meeting the growing demand for gas from asia: prospects ... the growing demand for ga… · meeting...

TRANSCRIPT

1

Meeting the growing demand for gas from Asia: Prospects and challenges 1

Armelle Lecarpentier, Chief Economist, CEDIGAZ, France,

January 2014

INTRODUCTION With a consumption of 645 billion cubic metres (bcm) in 2012, Asia-Oceania became the second largest regional market in the world after North America. Currently booming, this market has the largest growth potential in the medium and long term and will significantly impact the international gas landscape. The Asian gas market is facing structural and institutional reforms needed for natural gas to ensure its crucial role in the future energy mix. In this paper, the international association CEDIGAZ analyses the specific characteristics of the Asian gas market and presents its growth prospects in the medium and long term. These prospects are contingent upon an economic and regulatory environment in favour to natural gas.

1. Specific characteristics of the Asian gas indust ry The Asian gas market is a relatively young market. Its specific geographical situation, characterized by long distances between producing and consuming centres and vast offshore areas, has originally limited its development. Natural gas demand was initially restricted in the 60s to some uses in the fertilizer industry in Pakistan and some in gas-fired power plants in Japan. The market really started to take off in the 80s, stimulated by a willingness to diversify energy sources and limit the dependence on oil, especially in Japan. Since then, the tremendous economic and demographic growth in the region has been accompanied by a dramatic rise in the demand for energy, particularly natural gas. In the last three decades, natural gas demand in Asia has grown by more than 7%/year, compared to a total energy growth of 4%/year. Even though the share of natural gas in the regional energy mix almost tripled over the period, to reach 11% today, it remains well below the world average of 22%. As some markets are at a relatively recent stage of development, this evolution demonstrates the tremendous scope the Asian market has for future growth. Natural gas stands as the fourth-largest source of energy, after coal, oil and renewables. Coal constitutes the backbone of the regional energy supply, with around 50% of the total energy consumed. The regional mix is strongly influenced by the Chinese market, which became the largest energy consumer in 2009. It's important to note that without China, the market share of natural gas in the region would reach 16%, while that of coal would drop to 26%.

1 This paper has been presented at the 21

st World Petroleum Congress (Moscow, June 2014) in the technical

session “Meeting the growing demand for gas from Asia – Implications for supply and transportation” where

CEDIGAZ was represented.

2

Asia-Oceania is characterized by strong disparities among national gas markets, especially as regards the maturity and the density of the gas network and the role of gas in the energy mix. This latter can be extremely low, in particular in China (5%) and India (8%), or, on the contrary, predominant (Brunei, Bangladesh, Malaysia). As regards consumption uses, natural gas has experienced the most rapid growth in the power sector. The power sector represents the first possible outlet for gas in the absence of a well-developed and mature gas network. It covers the largest proportion of Asian’s gas consumption, with a 44% share. The share of gas in the power generation mix is currently at around 14% at regional level, and reaches 26% in OECD Asian countries. Natural gas has gained a predominant share of power generation in many countries like Bangladesh (67%), Malaysia (60%), Singapore (78%), the Philippines (27%) or Vietnam (46%), due to its economic and environmental advantages.

2. The fastest-growing natural gas market in the wo rld The most important driver of the global expansion of gas demand According to CEDIGAZ, Asia-Oceania has been the most dynamic gas market worldwide and the largest contributor to the global growth in natural gas demand in recent years. The growth of the Asian market was particularly impressive in the 2000s, when Asia-Oceania made huge inroads into the global market. The share of the Asian gas demand in the world total has progressed steadily and almost doubled from 10% in 2000 to around 20% today. The Asian market has accounted for 40% of the global gas demand growth over the same period and for almost half of it in the last five years. Asia overtook Europe in 2011 and then the CIS in 2012 to become the second-largest regional market behind North America2. In 2012, gas consumption in Asia amounted to 645 bcm, representing a strong 7% rise from the previous year, in line with the previous five-year average growth. In 2013, the Asian market even became the main contributor to the global growth in gas demand. According to CEDIGAZ provisional estimates, natural gas demand increased by approximately 1.5 % in 2013 worldwide, a net slowdown in natural gas growth at global level. However, this overall trend should not hide a sharp rise of 5% in gas consumption in the Asian market. The most significant growth rates were recorded in China and Southeast Asia, where natural gas is gaining ground in the power and transportation sectors, at the expense of oil.

2 The seven regional markets considered in the methodology of CEDIGAZ are: North America (including

Mexico), Latin America, Europe (including Turkey), the Community of Independent States (CIS), the Middle

East, Africa and Asia-Oceania.

