megan williams associate economist, oklahoma city branch...associate economist, oklahoma city branch...

TRANSCRIPT

Megan Williams

Associate Economist, Oklahoma City Branch

Federal Reserve Bank of Kansas City

www.kansascityfed.org/oklahomacity

• The “Fed” consists of three main entities:

• Board of Governors: 7 members appointed by U.S. President

• Federal Reserve Banks: 12 total; semi-independent by design

• Federal Open Market Committee: 19 members; 12 voting

• As with most central banks, the Fed’s primary

responsibilities fall within four general areas:

• Lender of last resort – provide liquidity in times of crisis

• Monetary policy – promote full employment and low inflation

• Bank regulation – ensure safety and soundness of banks

• Financial services – bank for banks, bank for federal govt.

Overview of the

Federal Reserve System

Federal Reserve Districts

and Office Locations

• History, staff, and functions

• Branch office opened in 1920; currently have about 35 staff

• Functions include economic research, bank examinations, public outreach

• 2011 branch board of directors

• Steve Agee (chairman), Dean, Oklahoma City Univ. Business School, OKC

• Jim Dunn, Chairman, Mill Creek Lumber and Supply Co., Tulsa

• Jacque Fiegel, Senior EVP and COO, Coppermark Bank, OKC

• Rose Washington Rentie, Executive Director, TEDC Creative Capital, Tulsa

• Doug Tippens, President and CEO, Bank of Commerce, Yukon

• K. Vasudevan, Chairman, Service and Technology Corp., Bartlesville

The Oklahoma City Branch of the

Federal Reserve Bank of Kansas City

The U.S.

Economy

-10

-8

-6

-4

-2

0

2

4

6

2006 Q3 2007 Q3 2008 Q3 2009 Q3 2010 Q3 2011 Q3

Real GDP growth picked up somewhat

in Q3, but still remains moderate

U.S. Real Gross Domestic Product

Percent change from the previous period, SAAR

Source: U.S. Bureau of Economic Analysis, FOMC

1.3 0.7

4.2

10.3

3.6

-0.9

1.8 1.7 1.3

15.7

4.7

-0.1

-2

0

2

4

6

8

10

12

14

16

18

Total GDP Consumer spending

Residential investment

Business investment

Exports Government spending

2011 Q2

2011 Q3

Growth in Components of Real GDP

Percent change from the previous period, SAAR

Source: U.S. Bureau of Economic Analysis

Business investment was strong, exports

grew further, and consumers spent more

25

30

35

40

45

50

55

60

65

-1000

-800

-600

-400

-200

0

200

400

600

Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11

Private Employment (left axis)

ISM Manufacturing Index (right axis)

ISM Non-Manufacturing Index (right axis)

Change from previous month, thousands

Source: Institute for Supply Management, Bureau of Labor Statistics

U.S. Private Payroll Employment and Business Indexes

Recent U.S. data have improved slightly

overall, but growth still remains moderate

Index

The unemployment rate eased further in

December, but joblessness remains high

U.S. Unemployment Rate and Employment-to-Population

Source: U.S. Bureau of Labor Statistics

Percent

58

59

60

61

62

63

64

0

2

4

6

8

10

12

Dec-01 Dec-02 Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11

Unemployment Rate

(left axis)

Employment-to-

Population (right axis)

-8

-6

-4

-2

0

2

4

6

8

-8

-6

-4

-2

0

2

4

6

8

Nov-01 Nov-02 Nov-03 Nov-04 Nov-05 Nov-06 Nov-07 Nov-08 Nov-09 Nov-10 Nov-11

Overall CPI

Core CPI

Overall inflation eased considerably in late

2011, and core prices also edged lower

U.S. CPI Index

Source: U.S. Bureau of Labor Statistics

Percent change, six-months annualized

Financial stress continues to rise

in Europe, and also beyond

3-month EURIBOR & LIBOR Spreads (to OIS)

