oil price decline, Russia recession and slowdown in marine activity

Divisional overview

Handling

26

● Agriculture SA continues to deliver good sales

● Strong order book in Mozambique despite post-election slowdown

● Negotiations with BayWa AG to form an agriculture JV in Zambia

● Russian operation impacted by recession & Rouble decline

● SEM product range expanded

● Hyster operation improves SA market share, however margins under pressure

Operational update – Handling

Divisional overview

Automotive and Logistics

28

Strategic positioning

Barloworld Automotive

(Automotive Business model)

Au

tom

otive

an

d L

og

istics D

ivis

ion

Barloworld Logistics

Communication, HR, IT, Legal, Finance, Sustainable Development, Strategy,

Empowerment and Transformation, Risk Management, Business Development and

Sales, Governance, Ethics and Compliance

Customers

Car

Rental

Fleet

Services

Digital

Disposal

Solutions

Motor

Retail

Southern

Africa

Freight

Mangmt

and

Services

Supply

Chain

Mangmt

Supply

Chain

Mangmt

Transport

Solutions

• Inter-business unit synergies and cost efficiencies

• Apply Collective Wisdom

• Leveraging Automotive infrastructure to achieve

critical mass for growth

• Retain strategic focus on each business unit

29

Sense of scale

General Information

Employees 11 203

Countries 16

Automotive Principals

Avis Budget Group, Audi, BMW, Ford, General Motors, Jaguar

Land Rover, Mazda, Mercedes-Benz, Toyota, Volkswagen.

Car Rental locations >190

Wholly owned Motor Retail dealerships (SnA) 43

Key Indicators FY Sep ’13 FY Sep ’14

Rental Days 6.06m 6.66m

New & Used retail units sold 82 929 84 512

Total vehicles under management 277 164 307 456

New vehicles sold per dealership per month 75 73

DTS km’s travelled FY’14 97.9m

SAT tons shipped FY’14 5 917t

30

● Strong result in a demanding trading environment

● Revenue: R31.1bn (FY’13: R28.8bn) – up 8.1%

● Record operating profit R1 644m (FY’13: R1 322m) – up 24%

● Operating margin for the year 5.3% (FY’13: 4.6%)

● All business segments performed well

Operational review

0 100 200 300 400 500 600

Logistics

Fleet Services

Motor Retail

Car Rental

Operating Profit (Rm)

