memory trends and implications for lithography...

TRANSCRIPT

©2015 Micron Technology, Inc.1

Linda K. Somerville, Ardavan Niroomand, Pierre Fazan

Memory Trends and

Implications for Lithography

and DSA Technology

©2015 Micron Technology, Inc.2

Agenda

About Micron & Memory Market

Patterning with DSA: Challenges and Opportunities

Trends and Challenges in Memory Innovation

1

2

3

©2015 Micron Technology, Inc.3

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

FY-95 FY-96 FY-97 FY-98 FY-99 FY-00 FY-01 FY-02 FY-03 FY-04 FY-05 FY-06 FY-07 FY-08 FY-09 FY-10 FY-11 FY-12 FY-13 FY-14

$M

Micron acquires TI’s

memory operations

Micron acquires Toshiba’s commodity

DRAM operations

Micron and Intel

form IMFT

Micron acquires

Lexar Media

Micron and Intel form IMFS

Micron and Nanya form DRAM Joint

venture

Micron acquires Numonyx

IMFT & IMFS restructuring

Inotera JV restructure

Micron acquires Elpida and Rexchip

Micron’s Historical Performance and Revenue

20-years of Growth…and we believe strongly in the future

©2015 Micron Technology, Inc.4

Micron Around the WorldManufacturing

FAB 15

Japan

FAB 11

TaiwanFAB 16

Taiwan

FAB 10

Singapore19%

FAB 13

66%

34%

FAB 2Lehi FAB 6

Virginia

DRAMNANDNOR

©2015 Micron Technology, Inc.5

R&D Around the World“One R&D Team”

Milpitas & Folsom, CA:

Emerging memory design,

product engineering

Boise, ID: NAND,

emerging memory, DRAM,

package R&D, mask

technology

United States Japan Singapore

Italy India Belgium

Hiroshima: DRAM

Hashimoto: Emerging

memory design, product

engineering, package

R&D, NAND device

Akita: Package R&D

Singapore: NAND,

STTRAM, package R&D

Vimercate: Emerging

memory, NAND

Bangalore: Live die and

test structure design/

layout, device analysis

Leuven: IMEC core partner

program

©2015 Micron Technology, Inc.6

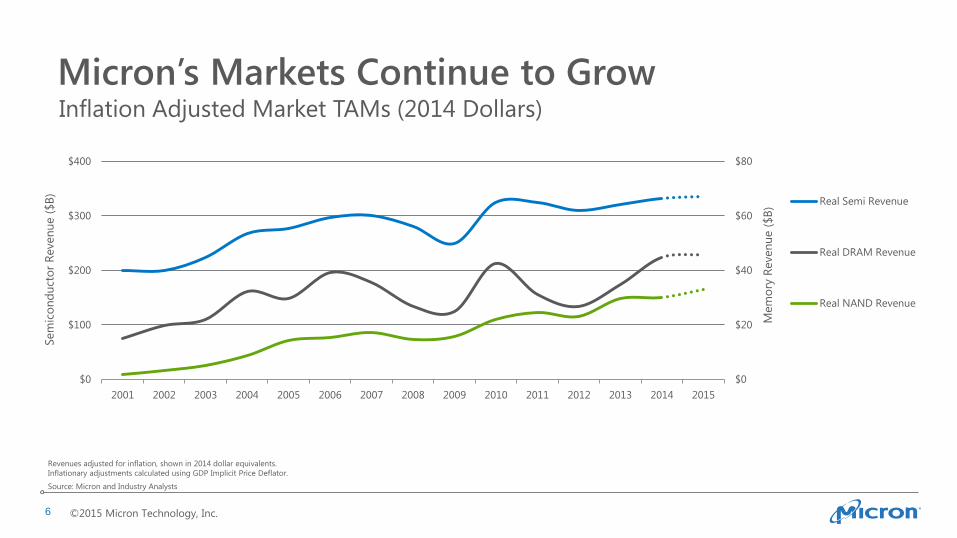

Micron’s Markets Continue to Grow

$0

$20

$40

$60

$80

$0

$100

$200

$300

$400

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Mem

ory

Reven

ue (

$B

)

Sem

ico

nd

uct

or

Reven

ue (

$B

)

Real Semi Revenue

Real DRAM Revenue

Real NAND Revenue

Inflation Adjusted Market TAMs (2014 Dollars)

Source: Micron and Industry Analysts

Revenues adjusted for inflation, shown in 2014 dollar equivalents.

