mercedes-benz prestige motor vehicle insurance · mercedes-benz insurance is a registered name of...

TRANSCRIPT

Mercedes-Benz Prestige Motor Vehicle InsuranceProduct Disclosure Statement and Policy Document

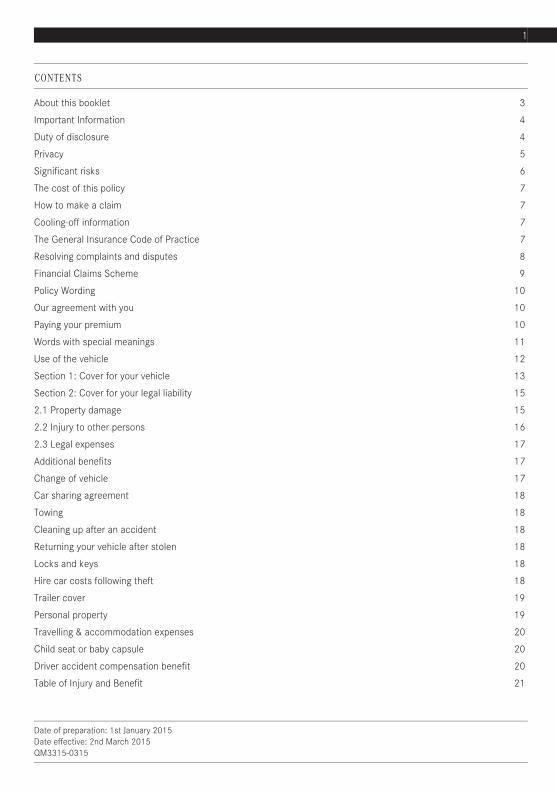

CONTENTS

3About this booklet

4Important Information

4Duty of disclosure

5Privacy

6Significant risks

7The cost of this policy

7How to make a claim

7Cooling-off information

7The General Insurance Code of Practice

8Resolving complaints and disputes

9Financial Claims Scheme

10Policy Wording

10Our agreement with you

10Paying your premium

11Words with special meanings

12Use of the vehicle

13Section 1: Cover for your vehicle

15Section 2: Cover for your legal liability

152.1 Property damage

162.2 Injury to other persons

172.3 Legal expenses

17Additional benefits

17Change of vehicle

18Car sharing agreement

18Towing

18Cleaning up after an accident

18Returning your vehicle after stolen

18Locks and keys

18Hire car costs following theft

19Trailer cover

19Personal property

20Travelling & accommodation expenses

20Child seat or baby capsule

20Driver accident compensation benefit

21Table of Injury and Benefit

Date of preparation: 1st January 2015Date effective: 2nd March 2015QM3315-0315

1

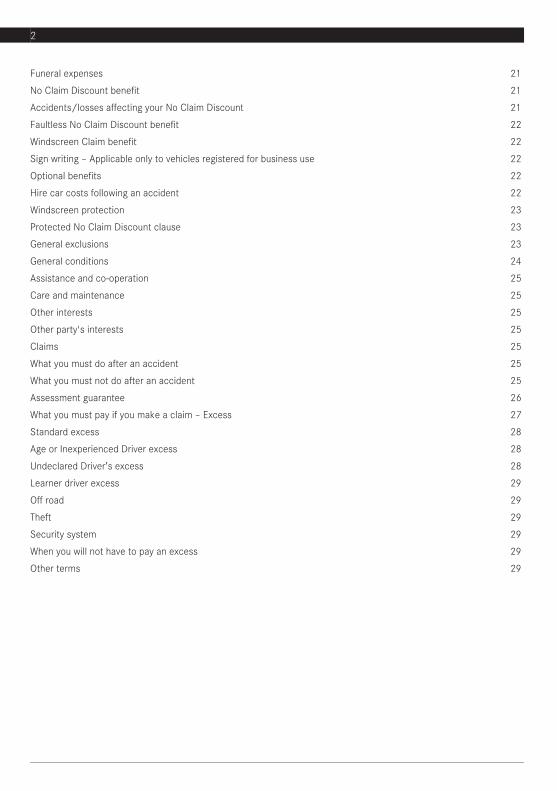

21Funeral expenses

21No Claim Discount benefit

21Accidents/losses affecting your No Claim Discount

22Faultless No Claim Discount benefit

22Windscreen Claim benefit

22Sign writing – Applicable only to vehicles registered for business use

22Optional benefits

22Hire car costs following an accident

23Windscreen protection

23Protected No Claim Discount clause

23General exclusions

24General conditions

25Assistance and co-operation

25Care and maintenance

25Other interests

25Other party's interests

25Claims

25What you must do after an accident

25What you must not do after an accident

26Assessment guarantee

27What you must pay if you make a claim – Excess

28Standard excess

28Age or Inexperienced Driver excess

28Undeclared Driver’s excess

29Learner driver excess

29Off road

29Theft

29Security system

29When you will not have to pay an excess

29Other terms

2

About this booklet

This booklet is a Product Disclosure Statement (PDS) and is also the Policy Wording. Other documents may comprisethe PDS and we will tell you if this is the case in the relevant document.

This booklet has two (2) parts: Important Information to help you understand the insurance, and the Policy Wording,which sets out terms and condition of the cover provided. It is up to you to choose the cover you need. Any advice inthis booklet is general in nature only and has not considered your objectives, financial situation or needs. You shouldcarefully consider the information provided having regard to your personal circumstances to decide if it is right for you.

Updating our PDS

We may update the information contained in this PDS when necessary. A paper copy of any updated information isavailable to you at no cost by calling us. We will issue you with a new PDS or a supplementary PDS, where the update isto rectify a misleading or deceptive statement or omission, which is materially adverse from the point of view of areasonable person deciding whether to obtain or renew this insurance.

For more information

Please take the time to read through this booklet and if you have any questions or need more information, please contact:

Mercedes-Benz Insurance on 1300 730 200.

About QBE Australia

QBE Insurance (Australia) Limited ABN 78 003 191 035 AFSL 239545 is a member of the QBE Insurance Group LimitedABN 28 008 485 014 (ASX: QBE). QBE Insurance Group is Australia’s largest international general insurance andreinsurance group, and one of the top 25 insurers and reinsurers worldwide. The company has been operating in Australiasince 1886 and continues to provide insurance solutions that are focused on the needs of policyholders.

QBE is a respected name in Australian insurance, backed by sizeable assets, and well known as a strong and financiallysecure organisation.

About Mercedes-Benz Financial Services

Welcome and thank you for choosing Mercedes-Benz Financial Services Australia Pty Limited ABN 73 074 134 51, AFSLicence No. 247271 (Merceded-Benz Insurance). Mercedes-Benz Insurance utilises years of local expertise combinedwith global experience to offer a range of multi-featured products and services to our customers. As members of theworldwide Daimler Group, Mercedes-Benz Insurance is committed to continuous improvement of our products andservices, and aspires to insurance industry best practice procedures in all aspects of its business. This policy is underwrittenby QBE Insurance (Australia) Limited, one of Australia’s largest general insurers.

3

Important Information

The information provided in this section includes high level information about this Policy including your duty of disclosure,privacy, how to make a claim, our dispute resolution process and other relevant information. This section may also setout other information such as options in cover you can choose from, factors that affect the cost and any cooling offrights.

The Policy Wording section sets out the detailed terms, conditions and exclusions relating to the insurance.

If we issue you with a Policy, you will be given a Policy Schedule. The Policy Schedule sets out the specific terms applicableto your cover and should be read together with the Policy Wording.