3

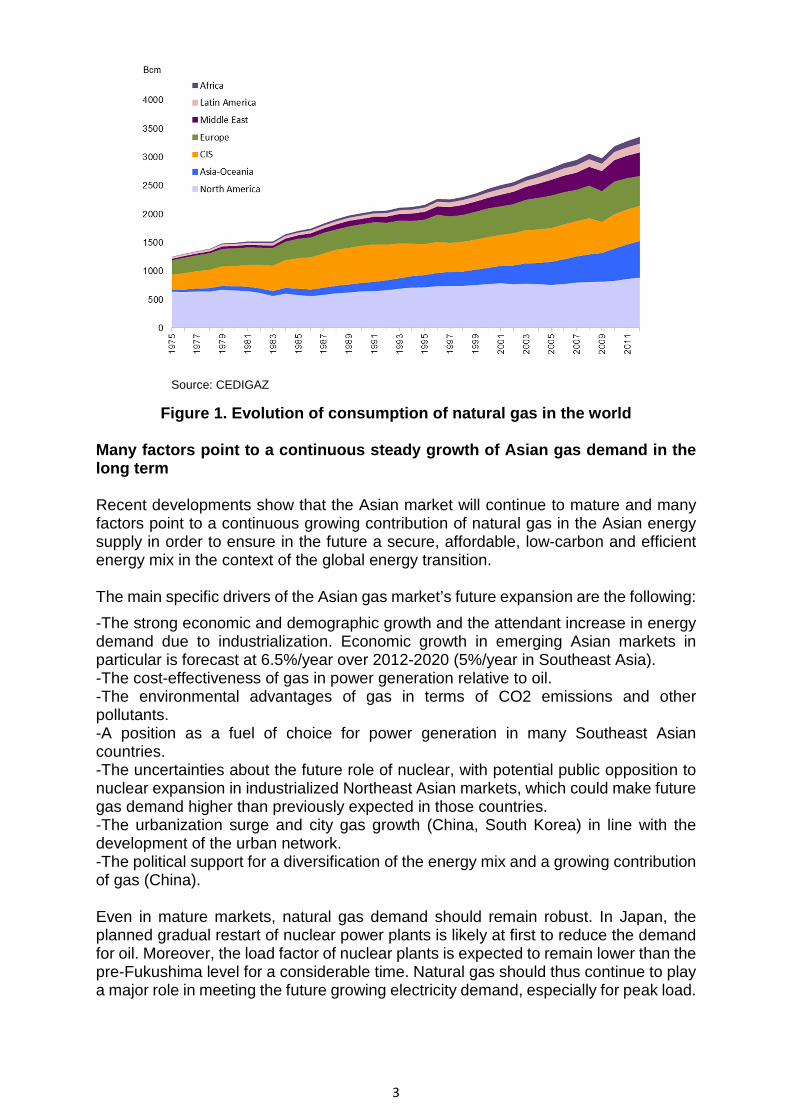

Source: CEDIGAZ

Figure 1. Evolution of consumption of natural gas i n the world Many factors point to a continuous steady growth of Asian gas demand in the long term Recent developments show that the Asian market will continue to mature and many factors point to a continuous growing contribution of natural gas in the Asian energy supply in order to ensure in the future a secure, affordable, low-carbon and efficient energy mix in the context of the global energy transition. The main specific drivers of the Asian gas market’s future expansion are the following:

-The strong economic and demographic growth and the attendant increase in energy demand due to industrialization. Economic growth in emerging Asian markets in particular is forecast at 6.5%/year over 2012-2020 (5%/year in Southeast Asia). -The cost-effectiveness of gas in power generation relative to oil. -The environmental advantages of gas in terms of CO2 emissions and other pollutants. -A position as a fuel of choice for power generation in many Southeast Asian countries. -The uncertainties about the future role of nuclear, with potential public opposition to nuclear expansion in industrialized Northeast Asian markets, which could make future gas demand higher than previously expected in those countries. -The urbanization surge and city gas growth (China, South Korea) in line with the development of the urban network. -The political support for a diversification of the energy mix and a growing contribution of gas (China). Even in mature markets, natural gas demand should remain robust. In Japan, the planned gradual restart of nuclear power plants is likely at first to reduce the demand for oil. Moreover, the load factor of nuclear plants is expected to remain lower than the pre-Fukushima level for a considerable time. Natural gas should thus continue to play a major role in meeting the future growing electricity demand, especially for peak load.

4

In South Korea, the demand for gas will be boosted by the city gas sector (residential, commercial and small industry). Natural gas can also have a potential for positive growth in the electricity sector in South Korea, as well as in Taiwan, if nuclear security concerns continue to mount. Emerging markets, firstly China and India, are undoubtedly the major drivers of natural gas demand in Asia. In these markets, two consumption sectors offer strong potential for natural gas demand growth: power generation and transport. The use of natural gas in the transport sector is encouraged by a political willingness to reduce pollution in big cities and improve energy security by reducing oil dependence. In Southeast Asia, natural gas has often become the preferred option for power generation because of its energy and environmental performance, at the expense of oil which is considered a costly and dirty fuel. In CEDIGAZ projections towards 2030, natural gas demand in Asia-Oceania is projected to grow by 3.5%/year, compared to a growth of just over 2%/year in the energy demand. Natural gas demand in emerging countries in particular is set to register a growth of 4.6%/year, with the strongest growth recorded in China and India, and to a lesser extent in Indonesia, Malaysia and Thailand. In volume terms, Asia-Oceania will account for up to 45% of the global gas demand growth over the projection period. It is now expected to surpass North America to become the largest consumer market towards 2025.