Inflationary adjustments calculated using GDP Implicit Price Deflator.

©2015 Micron Technology, Inc.7

0

20

40

60

80

100

120

140

160

2015 2016 2017 2018 2019

DRAM Industry Bit Demand (B Gb EU)

Growing and Diversifying Memory Demand

Tablet

PC

Handset

AIMM

Consumer &

Graphics

Server/Storage/

Networking

Tablets contain a mix of mobile DRAM, standard DRAM, and reduced-power solutions. Upgrade modules included with PC.Source: Micron and Industry Analysts

0

50

100

150

200

250

300

350

2015 2016 2017 2018 2019

NAND Industry Bit Demand (B GB EU)

Tablet

Enterprise

SSD

Other

Removable

Storage

Handset

Client SSD

Consumer

Datacenter

SSD

©2015 Micron Technology, Inc.8

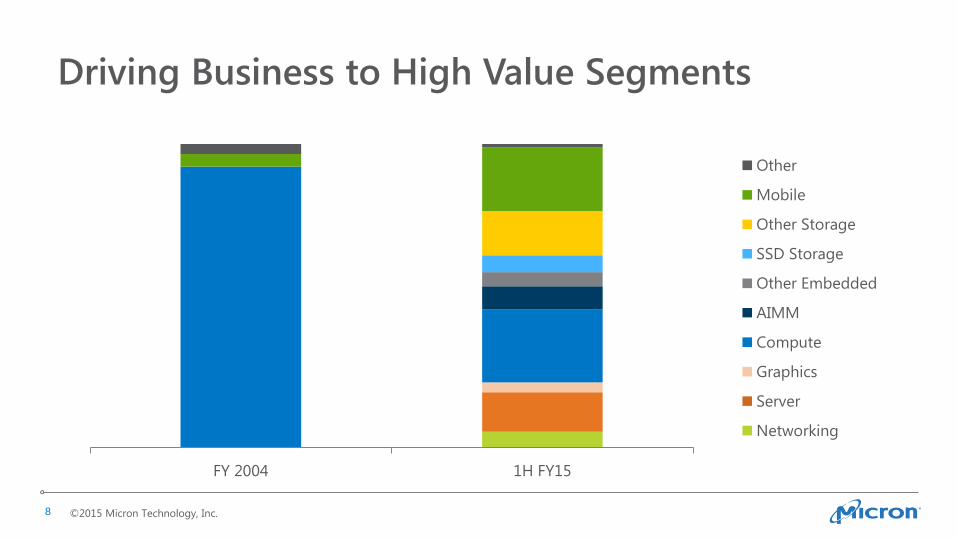

Driving Business to High Value Segments

Micron acquires Toshiba’s

commodity DRAM

operations

FY 2004 1H FY15

Other

Mobile

Other Storage

SSD Storage

Other Embedded

AIMM

Compute

Graphics

Server

Networking

©2015 Micron Technology, Inc.9

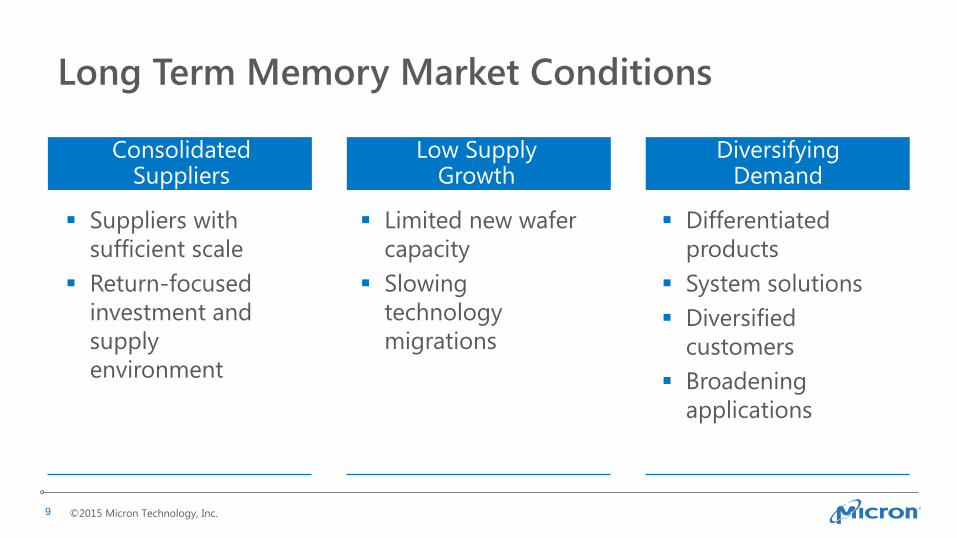

Long Term Memory Market Conditions

Suppliers with

sufficient scale

Return-focused

investment and

supply

environment

Limited new wafer

capacity

Slowing

technology

migrations

ConsolidatedSuppliers

Low Supply Growth

Differentiated

products

System solutions

Diversified

customers

Broadening

applications

DiversifyingDemand

©2015 Micron Technology, Inc.10

Trends and Challenges in Memory Innovation

©2015 Micron Technology, Inc.11

Micron’s Portfolio of Innovative “Firsts”DRAM 6F2 architecture