The Policy Wording and Policy Schedule form your legal contract with us so please keep them in a safe place for futurereference. You should check the Policy Schedule, or renewal schedule if you are issued one, when you receive it to ensureit accurately states what you have insured.

Duty of disclosure

New business

What you must tell us

When answering our questions, you must be honest and you have a duty under the law to tell us anything known to you,and which a reasonable person in the circumstances would include in answer to the questions. We will use the answersin deciding whether to insure you and anyone else to be insured under this insurance and on what terms.

Who needs to tell us

It is important that you understand you are answering our questions in this way for yourself and anyone else who is aninsured under this insurance.

If you do not tell us

If you do not answer our questions in this way, we may reduce or refuse to pay a claim, or cancel your insurance. If youanswer our questions fraudulently, we may refuse to pay a claim and treat the insurance as never having worked.

Renewals, variations, extensions and reinstatements

Once your insurance is entered into and is no longer new business then your duty to us changes. You are required beforeyou renew, vary, extend or reinstate your insurance, to tell us everything you know and that a reasonable person in thecircumstances could be expected to know, is a matter that is relevant to our decision whether to insure you, and anyoneelse to be insured under this insurance, and if so, on what terms.

You do not have to tell us about any matter:

that diminishes the risk to be undertaken by us;that is of common knowledge;that we know or should know or, in the ordinary course of our business, we ought to know;as to which compliance with your duty is waived by us.

Non-disclosure

If you fail to comply with your duty of disclosure, we may be entitled to reduce our liability under the insurance in respectof a claim or may cancel the insurance.

4

If your non-disclosure is fraudulent, we may also have the option of avoiding the insurance from its beginning.

You must disclose to us all previous claims

You are asked at the time you take out this insurance to give us full and correct details concerning any:

renewal or insurance policy declined, cancelled or refused, or where any excess was imposed;claim refused by an insurer;claim made;criminal conviction or finding of guilt for an offence,

in relation to you and your family because any of these may affect the premium and extent of insurance.

For example, we may be entitled to:

charge you an additional premium;impose (back-dated) restrictions including declining your insurance back to when this information should have beenprovided;decline to insure your building, contents or valuables;refuse a claim.

When renewing your Policy with us you must also advise us of any changes to your:

claims;insurance; orcriminal history.

We will notify you in writing of the effect a change may have on your renewal.

Privacy

All companies in the QBE Group are committed to safeguarding your privacy and the confidentiality of your personalinformation. QBE collects only that personal information from or about you for the purpose of assessing your applicationfor insurance and administering your insurance policy, including any claim made by you. QBE will only use and discloseyour personal information for a purpose you would reasonably expect. We will request your consent for any other purpose.

Without this personal information we may not be able to issue insurance cover, administer your insurance or processyour claim. Our aim is to always have accurate and up-to-date information. When you receive a Policy Schedule, Certificateof Insurance, Renewal or other document from us, you should contact us if the information is not correct.

QBE uses the services of a related company located in the Philippines to provide Call Centre sales and claims handling,accounting and administration services to QBE in Australia.

QBE or our authorised agent may collect or disclose your personal information from or to:

any person authorised by you;a mail house, records management company or technology services provider (for printing and/or delivery of mailand email, including secure storage and management of our records). These companies may be located or therecords stored using 'Cloud' technology overseas, including in India, Ireland, USA or the Netherlands;a financier whose name appears on your Policy Schedule (for the purpose of confirming the currency of your Policyor when you have a claim and the insured property is a total loss, to confirm if the financier has a current interest);an organisation that provides you with banking facilities (for the purpose of arranging direct debit or other paymenttransactions or confirming payments made by you to us);

5

a financial services provider or our agent who is arranging your insurance (for the purpose of confirming your personaland insurance details);another person named as a co-insured on your Policy (for the purpose of confirming if full disclosure has been madeto us);another insurer (to obtain confirmation of your no claim bonus or to assess insurance risks or to assist with aninvestigation);our reinsurer that may be located overseas (for the purpose of seeking recovery from them);a dispute resolution organisation such as the Financial Ombudsman Service (for the purpose of resolving disputesbetween QBE and you or between QBE and a third party);a company to conduct surveys on our behalf for the purpose of improved customer services; andan insurance reference bureau (to record any claims you may make upon us).

In addition to the above, in the event of a claim, QBE or our authorised agent may disclose your personal information:

to a repairer or supplier (for the purpose of repairing or replacing your insured items);to an investigator, assessor (for the purpose of investigating or assessing your claim);to a lawyer or recovery agent (for the purpose of defending an action by a third party against you or recovering ourcosts including your excess or seeking a legal opinion regarding the acceptance of a claim);to a witness to a claim (for the purpose of obtaining a witness statement);to another party to a claim (for the purpose of obtaining a statement from them or seeking recovery from them orto defend an action by a third party).

Personal information (about you) may also be obtained from the above people or organisations.

In addition we will:

give you the opportunity to find out what personal information we hold about you and when necessary, correct anyerrors in this information. Generally we will do this without restriction or charge; andprovide our dispute resolution procedures to you, should you wish to complain about how we handle your personalinformation.

To obtain further information about our Privacy Policy, to request access to or correct your personal information, or tomake a complaint please email: [email protected].

Significant risks

Your sum insured may not be adequate.

If you have insured your vehicle for an agreed value, we will at our option replace your vehicle with an equivalent vehicleor pay the agreed value shown on your Policy Schedule. You should review the agreed value of your vehicle at the timeof each renewal of your Policy.

Cover on your vehicle includes standard equipment for the particular make and model of your vehicle fitted by the originalmanufacturer. Some limits apply to other equipment and accessories unless they are specified on your Policy Schedule.You should refer to the section headed ‘What you are insured against’ under ‘Section 1: Cover for your Vehicle’ for detailsof these limits. It is important that you ensure all equipment and accessories valued above the policy limits are separatelylisted on the Policy Schedule with their respective agreed values otherwise the maximum amount the Insurers will payfor any part or item will be its current market value.

6

The cost of this policy

The total premium is the amount we charge you for this Policy. It includes the amount we have calculated for the riskand the taxes and government charges applicable. The premium will be shown on the Policy Schedule.

When calculating the premium we take a number of factors into account. These factors and the degree to which theyaffect the premium will depend on the information you give us, and the level and type of cover you choose. The mainfactors that impact your premium include:

where the vehicle is located;the sum insured;your previous insurance and claims history;tour driving history; andages of the drivers of the vehicle.

How to make a claim

Full details of what you must do for us to consider your claim are provided in the ‘Claims’ section at the end of thisbooklet. To make a claim under this Policy please contact:

Mercedez-Benz Insurance on 1300 730 200.

We will only accept responsibility for repairs or payments to third parties under a claim where you have told us aboutthem beforehand and we have accepted your claim. Full details of what you must do for us to consider your claim areprovided at the end of this booklet.

Cooling-off information

If you want to return your insurance after your decision to buy it, you may cancel it and receive a full refund. To do thisyou may notify

Mercedez-Benz Insurance on 1300 730 200.

within 30 days from the date the Policy commenced.

This cooling off right does not apply if you have made or are entitled to make a claim. Even after the cooling off periodends, you still have cancellation rights however we may deduct certain amounts from any refund for administration costsor any non-refundable taxes.

The General Insurance Code of Practice

QBE Insurance (Australia) Limited is a signatory to the General Insurance Code of Practice.