2014 2013

9.3%7.8%

2.8%2.4%

18.1%16.7%

2.8%2.3%

Margin

+33%

+29%

+16%

+22%

31

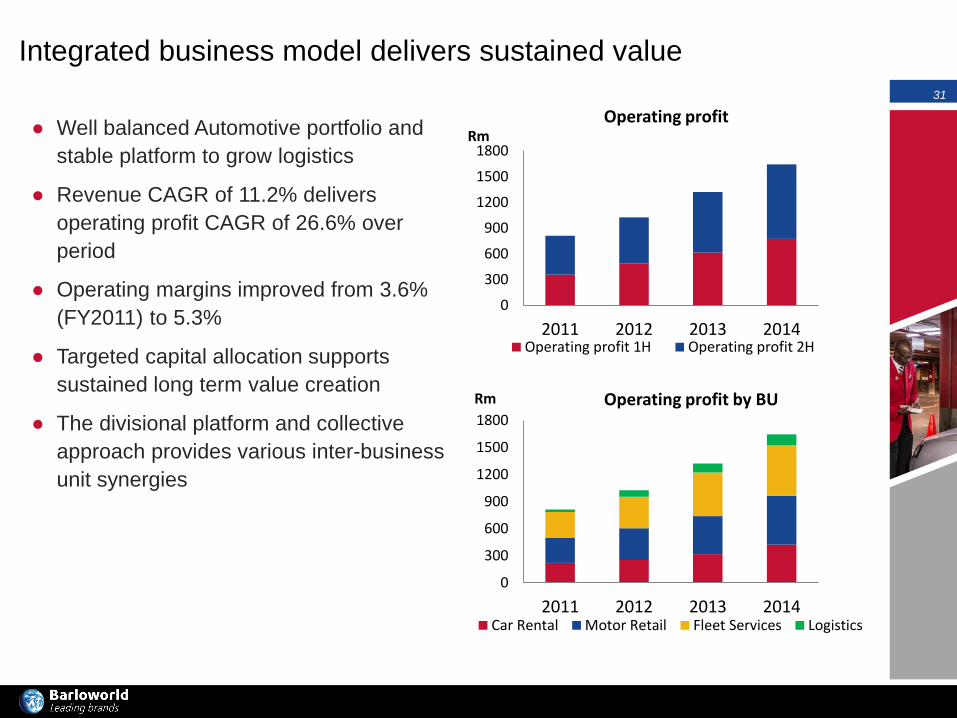

● Well balanced Automotive portfolio and

stable platform to grow logistics

● Revenue CAGR of 11.2% delivers

operating profit CAGR of 26.6% over

period

● Operating margins improved from 3.6%

(FY2011) to 5.3%

● Targeted capital allocation supports

sustained long term value creation

● The divisional platform and collective

approach provides various inter-business

unit synergies

Integrated business model delivers sustained value

0

300

600

900

1200

1500

1800

2011 2012 2013 2014

RmOperating profit

Operating profit 1H Operating profit 2H

0

300

600

900

1200

1500

1800

2011 2012 2013 2014

Rm Operating profit by BU

Car Rental Motor Retail Fleet Services Logistics

32

Division overview

● Leadership continuity

● Enhance return on equity

● Continued cash focus

● Targeted capital allocation

● Growing market share

● Optimising vehicle fleets (utilisation)

● Managing working capital levels

● Improving asset turn

● Expense management

● Controlling interest costs

● Implementing Logistics growth strategy

● Targeted growth opportunities across all

units

● Exceeding customer expectations

● Integrate Budget Brand into existing car

rental operations

33

Car Rental

● Improved rental days despite competitive market

● Improved revenue per day

● Continued focus on operating costs

● Fleet utilisation remains well controlled

● Continued solid used vehicle profit contribution

● Sustained customer satisfaction above 90%

● Budget Brand

-4

-2

0

2

4

6

8

10

12

Rental Days Revenue per day Fleet Utilisation Fleet Size

% G

row

th

Leading IndicatorsJan '15 YTD Sep '14 YTD

34

Motor Retail

0

100

200

300

400

500

600

700

800

900

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Total South African Vehicle Market

Passenger LCV M&HCV

Source: Lightstone Auto & 2015–2021 forecast by Dr. Neal Bruto

35

Motor Retail

● Fewer, Bigger, Better” Strategy continues

● 73 new vehicles sold per dealership per month

(Sep’13: 75)

● Appropriate dealership footprint

● Focused brand strategy aligned to overall

Automotive business model

● Improved operating margin through cost

containment and margin expansion

● Continue strong OEM alignment

-10

-

10

20

30

New Units Service Hours Parts Revenue F & I Net Profit

% G

row

th

Leading IndicatorsJan '15 YTD Sep '14 YTD

36

Fleet Services

● Pleasing performance in low interest rate

environment

● Finance fleet growth slows post large contract

roll-outs

● Strong growth in fleets under maintenance

● Continued strong used vehicle profits

● Awaiting adjudication on further tenders

● African growth: Ghana, Tanzania, Zambia in focus

-10

0

10

20

30

Maintenance Fleet Finance Fleet Total Fleet

% G

row

th

Leading IndicatorsJan '15 YTD Sep '14 YTD

37

Logistics

● Well positioned for organic and acquisitive growth

● Barloworld Transport provides good operating

profit contribution

● Extra heavy transport acquisition Sept 2014

enhances capability in the abnormal load transport

business

● Barloworld Cranes business unit launched

● Ellerines finalised with no further impact

● International operations continue to face difficult

trading conditions – actions being taken

● Exited loss making Far East airfreight business in

FY2014

Merrill Lynch Conference