merc, order in case no. 91 of 2013 page 1 before the

TRANSCRIPT

MERC, Order in Case No. 91 of 2013 Page 1

Before the

MAHARASHTRA ELECTRICITY REGULATORY COMMISSION

World Trade Centre, Centre No.1, 13th Floor, Cuffe Parade, Mumbai – 400 005

Email: [email protected]

Website: www.mercindia.org.in/www.merc.gov.in

Case No. 91 of 2013

IN THE MATTER OF

Petition filed by Vidarbha Industries Power Limited (VIPL) and Reliance

Infrastructure Limited for determination of provisional Tariff for VIPL’s

Butibori Power Plant of 600 MW for FY 2014-15 and FY 2015-16

Shri Vijay L. Sonavane, Member

Smt Chandra Iyengar, Member

ORDER

Date: 17 January, 2014

Vidarbha Industries Power Limited and Reliance Infrastructure Limited submitted a

Petition under Sections 86 (1)(a), 86(1)(b), 62 of the Electricity Act, 2003 and Part E,

Part F and Regulation 100 of MERC MYT Regulations, 2011 before the Maharashtra

Electricity Regulatory Commission (MERC or the Commission) on 24 July, 2013 for

determination of Provisional Tariff for Vidarbha Industries Power Limited’s Butibori

Power Plant for FY 2014-15 and FY 2015-16. The Commission, in exercise of the

powers vested in it under Section 61 and Section 62 of the Electricity Act, 2003 (EA

2003) and all other powers enabling it in this behalf, and after taking into

consideration all the submissions made by the Petitioners, issues raised during the

Public Hearing, and all other relevant material, determines the provisional Tariff of

VIPL’s Butibori Power Plant for FY 2014-15 and FY 2015-16 as under.

MERC Order in Case No 91 of 2013 Page 2

Table of Contents

1 BACKGROUND AND BRIEF HISTORY ........................................................... 5

1.1 Background ..................................................................................................... 5

1.2 Admission of the Petition and Public Process ................................................ 6

1.3 Organisation of the Order ............................................................................... 7

2 OBJECTIONS RECEIVED, VIPL’S RESPONSE AND COMMISSION’S

VIEWS ................................................................................................................... 8

2.1 Offer for supply of power from Wardha power company limited .................. 8

3 APPROACH OF THIS ORDER .......................................................................... 11

4 PROVISIONAL TARIFF OF VIPL’S BUTIBORI POWER PLANT ................ 13

4.1 Background to Project Commissioning ........................................................ 13

4.2 Capital Cost ................................................................................................... 14

4.3 Capital Cost for determination of Tariff ....................................................... 29

4.4 Commission's Views on Prudence Check of Capital Cost ........................... 30

4.5 Means of Finance .......................................................................................... 33

4.6 PROVISIONAL TARIFF ............................................................................. 34

MERC Order in Case No 91 of 2013 Page 3

List of Abbreviations

ACQ Annual Contracted Quantity

AFC Annual Fixed Charges

ARR Aggregate Revenue Requirement

BoP Balance of Plant

BFP Boiler Feed Pump

BTG Boiler Turbine Generator

CA Chartered Accountant

CAPEX/Capex Capital Expenditure

CCEA Cabinet Committee on Economic Affairs

CEA Central Electricity Authority

CERC Central Electricity Regulatory Commission

CIL Coal India Limited

CWIP Capital Work In Progress

EAC Expert Advisory Committee

ECB External Commercial Borrowing

EPC Engineering, Procurement and Construction

ERP Enterprise Resource Planning

FBSM Final Balancing and Settlement Mechanism

FERV Foreign Exchange Rate Variation

FO Furnace Oil

FSA Fuel Supply Agreement

GCPP Group Captive Power Project

GCV Gross Calorific Value

GFA Gross Fixed Assets

ICAI Institute of Chartered Accountants of India

IDC Interest During Construction

IPP Independent Power Project

LoA Letter of Assurance

LDO Light Diesel Oil

LIBOR London Interbank Offered Rate

MAHAGENCO Maharashtra State Power Generation Company Limited

MERC Maharashtra Electricity Regulatory Commission

MIDC Maharashtra Industrial Development Corporation

MLD Million Litres per Day

MERC Order in Case No 91 of 2013 Page 4

MMT Million Metric Tonnes

MMTPA Million Metric Tonnes per Annum

MoC Ministry of Coal

MoEF Ministry of Environment and Forests

MoP Ministry of Power

MoPNG Ministry of Petroleum and Natural Gas

MSPGCL Maharashtra State Power Generating Company Limited

MT Metric Tonnes

OEM Original Equipment Manufacturer

OSBL Outside Boundary Limits

O&M Operation & Maintenance

PLF Plant Load Factor

RBI Reserve Bank of India

RH Relative Humidity

RHT Re-Heat Temperature

RInfra-D Reliance Infrastructure Limited-Mumbai Distribution

RO Reverse Osmosis

RoE Return on Equity

RPL Reliance Power Limited

SFOC Secondary Fuel Oil Consumption

SHR Station Heat Rate

SHT Super Heat Temperature

SICOM State Industrial & Investment Corporation Of

Maharashtra

SPV Special Purpose Vehicle

STPS Super Thermal Power Station

TMCR Turbine Maximum Continuous Rating

TVS Technical Validation Session

USD United States Dollar

VAT Value Added Tax

VIPL Vidharbha Industries Power Limited

WCL Western Coalfields Limited

WPCL Wardha Power Company Limited

MERC Order in Case No 91 of 2013 Page 5

1 BACKGROUND AND BRIEF HISTORY

1.1 Background

1.1.1 This order relates to the Petition filed by Vidarbha Industries Power Limited

(VIPL) and Reliance Infrastructure Limited (RInfra) for the determination of

provisional Tariff of VIPL’s Butibori Power Plant. VIPL is a Generating

Company, which has developed a 600 MW (2 x 300 MW) Power Plant at

Butibori, Nagpur in the State of Maharashtra. Reliance Infrastructure Limited

– Mumbai Distribution (RInfra-D) is a distribution licensee having been

granted a licence under the provisions of Section 14 of the Electricity Act,

2003 for distribution of electricity in the area of supply specified therein

comprising primarily of the suburbs of Mumbai and certain areas falling in the

Mira Bhayander Municipal Corporation.

1.1.2 The Petitioners, in the Petition, has prayed as under:

“

(a) admit the present Petition;

(b) approve the provisional tariff for the 1st Petitioner’s Butibori project

for 600 MW;

(c) approve the request for relaxation of norms and/or removal of

difficulty in respect of (i) Station Heat Rate; (ii) Auxiliary Power

Consumption; and (iii) treatment of cost for hedging foreign currency

loans and/or treatment of foreign exchange rate variation on foreign

currency loans;

(d) dispose-off the present Petition expeditiously

(e) condone any inadvertent omissions/errors or shortcomings in the

Petition;

(f) allow additions/alterations/changes/ amendments to the Petition at a

future date;

(g) grant such order as deemed appropriate under the facts and

circumstances of the case.”

1.1.3 The Petitioners submitted that by the Order dated 20 February, 2013, the

Commission had accorded in-principle approval to the Power Purchase

MERC Order in Case No 91 of 2013 Page 6

Agreement (PPA) between RInfra-D and VIPL for procurement of 300 MW

power on long-term basis from Unit # 2 of VIPL’s Butibori Power Plant.

1.1.4 The Petitioners submitted that by the Order dated 19 July, 2013, the

Commission had accorded in-principle approval to the PPA between RInfra-D

and VIPL for the procurement of 300 MW power on long term basis from

Unit # 1 of VIPL’s Butibori Power Plant.

1.1.5 The Petitioners further submitted that the Commission vide its Order dated 19

July, 2013 had also approved the Consolidation Agreement dated 4 June, 2013

executed between RInfra-D and VIPL for supply under the two PPAs for Unit

# 1 and Unit # 2 to be treated as supply from the Power Plant as a whole for

Tariff and Regulatory purposes.

1.2 Admission of the Petition and Public Process

1.2.1 A set of datagaps were forwarded to VIPL on 8 August, 2013. Another set of

datagaps were forwarded to VIPL on 12 August, 2013. The replies to datagaps

were submitted by VIPL vide its letters dated 16 August, 2013, 17 August,

2013, 19 August, 2013, 27 August, 2013, 28 August, 2013 and 5 September,

2013.

1.2.2 The Technical Validation Session (TVS) was held on 20 August, 2013. During

the TVS, the Petitioner made a presentation focusing on salient features of the

Petition. The list of individuals, who participated in the TVS held on 20

August, 2013 is provided at Appendix-1.

1.2.3 Further, on the directives of the Commission, the Officers of the Commission

held meetings with VIPL and RInfra on 19 August, 2013 and 20 August, 2013

to ensure adequacy of information submitted.

1.2.4 VIPL submitted the revised Consolidated Petition on 5 September, 2013. The

Commission admitted the revised Consolidated Petition on 10 September,

2013. In accordance with Section 64 of the Electricity Act, 2003, the

Commission directed VIPL to publish its Petition in the abridged form to

ensure public participation. The public notice was published in the following

newspapers inviting suggestions/objections from the stakeholders.

MERC Order in Case No 91 of 2013 Page 7

Table 1.1: Newspaper Notice of Public Hearing

Name of the Newspaper Date of publication

Saamna 13 September, 2013

LokSatta 13 September, 2013

Indian Express 13 September, 2013

Hindustan Times 13 September, 2013

1.2.5 The copies of VIPL’s Petition and its Executive summary were made available

at VIPL’s office and on VIPL’s website (www.reliancepower.co.in). The copy

of the Public Notice and the Executive Summary of the Petition were also

made available on the website of the Commission (www.mercindia.org.in/

www.merc.gov.in) in a downloadable format. The Public Notice specified that

the suggestions and objections, either in English or Marathi, may be filed in

the form of an affidavit along with proof of service on VIPL.