The Code aims to:

promote more informed relations between insurers and their customers;improve consumer confidence in the general insurance industry;provide better mechanisms for the resolution of complaints and disputes between insurers and their customers;andcommit insurers and the professionals they rely upon to higher standards of customer service.

7

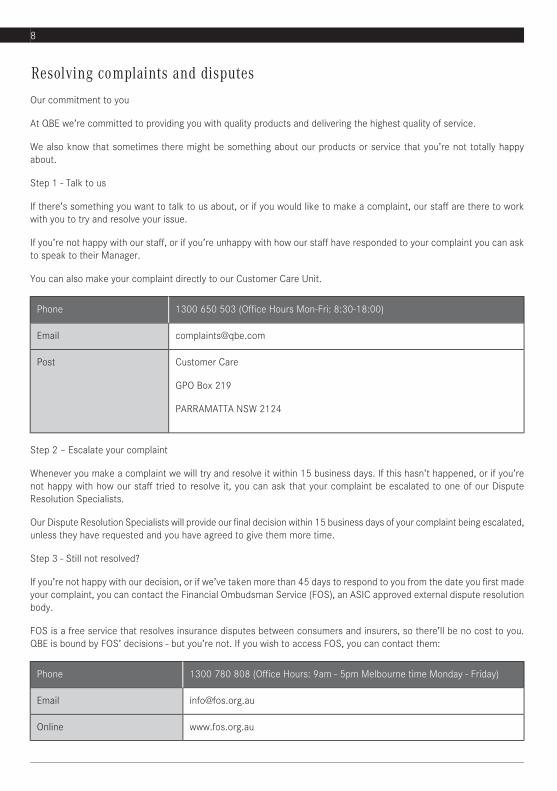

Resolving complaints and disputes

Our commitment to you

At QBE we’re committed to providing you with quality products and delivering the highest quality of service.

We also know that sometimes there might be something about our products or service that you’re not totally happyabout.

Step 1 - Talk to us

If there’s something you want to talk to us about, or if you would like to make a complaint, our staff are there to workwith you to try and resolve your issue.

If you’re not happy with our staff, or if you’re unhappy with how our staff have responded to your complaint you can askto speak to their Manager.

You can also make your complaint directly to our Customer Care Unit.

1300 650 503 (Office Hours Mon-Fri: 8:30-18:00)Phone

Customer CarePost

GPO Box 219

PARRAMATTA NSW 2124

Step 2 – Escalate your complaint

Whenever you make a complaint we will try and resolve it within 15 business days. If this hasn’t happened, or if you’renot happy with how our staff tried to resolve it, you can ask that your complaint be escalated to one of our DisputeResolution Specialists.

Our Dispute Resolution Specialists will provide our final decision within 15 business days of your complaint being escalated,unless they have requested and you have agreed to give them more time.

Step 3 - Still not resolved?

If you’re not happy with our decision, or if we’ve taken more than 45 days to respond to you from the date you first madeyour complaint, you can contact the Financial Ombudsman Service (FOS), an ASIC approved external dispute resolutionbody.

FOS is a free service that resolves insurance disputes between consumers and insurers, so there’ll be no cost to you.QBE is bound by FOS’ decisions - but you’re not. If you wish to access FOS, you can contact them:

1300 780 808 (Office Hours: 9am - 5pm Melbourne time Monday - Friday)Phone

www.fos.org.auOnline

8

Financial Claims Scheme

This Policy is a protected policy under the Financial Claims Scheme (FCS), which protects certain insureds and claimantsin the event of an insurer becoming insolvent. In the unlikely event of QBE becoming insolvent you may be entitled toaccess the FCS, provided you meet the eligibility criteria.

More information may be obtained from APRA - www.apra.gov.au or1300 55 88 49.

9

Policy Wording

Our agreement with you

Your Policy is an agreement between you and us, made up of:

this Policy Wording; andyour Policy Schedule, which sets out the cover you’ve chosen and any terms specific to you.

The cover under this Policy is provided during the period of insurance, once you’ve paid us your premium. There are also:

conditions and exclusions which apply to specific covers or sections;general exclusions, which apply to any claim you make;general conditions, which set out your responsibilities under this Policy;claims conditions, which set out your responsibilities when you make a claim; andother terms, which set out how this Policy operates.

Excesses

If you make a claim, you must pay the excess set out in the Policy Schedule for every claim you make which applies tothat cover or section.

How much we will pay

The most we will pay for a claim is the sum insured set out in the Policy Schedule for the cover or section you are claimingunder, less any excess.

Paying your premium

The ways you can pay your premium, and the frequency you can pay it, are described below:

in one annual payment by cash, cheque, credit card or EFTPOS, orin monthly instalments by direct debit from your credit card or from your account with your financial institution, orit can be included in your financing arrangement for your loan.

If you include the premium in your financing arrangement, the premium will be included in the total cost payable by youplus interest for the full length of the finance term - irrespective of when this insurance cover commences or the termof the cover being shorter than the financing term.

Paying your annual premium

You must pay your premium by the due date, if it has not been included in your financing arrangements. If we do notreceive your premium by the due date or your payment is dishonoured then this Policy will not operate and there will beno cover under this Policy.

Instalment payments

If you are paying your premium by instalments, we will specify on your Policy Schedule when we will deduct the firstinstalment. Thereafter, instalment payments will be debited on the date or frequency you have nominated. If you arepaying your premium in instalments by direct debit from your credit card or financial institution account, you must tellus if these details change no later than seven (7) days before your next instalment is due. We will not pay a claim underthis Policy if, at the time the claim occurred, any premium instalment has remained unpaid for one (1) month or more.

10

If any instalment of premium has remained unpaid for one (1) month, we may cancel this Policy. However, we will sendyou a notice confirming the action we intend to take and when any cancellation will become effective.

At renewal

If you have been paying your premium by instalment, we will continue to deduct instalments for your Renewal Policy onthe same day of the month at the new premium level unless you tell us otherwise.

If any instalment of premium has remained unpaid for one (1) month, we will cancel this Policy. We will send you areminder setting out our intention to take two (2) instalments on the next payment date. If payment is not received afterthis reminder, we will send you a notice telling you of the date the Policy will cease unless payment is received. We senda notice to confirm the Policy has been cancelled.

Adjustment of premium on renewal

If a claim occurs in the previous period of insurance and you do not notify us until after the premium for the currentperiod of insurance was calculated, then you must pay any additional premium that would have been calculated had youtold us about the claim on the day that the claim occurred. This condition does not affect any other rights that we have,including the rights that we have under 'Your duty of disclosure'.

If your payment details change

If the direct debit arrangements you use to pay by instalment changes, such as you are issued a new credit card orchange your bank arrangements, you must tell us. You should do this at least seven (7) days in advance of your nextpayment date.

Words with special meanings

Some key words and terms used in this Policy have a special meaning. If words and terms are only used in one (1) sectionof the Policy, we will describe their special meaning in that section.

Wherever the following words or terms are used in the Policy, they mean what is set out below:

MeaningWord or term

The person or entity with a security interest in your vehicle.Financier

The period shown on the Policy Schedule.Period of insurance

The schedule of insurance or any endorsement schedule we give you.Policy Schedule

Means a security interest as defined in Section 12 of the Personal Property Securities Act2009 (Cth).

Security Interest

QBE Insurance (Australia) Limited, ABN 78 003 191 035 AFSL 239545.We, our or us

Any member of your family who lives permanently with you, including your partner.Your family

The vehicle described in the schedule.Your vehicle

The person(s), companies or firms named on the Policy Schedule as the ‘Insured’.You or your

11

Use of the vehicle

We cover your vehicle only when you are using it for the type of use shown on the Policy Schedule. Refer also to thesection titled ‘When you are not covered’.