Source: Bloomberg

Percentage points

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

LIBOR

EURIBOR

December 11, 2011 FOMC Statement

“To support a stronger economic recovery and to help ensure that

inflation, over time, is at levels consistent with the dual mandate,

the Committee decided today to continue its program to

extend the average maturity of its holdings of securities as

announced in September…

“The Committee is maintaining its existing policies of reinvesting

principal payments from its holdings of agency debt and

agency mortgage-backed securities in agency mortgage-

backed securities and of rolling over maturing Treasury

securities at auction… The Committee also decided to keep

the target range for the federal funds rate at 0 to 1/4 percent

and currently anticipates that economic conditions--including low

rates of resource utilization and a subdued outlook for inflation over

the medium run--are likely to warrant exceptionally low levels for

the federal funds rate at least through mid-2013…

“Voting against the action was Charles L. Evans, who supported

additional policy accommodation at this time.”

The Oklahoma

Economy

Source: U.S. Bureau of Labor Statistics

Employment Growth, Year-over-Year (percent) November 2011

There is considerable variation in

economic strength across the nation

92

94

96

98

100

102

92

94

96

98

100

102

Jan-08 Jan-09 Jan-10 Jan-11

Index: Jan-08=100

Source: U.S. Bureau of Labor Statistics

Level of Payroll Employment

OK employment remains below pre-recession

levels, but much less so than in the U.S.

OK

U.S.

Percent change year-over-year

Source: Bureau of Labor Statistics

Employment Growth November 2011

Most Oklahoma sectors have grown solidly

in 2011, led by energy and manufacturing

-4

-2

0

2

4

6

8

10

12

14

Total Energy Mfg Const Leis & Hosp

Prof & Bus Svcs

Educ & Health

Trade, Transp.

& Utilities

Finance State & Local Govt

Info

U.S.

OK

0.5 0.6

-0.2

0.7

1.2

3.1

2.5 2.7

-1

-1

0

1

1

2

2

3

3

4

U.S. OKC Metro

Tulsa Metro

Rest of State

Nov-10

Nov-11

Percent

Source: U.S. Bureau of Labor Statistics

Employment Growth Year-over-year

Recent job growth has been especially

strong in OKC and solid in other areas

Unemployment Rate Seasonally Adjusted

Percent

Source: Bureau of Labor Statistics

Yet unemployment in the state has risen, as

discouraged workers resume job hunting

0

2

4

6

8

10

12

0

2

4

6

8

10

12

Nov-06 Nov-07 Nov-08 Nov-09 Nov-10 Nov-11

OK

U.S.