1.2.6 The Commission received objections/suggestions/comments from one (1)

stakeholder in writing. The Public Hearing was held on 17 October, 2013 at

Centrum Hall, World Trade Centre-1, Cuffe Parade, Colaba, Mumbai-400005.

The list of individuals who participated in the Public Hearing is provided at

Appendix – 2. The Commission has ensured that the due process as

contemplated under the law to ensure transparency and public participation

was followed at every stage meticulously and adequate opportunity was given

to all persons concerned to file their say in the matter.

1.3 Organisation of the Order

This Order is organised in the following Sections:

Section 1 of the Order provides a brief history of the quasi-judicial regulatory

process undertaken by the Commission. For the sake of convenience, a list of

abbreviations with their expanded forms has been included.

Section 2 of the Order discusses the suggestion raised by the stakeholder in

writing as well as during the Public Hearing before the Commission.

Section 3 of the Order deals with the approach of this Order.

Section 4 of the Order deals with the approval of Provisional Tariff for

VIPL’s Butibori Power Plant for FY 2014-15 and FY 2015-16.

MERC Order in Case No 91 of 2013 Page 8

2 OBJECTIONS RECEIVED, VIPL’S RESPONSE AND COMMISSION’S

VIEWS

2.1 OFFER FOR SUPPLY OF POWER FROM WARDHA POWER

COMPANY LIMITED

2.1.1 Wardha Power Company Limited (WPCL) submitted that it is currently

operating a power plant of installed capacity 540 MW (4 x 135 MW) at

Warora, Maharashtra. WPCL submitted that the Fuel Supply Agreement had

been signed with Western Coal Fields Limited for approximately 70% of the

coal requirement and it is in discussion with Western Coal Fields Limited for

execution of Fuel Supply Agreement for the balance requirement also.

2.1.2 WPCL submitted that the first two Units (2 x 135 MW) are currently

supplying power to RInfra-D in accordance with Power Purchase Agreement

dated 4 June, 2010 executed in pursuance of medium term bidding conducted

by RInfra-D. WPCL submitted that the power from the third and fourth Units

(2 x 135 MW) is being supplied primarily to captive consumers.

2.1.3 WPCL submitted that RInfra-D, in 2009, had floated a long term bid for

procurement of power to the extent of 1500 MW ± 20% for 20 years. WPCL

submitted that it had offered 320 MW at a Levellised Tariff of Rs. 3.421 per

kWh and was the lowest bidder. WPCL submitted that the bid was not taken

up and subsequently lapsed in July, 2010.

2.1.4 WPCL submitted that RInfra-D had floated a medium term bid for supply of

power for 3 years. WPCL submitted that it had offered 270 MW and was the

lowest bidder. WPCL submitted that in spite of RInfra-D seeking to terminate

the PPA, it could commence supply on the intervention of the Commission.

WPCL submitted that this PPA expires on 31 March, 2014.

2.1.5 WPCL submitted that RInfra-D again floated a long term tender for

procurement of 1000 MW ± 20% for supply of power for 25 years. WPCL

submitted that it had offered 220 MW and KSK Mahanadi Power Limited, a

Group Company of WPCL, had offered another 400 MW. WPCL submitted

that the bid was ultimately scrapped by RInfra-D.

2.1.6 WPCL submitted that the Commission vide its Order dated 20 February, 2013

accorded in-principle approval for the PPA between RInfra-D and VIPL for

MERC Order in Case No 91 of 2013 Page 9

supply of 300 MW for 25 years. WPCL submitted that vide its letter dated 5

March, 2013 it had offered to supply to RInfra-D on the same terms and rate

as indicated by VIPL on a long term basis, commencing April 2014.

2.1.7 WPCL submitted that the Commission vide its Order dated 19 July, 2013

accorded in-principle approval for the PPA between RInfra-D and VIPL for

supply of additional 300 MW for 25 years, totalling to 600 MW.

2.1.8 WPCL submitted that its project cost is Rs. 2811 Crore i.e. Rs. 5.2 Crore/MW

as against VIPL’s project cost of Rs. 4063 Crore i.e. Rs. 6.77 Crore/MW.

WPCL submitted that in view of the lower project cost, it would be in a

position to offer supply at a fixed cost lower than Rs. 2.25/ kWh as submitted

by VIPL.

2.1.9 WPCL submitted that while VIPL has Letter of Assurance (LoA) for supply of

coal from WCL, it has a commitment from WCL for full supply of coal

requirement and had been procuring coal from WCL. WPCL submitted that

from fuel preparedness and supply perspective, availability of fuel is more

secure for WPCL. WPCL submitted that its power station is fully operative

and has a track record of continuous supply of 270 MW to RInfra-D and no

changes would be required for physical enabling of the connectivity and

supply.

2.1.10 WPCL submitted that its power station within Maharashtra has not only been

supplying power to RInfra-D under the medium term PPA but has also been

consistently offering the capacity to RInfra-D on long term basis since 2009.

WPCL submitted that procurement from two sources and more than one

generating station would be a good practice and would ensure stability to the

procurement system.

2.1.11 WPCL submitted that on approval for supply at least to the extent of 270 MW,

it would make a detailed presentation on various costs and the likely Tariff for

RInfra-D, to ensure that the Tariff to the end consumer becomes competitive.

WPCL submitted that its participation in the procurement by RInfra-D would

render the Tariff discovery transparent and market determined. WPCL

submitted that it offers to supply 270 MW of power to RInfra-D at the same

Tariff and on the same terms and conditions as is being presently offered by

VIPL. WPCL submitted that being a distribution licensee, RInfra-D is bound

to afford it an opportunity prior to any finalisation and seeking approval of

MERC Order in Case No 91 of 2013 Page 10

PPA by the Commission and prayed that RInfra-D as well as the Commission

would consider its offer.

VIPL’s Reply

2.1.12 VIPL submitted that the present proceedings are for Tariff determination

pursuant to PPA between RInfra-D and VIPL approved by the Commission

and objections raised by WPCL are not relevant in these proceedings.

Commission’s view

2.1.13 In exercise of powers conferred under the Electricity Act, 2003 under Section

86 among others, the Commission has notified MERC MYT Regulations,

2011 and has specified the provisions for approval of Power Purchase

Agreement for supply of power from a Generating Station to a Distribution

Licensee. The Commission in accordance with the provisions of MERC MYT

Regulations, 2011 shall determine the Tariff for supply of electricity from a

Generating Station to a Distribution Licensee pursuant to the approval of PPA

between the Generating Station and Distribution Licensee. The Commission

had approved the PPAs as well as the Consolidation Agreement entered into

between VIPL and RInfra-D for supply of power from VIPL’s Butibori Power

Plant to RInfra-D after due regulatory process in accordance with MERC

MYT Regulations, 2011.

The Commission is of the view that the purchase of power by RInfra-D from

WPCL is a decision to be taken by RInfra-D. Moreover, the issue raised by

WPCL is not relevant as far as determination of provisional Tariff for VIPL

for supply of power to RInfra-D is concerned.

MERC Order in Case No 91 of 2013 Page 11

3 APPROACH OF THIS ORDER

3.1.1 VIPL filed the present Petition for determination of Provisional Tariff for

supply of 600 MW from its Butibori Power Plant for FY 2014-15 and FY

2015-16 under Sections 86 (1)(a), 86(1)(b), 62 of the Electricity Act, 2003 and

Part E, Part F and Regulation 100 of MERC MYT Regulations, 2011.

3.1.2 Regulation 17.2.1 of MERC MYT Regulations, 2011 specifies as under:

“The tariff for the supply of electricity by a Generating Company to a

Distribution Licensee from a new generating Unit/Station shall be in

accordance with tariff as per power purchase agreement approved by the

Commission, except if such power purchase agreement has been exempted

from requiring such approval in accordance with Part D of these

Regulations.”

3.1.3 The Commission accorded in-principle approval to the PPA executed between

VIPL and RInfra-D for supply from Unit # 2 of VIPL’s Butibori Power Plant

vide its Order dated 20 February, 2013 and for supply from Unit # 1 of VIPL’s

Butibori Power Plant vide Order dated 19 July, 2013. Further, the Commission

also approved the Consolidation Agreement for supply of 600 MW from

VIPL’s Butibori Power Plant to RInfra-D.

3.1.4 Regulation 38.4 of MERC MYT Regulations, 2011 specify as under:

“A Generating Company may make a Petition for determination of

provisional tariff in advance of the anticipated Date of Commercial Operation

of Unit or Stage or Generating Station as a whole, as the case may be, based

on the capital expenditure actually incurred up to the date of making the

Petition or a date prior to making of the Petition, duly audited and certified by

the statutory auditors and the provisional tariff shall be charged from the date

of commercial operation of such Unit or Stage or Generating Station, as the

case may be.”

3.1.5 VIPL submitted that Unit # 1 has achieved COD on 4 April, 2013 and COD of

Unit # 2 has taken longer time than expected due to non availability of

SICOM/railway land that constitutes small portion of total land required for

MERC Order in Case No 91 of 2013 Page 12

completion of Railway Siding. VIPL submitted that all efforts are being made

to get the approval for transfer of SICOM/Railway land at the earliest. VIPL

in its petition submitted that majority of works on railway siding have already

been completed and the completion of works for railway siding and COD of

Unit # 2 is expected to be achieved by March, 2014.

3.1.6 The regulated supply of power from VIPL to RInfra-D shall commence from 1

April, 2014. The Commission in this Order has approved the Provisional

Tariff of Butibori Power Plant for FY 2014-15 and FY 2015-16 based on the

scrutiny of information furnished by VIPL in accordance with the provisions

of MERC MYT Regulations, 2011.