1. Private Use means

Your vehicle must be registered for ‘private use’ only in your name and used for the following purposes:

social, domestic and pleasure purposesdemonstration for salein connection with servicing, repairing and subsequent testingfor tuition, as long as it is not for paymenttowing a caravan, trailer or vehicle, as long as it is not for paymentdriving to or from workin connection with your occupation or business as, long as:

it is driven only by you, andthe business use does not exceed 20% of the vehicle’s usage.

2. Executive Use means

Your vehicle is registered for ‘business use’ but is used only for the following purposes:

social, domestic and pleasure purposesdemonstration for salein connection with servicing, repairing and subsequent testingfor tuition, as long as it is not for paymentdriving to or from worktowing a caravan, trailer or vehicle, as long as it is not for payment.

Executive use does not cover loss or damage if your vehicle is let on hire or is being used by you or someone authorisedby you to carry passenger or goods for payment, other than private pooling arrangement.

3. Business Use means

Your vehicle is registered for ‘business use’, but is used only for the following purposes:

in connection with your business or occupationsocial, domestic and pleasure purposesdemonstration for salein connection with servicing, repairing and subsequent testingfor tuition, as long as it is not for paymenttowing a caravan, trailer or vehicle, as long as it is not for payment.

Business use does not cover loss or damage if your vehicle is let on hire or is being used by you or someone authorisedby you to carry passenger or goods for payment, other than private pooling arrangement.

12

Section 1: Cover for your vehicle

What you are insured against

We cover you against loss or damage to your vehicle shown in the Policy Schedule.

Cover on your vehicle includes

(a) Standard equipment for your particular make and model of your vehicle fitted by the original manufacturer.(b) Any specified equipment or accessories shown on the Policy Schedule.(c) Other fitted accessories, and your vehicle’s tools or spare parts in or on your vehicle, up to $500 in total.(d) Theft or accidental loss or damage to your vehicle.

What you are not insured against

We do not cover your vehicle for the following:

(a) damage to its tyres caused by the application of brakes, road punctures, cuts or bursting, unless caused as aresult of an incident covered

(b) depreciation, wear, tear, rust or corrosion(c) failure or breakdown of a structural, electrical, mechanical or electronic nature(d) faulty design or workmanship of your vehicle parts. However, we do cover you for loss or damage to your vehicle

resulting from faulty design or workmanship if such loss is otherwise covered by this Policy(e) mechanical damage caused by escape of oil or coolant unless whilst your vehicle is being driven by a thief(f) loss or damage to your vehicle as a result of using a type of fuel that is not intended for the specific make and

model of your vehicle and engine.

What we pay for loss or damage

At our option we treat the loss or damage as a:

(a) partial loss, or(b) total loss.

These types of losses are defined below and we settle on the terms described:

a) Partial loss

If we decide to repair your vehicle, we will repair it to a similar condition to that which it was in before the loss or damageoccurred.

If it is necessary to repair it to a better condition than it was in before the loss or damage occurred, then we may askyou to contribute the additional amount to repair it to the better condition.

If you have insured any accessories we will either repair them or pay for the cost to replace them as new, less an amountfor depreciation, wear and tear.

Genuine parts guarantee

If your vehicle is damaged in an accident we will repair, replace any damaged part where required and incident relatedwith a genuine part for your make and model. We will only do this if the part is locally available at the time of repair.

13

Lifetime repair guarantee

Repairs are guaranteed for the life of your vehicle, even if you sell it.

If we authorise repairs to your vehicle, we will guarantee the quality of the repairs for any defect due to faulty workmanshipor faulty material for the life of your vehicle. For entitlement to any repairs under this guarantee you must first allow usto inspect the vehicle and we must agree that repairs are necessary.

Imported vehicles

If your vehicle has been imported and any part is not available in Australia, we will only pay for the cost of parts used inthe repair of your vehicle up to the manufacturer’s recommended list price in Australia. However if such list is not available,we will only pay for the cost of the parts plus the cost of freighting such parts by sea transport.

If there is a delay in the repair process due to the importation of parts, you are not covered for any loss of use of yourvehicle during that time.

b) Total loss

A vehicle will be declared a ‘total loss’, if:

the cost to repair your vehicle plus the value of any salvage (if applicable) exceeds the agreed value or market value,oryour vehicle is stolen and not recovered within a reasonable period of time as determined by us.

We will settle the claim on the basis of market value or agreed value depending on the cover shown on the Policy Schedule.

Market value

If you have insured your vehicle for market value, we will at our option:

replace your vehicle with an equivalent vehicle or pay you its market value at the time of the total loss, plusreplace all insured accessories or pay you the cost to replace them as new, less depreciation.

Market value means

The cash purchase price of a vehicle of the same age, type and condition, in your local area, but excluding costs andcharges for registration, stamp duty transfer and any dealer warranty costs.

Agreed value

If you have insured your vehicle for agreed value, we will at our option replace your vehicle with an equivalent vehicle orpay the agreed value shown on the Policy Schedule.

Agreed value means

The fixed amount for which your vehicle is insured for each period of insurance regardless of any price change for yourvehicle during that period.

The agreed value includes the value of insured accessories and equipment.

14

Replacement with a new vehicle

We will replace your vehicle with a new vehicle of the same model or series so long as it is available in Australia and:

your vehicle is a total loss, andyou purchased it new from the manufacturer or their dealer or as a demonstrator vehicle, andyour vehicle is less than 36 months old from when it was first registered, andwhere your vehicle is financed, your financier has given us written consent.

If a new replacement vehicle is not available, we will replace your vehicle with the nearest equivalent vehicle available,so long as it is available in Australia. If we cannot agree on a replacement vehicle, we will pay you the amount it wouldcost to buy a new vehicle the same as, or a near equivalent of, the vehicle which needs replacing.

If the Excess is applicable it is payable to us before we replace your vehicle.

We also pay the registration, stamp duty and dealer charges for the period registered but not exceeding 12 months onthe new vehicle but any refund of registration fees or stamp duty applicable must be refunded to us.

Financier

If a security interest is registered over your vehicle, we will:

pay the financier the sum insured, up to the amount required to discharge your loan or finance agreement; andif applicable, pay you the remaining balance of the sum insured;

Or

If no security interest is registered over your vehicle, we will either:

pay you the sum insured; orif your car is less than 36 months old, we may replace your vehicle in accordance with the terms of 'Replacementwith a new vehicle' ( Could not find copy_641501_ID_308).

Discharging a security interest

You must take the necessary steps which we require to remove any security interest in your vehicle after your loan orfinance agreement has been discharged.

Salvage

If we replace your vehicle or pay you the market value or agreed value, your vehicle and its insured equipment becomesour property.

Section 2: Cover for your legal liability

2.1 Property damage

Damage to property

We will pay the amount you, or any person you have allowed to drive, use or to be in charge of your vehicle may be heldlegally liable to pay, for accidental damage to property belonging to other people caused by or arising out of the use of:

your vehicle or goods falling from your vehiclea single trailer or caravan attached to your vehicle.

15

Property under your control

We do not cover the legal liability of you or the driver of your vehicle for damage by your vehicle to any property belongingto you or the driver of your vehicle, or any property in your or the driver’s care or custody, except to:

a residential building that you are renting or is on loan to you, oremployee’s or visitor’s vehicles and their contents while contained in a car park provided by you.