Leading DRAM capacitor technology

Copper metallization

Packaging (3Di) Hybrid memory cube, Through Silicon Via (TSV)

0.8mm four-layer LPDRAM package

NAND Pitch multiplication patterning

Award-winning, industry-leading

planar NAND cell technology

New Memory Productization of phase change memory

Demonstration of 16Gb resistive RAM

Development of 3D XPoint memory

©2015 Micron Technology, Inc.12

DRAM NAND New Memory Package

Edge yield improvements – continuous yield improvement

Ramp execution – new tool installs and matching, cost of transition

Process equipment maturity improvement: uniformity, capability

Defect detection and reduction

Development of new in-line characterization techniques to prevent

excursion, improve quality and yield

Development of

baseline 3Di

technology

Development of

first 3Di products

Challenges Faced in Technology Development

Continuous innovation in core process technology capability

©2015 Micron Technology, Inc.13

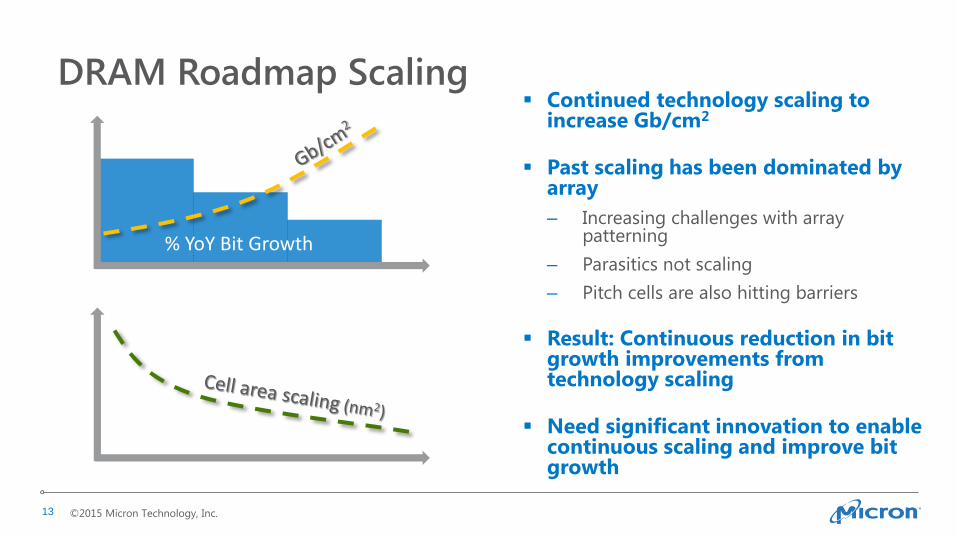

DRAM Roadmap Scaling Continued technology scaling to

increase Gb/cm2

Past scaling has been dominated by array

– Increasing challenges with array patterning

– Parasitics not scaling

– Pitch cells are also hitting barriers

Result: Continuous reduction in bit growth improvements from technology scaling

Need significant innovation to enable continuous scaling and improve bit growth

% YoY Bit Growth

©2015 Micron Technology, Inc.14

DRAM Scaling ChallengesARRAY (bottom of containers)