3. A growing dependence on imports A growing gas deficit has emerged as production fails to keep pace with demand. In recent years, Asia’s dependence on extra-regional imports has surged, passing from 15% in 2010 to 20% in 2011, 23% in 2012 and an estimated 25% in 2013. This shortage of natural gas is due to the following: -The decline of mature fields, the underdevelopment of resources and an insufficient renewal of reserves. -The rapid growth of natural gas in the energy mix (Southeast Asia), due to its competitiveness. A large part of downstream pricing continues to be regulated and subsidy regimes have often maintained gas prices at artificially low levels, stimulating consumption but also deterring investment on the upstream and import side. The gas shortage is especially acute and problematic in some countries like China, Pakistan and India, and also in some major exporting countries like Indonesia and Malaysia. These latter have to resolve a complex equation in order to balance export and domestic requirements, all the more so because the management of the gas shortage is hampered by the growing distances between local producing and consuming centres. In 2012, total imports in Asia-Oceania reached 272 bcm, of which 53% came from regional sources, the rest being imported from extra-regional suppliers. Imports via pipelines represented a volume of 52 bcm, or only 19% of the total. Indeed, one main characteristic of the Asian gas market is the lack of pipeline exchanges and infrastructures. Asia has only 7% of international pipeline flows, and more precisely 9% of extra-regional pipeline flows and 6% of intra-regional pipeline flows.

5

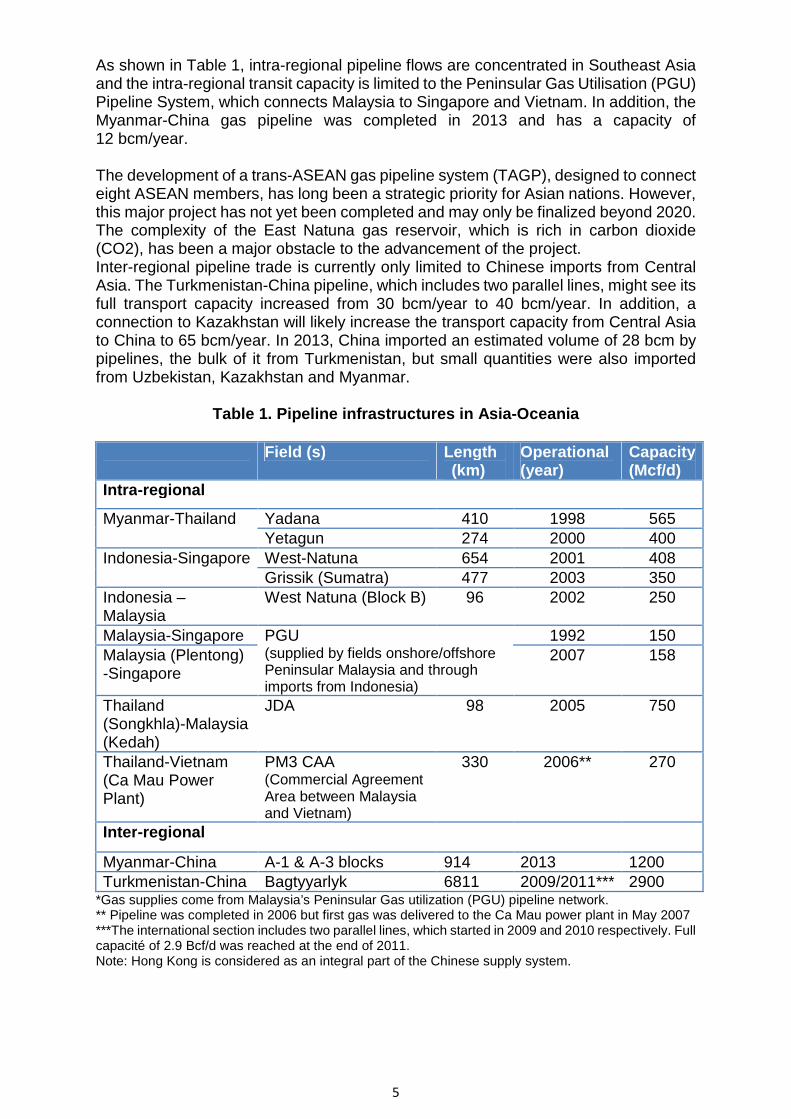

As shown in Table 1, intra-regional pipeline flows are concentrated in Southeast Asia and the intra-regional transit capacity is limited to the Peninsular Gas Utilisation (PGU) Pipeline System, which connects Malaysia to Singapore and Vietnam. In addition, the Myanmar-China gas pipeline was completed in 2013 and has a capacity of 12 bcm/year. The development of a trans-ASEAN gas pipeline system (TAGP), designed to connect eight ASEAN members, has long been a strategic priority for Asian nations. However, this major project has not yet been completed and may only be finalized beyond 2020. The complexity of the East Natuna gas reservoir, which is rich in carbon dioxide (CO2), has been a major obstacle to the advancement of the project. Inter-regional pipeline trade is currently only limited to Chinese imports from Central Asia. The Turkmenistan-China pipeline, which includes two parallel lines, might see its full transport capacity increased from 30 bcm/year to 40 bcm/year. In addition, a connection to Kazakhstan will likely increase the transport capacity from Central Asia to China to 65 bcm/year. In 2013, China imported an estimated volume of 28 bcm by pipelines, the bulk of it from Turkmenistan, but small quantities were also imported from Uzbekistan, Kazakhstan and Myanmar.