Substitute vehicle

We cover your legal liability to pay for accidental damage caused by a registered vehicle used by you as a substitutewhile your vehicle is being serviced, repaired or is not driveable. There is no cover for loss or damage to the substitutevehicle.

We give you this benefit only if:

the substitute vehicle is not already covered under another insurance policy, andthe substitute vehicle is not owned by you and you have the owner’s permission to drive it.

Your employer’s or principal’s liability

We will pay the amount that your employer, principal or partner may be held legally liable to pay, for accidental damageto property belonging to other people as a result of an incident covered by this Policy while you are using your vehicleon business, as long as it is not a use that is excluded by this Policy as described under ‘Use of the vehicle’.

Maritime liability

If your vehicle is being transported by sea between Australian ports, we will pay your contribution for your vehicle if‘general average’ is declared.

General Average is declared when goods or cargo are thrown overboard to safeguard the vessel and the remainingproperty on the vessel. Those whose property is saved share the expenses or salvage costs incurred by a ship owner inpreserving the vessel and cargo.

Passenger Liability

We will insure a passenger who is lawfully travelling in or getting in or out of your vehicle or a substitute motor vehicle.

What we pay for legal liability for damage to other people’s property

We will pay up to the maximum amount shown on the Policy Schedule, for all claims arising out of any one incident orseries of incidents arising out of the one cause or event covered under the heading ‘Property damage’, in this section.

2.2 Injury to other persons

We will pay the amount which you, or any person driving, using or in charge of your vehicle with your permission may beheld legally liable to pay by way of compensation or damages (excluding aggravated, punitive or exemplary damages) fordeath or bodily injury to persons arising out of the use of your vehicle.

We do not cover legal liability for death or bodily injury to:

you or any person driving, using or in charge of your vehicle, oran employee of yours or who is deemed by any law to be your employee arising out of their employment with you.

16

We do not pay if:

(a) your vehicle is not registered

(b) you or any person using your vehicle:

is wholly or partly covered under any compulsory statutory insurance scheme or accident compensationscheme, orwould have been entitled to be covered under any such scheme as it existed at the commencement date ofthe relevant period of insurance, even though there may have been a change in the law during that periodof insurance, orwould have been entitled to be covered under any such scheme if it were not for the application of any excessor deductible applying under the scheme, orwould have been entitled to be covered under any such scheme had cover not been refused because youdid not:

register your vehicleapply for cover under the schemecomply with a term or condition of the scheme.

(c) If your vehicle is registered in the Northern Territory of Australia.

What we pay for legal liability for injury to other persons

We will pay up to the maximum amount shown in the Policy Schedule, for all claims arising out of any one incident orseries of incidents arising out of the one cause or event covered under ‘Injury to other persons’, in this section.

However, we do not pay more than this amount in total under all policies we have issued to you in relation to loss, damageor liability arising out of any one incident.

2.3 Legal expenses

We will pay your reasonable legal costs and expenses in defending or settling claims if you have our agreement in writing.We pay this in addition to the amount payable under ‘Damage to property’ and ‘Injury to other persons’, in this section.

Additional benefits

If you make a claim under this Policy and we agree to pay your claim, we will also give you the following additional benefits:

Change of vehicle

We will cover any permanent replacement sedan, wagon or van, from the time of its purchase for 21 days under theterms of this Policy if you:

have disposed of the replaced vehicle, and

bear any additional excess applicable to the replacement vehicle in the event of a claim.

If before you have given us full details as required below, the replacement vehicle is damaged or stolen, the maximumamount payable is the purchase price of the replacement vehicle up to $150,000.

If you give us details of your replacement vehicle within 21 days of its purchase we will insure it for the remainder of theperiod of insurance, if it is acceptable to us and you pay us any additional premium we may require.

17

If your replaced vehicle was due to a total loss claim under this Policy this benefit does not apply.

Car sharing agreement

We will pay for accidental loss or damage when your vehicle is being used in a car sharing agreement, including travellingto and from work, as long as any payment by passengers does not involve commercial use for profit.

Towing

If your vehicle is not driveable following an accident or theft covered under the policy, we will pay for the reasonablecosts of:

towing your vehicle to the repairer nearest to where it was damaged, or

any other place that we first approve.

Cleaning up after an accident

We cover your legal liability to pay for the cleaning up of any debris of your vehicle following an accident.

The maximum amount we will pay is $1,000 for any one accident.

Returning your vehicle after stolen

We will pay for the reasonable costs of returning your vehicle to the place where it is normally parked if it is found afterhaving been stolen.

Should the cost of returning the vehicle plus the necessary repairs exceed the relevant agreed value or market value atthe time of the theft, we reserve the right to treat the vehicle as a total loss.

Locks and keys

If your keys are lost, destroyed or damaged, or if there are reasonable grounds to believe the keys may have been illegallyduplicated, we will pay the costs of replacing and recoding the locks and/or keys. We will pay up to $2,000 during anyone period of insurance and this benefit is not subject to loss or damage to the vehicle covered under this Policy.

Hire car costs following theft

If your vehicle is stolen and the theft is covered under this Policy, we will reimburse you for the reasonable cost of hiringa similar vehicle providing you first obtain our approval, but:

we do not pay for hiring charges incurred after your vehicle is found,

we do not pay for fuel or other running costs,

cover is limited to a total period of 14 days or 7 weekends, and

cover stops once we pay the claim.

You will need to organise and pay for the hire car. We are not responsible for ensuring that a hire car is available. Youmust also give us a copy of the rental agreement and any receipts for the hire car before we will pay you.

18

If the cost of the hire car is more than the amount shown below you will have to pay the difference.

We do not pay for:

additional hiring costs

running costs, including the cost of fuel

damage to the hire car

any insurance, insurance excess or other costs you may be liable for under the hire car rental agreement.

The maximum amount we will pay is $2,000 for any one event.

Trailer cover

We will pay for theft, or accidental loss or damage to any trailer (other than a caravan) which is owned by you while it is:

attached to your vehicle, or

detached from your vehicle but within the domestic land boundaries of your usual home as long as it was not in acommon area of home units, flats and the like.

We do not pay for any property in or on the trailer.

The maximum amount we will pay is the market value of the trailer, limited to $1,000.

Personal property

If your personal property is lost or damaged in an event covered by this Policy we will pay for the loss or damage of suchpersonal property.

However, we will not pay for more than the actual value of the property, that is, we will only pay the new replacementcost of any item which can be purchased in Australia less an allowance for age, wear, tear and depreciation.

There is no cover under this section:

if the vehicle is only broken into whilst parked,

for money, cheques or negotiables ,

for unset gemstones, gold or silver nuggets,

for any animal, bird or fish,

for trade tools, stocks or samples,

for mobile phones or two way radios, or

for GPS or personal music devices

19

In this clause, ‘personal property’ means private household or personal possessions belonging to you or any member ofyour family who normally lives with you.

The maximum amount we will pay is $500 for any one event.

Travelling & accommodation expenses

We will pay for any reasonable travelling and accommodation expenses resulting from a claim for accidental damage,fire or theft to your vehicle which we accept under this Policy, as long as at the time of accident, fire or theft your vehiclewas more than 150 kilometres from the address where it is normally parked at night.

We will not pay if you had intended to pay for overnight accommodation in any event.

The maximum amount we will pay is $1,000 for any one event.

Child seat or baby capsule

We will pay for loss or damage to a child’s seat or baby capsule that is stolen from your vehicle or damaged in an accidentor fire while in your vehicle.