Cell Contact

Technology Node

Wtotal 6~7nm

Materials development required to improve array

efficiency and word line/bit line resistance

Capacitor structure

• Paradigm shift may be needed for cost effective scaling

Bit line and Word line

• Materials innovation required

Advanced device engineering

• To address materials/process limitations

Overlay and patterning demands

• May drive EUV adoption

Gap fill of narrow structures

• Need low T solutions

Advanced characterization

• HAR measurements, OCD

©2015 Micron Technology, Inc.15

NAND Roadmap Scaling

Planar NAND scaling

Planar NAND can still be scaled below 16nm, but performance & cost are not competitive with 3D

3D NAND scaling

3D NAND cost improvement over planar expands with subsequent nodes

3D cell architecture enables significant performance improvement relative to planar technology

25nm 20nm 16nm 1Znm 1Z'nm

32-tier TLC

48-tier TLC

64-tier TLC

96-tier TLC

GB

/cm

2

Technology Node

34nm

25nm

20nm 16nm 1Znm 1Z'nm

MU 32-tier MLC 32-tier TLC

48-tier TLC64-tier TLC

96-tier TLC

Co

st/G

B

Technology Node

3D NAND

3D NAND

PLANAR TLC

PLANAR TLC

Future Technology Projection

Future Cost Projection

©2015 Micron Technology, Inc.16

Vertical NAND Scaling Challenges

Tier Stack Scaling

High aspect ratio etch capability

Thin film deposition in high AR structures

Uniformity – WIW, WIF, WID, but also within localized high aspect

ratio structures

Advanced characterization – HAR measurements, OCD, embedded

defects and measurements

Staircase Contact Scaling

Advanced gap fill requirements for range of dimensions

Low temperature films deposition and treatment

Demanding Planarization

Thick film removal, new films, tighter uniformity specifications

©2015 Micron Technology, Inc.17

Packaging Technology Challenges

Development and deployment of baseline 3Di manufacturing processes

Transition from discrete-packaged memory to in-package memory

Thermal management of memory which shares a thermal solution with the ASIC or is inside the ASIC package

Control of warpage/coplanarity for ultra-thin dice used in ultra-thin packages

Accelerating development cycles, especially for market segments with short product life cycles