MERC Order in Case No 91 of 2013 Page 13

4 PROVISIONAL TARIFF OF VIPL’S BUTIBORI POWER PLANT

4.1 Background to Project Commissioning

4.1.1 VIPL is a Special Purpose Vehicle (SPV) established for implementation of a

Group Captive Power Project through Competitive Bidding Process conducted

by MIDC.

4.1.2 The Generating Station awarded to VIPL for implementation was initially of

130 MW capacity and later enhanced to 300 MW. Further, VIPL was

permitted to expand the capacity of the Station by adding Unit # 2 of 300 MW

capacity under IPP route.

4.1.3 As adequate industrial consumers have not shown interest in procuring power

from Unit # 1 of Generating Station under GCPP route, VIPL has offered the

entire 600 MW to RInfra-D and has executed PPAs for supply of 600 MW to

RInfra-D under the provisions of Electricity Act, 2003 and MERC MYT

Regulations, 2011.

4.1.4 The Commission vide its Order dated 20 February, 2013 in Case No. 2 of

2013 accorded in-principle approval to the PPA between VIPL and RInfra-D

for supply of 300 MW from Unit # 2 (IPP).

4.1.5 The Commission vide its Order dated 19 July, 2013 in Case No. 76 of 2013

accorded in-principle approval to the PPA between VIPL and RInfra-D for

supply of 300 MW from Unit # 1 (GCPP converted to IPP).

4.1.6 VIPL submitted that it had awarded 3 separate EPC Contracts to Reliance

Infrastructure Limited for Unit # 1, Unit # 2 and Railway siding works.

4.1.7 VIPL submitted that Unit # 1 has achieved Commercial Operation Date

(COD) on 4 April, 2013 and Unit # 2 is expected to get commissioned by

March, 2014. VIPL further submitted that COD of Unit # 2 has taken longer

than expected time due to non-availability of SICOM/ railway land which

constitutes a small portion (~12%) of the total land required for completion of

Railway siding. VIPL submitted that all efforts are being made to get the

approval for transfer of SICOM/ Railway land at the earliest. VIPL also

submitted that since majority of works on railway siding have already been

MERC Order in Case No 91 of 2013 Page 14

completed, assuming availability of SICOM/ Railway land by October 2013,

the completion of works for railway siding and COD of Unit # 2 is expected to

be achieved by March, 2014.

4.1.8 The key milestones submitted by VIPL are shown in the Table below:

Table 4.1: Key milestones

S. No. Event Unit # 1 Unit # 2

1 Investment approval by the

Board 17 October, 2009 13 September, 2010

2 Date of synchronisation 25 June, 2012 2 January, 2013

3 Date of taking full load 17 August, 2012 19 March, 2013

4 Performance Guarantee

Tests Not carried out Not carried out

5 COD 4 April, 2013 Expected by March

2014

4.1.9 VIPL submitted the Audited Accounts for FY 2012-13. VIPL also submitted

the CA certificate for capital expenditure incurred till 31 May, 2013.

4.2 Capital Cost

4.2.1 As regards Capital Cost, Regulation 27 of MERC MYT Regulations, 2011

specifies as under:

“27.1 Capital cost for a project shall include

(a) the expenditure incurred or projected to be incurred, including

interest during construction and financing charges, any gain or

loss on account of foreign exchange risk variation on the loan

during construction up to the date of commercial operation of the

project, as admitted by the Commission, after prudence check;

(b) capitalised initial spares subject to the ceiling rates specified in

this Regulation; and

(c) additional capital expenditure determined under Regulation 28:

.....”

4.2.2 VIPL submitted that Unit # 1 achieved COD on 4 April, 2013 and Unit # 2 is

expected to get commissioned by March, 2014. VIPL submitted that COD of

Unit # 2 has taken longer than expected time due to non-availability of

MERC Order in Case No 91 of 2013 Page 15

SICOM/ railway land which constitutes a small portion (~12%) of the total

land required for completion of Railway siding. VIPL further submitted that

all efforts are being made to get the approval for transfer of SICOM/ Railway

land at the earliest. VIPL submitted that since majority of works on railway

siding have already been completed, assuming availability of SICOM/

Railway land by October 2013, the completion of works for railway siding and

COD of Unit # 2 is expected to be achieved by March, 2014. VIPL submitted

that for the purpose of this Petition, the COD of the station as a whole implies

that the second Unit of 300 MW is also declared to be commercially

operational.

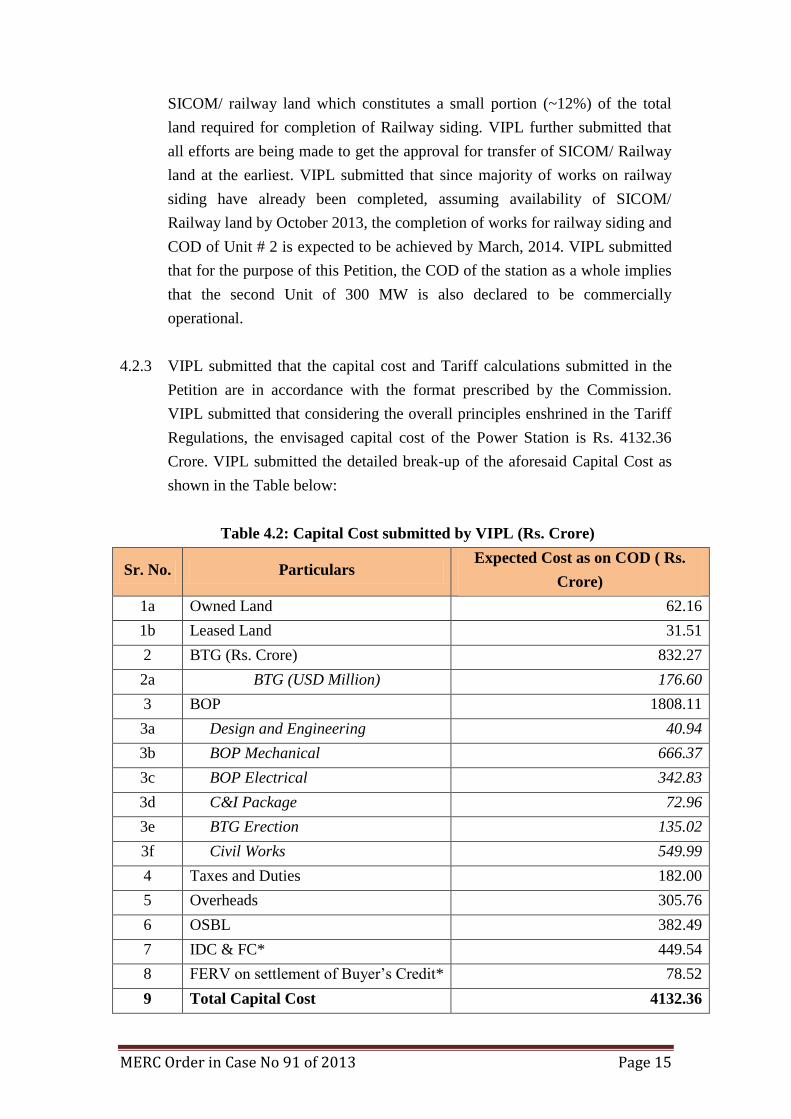

4.2.3 VIPL submitted that the capital cost and Tariff calculations submitted in the

Petition are in accordance with the format prescribed by the Commission.

VIPL submitted that considering the overall principles enshrined in the Tariff

Regulations, the envisaged capital cost of the Power Station is Rs. 4132.36

Crore. VIPL submitted the detailed break-up of the aforesaid Capital Cost as

shown in the Table below:

Table 4.2: Capital Cost submitted by VIPL (Rs. Crore)

Sr. No. Particulars Expected Cost as on COD ( Rs.

Crore)

1a Owned Land 62.16

1b Leased Land 31.51

2 BTG (Rs. Crore) 832.27

2a BTG (USD Million) 176.60

3 BOP 1808.11

3a Design and Engineering 40.94

3b BOP Mechanical 666.37

3c BOP Electrical 342.83

3d C&I Package 72.96

3e BTG Erection 135.02

3f Civil Works 549.99

4 Taxes and Duties 182.00

5 Overheads 305.76

6 OSBL 382.49

7 IDC & FC* 449.54

8 FERV on settlement of Buyer’s Credit* 78.52

9 Total Capital Cost 4132.36

MERC Order in Case No 91 of 2013 Page 16

* till 31 May, 2013

4.2.4 VIPL submitted that the Capital Cost submitted is the expected Capital Cost of

the power station as a whole and the same is based on the following

considerations:

i. VIPL submitted that the IDC and Financing Charges submitted in the

Petition are till 31 May, 2013. VIPL submitted that IDC for Unit # 1 is

considered till its COD on 4 April, 2013. VIPL submitted that post

April 2013, 40% of the overall interest liability for the Station is

allocated to Unit # 1 and the balance has been considered as IDC

against Unit # 2. VIPL submitted that the same is assumed on a

notional basis since the loans have been taken for both Units together

and there is no segregation of loans between the two Units. VIPL

submitted that it would furnish the actual IDC for the project at the

time of final determination of Tariff.

ii. VIPL submitted that the capital cost is inclusive of overheads, start-up

expenses and the realized foreign exchange differences on settlements

of Buyer’s Credit as on 31 May, 2013 as per CA certificate. VIPL

submitted that the capital cost does not include any unrealized

exchange rate differences on foreign currency loan and liability and the

same shall be submitted to the Commission post the COD of the

station along with audited accounts at the time of final determination

of Tariff. VIPL submitted that it would submit the final capital cost

including IDC and other breakup post COD of the station along with

audited accounts at the time of final determination of Tariff.