Driver accident compensation benefit

We will pay the following scale of benefits to the driver of your vehicle who is injured as a result of an accident whiledriving your vehicle if:

the driver was driving your vehicle with your consent

the claim has been accepted under this Policy, and

the driver is not entitled to any benefits under any compulsory statutory insurance scheme or accident compensationscheme, or would have been so entitled if:

it were not for the application of any excess or deductible applying under the scheme, or

compensation under the scheme had not been refused, because you did not register our vehicle or apply forcover under the scheme.

Choice of repairer

We will arrange for a licenced Mercedes-Benz Autobody Repairer to repair damage to your vehicle.

You may also choose any licensed repairer to repair your vehicle. However we may invite, accept, adjust or declineestimates or arrange to move your vehicle to another repairer acceptable to both of us.

Mercedes-Benz Agility Finance Programme Customers: Should you elect to take your vehicle to a licenced Mercedes-BenzAutobody Repairer or an agreed repairer, it will be repaired by qualified technicians, using only genuine Mercedes-Benzparts in accordance with the Agility finance contract repurchase return condition clause. By insuring with Mercedes-Benzcomprehensive insurance, we will guarantee all repairs will be completed in accordance with the repurchase returncondition clause.

20

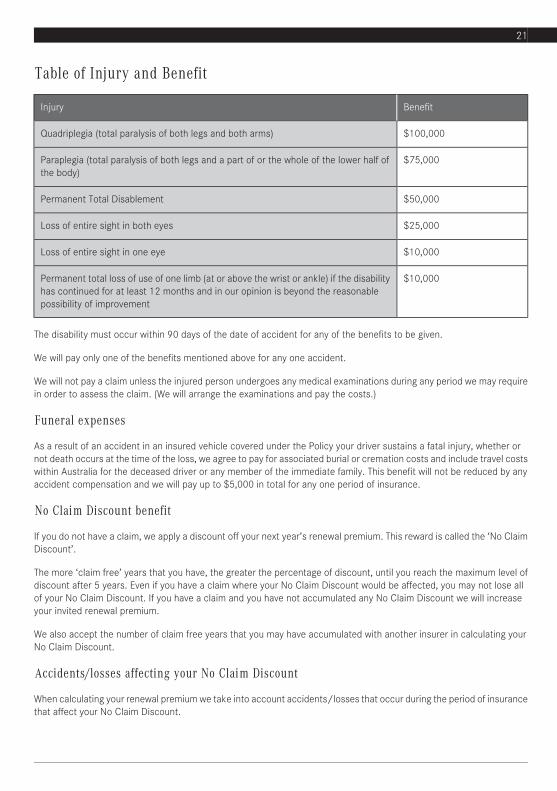

Table of Injury and Benefit

BenefitInjury

$100,000Quadriplegia (total paralysis of both legs and both arms)

$75,000Paraplegia (total paralysis of both legs and a part of or the whole of the lower half ofthe body)

$50,000Permanent Total Disablement

$25,000Loss of entire sight in both eyes

$10,000Loss of entire sight in one eye

$10,000Permanent total loss of use of one limb (at or above the wrist or ankle) if the disabilityhas continued for at least 12 months and in our opinion is beyond the reasonablepossibility of improvement

The disability must occur within 90 days of the date of accident for any of the benefits to be given.

We will pay only one of the benefits mentioned above for any one accident.

We will not pay a claim unless the injured person undergoes any medical examinations during any period we may requirein order to assess the claim. (We will arrange the examinations and pay the costs.)

Funeral expenses

As a result of an accident in an insured vehicle covered under the Policy your driver sustains a fatal injury, whether ornot death occurs at the time of the loss, we agree to pay for associated burial or cremation costs and include travel costswithin Australia for the deceased driver or any member of the immediate family. This benefit will not be reduced by anyaccident compensation and we will pay up to $5,000 in total for any one period of insurance.

No Claim Discount benefit

If you do not have a claim, we apply a discount off your next year’s renewal premium. This reward is called the ‘No ClaimDiscount’.

The more ‘claim free’ years that you have, the greater the percentage of discount, until you reach the maximum level ofdiscount after 5 years. Even if you have a claim where your No Claim Discount would be affected, you may not lose allof your No Claim Discount. If you have a claim and you have not accumulated any No Claim Discount we will increaseyour invited renewal premium.

We also accept the number of claim free years that you may have accumulated with another insurer in calculating yourNo Claim Discount.

Accidents/losses affecting your No Claim Discount

When calculating your renewal premium we take into account accidents/losses that occur during the period of insurancethat affect your No Claim Discount.

21

Faultless No Claim Discount benefit

If you have been involved in a collision (and not any other type of accident) with another vehicle we will not penalise yourNo Claim Discount entitlement when you renew your Policy if:

you can satisfy us that the collision was totally the fault of the driver of another vehicle, and

you tell us the registration number of the other vehicle and the full name, licence number and address of the otherdriver.

We give this benefit only if we are allowed legally to recover the amount of any loss including any applicable excessesfrom the responsible person.

This benefit does not apply to windscreen or window glass damage only claims.

If you live in a State or Territory where liability is apportioned in the courts, or determined by the Barometer ofResponsibility, you will qualify as ‘faultless’ if you are 20% or less to blame for any accident.

Where the driver of the other vehicle disputes who was at fault, the No Claim Discount will be affected but reinstated tothe level it was before the claim, if it can be established to our satisfaction that the other driver was totally at fault.

Windscreen Claim benefit

We will not reduce your No Claim Discount for any broken or damaged windscreen or window glass only claim.

Sign writing – Applicable only to vehicles registered for business use

We will cover you for loss or damage to sign writing or fixed advertising signs or material forming a permanent part ofyour vehicle at the time of the loss or damage.

Optional benefits

You can also choose to have cover under any or all of the following optional benefits. You must pay us any additionalpremium we ask for, and we will confirm your cover by showing the optional benefits you have chosen on your PolicySchedule.

Hire car costs following an accident

If your vehicle is damaged in an accident which is covered under this Policy, and we have agreed to pay your claim, wewill reimburse you for the costs you incur of hiring a car while your vehicle is being repaired or if deemed a total loss.

We will reimburse you an amount up to the maximum daily rate shown on your Policy Schedule:

for a maximum of 14 days, or 7 weekends (Saturday and Sunday), or

until your vehicle is repaired, or

until we pay your claim

whichever happens first.

The cover will commence on the date your vehicle is taken to the repairer.

22

You will need to organise and pay for the hire car. We are not responsible for ensuring that a hire car is available. Youmust also give us a copy of the rental agreement and any receipts for the hire car before we will pay you.

If the cost of the hire car is more than the maximum daily rate shown on your Policy Schedule, you will have to pay thedifference.

We do not pay for:

additional hiring costs

running costs, including the costs of fuel

damage to the hire car

any insurance, insurance excess or other costs you may be liable for under the hire car rental agreement.

We will not cover you under this optional benefit if:

the only damage to your vehicle is to its windscreens or window glass, or

your vehicle is stolen, because you may be able to claim under the ‘Hire car costs following theft’ additional benefit.

Windscreen protection

If the only damage in an accident is a broken or damaged windscreen or window glass the standard excess shown in thePolicy Schedule does not apply for any windscreen or window glass claim.

Protected No Claim Discount clause

If you are involved in an accident and you make a claim where your No Claim Discount would normally be affected, thenyour No Claim Discount entitlement will not be reduced at renewal of your Policy provided you:

are, at the time of the accident, on maximum No Claim Discount, and

do not have more than one claim, where this clause is applicable, in any one annual period of insurance.