Table 1. Pipeline infrastructures in Asia-Oceania Field (s) Length

(km) Operational (year)

Capacity (Mcf/d)

Intra -regional

Myanmar-Thailand Yadana 410 1998 565 Yetagun 274 2000 400

Indonesia-Singapore West-Natuna 654 2001 408 Grissik (Sumatra) 477 2003 350

Indonesia – Malaysia

West Natuna (Block B) 96 2002 250

Malaysia-Singapore PGU (supplied by fields onshore/offshore Peninsular Malaysia and through imports from Indonesia)

1992 150 Malaysia (Plentong) -Singapore

2007 158

Thailand (Songkhla)-Malaysia (Kedah)

JDA 98 2005 750

Thailand-Vietnam (Ca Mau Power Plant)

PM3 CAA (Commercial Agreement Area between Malaysia and Vietnam)

330 2006** 270

Inter -regional

Myanmar-China A-1 & A-3 blocks 914 2013 1200 Turkmenistan-China Bagtyyarlyk 6811 2009/2011*** 2900

*Gas supplies come from Malaysia’s Peninsular Gas utilization (PGU) pipeline network. ** Pipeline was completed in 2006 but first gas was delivered to the Ca Mau power plant in May 2007 ***The international section includes two parallel lines, which started in 2009 and 2010 respectively. Full capacité of 2.9 Bcf/d was reached at the end of 2011. Note: Hong Kong is considered as an integral part of the Chinese supply system.

6

With an estimated total imported volume of around 220 bcm in 2012, Asia-Oceania is thus considered as the “king” of LNG. In the past three years, Asia has even strongly enforced its leadership on the international LNG market, with a market share surging from 60 % in 2010 to 63% in 2011, 70% in 2012 and an estimated 74% in 2013. This expansion was primarily explained by two countries, China and Japan, as this latter boosted LNG imports to offset nuclear power deficit following the March 2011 Fukushima accident. At the end of the 70s, the geographical situation of the Asian market initially encouraged the development of the regional LNG trade, mainly from producers in the south (Australia, Indonesia, Malaysia and Brunei) to consumers in the Northeast, like Japan, South Korea and Taiwan, which are today seen as “well-established” or “traditional” LNG markets. More recently, emerging countries have started to import LNG: India (2004), China (2006), and some markets in the Southeast like Thailand (2011), Malaysia (2013) and Singapore (2013). On the supply side, the development of liquefaction units in the Middle East in the 2000s represented a major development in the Asian gas supply, opening new supply routes and sources. LNG deliveries from the Middle East to Asia have more than tripled in the last decade. Qatar in particular became the largest supplier to the region in 2007 and its exports have since continued to grow to account for 30% of Asia’s total current LNG imports, easily outstripping Malaysia (14%), Australia (12%) and Indonesia (11%). In the future, the dependence of Asia on extra-regional imports is forecast to continue to increase, passing from 23% in 2012 to 28% in 2030 to meet the fast-growing demand. In volume terms, net regional imports will increase from 149 bcm in 2012 to 220 bcm in 2020 and 345 bcm in 2030. China alone will account for more than 80% of these rising import needs.

Source: CEDIGAZ

Figure 2. Evolution of regasification capacity in A sia-Oceania

7

4. Implication for supply and transportation in the long term In parallel with this growing external dependence, inter-relations and competition between regional markets (especially Europe) for access to international natural gas and LNG supply will intensify. The Middle East will remain a major source of supply but in order to meet the growing regional demand, Asia’s gas supply will evolve and diversify with Southeast Asia’s share in decline, and the CIS, Africa and North America playing a growing role. There are currently two technological options to import natural gas from international sources in the long term: by pipeline or LNG. Several international gas pipeline projects are designed to supply natural gas from the Middle East, Russia and Central Asia to Asia-Pacific. However, because of different economic and/or geopolitical obstacles surrounding their development, many are delayed or uncertain. Of all inter-regional pipeline projects, the Russia-China gas pipeline, whether from Western or Eastern Siberia, has the greatest likelihood of being finalized successfully.