Land and Site development

4.2.5 VIPL submitted that the land acquired for the project is a mix of

MIDC/SICOM land and private land. VIPL submitted that as against the

original estimate of Rs. 80 Crore for land and site development, the expected

cost as on COD of the project is Rs. 93.67 Crore. VIPL submitted that the

increase in cost of land and site development is because of the increase in

price of MIDC land from Rs. 4 Lakh/acre to Rs. 19 Lakh/acre. VIPL

submitted that this increase also had an impact on private land acquisition.

4.2.6 The Commission directed VIPL to submit the summary statement of land

acquired from all the sources along with the acquisition rate. Further, the

MERC Order in Case No 91 of 2013 Page 17

Commission asked VIPL to submit the supporting documents for increase in

price of MIDC land from Rs. 4 Lakh/acre to Rs. 19 Lakh/acre.

4.2.7 VIPL submitted the summary statement of land acquired from all sources as

shown in the Table below:

Table 4.3: Summary statement of land acquired as submitted by VIPL

S. No. Source Area (in acres) Total cost

(Rs. Crore)

Average

acquisition rate

(Rs. Crore/acre)

1 MIDC Land 298 23 0.08

2 Private Land 257 61 0.24

4.2.8 VIPL submitted the details of land acquired from MIDC as shown in the Table

below:

Table 4.4: Details of MIDC land acquired submitted by VIPL

MIDC land Area Cost of land Rate

Sq. m Acre Rs. Crore Rs. Crore/acre

D-3 700000 173 7.00 0.04

D-3/Part 200000 49 3.45 0.07

D-3/Part 1 205099 51 8.20 0.16

RS-1 101175 25 4.05 0.16

P-81 1250 0.31 0.06 0.19

P-82 1440 0.36 0.07 0.19

4.2.9 VIPL submitted that the details regarding the SICOM and Railway land would

be provided after the completion of transfer process.

4.2.10 VIPL submitted the lease deed of MIDC land D-3 that was acquired at rate of

Rs. 4 Lakh/acre and lease deed of MIDC land P-81 acquired at rate of Rs. 19

Lakh/acre.

4.2.11 The Commission further directed VIPL to submit the comparison of cost of

land and site development between original estimates and expected cost as on

COD of the project in terms of quantum and price. VIPL submitted the details

of land for Butibori Power Plant as shown in the Table below:

MERC Order in Case No 91 of 2013 Page 18

Table 4.5: Details of Land for Butibori Power Plant submitted by VIPL

S.

No. Particulars

Quantum of land

acquired/leased

(Acres)

Cost per acre of

land (Rs. Crore)

Total Cost (Rs.

Crore)

Original

estimate Actual

Original

estimate Actual

Original

estimate Actual

1 MIDC 305 298 0.040 0.078 12.20 23.24

2 Private 263 270 0.235 0.239 61.81 65.61

3 SICOM 47 47 0.110 0.113 5.17 5.31

4 Railway 3 3 0.167 0.167 0.50 0.50

Total 618 618 - - 79.68 93.67

EPC Contracts for Unit # 1 and Unit # 2

4.2.12 VIPL submitted that it has awarded two separate EPC contracts for Unit # 1

and Unit # 2 to Reliance Infrastructure Limited.

4.2.13 The Commission directed VIPL to submit the copies of EPC Contracts for

Unit # 1 and Unit # 2. The Commission also asked VIPL to submit the basis of

allocation of EPC cost under various heads as in Form 3.1.

4.2.14 VIPL submitted the copies of EPC contracts and amendments thereto for Unit

# 1 and Unit # 2.

4.2.15 VIPL submitted that the EPC contracts were awarded by VIPL as turnkey

project execution where the EPC contractor is responsible for engineering to

commissioning of the plant. VIPL submitted that the EPC cost has been

finalised as lump sum turnkey contract for total scope and not based on

individual package basis. VIPL submitted that the break-up of prices for

mechanical, electrical, civil and other packages have been provided in Form

3.1 based on the agreed billing schedule between the parties for the purpose of

payment, out of the total lump sum turnkey contract which provides the values

for onshore equipment supply, construction and services (other than BTG).

VIPL submitted that these prices are inclusive of Taxes and Duties as per the

EPC contracts.

MERC Order in Case No 91 of 2013 Page 19

4.2.16 The Commission also directed VIPL to submit how the least cost principle

was ensured in the award of contracts.

4.2.17 VIPL submitted that it is a 100% owned subsidiary of Reliance Power Limited

(RPL). VIPL submitted that as a leading private sector power developer, RPL

has institutionalised rigorous procurement processes. VIPL submitted that the

same are backed by repository of data gathered from own project development

experiences, information available in public domain and market intelligence.

4.2.18 VIPL submitted that all the special purpose vehicles (SPVs) set up by RPL

adopt the rigorous procurement processes stipulated by the parent company.

VIPL submitted that while undertaking capital procurement, the relevant

project development teams undertake a detailed benchmarking exercise. VIPL

submitted that all underlying cost assessments involve; (a) Total capital cost

and (b) Life cycle cost considering both, capital cost and operating cost.

4.2.19 VIPL submitted that the cost benchmarking exercise for EPC cost entails a

bottom-up build up of costs of distinct system/packages, considering

(a) Least purchase price ever paid for a given system/package – adjusted for

inflation /applicable commodity prices changes

(b) Bill of Materials based estimates, where possible

(c) Market comparables

(d) Price which can be sustained by the project to remain competitive

4.2.20 VIPL submitted that the target benchmark cost is based on the lowest of the

cost benchmarks developed using above approaches. VIPL submitted that the

confidentiality of the same is strictly maintained to ensure sanctity of the

procurement process and effectiveness of its outcome. VIPL submitted that the

target benchmark cost forms the critical guiding input for the decision to

award EPC Contract. VIPL submitted that other factors which also form key

inputs to the procurement decision are (a) Schedule of Delivery (b) Quality (c)

Sustainability and (d) Environmental impact. VIPL submitted that the above

approach ensures that capital procurement decisions are based on a sound and

rigorous process aimed at optimizing life cycle cost of the project.

MERC Order in Case No 91 of 2013 Page 20

4.2.21 VIPL submitted that Butibori project was originally conceived as one Unit of

300 MW to be developed as GCPP. VIPL submitted that the same was

awarded through competitive bidding process by MIDC. VIPL submitted that

51% of power to be produced by the project was proposed to be sold to

industrial consumers with their equity participation, to qualify as GCPP. VIPL

submitted that in addition, an additional capacity of 300 MW was undertaken

at the same site. VIPL submitted that ensuring competitiveness of the project

has been at the core of development philosophy of this project.

4.2.22 VIPL submitted that the project was executed by awarding the EPC contract,

whereby the entire responsibility of construction of the project is with the EPC

contractor. VIPL submitted that the EPC contract price offered by Reliance

Infrastructure Limited was compared with EPC contract cost benchmarks for

similar projects at that point of time, with BTG supply awarded to Reliance

Infra Projects (UK) Limited. VIPL submitted that for competiveness of

procurement, it had also undertaken due-diligence on the market dynamics

prevalent at the time of award of the contract.

4.2.23 VIPL submitted that for the construction of a power plant, there exist two

kinds of packages namely mandatory packages (BTG, BOP, Civil etc) and

project specific additional packages (township, transmission line and railway

siding). VIPL submitted that the comparison was undertaken for mandatory

packages.

4.2.24 VIPL submitted that post award of contracts, it has undertaken an exercise to

compare the EPC costs of some other stations developed by Central Sector

entities and State Sector entities. VIPL submitted that appropriate correction

factors (escalation factors for year of award, Unit size correction factors,

taxes) have been applied to make the comparison on a like-to-like basis.

4.2.25 The Commission asked VIPL to submit the Detailed Project Report (DPR) for

the project. VIPL submitted the DPR for Unit # 1 and Unit # 2. In the said

DPRs, the estimated capital cost for Unit # 1 is Rs. 2070 Crore including IDC

and the estimated capital cost for Unit # 2 is Rs. 1563 Crore including IDC.

Hence, the estimated capital cost as per the DPRs for the project is Rs. 3633

Crore including IDC.

MERC Order in Case No 91 of 2013 Page 21

Railway siding

4.2.26 VIPL submitted that it has awarded EPC contract for Railway siding works to

Reliance Infrastructure Limited.

4.2.27 VIPL submitted that as against the original estimate of Rs. 273 Crore, the

expected cost of Railway siding works as on COD of the project is Rs. 347.03

Crore.

4.2.28 VIPL submitted that the scope of Railway siding work changed due to

relocation of marshalling yard and route alignment change as per the

requirement of Railways. VIPL submitted that the variation is primarily on

account of following:

a. VIPL submitted that scope addition of Minor Bridges contributed to

increase of Rs. 20 Crore.

b. VIPL submitted that the span of major bridges has changed due to change

in location of marshalling yard. VIPL submitted that the scope addition of

Major Bridges contributed to increase of Rs. 22 Crore.

c. VIPL submitted that the track length had increased due to change in

location of marshalling yard and this contributed to increase of Rs. 4

Crore.

4.2.29 VIPL submitted that in order to have operational flexibility for handling

loaded rakes additional locomotive has been envisaged and this scope addition

of Diesel locomotive contributed to Rs. 11 Crore.

4.2.30 VIPL submitted that the scope addition of Station yard/Railway Utility

building and other miscellaneous works as per Railways requirement

contributed to Rs.10 Crore.

4.2.31 The Commission asked VIPL to submit the copy of EPC contract for Railway

siding. VIPL submitted the copy of EPC contract and amendments thereto for

Railway siding.

4.2.32 The Commission observed that the contract price in the EPC contract

submitted is Rs. 342.54 Crore where VIPL submitted the cost of Rs. 347.03

MERC Order in Case No 91 of 2013 Page 22

Crore. The Commission asked VIPL to submit the reason for this variation.