General exclusions

These general exclusions apply to all sections of this Policy.

Your policy does not cover any loss or damage, if your vehicle:

(a) was not reasonably secured against further damage or theft, following an accident(b) was being driven by someone:

who does not hold a legal driving licence to drive your vehicle in Australia, orwho is under the influence of alcohol or drugs, orwhose blood alcohol reading exceeds the legal limit (unless there is a law that says otherwise), orwho following an accident, refuses to provide or allow the taking of a sample of breath, blood or urine fortesting analysis as required by the law of any State or Territory in which the accident occurred.

23

However, we do give cover if you have allowed another person to drive your vehicle, but you did not know or couldnot be reasonably expected to know that they were not so licensed or would be under the influence of alcohol ordrugs. Where permitted by law, we reserve the right to recover the amount we pay from the driver of your vehicleat the time of the loss or damage.

(c) is stolen or is involved in an accident and you incur costs because you cannot use your vehicle – except as maybe covered elsewhere in the policy

(d) has been modified in a way that materially increases its designed top speed or performance and we were not toldthis and agreed to it in writing

(e) is being used to carry more passengers or carrying or towing a heavier load than it was designed for, unless youcan prove that this did not contribute to the loss or damage

(f) or an attached caravan or trailer was being used when you knew or should have known it was un-roadworthy orunsafe, unless you can prove that this did not contribute to the loss or damage

(g) is being used in a test, trial, experiment or demonstration other than a demonstration for the purpose of sellingthe vehicle or involved in a defensive driving course

(h) is being used or tested in preparation for racing, pace making, reliability trial or a speed or hill climb(i) is let on hire, used to carry passengers for payment, other than private pooling arrangements, or to carry other

people’s goods for payment(j) is used for purposes other than those shown in the Policy Schedule(k) is not registered for use on a public road(l) runs on rails or is designed to run in water such as in a lake or sea(m) has been legally seized or repossessed(n) is outside Australia except when being transported between places in Australia(o) is being used when it is an unsafe condition, and you knew or should have known that it was unsafe to use.

Your policy does not cover any loss damage or liability arising out of:

(a) a deliberate act by you or anyone acting with your permission except when it is to avoid or reduce damage whichwould otherwise happen

(b) any intentional criminal or dishonest act by you or any person acting with your consent(c) your admission of liability or fault for damage or injury without our consent, except where such liability would have

been incurred even if you had not admitted fault or liability(d) the illegal carrying of quantities of inflammable liquids, gases or explosives.

Sanctions limitation and exclusion clause

You are not insured under any section of this Policy where a claim payment breaches any sanction, prohibition or restrictionunder United Nations resolutions or the trade or economic sanctions, laws or regulations of Australia, the EuropeanUnion, United Kingdom or United States of America.

General conditions

There are conditions set out in these general conditions, in the claims section and under each particular cover andsection. If any of these conditions are not met, we may refuse to pay a claim, reduce the amount we pay for a claim orin some circumstances wemay cancel your Policy. Whenmaking a claim, you must have met and then continue to complywith the conditions of this Policy.

If you make a fraudulent claim we may refuse to pay that claim or reduce the amount we pay you for it and we may alsocancel your Policy.

24

Assistance and co-operation

You must provide us with all reasonable assistance we require when you deal with us and you will:

be truthful and frank;not behave in a way that is abusive, dangerous, hostile, improper or threatening;co-operate fully with us, even after we have paid a claim.

Care and maintenance

You must take reasonable care to prevent damage, injury or loss. We will not pay for damage, injury, loss or your liabilityto which your failure to take reasonable care is a contributing factor. At all times, you must:

prevent damage to others or their property;minimise the cost of any claim under this Policy;comply with all laws.

Other interests

You must not transfer any interests in this Policy without our written consent.

Any person whose interests you have told us about and we have noted on your Policy Schedule is bound by the termsof this Policy.

Other party's interests

You must tell us of the interest of all parties (e.g. financiers, lessors or owners) who will be covered by this insurance.We will protect their interests only if you have told us about them and we have noted them on your Policy Schedule.

Claims

What you must do after an accident

If an incident happens which may give rise to a claim you must:

take all reasonable steps to secure your vehicle to prevent further loss, damage or liabilitynotify the police immediately if your vehicle or any of your property is stolen or maliciously or intentionally damagedtell us as soon as possible. We will provide you with a claim form and advice on what to dosupply us with all information we require to settle or defend the claimsend to us immediately any letter or communication from other partiestell us immediately of any notice of impending prosecution or details of any inquest or official inquiry.

In an emergency outside normal business hours you may ring our emergency service on 1800 023 387 for assistance.

If in doubt at any time, ring us on 1300 361 823.

What you must not do after an accident

In the event of an incident that may give rise to a claim, you must not:

admit liability if an accident occurs which is likely to result in someone claiming against youmake an offer, settlement, promise or payment

25

incur any costs or expenses without our written consent, in respect of any right or claim which may be the subjectof a claim by you against us under this Policyauthorise repairs to your vehicle without our prior consent. However you may authorise:

the fitting of an identical replacement windscreen or window glassrepairs up to $500 (over and above any applicable excesses) if you are more than 150 kilometres from the normalnightly parked address and they are necessary to enable you to continue your journey.

We pay only once for loss or damage from the same event covered by this Policy even if it is covered under more thanone section of the Policy.

Assessment guarantee

We undertake to assess your vehicle within one working day of being notified of an incident resulting in a claim, if yourvehicle is at a repairer in the metropolitan area of any major city.

Policy comes to an end following a total loss

If we declare your vehicle a total loss and pay you the market value or agreed value or replace your vehicle, then thePolicy will come to an end and you will no longer have any cover. This means you will not be entitled to make any furtherclaim under this Policy and:

where the premium has been paid in full for the period of insurance there will be no refund of any premium, orwhere the premium is paid by instalments, we are entitled to deduct from any claim paid or payable, the balance ofthe unpaid premium or instalments of premium.

Preventing our right of recovery

If you have agreed not to seek compensation from another person who is liable to compensate you for any loss, damageor liability which is covered by this Policy, we will not cover you under this Policy for that loss, damage or liability.

Providing proof

You must be able to prove to us that you have suffered a loss that is covered by this Policy before we will pay you for it.We may ask you for this proof if you make a claim under this Policy. So that your claim can be assessed quickly youshould keep the following:

police reports;receipts or other confirmation of purchase of your vehicle or any accessories, andall service and repair records.

Recovery action and uninsured loss

If we pay your claim, we may seek to recover the amount paid to you from the third party who caused the loss. We willdo this in your name and you must assist us with any reasonable requests.

If you have suffered loss which was not covered by this Policy as a result of the incident, we may offer to attempt torecover this for you. You may specifically ask us to recover this for you. You will need to give us documents supportingyour loss. Before we include any uninsured loss in the recovery action we will also ask you to agree to the basis on whichwe will handle your recovery action. You may need to contribute to legal costs in some circumstances.

26

Salvage

We are entitled to obtain and retain any items or materials that are salvaged or recovered after you make, and we agree,to pay a claim by replacing or paying to replace any items or materials. We may sell the items or materials and keep theproceeds. We may choose to sell the items or materials to you, if you agree to pay the market price for the items ormaterials.

Subrogation

We may at any time, at our expense and in your name, use all legal means available to you of securing reimbursementfor loss or damage arising under this Policy. In the event we do so, you agree to give all reasonable assistance for thatpurpose.

Taxation implications

The amount of premium payable by you for this Policy includes an amount on account of the GST on the premium.