Source: CEDIGAZ

Figure 3. Net natural gas trade by region Despite strong opposition from the US, the long-delayed Iran-Pakistan-India pipeline seemed to take a major step forward when the presidents of Iran and Pakistan celebrated the commencement of construction of the Pakistani section in early 2013. The severity of the energy crisis in Pakistan has kept the country determined to develop the project. The 2,670 km pipeline aims to deliver South Pars gas to the Balochistan and Sindh provinces in Pakistan, as well as Delhi and Northwest India. The pipeline’s initial capacity is set at 22 bcm/y, extendable to 55 bcm/y. Another pipeline project, the 1,700 km TAPI pipeline project, is intended to deliver gas from the Dauletabad field in Turkmenistan to Pakistan and India via Afghanistan. CEDIGAZ has assumed that these two latter pipelines will be long delayed due to geopolitical risks, and security, financial and technical issues, but may begin operations post-2020, primarily due to the cost incentive that pipeline gas will probably offer as opposed to LNG and the tremendous needs of India and Pakistan for additional supply.

8

It is not predicted in CEDIGAZ projections that natural gas from Russia will reach markets other than China in the forecast period. Although pipeline gas may be cheaper and allow the LNG buyer to leverage its position as a pipeline gas buyer in LNG price negotiations, pipeline imports from Russia to Northeast Asia (Japan, South Korea) have long been delayed for many reasons, including the risks of transiting through the Korean Peninsula and economic and political issues. As a result of these developments, pipeline imports into Asia-Oceania are thus expected to remain minimal compared to LNG imports, with the exception of the Chinese market.

Source: CEDIGAZ

Figure 4. Asia/Oceania natural gas supply forecast Indeed, China is well-positioned to diversify and optimize its gas supply between unconventional gas, LNG and pipeline gas imports from current and new potential sources.

Source: CEDIGAZ

Figure 5. China natural gas supply forecast

9

According to CEDIGAZ projections, Asia’s total LNG demand is estimated to rise by 4.3%/year until 2030. Emerging markets in particular will contribute for almost 85% of the rising regional LNG demand, with China and India growing the strongest. In addition to these two countries, it is worth noting the breakthrough of Southeast Asia on the international LNG scene. This region already accounts for more than 2% of global LNG trade today. Towards 2020, new potential Asian LNG importers, such as Pakistan, Vietnam, Bangladesh, Myanmar and the Philippines, are expected to enter the club of LNG importers. These new potential markets could add another 30 bcm of LNG demand by 2030. Asia will thus remain the “key market” for LNG, accounting for almost two-thirds of the growth in volumetric global LNG demand until 2030. The expansion of the Asian LNG market is accompanied by a flurry of regasification projects in emerging markets, which intensify the growth of the Asian gas demand. As of 1st January 2014, 28 bcm/year of regasification capacity was under construction in emerging markets, in addition to an existing capacity of 90 bcm/year. Other identified planned projects total a potential capacity of more than 180 bcm/year, of which 60% is located in China and India.

Source: CEDIGAZ

Figure 6. LNG regasification in emerging markets (existing, under construction, projects)

In many countries in Southeast Asia, FSRU technology has been considered as a quicker and cheaper alternative to importing LNG. In Malaysia and Indonesia, FSRUs also provide a solution to the problems of delivering gas over very long distances from one part of the country to another. However, financial and economic difficulties related to planned projects in potential new markets (Pakistan, Bangladesh, the Philippines) have delayed the development of LNG receiving projects.

10

5. Supply patterns are evolving to improve the secu rity, flexibility and affordability of gas supply

International market conditions are leading Asian LNG supply and trading patterns to evolve in order to both improve the security, and the flexibility and the affordability of gas supply. These three strategic pillars are key for a “golden age of gas” in Asia. The new trading and pricing dynamics which are emerging are necessary for the Asian market to better adapt to the changing global market conditions and ensure the growth of the Asian economy and LNG industry. Security of supply can be prioritized All Asian import markets will be under pressure to secure additional supplies in the next two decades as output from operating projects declines, contracts expire, and demand grows. As shown in the following graph, the LNG demand which remains to be contracted will increase substantially from 2017, both in Japan and emerging markets, like China. As of today, around two-thirds of the required regional LNG supply in 2030 remains un-contracted.

Source: CEDIGAZ

Figure 7: Un-contracted LNG demand forecast, 2013-2 030 LNG liquefaction projects require security of contracted volume and assured demand to be economically viable. The security of LNG supply is a key priority in mature markets, in particular Japan, where utilities and gas companies are responsible for supply reliability in their operating areas. Uncertainties about future energy policies, the future outcome of contractual and commercial arrangements (pricing level), the regulatory environment (market liberalization in Japan) and the outlook for nuclear power could delay necessary Asian-targeted supply projects and thus maintain tightness on the Pacific LNG market. Policies in mature markets need to be sufficiently clarified to trigger timely, firm LNG procurement decisions. The different strategic measures which are developed to improve the security of supply are the following:

11

-The increase of the supply potential with a diversification of sources (unconventional gas and pipeline gas from the CIS to China) to soften the impact of a disruption in the LNG supply. However, traditional and mature LNG markets (Japan, South Korea) so far have few alternative sources other than imported LNG to meet demand. -A “portfolio approach” and an integration of companies along the whole LNG value chain, with a combination of various upstream sources in different geographical locations. -The recourse to new suppliers (US, Canada, Mozambique, etc.), a strategy favoured by mature markets (Japan). -The appreciation of risks and opportunities of the different liquefaction projects. In this respect, greenfield projects, such as in Australia or Canada, can guarantee a relative certainty and reliability of supply, while some US LNG projects can introduce new risks including the volatility of Henry Hub prices, uncertainty on reserves (market-sourced gas rather than reserve-dedicated), political risk and plants operated by companies that have no previous LNG experience. Flexibility of supply is increasingly important A more flexible LNG supply is required in many Asian markets to cope with short-term and seasonal fluctuations in demand, especially in South Korea and China. Flexible LNG can complement other flexibility tools, like underground gas storage (China) and onshore LNG storage at regasification terminals (Japan, South Korea). Last but not least, increasing flexibility would reduce pressure over prices. The lack of integration of national gas markets is caused by the lack of cross-border pipelines and the still early stage of development of infrastructures in emerging markets. This lack of pipeline connections will keep Asian markets still fragmented for a long time. This situation limits to some extent the flexibility and the short-term responsiveness of supply to the changes in demand. In the medium-term future (2014-2017), new LNG production will provide limited flexibility as almost 80% of it is allocated under firm long-term contracts. Flexibility is limited in existing long-term contracts in the Pacific Basin as the majority of these (contrary to those in the Atlantic Basin) are on a DES-basis and contain destination clauses which result in some rigidity in the LNG supply chain. However, major developments will help improve the flexibility of the LNG supply in Asia in the longer term: - An increase of third-party access to regasification terminals. - The development of spot and short-term LNG trade which increases arbitrage opportunities. In the last three years, the latter has doubled to account for more than a quarter of world LNG supply today. - The commercial and contractual renegotiations aimed at increasing flexibility (increase of the quantity tolerance to 15% or even 25% accepted by some portfolio sellers), including some upcoming marketing innovations (review of destination clauses, improved flexibility conditions from future long-term contracts to sustain the crude price correlation, with significantly increased off-take flexibility). - The growing role of “flexible LNG portfolios” and “equity LNG” on the international LNG market. - The expansion of floating regasification.

12

- Consortium buying which can provide operational flexibility: buyers could for instance switch delivery schedules with one another according to inventory levels, or swap cargoes depending on individual demand. - The development of new LNG projects with destination flexibility. US LNG projects are mainly proposing to use a tolling structure rather than the traditional models. The companies that have committed to capacity will be responsible for procuring natural gas supply and paying a tolling fee to the developer of the liquefaction plant. The result will be an increased volume of LNG available on an FOB basis. In addition, projects in East Africa are characterized by the presence of many portfolio LNG suppliers, with no export destination restriction. -The diversification of LNG suppliers and the rise in the number of LNG markets which have increased the complexity of the trade and introduced new permutations and links between buyers and sellers. As investors take time to launch the major projects required to meet growing demand in Asia and buyers delay long-term supply agreements, short-term and flexible LNG portfolios are set to play a major role in the medium term to meet demand in price-sensitive emerging markets in Southeast Asia and India (Figure 7), which have made destination and volume flexibility their priority. The affordability of gas supply is a critical issue for every Asian market Natural gas has to be competitive with other energy sources at the regional and local level in order to expand its market share in the regional energy mix in a context of internationalization of gas markets. But on average, LNG purchase prices in Asia have remained the highest in the world in recent years, while changing market conditions in the Atlantic Basin (US shale gas revolution, European economic crisis, competition between spot LNG and pipeline gas in Europe) have brought a new reality to pricing. The majority of imports in Asia are carried out under long-term contracts in which the price of gas is determined by that of oil, which sets a reference level. Because of this indexation model, LNG prices can outstrip spot prices when oil prices are high. Moreover, natural gas is increasingly in competition with coal, especially in the power generation sector, which questions the rationale of oil indexation. US LNG offers Asian buyers the opportunity to diversify away from oil indexation to a spot-based indexation. Henry Hub-linked LNG offers the possibility to make savings when oil prices are high (> $100/bbl). CEDIGAZ analyses show that until a maximum level of the Henry Hub price at $7/MBtu, the costs of LNG deliveries from US Gulf Coast projects (via the Panama Canal) to Japan are lower than the JCC-indexed price for an oil price of $100/bbl and a slope of 13%. The expected future growing role of US Henry Hub-linked LNG will encourage other suppliers to use new models that index LNG to spot market prices. However, the share of spot-based LNG is not expected to become very significant and exceed 30% in Asia in the next decade. In addition, it remains to be seen whether some of the off-takers will fix the DES price by adding the shipping costs and a margin to the FOB price or choose to sell on an oil-indexed basis. Asian spot prices can show strong volatility and can peak at extremely high levels, especially in periods of peak and seasonal demand. In the absence of a trading hub, it is worth noting that spot prices do not reflect gas-gas competition but rather result from specific bilateral negotiations between a buyer and a seller depending on the buyers’ needs and the supply conditions on the seller’s side.