VIPL submitted that the difference is due to price adjustment of Rs. 4.49

Crore due to delay in transfer of land from SICOM and Railways.

Overheads

4.2.33 VIPL submitted that against the original estimate of Rs. 155 Crore, the

expected cost of overheads as on COD of the project is Rs. 305.76 Crore.

4.2.34 VIPL submitted that the increase in cost of overheads is due to the following

reasons:

i. Royalty payments for Railway siding embankment - VIPL submitted that

due to change in the rates of royalty from Rs. 100 per brass to Rs. 200 per

brass the variation in royalty is approximately Rs. 9 Crore.

ii. Capital cost contribution paid to MIDC for water allocation – VIPL

submitted that against the total water requirement of 22 MLD for one Unit,

MIDC initially allotted 15 MLD without charging capital cost contribution

(Onetime payment to MIDC) and for balance 7 MLD, MIDC charged

Rs.12 Crore as capital cost contribution fees.

iii. Restoration charges paid to Irrigation Department for water allocation –

VIPL submitted that as per MIDC policy, for the industries located in

MIDC area water shall be provided by MIDC. VIPL submitted that due to

non availability of water allocation to MIDC from Irrigation Department,

MIDC had asked VIPL to arrange water from alternate source. VIPL

submitted that it had approached Irrigation Department and got water

allocation. VIPL submitted that Irrigation Department charged restoration

charges of Rs. 13 Crore.

iv. Railway deposit works and codal charges – VIPL submitted that in Sindhi

station yard many modification works are being carried out as per the

instructions of Railways and the amount of such expenses is estimated at

Rs. 35 Crore.

v. Transmission line outage charges paid to MSETCL – VIPL submitted that

in Railway alignment one EHV line is crossing. VIPL submitted that it

MERC Order in Case No 91 of 2013 Page 23

necessitated increasing the height of EHV tower. VIPL submitted that for

raising the tower MSETCL has charged an outage charge of Rs.4 Crore.

vi. VIPL submitted that start up expenses have gone up primarily on account

of higher than anticipated spend on account of the following factors:

a. VIPL submitted that purchase of market coal due to non availability of

linkage coal resulted in additional cost of Rs. 15 Crore.

b. VIPL submitted that as per MSEDCL's policy, payments were made

only for infirm power during peak hours resulting in non recovery of

Rs. 20 Crore towards expenses for infirm power.

c. VIPL submitted that purchase of oil contributed to increase on start up

expenses.

d. VIPL submitted that start up power from MSEDCL contributed to

increase in start up expenses.

vii. VIPL submitted that administrative expenses have also gone up.

viii. VIPL submitted that increase in insurance and other expenses led to

increase of Rs.10 Crore.

ix. VIPL submitted that due to change in COD of units there is an increase in

overheads to the extent of Rs.10 Crore.

4.2.35 The Commission asked VIPL to submit the break-up of overheads cost. The

Commission also asked VIPL to submit the month wise details of fuel

consumed, revenue billed and revenue recovered by sale of infirm power.

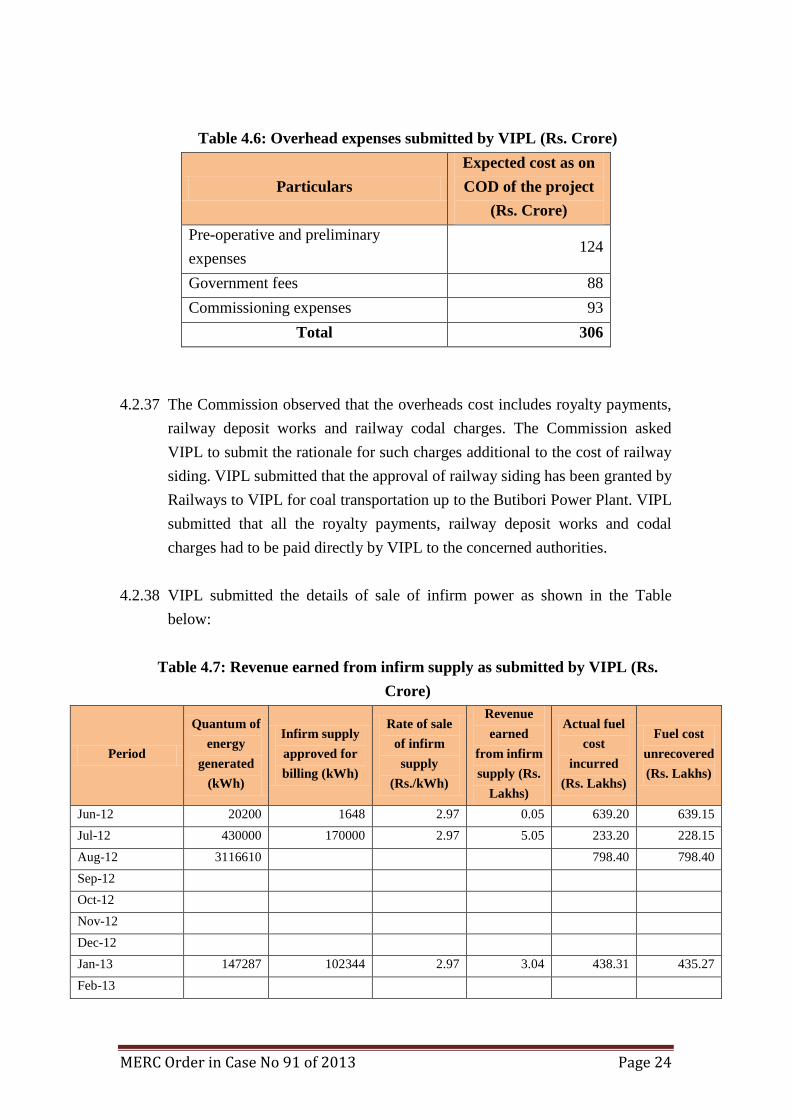

4.2.36 The break-up of overheads cost submitted by VIPL is shown in the Table

below:

MERC Order in Case No 91 of 2013 Page 24

Table 4.6: Overhead expenses submitted by VIPL (Rs. Crore)

Particulars

Expected cost as on

COD of the project

(Rs. Crore)

Pre-operative and preliminary

expenses 124

Government fees 88

Commissioning expenses 93

Total 306

4.2.37 The Commission observed that the overheads cost includes royalty payments,

railway deposit works and railway codal charges. The Commission asked

VIPL to submit the rationale for such charges additional to the cost of railway

siding. VIPL submitted that the approval of railway siding has been granted by

Railways to VIPL for coal transportation up to the Butibori Power Plant. VIPL

submitted that all the royalty payments, railway deposit works and codal

charges had to be paid directly by VIPL to the concerned authorities.

4.2.38 VIPL submitted the details of sale of infirm power as shown in the Table

below:

Table 4.7: Revenue earned from infirm supply as submitted by VIPL (Rs.

Crore)

Period

Quantum of

energy

generated

(kWh)

Infirm supply

approved for

billing (kWh)

Rate of sale

of infirm

supply

(Rs./kWh)

Revenue

earned

from infirm

supply (Rs.

Lakhs)

Actual fuel

cost

incurred

(Rs. Lakhs)

Fuel cost

unrecovered

(Rs. Lakhs)

Jun-12 20200 1648 2.97 0.05 639.20 639.15

Jul-12 430000 170000 2.97 5.05 233.20 228.15

Aug-12 3116610 798.40 798.40

Sep-12

Oct-12

Nov-12

Dec-12

Jan-13 147287 102344 2.97 3.04 438.31 435.27

Feb-13

MERC Order in Case No 91 of 2013 Page 25

Period

Quantum of

energy

generated

(kWh)

Infirm supply

approved for

billing (kWh)

Rate of sale

of infirm

supply

(Rs./kWh)

Revenue

earned

from infirm

supply (Rs.

Lakhs)

Actual fuel

cost

incurred

(Rs. Lakhs)

Fuel cost

unrecovered

(Rs. Lakhs)

1 March, 2013 to

19 March, 2013 1515509 243.71 243.71

31 March 2013 21 FBSM not yet

finalised

Rate of Net

Realisation

from FBSM

statement

55.00 55.00

Apr-13 1380602 FBSM not yet

finalised

Rate of Net

Realisation

from FBSM

statement

304.00 304.00

Total 6610228 273992 - 8.14 2711.82 2703.68

4.2.39 The Commission asked VIPL to submit the copies of agreements executed for

infirm power supply. VIPL submitted the copies of letters from MSEDCL and

RInfra-D regarding the approval of purchase of infirm power from Unit # 1 of

its Butibori Power Plant.

4.2.40 The Commission also asked VIPL to submit the increase in overheads cost

due to delay in COD of the Units.

4.2.41 VIPL submitted that to complete the Railway siding, few pockets of identified

land were required to be procured from SICOM and Central Railways. VIPL

submitted that railway siding is critical for securing sustained fuel supplies to

the power station. VIPL submitted that transportation of coal by road and

simultaneous sustained operation of both the Units based on coal transported

by road is not a feasible option from environmental and logistical point of

view.

4.2.42 VIPL submitted that majority of works on railway siding are completed except

the work on pockets of land mentioned above. VIPL submitted that without

completion of these works, the railway siding cannot be put to use. VIPL

submitted that non availability of pockets of land has delayed completion of

railway siding and has therefore delayed COD of the project.

MERC Order in Case No 91 of 2013 Page 26

4.2.43 VIPL submitted that an application for transfer of identified land from SICOM

was made in January, 2009. VIPL submitted that based on the demand note

given by SICOM, it had paid 50% advance amount for the land in May, 2011.