©2015 Micron Technology, Inc.18

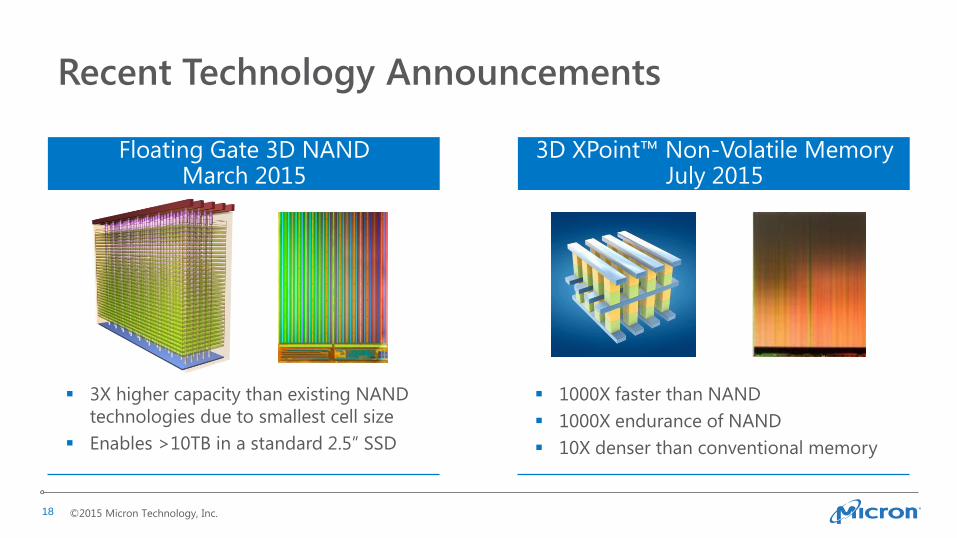

Recent Technology Announcements

3X higher capacity than existing NAND

technologies due to smallest cell size

Enables >10TB in a standard 2.5” SSD

1000X faster than NAND

1000X endurance of NAND

10X denser than conventional memory

Floating Gate 3D NAND March 2015

3D XPoint™ Non-Volatile MemoryJuly 2015

©2015 Micron Technology, Inc.19

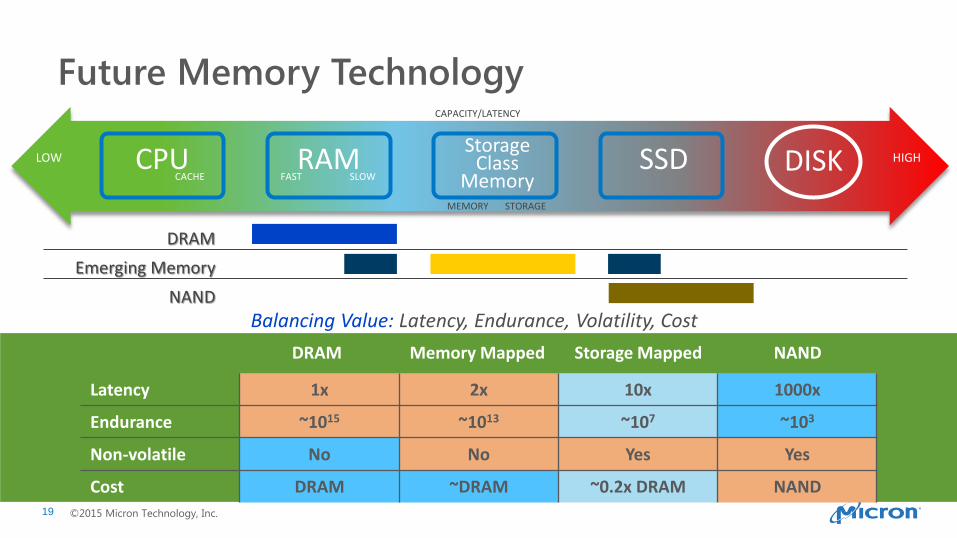

Future Memory Technology

DRAM

NAND

Balancing Value: Latency, Endurance, Volatility, Cost

Emerging Memory

LOW HIGHCPU RAM SSD DISKCACHE FAST SLOW

StorageClass

MemoryMEMORY STORAGE

Latency 1x 2x 10x 1000x

Endurance ~1015 ~1013 ~107 ~103

Non-volatile No No Yes Yes

Cost DRAM ~DRAM ~0.2x DRAM NAND

DRAM NANDMemory Mapped Storage Mapped

CAPACITY/LATENCY

©2015 Micron Technology, Inc.20

Polymers NanotubesNanowiresMagnetics

The Search for Successful New Memory Technology

It’s a great time to be a materials engineer!

W, TiN etc,.

Cu, Ag etc,.

+V -V Top lead

Free layer

Barrier

Fixed Layer

Antiferromagnet

Bottom lead

Cu/Ta

CoFeB

MgO

CoFeB

PtMn

Cu/Ta

MTJ

MTJ

Explosion of new memory concepts

Investigation focused on unique material

systems and product development

STT MRAMRRAM

PCM FeRAM

+

©2015 Micron Technology, Inc.21

Patterning with DSA: Challenges and Opportunities

©2015 Micron Technology, Inc.22

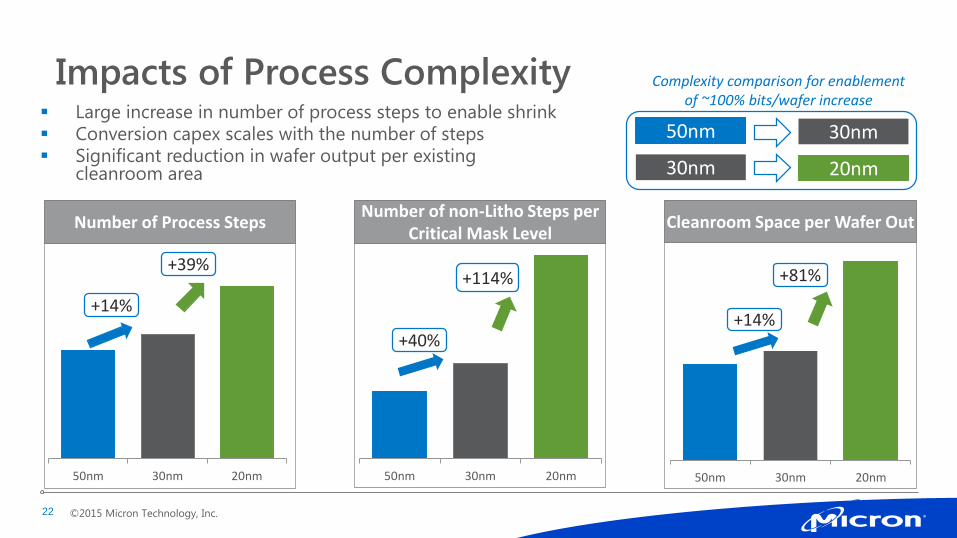

50nm 30nm 20nm

Impacts of Process Complexity Large increase in number of process steps to enable shrink