May: 5.3%

November: 6.1%

Percent

Source: BEA

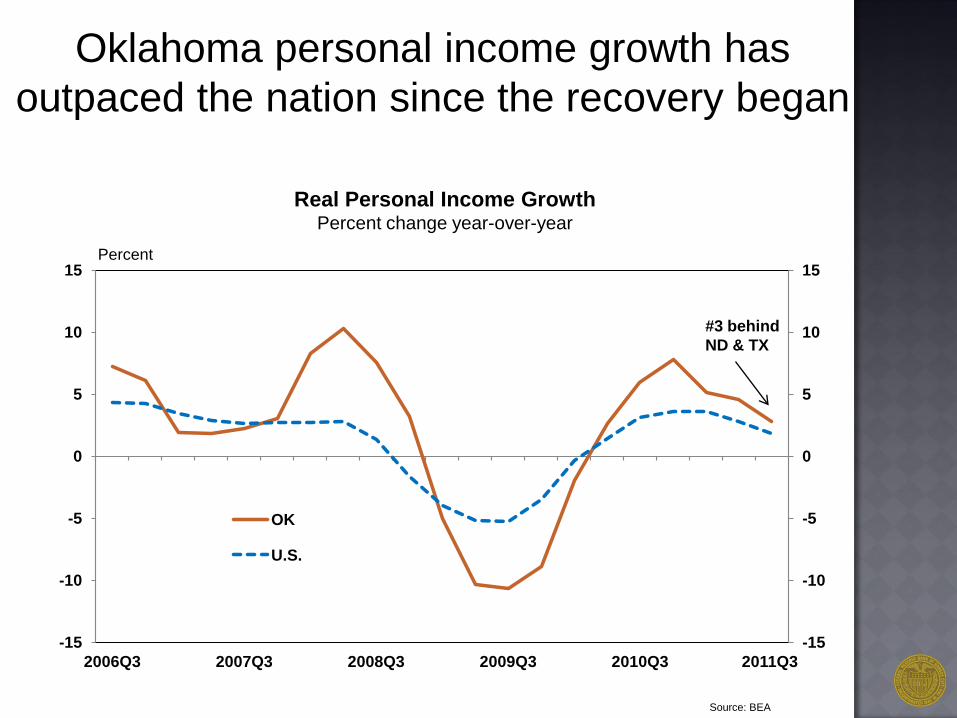

Real Personal Income Growth Percent change year-over-year

Oklahoma personal income growth has

outpaced the nation since the recovery began

-15

-10

-5

0

5

10

15

-15

-10

-5

0

5

10

15

2006Q3 2007Q3 2008Q3 2009Q3 2010Q3 2011Q3

OK

U.S.

#3 behind

ND & TX

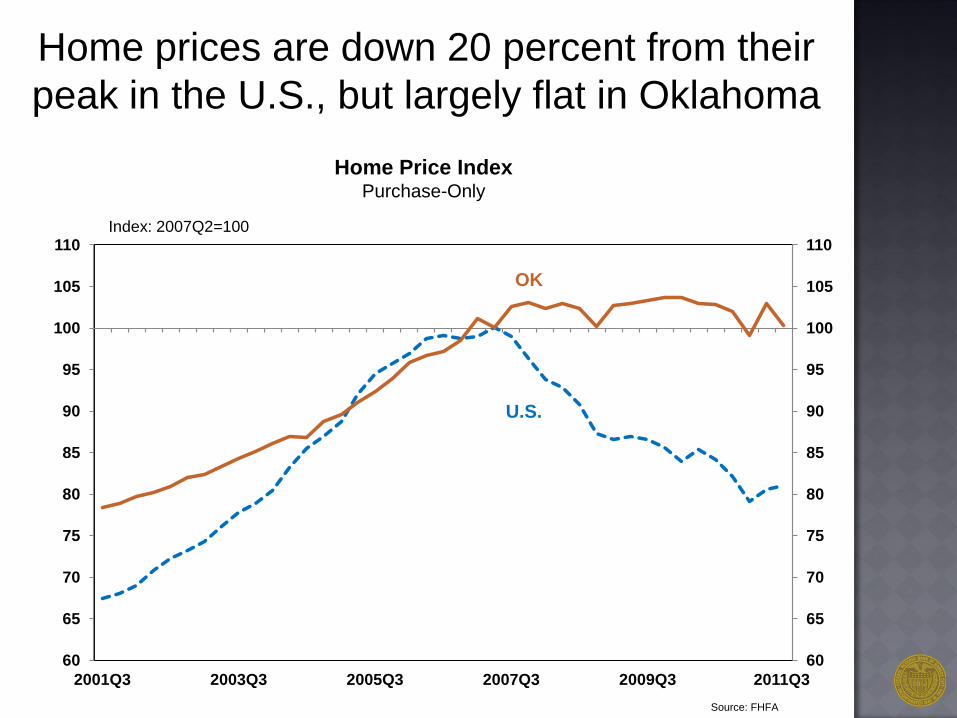

Index: 2007Q2=100

Source: FHFA

Home Price Index

Purchase-Only

Home prices are down 20 percent from their

peak in the U.S., but largely flat in Oklahoma

60

65

70

75

80

85

90

95

100

105

110

60

65

70

75

80

85

90

95

100

105

110

2001Q3 2003Q3 2005Q3 2007Q3 2009Q3 2011Q3

OK

U.S.

Dollars

Source: NAR

Median Home Prices in U.S. and Large Tenth District Cities

Home prices in large metros now compare

more favorably to the U.S. and region

75000

100000

125000

150000

175000

200000

225000

250000

275000

75000

100000

125000

150000

175000

200000

225000

250000

275000

2001:Q3 2003:Q3 2005:Q3 2007:Q3 2009:Q3 2011:Q3

Denver

U.S.