VIPL submitted that for the final transfer of land, SICOM is required to take

clearance from Industry, Revenue and Law and Judiciary departments of

Government of Maharashtra. VIPL submitted that it had made significant

efforts at almost every level in each government department to speed up the

clearance process for land acquisition with the relevant authorities. VIPL

submitted that despite relentless follow-up, the process of clearance from

various departments has taken time far beyond expectations. VIPL submitted

that recent discussions with authorities have confirmed that final go through

for land acquisition from SICOM would be given soon.

4.2.44 VIPL submitted that similar application for transfer of identified land pocket

had been made to Central Railways in August, 2010. VIPL submitted that the

Detailed Engineering Scale Plan was approved by the relevant authorities in

June, 2011 enabling Railway Land Licensing approval process. VIPL

submitted that the final go ahead of Central Railways has not yet been

received because of prolonged internal clearance process. VIPL submitted that

recent discussions with authorities has confirmed that final go ahead will be

released soon by the Head Office of Central Railways enabling land

possession process. VIPL submitted that completion of railway siding is a

must for procurement of coal for sustained operation of the plant and the

procurement is not possible through other transportation means such as road

transport as it would lead to huge traffic congestion due to continuous

movement of vehicles and restrictions on such movement of vehicles on

account of railway crossing that the vehicles have to traverse for such coal

transport. VIPL submitted that in spite of such coal procurement issues, it had

declared the commercial operation of Unit # 1 based on market coal procured

through road transport. VIPL submitted that the same is not possible for entire

plant as this will lead to movement of at least 430 trucks carrying aggregate

8600 MT of coal on a daily basis from Butibori Railway Station to the Plant

Coal Yard. VIPL submitted that it would cause huge traffic congestion and is

logistically infeasible due to existence of railway crossing as mentioned

above.

4.2.45 VIPL submitted that although Unit # 1 has achieved full load operation on 17

August, 2012 the COD of the Unit was delayed on account of non availability

of Carpet Coal required for commissioning purposes from WCL. VIPL

MERC Order in Case No 91 of 2013 Page 27

submitted that Carpet coal was recommended by CEA and WCL has not

supplied the same.

4.2.46 VIPL submitted that because of the reasons stated above, the COD of the

Project has been delayed and the same has led to increase in overhead cost and

increase in IDC. VIPL submitted that none of the reasons can be attributed to

VIPL and have been caused primarily by external agencies and thus are

uncontrollable in nature. VIPL requested the Commission to accord its

approval for the increase in overheads as the same have arisen due to reasons

beyond its control and could not be avoided despite its best efforts.

Initial spares

4.2.47 The Commission asked VIPL to submit the list of initial spares included in

Capital Cost. VIPL submitted that the procurement of initial spares was done

as recommended by OEMs to the EPC contractor. VIPL submitted that the

quantum of initial spares lie within the normative limits as per MERC MYT

Regulations, 2011 and submitted the list of initial spares.

4.2.48 The Commission also asked VIPL to submit the cost of equipment and cost of

spares under each package separately inclusive of taxes and duties. VIPL

submitted the details of cost of spares as shown in the Table below:

Table 4.8: Cost of spares submitted by VIPL

Package Package Cost

(Rs. Crore)

Equipment cost

(Rs. Crore)

Spares cost

(Rs. Crore)

BTG 176.60 169.00 7.60

BOP Mechanical 666.37 616.88 49.48

BOP Electrical 342.83 337.16 5.68

BOP C&I 72.96 70.10 2.86

Total 65.62

Interest During Construction (IDC)

4.2.49 VIPL submitted Rs. 449.54 Crore as IDC as on 31 May, 2013 as against the

original estimate of Rs. 398.00 Crore. VIPL submitted that post COD of Unit

# 1, 40% of IDC is allocated to Unit # 1 and the balance has been allocated to

Unit # 2. VIPL submitted that the increase in IDC is due to delay in COD of

MERC Order in Case No 91 of 2013 Page 28

Unit # 1 and non achievability of COD of Unit # 2 due to non availability of

SICOM and Railway land required for completion of railway siding.

4.2.50 The Commission asked VIPL to submit the computations of original estimates

of IDC of Rs. 398.00 Crore submitted in the Petition. VIPL submitted the

excel workings of original estimates of IDC.

4.2.51 The Commission also asked VIPL to submit the rationale of allocating IDC

post COD of Unit # 1. VIPL submitted that the financing of the project is

combined financing. VIPL submitted that as the loans were not allocated Unit

wise, the allocation of interest liability post COD of Unit # 1 has been

considered based on the ratio of capitalisation of assets at the time of COD of

Unit # 1 (Rs. 1364 Crore) and the total hard cost of the project (Rs. 3604

Crore), which is around 40%.

Financing Charges

4.2.52 The Commission asked VIPL to submit the basis and computations of

financing charges, commitment charges and other charges as submitted in

Form 3.7. VIPL submitted that the financing charges submitted are based on

the audited accounts. The break-up of financing charges submitted by VIPL is

shown in the Table below:

Table 4.9: Breakup of financing charges submitted by VIPL

Loan Particulars

Financing

charges

(Rs. Crore)

Rupee Term Loan

Upfront fee paid to Rupee lenders in the consortium

14.16 Bank Guarantees issued in favour of

coal/customs/statutory bodies for performance

purposes. Commission paid on quarterly/upfront basis

ECB Loan Upfront fee paid 10.17

Buyer’s Credit

Commission/Bank charges/LC fee paid to domestic

lenders issuing the letter of undertaking to the foreign

bank for Buyer’s credit. Fee on sharing basis with lead

bank and domestic bank in consortium involving

multiple entities.

24.91

Arranger fee/upfront fee paid to foreign bank 0.99

Total 50.22

MERC Order in Case No 91 of 2013 Page 29

4.3 Capital Cost for determination of Tariff

4.3.1 VIPL submitted that for the purpose of provisional Tariff, it has considered the

written down value of the project as on 1 April, 2014 as Rs. 4063.05 Crore.

4.3.2 VIPL submitted that the envisaged capital cost of the project is Rs. 4132.36

Crore. VIPL submitted that Unit # 1 has achieved COD on 4 April, 2013 and

COD of Unit # 2 is envisaged by March, 2014. VIPL submitted that it would

be prudent to consider the written down value of assets for the purpose of

determination of Tariff under the PPA from 1 April, 2014.

4.3.3 VIPL submitted that it had deducted the depreciation amount of Rs. 69.31

Crore pertaining to the period from April, 2013 to March, 2014. VIPL

submitted that it would submit the corresponding depreciation amount

pursuant to COD of the project for the purpose of estimation of written down

value of the generating station during the determination of final Tariff. VIPL

submitted that the overall written down value of the power station considered

for the purpose of Tariff determination is Rs. 4063.05 Crore after deducting

the depreciation of Rs. 69.31 Crore from expected capital cost of Rs. 4132.36

Crore as on COD of the project.

4.3.4 VIPL submitted that it has considered the Debt Equity ratio of 70:30 as

envisaged at the time of COD of the station. VIPL submitted the overall loan

and equity components as on 1 April, 2014 based on the written down value of

the capital cost of the Station as shown in the Table below:

Table 4.10: Project funding based on written down value of capital cost as on

1 April, 2014 as submitted by VIPL

Source Amount

(Rs. Crore)

Rupee Loan 2006.98

ECB 602.65 ($ 128.57 million)

Normative additional loan for meeting

the written down value of the Project

as on 1 April, 2014

234.51

Total Loan 2844.14

Equity 1218.92

Total Capital Cost 4063.05

MERC Order in Case No 91 of 2013 Page 30

4.4 Commission's Views on Prudence Check of Capital Cost

4.4.1 The Commission in order to undertake prudence check of capital cost of

Butibori Power Plant asked VIPL to submit the necessary information to

establish the reasonability of expected capital cost as on COD of the project.

While VIPL has submitted most of the information, some vital information

required for prudence check of capital cost could not be submitted by VIPL

as elaborated in the following paragraphs.

4.4.2 MERC MYT Regulations, 2011 specifies as under:

“38.4 A Generating Company may make a Petition for determination of

provisional tariff in advance of the anticipated Date of Commercial Operation

of Unit or Stage or Generating Station as a whole, as the case may be, based

on the capital expenditure actually incurred up to the date of making the

Petition or a date prior to making of the Petition, duly audited and certified by

the statutory auditors and the provisional tariff shall be charged from the date

of commercial operation of such Unit or Stage or Generating Station, as the

case may be.

38.5 A Generating Company shall make a fresh Petition in accordance with

these Regulations, for determination of final tariff based on actual capital

expenditure incurred up to the date of commercial operation of the Generating

Station duly certified by the statutory auditors based on Annual Audited

Accounts.

38.6 Any difference in provisional tariff and the final tariff determined by the

Commission and not attributable to the Generating Company may be adjusted

at the time of determination of final tariff for the following year as directed by

the Commission.”

4.4.3 VIPL in its Petition submitted that Unit # 1has achieved COD on 4 April,

2013 and Unit # 2 is envisaged to achieve COD by March, 2014. VIPL

submitted that land transfer process/possession of SICOM/railway land for

completion of railway siding expected in the month of November, 2013, the

expected schedule for completion of Railway siding is by February, 2014.

VIPL submitted the detailed activity schedule for railway siding.

MERC Order in Case No 91 of 2013 Page 31

4.4.4 As Unit # 1 has already achieved COD, it would be prudent to assess the

reasonability of expected capital cost based on the audited capital cost as on

COD of Unit # 1 and projected capital expenditure up to COD of Unit # 2.

4.4.5 VIPL submitted the audited accounts for FY 2012-13 and CA certificate for

capital expenditure till 31 May, 2013. As Unit # 1 has achieved COD on 4

April, 2013, the Commission observes that the audited accounts for FY 2012-

13 depict majority of the cost under CWIP. The CA certificate submitted

depicts only the capital expenditure incurred till 31 May, 2013.