Conversion capex scales with the number of steps Significant reduction in wafer output per existing

cleanroom area

Number of Process Steps Cleanroom Space per Wafer Out

50nm 30nm 20nm

+14%

+39%

+14%

+81%

50nm 30nm 20nm

Number of non-Litho Steps per Critical Mask Level

+40%

+114%

Complexity comparison for enablementof ~100% bits/wafer increase

50nm

30nm

30nm

20nm

©2015 Micron Technology, Inc.23

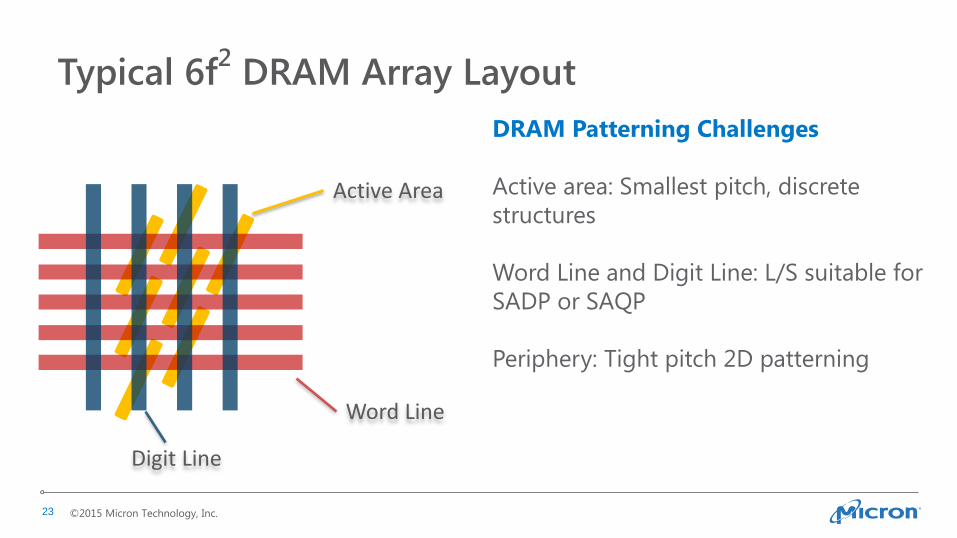

Active Area

Typical 6f2

DRAM Array Layout

Word Line

Digit Line

DRAM Patterning Challenges

Active area: Smallest pitch, discrete

structures

Word Line and Digit Line: L/S suitable for

SADP or SAQP

Periphery: Tight pitch 2D patterning

©2015 Micron Technology, Inc.24

Active Area Patterning

Dense lines are initially formed

by SADP or SAQP

Lines are then chopped to create

islands

Contact chop pattern

1Ynm – 1Znm LELE

Beyond 1Znm, EUV

Option (1Znm and beyond)