13

*The price is determined by bilateral discussions and agreements between a large seller and a large buyer, with the price fixed for a period of time. Source: International Gas Union, Wholesale Gas Price Survey, 2013 Edition

Figure 8. World price formation 2012 – Total import s The anticipated market tightness, at least in the short term, has meant a number of markets are paying growing attention to the issues of cost, subsidies and pricing. In a context of a global restricted LNG supply, large spreads can occur between spot Northeast Asian LNG and European spot prices beyond netback and business consideration. Asian buyers have to pay a premium, while few alternative gas supply sources exist due to a lack of pipeline connections. This situation undermines the competitiveness of natural gas on the Asian market. The pressure on Asian buyers from their governments and from the public is intensifying. A reduction in the price of LNG procurement is crucial given the significant impact on the economy. In Japan, the government introduced a top runner price beyond which power utilities cannot increase tariffs to customers, and this trend is likely to spread to city gas utilities. The LNG supply cost is of prime importance in emerging markets where demand is the most reactive to prices. Prospects for LNG imports in these markets will depend on the ability of customers to pay international reference prices, especially in India and Southeast Asia, where almost all consumers purchase natural gas at domestic prices below $10/MBtu. However, if LNG imports are aimed at replacing more expensive fuel oil, LNG can still be a cost-effective option. Companies have developed different strategies to procure a more competitive LNG supply in response to changing market conditions in recent years. As mentioned above, portfolio players with flexibility in supply volumes and destinations and with arbitrage opportunities are better positioned in price negotiations. Companies from existing and emerging LNG countries in Asia are actively seeking upstream and liquefaction opportunities. Equity participation in LNG production projects is supported by governments (Japan, China) as it is based on expectations that an importer’s proactive involvement could lead to lower procurement costs. Since

14

Chinese firms have no control over international prices, Beijing has ordered companies that signed long-term LNG agreements to ensure profits by securing upstream assets and establishing their own LNG shipping fleets. Another way to enhance the bargaining power of LNG buyers is to create some form of collaboration. Some Asian buyers have been interested in joint LNG procurement, as shown by the MoU signed between the Japanese and Indian governments in September to look into ways of lowering Asian LNG prices. Asian companies’ discussions and specific initiatives on joint-buying underscore Asian buyers’ determination to increase their bargaining power. A new generation of long-term contracts is emerging with buyers seeking a more specific wording of price review clauses, with a possibility of arbitration. Since it would be hard to introduce hub pricing in existing long-term contracts, buyers are pushing for weaker oil slopes (13%-13.5%). The activation of price-opening clauses responding to changing market environments is another strategic option: some buyers are understood to be studying a switch from time-based price re-openers to “triggers” prompted by a significant market change, such as the US shale revolution.

6. Main challenges raised by the expansion of the A sian gas market Massive investment requirements along the whole gas chain The lack of adequate infrastructures, particularly cross-border gas pipelines, limits the formation of a regional physical wholesale market able to compete with other regional markets worldwide. It also prevents proper responsiveness of supply to variations in demand. Massive investments are required to develop infrastructures in order to improve interconnection between markets. Investments are also required on the upstream side, not only to ensure future development of conventional reserves and limit their decline, but also to develop the ample unconventional gas resources which have a major role to play in ensuring the future security and flexibility of the gas supply. Issues and uncertainties relative to unconventional gas Alongside North America, Asia-Oceania is particularly well-endowed with unconventional resources, namely shale gas and Coalbed Methane. The most recent US Energy Information Administration’s study (June 2013) even shows impressive numbers of shale gas resources in countries like China and Australia, which amount respectively to 1,115 Tcf (1st rank) and 437 Tcf (7th rank). Substantial shale gas resources have also been identified in Indonesia (46 Tcf), Pakistan (105 Tcf) and India (96 Tcf). The Asian market thus presents a strong potential for shale gas production growth, provided these resources can be developed. Exploration and development of shale gas has already started in China and Australia, which have recently managed to commercially produce marginal quantities. But the development of shale gas in these countries is still in its infancy. Many obstacles slow the pace of development of shale gas, especially in China: -the lack of an incentive fiscal, legal and land access regime, -the level of drilling costs, which can be three times higher than in the US, -the shortage of equipment and infrastructures,