4.4.6 The Commission asked VIPL to submit the revised Form 3.1 showing the

details of audited capital cost as on COD of Unit # 1 i.e., 4 April, 2013 and

projected capital cost up to COD of the project. VIPL replied that out of the

two Units of Butibori Power Plant, only one Unit has achieved COD. VIPL

submitted that the required information would be submitted after the COD of

the project. VIPL submitted that the capital expenditure is reflected in the

auditor certified statement that has already been submitted.

4.4.7 Further, IDC of Rs. 449.54 Crore submitted by VIPL is only up to 31 May,

2013. As Unit # 2 is yet to achieve COD, the IDC for the project is subject to

change. VIPL also submitted Rs. 78.52 Crore towards realised exchange rate

variation on settlement of Buyer’s Credit. VIPL submitted that this is subject

to change as the same does not include unrealised exchange rate differences

on foreign currency loan. The Commission also asked VIPL to submit the

details of cost towards foreign exchange rate variation separately for Unit # 1

and Unit # 2. VIPL submitted that it could not submit the required information

as the financing has been arranged for the entire project and the Unit wise

allocation could not be submitted.

4.4.8 VIPL submitted the written down value of capital cost as on 1 April, 2014.

The Commission asked VIPL to submit the computation of depreciation

considered for FY 2013-14 for arriving at the written down value of capital

cost as on 1 April, 2014. VIPL submitted the computations of depreciation for

FY 2013-14. The Commission observed that for computing the depreciation of

Unit # 1 for FY 2013-14, VIPL has considered only the Hard Cost without

allocating the pre-operative expenses and IDC expenses separately for Unit #

1 and Unit # 2.

MERC Order in Case No 91 of 2013 Page 32

4.4.9 VIPL in its Petition submitted that the capital cost does not include any

unrealized exchange rate differences on foreign currency loan and liability and

the same shall be submitted to the Commission post COD of the station along

with audited accounts at the time of final determination of Tariff. VIPL

submitted that it would submit the final capital cost including IDC and other

breakup post COD of the station along with audited accounts at the time of

final determination of Tariff.

4.4.10 The Commission has taken the submissions of VIPL on record. However, the

Commission is of the view that at this stage, any attempt to approve the

Capital Cost by carrying out the prudence check based on limited information

will not serve any purpose as the some components of cost are likely to

undergo change up to COD of the Project as submitted by VIPL in its Petition.

As regards the details of audited Capital Cost as on COD of Unit # 1 and

projected Capital cost in Form 3.1, VIPL submitted that the required

information would be submitted after the COD of the project.

4.4.11 The Commission in its previous Orders on approval of Capital Cost has

carried out the detailed prudence check by analysing the reasons for variation

in Actual Capital Cost as on COD with respect to original estimated cost.

VIPL in its Petition has included the IDC only up to May 2013 as part of

Capital Cost, though the project is yet to achieve COD. Therefore, the

variation in capital cost till COD of the Project will also undergo change and it

will be more appropriate to analyse the reasons for variation in actual Capital

Cost with respect to original estimated capital cost. Further, to arrive at

Written Down Value of the Project as on April 1, 2014, another crucial aspect

is the depreciation to be considered for FY 2013-14 from COD of Unit 1 for

Unit 1 and from COD of Unit 2 for Unit 2. As discussed earlier, the

Commission also observed that for computing the depreciation of Unit # 1 for

FY 2013-14, VIPL has considered only the Hard Cost without allocating the

pre-operative expenses and IDC expenses separately for Unit # 1 and Unit # 2.

4.4.12 Hence, the Commission is of the view any approval of capital cost at this

stage will be based on limited prudence and based on certain

assumptions, which will undergo change based on actual capital cost till

COD of the Project. Hence, the Commission is not approving the capital

cost of Butibori Power Plant in this Order. The Commission shall

approve the capital cost of the project after carrying out the prudence

check of the capital cost while determining the final Tariff in accordance

MERC Order in Case No 91 of 2013 Page 33

with Regulation 38.5 of MERC MYT Regulations, 2011 based on audited

capital cost as on COD.

4.5 MEANS OF FINANCE

4.5.1 VIPL submitted that the envisaged capital expenditure of Rs. 4132.36 Crore as

on COD of the project would be financed at debt equity ratio of 70:30. VIPL

submitted that the requisite debt is funded by a consortium of banks led by

Axis Bank. VIPL submitted that additionally, during the construction period, it

has taken Buyer’s Credit for part funding of foreign equipment supply, which

has an interest rate of 3.5%. VIPL submitted that Buyer’s Credit of US $97.63

million would be converted into domestic loan post COD of the Power Plant.

VIPL submitted that it would infuse Rs. 1239.71 Crore as equity contribution

towards completion of the Butibori project.

4.5.2 VIPL submitted the details of financing arrangement as shown in the Table

below:

Table 4.11: Debt and Equity as on COD of the project as submitted by VIPL

Means of finance Amount

( Rs. Crore) %

Domestic Loan 2193.16 53.07%

ECB ( USD 150 Million) 699.49 16.93%

Equity 1239.71 30.00%

Total 4132.36 100.00%

4.5.3 The Commission observed that VIPL submitted an additional loan of Rs.

145.21 Crore in the details of financial package. The Commission asked VIPL

to submit the details regarding this additional loan. VIPL submitted that there

had been certain repayments envisaged for the actual portfolio of loans and

hence normative loans have been considered to maintain debt equity ratio of

70:30. VIPL submitted that for financing the additional loan, it had already

approached Banks and Financial Institutions. VIPL submitted the expected

terms and conditions of additional loan as shown in the Table below:

MERC Order in Case No 91 of 2013 Page 34

Table 4.12: Terms and Conditions of additional loan as submitted by VIPL

Particulars Terms and Conditions of

additional loan

Loan amount Rs. 145.21 Crore

Nature Rupee Term Loan

Source Banks and Financial Institutions

Interest Rate 13.75%

Duration 15 years

Moratorium period 1 year

Repayment 56 equal quarterly instalments

4.5.4 VIPL submitted that the financing for the project has been arranged in the

form of Rupee Term loan, ECB loan and Buyer’s Credit. The Commission

asked VIPL to submit the statement of loan disbursement and corresponding

assets purchased. VIPL submitted the statement of loan disbursement of

Rupee Term loan, ECB loan and Buyer’s Credit. VIPL submitted that the

Buyer’s Credit has been arranged for financing of specific assets and

submitted the details of the same. VIPL submitted that the balance assets have

been financed by a mix of Rupee Term loan and ECB loan. VIPL submitted

that it would not be possible to provide a statement showing date wise

disbursement of Rupee Term loan and the corresponding assets purchased.

4.5.5 The Commission also asked VIPL to submit the basis of exchange rate

considered for converting the foreign currency loan amounts to Rupees. VIPL

submitted the exchange rates considered for conversion of foreign currency

loan amounts to Rupees. VIPL has not submitted the basis of exchange rates

considered for converting the foreign currency loan amounts to Rupees.

4.6 PROVISIONAL TARIFF

ANNUAL FIXED CHARGES

4.6.1 As discussed in Section 4.4, as the Commission has not approved the Capital

Cost of the Project in this Order, the Commission has not analysed the various

components of Annual Fixed Charges in this Order. The submissions of VIPL

towards provisional Annual Fixed Charges and the approach adopted by the

Commission for approving the provisional Annual Fixed Charges is discussed

in subsequent paragraphs.

MERC Order in Case No 91 of 2013 Page 35

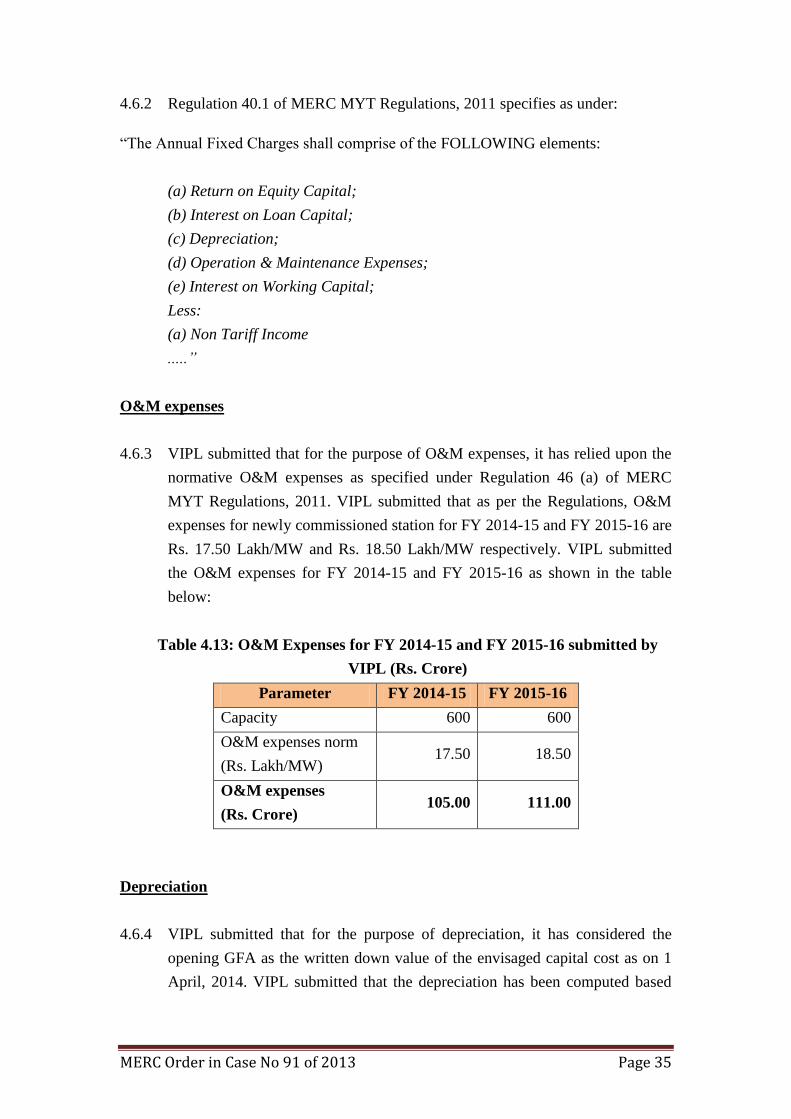

4.6.2 Regulation 40.1 of MERC MYT Regulations, 2011 specifies as under:

“The Annual Fixed Charges shall comprise of the FOLLOWING elements:

(a) Return on Equity Capital;

(b) Interest on Loan Capital;

(c) Depreciation;

(d) Operation & Maintenance Expenses;

(e) Interest on Working Capital;

Less:

(a) Non Tariff Income

.....”