Kansas City

Omaha

Tulsa

OKC

Index

Source: KCFRB Manufacturing Survey

Manufacturing Composite Indexes

Regional manufacturing growth fell slightly

in December while national conditions rose

Index

Note –Tenth District calculated on an ISM basis; Above 50 indicates expansion

30

35

40

45

50

55

60

65

30

35

40

45

50

55

60

65

Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11

KC Fed

ISM

Percent

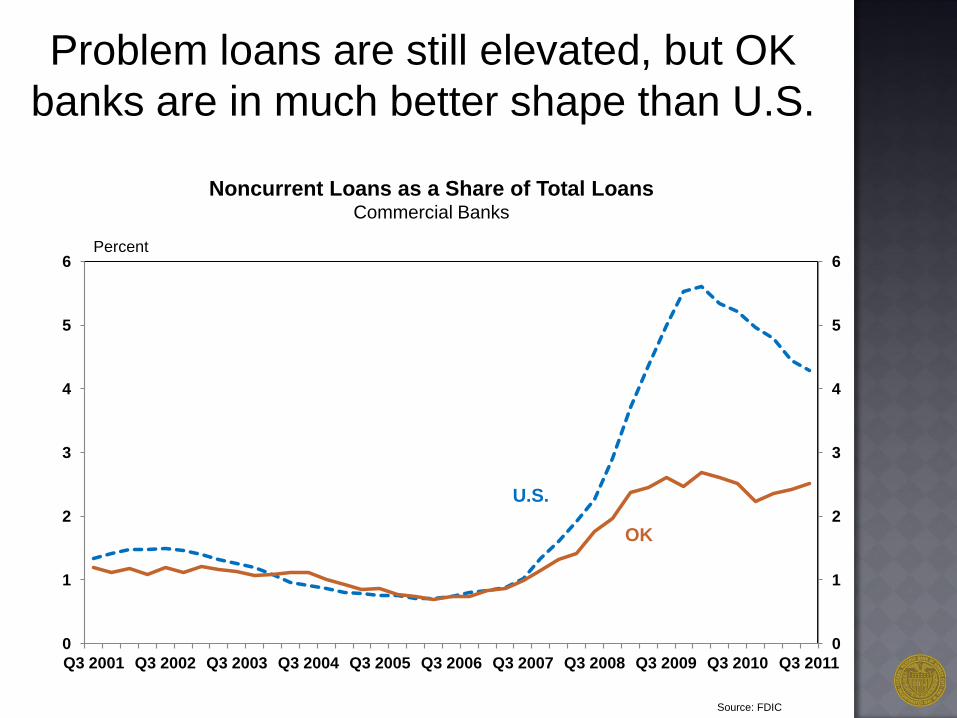

Source: FDIC

Noncurrent Loans as a Share of Total Loans Commercial Banks

Problem loans are still elevated, but OK

banks are in much better shape than U.S.

0

1

2

3

4

5

6

0

1

2

3

4

5

6

Q3 2001 Q3 2002 Q3 2003 Q3 2004 Q3 2005 Q3 2006 Q3 2007 Q3 2008 Q3 2009 Q3 2010 Q3 2011

U.S.

OK

0

5

10

15

20

25

30

35

40

0

5

10

15

20

25

30

35

40

District NE KS MO Mtn States (CO, NM,

WY)

OK

Q1 2011

Q2 2011

Q3 2011

Source: FRBKC Agricultural Credit Survey

Tenth District Non-Irrigated Cropland Values Percent Change, Year-over-year

Surging farmland prices pose a risk

in some parts of the region

Percent

0

30

60

90

120

150

0

3

6

9

12

15

Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13

Crude Oil &

Futures (WTI)

Natural Gas & Futures

(Henry Hub)

$/MMBTU $ per Barrel

Source: Bloomberg

Energy Prices

Energy prices are always a big risk, but

oil prices are expected to remain high

Moody’s

Forecast

The U.S. economy is growing moderately

but facing headwinds after only modest

expansion throughout 2011

Oklahoma’s growth has been more solid

in 2011, and fundamentals remain better

in the state than the nation

Summary