High NA, EUV, single print

DSA has an opportunity to

replace SAQP for dense line

patterning, when ready and

cost competitive

©2015 Micron Technology, Inc.25

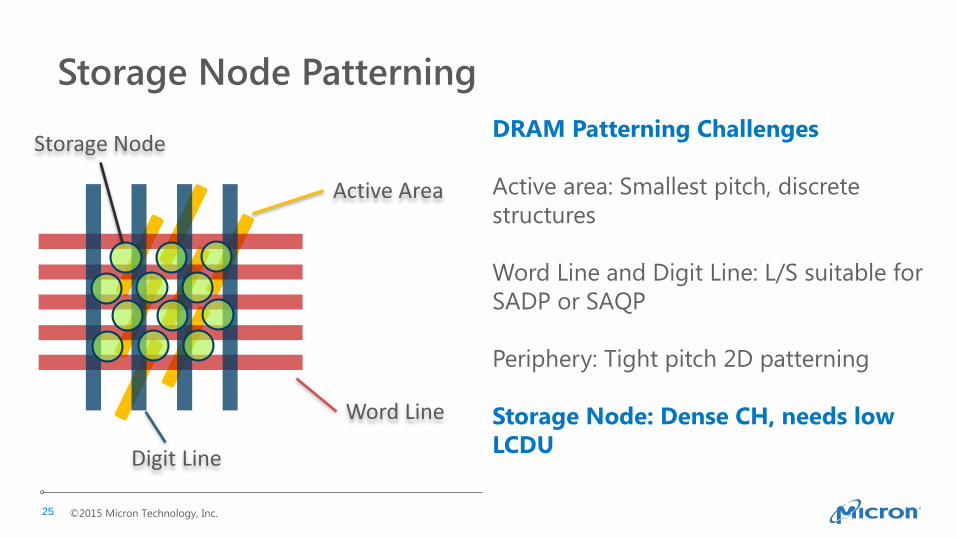

Active Area

Storage Node Patterning

Word Line

Digit Line

Storage NodeDRAM Patterning Challenges

Active area: Smallest pitch, discrete

structures

Word Line and Digit Line: L/S suitable for

SADP or SAQP

Periphery: Tight pitch 2D patterning

Storage Node: Dense CH, needs low

LCDU

©2015 Micron Technology, Inc.26

Storage Node Patterning

Main challenge is local

CD uniformity

CD uniformity needs

improvement for

single patterning

Potential path but need

to address LCDU,

defects, placement error

ArF Immersion EUV DSA CHIPS Flow

©2015 Micron Technology, Inc.27

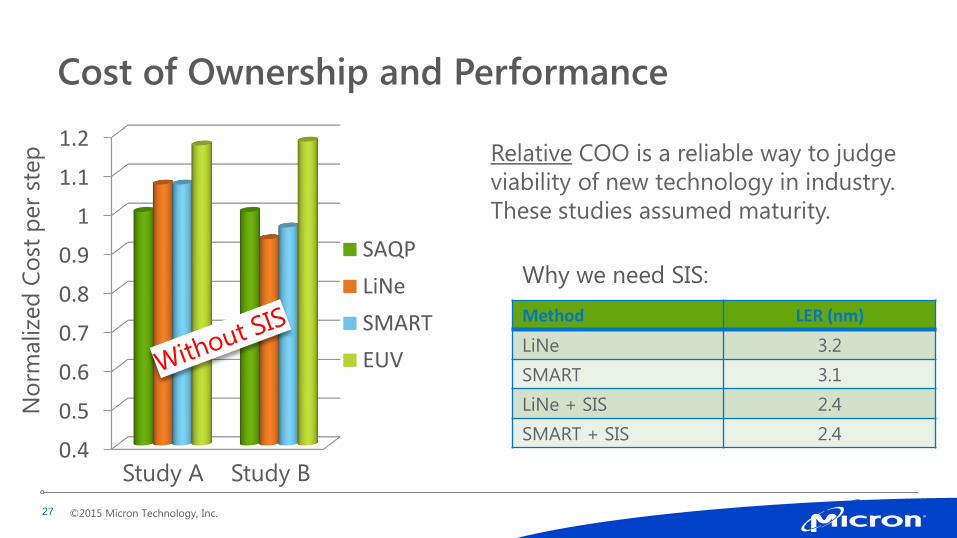

Cost of Ownership and Performance

0.4

0.5

0.6

0.7

0.8

0.9

1

1.1

1.2

SAQP

LiNe

SMART

EUV

Method LER (nm)

LiNe 3.2

SMART 3.1

LiNe + SIS 2.4

SMART + SIS 2.4

No

rmalize

d C

ost

per

step

Study A Study B

Why we need SIS:

Relative COO is a reliable way to judge

viability of new technology in industry.

These studies assumed maturity.

©2015 Micron Technology, Inc.28

DSA Adoption Challenges

Defectivity

Needs to improve by a few orders of magnitude

Pattern roughness

Needs to be comparable or better than SAQP

SIS and other post processing may help, but add cost, complexity and potentially

defectivity

Process/Integration complexity

Pattern placement error and overlay issues need to be further studied

Integration issues such as termination, edge of array, etch, alignment and overlay

marks

Cost

Cost advantage over SAQP needs to be significant

©2015 Micron Technology, Inc.29

Highlights

Exciting time for memory: diversifying markets, new applications

Lots of challenges ahead in both silicon processing and package development

Winning patterning technologies have to win for performance and cost

Trend is 3D and materials innovation

1

2

3

4

©2015 Micron Technology, Inc.30

Thank You

©2015 Micron Technology, Inc.31