When we pay a claim, your GST status will determine the maximum amount we pay.

When you are:

(a) not registered for GST, or are otherwise not entitled to claim an Input tax Credit the maximum amount we pay isthe sum insured or the other limits of insurance cover including GST, and the sum insured and other limits ofinsurance cover shown on your Policy documentation are inclusive of GST;

(b) registered for GST, we will pay the sum insured/limit of indemnity or the other limits of insurance and where youare liable to pay an amount for GST in respect of an acquisition relevant to your claim (such as services to repaira damaged item insured under the Policy) we will pay for the GST amount.

We will reduce the GST amount we pay by the amount of any input tax credits to which you are or would be entitled ifyou made a relevant acquisition.

In these circumstances, the Input Tax Credit may be claimable through your Business Activity Statement (BAS), and thesum insured and other limits of insurance cover shown on your Policy documentation are exclusive of GST.

You must advise us of your correct Australian Business Number & Taxable Percentage. Any GST liability arising from yourincorrect advice is payable by you.

Where the settlement of your claim is less than the sum insured or the other limits of insurance cover, we will only payan amount for GST (less your entitlement for Input Tax Credit) applicable to the settlement. This means that if theseamounts are not sufficient to cover your loss, we will only pay the GST relating to our settlement of the claim.

We will (where relevant) pay you on your claim by reference to the GST exclusive amount of any supply made by anybusiness of yours which is relevant to your claim.

GST, Input Tax Credit ,Business Activity Statement (BAS) and Acquisition have the same meaning as given to thoseexpressions in A New Tax System (Goods and Services Tax) Act 1999 (Cth) and related legislation as amended from timeto time.

Taxable Percentage is your entitlement to an Input Tax Credit on your premium as a percentage of the total GST on thatpremium.

What you must pay if you make a claim – Excess

‘Excess’ means the first amount you must contribute to any claim you make under this Policy.

27

Depending on the age or experience of the driver, and whether you have told us about them and we have noted themon your Policy Schedule, you may have to contribute more than one excess. Each excess is shown on your Policy Scheduleand is explained below.

Where more than one vehicle is covered under this Policy and those vehicles are involved in the same incident whichgives rise to a claim, you will have to pay the applicable excesses in respect of each vehicle insured under the Policy.

If we accept your claim you must pay the total amount of the applicable excesses either to us or to the repairer. We willtell you to whom they must be paid. However, if your vehicle is a total loss, we may deduct any excess that you mustpay before we make any payment under a claim.

Standard excess

You will have to contribute the first amount of every claim. This amount is shown on the Policy Schedule as the standardexcess.

Age or Inexperienced Driver excess

In addition to the standard excess, you will have to contribute an age excess or inexperienced driver’s excess if at thetime of any incident giving rise to a claim your vehicle is driven by a person:

under the age of 25, or

aged 25 or more but has not held a driver’s licence for 2 or more years.

The amount of the age or inexperienced driver’s excess is shown on your Policy Schedule. You will not have to contributethis age or inexperienced driver’s excess if the only damage to your vehicle is a broken windscreen, or window glass, orcaused by storm or hail damage.

Undeclared Driver’s excess

In addition to any other excesses which apply, you will have to contribute an undeclared driver’s excess if, at the timeof an incident which gives rise to a claim, your vehicle was being driven by or in the charge of a person:

who is a member of your family and they normally live with you, and

whose name has not been shown as a driver on your Policy Schedule.

You will not have to pay this excess if:

the driver of your vehicle is over 25 years of age and has not been convicted of driving under the influence of alcoholor had their licence suspended or cancelled in the 5 years immediately before the accident or loss, or

you satisfy us that an emergency existed, or

the use of your vehicle is shown as business on the Policy Schedule, or

the only damage to your vehicle is a broken windscreen, window glass, hail damage, or loss or damage which occurwhen the vehicle is parked or unattended.

The amount of the undeclared driver’s excess is shown on your Policy Schedule.

28

Learner driver excess

If at the time of a loss or damage a licensed learner driver is in control of the vehicle the excesses that will apply arethose that would have applied to the licensed passenger who is instructing the learner.

Off road

The standard excess plus any other applicable excesses payable under the Policy are doubled if your vehicle is damagedwhile it is being driven on any beach or off any public road (excluding driveways) on land not belonging to you.

Theft

If your vehicle is stolen you must contribute an excess for theft as shown on the Policy Schedule, which is in addition toany other excesses payable.

Security system

If your vehicle is stolen and the security system was not active at that time, you must contribute an excess of $200 inaddition to any other excesses payable.

When you will not have to pay an excess

You will NOT have to contribute any excess towards a claim, if:

(a) you can satisfy us that the claim involves a collision with another vehicle and the collision which gave rise to theclaim was totally the fault of the driver of another vehicle, and

(b) you tell us the registration number of the other vehicle and the full name, licence number and address of the otherdriver, and

(c) the amount of your claim exceeds the applicable excesses under the Policy.

We give this benefit only if we are allowed legally to recover the amount of any loss, including any applicable excessesfrom the responsible person.

If you live in a State or Territory where liability is apportioned in the courts or determined by the Barometer of Responsibility,you will qualify as ‘faultless’ if you are 20% or less to blame for any incident.

This clause does not apply to windscreen damage and you will have to pay any excess applicable for windscreen onlydamage.

Where the driver of the other vehicle disputes who was at fault, you must pay any excess which applies but we will refundit if we are successful in establishing that the other driver was at fault.

Other terms

These other terms apply to how your Policy operates, including what you must do once you've taken out this Policy andwhen you make a claim.

Cancelling your policy

How you may cancel this Policy

29

You may cancel this Policy at any time by telling us in writing that you want to cancel it.Where ‘you’ involves more than one person, we will only cancel the Policy when a written agreement to cancel thePolicy is received from all persons named as the insured.

How we may cancel your Policy

We may cancel this Policy in any of the circumstances permitted by law (e.g. failure to pay the premium by the duedate) by informing you in writingWe will give you notice in person or send it to your address (including an electronic address) last known to us.

Where you have paid your premium in advance of the date you wish to cancel from, we will refund to you the proportionof the premium for the remaining period of insurance. Unless directed otherwise by all insured, the refund will be madepayable to all insured.

Changing your policy

If you want to make a change to this Policy, the change becomes effective when:

we agree to it; andwe give you a new Policy Schedule detailing the change.

Jurisdiction

This Policy will be governed and construed in accordance with the laws of the State of New South Wales, Australia. Youirrevocably and unconditionally agree to submit to the non-exclusive jurisdiction of the courts of New South Wales.

Notices

Any notice we give you will be in writing, and it will be effective:

If it is delivered to you personally; orIt is delivered to you at your address (including an electronic address) last known to us.

It is important for you to tell us of any change of address as soon as possible.

30

This Policy is underwritten by QBE Insurance (Australia) Limited ABN 78 003 191 035 of 2 Park Street, Sydney.

Mercedes-Benz Insurance is a registered name of Mercedes-Benz Financial Services Australia Pty Ltd ABN 73 074 134 517. This insurance is provided on behalf of QBE Insurance Australia Limited ABN 78 003 191 035 AFS Licence No 239545 (QBE). In arranging this insurance, Mercedes-Benz Financial Services Australia Pty Ltd ABN 73 074 134 517 AFS Licence No. 247271 and its authorised Dealers act as agents of the insurer QBE Insurance Australia Limited ABN 78 003 191 035 AFS Licence No 239545 and not as your agent.

QM3315