15

-the limited market access (no “unbundling”) and commercial award for private companies, -the geological challenges and difficulties raised by the transfer of technologies, -the lack of experience of Chinese companies, -the lack of maturity of the gas market and the gas industry, -the scarcity of water (Tarim Basin). In the CEDIGAZ Scenario, shale gas production in China could reach a maximum of 90 bcm by 2030-2035. This volume would require the drilling of 8000 - 10,000 wells in aggregate by 2030, which will entail an investment of more than US$ 70 billion for horizontal drilling and fracturing at current drilling costs. Technical progress and improvements in productivity are thus necessary to reduce this massive sum. Shale gas in China is crucial for improving the security and flexibility of the gas supply and mitigating the pressures on the Asian market. The stakes are such that the Chinese government intends to establish an appropriate and transparent regulatory and legal framework and offer economic incentives to attract foreign investment. Other Asian emerging markets (India) are on the way to implementing perspicuous, shale-specific regulations to guarantee a transparent market and ensure the commercialized development of shale gas resources. The context is somewhat different in Australia, because of a relatively well-liberalized market structure, a mature industry and an existing network of infrastructures. But the main obstacle to large-scale development of shale gas is the distance of some major shale gas fields from gas infrastructures and markets. Challenges to Australia’s shale gas development also include the constraints on water resources and the cost which today seems too high to encourage production. Lack of a trading hub and regional index Despite the large volume of gas consumption, which continues to rise strongly, Asia does not have a trading hub or regional index. The creation of a reliable liquid hub is of prime importance to enable exchanges between a sufficiently large number of participants and create a confident and efficient structure for flexible LNG. In the absence of “gas to gas” competition, Asian gas prices have remained very high compared to those in North America and Europe. The lack of a liquid trading hub prevents the emergence of a transparent price signal which can reflect market conditions and steer required investments along the gas chain. As the network of infrastructures matures, the Asian market will likely see the development of several pricing areas. Singapore is seen as the best-placed to develop a trading hub in the medium term as the government has a “free-market approach” to markets, with Japan, Korea and China also well-positioned for future developments. In Singapore, the government plans to introduce a spot LNG import policy: domestic buyers will be allocated annual spot credits – initially capped at 10% of their long-term imports – which will be tradable and valid for one year. Despite some existing infrastructures in place (LNG terminal, pipeline connectivity) which are set to be expanded, natural gas and LNG imports in Singapore are relatively low, resulting in a lack of liquidity which may slow the development of a trading hub there in the medium term. In this respect, Japan and China may have an advantage.

16

7. The pace of reforms is uncertain A reliable and incentive investment climate, with a correct alignment between private and public investment, is crucial for meeting the scale and timing of massive natural gas investments which are of a long-term nature. Reforms to liberalize the gas pricing regime and upstream and downstream markets, and to promote private investment have already been implemented in most emerging markets. These reforms are not only necessary to trigger investment and encourage the development of the gas industry, but also to increase economic efficiency. China started to implement pricing reforms in the Guangxi and Guangdong provinces in early 2012. The authorities have announced price increases for non-residential users which would raise average city gas prices by 15.4% to about $8.9/MBtu. Prices will be higher at up to $10-$12/MBtu in many coastal provinces. Further substantial increases are expected in the next two years. In July 2012, China officially launched its first natural gas physical spot trading market at the Shanghai Petroleum Exchange (SPEX) in order to adjust its summer supply and peak demand via an efficient market-based pricing system. This move reflects an attempt to step up the domestic natural gas reform, but the feasibility of the spot trading market remains to be confirmed. In June 2013, India approved a new pricing formula with a direct link to global benchmark LNG and gas hub prices, which brings prices to around $8.40/MBtu from 1 April 2014. However, this was blocked by the Election Commission. In Malaysia, where domestic gas prices are the lowest in Southeast Asia, the current plan is to raise domestic gas prices to around international level by 2016. If Malaysian market reforms are achieved, it will provide some interesting new flexibility on the LNG market in Southeast Asia because of the possibility of switching supply to and from the domestic market. The way the deregulation of the gas market will be achieved and the pace of reforms leading to a market-based model vary from country to country and will depend on the respective state of the natural gas market. But it is worth noting that even mature industrialized markets like Japan and South Korea do not comply with some of the institutional and structural requirements to create a competitive gas market, as shown in the table below.

Table 2. Competitive market requirements in selecte d countries Japan Korea China Singapore Hands -off government approach - - - + Separation of transport and commercial activities

- - - +

Wholesale price deregulation + - +/- + Sufficient network capacity and non-discriminatory access

- - - +

Competitive number of market participants + - + +/- Involvement of financial institutions +/- - - +

Source: International Energy Agency (2013), Developing a Natural Gas Trading Hub in Asia Note: “+”= currently contributing towards a competitive natural gas market, “-” = currently not contributing towards a competitive natural gas market, “+/-” = currently unclear

17

CONCLUSION In the future, interactions between energy, regional markets and prices will intensify in a context of the internationalization of gas markets and the growth of a flexible LNG supply. Asia needs to adapt global market changes to its own regional market. Some regulatory, commercial and contractual moves are underway for natural gas to be competitive and attractive at regional and local level. These changes must enable the materialization of the massive investments required to ensure the expansion of the Asian gas market, which is crucial for a successful energy transition. However, the perspectives for a competitive wholesale market with convergence of spot prices within the region (as with the European gas market) are restricted by the low level of pipeline exchanges, the lack of liquidity and the disparate stages of development of the natural gas markets. In addition, the details of how reforms will be achieved and their direction will require a clear political willingness, as the expected growth of natural gas could be held back by changing priorities in government strategies.