O&M expenses

4.6.3 VIPL submitted that for the purpose of O&M expenses, it has relied upon the

normative O&M expenses as specified under Regulation 46 (a) of MERC

MYT Regulations, 2011. VIPL submitted that as per the Regulations, O&M

expenses for newly commissioned station for FY 2014-15 and FY 2015-16 are

Rs. 17.50 Lakh/MW and Rs. 18.50 Lakh/MW respectively. VIPL submitted

the O&M expenses for FY 2014-15 and FY 2015-16 as shown in the table

below:

Table 4.13: O&M Expenses for FY 2014-15 and FY 2015-16 submitted by

VIPL (Rs. Crore)

Parameter FY 2014-15 FY 2015-16

Capacity 600 600

O&M expenses norm

(Rs. Lakh/MW) 17.50 18.50

O&M expenses

(Rs. Crore) 105.00 111.00

Depreciation

4.6.4 VIPL submitted that for the purpose of depreciation, it has considered the

opening GFA as the written down value of the envisaged capital cost as on 1

April, 2014. VIPL submitted that the depreciation has been computed based

MERC Order in Case No 91 of 2013 Page 36

on the rates prescribed in MERC MYT Regulations, 2011. VIPL submitted the

depreciation for FY 2014-15 and FY 2015-16 as shown in the table below:

Table 4.14: Depreciation for FY 2014-15 and FY 2015-16 submitted by VIPL

(Rs. Crore)

Asset

Classification

Capital

Cost as on

COD of the

project

Written down

value of the

capital cost as

on 1 April, 2014

Depreciation

Rate (%)

Depreciation

FY 2014-15 FY 2015-16

Land owned under

full title 73.29 73.29 0.00% - -

Land under lease 37.79 37.79 3.34% 1.26 1.26

Building 2.06 2.06 3.34% 0.07 0.07

Cooling Towers &

CWS 114.91 112.30 5.28% 6.07 6.07

Hydraulic works - - 5.28% - -

Plant & Machinery 3378.05 3312.59 5.28% 178.36 178.36

Batteries 16.50 16.23 5.28% 0.87 0.87

Air conditioning 19.81 19.76 5.28% 1.05 1.05

Overhead Lines,

cables & networks 75.57 74.66 5.28% 3.99 3.99

Vehicles 0.17 0.17 9.50% 0.02 0.02

Furniture & fixtures 1.16 1.16 6.33% 0.07 0.07

Office equipment 1.93 1.93 6.33% 0.12 0.12

Civil works (Roads

and Railway

sidings)

411.11 411.11 3.34% 13.73 13.73

Total 4132.36 4063.05 205.61 205.61

4.6.5 The Commission observed that VIPL has arrived at the written down value of

capital cost as on 1 April, 2014 by deducting the depreciation for FY 2013-14

computed at the depreciation rates specified in MERC MYT Regulations,

2011. The Commission further observed that the VIPL has computed

depreciation only under some of the asset classes. In this regard, the

Commission asked VIPL to submit the computations of depreciation for FY

2013-14 to arrive at the written down value at the beginning of FY 2014-15.

VIPL submitted the computations of depreciation for FY 2013-14. The

Commission observed that for computing the depreciation of Unit # 1 for FY

MERC Order in Case No 91 of 2013 Page 37

2013-14, VIPL has considered only the Hard Cost without allocating the pre-

operative expenses and IDC expenses separately for Unit # 1 and Unit # 2.

Interest on loans

4.6.6 VIPL submitted that the total debt amount is raised from consortium of banks

through a mix of domestic (Rupee) loan and ECB. VIPL submitted that the

applicable interest rate post COD on domestic loan is is linked with the Axis

Bank Base Rate/Other Rupee Lenders’ base rate plus reset interest spread rate,

as applicable as per the terms of the loan agreement. VIPL submitted that the

domestic loan has repayment period of 11 years with quarterly repayment

frequency. VIPL submitted that ECB of US $ 150 Million is availed at interest

rate of 3 month LIBOR plus margin of 4.60%.

4.6.7 VIPL submitted that the project funding as on 1 April, 2014 is considered on a

normative basis as loan equal to 70 % of the written down value of capital cost

as on 1 April, 2014 and balance 30% as equity contribution for the purpose of

determination of Tariff. VIPL submitted that the rationale for the same is

based on the fact that the accounting principles always adopt a matching

concept of assets and liabilities. VIPL submitted that by considering the

written down value of capital cost as on 1 April, 2014, there has to be a

matching liability for considering the funding of these assets. VIPL submitted

that, to the extent, the value of the assets has been brought down under the

regulatory purview, the same needs to be considered to be funded in a

normative manner. VIPL submitted that since deployment of 30% equity has

already been envisaged in the project, the balance quantum has to be

considered to be funded through loan component in line with Regulation 30.1

of MERC MYT Regulations, 2011.

4.6.8 VIPL submitted that even otherwise, repayments and interest expenses being

incurred by it prior to COD of Unit # 2 will have to be met by internal accruals

or drawal of additional loans. VIPL submitted that since 30% of ceiling on

equity has already been considered as per Tariff Regulations, such additional

amount of deployment of funds needs to be considered as normative loan only.

VIPL submitted that the loan portfolio has been considered for the project as a

whole and it is not possible to segregate the loan portfolio for the two Units.

4.6.9 VIPL submitted that the Tariff Regulations permits variation between actual

loan portfolios as per books of accounts vis-a-vis the loan amount as per

MERC Order in Case No 91 of 2013 Page 38

regulatory accounts. VIPL submitted that in consideration of the aforesaid

provision in the Regulations, it has considered the matching principle and has

considered normative loans for funding the written down value of the capital

cost.

4.6.10 VIPL submitted that interest claimed as part of ARR is calculated in line with

the MERC MYT Regulations, 2011. VIPL submitted that the repayment for

FY 2014-15 and FY 2015-16 is assumed to be equal to the depreciation for the

respective years. VIPL submitted that the interest rate applied on normative

loan amount is calculated as weighted average of interest on basis of actual

loan portfolio at the beginning of the year. VIPL submitted the actual loan

portfolio as shown in the Table below:

Table 4.15: Actual Loan portfolio submitted by VIPL

Particulars Units FY 2014-15 FY 2015-16

Actual Domestic Loan

Opening domestic loan Rs. Crore 2006.98 1807.60

Repayment Rs. Crore 199.38 199.38

Closing domestic loan Rs. Crore 1807.60 1608.22

Interest rate on domestic loan % 13.75% 13.75%

Actual ECB

Opening ECB outstanding Rs. Crore 602.65 502.21

Repayment Rs. Crore 100.44 100.44

Closing ECB outstanding Rs. Crore 502.21 401.77

Interest rate on ECB % 5% 5%

Weighted average Interest Rate % 11.73% 11.85%

4.6.11 VIPL submitted the interest expenses for FY 2014-15 and FY 2015-16 as

shown in the Table below:

Table 4.16: Interest expenses for FY 2014-15 and FY 2015-16 submitted by

VIPL (Rs. Crore)

Particulars FY 2014-15 FY 2015-16

Opening Loan 2844.14 2638.53

Repayment 205.61 205.61

Closing loan 2638.53 2432.92

Weighted average interest rate 11.73% 11.85%

Interest 321.54 300.42

MERC Order in Case No 91 of 2013 Page 39

Removal of difficulty in treatment of cost of hedging foreign loans and/or

allowing the foreign exchange rate variation

4.6.12 VIPL submitted that it has taken a USD denominated loan for the project to

save on the interest costs in the long-term. VIPL submitted that the same is

exposed to exchange rate fluctuations. VIPL submitted that the benefit of

lower interest rate is transparently passed on in interest calculations in Tariff.

VIPL submitted that the hedging costs can be prohibitively high in a volatile

exchange rate scenario and is expected to be about 8% p.a. VIPL submitted

that currently Indian Rupee is going through this phase. VIPL submitted that

with active efforts by the Government to regain the reform momentum, the

economy is expected to bounce back to high growth trajectory in the medium-

term. VIPL submitted that a stronger economy with healthy foreign exchange

reserves is expected to strengthen Indian Rupee vis-à-vis US Dollars and other

hard currencies in the medium term. VIPL submitted that appreciation of

Rupee vis-à-vis USD would reduce the debt servicing obligations on its

foreign currency loans.

4.6.13 VIPL submitted that MERC MYT Regulations, 2011 do not explicitly cover

the treatment of such foreign exchange rate variations post the commissioning

of the project. VIPL submitted that currently no hedging of these foreign loans

is considered. VIPL submitted that a directive in this regard regarding whether

the actual cost can be passed through Tariff or else if such transactions are to

be hedged in future then the actual cost of hedging shall be passed through

Tariff may be issued by the Commission. VIPL submitted that Regulation 40

of CERC Tariff Regulations, 2009 allow for recognition of hedging cost and

extra Rupee liability towards foreign currency loan.

4.6.14 The Commission asked VIPL to submit the details of proposed hedging

arrangements for foreign currency loans.